the future of digital retail - asia retail congress 2016

TRANSCRIPT

1

THE FUTURE OF DIGITAL RETAIL

Deborah Weinswig

Fung Business Intelligence Centre Global Retail & Technology

Cell: 917-655-6790

@debweinswig

2

AGENDA

• About Fung Business Intelligent Centre (FBIC)

• Top 16 Disruptors for 2016

• Top Five Retail Technology Trends in Asia

3

Fung Business Intelligence Centre (FBIC)

• Established in 2000 and headquartered in Hong Kong

• FBIC serves as the knowledge bank and think tank for the Fung Group

– Collects and analyzes market data on sourcing, supply chains, distribution and retail

– Provides thought leadership on technology and other key issues

• New York–based Global Retail & Technology team

– Follows broader retail and technology trends

– Provides advice and consultancy services to colleagues and business partners of the

Fung Group

– Builds collaborative knowledge communities

4

Futureproofing

• Anticipating future trends and developments

• Plan for future value and avoid obsolescence

– What problem are you trying to solve?

– How will the solution be used?

– How robust does it need to be?

• Ensure flexibility to manage changing formats and deployment patterns

5

OUR PARTNERSHIP WITH ACCELERATORS

Alchemist Accelerator is an accelerator exclusively for startups whose revenue comes

from enterprises, not consumers.

CoCoon is a coworking space where entrepreneurs, creative talent, successful leaders

and investors meet, collaborate and deliver results together. Member companies get

access to networking opportunities, work space, a photography studio and mentors.

Entrepreneurs Roundtable Accelerator (ERA) provides participant companies with an

intensive four-month program, with the goal of helping early-stage companies progress

rapidly into exciting, viable businesses.

New York Fashion Tech Lab is an accelerator that is a result of a collaboration between

the Partnership Fund for New York City, Springboard Enterprises and major fashion retailers.

It focuses on early- and growth-stage companies.

Plug and Play is a global innovation platform. It connects startups to corporations, and

invests in over 100 companies every year. Its 360° ecosystem allows for remarkable

innovation to take shape on an international scale.

Techstars is a global ecosystem that empowers entrepreneurs to bring new technologies

to market wherever they choose to build their business.

6

Fung Capital/FBIC

Commerce Technology Landscape

7

TOP 16 DISRUPTORS IN 2016

8

Top 16 DISRUPTORS in 2016

1. IoT-DrivenPartnerships

2. E-Commerce Players Go Offline

3. Ready-to-Cook/Eat Economy

4. Online Grocery Shopping

5. Online Fashion Resale Marketplaces

Show Explosive Growth

6. Samsung Pay Accelerates Contactless

Payment Adoption

7. Sharing Economy

8. A Subset of the Sharing Economy Is

the Rental Economy

9. Subscription Economy Is Nibbling Away

at Traditional Retailers’ Sales

10. Caring Economy Promotes Startups for

Social Good

11. Experience Economy Is Taking Away

Retail Spending

12. Home Furnishings Market Disrupted by

E-Commerce Pure Plays

13. Jet.com

14. Athletic Brands Investing in Fitness Apps

15. Facial Recognition

16. Lack of Disruptors: Victoria’s Secret

9

1. IoT-Driven Partnerships

• Unprecedented cross-industry partnerships being formed

• Samsung and Microsoft developing IoT devices based on Windows 10

• Panasonic is partnering with Denver to transform it into the first smart city

– Create an energy-efficient hub

– Solar technology, tele-medicine tech, traffic management

and security

• Audi and Qualcomm are partnering to integrate Qualcomm’s Snapdragon 602A to provide cutting-edge connectivity technology

– Infotainment, advanced smartphone connectivity,

navigation, voice quality and control features

10

1. IoT-Driven Partnerships

• Ford is partnering with Amazon to integrate

vehicles with Echo, Amazon’s smart-home

device

• Intel is working with New Balance on an

Android Wear fitness watch that is due out next

holiday season

• IBM and Under Armour are integrating the

Watson supercomputer with the Connected

Fitness network to analyze data and provide

real-time coaching on health and fitness

• Volvo pursued a partnership with Microsoft to

enhance connected-car strategies

– The Microsoft Band can be pressed and told to start

the car heater, for example

11

2. E-Commerce Players Go Offline

• Millennials prefer mono-brand brick-and-mortar stores, and they shift between online and offline along the shopping journey

Retailer # of Stores

1

1

20

19

12

2. E-Commerce Players Go Offline

Case Study: Warby Parker

– Targeting millennials

– Started exploring offline with pop-ups and

a showroom in its NYC office; now

expanding to over 20 cities in the US

– Warby Parker’s stores make more than

$3,000 per sq. ft., putting the retailer in

an elite category with companies such as

Tiffany and Apple

– More than 85% of store shoppers will

later visit the website, increasing the

chances for further orders

13

3. Ready-to-Cook/Eat Economy

Disruptors: Blue Apron, Munchery, Plated, HelloFresh

• Blue Apron was the fastest-growing US e-tailer in 2014, with

sales growing 550%, to $65 million

• Healthier and cheaper than eating out and takeout

• Convenience: ready-to-cook boxes and curated grocery

according to menus, delivered to your doorstep

• US food market

– $1.2 trillion, with $600 billion

in restaurants

– Millennial focused

550% in 2014

14

4. Online Grocery Shopping

Disruptors: Instacart, AmazonFresh

• Walmart Grocery Pickup

– Order online

– Pick up at the store

• Amazon Prime Pantry, $5.99

– Order everyday items online, filling the box

– Ship to your home

– Gamified promotion, slower shipping options in

exchange for free Pantry

• Instacart: Personal Grocery Shopper/Multiple Stores

15

5. Online Fashion Resale Marketplaces

Show Explosive Growth

Disruptors: thredUP, Tradesy, The RealReal, Poshmark, Vestiaire Collective

• Online resale industry is worth $34 billion in the US

• SnobSwap estimates the market is growing at a 10% compound annual rate

• Mobile is hot in resale; over 45% of thredUP’s sales come from mobile devices

• Patagonia, Eileen Fisher and H&M launched resale programs

Source: thredUP

16

Disruptors: thredUP, Tradesy, The RealReal, Poshmark, Vestiaire Collective

• Why Online Resale Marketplaces Took Off

– Heavy venture capital investment in online consignment industry (over $450 million)

– Retail brands’ resale programs encouraged consumers’ sustainable consumption habits

– Consumers are convinced by great quality

of secondhand apparel bought via online

platforms

– Societal shift toward less ownership —

the art of decluttering

5. Online Fashion Resale Marketplaces

Show Explosive Growth

17

6. Samsung Pay Accelerates Contactless

Payment Adoption

Disruptor: Samsung Pay

• Samsung Pay will accelerate the current slow adoption of contactless payment because it uses magnetic stripe capability (MST) chips

– MST works with new and older credit card

terminals—no additional investment required

– Most widely accepted mobile wallet in the

US

– Consumers can incorporate loyalty cards

into Samsung Pay

– In 2016: expanding to China, lower-priced

handsets and online transactions

Digital Payment Method Acceptance by North American Retailers

As of July 2015 Source: Boston Retail Partners

18

7. Sharing Economy

Disruptors: Uber, Airbnb, Lending

Club, WeWork

• Valuations of sharing economy

companies have skyrocketed

• Revenues are projected to catch

up to aggressive valuations:

Startup Industry Valuation

Uber Car Sharing $50.0 B

Airbnb Peer-to-Peer Accommodation $25.0 B

Didi Kuaidi Car Sharing $16.5 B

WeWork Office Sharing $10.0 B

Lending Club Peer-to-Peer Lending $7.4 B

OLA Car Sharing $5.0 B

Etsy Maker Online Marketplace $3.5 B

HomeAway Peer-to-Peer Accommodation $3.0 B

Lyft Car Sharing $2.5 B

Instacart Logistics/Delivery $2.0 B

Prosper Peer-to-Peer Lending $1.9 B

TransferWise Finance $1.0 B

Funding Circle Finance $1.0 B

$15 Billion

2013

$335 Billion

2025

CAGR: 29.5%

Source: PwC

Source: Company reports/analysts’ estimates

19

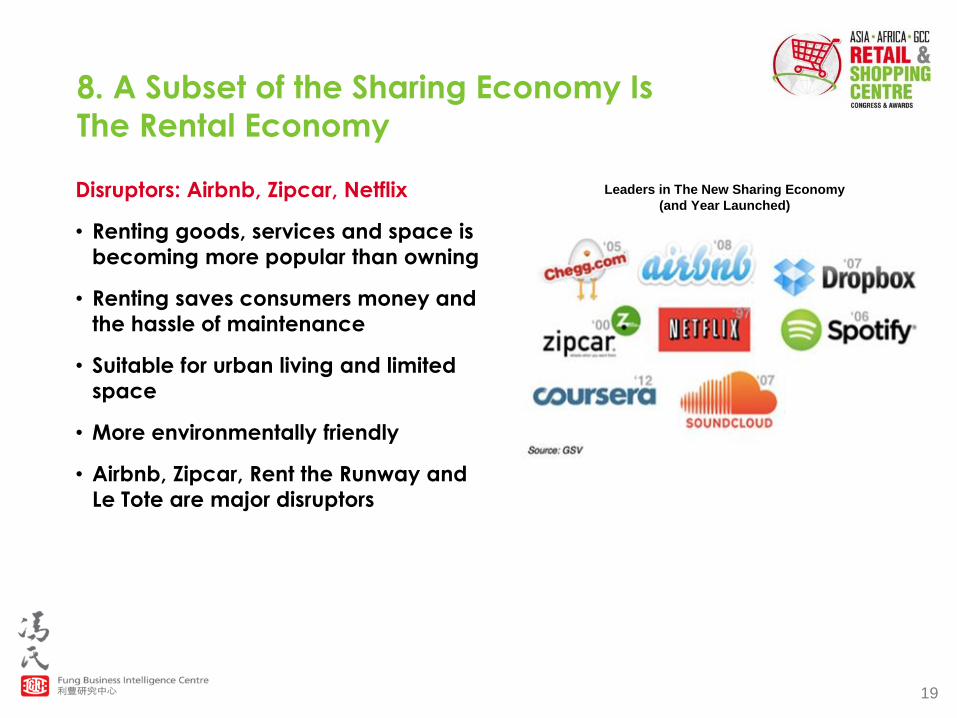

8. A Subset of the Sharing Economy Is

The Rental Economy

Disruptors: Airbnb, Zipcar, Netflix

• Renting goods, services and space is

becoming more popular than owning

• Renting saves consumers money and

the hassle of maintenance

• Suitable for urban living and limited

space

• More environmentally friendly

• Airbnb, Zipcar, Rent the Runway and

Le Tote are major disruptors

Leaders in The New Sharing Economy

(and Year Launched)

20

9. Subscription Economy Is Nibbling Away at

Traditional Retailers’ Sales

Disruptors: Le Tote, Birchbox, BarkBox, Pijon, Stitch Fix

• Convenience and curated products for consumers

• Recurring revenue model for retailers

• Element of self-gifting

• Beauty is the biggest category

• Fashion styling subscriptions

are becoming popular

21

10. Caring Economy Promotes Startups for

Social Good

Disruptors: TOMS, Reformation, Warby Parker,

NOURI, SoapBox Soaps, Zady, GoodXChange

• Social activism over self-indulgence

– Consumers, especially Gen Z, are increasingly demanding

integrity from brands and retailers

• Startups for social good apply market-based

strategies to achieve a social goal

– TOMS, the shoe company, has a “one for one” business model

– Reformation designs and manufactures sustainable apparel,

sourcing sustainable fabrics and vintage garments

22

11. Experience Economy Is Taking Away

Retail Spending

Disruptors: Gigzolo, Zaptravel, OpenTable, Beautified

• Consumers are spending less on apparel and more on experiences

• 78% of millennials prefer to spend money on an experience rather than

buying something desirable

• Gigzolo: curated network of musicians and DJs available for hire for events

• Zaptravel:

– Digital travel agent

– Uses a semantic search engine to scroll through its database

23

12. Home Furnishings Market Disrupted by E-

Commerce Pure Plays

Disruptors: Wayfair, Hayneedle,

Art.com, Houzz

• E-commerce pure plays are gaining

significant market share from omni-

channel home retailers

• They offer more curated products

and good customer service

• Houzz is an online home-remodeling

community of 35 million users

worldwide that connects

homeowners with design inspirations

and home professionals

US Furniture E-Commerce Outlook

Source: eMarketer/Forrester Research

$15

$18 $20

$23

$26

$29

$32

2012 2013 2014 2015 2016 2017 2018F

Sales Forecast (USD Bil.)

24

12. Home Furnishings Market Disruptor: Houzz

• Founded in 2009, Houzz is aiming to

disrupt the home furnishings space

• Houzz is an online home-remodeling

community that connects homeowners

with design inspirations and home

professionals

• Its business model is driven by

community, content and commerce

• Houzz has already attracted 35 million

users across 200 countries

25

13. Jet.com (Pricing Model and Smart Cart Technology)

Disruptor:

• Smart Cart technology: savings increase

with each item added, based on the

location of the sellers and the buyer

• Pulls costs out of the supply chain and

bumps them back to customers

• A win-win situation for retailers and

consumers

• On average, 9% cheaper than Amazon

and 6% cheaper than Walmart (Profitero)

+10% +10%

+6% +7%

+11%

+7%

+12%

+8% +7%

+4%

-2%

+7% +6%

+10%

Baby Beauty Electronics Grocery Household OfficeSupplies

Pet Supplies

Price Comparison of Jet, Amazon and Walmart

Amazon vs. Jet Walmart vs. Jet

More Expensive than Jet

Less Expensive than Jet

26

13. Jet.com (Customers Can Feel Smart)

• Website offers constant comparison and savings versus Amazon.com

• Also tracks cumulative savings on Jet.com

• Customers can “see” savings by waiving return privileges or through shipping synergies (Smart Cart)

• Clean, simple website and mobile app

27

14. Athletic Brands Investing in Fitness Apps

Disruptor: Under Armour

• Under Armour’s Connected Fitness Platform

– Company launched its own fitness app, UA Record

– Introduced UA HealthBox: set includes wristband, heart

rate monitor and scale, priced at $400

– Under Armour owns the world’s largest digital health and

fitness community, with 130 million users

– One of eight people purchasing a fitness device will be

synced on UA’s platform—Apple Watch and Google are

not competing

2013

2015

2015

2015

$475 million (cash)

Feb. 2015

$85 million (cash)

Jan. 2015

Jul. 2015

(terms undisclosed)

$150 million (cash)

Dec. 2013

28

15. Facial Recognition

Disruptor: Intel

• The global advanced Facial Recognition market expected growth: $2.77 Bil. in 2015 to $6.19 Bil. in 2020

(CAGR 17.4%)

• 30% of retailers are using facial recognition technology to track customers in stores (CSC)

• Applications are increasing: health, wellness, beauty and advertising

– Determine the thickness and application of makeup

– Analyze in-store shopper data

• In 2015, Walmart tested with FaceFirst:

– Cameras check you in at location

– Smartphone receives customized deals based on demographic

• Intel released RealSense facial recognition technology

in 2015

– Consumer grade 3D cameras

– Home usage: camera recognizes face to unlock front door

• Challenges: Consumers are not especially comfortable with technology use in retail

29

16. Lack of Disruptors: Victoria’s Secret

Disruptor: Who will it be?

• Victoria’s Secret’s Success Formula

– Marketing via $12 million annual fashion show

– A brand that creates celebrities

– Benefits from athleisure/loungewear trend

– Close attention to in-store experience

– Wise international expansion strategy

– 20% e-commerce penetration

– L Brands reported 8% holiday comps

Victoria’s Secret Store and Beauty Comparable

Store Sales

14% 13%

6%

4% 3%

4%

8%

Q3 2010 Q3 2011 Q3 2012 Q3 2013 Q3 2014 Q3 2015 Q4 2015

30

TOP FIVE RETAIL TECHNOLOGY TRENDS IN ASIA

1. Uberification in Asia

2. Streaming Media

3. Fast Adoption of 3D Printing

4. Inconsistent Mobile Payment Growth

5. End of One-Child Policy in China Driving Retail

31

1. Uberification in Asia

• On-demand services are available for everything from accommodation to

personal chefs in Asia

• Home Cooked is the most successful uberified service in China

• Uberified services faced legal and regulatory challenges

• Not expected to replace established industries

Service Company (Location)

Accommodation Hanintel (S. Korea), Kozaza (S. Korea)

Babysitting Caregiver Asia (Singapore)

Food and Drink Delivery Grain (Singapore), Home Cooked (China)

Home Cleaning Whome365 (China)

Home Finder AnAnZu (China)

Logistics (Pickup and Delivery) GogoVan (Hong Kong), EasyVan (Hong Kong)

Taxi Service Kuaidi ONE (China), Ola (India)

Selected Asian Startups that Provide Uber-Like Services

32

2. Streaming Media

• Netflix will expand into Hong Kong,

Singapore, South Korea and Taiwan

in early 2016

• HOOQ, a joint venture of Singtel,

Sony Pictures and Warner Bros., is

competing directly with Netflix

• Alibaba recently acquired streaming

media company Youku Tudou for

$4.4 billion

• Growth driven by the rising affluence

of consumers, growing Internet

penetration and increasing

smartphone ownership

Rank Country Minutes per

Day

2-Year

Growth Rate

1 China 67 5%

2 Vietnam 61 84%

3 Thailand 60 14%

4 UAE 54 43%

5 Hong Kong 51 16%

6 Philippines 51 74%

Time Spent Watching Online Video Top Six Countries (4Q 2014)

Source: GlobalWebIndex

33

3. Fast Adoption of 3D Printing

• The Asia-Pacific region accounted

for 27% of global 3D printer

shipments in 2014

• Key region for fast adoption due to

government support and extensive

industrial funding in important

markets

• China plans to invest $300 million in

3D printing over three years

3D Product Shipments: Market Share by Region, 2014

Source: Canalys/FBIC Global Retail & Technology

AMERICAS 42%

ASIA-PACIFIC 27%

ASIA-PACIFIC 27%

Asia-Pacific 27%

The Americas

42%

Europe, Middle East

& Africa 31%

34

4. Inconsistent Mobile Payment Growth

• China is experiencing fast adoption of mobile

payment via Alipay and WeChat Wallet

• South Korea, Japan, Hong Kong, Taiwan and

Singapore have the infrastructure, but are not yet

seeing substantial growth

• Several banks in Singapore have launched mobile

payment services and new services using NFC on

USIM cards

Mobile Payments Readiness Index: Selected Countries in Asia

Source: MasterCard

Global

Ranking COUNTRY

1 Singapore

5 South Korea

6 Japan

10 China

11 Taiwan

12 Philippines

13 Malaysia

14 Hong Kong

20 Thailand

21 India

35

5. End of One-Child Policy in China Driving Retail

• Starting in 2016, couples in

China will be allowed to have

two children without risk of fine

• Huatai Financial estimates that

the relaxation of the one-child

policy could create a $15 billion

market

• The second-child boom will

benefit several categories,

including food and dairy,

healthcare, garments,

automotive and education

• The first wave of the second-

child boom is expected in 2017

Source: MasterCard

36

THANK YOU!

[email protected] Cell: 917-655-6790 HK: 852.6119.1779

CHN: 86.186.1420.3016 @debweinswig