the future of consumer finance in the next five years

Post on 22-Oct-2014

3.033 views

DESCRIPTION

In this document we’re concentrating on the likely impact of some sizeable socio-demographic trends, technological advances and legislative changes in the near future.By near future we mean in the next five years, so we’re hardly crystal ball gazing, and while the outcome of these developments is obviously uncertain, we believe the RDR, social media, financial services, fs, consumer finance, viewpoint, pensions ace are already some interesting insights into what the future may have in store for tomorrow’s financial consumers.TRANSCRIPT

Viewpoint / August 09 p.01

1

2

3

4

5

IntroductionThe future, it’s all about the experience

The future of consumer finance

DemographicsThe baby boomers

Ethnic diversity

Increasing connectivity

LegislationRDR

The pensions Act 2008

Free money guidance

FutureWhat’s the future for financial services?

Being online or digital isn’t enough

What should financial brands do?

A final word

ViewpointAugust 09 Looking ahead to changes in consumer finance over the next five years

Viewpoint / August 09 p.02

2

5

DemographicsThe baby boomers

Ethnic diversity

Increasing connectivity

A final word

IntroductionWith all the ongoing turmoil in the world of financial services, it would be all too easy to get caught up in the headlights of the present perils and dangers and forget about what’s on the horizon.

Therefore it seemed fitting to use the future of consumer finance as a starting point for our new viewpoint.

In this edition we’re concentrating on the likely impact of some sizeable socio-demographic trends, technological advances and legislative changes in the near future.

By near future we mean in the next five years, so we’re hardly crystal ball gazing, and while the outcome of these developments is obviously

uncertain, we believe there are already some interesting insights into what the future may have in store for tomorrow’s financial consumers.

We hope you enjoy reading it. And if you’ve any thoughts of your own you’d like to add, please send them to us at [email protected] or call David McCann on 020 7360 7878.

1IntroductionThe future, it’s all about the experience

The future of consumer finance

3

4

LegislationRDR

The pensions Act 2008

Free money guidance

FutureWhat’s the future for financial services?

Being online or digital isn’t enough

What should financial brands do?

Welcome to the first Teamspirit Viewpoint

Viewpoint / August 09 p.03

Financial services in the future will need to concentrate on creating more than hard facts, big numbers and mere products.

The future, it’s all about the experience

Whether you’re HSBC or The Century Building Society, the UK’s smallest Mutual, financial institutions new and old will need to create memorable customer experiences and environments to ensure their future success.

Just relying on the commodity of a good rate of return and consumer apathy will no longer ensure a future. In short, financial services companies are going to have to develop the more-intangible aspects of their business – their brands.

They will need to create reasons to believe, have a valued purpose and promise beyond the purely functional aspects of their offer, and create a physical manifestation that embodies the more elusive qualities of what they offer.

2

5

DemographicsThe baby boomers

Ethnic diversity

Increasing connectivity

A final word

1IntroductionThe future, it’s all about the experience

The future of consumer finance

3

4

LegislationRDR

The pensions Act 2008

Free money guidance

FutureWhat’s the future for financial services?

Being online or digital isn’t enough

What should financial brands do?

Viewpoint / August 09 p.04

As marketers we all probably feel that we’ve seen enough turbulence in the past few months to last a lifetime.

The future of consumer finance

Financial services have undergone irreversible changes and it’d be nice to have some stability, wouldn’t it?

But unfortunately, while recessions and future government policies will come and go, what we’ve just experienced in the financial markets is nothing compared to the challenges that’ll continue to happen in the next few years.

For consumers, intermediaries and providers alike, the future of consumer finance is going to look a lot different from how it does now – in fact we believe that we should expect a tidal wave of change.

So what changes are we talking about?

We have identified a number of developments all colliding at the same time to create this tsunami. These include:

1. socio-demographics 2. regulation and policy 3. technology

All these developments are rushing towards banks and financial services at a time when consumers have not just lost trust but have started to question the very nature of what they once believed was true about them, namely that these institutions and

businesses were competent at managing money.

The credit crunch, the nationalisation of banks and the subsequent recession have allowed consumers to question the very core of why they choose these brands.

This array of well-defined developments and distinct trends are not only heading our way at roughly the same time, but they are interdependent and heavily overlap.

And over the next three to five years, we can expect these changes to have a profound, lasting impact upon the world of financial services.

2

5

DemographicsThe baby boomers

Ethnic diversity

Increasing connectivity

A final word

1IntroductionThe future, it’s all about the experience

The future of consumer finance

3

4

LegislationRDR

The pensions Act 2008

Free money guidance

FutureWhat’s the future for financial services?

Being online or digital isn’t enough

What should financial brands do?

Viewpoint / August 09 p.05

DemographicsDemographic change 1: the baby boomers

The biggest demographic change to affect the UK in recent years has been the growth in our ageing population. In fact the fastest-growing age group in the UK are those aged 80+ who currently constitute 4.5% (2,749,507) of the total population*.

In fact, last year saw the number of people of state pensionable age exceed the number of children in the UK for the first time.

This trend is set to continue. It’s estimated that by 2031 over one third of the total UK population will be over 55. The obvious knock-on effect of this ageing population is that future

generations can expect to have longer and longer retirements. In fact for those retiring in 2012, they’ll spend on average over 20 years in retirement.

The other thing to consider is that the generations facing retirement now, won’t be anything like the retirees of the past.

1

2

5

IntroductionThe future, it’s all about the experience

The future of consumer finance

DemographicsThe baby boomers

Ethnic diversity

Increasing connectivity

A final word

*Source: www.statistics.gov.uk/cci/nugget.asp?id=2157

3

4

LegislationRDR

The pensions Act 2008

Free money guidance

FutureWhat’s the future for financial services?

Being online or digital isn’t enough

What should financial brands do?

The demographic changes

Viewpoint / August 09 p.06

This up-and-coming retirement generation are made up of the baby boomers, the post Second World War children who’ve enjoyed a life of relative comfort and ease. They’ll demand the same from their retirement and will choose to lead a fuller, more active life after work than any previous generation.

The opportunities post-work

Start a new career?Volunteering?Go travelling?Open a business?Take gap years?70 becomes the new 50

Importantly, the over-50s account for 80% of the UK’s wealth, which is expected to rise to 84% by 2012. However, while they have the assets and the cash, in a recent poll, 63% of boomers haven’t reviewed their retirement plans as a result of the current financial crisis and are likely to suffer as a consequence.

So if you were expecting to go to the bank of mum and dad any time soon, you might be in for a shock, as they will have spent your prospective inheritance on a hedonistic haze of retirement frippery or survival.

That begs the question that no matter what this expanding post-work generation choose to do in retirement, just how is the state going to fund this populace if they can’t fund it themselves – especially when the size of the next generation is shrinking?

1

2

5

IntroductionThe future, it’s all about the experience

The future of consumer finance

DemographicsThe baby boomers

Ethnic diversity

Increasing connectivity

A final word

3

4

LegislationRDR

The pensions Act 2008

Free money guidance

FutureWhat’s the future for financial services?

Being online or digital isn’t enough

What should financial brands do?

Viewpoint / August 09 p.07

1

2

5

IntroductionThe future, it’s all about the experience

The future of consumer finance

DemographicsThe baby boomers

Ethnic diversity

Increasing connectivity

A final word

3

4

LegislationRDR

The pensions Act 2008

Free money guidance

FutureWhat’s the future for financial services?

Being online or digital isn’t enough

What should financial brands do?

Demographic change 2: ethnic diversity

To fund the cost of this growing group of pensioners expecting to lead an active and fulfilled retirement, the UK will need to attract significant numbers of migrant workers into its economy.

We’ve seen a steady influx of migrants since 1995, and this has grown to a point where skilled migrants now account for 2.75% of the country’s workforce and their spending supported £8.4bn of the UK economy in 2007. This is estimated to rise to a record £77bn by 2012.*

This influx of new migrants will not only enhance our ethnic diversity over the short and medium term, but will affect the future landscape of financial brands and products.

The increasing financial diversity, driven by distinct communities’ financial capabilities, channel preferences, and cultural attitudes towards banking, saving and investing, will in turn drive a requirement for new products, services and ultimately new competitors as their home-grown financial brands will follow these immigrant communities.

This might feel far-fetched, but we’ve already seen some changes with the development of Polish bank accounts and Shariah-compliant products. This however is just the tip of the iceberg, as over the next few years we will see an explosion of new solutions.

So whether it’s money transfer or multi-jurisdictional savings accounts, the need for ever-more products to satisfy the needs of increasingly niche

ethnic and cultural audiences over the next few years, means we’d better get used to saying a financial hello, or is that:

• Bonjour• Hola• Witaj• Hei• Здороваться• Salut

Increasing immigration and diversity

*Source: www.hrmagazine.co.uk/news/798191/Migrants-will-contribute-77-billion-UK-economy-2012/

Viewpoint / August 09 p.08

Demographic change 3: increasing connectivity – the boom in social networking

The recommendation generation are the next big group waiting in the wings that’ll have a major impact upon financial services.

Central to the rise of this generation has been the rapid growth of social networking sites and technologies.

There are an estimated 11 million active social networkers in the UK who use online message boards, social communities and blogs, for information about brands and products. That’s double what it was two years ago and, of these, 38% access their profile at least once a day!

When you couple this trend with the fact that during the next three years 68% of consumers will happily use

the internet as a retail channel, it means the likely battleground for the next generation’s £ or € is set to be fought in the aisles of social networking sites, where the power of recommendation will rule.

Age is not a barrier

Although 58% of social networkers are under 35 years of age, the baby-boomer generation aren’t excluded, with sites such as Saga Zone now bringing the older age groups into the social networking fold.

No matter what is said of this phenomenon, whether good or bad, as these networks develop to include more mobile technologies and other forms of media such as video, text and speech, you can be sure that the stories, messages and opinions they spread travel ever quicker.

With the scale and impact of the ‘Recommendation Generation’ set to increase over the next ten years, this new breed of consumer will become an increasingly lucrative target due to their financial clout, purchasing power and size.

Increasingly seeking recommendation

MySpace, founded August 2003

Facebook, founded February 2004

Bebo, founded January 2005

All these are in the top ten of the UK’s most-used websites.

1

2

5

IntroductionThe future, it’s all about the experience

The future of consumer finance

DemographicsThe baby boomers

Ethnic diversity

Increasing connectivity

A final word

3

4

LegislationRDR

The pensions Act 2008

Free money guidance

FutureWhat’s the future for financial services?

Being online or digital isn’t enough

What should financial brands do?

Viewpoint / August 09 p.09

LegislationThere are three bits of important market legislation that are about to impact the market in the next few years. These initiatives will have a profound and lasting impact upon distribution, as well as consumer attitudes and behaviours.

They are:

1. RDR2. Pensions Act 2008 3. Money guidance

Regulation, regulation, regulation

1

2

5

IntroductionThe future, it’s all about the experience

The future of consumer finance

DemographicsThe baby boomers

Ethnic diversity

Increasing connectivity

A final word

3

4

LegislationRDR

The pensions Act 2008

Free money guidance

FutureWhat’s the future for financial services?

Being online or digital isn’t enough

What should financial brands do?

Viewpoint / August 09 p.10

Legislation change 1: RDR

RDR is set to be a huge catalyst for change in how financial investment products and services can and will be sold in the future. Currently it affects just investments and their advisers, but surely it will broaden out to include a much wider range of products such as mortgages.

RDR outlines distinct types of advice and sales process that can be used with consumers, as it makes a

distinction between independent, restricted and tied advice.

RDR will no doubt lead to a fragmentation and polarisation of the market, with some brands and organisations choosing to focus on distinct audiences such as high-net-worth or specialist areas.

It is affectionately called the RD implementation programme and has an expected date of instigation of 2012.

What’s almost certain about RDR is that it will continue the well- defined exodus of advisers from financial services.

Because since the beginning of the 1990s, with each subsequent piece of regulation, there has been a decrease in the total number of advisers in the industry.

The changes in distribution

1

2

5

IntroductionThe future, it’s all about the experience

The future of consumer finance

DemographicsThe baby boomers

Ethnic diversity

Increasing connectivity

A final word

3

4

LegislationRDR

The pensions Act 2008

Free money guidance

FutureWhat’s the future for financial services?

Being online or digital isn’t enough

What should financial brands do?

Viewpoint / August 09 p.11

Legislation change 2: The Pensions Act 2008

To make sure we [UK plc] have some way of funding future retirees, the Government introduced the Pensions Act in 2008, the name for the new, Government-backed national pension plan.

This piece of legislation will introduce in 2012 the first piece of compulsory national pension saving the UK has ever seen. If you’re wondering, your current National Saving Investment contributions aren’t actually saved. The Pensions Act is putting an end to that ambiguity by setting up personal

accounts where your pension monies will accumulate over time.

While it should mean a better-funded retirement for future generations, it is also likely to create a huge swell of consumer desire for information and interest about their money, where it’s going and how it’s invested.

This likely outcome of increased interest and desire for knowledge will mean a much better form of communication than an annual black-and-white statement of funds under management. What they’ll want to know is, if they change the underlying investments, what could

be the possible outcomes? Are the BRIC economies riskier than the UK? What’s the difference between large cap and special situations? And when’s the right time to buy a pension annuity?

All of which hasn’t been planned for as yet, or if it has, it isn’t clear how this is going to be communicated, but not to worry, the government has decided that.

Compulsion won’t come from advice, the Government has decided to provide guidance.

Compulsion is on the horizon and approaching fast Increased action will lead to increased interest

1

2

5

IntroductionThe future, it’s all about the experience

The future of consumer finance

DemographicsThe baby boomers

Ethnic diversity

Increasing connectivity

A final word

3

4

LegislationRDR

The pensions Act 2008

Free money guidance

FutureWhat’s the future for financial services?

Being online or digital isn’t enough

What should financial brands do?

Viewpoint / August 09 p.12

Legislation change 3: Free money guidance

Money guidance is the free advice service that is being implemented to coincide with the launch of the national pension plan or personal accounts.

The service has been developed as a response to the earlier findings of the Thoresen Review on Generic Financial Advice.

The guidance service is expected to be a multichannel solution, including face-to-face, web and telephone support.

Importantly, once we’ve put the funding issues to one side, this service should have a major impact on increasing the levels of financial literacy and capabilities among the UK population.

The exact nature of this service and how it complements independent, restricted or basic advice isn’t yet clear, but it will ensure that everyone in the UK has access to at least basic levels of financial information and guidance.

While this service will most probably be launching in 2012 to give a flavour of the volume of interest that could develop, just look at the one million or more mobile bank account enquires during October 2008 when stock markets tumbled. It’s just not clear how the Pensions Delivery Service will cope with that volume of interest in information.

One way this increased desire for more and more financial information will play out will be the creation of big financial celebrities. This desire for

gurus and personalities will likely lead to the likes of Martin Lewis, Alvin Hall and Robert Peston being treated like Rock’ n’ Roll Legends and filling concert halls [virtually] with screaming hordes of silver-surfer fans.

Help and guidance are on the way With compulsion comes guidance and true consumer interest

The service will help people with:

•budgetingtheirweeklyormonthly spending;

• savingandborrowing,andinsuring and protecting themselves and their families;

• retirementplanning;• understandingtaxandwelfare

benefits; • jargon-busting–explainingthe

technical language we use in the financial services industry;

• importantly,moneyguidanceisalso completely sales-free.

1

2

5

IntroductionThe future, it’s all about the experience

The future of consumer finance

DemographicsThe baby boomers

Ethnic diversity

Increasing connectivity

A final word

3

4

LegislationRDR

The pensions Act 2008

Free money guidance

FutureWhat’s the future for financial services?

Being online or digital isn’t enough

What should financial brands do?

Viewpoint / August 09 p.13

FutureWith so many policies, trends, social and economic changes all converging at once, there will be plenty of interesting solutions to come.

What I believe is that no one solution will win out, in fact we’re not going from business model A to business model B, we’re going from business model A to business model A to Z.

What’s the future for financial services?

1

2

5

IntroductionThe future, it’s all about the experience

The future of consumer finance

DemographicsThe baby boomers

Ethnic diversity

Increasing connectivity

A final word

3

4

LegislationRDR

The pensions Act 2008

Free money guidance

FutureWhat’s the future for financial services?

Being online or digital isn’t enough

What should financial brands do?

I’m a child of a certain generation, so forgive me when I say ‘It’s broadband Jim, but not as we know it!’ The fact is, putting the Digital Britain Report to one side, the UK is on the cusp of introducing superfast broadband services that will offer huge swathes of the UK 50, 100 or 250 megabit per second download speeds over the next five years.

With this radical change to high-definition multiscreen and application connectivity, UK consumers will want content that’s richer, smarter and more dynamic than ever before.

Yet despite this rampant charge to the internet, they’ll still continue to crave a personal relationship with their bank or financial services provider.

What is noticeable is that although banks and financial services companies are always among the early adopters of new technology,

the industry as a whole is relatively slow at realising its true potential for building stronger and more meaningful experiences for their clients.

There are other emerging technologies that will shape consumers expectations of the type and quality of service they want from financial companies, but as a starter I have outlined a few in the following pages.

Being online or digital isn’t enough

The UK’s first home online banking service was set up by the Nottingham Building Society back in 1983!

To infinity and beyond!

Although financial services have been online for a long time and internet banking has revolutionised the way we manage our finances, today’s consumers still expect more...

Viewpoint / August 09 p.14

1

2

5

IntroductionThe future, it’s all about the experience

The future of consumer finance

DemographicsThe baby boomers

Ethnic diversity

Increasing connectivity

A final word

3

4

LegislationRDR

The pensions Act 2008

Free money guidance

FutureWhat’s the future for financial services?

Being online or digital isn’t enough

What should financial brands do?

Viewpoint / August 09 p.15

I’ve already written about connected and social customers, but the technology that’s allowing them to connect is also changing.

Google’s ‘OpenSocial’ programme is a new platform that will help build social networking or documents into the very fabric of the internet.

This will obviously give the power of recommendation a real boost, as consumers will no longer be restricted in having to go where the conversations are, but simply follow the conversations seamlessly from one network to another. Eventually this will expand to include more than just the single channel, and the written word and conversations will move from one media to another!

By the way, Google’s OpenSocial has a name: it’s called Wave and it’s here now wave.google.com And just what is a wave?

A wave is equal parts conversation and document. People can communicate and work together with richly formatted text, photos, videos, maps, and more.

A wave is shared. Any participant can reply anywhere in the message, edit the content and add participants at any point in the process. Then playback lets anyone rewind the wave to see who said what and when.

A wave is live. With live transmission as you type, participants on a wave can have faster conversations, see edits and interact with extensions in real-time.

But technology goes beyond the current view of the internet, it includes other dynamic elements and will start to seamlessly integrate in to our offline experience as well as just our online life.

Social technologies

1

2

5

IntroductionThe future, it’s all about the experience

The future of consumer finance

DemographicsThe baby boomers

Ethnic diversity

Increasing connectivity

A final word

3

4

LegislationRDR

The pensions Act 2008

Free money guidance

FutureWhat’s the future for financial services?

Being online or digital isn’t enough

What should financial brands do?

Viewpoint / August 09 p.16

Smartphones

You can’t walk down any high street in the UK without being bombarded by advertising for the latest iPhone or HTC Hero. The rise in use of PDAs and Smartphones means users are browsing on the go, and if they’re connected they can make payments at the point of sale or arrange finances remotely.

Now many believe that the size, scale and importance of mobile systems are overestimated. However, by the end of 2011 – that’s just 28 months away – mobile contactless payments will make up 10% of the contactless payment market, and that’s before Barclaycard contactless really gets off the ground.

The change towards mobile banking is already happening: Monilink, the UK mobile banking network, says it processed over one million account

enquiries in October 2008 alone as customers feeling the economic downturn, kept a watchful eye on their money.

And continuing on this theme, a recent study by financial consultancy Celent suggests 35% of online banking households will be using mobile banking by 2010 – that’s next year!

VoIP solutions

If your children are anything like mine they’ve been using VoIP protocols, like Windows Messenger, Windows Live or Skype for as long as they can remember.

These technologies combine the power of text, voice, and video in real-time. They allow for instant messaging, file transfer and video conferencing all over the same networks.

And to give you an idea of the scale of the networks, Skype currently has

more than 400 million members worldwide. This by size would make it the third most populated country in the world, bigger than the US!

The take-up and use of these technologies by financial services brands is slow, but ultimately it’s inevitable, as consumers expect financial services organisations to deliver communications using the media and technology that they’re already using.

Lots of financial marketers will say, ‘but I am digital. I’m online, look at my banners, my MPUs’. But in today’s and tomorrow’s technological world, being online isn’t enough.

What consumers expect is for you to be there, wherever there is, and connected is so integrated into future consumer behaviour it is no longer an activity in its own right.

1

2

5

IntroductionThe future, it’s all about the experience

The future of consumer finance

DemographicsThe baby boomers

Ethnic diversity

Increasing connectivity

A final word

3

4

LegislationRDR

The pensions Act 2008

Free money guidance

FutureWhat’s the future for financial services?

Being online or digital isn’t enough

What should financial brands do?

Viewpoint / August 09 p.17

The low-down on the high street

Another trend on its way in the next few years is the change in the traditional high street and the way we all shop.

Soon we won’t distinguish between internet shopping and shopping in the high street any more: there’ll just be shopping.

Shopping in the high street will evolve to include computers, touchscreens and the internet, so that consumers can know straightaway the information they want and the availability of items they need. The move will be facilitated by a network – and this network will be ubiquitous. So the use of any traditional physical retail space will be dependent solely on what it adds to the consumers’ experience and their desire for it.

What does this mean for banks?

Banks and financial services providers have already started to compare themselves with retailers rather than with other financial institutions.

And they’ll have to continue to do so, as customers are happy to buy any commodity, be it toilet tissue or personal loans, from anyone who offers a good rate or price, but more importantly offers a better and more enjoyable experience.

It’s important to remember that retailers aren’t new to this game, retailers such as Tesco have already been supplying financial products for more than a decade!

Historically, the argument has been that other retailers didn’t have the banking expertise to offer financial

products, but recent events have thrown all that into question.

And it will increasingly become market share that makes the biggest difference, as other brands start to consider the limitations of white-labelling and think about the benefits of being regulated themselves.

The key to this shift is customer emotions. Other retailers and FMCG brands have already exploited this territory, but financial services brands have found it difficult, as they’ve lacked the physical environment or experience needed to build brand empathy. But this will have to change.

1

2

5

IntroductionThe future, it’s all about the experience

The future of consumer finance

DemographicsThe baby boomers

Ethnic diversity

Increasing connectivity

A final word

3

4

LegislationRDR

The pensions Act 2008

Free money guidance

FutureWhat’s the future for financial services?

Being online or digital isn’t enough

What should financial brands do?

So just where will all this change lead us. We believe that this new future will fall neatly into the hands of a new sales advice channel that will be in part restricted and independently advised.

What’s not clear is who will be offering it: banks, supermarkets or intermediary firms, or indeed soft drinks companies.

What is clear is that in most instances the web will be used as a distinct communications and sales channel in its own right; it will seamlessly mix distinct advice and recompense models for a mix of clients based upon relationship, need and value.

What they actually look like is difficult to say. We have however started to see a number of new quasi guided sales solutions [that’s restricted sales in the new RDR world] come to market, particularly in the US. Here are some examples.

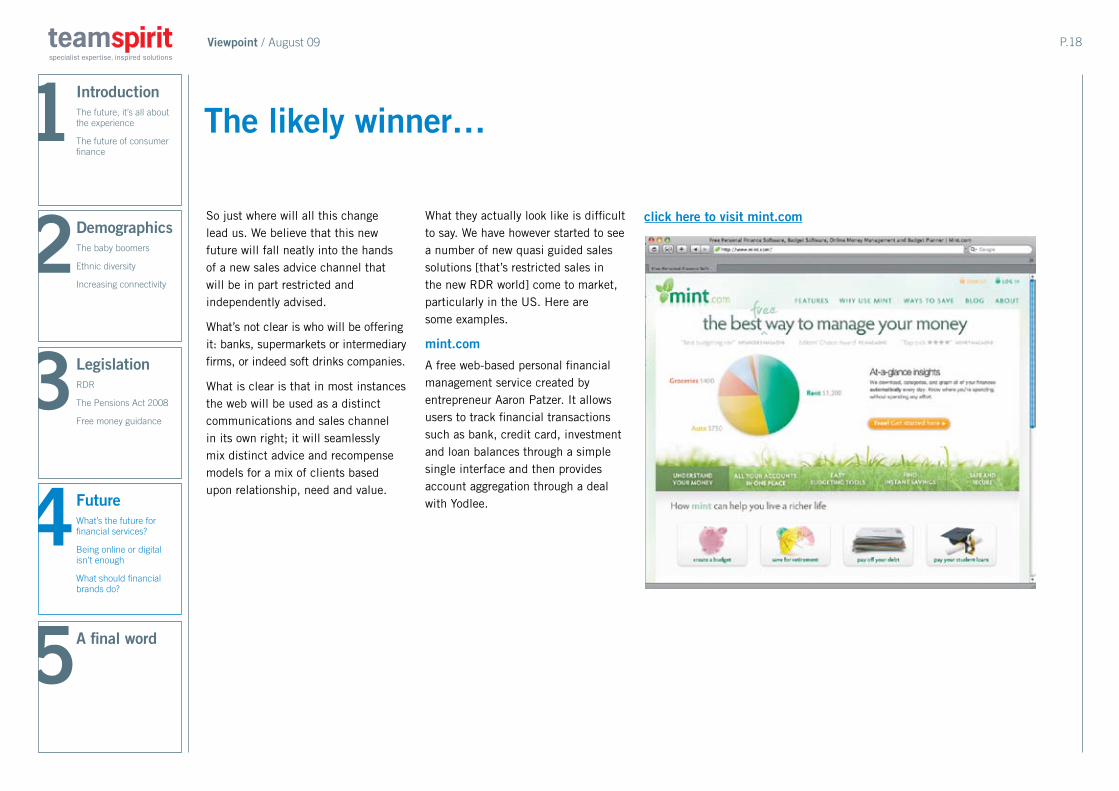

mint.com

A free web-based personal financial management service created by entrepreneur Aaron Patzer. It allows users to track financial transactions such as bank, credit card, investment and loan balances through a simple single interface and then provides account aggregation through a deal with Yodlee.

click here to visit mint.com

The likely winner…

Viewpoint / August 09 p.18

1

2

5

IntroductionThe future, it’s all about the experience

The future of consumer finance

DemographicsThe baby boomers

Ethnic diversity

Increasing connectivity

A final word

3

4

LegislationRDR

The pensions Act 2008

Free money guidance

FutureWhat’s the future for financial services?

Being online or digital isn’t enough

What should financial brands do?

Wesabe

Similar to mint in that it offers a money management tool. But it goes one step further by introducing the community element, to help consumers learn and benefit from the actions and knowledge of other members.

click here to visit Wesabe

Viewpoint / August 09 p.19

1

2

5

IntroductionThe future, it’s all about the experience

The future of consumer finance

DemographicsThe baby boomers

Ethnic diversity

Increasing connectivity

A final word

3

4

LegislationRDR

The pensions Act 2008

Free money guidance

FutureWhat’s the future for financial services?

Being online or digital isn’t enough

What should financial brands do?

lovemoney.com is the new offering from the people at Motley Fool. It has great content and savings ideas as well as product aggregation. With a little imagination you can picture it with a Skype interface, some decision trees, and all of a sudden you’ve got the starting of mass intermediation or an enriched sales advice channel.

click here to visit lovemoney.com

Viewpoint / August 09 p.20

1

2

5

IntroductionThe future, it’s all about the experience

The future of consumer finance

DemographicsThe baby boomers

Ethnic diversity

Increasing connectivity

A final word

3

4

LegislationRDR

The pensions Act 2008

Free money guidance

FutureWhat’s the future for financial services?

Being online or digital isn’t enough

What should financial brands do?

MoneySavingExpert.com

The most visited financial site in the UK, and for that reason alone it is well worth a mention.

However it doesn’t take too much hard work or imagination to see how this site could develop in the future. What about this site expanding its current core premise and becoming an all-inclusive advice environment, or the first people-based ratings agency? Yes move over S&P, the people are coming.

Viewpoint / August 09 p.21

click here to visit MoneySavingExpert.com

1

2

5

IntroductionThe future, it’s all about the experience

The future of consumer finance

DemographicsThe baby boomers

Ethnic diversity

Increasing connectivity

A final word

3

4

LegislationRDR

The pensions Act 2008

Free money guidance

FutureWhat’s the future for financial services?

Being online or digital isn’t enough

What should financial brands do?

1 Focus on being useful

Financial services brands need to think beyond their core products to ensure that they develop their brands as a utility. This will allow them to add value to customers. And it will free customers from thinking about these brands as interested only in product and profit. Think calculators, tools, context case studies and education.

2 Find a voice and connect with your audience

It’s not enough just being online. Financial brands need to have opinions and add to the conversations that consumers are having, and not sit on the sidelines. You need to demonstrate your beliefs and facilitate the debates on risk and finance. This way you’ll create a valued reason for audiences to reference and find you. Currently so many big organisations, especially financial ones, are silent in this conversation-driven world. They need to create, have a view and voice it in a relevant and interesting way that distinct communities can use.

3 Create an experience

Serious competitive advantage lies in making any customer feel better in ways which don’t just relate to actual product consumption. So by concentrating on the customer experience first, then the message and finally product, financial brands will be able to grab market share. This means a change in traditional systems: offline communications such as brochures and branches will become a means of driving traffic online and creating desire, as well as being a retail channel.

What should financial brands do?

Viewpoint / August 09 p.22

Here are three things that we believe financial services brands should start to do to ensure that they can compete for the future of financial consumers.

1

2

5

IntroductionThe future, it’s all about the experience

The future of consumer finance

DemographicsThe baby boomers

Ethnic diversity

Increasing connectivity

A final word

3

4

LegislationRDR

The pensions Act 2008

Free money guidance

FutureWhat’s the future for financial services?

Being online or digital isn’t enough

What should financial brands do?

Viewpoint / August 09 p.23

A final wordPredicting the future of the financial services industry isn’t a precise science. However there are a number of certainties that will definitely impact us all, such as the Pensions Act, RDR and the development and growth of networked consumers.

The survival of Financial services brands will depend upon their ability to adapt to changing circumstances – and to do that we need to start developing strategies now.

We hope you enjoyed reading this. And if you’ve any thoughts of your own you’d like to add, please send them to us at [email protected] or call David McCann on 020 7360 7878.

1

2

5

IntroductionThe future, it’s all about the experience

The future of consumer finance

DemographicsThe baby boomers

Ethnic diversity

Increasing connectivity

A final word

3

4

LegislationRDR

The pensions Act 2008

Free money guidance

FutureWhat’s the future for financial services?

Being online or digital isn’t enough

What should financial brands do?