the economy, interest rates and housing markets in 2005 … · 1 economics@ the economy, interest...

TRANSCRIPT

1 economics@

The economy, interest rates and The economy, interest rates and housing markets in 2005housing markets in 2005--0606

Presentation to a luncheon for Presentation to a luncheon for UDIA QueenslandUDIA Queensland

Saul EslakeSaul EslakeChief EconomistChief EconomistANZ BankANZ Bank

Brisbane ConventionBrisbane Convention& Exhibition Centre& Exhibition Centre

77thth October 2005October 2005

www.anz/com/go/economicswww.anz/com/go/economicswww.anz/com/go/economics

2 economics@

Key assumptions about the world economyKey assumptions about the world economyKey assumptions about the world economy

Expensive oil is here to stay– crude oil prices will probably stay close to US$70/barrel near

term, and will still be in the $55-65 range through 2006-07World economic growth is slowing from 5% in 2004 to around 4¼% pa in 2005 and 3¾-4% in 2006 and 2007

– higher oil prices and higher US interest rates to have some dampening impact – but much less than in previous ‘oil shocks’

– although most economies will slow a bit, note that Japan is actually picking up after more than a decade of stagnation

The Fed will continue to raise US short-term interest rates ‘at a measured pace’, reaching 4½ % by mid-2006The US$ has bottomed (for the time being) against the euro and other ‘freely floating’ currencies (including the A$)

– US now has the highest, not the 2nd lowest, interest rates among major economies

– confidence in the euro undermined by political developmentsAsian central banks will continue to resist significant revaluations of their currencies

– China’s abandonment of its US$ peg does not mean than the yuan will rise significantly against the dollar

3 economics@Sources: Datastream; OECD; Economics@ANZ.

Higher oil prices aren’t (thus far) leading to higher inflation and interest ratesHigher oil prices aren’t (thus far) leading to Higher oil prices aren’t (thus far) leading to higher inflation and interest rateshigher inflation and interest rates

Oil prices and inflation

Note: Shaded areas denote “oil price shocks”

0

10

20

30

40

50

60

70

80

90

100

70 75 80 85 90 95 00 050

2

4

6

8

10

12

14

16US$ per barrel(2005 prices)

Real oil prices

% change fromyear earlier

G7 consumer prices (right scale)0

10

20

30

40

50

60

70

80

90

100

70 75 80 85 90 95 00 050

2

4

6

8

10

12

14

16US$ per barrel(2005 prices)

Real oilprices

% per annum

G7 3-mth interest rates(right scale)

Oil prices and interest rates

4 economics@

Economic growth has been much less affected by higher oil prices than in previous ‘oil shocks’Economic growth has been much less affected Economic growth has been much less affected by higher oil prices than in previous ‘oil shocks’by higher oil prices than in previous ‘oil shocks’

Oil prices and economic growth

Note: Shaded areas denote oil price ‘shocks’.Source: Thomson Financial Datastream; OECD.

0

10

20

30

40

50

60

70

80

90

100

70 75 80 85 90 95 00 05-2

-1

0

1

2

3

4

5

6

7

8US$ per barrel(2005 prices) Real oil price

(left scale)

Real % changefrom year earlier

OECD GDP growth(right scale)

5 economics@

In the developing world, gross saving has risen much more than gross investmentIn the developing world, gross saving has risen In the developing world, gross saving has risen much more than gross investmentmuch more than gross investment

Source: Bank for International Settlements, 75th Annual Report.

21

22

23

24

25

26

1990-99

2000-02

2003 2004

% of GDP

World

12

14

16

18

20

22

1990-99

2000-02

2003 2004

% of GDP

United States

Euro area

16

18

20

22

1990-99

2000-02

2003 2004

% of GDP

22242628303234

1990-99

2000-02

2003 2004

% of GDP

Japan

Developing Asia

25

30

35

40

1990-99

2000-02

2003 2004

% of GDP

16

18

20

22

1990-99

2000-02

2003 2004

% of GDP

Latin America

Saving Investment

6 economics@

Higher saving by developing economies is allowing (forcing?) the US to run big deficitsHigher saving by developing economies is allowing Higher saving by developing economies is allowing (forcing?) the US to run big deficits(forcing?) the US to run big deficits

‘Net lending’ is gross saving minus gross investment. It is conceptually equal to the current account balance.Source: BIS; Economics@ANZ.

-8

-6

-4

-2

0

2

1990-99

2000-02

2003 2004

% of GDP

United States

Euro area World

Japan

Developing Asia

Latin America

-1

0

1

2

1990-99

2000-02

2003 2004

% of GDP

0

1

2

3

4

1990-99

2000-02

2003 2004

% of GDP

-2

-1

0

1

2

3

1990-99

2000-02

2003 2004

% of GDP

-3

-2

-1

0

1

2

1990-99

2000-02

2003 2004

% of GDP

-2

-1

0

1

1990-99

2000-02

2003 2004

% of GDP

Net lending as a % of GDP

7 economics@

0

1

2

3

4

5

03 04 05

% pa

Fed funds(cash) rate

10-year bond yield

8

10

12

14

16

18

20

79 80 81 82

% pa Fed funds (cash) rate

10-yearbond yield

Strikingly, US long-term rates have fallen even though US short rates have more than trebledStrikingly, US longStrikingly, US long--term rates have fallen even term rates have fallen even though US short rates have more than trebledthough US short rates have more than trebled

Four episodes of rising US interest rates

Note: Shaded areas show periods when the Federal Reserve has been tightening monetary policy by raising the ‘Federal funds’ (cash) rate. Sources: Datastream; Federal Reserve

6

7

8

9

10

11

88 89 90

% pa Fed funds (cash) rate

10-yearbond yield

23456789

93 94 95

% pa

Fed funds(cash) rate

10-year bond yield

Unlike Australia, in the US most personal and business borrow-ing is done at fixed rates

Thus, what happens to long-term rates is much more important

Usually, long-term rates rise while the Fed is tightening monetary policy

But in this latest episode, long-term rates have fallen

8 economics@

-15

-10

-5

0

5

10

15

20

1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000

% change from previous year

(f)

Australia is enjoying its longest run of uninter-rupted economic growth since FederationAustralia is enjoying its longest run of uninterAustralia is enjoying its longest run of uninter--rupted economic growth since Federationrupted economic growth since Federation

Australian real GDP growth, 1901 - 2006Australian real GDP growth, 1901 - 2006

Note: data are for financial years ended 30 June.Sources: Angus Maddison, Monitoring the World Economy 1820-1992; Reserve Bank; ABS; Economics@ANZ.

25 quarters of negativegrowth in this period,

including 6 episodes of2 or more consecutivequarters of –ve growth

3 qtrsof –vegrowthin thisperiod

2 qtrsof –vegrowthin thisperiod

no quarterly data before 1959

9 economics@

Capacity utilization

Sources: ABS; National Australia Bank;Economics@ANZ.

8090

100110120130140150160

00 01 02 03 04 05

'000

Job vacancies

After 15 years of continuous growth Australia’s economy is starting to run into capacity limitsAfter 15 years of continuous growth Australia’s After 15 years of continuous growth Australia’s economy is starting to run into capacity limitseconomy is starting to run into capacity limits

Labour shortages

0

5

10

15

20

25

00 01 02 03 04 05

%

Businesses reporting labour shortages as aconstraint on output

Highest in 26-year history of

this series

Edgeddownfrom15-yrhigh

Highestin the15-year history of this survey

5.0

5.5

6.0

6.5

7.0

7.5

00 01 02 03 04 05

% of the labour force

Actual

Trend

Unemployment rate

Lowest since Nov 1976

Sources: ABS; National Australia Bank;Economics@ANZ.

78

79

80

81

82

83

00 01 02 03 04 05

%

Actual (seas. adj. by ANZ)

Trend

10 economics@

Wage and price pressures are beginning to pick up although A$ strength is offsetting some of thisWage and price pressures are beginning to pick up Wage and price pressures are beginning to pick up although A$ strength is offsetting some of thisalthough A$ strength is offsetting some of this

Sources: Dept of Employment & Workplace Relations; ABS.

Wage price index

Enterprise bargaining settlements Producer prices

-15

-10

-5

0

5

10

97 98 99 00 01 02 03 04 05

% change fromyear earlier

Domesticallyproduced

Imported

Consumer prices*

-1

0

1

2

3

4

5

97 98 99 00 01 02 03 04 05

% change from year earlier

'Non-tradeables'

'Tradeables'2.0

2.5

3.0

3.5

4.0

4.5

5.0

00 01 02 03 04 05

% change from year earlier

Public sector

Private sector

2.5

3.0

3.5

4.0

4.5

5.0

00 01 02 03 04 05

Average % increase,all current agreements

Private sector

Public sector

11 economics@

The economy is near the point in the cycle where the seeds of previous recessions have been sownThe economy is near the point in the cycle where The economy is near the point in the cycle where the seeds of previous recessions have been sownthe seeds of previous recessions have been sown

Allowing wages to grow faster than justified by productivity in a tight labour market

– much less of a risk now that centralized wage fixation is (almost) dead

Failing to allow the Reserve Bank to raise interest rates before inflation has begun to accelerate

– not a serious risk now that the RBA is ‘independent’

‘Giving away too much’ of the revenue dividend in spending increases and tax cuts

– still a significant risk (as demonstrated in 2004)

In some important respects the Australian economy is at a similar stage to where it was in 1960, 1973, 1981 and 1989 – just before each of the past 4 recessions

Three policy mistakes have traditionally been made at this stage of the business cycle -

12 economics@

Australian governments are rolling in cash thanks to sustained strong growthAustralian governments are rolling in cash thanks Australian governments are rolling in cash thanks to sustained strong growthto sustained strong growth

Tax revenue as a pc of GDP

Sources: ABS; Australian Government Budget Papers.

Budget balances

20

22

24

26

28

30

32

34

70 75 80 85 90 95 00 05

% of GDP

-8

-6

-4

-2

0

2

4

70 75 80 85 90 95 00 05

% of GDP (fiscal years ended 30 June)

Federal government

Consolidated'generalgovernment'

13 economics@

In 2004 Federal outlays grew 10¾% in real terms – the fastest in over 20 years In 2004 Federal outlays grew 10¾% in real In 2004 Federal outlays grew 10¾% in real terms terms –– the fastest in over 20 years the fastest in over 20 years

* ie, excluding payments to State & local governments.Source: ABS, quarterly national accounts; Economics@ANZ.

Government outlays (excl. defence and interest)

-5

0

5

10

15

20

74 77 80 83 86 89 92 95 98 01 04

Federal own-purpose*

State & local

Real % change from previous year

14 economics@Sources: ABS; Reserve Bank; Economics@ANZ.

Capital city house prices

Household saving rate

-5

0

5

10

15

20

97 98 99 00 01 02 03 04 05

% change fromyear earlier

Household net worth

4.5

5.0

5.5

6.0

6.5

7.0

97 98 99 00 01 02 03 04 05

Multiple of annual householddisposable income

Household debt

-4

-2

0

2

4

6

8

97 98 99 00 01 02 03 04 05

% of householddisposable income

Actual

Trend

Australia’s property boom has ended with a sigh, not a bang: but its passing will dampen spendingAustralia’s property boom has ended with a sigh, Australia’s property boom has ended with a sigh, not a bang: but its passing will dampen spendingnot a bang: but its passing will dampen spending

5

10

15

20

25

97 98 99 00 01 02 03 04 05

% change from year earlierMortgage

Other

15 economics@

-4

-2

0

2

4

6

8

00 01 02 03 04 05 06 07

% pt contrbn to annual change in GDP

Domesticspending

Net exports

0

1

2

3

4

5

00 01 02 03 04 05 06 07

% ch. from year earlierAvge of last 10 yrs

4

5

6

7

8

00 01 02 03 04 05 06 07

% ch. from year earlier

-8-7-6-5-4-3-2-10

00 01 02 03 04 05 06 07

% of GDP

Australia’s economy will grow more slowly over the next few years than over the past decade Australia’s economy will grow more slowly over Australia’s economy will grow more slowly over the next few years than over the past decade the next few years than over the past decade

Sources: ABS; Economics@ANZ.

Real GDP growth

Drivers of GDP growth

Unemployment rate

Current account balance

16 economics@

4.0

4.5

5.0

5.5

6.0

6.5

01 02 03 04 05 06 07

% pa

90-day bill yield

Cash rate

Short-term interest rates

Australian cash rate is ‘on hold’ for the rest of 2005 but the next move will likely be upAustralian cash rate is ‘on hold’ for the rest of Australian cash rate is ‘on hold’ for the rest of 2005 but the next move will likely be up2005 but the next move will likely be up

The RBA’s August Monetary Policy Statement dropped the previous mild tightening bias (‘it would be surprising if rates did not move higher before the current expansion ends’) …… and indicated that it saw the probabilities of the next change in rates being up or down as being equalIt’s hard to see anything which would cause the RBA to alter its ‘no change’ view on rates over the rest of 2005 …… although on our forecasts its easier to see changes which would cause the next move in rates to be up (in particular, labour costs and the A$) than downSources: Datastream; Economics@ANZ.

17 economics@

Somewhat unusually, fixed rates are now significantly lower than variable ratesSomewhat unusually, fixed rates are now Somewhat unusually, fixed rates are now significantly lower than variable ratessignificantly lower than variable rates

Sources: RBA; Economics@ANZ.

2

3

4

5

6

7

8

9

00 01 02 03 04 05 06

% pa

Standard variablemortgage rate

3yr fixed mortgage rate

3-year swap yieldsand fixed-rate mortgages

2

3

4

5

6

7

8

00 01 02 03 04 05

% pa

US

Australia

3 year fixed mortgage rate

Fixed and floatingmortgage rates

18 economics@

Housing activity has been remarkably little affected by the rises in rates since late 2003Housing activity has been remarkably little Housing activity has been remarkably little affected by the rises in rates since late 2003affected by the rises in rates since late 2003

Housing finance commitments*

- owner occupiers

4

5

6

7

8

9

00 01 02 03 04 05

$ bn per monthTrend

Actual

60

80

100

120

140

160

00 01 02 03 04 05

'000s (annual rate)

Trend

Actual

Residential building approvals- private houses

* Excl. re-financing. Sources: ABS; Economics@ANZ.

2

3

4

5

6

7

8

00 01 02 03 04 05

$ bn per month

Trend

Actual

Investors

20

40

60

80

100

00 01 02 03 04 05

'000s (annual rate)

Trend

Actual

Units

19 economics@

There’s no real evidence of an ‘over-supply’ of housing, at least not in aggregateThere’s no real evidence of an ‘overThere’s no real evidence of an ‘over--supply’ of supply’ of housing, at least not in aggregatehousing, at least not in aggregate

Rental vacancy rates*

2

3

3

4

4

5

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05

% (moving annual median)

Residential rents *

125

150

175

200

225

250

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05

$ per week 3br houses

2br apartments

Rental yields *

2

3

4

5

6

7

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05

% pa (moving annual median)

3br houses

2br apartments

Apartment construction

10

20

30

40

50

60

70

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05

'000s Under construction

Completions(annual rate)

* Weighted average of all 8 capital cities.Source: Real Estate Institute of Australia; ABS.

20 economics@

-20

0

20

40

60

80

94 95 96 97 98 99 00 01 02 03 04 05 06 070

20

40

60

80

100

120

140

160

180

200'000 units'000 units

Underlying requirements(right scale)

Completions(right scale)

Surplus

"Short-age"(left

scale)

"Surplus"(left scale)

National housing market balance

Housing supply and demand fundamentals remain reasonably soundHousing supply and demand fundamentals Housing supply and demand fundamentals remain reasonably soundremain reasonably sound

Note: ‘Surplus’ or ‘shortage’ is the cumulative difference between completions and underlying demand from an historical starting point. The direction of movements in this measure is more significant than the level. Sources: ABS; Economics@ANZ.

Underlying demand for housing is running at around 165K units pa, driven by strong immigration and declining average household size

Approvals and completions are running below this level, at around 150K per annum

So the market remains in an ‘underlying shortage’ position

In the absence of sharp rises in interest rates, we expect 160K starts in 2005-06, followed by 180K in 2006-07

21 economics@

-30

-20

-10

0

10

20

30

40

94 95 96 97 98 99 00 01 02 03 04 05 06 070

5

10

15

20

25

30

35

40

45

50'000 units'000 units

Underlyingrequirements(right scale)

Completions(right scale)

"Surplus"(left scale)

"Shortage"(left scale)

Queensland housing market balance

Queensland housing market fundamentals also point to continued growth in housing activityQueensland housing market fundamentals also Queensland housing market fundamentals also point to continued growth in housing activitypoint to continued growth in housing activity

Note: ‘Surplus’ or ‘shortage’ is the cumulative difference between completions and underlying demand from an historical starting point. The direction of movements in this measure is more significant than the level. Sources: ABS; Economics@ANZ.

Migration to Queensland

0

200

400

600

800

96 97 98 99 00 01 02 03 04 05

No per week (4-qtrmoving average)

From overseas

From interstate

Queensland population

0.0

0.5

1.0

1.5

2.0

2.5

3.0

96 97 98 99 00 01 02 03 04 05

% change fromyear earlier

Queensland

Rest of Australia

22 economics@

However the supply of housing has barely kept However the supply of housing has barely kept pace with the increase in underlying demandpace with the increase in underlying demand

Number of households and number of dwellings

Note: Dwelling stock estimates for 1991, 1996 and 2001 based on census figures; other years interpolated using completions data. Sources: RBA; ABS; Economics@ANZ.

Over the twelve years to 2003-04, the number of households rose by 1.42 million or 23%

– faster than the increase in population (15%) because of falling average household size

Over the same period, the stock of housing increased by 1.60 million or 25%

– 1.78 mn new dwellings were completed during this period, but around 180,000 old dwellings were demolished

In effect, around 89% of the increase in the supply of housing was absorbed by increased demand

5.5

6.0

6.5

7.0

7.5

8.0

8.5

92 93 94 95 96 97 98 99 00 01 02 03 04

Number of dwellings

Number of households

Mn

23 economics@

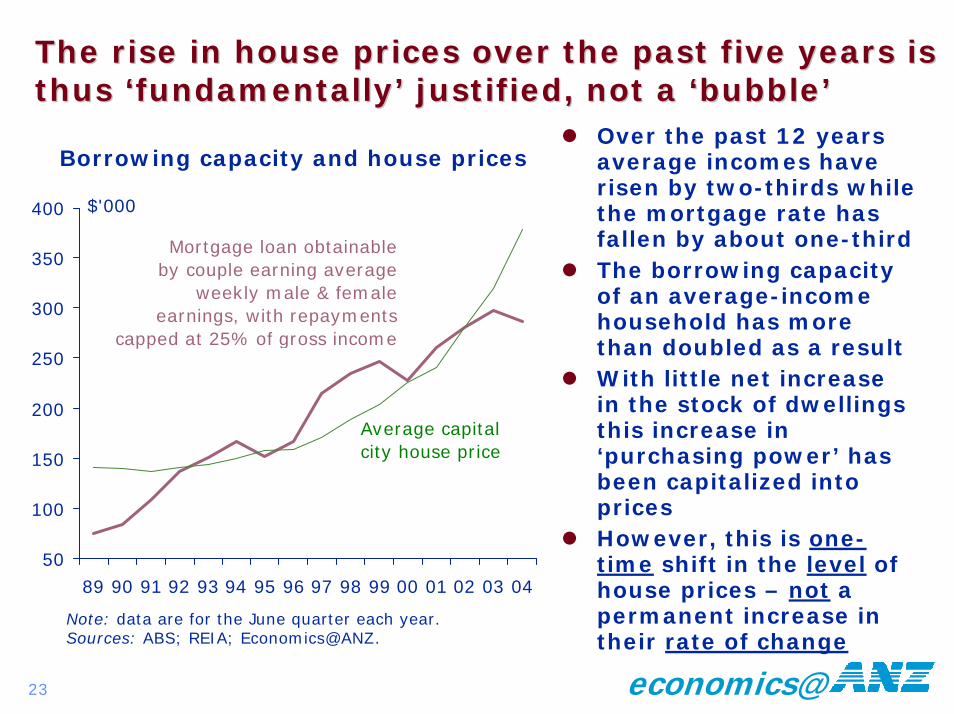

The rise in house prices over the past five years is The rise in house prices over the past five years is thus ‘fundamentally’ justified, not a ‘bubble’thus ‘fundamentally’ justified, not a ‘bubble’

Note: data are for the June quarter each year.Sources: ABS; REIA; Economics@ANZ.

Borrowing capacity and house prices

50

100

150

200

250

300

350

400

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04

$'000

Mortgage loan obtainableby couple earning average

weekly male & femaleearnings, with repayments

capped at 25% of gross income

Average capitalcity house price

Over the past 12 years average incomes have risen by two-thirds while the mortgage rate has fallen by about one-thirdThe borrowing capacity of an average-income household has more than doubled as a resultWith little net increase in the stock of dwellings this increase in ‘purchasing power’ has been capitalized into pricesHowever, this is one-time shift in the level of house prices – not a permanent increase in their rate of change

24 economics@

Australia’s tax system has played a key role in encouraging investment in rental propertyAustralia’s tax system has played a key role in Australia’s tax system has played a key role in encouraging investment in rental propertyencouraging investment in rental property

Note: Data are for fiscal years ended 30 June.Sources: Australian Taxation Office; Economics@ANZ .

Taxpayers with rental income

9

10

11

12

13

14

94 95 96 97 98 99 00 01 02 03

% of total no. of personaltaxpayers

Interest paid by property investors

3

4

5

6

7

8

94 95 96 97 98 99 00 01 02 03

$bn

Net rental income

-1.5

-1.0

-0.5

0.0

0.5

1.0

94 95 96 97 98 99 00 01 02 03

$bn

50525456586062

94 95 96 97 98 99 00 01 02 03

% of total

Loss-making property investors

25 economics@

House prices in major East Coast cities have peaked while smaller cities still catching upHouse prices in major East Coast cities have House prices in major East Coast cities have peaked while smaller cities still catching uppeaked while smaller cities still catching up

Sources: ABS; Economics@ANZ.

Capital city house prices

100

150

200

250

300

350

97 98 99 00 01 02 03 04 05

1989-90=100

Sydney

Melbourne

Brisbane

100

150

200

250

300

350

97 98 99 00 01 02 03 04 05

1989-90=100

Adelaide

Perth

Hobart

26 economics@

-20

-10

0

10

20

30

40

Sydney Melbourne Brisbane Adelaide Perth Hobart

June qtr 2005 June qtr 2004

% change

Brisbane house prices are now more ‘over-valued’ than in any other capital cityBrisbane house prices are now more ‘overBrisbane house prices are now more ‘over--valued’ valued’ than in any other capital citythan in any other capital city

Capital city house prices – deviation from ‘fair value’*

*‘Fair value’ based on interest rates and average disposable incomes. Source: ABS; Economics@ANZ.

27 economics@

SummarySummarySummaryWorld economy will continue to show reasonable growth at least until 2008

– despite higher oil prices and rising US interest rates– ‘excess savings’ in Asia and elsewhere are helping to keep long-

term rates down and finance otherwise ‘unsustainable’ current account imbalances

Nearly 15 years out from the last recession, Australia’s economy is beginning to encounter capacity constraints

– whenever the economy has previously been at this stage of the cycle, policy mistakes have led to recession within two years

– it’s dangerous to say, but ‘this time it should be different’Interest rates are ‘on hold’ for the remainder of this year, butwill probably rise again in 2006

– unusually, fixed rates are lower than variable rates, presentingan opportunity to ‘lock in’

There’s unlikely to be a significant downturn in housing activity– 160K housing starts nationally in 05-06, rising to 180K in 06-07– Queensland starts 41K in 05-06, rising to 48K in 06-07

Residential property prices have peaked in most capital cities– Brisbane prices look more ‘over-valued’ than anywhere else