the geography of executive compensation - drexel university · the geography of executive...

TRANSCRIPT

The Geography of Executive Compensation

Christa H.S. Bouwman

Case Western Reserve University and

Wharton Financial Institutions Center

June 2013

This paper documents that CEO pay is strongly correlated with that of geographically-close CEOs. Specifically, a 1% higher level of total pay enjoyed by geographically-close CEOs in the previous year is associated with a 0.122% higher level of CEO total pay in the current year ceteris paribus. This result is established while controlling for previously-documented factors that affect CEO pay – including the average CEO pay at similar-sized industry peers – and proxies for the cost of living. Hand-collected data on the official peer groups used by the firm to set CEO pay suggest that the results do not reflect competitive benchmarking. Similar results are obtained using a variety of alternative specifications and by examining headquarter relocations to deal with potential endogeneity concerns. To understand what drives the link between geography and CEO compensation, four possible theoretically-motivated channels are examined: (i) local hiring of similar CEOs; (ii) the effect of “leading firms” in the vicinity; (iii) local labor market competition for CEOs; and (iv) relative status concerns among geographically-close CEOs.

† Weatherhead School of Management, Case Western Reserve University, 10900 Euclid Avenue, 362 PBL, Cleveland, OH 44106. Tel.: 216-368-3688. Fax: 216-368-6249. E-mail: [email protected]. Keywords: CEO Compensation; Peer Groups; Benchmarking; Geography; Labor Market Competition; Relative Status Concerns JEL Classification: D8, G3, J31, J33, R1 I am grateful to Zahi Ben-David, Jesse Fried, Yaniv Grinstein, Dirk Jenter, Li Jin, Cami Kuhnen, Elena Loutskina, Kevin Murphy, Antoinette Schoar, and Yuhai Xuan for helpful suggestions, and to seminar participants at Penn State University, the University of Virginia, MIT Sloan School of Management, the University of Vienna, Case Western Reserve University, the Financial Intermediation Research Society Meeting, and the Financial Management Association for useful comments. Burch Kealey (directEDGAR) and Rimas Biliunas kindly provided me with part of the headquarter relocation data, and the Council for Community and Economic Research (C2ER) generously gave me the ACCRA Cost of Living Index data for all the geographies in the sample in the fourth quarter of every year.

1

THE GEOGRAPHY OF EXECUTIVE COMPENSATION

“It isn’t that the CEOs are such terrible people, it’s that the system, with its envy-driven

compensation mania, has developed to a place where it brings out the absolute worst in good

people. […] What makes CEO pay so difficult is that only a few of the people who are earning

these huge amounts are actually worth it. Everyone else figures they have to keep up, or recognize

that their guy isn’t as good. Who wants the recognition that the company down the street has a

remarkable CEO, but we have a mediocre klutz?”

Berkshire Hathaway’s Charles Munger (“Taking on envy-driven CEO pay,” Chicago Tribune,

January 7, 2007.)

1. INTRODUCTION

While distance has been shown to matter in economic transactions for a variety of reasons, related

primarily to information frictions (e.g., Coval and Moskowitz, 1999, 2001; Hong, Kubik, and

Stein, 2005; Kedia and Rajgopal, 2009), standard optimal contracting theory suggests that

geography has no role to play in executive compensation. The CEO’s pay should merely depend

on his reservation utility, his disutility for effort, his risk aversion, the risk in the payoff (e.g.,

Holmstrom, 1979), and possibly his perceived ability (e.g., Holmstrom and Ricart i Costa, 1986).

Yet, if one goes beyond the standard model, there may be many reasons why the CEO’s

compensation may be related to the pay packages of geographically-proximate CEOs. One may

be that certain areas, for some reason, tend to attract firms that employ CEOs with similar

performance-relevant attributes, leading to pay clustering within geographies. Another reason

may be due to a “leading-firm” effect, whereby firms in a given area follow leading firms in that

area when it comes to setting CEO pay (e.g., Glaeser, Sacerdote, and Scheinkman, 1996; Kedia

and Rajgopal, 2009). A third reason may be geographic idiosyncracies of labor market

competition for CEOs (e.g., Vietorisz and Harrison, 1973; Kennan and Walker, 2011). A fourth

reason may be peer comparisons rooted in social pressure, equity considerations, and envy, which

may affect not just worker pay (e.g., Dur and Glazer 2008; Bartling and Von Siemens, 2010; Card,

Mas, Moretti, and Saez, 2012) but also CEO compensation (e.g., Goel and Thakor, 2010; Liu,

2

2011); and a link between geography and compensation could emerge because reference groups

are typically geographically based (e.g., Persky and Tam, 1990). These considerations motivate

the question empirically addressed in this paper: is there a relationship between CEO

compensation and geography and if so, what factors generate this relationship?

The first part of the paper examines the relationship between geography and executive

compensation and documents a strong link. Specifically, I show that CEO total pay is positively

and significantly related to the average level of pay of CEOs employed at other firms

headquartered within a 100-kilometer radius. This result is obtained while controlling for other

factors that have been found to affect CEO compensation, including the average compensation at

similar-sized firms in the same industry (Bizjak, Lemmon, and Naveen, 2008; Faulkender and

Yang, 2010).1 Differences in the cost of living are also controlled for.

The relationship between geography and CEO pay is robust to using a variety of

alternative specifications. Small-sample evidence based on hand-collected data on the official

peer groups used by firms to set CEO pay suggests that the results do not reflect competitive

benchmarking. A random assignment exercise reveals that CEO pay is not significantly related to

the pay of randomly-assigned geographically-close CEOs. A headquarter-relocation analysis

suggests a potentially causal interpretation of the results: before the move, CEO pay is related only

to the compensation of geographically-close CEOs at its pre-move location; after the move, it is

related to the pay of geographically-close CEOs at its new location, and to a lesser extent to the

pay of geographically-close CEOs at its previous location.

The coefficient on the (natural log of the) average total pay of geographically-close CEOs

is positive and generally highly statistically significant. The results are also economically

significant. For example, the main regression result suggests that a 1% higher level of total pay

enjoyed by geographically-close CEOs in the previous year is associated with a 0.122% higher

level of CEO total pay in the current year. The effect of geography on CEO pay is sizeable and

tends to be at least as big as the effect of industry peer pay.

1 To further ensure that I pick up a geography effect instead of an industry benchmarking effect, the main variable (pay of geographically-close CEOs) excludes the compensation of CEOs at geographically-close industry peers. Including the compensation of these CEOs yields results that are somewhat stronger than those presented in the paper.

3

Why is there such a strong association between CEO compensation and geography? The

second part of the paper addresses this by exploring possible channels that may create a link

between geography and CEO compensation. The first channel is that geography may introduce

commonalities in the performance-relevant characteristics of CEOs that firms in a given area

emphasize in their selection of CEOs. Since CEOs with similar characteristics are likely to be

paid similarly, this would introduce geographical clustering in CEO pay. Test results suggest,

however, that this is not a driver of the results.

A second channel through which geography may matter is that physical proximity could

create “neighborhood effects” that cause firms to follow “leading” firms in the vicinity in setting

CEO pay (Glaeser, Sacerdote, and Scheinkman, 1996; Kedia and Rajgopal, 2009). This literature

asserts that leading firms influence others but are themselves not influenced by others. If the

leading-firm effect holds, then my previous results could be attributed to the dominant effect of

leading firms that happened to be in the geographic proximity, rather than the independent effect

of geography per se. To investigate this, I classify the top three firms in any geographic area as

the leading firms in that area, and base this classification on a variety of metrics. I then perform

two tests. The first is an examination of whether CEO pay at these leading firms is related to the

pay of CEOs of other firms in the area. In contrast to the leading-firm hypothesis, I find that it is.

Second, if the leading-firm hypothesis is correct, CEO pay at “non-leading” firms should be more

strongly related to CEO pay at leading firms than to CEO pay at all firms in that geographic area.

However, my tests reveal the opposite. Thus, both tests produce results that are generally

inconsistent with the leading-firm effect.

A third potential channel is local labor market competition for CEOs (e.g., Vietorisz and

Harrison, 1973; Kennan and Walker, 2011). If firms limit themselves to hiring CEOs from the

geographic areas in which their headquarters are located, then local competition for talent will link

geography and CEO pay. To explore this, I perform two analyses. The first is a counterfactual in

which the sample is limited to companies that were part of the S&P 500 in the previous year.

These are the largest and most prominent firms that compete in national or global labor markets

for their executives (Kedia and Rajgopal, 2009), so the compensation contracts for their CEOs are

4

the least likely to be affected by the locations of the headquarters of these firms. I find a link

between geography and CEO compensation even at these firms, providing little support for a

local-labor-market explanation. The second analysis focuses on (non-CEO) top executives: if

local labor market competition for talent drives my results, I should find a similar relationship for

these executives. The results show, however, that this is not the case. Both tests confirm that

local labor market competition is an unlikely driver of the geography effect in CEO compensation

that I document.

A fourth possible channel through which geography may affect CEO compensation is peer

comparisons arising from relative-consumption preferences. For expositional ease, I will use the

term “relative status concerns” to represent this aspect of preferences, but it should be understood

that this term is being used rather broadly to represent a range of phenomena – such as peer

pressure, “keeping up with the Joneses,” envy, etc., that all generate similar compensation-setting

incentives and observable characteristics of compensation contracts. The literature asserts that this

aspect of preferences is hardwired in people by evolution, just like risk aversion (Foster, 1972;

Robson, 2001), and emphasizes five aspects that are relevant to my tests. First, relative status

concerns are strongest within reference groups – people compare themselves more with those who

they feel more similar to (Adams, 1963; Clark and Oswald, 1996; Elster, 1991; and Festinger,

1954). Second, reference groups have a geographic component (Persky and Tam, 1990; Ferrer-i-

Carbonell, 2005; Luttmer, 2005), as first highlighted by the philosopher Thomas Aquinas (1265-

1274): “A man envies not those who are far removed from him, whether in place, time, or station,

but those who are near him.” Third, relative status concerns often involve income comparisons

(Duesenberry, 1949; Frank, 1985; Easterlin, 1995; McBride, 2001; Ferrer-i-Carbonnell, 2005;

Goel and Thakor, 2005, 2010; Dur and Glazer, 2008; Bartling and Von Siemens, 2010; Liu, 2011),

and the bigger the gap in income between an individual and his reference group, the stronger the

effect of envy (Kapteyn and van Herwaarden, 1980; Clark and Oswald, 1996; McBride, 2001;

Ferrer-i-Carbonell, 2005; Card, Mas, Moretti, and Saez, 2012).2 Fourth, high-level executives

2 There is an evolutionary explanation for this. When competing for access to scarce resources, the goal is to be better than rivals. For example, when competing for a mate, women place a premium on their potential mates’ financial prospects because they are able to invest in themselves and their offspring, while men value a woman’s youth and

5

tend to compare their income to that of others outside the firm (Goodman, 1974; Oldham, Kulik,

Stepina, and Ambrose, 1986; Kulik and Ambrose, 1992). Fifth, the effect of relative status

concerns is asymmetric in the sense that an agent envies those who make more but does not derive

positive utility from those who make less (Duesenberry, 1949; Frank, 1985; Hollander, 2001;

Ferrer-i-Carbonell, 2005; Goel and Thakor, 2005, 2010; Card, Mas, Moretti, and Saez, 2012).

A particularly important question is how CEOs choose their reference groups. Oldham,

Kulik, Stepina, and Ambrose (1986) find that most employees use only one or two. A natural first

reference group for CEOs seems to be other CEOs at similar-sized industry peers. However, since

pay consultants and executive compensation committees benchmark CEO pay against that earned

at similar-sized firms in the same industry (Bizjak, Lemmon, and Naveen, 2008; Faulkender and

Yang, 2010), one would expect a link between CEO pay and that of its industry peers even absent

envy. To account for this, all regressions control for similar-sized industry-peer compensation. A

second natural reference group for a CEO is suggested by the spatial aspect of relative status

concerns, and is comprised of the CEOs of companies in physical proximity of the CEO’s own

company. Thus, spatial considerations might influence the CEO’s expectation of pay in

negotiations with the board, and also influence the responsiveness of the board to such

considerations, thereby introducing geographical clustering in CEO compensation.3

Two tests are performed to examine the effect of relative status concerns. The first is

based on the insight that the effect of envy should be strongest (weakest) the further the CEO’s

pay lies below (above) the average of geographically-proximate CEOs ceteris paribus. This

attractiveness because she can deliver healthy offspring. As a result, other women being more attractive elicits envy in women, while men experience envy when other men have more financial resources (Hill and Buss, 2008). 3 Even if CEOs do not explicitly demand higher pay based on relative status concerns, their demands may more subtly reflect expectations that have been shaped by them observing the compensation of others in the area. The board, which is aware of the same pay data, may perceive some pressure to adjust CEO pay to be comparable to that of local CEOs, as the following quotes suggest: “A few CEOs actually feel uncomfortable with the high pay their boards urge them to accept. But given their directors' fear that lower pay might send the wrong message to the company or investors, they feel they can't afford the luxury of such modesty.” (“CEO pay: The prestige, the peril.” BusinessWeek, November 20, 2006.) “Every board wanted to pay their CEO in the top quartile.” (“U.S. companies tweak CEO pay packages ahead of vote.” Reuters, January 5, 2011.) While the expressed discomfort of CEOs with higher pay may be little more than “politically correct” public modesty, the point remains that boards may perceive pressure (implicitly from the CEO) to make CEO pay comparable to that of others in the area. The maintained hypothesis throughout is that CEOs possess some bargaining power in the determination of their pay. For evidence and discussions, see Lorsch and Maciver (1989); Hermalin and Weisbach (1998); Baker and Gompers (2003); Bebchuk and Fried (2004); Fahlenbrach (2009).

6

suggests that CEOs who earn the least relative to their geographic peers will obtain the biggest pay

increases. I therefore regress the percentage change in CEO pay on the CEO’s percentage “pay

gap,” the difference between the pay of geographically-close CEOs and the CEO’s own pay, plus

control variables. The coefficient on the pay gap is positive and significant. This result cannot be

explained away as a mere “economic mean reversion” effect. The CEO is catching up with the

mean, but it is the pursuit of a mean that should be irrelevant, were it not for relative status

concerns.

A second test of relative status concerns focuses on professional sports players’

compensation. The idea is as follows. Based on existing executive pay theories, the pay of sports

stars should be of no consequence for CEO pay. However, if CEOs envy how much sports stars in

their geographic areas make, then their wages may exhibit a correlation with CEO pay. The

results provide some evidence that CEO pay is related to the compensation of sports stars in their

areas. A robustness check which randomly assigns each city’s sports teams to another city shows

that CEO pay is not related to the pay of sports stars from randomly-chosen geographies, but is

related only to the pay of spatially-affiliated sports stars.4

In closing, this paper documents strong geographical clustering in CEO compensation and

this does not appear to reflect an industry effect or official compensation peer benchmarking.

Examination of the potential channels that may drive the link between geography and CEO pay

indicate that this result may be driven by relative status concerns or envy (e.g., Duesenberry, 1949;

Frank, 1985; Solnick and Hemenway, 1998; Ang, Nagel, and Yang, 2012; Card, Mas, Moretti, and

Saez, 2012; Shue, 2012).

The rest of the paper is organized as follows. Section 2 discusses the literature. Section 3

discusses the methodology and describes the data. Section 4 establishes a link between geography

and CEO pay – it presents the main results, robustness checks and additional analyses. Section 5

4 One may wonder why any firm would be willing to pay its CEO more because sports stars in the area make more. However, the effect of envy in this case may not be manifested quite as literally. Higher sports star compensation may simply be at work in the background, creating an environment that is more conducive to CEOs bargaining more aggressively for higher pay and boards more willing to listen because very large pay packages are in the news and “socially acceptable.” Such a political-economy explanation is consistent with the view that CEO pay determination is the outcome of a Nash bargaining game between the CEO and the board (Bebchuk and Fried, 2004).

7

examines the four alternative explanations for why geography is related to CEO pay. Section 6

summarizes and concludes.

2. THE RELATED LITERATURE

This paper is related to three strands of the literature. The first is the literature on the economic

ramifications of distance. In most papers in this strand, distance matters because information is

more efficiently procured when distances are smaller. They document that investors prefer to

invest in the stock of geographically-close firms (Coval and Moskowitz, 1999, 2001; Huberman,

2001); mutual fund managers in the same city hold similar portfolios (Hong, Kubik, and Stein,

2005); “local” investment banks have a competitive advantage in municipal bond underwriting

(Butler, 2008); analysts provide more accurate forecasts when located closer to the firms they

analyze (Malloy, 2005); acquirer returns are significantly higher in geographically-proximate

deals (Uysal, Kedia, and Panchapagesan, 2008).; greater usage of information technology at banks

has enabled small firms to borrow over greater distances (Petersen and Rajan, 2002). Distance

matters for different reasons in a small group of papers. For example, John and Kadyrzhanova

(2008) document a geographical clustering of firms with anti-takeover provisions due to peer

effects. Kedia and Rajgopal (2009) argue that labor markets for rank-and-file employees are

geographically segmented, and that this causes firms, for competitive reasons, to offer options if

geographically-close firms offer options. My paper is most closely related to this smaller group of

papers.

The second strand of related literature contains papers that examine the level of executive

compensation. For example, Bebchuk and Grinstein (2005) find that from 1993-2003, executive

pay has grown beyond what can be explained by changes in firm performance, size, and industry

mix. Gabaix and Landier (2008) argue that the substantial increase in CEO pay between 1980 and

2003 can be attributed to increases in market capitalization. Bizjak, Lemmon, and Naveen (2008)

and Faulkender and Yang (2010) show that competitive benchmarking using peer groups affects

the level of CEO pay. Yermack (1997), Bertrand and Mullainathan (2001), Bebchuk and Fried

(2004), and Kuhnen and Zwiebel (2009) explain the rise in CEO pay on the basis of an increase in

8

managerial entrenchment. By contrast, this paper focuses on the effect of local hiring of similar

CEOs, leading firms, labor market competition, and envy on CEO pay.

The paper is also related to the growing literature on relative consumption preferences and

peer comparisons of various sorts as determinants of many individual and corporate practices.

This literature was discussed in the Introduction.

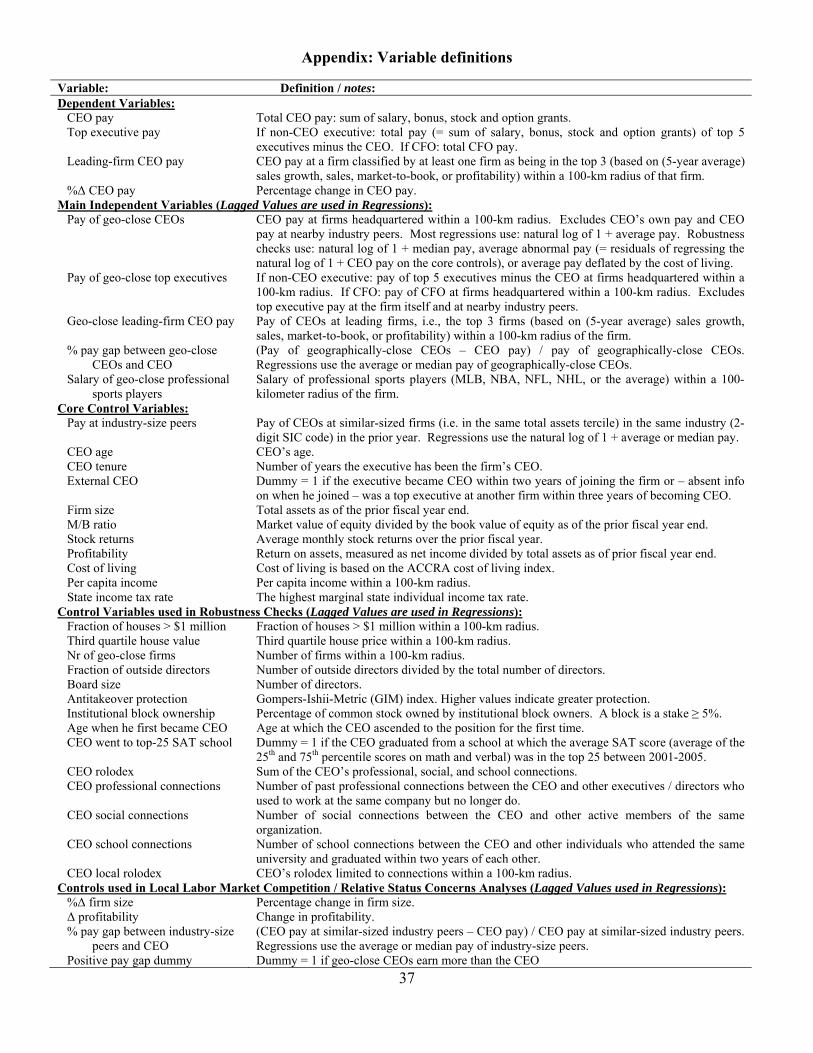

3. METHODOLOGY, VARIABLE DESCRIPTIONS, AND SAMPLE

This section first explains the methodology. It then explains how distances are calculated and

defines “geographic closeness.” Finally, the variables and the sample are described.

3.1. Methodology and Dependent Variable

Data on CEO pay are obtained from ExecuComp. Following Milbourn (2003), three variables are

used to classify whether an executive was the firm’s CEO during the fiscal year: “Became CEO,”

“Left Office,” and “Month of fiscal year-end.” In particular, if a person became CEO or left office

during the fiscal year, the executive is classified as the firm’s CEO in that fiscal year only if he

was in office for at least six months. Most analyses focus on total pay (ExecuComp item: tdc1),

which includes salary, bonus, long-term incentive payouts, other compensation, restricted stock

grants, and the Black-Scholes value of stock option grants.

To test the relationship between the compensation of geographically-close CEOs and CEO

compensation, the following model is estimated:

, , , (1)

where , is the natural log of (1 plus) CEO i’s pay in period t.

, is the natural log of (1 plus) the average compensation of CEOs

geographically-close to CEO i in period t-1 (defined in Section 3.2). X is a matrix of control

variables (discussed in Section 3.3) including the natural log of (1 plus) the average compensation

of CEOs at similar-sized industry peers, CEO age, CEO tenure, an external CEO dummy, firm

size, growth options, firm performance, the state individual income tax rate, and proxies for local

market conditions. Year fixed effects ( ) and industry fixed effects ( ) are included. Industries

9

are defined by two-digit SIC codes. Similar results are obtained when 48 Fama-French industry

groupings are used (not shown for brevity). Robust standard errors clustered by locality are

reported.5 Results are similar when standard errors are clustered by firm (not shown for brevity).

Note that the dependent variable is the log of pay while the key independent variable is the

log of average pay. The justification is that CEOs care about their pay relative to the pay of

geographically-close CEOs who they compare themselves with (e.g., Liu, 2011). The empirical

specification most consistent with the motivating theoretical foundation is one that regresses CEO

pay at date t on the average pay of geographically-close CEOs at date t-1. Taking logs of both the

dependent and independent variables is done for the usual reasons – it accounts for non-linearities,

skewness, and mitigates the effect of outliers. Using the log of pay and the log of average pay is

also consistent with the literatures on CEO pay (e.g., Faulkender and Yang, 2010) and top

executive pay (e.g., Bebchuk and Grinstein, 2005; Garmaise, 2011), and papers that examine CEO

pay relative to the pay of top earners in the firm (e.g. Bebchuk, Cremers, and Peyer, 2011).

Note that is lagged relative to in part to address

endogeneity concerns (reverse causality). This approach is in line with the literature that examines

the impact of peer pay on CEO pay (e.g., Bizjak, Lemmon, and Naveen, 2008; Faulkender and

Yang, 2010). Realizing that this may not be sufficient to establish a causal relationship, I interpret

the results with care and merely claim that they show interesting correlations. To further address

causality, Section 4.3.1 examines what happens when firms relocate their headquarters.

3.2. Key Independent Variable: Average Compensation of Geographically-Close CEOs

The key independent variable in most regressions is , , the natural log

of (1 plus) the average total compensation received in the previous year by CEOs who work at

firms headquartered within a 100-kilometer radius of the firm, i.e., that are “geographically close”

(e.g., Coval and Moskowitz, 2001; Malloy 2005; Uysal, Kedia, and Panchapagesan, 2008; Kedia

and Rajgopal, 2009). The average compensation of geographically-close CEOs does not include

5 Localities correspond to “cityfips” (from the U.S. Gazetteer “places” files): five-digit Federal Information Processing Standard (FIPS) codes that uniquely identify “populated places,” including cities, towns, and census districts. There are 639 localities in the sample.

10

the CEO’s own pay. As indicated above, it also excludes CEO pay at industry peers in the area.

This is important because the average large firm’s stated peer group in 2006 contains almost 50%

industry peers (Faulkender and Yang, 2010). Purging industry peers from my measure ensures

that I do not accidentally pick up an industry benchmarking effect. Not surprisingly, not purging

industry peers leads to somewhat stronger results (not shown for brevity).

To calculate geographic closeness, I start by obtaining the location (city) of the

headquarters of every firm in the sample from Compustat, and latitude and longitude data from the

Census 2000 U.S. Gazetteer. Two checks are performed. First, since Compustat assigns the latest

headquarter location to all years, I verify the headquarter location for every firm over the entire

sample period using 10Ks (and other financial documents if needed), and correct the location, if

necessary. To see why this is important, consider a firm that relocated its headquarters from

Dallas to New York in 2000. Absent this correction, I would use the average compensation of

CEOs in the New York area in all years, rather than Dallas compensation for the pre-2000 period.

The second check involves checking city names to ensure that they correspond with the names

found in the Gazetteer “places” files and correcting them when needed. In case a city name could

not be found on the Gazetteer file (90 instances), I check the actual location of the city on

maps.google.com and assign the observation to the nearest place that is on the Gazetteer file

within a 15-kilometer radius of the original location. The actual distance between cities is then

estimated using the Haversine formula.6

3.3. Control Variables

Executive compensation committees often use data on executive pay at similar-sized industry

peers for benchmarking purposes to determine the compensation packages awarded to top

management at their firms (e.g., Bizjak, Lemmon and Naveen, 2008; Faulkender and Yang, 2010).

To ensure that this practice is not driving my results, I create industry-size terciles (based on total

6 The haversine formula gives great-circle distances between two points on a sphere. The distance between cities 1 and 2 is calculated as d12 = R × 2 × arcsin(min(1, sqrt(a))), where R is the earth’s radius (approximately 6371 kilometers), a = (sin(dlat / 2))2 + cos(lat1) × cos(lat2) × (sin(dlon / 2))2. In this expression, dlat = lat2 − lat1 and dlon = lon2 − lon1. Lat1 and lon1 (lat2 and lon2) are the latitudes and longitudes of City1 and City2, respectively.

11

assets in the same two-digit SIC code) in each year and assign each firm to the appropriate peer

group in that year. The average peer compensation (excluding the CEO’s own pay) in the

previous year is then included in the regressions as a control variable.

Age is a well-recognized determinant of CEO pay (e.g., Gibbons and Murphy, 1992;

Bognanno, 2001). I therefore control for the CEO’s age in the regressions.

CEOs who have been in office longer may receive higher compensation because they are

more reputable/skilled and the passage of time has enabled this skill to be revealed (e.g.,

Milbourn, 2003), or because longer tenure strengthens the CEO’s ability to influence the board

and hence, his pay (Lorsch and Maciver, 1989; Hermalin and Weisbach, 1998; Baker and

Gompers, 2003; Fahlenbrach, 2009). To capture this, I control for CEO tenure, defined as the

number of years the executive has been the firm’s CEO.

CEO pay may also be affected by whether he was an external or internal hire. An external

CEO may have greater perceived ability than an insider with in-depth knowledge of the firm

(Milbourn, 2003) and may have more general managerial skills needed to run a modern firm

(Murphy and Zabojnik, 2004). If ExecuComp provides data on when the CEO joined the firm, he

is classified as external if he becomes CEO within two years of joining the firm and as internal

otherwise. If data on when the CEO joined is lacking, I use data on the top five executives: if a

CEO is a top executive at another firm within three years of becoming CEO, he is categorized as

external; if he is a top executive at the hiring firm for at least three years before becoming CEO, he

is considered an internal hire. 7

The CEO pay literature finds that compensation tends to be highly correlated with

organization size and growth opportunities, presumably because it requires greater skill to manage

a larger, more complex company with higher growth prospects (e.g., Rosen, 1982; Smith and

Watts, 1992). Firm size and growth opportunities are therefore added as control variables. Firm

size is measured as the natural log of total assets as of the prior fiscal year end. Growth

7 CEOs who cannot be classified (no prior affiliation can be found and he has been an executive of the hiring firm for less than two years) are dropped from the analysis. The use of the external hire variable causes a significant reduction in sample size. Importantly, however, when I rerun the regressions in the paper without this variable, I obtain comparable results.

12

opportunities are measured by the firm’s market-to-book (M/B) ratio, calculated as the market

value of equity divided by the book value of equity as of the prior fiscal year end.

Agency theory predicts a positive (causal) relationship between firm performance and

CEO compensation, as long as the monotonicity condition for performance/output to be increasing

in effort is satisfied (Grossman and Hart, 1983; Prendergast, 1999). Moreover, if more skilled

agents produce higher output on average, wages will also be increasing in output (see Prendergast,

1999). To capture these effects, two measures of firm performance are included: stock returns and

profitability. Stock returns are the average monthly stock returns over the prior fiscal year.

Profitability is return on assets, measured as net income divided by total assets as of the prior

fiscal year end.

The cost of living in the area may also affect CEO pay. I address this in several ways. The

main approach is to include the ACCRA Cost of Living Index, obtained from the Council for

Community and Economic Research (C2ER), in the regressions. This index is constructed as

follows. Every quarter, C2ER obtains pricing data on six major consumer expenditure categories

(housing, groceries, utilities, transportation, health care, and miscellaneous) from chambers of

commerce, economic development agencies, and universities in over 300 U.S. cities. C2ER then

applies weights to these categories based on data from the U.S. Bureau of Labor Statistics’

Consumer Expenditure Survey to obtain each participating place’s actual cost of living, which is

used to construct the ACCRA Cost of Living Index: the average price level of all participating

places in a quarter is set to 100, and each place’s score is expressed as a percentage of this

average. For example, in 2006, cost of living in the most expensive place (New York City) was

214.7 percent of the average, while that in the least expensive place (Joplin, MO) was 82.0 percent

of the average. The ACCRA Cost of Living Index is available for virtually every place in my

sample for most years. I calculate the average cost of living around each firm’s headquarters

using the same 100-km radius as before.

One might argue that my cost-of-living proxies may not fully capture the real cost-of-

living differences across geographies because not all the goods and services being consumed by

residents in an area are included in those proxies. To deal with this, I rely on the argument that

13

higher income levels go hand in hand with higher demand and higher prices of goods and services

in the area. That is, CEO compensation may be higher in areas in which the average income of all

geographically-proximate people is higher. Thus, I obtain the average per capita income for every

locality in my study from the 2000 decennial Census and use it to create an additional cost-of-

living control variable in all regressions. For consistency, the natural log of the average per capita

income is calculated using the same 100-kilometer distance cutoff as before.

It is possible that my cost-of-living proxies do not capture differences in state and local

income taxes that may impact a CEO’s effective compensation or “take-home” pay. To address

this, I obtain the individual income tax rates for every state in every sample year from the Tax

Foundation. The highest marginal rate is used in the regressions: it is 5.5% on average, and ranges

from 0% (in Arkansas, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas,

Washington, and Wyoming) to 12% (in North Dakota).8,9 Historical information on local taxes is

generally not available. To capture its effect, however, I cluster standard errors by locality (as

defined in Section 3.1) in which the firm is headquartered.

3.4. Sample

Data on CEO pay are retrieved for all firms included in ExecuComp from 1994 to 2006. Since the

analyses use lagged pay of geographically-close CEOs and industry-size peers, the sample period

is 1995-2006.

While studies on corporate policies such as capital structure and dividend policy typically

exclude financials and utilities, there is no fundamental reason to exclude them from a study that

focuses on compensation. In line with the compensation literature (e.g., Bizjak, Lemmon, and

Naveen, 2008; Kedia and Rajgopal, 2009; Faulkender and Yang, 2010), I therefore include these

firms. Hand-collected data on the actual compensation peer groups of part of the sample also

8 The CEO’s actual marginal rate is not used for two reasons. First, while ExecuComp provides the CEO’s pay and its components, his taxable income is unknown. Second, while the Tax Organization has the lowest and highest marginal tax rates and tax brackets in every sample year, it only recently started to collect all the marginal rates and tax brackets. 9 When I control for state-level differences more generally by including state fixed effects, I obtain similar results (not shown for brevity.)

14

shows the importance of doing so: 9% of the non-financial non-utility companies include

financials and/or utilities in their official compensation peer groups.10

The final sample includes 9,427 CEO-year observations from 1,563 firms and 2,269 CEOs.

The compensation of geographically-close CEOs is on average based on pay of 62 (median: 46)

CEOs.11

Table 1 Panel A contains summary statistics on the main regression variables. Panel B

presents correlations (which range from 0.05 to 0.19) between CEO pay, the average pay of

geographically-close CEOs, and the average pay of industry-size peers. Panel C lists the top and

bottom 25 cities in average compensation of CEOs at firms headquartered within a 100-kilometer

radius in 2005.

4. A LINK BETWEEN GEOGRAPHY AND CEO COMPENSATION

This section establishes a link between geography and CEO pay. It first presents the main

regression results. It then examines if the effect is robust to using alternative specifications and

introducing additional control variables. I conclude that it is. Additional analyses focus on

headquarter relocations and hand-collected data on firms’ official compensation peer groups.

All of the regression results are presented in Table 2. The main results are presented in

full. For most of the other analyses, only the coefficients on the compensation of geographically-

close CEOs and additional controls, if any, are displayed to save space.

4.1 Main Results

Table 2 Panel A Column (1) reports the main regression result: the remuneration of

geographically-close CEOs is positively and significantly related to CEO pay (t-statistics of 3.44).

Not surprisingly, the coefficient on the average compensation of CEOs in the same industry-size

10 Section 4.3.2 describes the hand-collected data in detail. A few examples: financials and utilities constitute 55% of Medco Health Solutions Inc.’s peers, 23% of Union Pacific Corp.’s peers, 19% of JC Penney Co. Inc.’s peers, and 5% of Walgreen Co.’s peers. Section 4.2.1 shows a robustness check that drops financials and utilities from the sample. 11 Recall that pay of nearby industry peers is purged from the pay of geographically-close CEOs to ensure that I do not pick up an industry benchmarking effect. The average (median) firm has 67 (51) nearby firms including industry peers.

15

tercile is also significant. This is consistent with the view that compensation consultants and

executive compensation committees take the compensation at similarly-sized firms in the same

industry into account when setting CEO pay.

The results are also economically significant. The coefficient on the average pay of

geographically-proximate CEOs is 0.122, suggesting that if other CEOs within a 100-kilometer

radius were paid 1% more in the previous year, the CEO would be paid 0.122% more this year

ceteris paribus. It is noteworthy that this effect is almost twice as large as the effect of industry-

peer compensation.12

The size of the effect may seem small compared to the finding in Faulkender and Yang

(2010) that a 1% pay increase at the firm’s stated peers is followed by a 0.58% pay increase.

However, besides differences in sample composition and period, it is important to note that they

focus on the official peers used by the firm to set CEO compensation (roughly half of which are

industry peers for the average firm), while I use geographically-close firms excluding industry

peers, so a smaller link is not surprising.

Using these results, one can conduct a simple, albeit qualified, thought experiment: how

would moving a firm’s headquarter from a bottom-25 city (in terms of average pay of

geographically-close CEOs) to a top-25 city affect CEO pay, ceteris paribus? The data suggest

that if we were to move a company from say Springfield, MO (a bottom-25 city) to Princeton, NJ

(a top-25 city) in 2006, the CEO’s compensation would be 25% higher, with the entire increase

being accounted for solely by the impact of geography. However, such a calibration exercise must

be interpreted with caution, since it extrapolates results based on local linearity assumptions that

may not be valid globally.

Not surprisingly, when using a 250-km (instead of 100-km) radius, the coefficient on the

pay of geographically-close CEOs is smaller and less significant (see Column (2)). Importantly,

12 The adjusted R-squared of 49% is comparable to other studies which include year and industry fixed effects like I do (see Gabaix and Landier, 2008; Faulkender and Yang, 2010; Engelberg, Gao, and Parsons, forthcoming).

16

randomly assigning geographically-close CEOs to CEOs yields a t-statistic close to zero (see

Column (3)).13

The results in this section indicate a strong relationship between the compensation of

geographically-proximate CEOs and CEO pay.

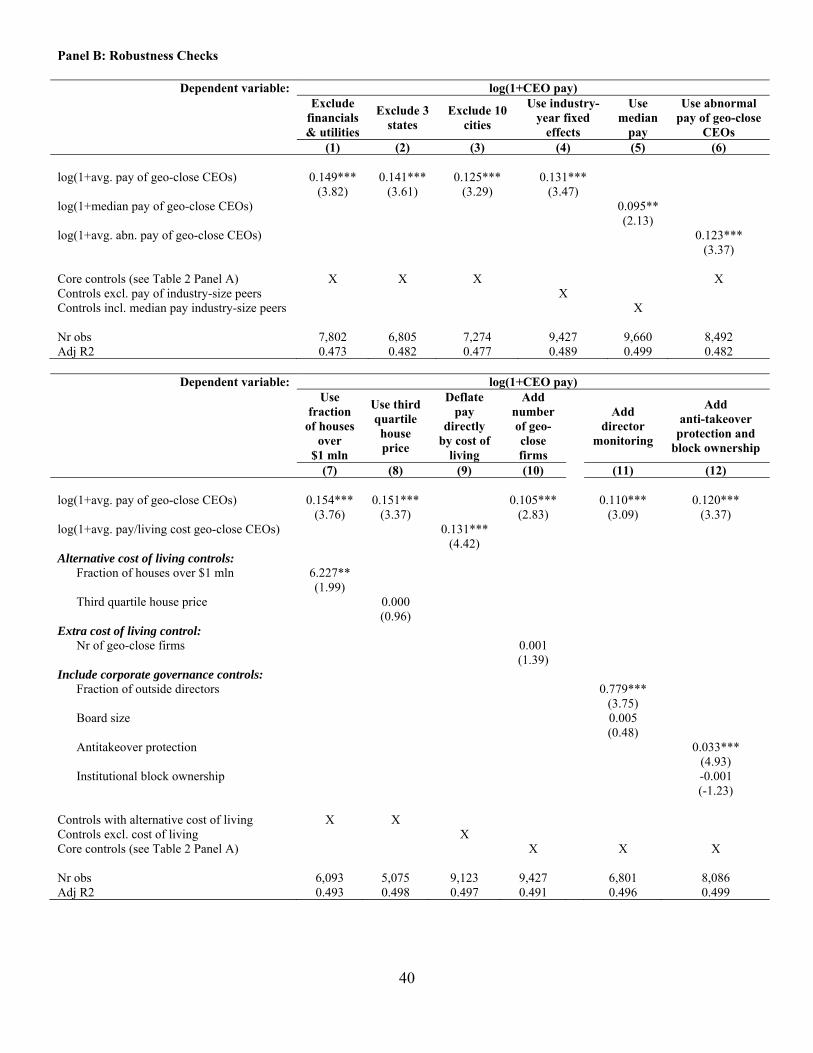

4.2. Robustness Checks

4.2.1 Excluding Financials and Utilities, Three Key States, or the Ten Largest Cities

One might suspect that compensation practices at financials and utilities differ from those in other

industries, and may not be representative of generalizable compensation practices. To ameliorate

concerns that these sectors are exercising a disproportionate influence on the results, the

regressions are rerun using a sample that excludes these industries. Similarly, compensation may

be set differently in three key states (New York, New Jersey and California) and the very largest

cities. I therefore also redo the analysis alternatively excluding key states or the ten largest cities

(as per the 2000 Census: New York City, Los Angeles, Chicago, Washington-Baltimore, San

Francisco, Philadelphia, Boston, Detroit, Dallas, and Houston).

Table 2 Panel B Columns (1) – (3) contain the results, which are comparable to the main

result presented in Panel A Column (1). Thus, the inclusion of financials and utilities, New York,

New Jersey, and California, or the ten largest cities does not seem to drive the main result.

4.2.2 Measuring Compensation

To remove the effect of industry peers on CEO pay, the main regression includes the average pay

at similar-sized industry peers and industry (and year) fixed effects. An alternative approach is to

include industry-year fixed effects. As shown in Table 2 Panel B Column (4), this does not

materially affect the results.

The main analysis examines whether the average pay of geographically-close CEOs

affects CEO pay. As a robustness check, I now use (the natural log of 1 plus) the median pay of

13 The number of observations drops: if the CEO of firm A with ten years of data is assigned the geographically-close CEOs of firm B with five years of data, the CEO of firm A will only have five years of data in this analysis.

17

geographically-close CEOs instead. All of the original control variables are included in these

regressions, except that the average compensation at similar-sized industry peers has also been

replaced by the median compensation at those firms. The coefficient on the median pay of

geographically-close CEOs in Table 2 Panel B Column (6) is smaller than in Panel A Column (1),

but continues to be statistically significant. Thus, the use of medians does not materially affect the

results.

A further concern is that abnormal (instead of actual) pay of geographically-close CEOs

may affect CEO pay. To address this, I first rerun the main regression while excluding the main

variable of interest (average pay of geographically-close CEOs), and view the residuals of this

regression as “abnormal pay,” i.e., CEO pay that cannot be explained by the core control variables.

The main regression is then rerun using (the log of 1 plus) the average abnormal pay of

geographically-close CEOs. As shown in Column (6), this yields results that are similar to the

main results.14

4.2.3 Differences in Cost of Living

The main regressions include the ACCRA Cost of Living Index to control for differences in the

cost of living. One could argue that because CEOs earn substantially more than the average

person in the area, the general cost of living may not be relevant for them. Rather, more “upscale”

benchmarks have to be used. To address this concern, I now use two alternative proxies in lieu of

the cost of living index. The first one is the fraction of houses in the area that exceeds $1 million.

This variable is obtained from the Census 2000 and is available in the year 2000 only. One

weakness of this proxy is that in some areas a $1 million house may not be representative of what

CEOs opt for; they may be living in more expensive houses. To deal with this, my second proxy

is the third quartile house price. As a first step, the Census 2000 third quartile house price is

obtained, i.e., only 25% of the houses in the area are more expensive than this price. To obtain a

different value in every sample year, the Census 2000 value is adjusted for annual house price

14 The number of observations drops: while the main analysis only requires the availability of pay of geographically-close CEOs, all the core control variables also need to be available to calculate abnormal pay of these CEOs.

18

appreciation in the area based on the Federal Housing Finance Agency House Price Index (FHFA

HPI).15 Both alternative cost of living proxies are average values calculated using the same 100-

km cutoff as before. While the sample sizes are considerably smaller, the results in Table 2 Panel

B Columns (7) and (8) are similar to the main results.

An alternative approach is to deflate compensation directly by the cost of living.

Specifically, I regress the log of (1+ CEO pay / cost of living) on the log of (1+ average pay / cost

of living of geographically-close CEOs), an alternative set of controls (the core controls except

that the average pay of similar-sized industry peers is deflated by the cost of living and no cost of

living proxy per se is included), plus year and industry fixed effects. The results (see Table 2

Panel B Column (9)) are qualitatively similar to the main results.

One could also argue that the number of geographically-close firms may proxy for the cost

of living in an area. Alternatively, one could potentially view the number of nearby firms as a

proxy for the CEO’s local job opportunities. I therefore rerun the main regression while including

the number of nearby firms as an additional control. Doing so leaves the main conclusion

unchanged (see Table 2 Panel B Column (10)).

4.2.4 Governance: Director Monitoring, Antitakeover Protection, Institutional Block Owners

Director monitoring may impact CEO pay. Although the evidence is inconclusive, this literature

tends to find that CEO compensation is positively related to the fraction of outside directors (e.g.,

Lambert, Larcker, and Weigelt, 1993; Core, Holthausen, and Larcker, 1999) and board size (e.g.,

Core, Holthausen, and Larcker, 1999). The main regressions do not control for these corporate

governance aspects because their inclusion results in a loss of a sizeable part of the sample.

However, as a robustness check, I now control for these governance characteristics. I obtain the

number of outside directors and board size from Riskmetrics’ Director database. The fraction of

outside directors is calculated as the number of outsiders (i.e., board members who are not current

executives, retired executives, or the family of present or past management) divided by the total

15 The implicit assumption is that the third quartile house price will appreciate at the same rate as an average house. Since this may not hold, the regression is also run using the unadjusted third quartile house price values. The coefficient and significance level is similar to that shown in Table 2 Panel B Column (8) (not shown for brevity).

19

number of directors. Table 2 Panel B Column (11) shows that, consistent with the existing

literature, the fraction of outside directors and board size have a positive effect on CEO pay (only

the former is significant). Importantly, however, the coefficient on the average compensation of

geographically-close CEOs remains positive and significant.

Antitakeover protection and monitoring by institutional blockholders could also affect

CEO pay. For example, antitakeover provisions may foster managerial entrenchment by

sheltering management from the market for corporate control (DeAngelo and Rice, 1983;

Gompers, Ishii, and Metrick, 2003; Dittmar and Mahrt-Smith, 2007), and entrenched managers

may find it easier to set their own pay (Bebchuk and Fried, 2004). Institutional blockholders have

sufficient capital at stake to monitor management and seem to affect their actions (Gillan and

Starks, 2000; Dlugosz, Fahlenbrach, Gompers, and Metrick, 2006; Dittmar and Mahrt-Smith,

2007). To measure antitakeover protection, I use the Gompers, Ishii, and Metrick (2003) index,

which counts the number of antitakeover provisions in a firm’s charter. The index is reported

about every two years by the Investor Responsibility Research Center (IRRC). To increase

sample size, I interpolate the index for the missing sample years. Higher values are associated

with more antitakeover protection. To measure monitoring by institutional blockholders, I obtain

data on institutional ownership from 13-F filings by Thomson Financial. The sum of all

ownership positions of at least five percent held by institutional investors is used in the analysis.

Greater ownership suggests better monitoring. Table 2 Panel B Column (12) contains the results.

As expected, greater antitakeover protection is positively associated with CEO pay, but somewhat

surprisingly, monitoring by institutional blockholders is not. Importantly, the coefficient on the

average pay of geographically-proximate CEOs continues to be highly significant.

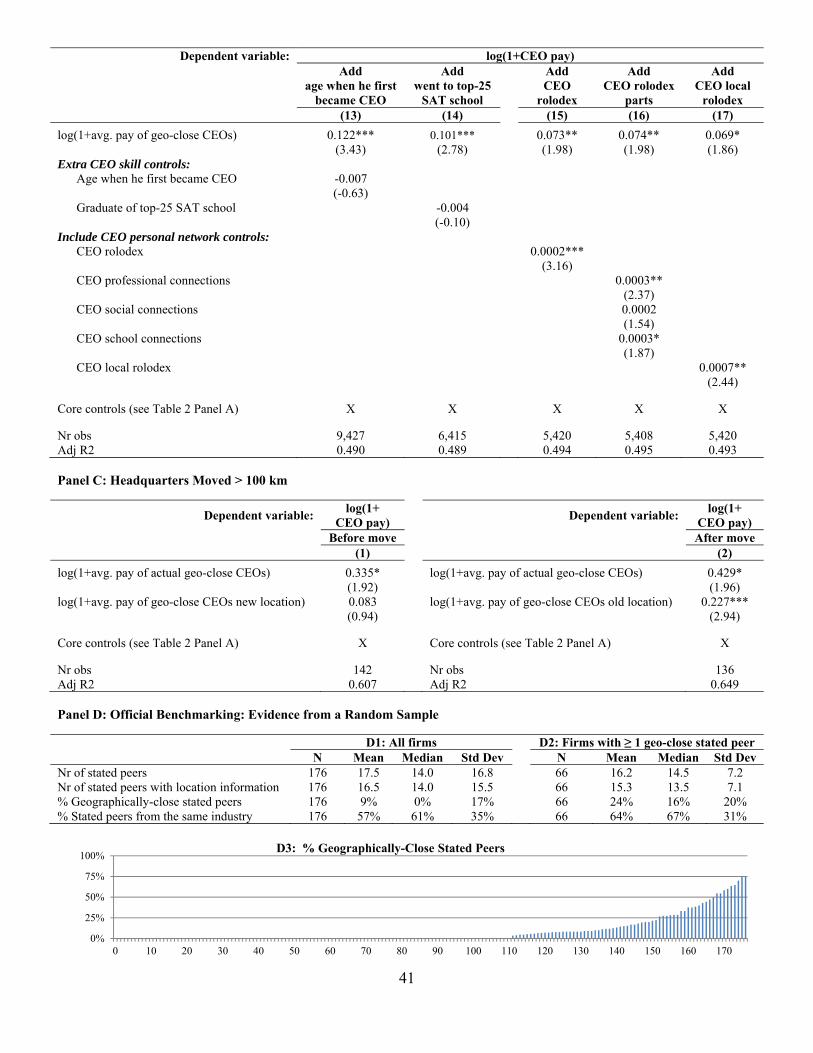

4.2.5 CEO Skill Revisited

CEOs with greater skill/ability are expected to earn more. The main regressions include CEO

tenure and an external CEO dummy as skill proxies. They also include two other variables that

may be interpreted as such: (i) firm size (it takes more skill to run a larger firm); and (ii) firm

performance, as reflected in stock returns and profitability (more skilled CEOs will show better

20

performance). However, as further robustness checks, I now consider two additional skill proxies.

The first proxy is the age at which the CEO ascended to the position for the first time. The second

skill proxy is a dummy that equals 1 if the CEO graduated from a top-25 SAT-score school

(Chevalier and Ellison, 1999; Cohen, Frazzini and Malloy, 2008). I obtain information on CEO

education from BoardEx and schools’ SAT scores from the IPEDS database maintained by the

Institute of Education Sciences at the U.S. Department of Education. Following Chevalier and

Ellison (1999) and Cohen, Frazzini and Malloy (2008), I calculate a composite SAT score using

the average of the 25th and 75th percentiles for the math and verbal scores from 2001-2005.16 The

use of this variable causes a loss of one-third of the sample since education data are only available

for a subset of CEOs.

Table 2 Panel B Columns (13) and (14) show the results. As can be seen, controlling for

the age when the CEO became CEO for the first time or including the top-25 SAT-score school

dummy does not materially affect the results.

4.2.6 Personal Networks

Engelberg, Gao, and Parsons (forthcoming) find that CEOs with large personal networks

(“rolodex”) earn more than those with small networks. The effect is particularly strong for local

connections. If CEOs located next to well-paid peers have more valuable networks, this could

possibly explain the observed link between CEO pay and pay at geographically-close firms.

To examine the validity of this claim, I construct each CEO’s rolodex following

Engelberg, Gao, and Parsons (forthcoming). I obtain the curriculum vitae of all senior executives

and directors at every firm in the BoardEx database. They include information on education

(degree, institution attended, and graduation year), social activities (memberships, positions held

in charities, etc.), and employment history (names of current and past employers, plus start and

end dates of various roles). Since BoardEx’ coverage prior to 2000 is very limited, I discard

observations before 2000 (as in Fracassi and Tate, 2012; Engelberg, Gao, and Parsons,

16 Top-25 SAT score schools include seven Ivy League institutions plus CalTech, MIT, Stanford, Chicago, Washington University in St. Louis, Northwestern, Rice, Harvey Mudd College, Pomona College, Swarthmore College, and others.

21

forthcoming). I match the BoardEx firms with CRSP and Compustat (based on CIK, ticker, cusip,

and using the name-recognition-based Levenshtein algorithm) and limit the sample to firms and

individuals that are part of this matched database.

For each CEO in this matched database, I establish the number of connections to other

individuals (excluding executives and directors at his current firm of employment) in the database.

The CEO’s rolodex is the sum of his past professional, school, and social connections. Past

professional connections are between individuals who used to work at the same company, but no

longer do. School connections are between individuals who attended the same university and

graduated less than two years apart. Social connections are between individuals who hold active

positions at the same social organization. I rerun the main regressions while first controlling for

the CEO’s rolodex, then including its components, and finally the local rolodex, i.e., ties to

directors and executives of firms within a 100-kilometer radius of the firm’s headquarters.

Table 2 Panel B Columns (15) – (17) show the results. I lose half the sample because

BoardEx data are only available for a subset of firms. Consistent with Engelberg, Gao, and

Parsons (forthcoming), the coefficients on the CEO’s rolodex and its components (professional

and school connections) are positive and generally significant, and the coefficient on the local

rolodex is significant and far larger than the coefficient on the (total) rolodex, suggesting that local

connections have a bigger impact on CEO pay than connections over greater distances.

Importantly, including these rolodex variables does not materially affect the main result: the

coefficient on CEO pay at geographically-close firms is significant in all regressions.

4.3. Additional Analyses

4.3.1 Headquarter Relocations

The results above show that CEO pay is related to the average pay of geographically-close CEOs.

Although there are some theoretical reasons why the two may be related (e.g., the vast literature

on envy) and although the main analysis uses lagged values of the main independent variable to

mitigate potential endogeneity concerns (reverse causality), it is difficult to unambiguously

establish causality. Thus, I have been careful thus far to interpret my results merely as showing

22

strong correlations rather than as evidence of a causal relationship. In an attempt to examine

causality, I now focus on headquarter relocations. Relocations are interesting because the CEO

has different geographic reference groups before and after the move. If geography causally affects

CEO pay, I should observe two things. First, before a firm relocates its headquarters, CEO pay

should be related to pay of CEOs in the firm’s actual location and not to the pay of CEOs in its

new location. Second, after the move, CEO pay should be related to pay of CEOs in its new

location and not anymore (or to a lesser extent) to the pay of CEOs in its old location.

Importantly, while the decision to relocate is endogenous, this does not matter here: to show that

geography matters, I only need the CEO’s compensation to start comoving with that of CEOs in

the new area.

While 201 sample firms relocated their headquarters, many of them moved only over a

short distance. That is problematic since in such cases, geographically-close CEOs before and

after the move overlap to a large extent, making it impossible to disentangle the effects of old

versus new peers on CEO pay. To avoid this, I require that the firm moved its headquarters over

at least 100 kilometers. This happened in 71 cases and the average distance over which they

moved is 1,548 kilometers.17

To address the first issue, I rerun the main regression using data from years t-4 to t-1

(where t=0 is the year of the move) and include the average pay of geographically-close CEOs at

both the actual (pre-move) location and the new (post-move) location. Table 2 Panel C Column

(1) shows that before the move, CEO pay is only related to what geographically-close CEOs at its

actual location earn.

To address the second issue, I run a similar regression using data from years t+1 to t+4 and

include the average pay of geographically-close CEOs at both the actual (post-move) location and

the old (pre-move) location. Table 2 Panel C Column (2) shows that after the move, CEO pay is

related to pay of geographically-close CEOs at its new location, and to a lesser extent to pay of

such CEOs at the old location.

17 In the analyses below, I lose many observations because compensation of the CEO and/or his geographically-close peers at the pre- and/or post-move location is not always available for several years.

23

The results of these relocation analyses are consistent with a causal effect of geography on

CEO pay. It would be interesting to address whether these results depend on whether the CEO

earns more or less than the average CEO in his new location. Unfortunately, it is not possible to

address this since in virtually all cases, headquarters move to locations where geographically-close

CEOs earn more than the CEO does.

4.3.2 Official Benchmarking

It is interesting to examine whether the link between CEO pay and pay of geographically-close

CEOs that I document merely reflects an official benchmarking effect. This would occur if the

official peer groups used for CEO compensation benchmarking purposes at my sample firms

included a large percentage of geographically-close firms. Unfortunately, it is not possible to

examine this over my entire sample period since firms have only been required to disclose the

names of compensation peers from December 15, 2006 onward. It is possible, however, to

analyze this issue using data from right after this compliance date. Below, I explain this analysis

and discuss the findings.

Faulkender and Yang (2010) were the first to examine large firms’ stated compensation

peer groups. They were able to find the names of such peers for 657 of S&P 900 firms. They

document that 46% of the compensation peers have the same two-digit SIC code as the disclosing

firm. They find that CEO pay is significantly affected by pay at stated peers, but do not focus on

the geographic proximity of those firms.

My sample includes 808 companies in 2006. I randomly select 25% of them and hand-

collect information on their compensation peer groups from proxy statements (DEF-14A) that are

available on EDGAR in the year after the compliance date. Out of the 202 firms included in my

random sample, 176 explicitly list the names of their compensation peers,18 yielding a grand total

18 The remaining 26 companies discuss their compensation peers in terms that are too vague to be included in this analysis. For example, electric motor manufacturer Regal-Beloit Corp. states it measures CEO pay against survey data “which consisted of information from over 100 comparable companies (referred to as our peer group).” Chocolate manufacturer Hershey’s indicates it compares executive pay against “a peer group of 54 consumer packaged goods and general industry companies” and “a subset of 15 primarily food, beverage and consumer products companies.”

24

of 3,072 peers. To calculate the distance between the 176 sample firms and each of its stated

peers, I need to know the exact location of the peers. To get this information, I try to match their

names as listed in the proxy statements with Compustat names. I am able to do so using the name-

recognition-based Levenshtein algorithm for 85% of the stated peers. Google searches are used to

try to match the remaining 15%: of these, 10% can be matched and 5% are discarded. The

manually-matched firms include firms that changed their names or were acquired later on. The

discarded set includes firms that are headquartered abroad and private firms. Latitude and

longitude data from the Census 2000 U.S. Gazetteer is then added. In case a city name could not

be found on the Gazetteer file, the actual location of the city is checked on maps.google.com and

the observation is assigned to the nearest place that is on the Gazetteer file within a 15-kilometer

radius of the original location.

Table 2 Panel D1 shows that the average firm in this random sample lists 17.5

compensation peers. I have location information for 16.5 of these peers. For the average firm, a

mere 9.0% of its stated peers are considered geographically close, i.e., are non-industry peers

located within a 100-km radius of the firm’s headquarters.19 This suggests that my main result is

not driven by competitive benchmarking.

Interestingly, out of the 176 firms in this random sample, over 60% (110) do not include

any peers that are considered geographically close using a 100-km cutoff. Panel D2 contains

summary statistics for the 66 firms that do include geographically-close firms as compensation

peers. Panel D3 shows that out of these 66 firms, in only 9 cases are more than half (55%-75%) of

the stated peers geographically close.

I also check how many firms explicitly mention in their proxy statement that they do take

geography into account when constructing pay peer groups: only 16 out of 176.20 To give a few

examples, Intuit Inc. considers firms “that have one or more attributes significantly similar to

Intuit, including size, location, general industry or products” and Southwestern Energy Co. states

19 CSX Corp. has the smallest number of peers (3) and JC Penney has the largest peer group (207). The peer groups of these two companies include no geographically-close firms. 20 One firm explicitly mentions it does not take location into consideration when setting CEO pay. Houston-based CenterPoint Energy Co. states: “we do not consider geographical differences relevant since we recruit on a national basis.” Its compensation peer group indeed does not include geographically-close firms.

25

it selects firms based on a number of factors, including “geographic location and types of

operations, total revenues, market capitalization and number of employees.” Somewhat

surprisingly, only 2 (Autodesk Inc. and Jefferies Group Inc.) of the 16 firms that mention

geography as a factor for setting CEO pay are part of the 9 firms for which over half of the peers

are considered geographically close. Maybe even more strikingly, despite considering geography

when deciding on CEO pay, only 7 out of these 16 firms list peers that are considered

geographically close.21

5. POTENTIAL EXPLANATIONS FOR THE LINK BETWEEN GEOGRAPHY AND

CEO PAY

The results above show that CEO pay is correlated with pay of geographically-close CEOs. In this

section, I examine four possible explanations for this link: (i) local hiring of similar CEOs, (ii) a

leading-firm effect, (iii) local competition for talent, and (iv) relative status concerns.

5.1. Local Hiring of Similar CEOs?

It may be that certain areas, for some reason, tend to attract firms that employ CEOs with similar

attributes. To the extent that these attributes are determinants of CEO pay, we would find

geographical clustering of CEO compensation due to this channel. I now investigate this

possibility by focusing on CEO characteristics included in the main regression and in the CEO

skills robustness check: CEO age, tenure, external CEO, degree from a top-25 SAT-score school,

and age at which the CEO ascended to the position for the first time.

If this explanation has merit, I should find that the standard deviation of each of these

characteristics variables within each local area is considerably smaller, on average, than its

standard deviation for the entire sample. For each CEO characteristic I find, however, that the two

are very similar. Specifically, the standard deviation of CEO age is 7.4 years in an average local

21 Paychex Inc. is an interesting case in this respect: while stating that its official peer group includes 15 companies that are similar-sized or are direct competitors, it adds: “The committee also receives data on CEO compensation at other large, Rochester-based public companies. This information, by itself, does not necessarily trigger a change of our CEO’s compensation.” So, while Paychex mentions geography as something it looks at, none of the firms in Paychex’ official peer group are geographically close.

26

area versus 7.3 years in the overall sample. For the other variables, the corresponding standard

deviations for the local area versus the overall sample are respectively 7.1 years versus 7.7 years

(CEO tenure), 0.46 versus 0.49 (external CEO), 0.46 versus 0.49 (top-25 SAT school graduate),

and 7.8 versus 8.0 (age when he first became CEO). I conclude that the results are unlikely to be

driven by local firms hiring “similar” CEOs.

5.2. Leading-Firm Effect?

The leading-firm effect is suggested by the literature on social interaction which proposes that

agents may be influenced by others (e.g., Murphy, Shleifer, and Vishny, 1993). Initially, a few

leading agents adopt a practice, and subsequent social interaction with these leaders causes others

to adopt the practice as well. Glaeser, Sacerdote, and Scheinkman (1996) argue that not all agents

are equal: some agents influence their neighbors but cannot themselves be influenced. Kedia and

Rajgopal (2009) use this insight to examine whether the existence of leading firms can explain

observed geographic differences in option grants for rank-and-file employees. In the context of

this paper, the social interaction effect suggests that leading firms determine the pay levels for

their CEOs and geographically-proximate firms then follow suit, generating the link between

geography and CEO pay that I find. This possibility is now examined by performing two tests.

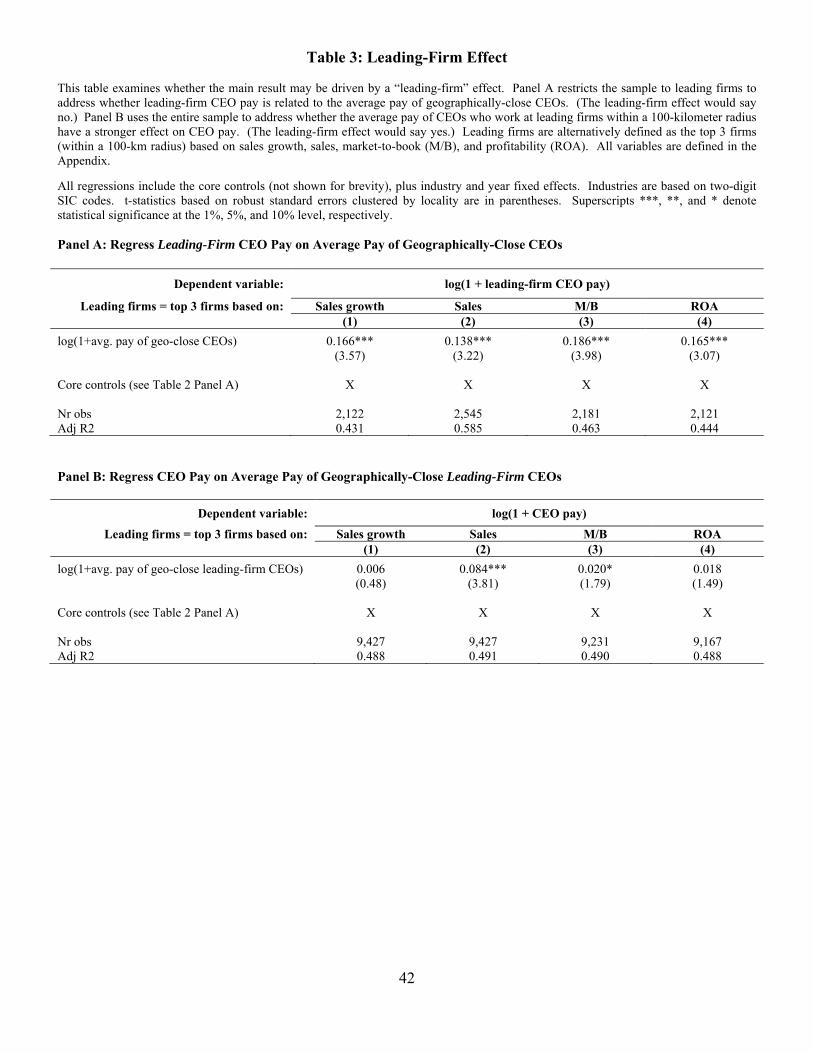

In both tests, leading firms are alternatively defined as the top three firms within a 100-km

radius based on (five-year average) sales growth; sales;22 market-to-book (M/B); and profitability

(return on assets; ROA). When presenting the results, only the coefficient on the variable of

interest is shown, although all the core controls, and industry and year fixed effects are included in

every regression.

As a first test, the base regression from Table 2 Panel A Column (1) is rerun while limiting

the sample to leading (top three) firms, and asking: is the compensation of CEO i at a leading firm

22 Kedia and Rajgopal (2009) identify leading firms based on sales. Since firm size is a strong predictor of CEO pay, one might think that a leading-firm measure based on sales is to be avoided because it could somehow cause me to pick up a firm-size effect. This concern is not warranted. It is true that the larger the leading firms are, the higher should be CEO pay at those leading firms (ceteris paribus). However, the leading firm analysis examines whether pay at leading firms is correlated with pay at nearby firms. That is, firm size is merely used to identify leading firms.

27

influenced by the average pay of CEOs at other firms in the geographic vicinity? The leading-firm

effect would say no.

Table 3 Panel A shows that the coefficients on the average pay of geographically-

proximate CEOs continue to be significant, indicating – contrary to what the leading-firm effect

would predict – that the pay of even a leading firm CEO is significantly related to the pay of other

CEOs in the geographic vicinity.

As a second test, the base regression is rerun, but in computing the average pay of CEOs of

“other firms” within a 100-km radius, attention is limited to CEO pay at leading firms. These

leading firms are subsequently excluded from the regressions. If the leading-firm effect is driving

the results, the coefficients on these alternative average CEO pay measures should be larger than

that presented in Table 2 Panel A Column (1) and more significant. That is, pay of firm i’s CEO

should be more strongly related to the average pay of geographically-close leading firms than to

the average pay of all geographically-close firms.

Table 3 Panel B shows that, contrary to what the leading-firm effect predicts, the

coefficients on the average compensation of geographically-close CEOs employed at top three

firms tend to be far smaller than in the base regression and only significant in two cases.

Thus, the evidence presented above does not seem to support a leading-firm effect.

5.3. Local Competition for CEOs?

If CEOs operate in geographically-segmented labor markets, the geographical clustering of

compensation could be driven by local labor market competition for CEOs (e.g., Vietorisz and

Harrison, 1973; Kennan and Walker, 2011). Evidence in Kedia and Rajgopal (2009), however,

suggests that labor markets are local for rank-and-file employees, but not for top executives. They

argue that this is probably driven by top executives being geographically mobile, which is

plausible since their sample includes relatively large, listed firms included in ExecuComp.

Nonetheless, to address whether local labor markets can explain geographical clustering of CEO

pay, I perform two analyses.

28

First, I start with a counterfactual. To do this, I rerun the main regression while limiting

the sample to the largest and most prominent companies in the U.S., those that were part of the

S&P 500 in the previous year. The labor market for the executives at these firms is global or

national rather than local (e.g., Kedia and Rajgopal, 2009). Therefore, if I find geographical

clustering of CEO compensation at even these firms, it represents evidence that my results are

unlikely to be driven by local labor market competition.

Table 4 Panel A contains the results. The coefficient on the average pay of geographically-

close CEOs in Column (1) is comparable to the main coefficient in Table 2 Panel A Column (1)

and continues to be highly significant. Since S&P 500 constituents are the very largest firms that

may operate in multiple industries, controlling for the average pay at similar-sized peers in the

same primary industry may not be appropriate. When I instead control for the average pay at other

S&P 500 firms, the results are very similar as shown in Column (2). Thus, even at the largest and

most prominent firms, for which CEO labor markets are global or national, CEO compensation is

significantly related to compensation of geographically-close CEOs.

Second, if local labor market competition for talent is the reason for geographic

benchmarking, one would expect to observe that all top executives get benchmarked

geographically, not just the CEO. To probe this line of reasoning, I obtain pay information on the

five highest-paid individuals at every firm in ExecuComp and keep the data only for the non-CEO

executives. I regress the natural log of (1+ average pay of top executives) in period t on the

natural log of (1+ average pay of geographically-close top executives) in period t-1, while

controlling for average top executive pay at similar-sized industry peers in period t-1, a set of

controls,23 and year and industry fixed effects. In line with the definition used for CEOs, the

average pay of geographically-close top executives excludes top executive pay at the firm itself

and at nearby industry peers.

Table 4 Panel B Column (1) shows results that differ from the CEO results – the

coefficient on the average pay of geographically-close top executives is small and not significant

23 These include the firm characteristics (firm size, M/B ratio, stock returns, and profitability) and local market condition proxies (cost of living index, per capita income, and state income tax rate) from the core controls. For data limitation reasons, top executive age, tenure, and external hire dummy are not included.

29

(t-statistic close to 0). In contrast, the coefficients on the other variables are highly significant (not

shown for brevity). To check whether this is a general result or driven by comparing executives

with very different job descriptions, I perform a similar analysis based on CFOs only. While an

advantage of this approach is that it compares individuals with the same job title, a disadvantage is

that I lose half the sample since information on CFO pay is only available if the CFO was among

the top five earners at the firm. Similar to the result for non-CEO executives, the coefficient on

the average pay of geographically-close CFOs is not significant (see Column (2)).

Thus, (non-CEO) top executive pay seems to be related to firm and industry characteristics

and cost of living rather than to what geographically-close peers earn. This may reflect lower

bargaining strength and/or the relevance of (soft) non-pecuniary factors that may enter the

executive’s perception of total rewards. To see this, note that top executives typically negotiate

with the CEO, not the board, even though formal approval of their pay may come from the board.

This negotiation includes not only a discussion of monetary compensation, but also decision-

making authority, degree of control over the allocation of resources, and the probability of being

promoted to CEO. Unobservable cross-sectional variations along these non-pecuniary dimensions

of utility-relevance to those below the CEO may swamp the effect of differences in observable

monetary compensation.

5.4. Relative Status Concerns?

As indicated in the Introduction, the first step in examining a relative-status-based explanation for

my results is the definition of the reference group. CEOs seem to have two natural reference

groups: CEOs at similar-sized industry peers and CEOs at companies headquartered near the

CEO’s own company. The first should matter even absent relative status concerns because

compensation consultants and executive compensation committees typically benchmark CEO pay

against that earned at similar-sized firms in the same industry. However, to make sure that this is

not driving my results, all regressions below control for industry-peer compensation. The second

reference group, defined by geography, has not been previously examined empirically and is the

key focus of the analyses described below. Table 5 contains all the results.

30

5.4.1. Main Relative Status Results

The first relative status test builds on the insight that the less a person earns relative to his peers,

the more envious he will be.24 This implies that the bigger the percentage pay gap between the

CEO and his peers, the greater the percentage increase in pay he will try to obtain in order to

“catch up with his peers” (e.g., “keep up with the Joneses” as in Abel, 1990; Gali, 1994). To

examine this, I regress the percentage change in CEO pay on the CEO’s percentage pay gap, the

difference between the pay of geographically-close CEOs and the CEO’s own pay (expressed as a