the future of the otc derivative market - eugene stanfield

TRANSCRIPT

The future of the OTC Derivative MarketThe impact of Central Clearing

1

Agenda

Impact of mandatory central clearing on OTC derivatives

Cost of doing business

Collateral management efficiency

Regulations still to shape how we do business

2

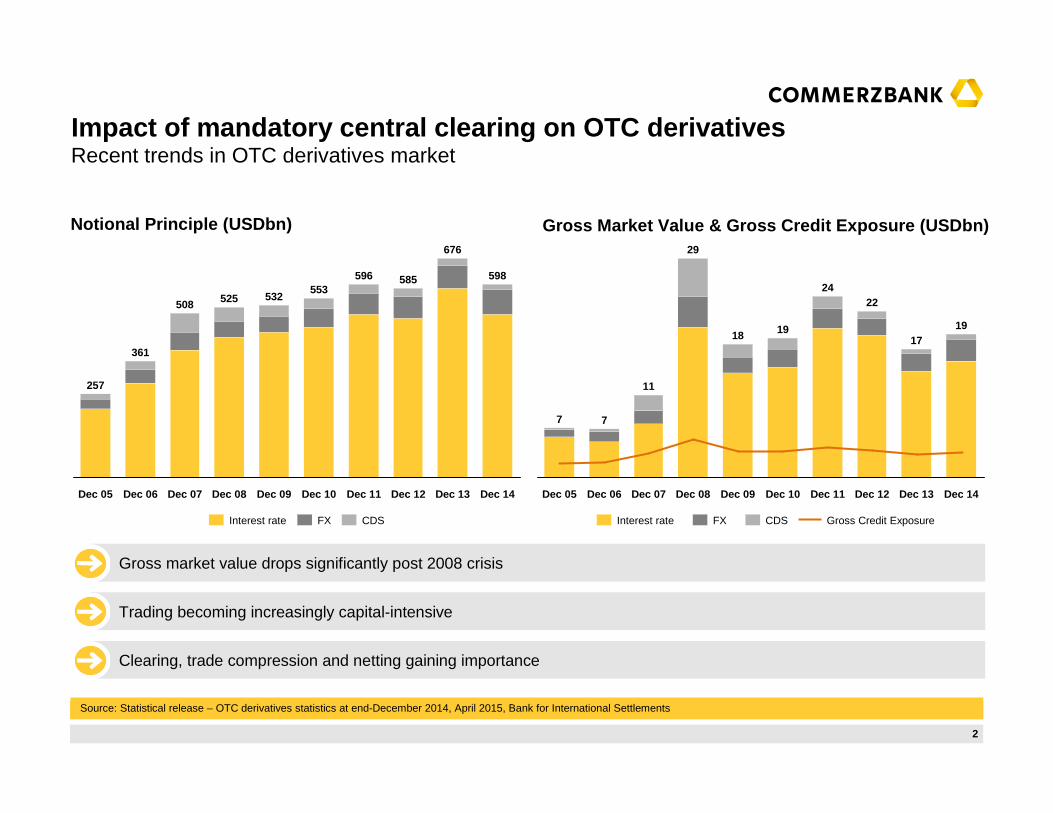

Impact of mandatory central clearing on OTC derivat ives

Source: Statistical release – OTC derivatives statistics at end-December 2014, April 2015, Bank for International Settlements

Gross market value drops significantly post 2008 crisis

Trading becoming increasingly capital-intensive

Clearing, trade compression and netting gaining importance

Recent trends in OTC derivatives market

Dec 12

585

Dec 11

596

Dec 10

553

Dec 09

532

Dec 08

525

Dec 07

508

Dec 06

361

Dec 05

257

Dec 14

598

Dec 13

676

CDSFXInterest rate

Notional Principle (USDbn)

Dec 10

19

Dec 09

18

Dec 08

29

Dec 07

11

Dec 14

19

Dec 13

17

Dec 12

22

Dec 11

24

Dec 06

7

Dec 05

7

Gross Credit ExposureCDSFXInterest rate

Gross Market Value & Gross Credit Exposure (USDbn)

3

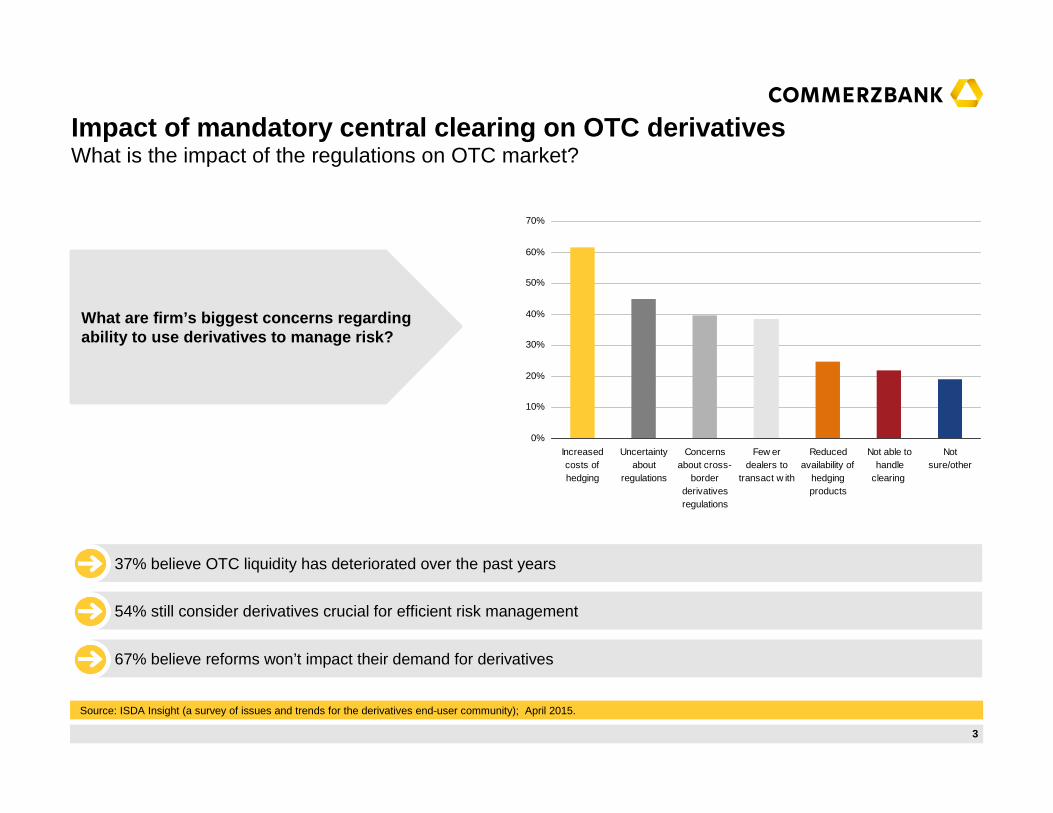

What is the impact of the regulations on OTC market?

37% believe OTC liquidity has deteriorated over the past years

54% still consider derivatives crucial for efficient risk management

67% believe reforms won’t impact their demand for derivatives

Source: ISDA Insight (a survey of issues and trends for the derivatives end-user community); April 2015.

Impact of mandatory central clearing on OTC derivat ives

What are firm’s biggest concerns regarding ability to use derivatives to manage risk?

0%

10%

20%

30%

40%

50%

60%

70%

Increasedcosts ofhedging

Uncertaintyabout

regulations

Concernsabout cross-

borderderivativesregulations

Few erdealers to

transact w ith

Reducedavailability of

hedgingproducts

Not able tohandle

clearing

Notsure/other

4

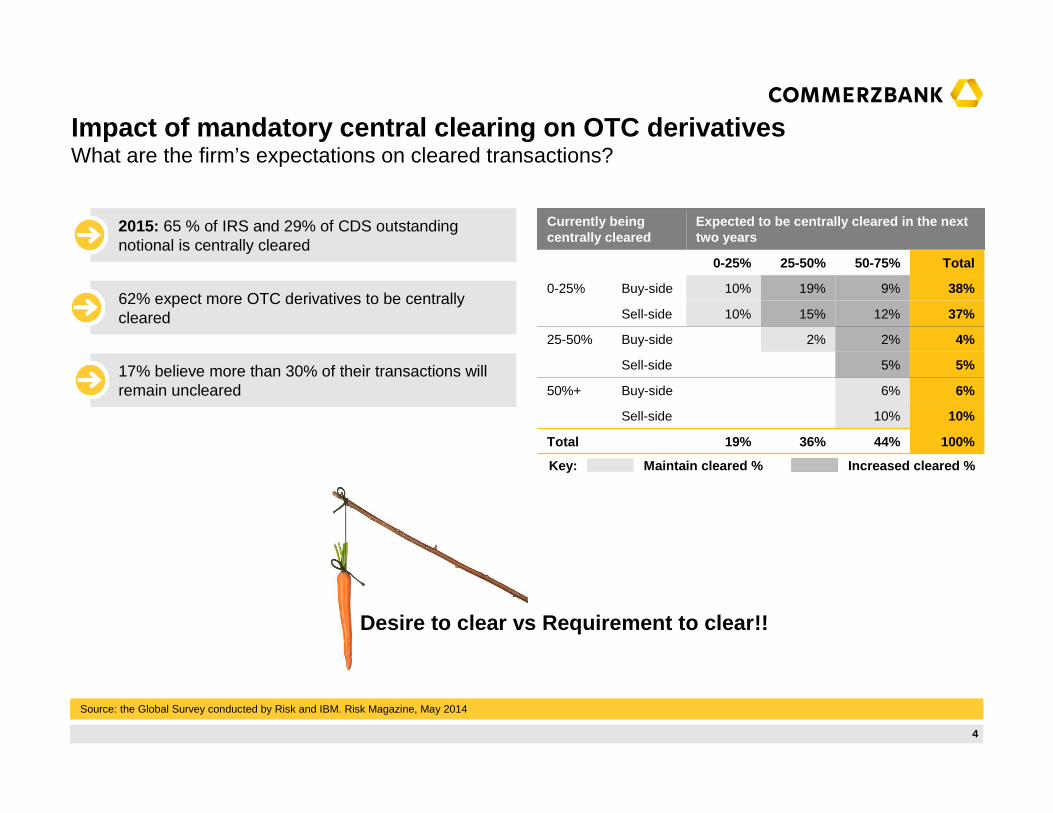

62% expect more OTC derivatives to be centrally cleared

17% believe more than 30% of their transactions will remain uncleared

Source: the Global Survey conducted by Risk and IBM. Risk Magazine, May 2014

2015: 65 % of IRS and 29% of CDS outstanding notional is centrally cleared

What are the firm’s expectations on cleared transactions?Impact of mandatory central clearing on OTC derivat ives

Currently being centrally cleared

Expected to be centrally cleared in the next two years

0-25% 25-50% 50-75% Total

0-25% Buy-side 10% 19% 9% 38%

Sell-side 10% 15% 12% 37%

25-50% Buy-side 2% 2% 4%

Sell-side 5% 5%

50%+ Buy-side 6% 6%

Sell-side 10% 10%

Total 19% 36% 44% 100%

Maintain cleared % Increased cleared %Key:

Desire to clear vs Requirement to clear!!

5

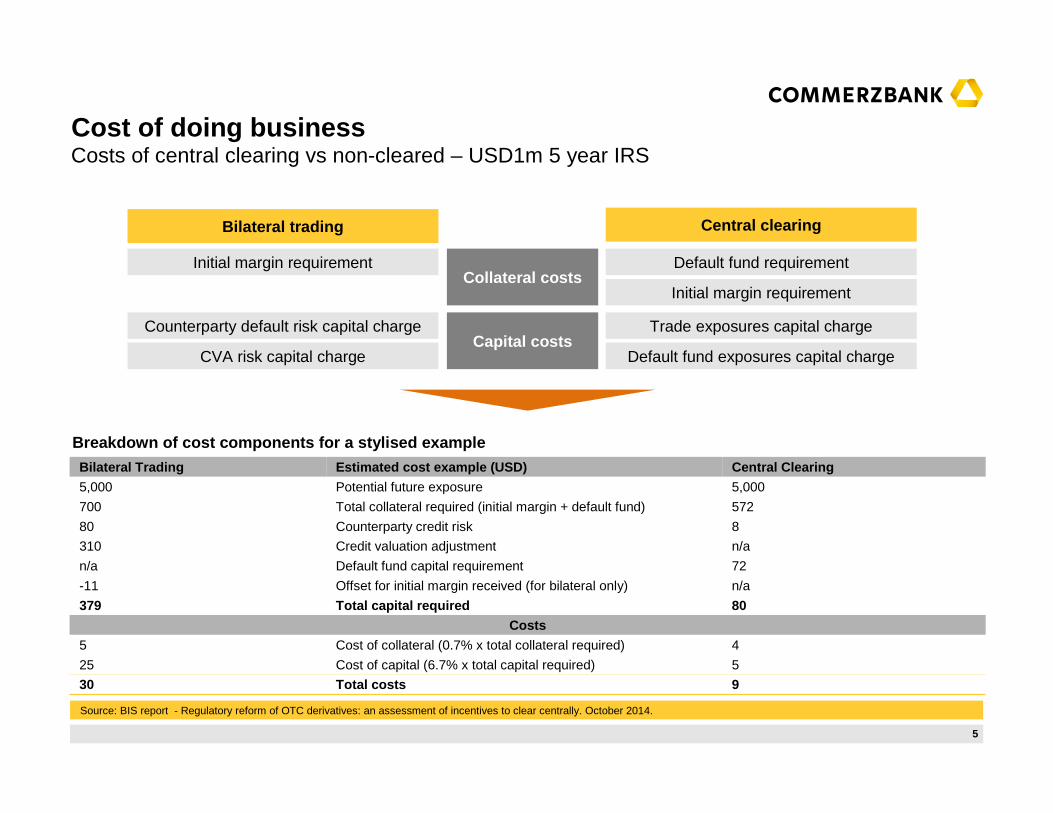

Source: BIS report - Regulatory reform of OTC derivatives: an assessment of incentives to clear centrally. October 2014.

Collateral costs

Capital costs

Initial margin requirement

Default fund requirement

Default fund exposures capital charge

Trade exposures capital charge

Initial margin requirement

CVA risk capital charge

Counterparty default risk capital charge

Central clearingBilateral trading

Cost of doing businessCosts of central clearing vs non-cleared – USD1m 5 year IRS

Breakdown of cost components for a stylised example

Bilateral Trading Estimated cost example (USD) Central Clearing

5,000 Potential future exposure 5,000

700 Total collateral required (initial margin + default fund) 572

80 Counterparty credit risk 8

310 Credit valuation adjustment n/a

n/a Default fund capital requirement 72

-11 Offset for initial margin received (for bilateral only) n/a

379 Total capital required 80

Costs

5 Cost of collateral (0.7% x total collateral required) 4

25 Cost of capital (6.7% x total capital required) 5

30 Total costs 9

6

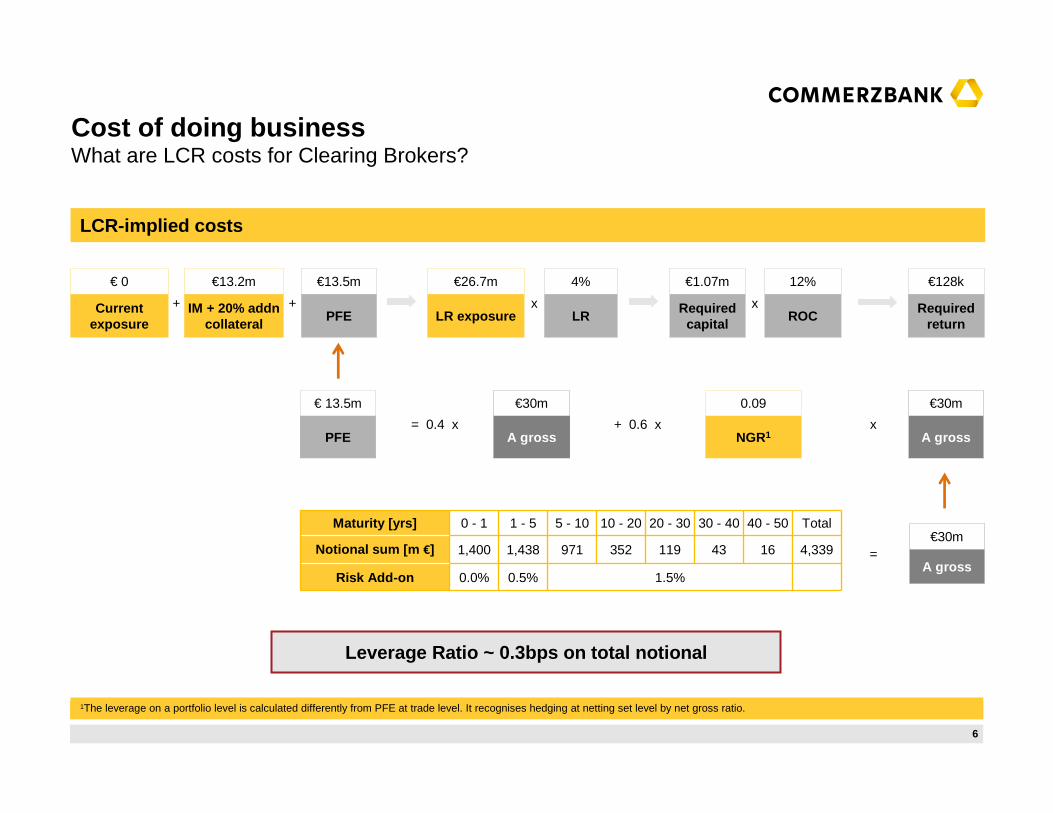

1The leverage on a portfolio level is calculated differently from PFE at trade level. It recognises hedging at netting set level by net gross ratio.

Cost of doing businessWhat are LCR costs for Clearing Brokers?

LCR-implied costs

Maturity [yrs] 0 - 1 1 - 5 5 - 10 10 - 20 20 - 30 30 - 40 40 - 50 Total

Notional sum [m €] 1,400 1,438 971 352 119 43 16 4,339

Risk Add-on 0.0% 0.5% 1.5%

= €30m

A gross

€ 13.5m

= 0.4 x

€30m

+ 0.6 x

0.09

x

€30m

PFE A gross NGR1 A gross

€ 0

+

€13.2m

+

€13.5m €26.7m

x

4% €1.07m

x

12% €128k

Current exposure

IM + 20% addn collateral

PFE LR exposure LRRequired

capitalROC

Required return

Leverage Ratio ~ 0.3bps on total notional

7

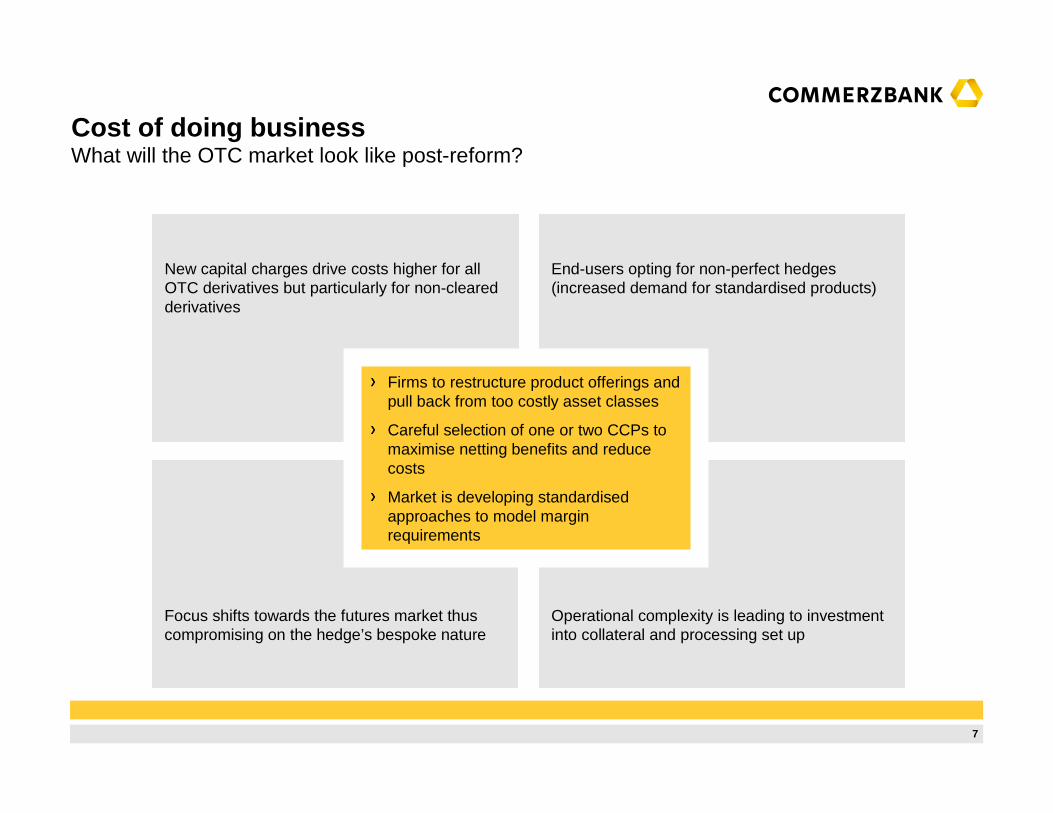

New capital charges drive costs higher for all OTC derivatives but particularly for non-cleared derivatives

Focus shifts towards the futures market thus compromising on the hedge’s bespoke nature

End-users opting for non-perfect hedges (increased demand for standardised products)

Operational complexity is leading to investment into collateral and processing set up

Firms to restructure product offerings and pull back from too costly asset classes

Careful selection of one or two CCPs to maximise netting benefits and reduce costs

Market is developing standardised approaches to model margin requirements

Cost of doing businessWhat will the OTC market look like post-reform?

8

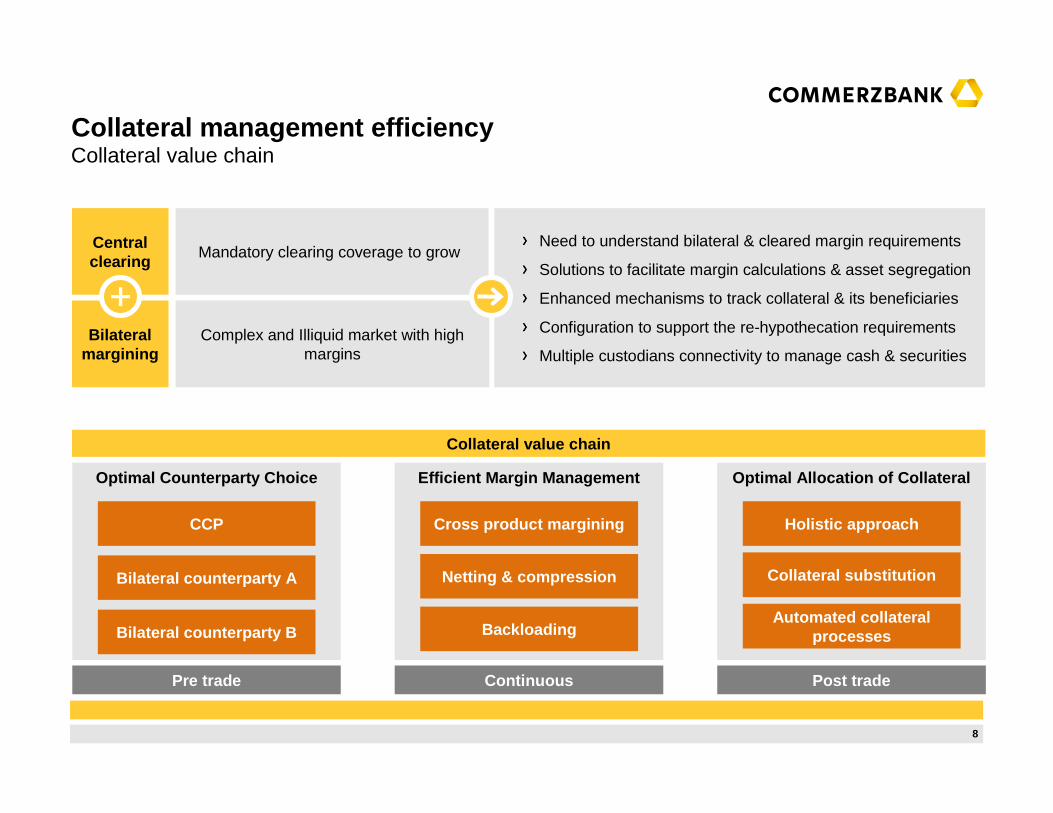

Collateral value chain

Need to understand bilateral & cleared margin requirements

Solutions to facilitate margin calculations & asset segregation

Enhanced mechanisms to track collateral & its beneficiaries

Configuration to support the re-hypothecation requirements

Multiple custodians connectivity to manage cash & securities

Central clearing

Mandatory clearing coverage to grow

Bilateralmargining

Complex and Illiquid market with high margins

Collateral value chain

Optimal Counterparty Choice Efficient Margin Management Optimal Allocation of Collateral

CCP

Bilateral counterparty A

Bilateral counterparty B

Cross product margining

Netting & compression

Backloading

Holistic approach

Collateral substitution

Automated collateral processes

Pre trade Continuous Post trade

Collateral management efficiency

99

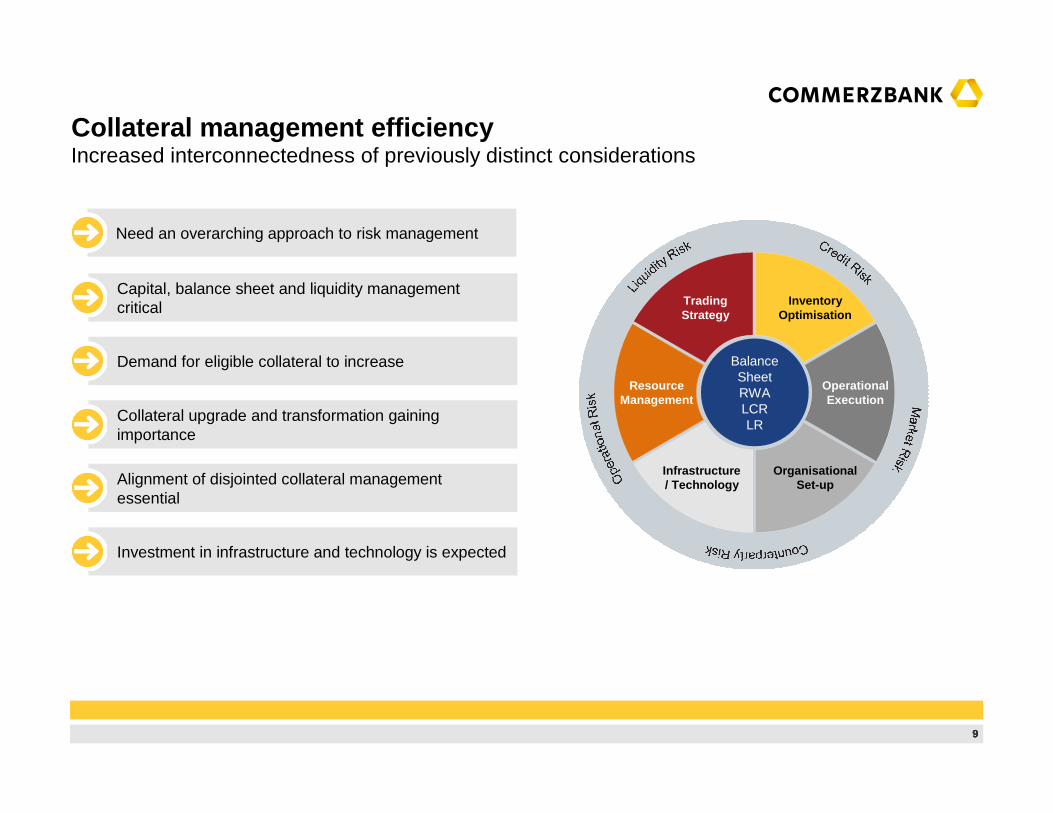

Need an overarching approach to risk management

Alignment of disjointed collateral management essential

Investment in infrastructure and technology is expected

Demand for eligible collateral to increase

Collateral upgrade and transformation gaining importance

Capital, balance sheet and liquidity management critical

Increased interconnectedness of previously distinct considerationsCollateral management efficiency

Inventory Optimisation

Operational Execution

Organisational Set-up

Infrastructure / Technology

Resource Management

Trading Strategy

Balance SheetRWALCRLR

10

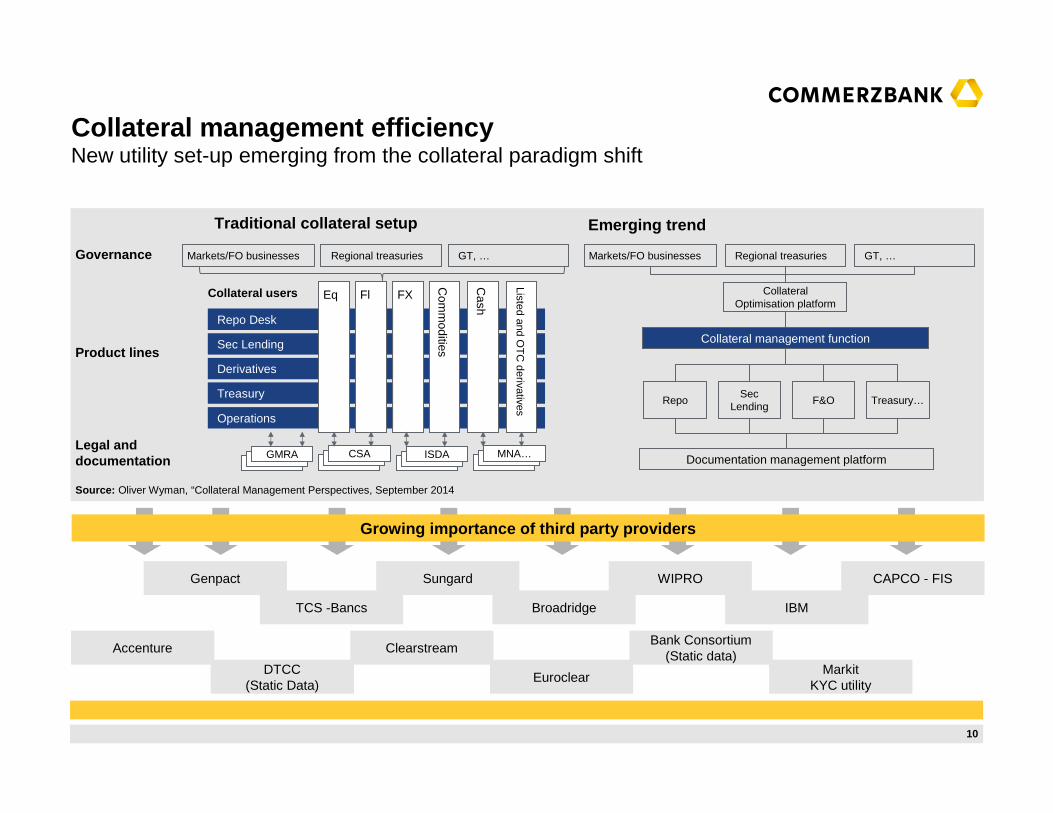

Documentation management platform

Sungard

Accenture

Markit KYC utility

DTCC(Static Data)

Genpact

TCS -Bancs

Clearstream

Broadridge

CAPCO - FIS

Euroclear

Bank Consortium(Static data)

WIPRO

IBM

Growing importance of third party providers

New utility set-up emerging from the collateral paradigm shiftCollateral management efficiency

Repo Desk

Sec Lending

Derivatives

Treasury

Operations

Collateral management function

Sec Lending

Repo F&O Treasury…

Markets/FO businesses Regional treasuries GT, …

Collateral Optimisation platform

Eq Fl FX

Com

modities

Cash

Listed and OT

C derivatives

Governance

Product lines

Legal and documentation

Collateral users

Traditional collateral setup Emerging trend

Markets/FO businesses Regional treasuries GT, …

MNA…ISDACSAGMRA

Source: Oliver Wyman, “Collateral Management Perspectives, September 2014

11

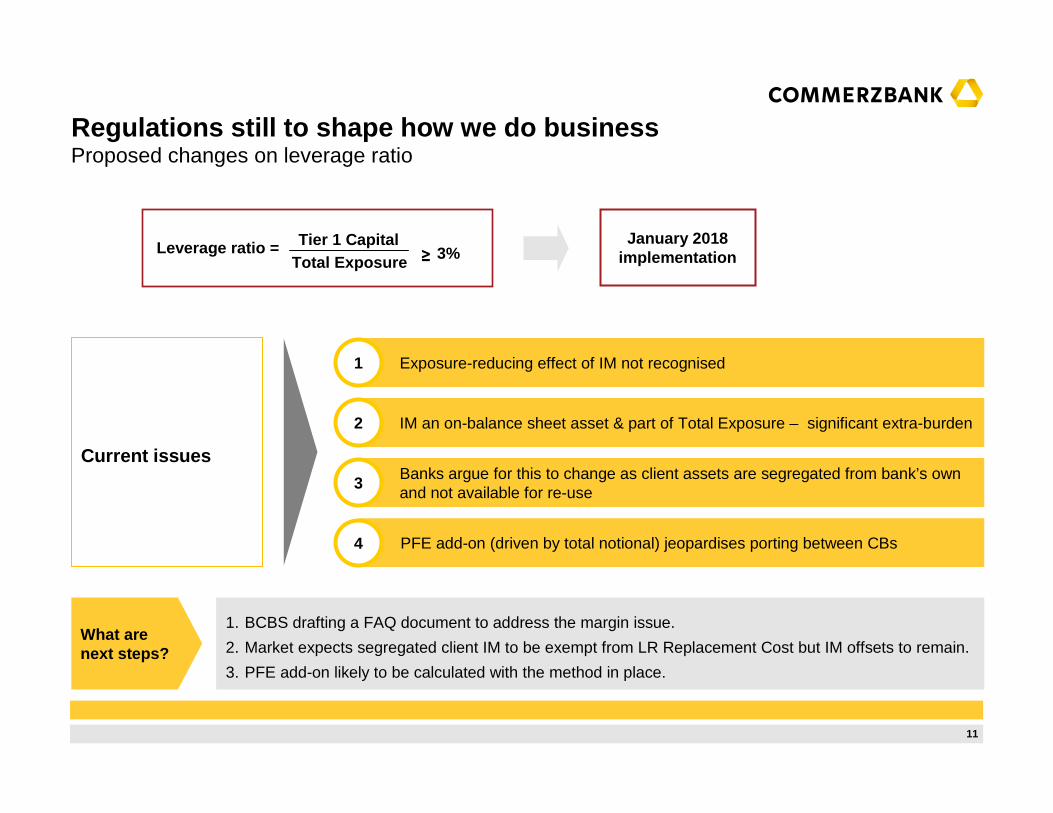

Current issues

Leverage ratio = Tier 1 CapitalTotal Exposure ≥ 3%

January 2018implementation

Proposed changes on leverage ratio Regulations still to shape how we do business

1. BCBS drafting a FAQ document to address the margin issue.

2. Market expects segregated client IM to be exempt from LR Replacement Cost but IM offsets to remain.

3. PFE add-on likely to be calculated with the method in place.

What are next steps?

Exposure-reducing effect of IM not recognised1

PFE add-on (driven by total notional) jeopardises porting between CBs4

IM an on-balance sheet asset & part of Total Exposure – significant extra-burden2

Banks argue for this to change as client assets are segregated from bank’s own and not available for re-use

3

12

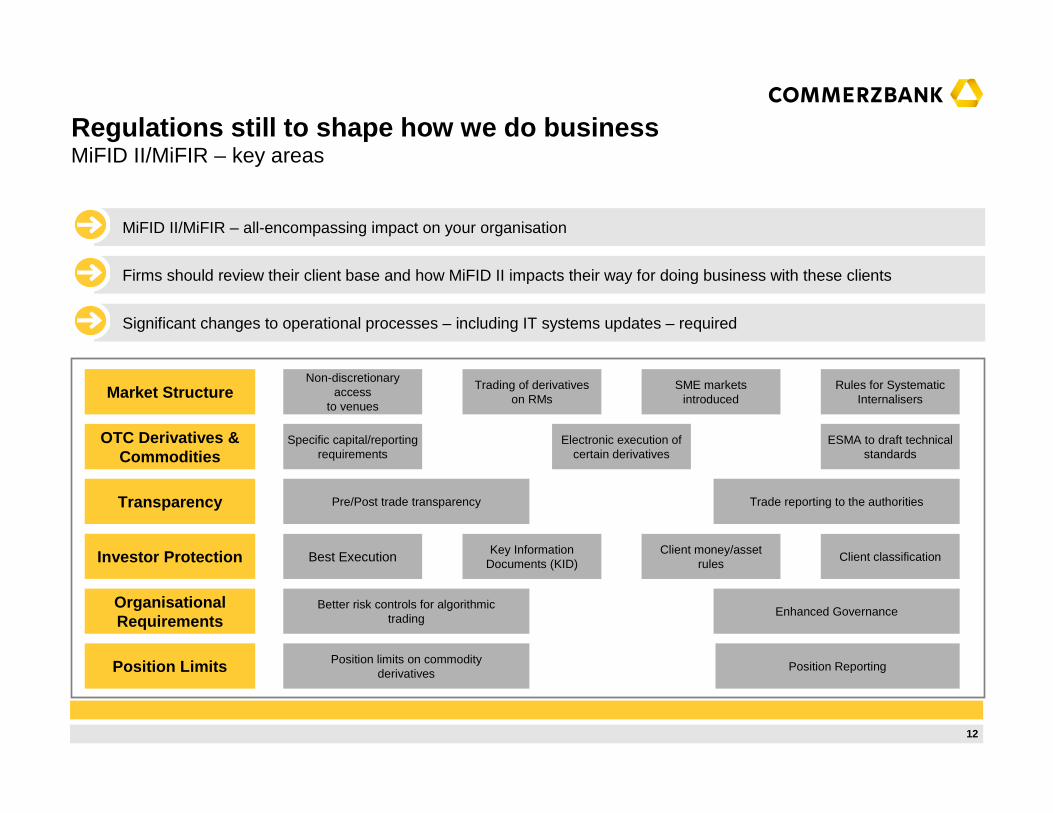

MiFID II/MiFIR – all-encompassing impact on your organisation

Transparency

Investor Protection

OrganisationalRequirements

Position Limits

OTC Derivatives &Commodities

Market StructureNon-discretionary

accessto venues

Trading of derivativeson RMs

SME marketsintroduced

Rules for SystematicInternalisers

Specific capital/reporting requirements

Electronic execution ofcertain derivatives

ESMA to draft technicalstandards

Pre/Post trade transparency Trade reporting to the authorities

Best ExecutionKey Information

Documents (KID)Client money/asset

rulesClient classification

Better risk controls for algorithmic trading

Enhanced Governance

Position limits on commodityderivatives

Position Reporting

Firms should review their client base and how MiFID II impacts their way for doing business with these clients

Significant changes to operational processes – including IT systems updates – required

MiFID II/MiFIR – key areasRegulations still to shape how we do business

13

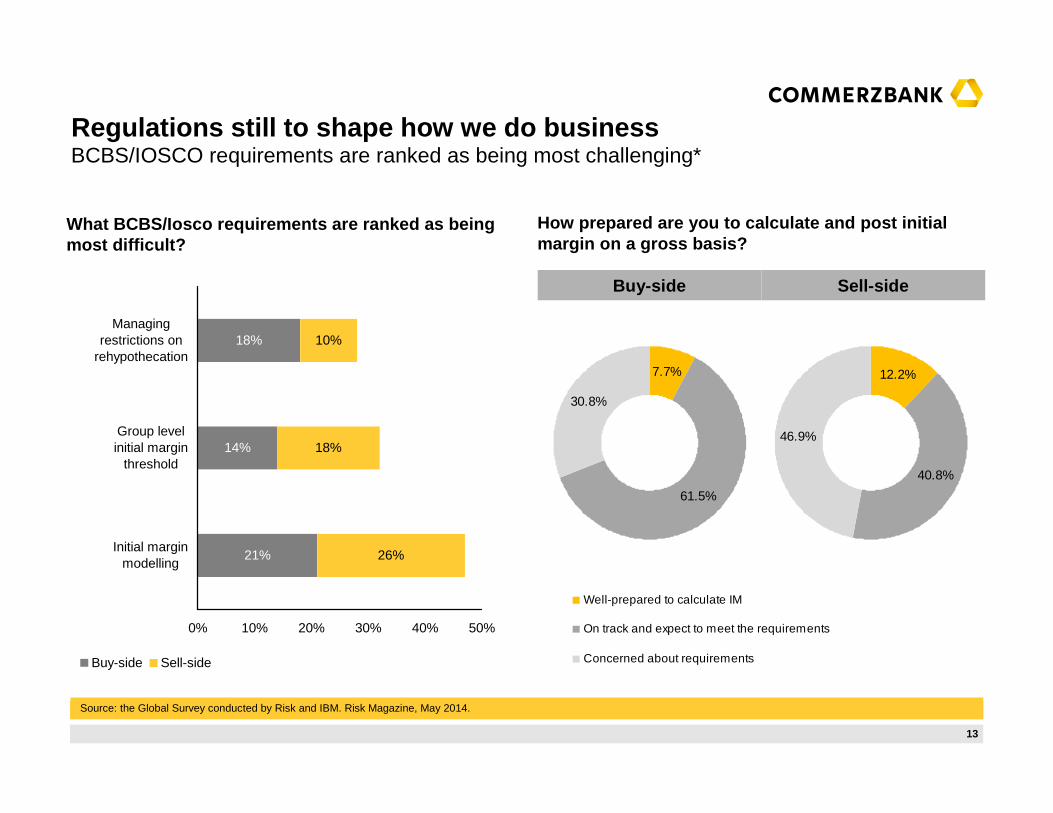

Source: the Global Survey conducted by Risk and IBM. Risk Magazine, May 2014.

What BCBS/Iosco requirements are ranked as being most difficult?

How prepared are you to calculate and post initial margin on a gross basis?

BCBS/IOSCO requirements are ranked as being most challenging*Regulations still to shape how we do business

26%

18%

10%18%

14%

21%

0% 10% 20% 30% 40% 50%

Initial marginmodelling

Group levelinitial margin

threshold

Managingrestrictions on

rehypothecation

Buy-side Sell-side

Buy-side Sell-side

7.7%

61.5%

30.8%

12.2%

40.8%

46.9%

Well-prepared to calculate IM

On track and expect to meet the requirements

Concerned about requirements

14

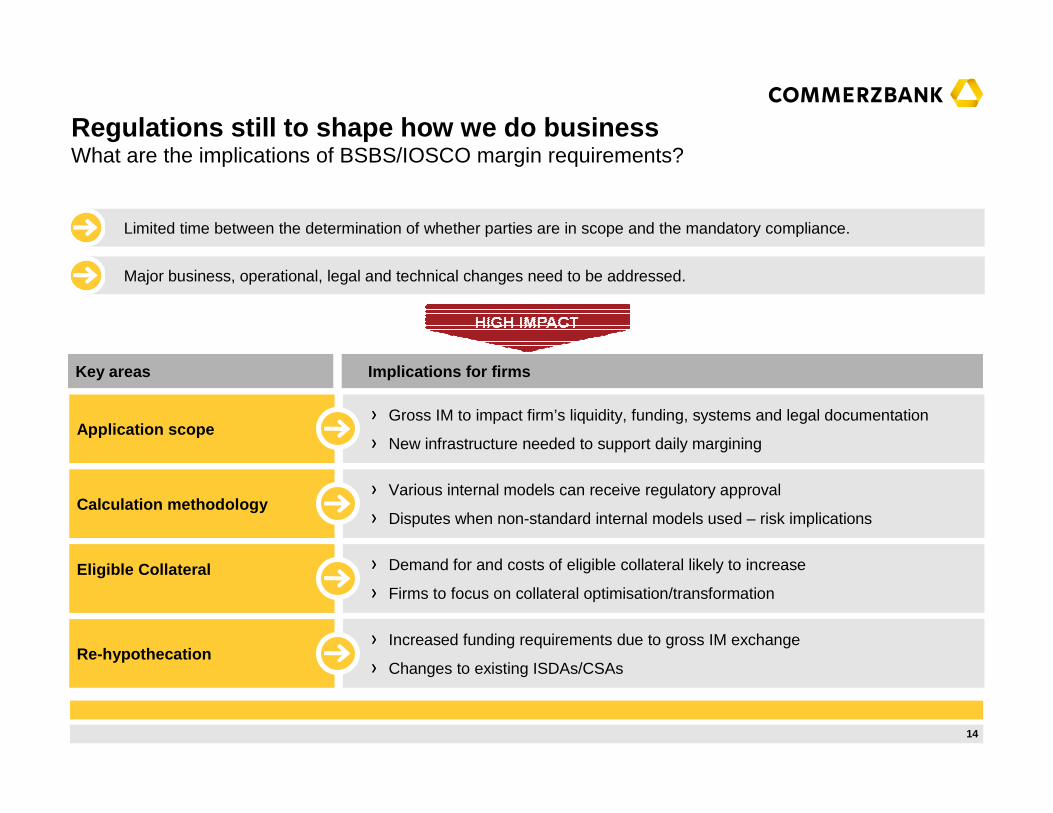

Limited time between the determination of whether parties are in scope and the mandatory compliance.

Major business, operational, legal and technical changes need to be addressed.

What are the implications of BSBS/IOSCO margin requirements?Regulations still to shape how we do business

Gross IM to impact firm’s liquidity, funding, systems and legal documentation

New infrastructure needed to support daily marginingApplication scope

Various internal models can receive regulatory approval

Disputes when non-standard internal models used – risk implicationsCalculation methodology

Demand for and costs of eligible collateral likely to increase

Firms to focus on collateral optimisation/transformation

Eligible Collateral

Increased funding requirements due to gross IM exchange

Changes to existing ISDAs/CSAsRe-hypothecation

Implications for firmsKey areas

15

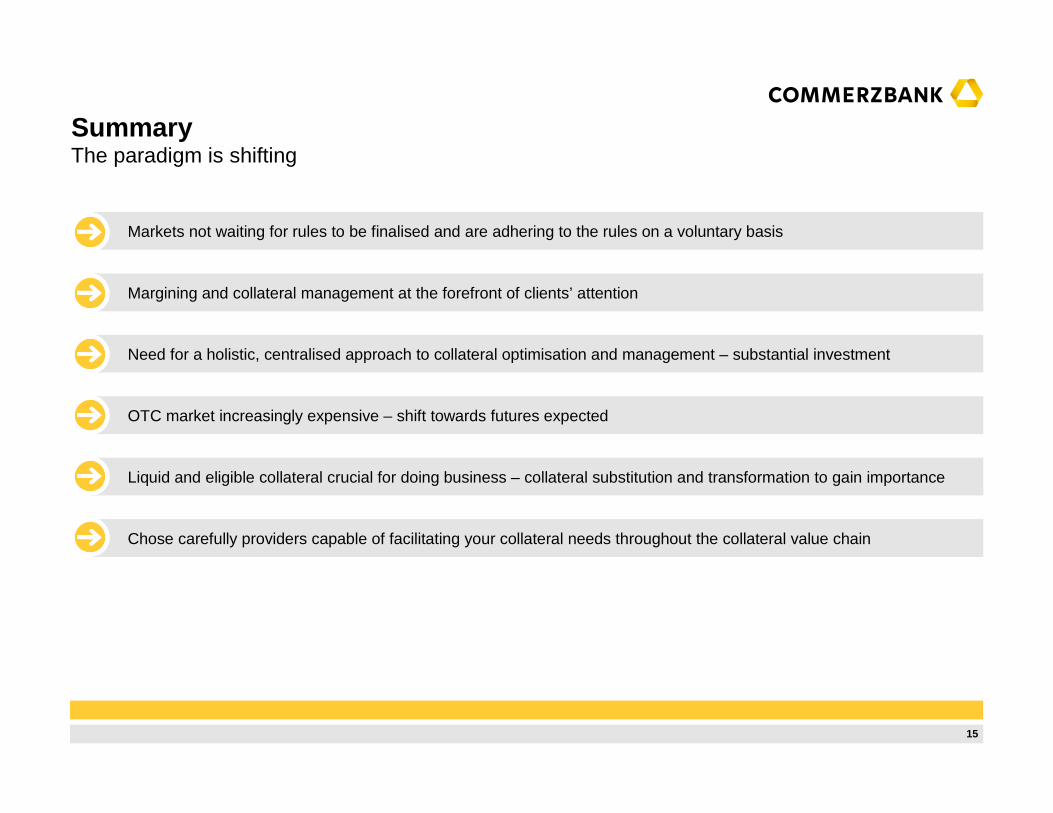

Markets not waiting for rules to be finalised and are adhering to the rules on a voluntary basis

The paradigm is shiftingSummary

Margining and collateral management at the forefront of clients’ attention

Need for a holistic, centralised approach to collateral optimisation and management – substantial investment

Chose carefully providers capable of facilitating your collateral needs throughout the collateral value chain

Liquid and eligible collateral crucial for doing business – collateral substitution and transformation to gain importance

OTC market increasingly expensive – shift towards futures expected

16

Thank you

Questions?

17

This presentation has been prepared by Commerzbank Corporates & Markets, which is the trading and investment banking division of CommerzbankAktiengesellschaft (“Commerzbank”). This document is for discussion purposes only. It is intended to provide information and outline certain basic points of business understanding relevant to OTC Clearing requirements and services. It does not attempt to describe all the relevant terms for such services. Recipients of this presentation should seek independent advice as to the legal and regulatory implications for them of the OTC clearing requirements referred to herein in order to determine their applicability to them in the light of their particular circumstances. Commerzbank is not acting as an adviser, and neither this document nor any communications from it should be treated as constituting professional advice. Commerzbank makes no representations as to the accuracy or completeness of any statements made herein or made at any time orally or otherwise in connection herewith and all liability (in negligence or otherwise) in respect of any such matters or statements is expressly excluded, except only in the case of fraud or willful default. The information in this presentation is subject to change without notice and may be amended, superseded or replaced in its entirety by subsequent material and developments. The material herein is based on data obtained from sources considered reliable and believed to be correct as at the date of issue, but its accuracy or completeness is not guaranteed. Any opinions expressed in this document are those of Commerzbank only as at the date of writing and are subject to change without notice.

This communication is issued by Commerzbank. Commerzbank AG, London Branch is authorised by Bundesanstalt für Finanzdienstleistungsaufsicht(BaFin) and subject to limited regulation by the Financial Conduct Authority and Prudential Regulation Authority. Details about the extent of our regulation by the Financial Conduct Authority and Prudential Regulation Authority are available from us on request. Copyright © Commerzbank 2015. All rights reserved.

Disclaimer

Commerzbank AG Corporates & Markets FICS Product Management 60261 Frankfurt am Main / Tel.: +49 (069)136-42020 / www.commerzbank.de