the determinant factors of profitability on sharia …

TRANSCRIPT

THE DETERMINANT FACTORS OF

PROFITABILITY ON SHARIA RURAL

BANKS IN INDONESIA

By

Devita Rahma Aryati

014201500150

A Skripsi presented to the

Faculty of Business President University

in partial fulfillment of the requirements for

Bachelor Degree in Management

January 2019

i

ii

iii

iv

PLAGIARISM DOCUMENT

v

vi

ACKNOWLEDGMENT

First of all, the researcher would like to deliver the highest gratitude to God

for His guidance and blessings so that this study can be done. Researcher also

would like to give the best appreciation and is thankful towards everyone who

always supports and helped me during the completion of this research.

1. Researcher’s adviser, Mr. Purwanto, ST., M.M. for his continuous

support, constructive feedbacks, and thorough guidance during the

research process.

2. Researcher’s beloved family: Mama (Supriyati), Ayah (Ajo Rianto),

brother (Hilmy Imtiyaz) and little sister (Rana Arista Mahardika) for their

caring, prays, and encouragement in every single step that researcher

takes.

3. Researcher’s dearest friends: Deviani Halim, Regina Angeline,

Maylananda and Raisa for the warm embrace and irreplaceable support

from classes’ era until we, together reach skirpsi moment.

4. Researcher’s beloved classmates and PUSU family, for the moral support

and togetherness along the college journey.

5. Researcher’s respectable lecturers and teachers, for their guidance,

knowledge shared, and continuous support and feedback.

To those who I cannot mention one by one, and who indirectly contribute in

this research, your help and kindness do matter for the researcher. Thank you

very much.

Cikarang, January 8, 2018

Devita Rahma Aryati

vii

CONSENT FOR

INTELLECTUAL PROPERTY RIGHT

Title of Skripsi: The Determinants Factors of Profitability on Sharia Rural Banks

in Indonesia

1. The Author hereby assigns to President University the copyright to the

Contribution named above whereby the President University shall have the

exclusive right to publish the Contribution and translations of it wholly or in

part throughout the world during the full term of copyright including

renewals and extensions and all subsidiary rights

2. The Author retains the right to re-publish the preprint version of the

Contribution without charge and subject only to notifying the University of

the intent to do so and to ensuring that the publication by the University is

properly credited and that the relevant copyright notice is repeated verbatim.

3. The Author retains moral and all proprietary rights other than copyright,

such as patent and trademark rights to any process or procedure described in

the Contribution.

4. The Author guarantees that the Contribution is original, has not been

published previously, is not under consideration for publication elsewhere

and that any necessary permission to quote or reproduce illustrations from

another source has been obtained (a copy of any such permission should be

sent with this form).

5. The Author guarantees that the Contribution contains no violation of any

existing copyright or other third-party right or material of an obscene,

indecent, libelous or otherwise unlawful nature and will indemnify the

University against all claims arising from any breach of this warranty.

6. The Author declares that any named person as co-author of the Contribution

is aware of this agreement and has also agreed to the above warranties.

viii

ix

TABLE OF CONTENTS

PANEL OF EXAMINERS .............................................................................. i

DECLARATION OF ORIGINALITY ......................................................... ii

PLAGIARISM DOCUMENT ....................................................................... iv

ACKNOWLEDGMENT ............................................................................... vi

CONSENT FOR INTELLECTUAL PROPERTY RIGHT ...................... vii

TABLE OF CONTENTS .............................................................................. ixi

LIST OF TABLES ....................................................................................... xiii

LIST OF FIGURES ..................................................................................... xiii

LIST OF ACRONYMS .............................................................................. xivi

ABSTRACT .................................................................................................. xiv

CHAPTER I INTRODUCTION .................................................................. xv

1.1 Background of the Study ............................................................................. 1

1.2 Problem Identification ................................................................................. 5

1.3 Statement of Problems ................................................................................ 6

1.4 Research Objectives .................................................................................... 6

1.5 Significance of the Study ............................................................................ 7

1.6 Scope and Limitations of the Study ............................................................ 8

1.7 Thesis Organization .................................................................................... 8

CHAPTER II LITERATURE REVIEW .................................................... 10

2.1 Sharia Bank ............................................................................................... 10

2.1.1 Sharia Rural Bank ......................................................................... 11

2.2 Macroeconomics ....................................................................................... 11

2.2.1 Gross Domestic Product ................................................................ 12

2.2.2 Inflation ......................................................................................... 13

2.3 Financial Performance .............................................................................. 14

2.3.1 Capital Adequacy Ratio ................................................................ 14

2.3.2 Financing to Deposit Ratio............................................................ 16

2.3.3 Non Performing Financing ............................................................ 17

x

2.3.4 Operational Efficiency Ratio......................................................... 17

2.4 Profitability ............................................................................................... 18

2.5 Previous Research ..................................................................................... 20

2.6 Research Gap ............................................................................................ 26

2.7 Theoretical Framework ............................................................................. 27

2.8 Hypothesis ................................................................................................. 28

CHAPTER III METHODOLOGY ............................................................. 29

3.1 Research Method ....................................................................................... 29

3.2 Research Framework ................................................................................. 29

3.3 Sampling Design ....................................................................................... 30

3.3.1 Size of Population ......................................................................... 30

3.3.2 Size of Sample............................................................................... 30

3.4 Research Instrument .................................................................................. 31

3.5 Data Collection Method ............................................................................ 32

3.6 Operational Definitions ............................................................................. 33

3.7 Data Analysis Method ............................................................................... 35

3.7.1 Descriptive Statistics Analysis ...................................................... 35

3.7.2 Classical Assumption Test ............................................................ 36

3.8 Multiple Regression Analysis ................................................................... 38

3.9 Hypothesis Testing .................................................................................... 39

3.9.1 Partial Test (t-Test) ....................................................................... 40

3.9.2 Simultaneously Test (f-Test) ......................................................... 42

3.9.3 Coefficient Determination (Adjusted R2) ..................................... 43

CHAPTER IV ................................................................................................ 45

ANALYSIS OF DATA AND INTERPRETATION OF RESULTS ......... 45

4.1 Company Profile ....................................................................................... 45

4.2 Descriptive Statistics Analysis .................................................................. 46

4.3 Data Analysis ............................................................................................ 48

4.3.1 Classical Assumption Test ............................................................ 48

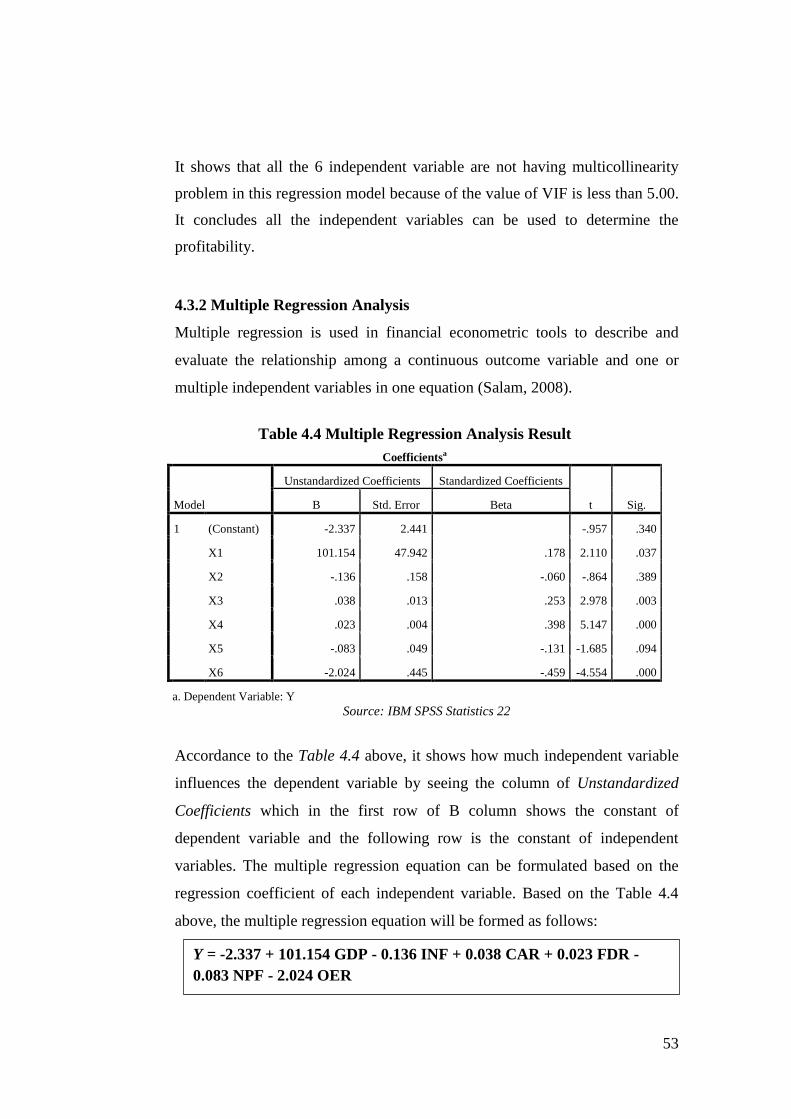

4.3.2 Multiple Regression Analysis ....................................................... 53

4.4 Hypothesis Testing .................................................................................... 55

xi

4.4.1 Partial Test (t-Test) ....................................................................... 55

4.4.2 Simultaneously Test (f-Test) ......................................................... 57

4.4.3 Coefficient of Determination ........................................................ 58

4.5 Interpretation of Results ............................................................................ 58

CHAPTER V CONCLUSIONS AND RECOMMENDATIONS ............. 64

5.1 Conclusions ............................................................................................... 64

5.2 Recommendations ..................................................................................... 66

REFERENCES .............................................................................................. 67

APPENDICES ............................................................................................... 74

Appendix 1. Raw Data for Sharia Rural Banks Performance Determinants .. 74

xii

LIST OF TABLES

Table 1.1 Financial Ratios of Sharia Rural Bank .............................................. 4

Table 2.1 Previous Researches ........................................................................ 20

Table 3.1 Sample Proportion .......................................................................... 31

Table 3.2 Operational Definitions ................................................................... 33

Table 4.1 Descriptive Statistics Result............................................................ 47

Table 4.2 Durbin-Watson Test Result ............................................................. 52

Table 4.3 Multicollinearity Test Result .......................................................... 52

Table 4.4 Multiple Regression Analysis Result .............................................. 53

Table 4.5 F-Test Result ................................................................................... 57

Table 4.6 Coefficient Determination of Result ............................................... 58

xiii

LIST OF FIGURES

Figure 1.1 Market Shares of Islamic Banks in Indonesia ................................. 2

Figure 1.2 Top 10 Countries in Islamic Banking Assets .................................. 3

Figure 2.1 Theoretical Framework .................................................................. 27

Figure 3.1 Research Framework ..................................................................... 29

Figure 4.1 Histogram ...................................................................................... 49

Figure 4.2 Normal P-P Plot ............................................................................. 50

Figure 4.3 Scatterplot ...................................................................................... 51

xiv

LIST OF ACRONYMS

BPRS : Bank Perkreditan Rakyat Syariah (Sharia rural bank)

BUS : Bank Umum Syariah (Sharia commercial bank)

UUS : Unit Usaha Syariah (Sharia business unit)

IFSB : Islamic Financial Service Board

GDP : Gross Domestic Product

INF : Inflation

CAR : Capital Adequacy Ratio

FDR : Financing to Deposit Ratio

NPF : Non-Performance Financing

CAR : Capital Adequacy Ratio

OER : Operational Efficiency Ratio

BPS : Badan Pusat Statistik (Central Statistics Agency)

OJK : Otoritas Jasa Keuangan (Financial Service Authority)

CPI : Consumer Price Index

PBI : Peraturan Bank Indonesia (Bank Indonesia Regulation)

DPK : Dana Pihak Ketiga (Third Party Fund)

PPAP : Penyisihan Penghapusan Aktiva Produktif (Provision for Loan

Losses)

xv

ABSTRACT

This research aimed to empirically examine the determinants of profitability

of Sharia rural banks in Indonesia with quarterly period of time from 2014Q1

to 2018Q3. This research uses cross-sectional data of quarterly financial report

and macroeconomic variables in Indonesia. The study is processed and

analyzed quantitatively by using multiple regression. This research is using 8

Sharia rural banks in Indonesia with the total of 152 data used. The research

reveals that inflation and NPF have no significant influence towards

profitability of Sharia rural banks in Indonesia. While, the other four variables,

GDP, CAR, FDR and OER are significantly influence the profitability of

Sharia rural banks in Indonesia as much as 31.6%. In terms of variables, GDP,

CAR and FDR are positively significant influence the profitability, while OER

has negatively significant influence the profitability of Sharia rural banks in

Indonesia.

Keywords: GDP, Inflation, CAR, FDR, NPF, OER, Profitability, Sharia Rural

Bank

1

CHAPTER I

INTRODUCTION

1.1 Background of the Study

Banking is considered as the important and influential sectors for the economy

of the country. In Indonesia, it started in 1983 when Bank Indonesia gave

freedom to banks by set up interest rates. Indonesian banks in carrying out

their functions are based on economic democracy and use the precautionary

principle. Bank is determined as the business entity which collecting funds in

the form of deposits and channel them in the form of credit and / or other

forms with the aim to develop the living standard of the community (Otoritas

Jasa Keuangan, 2018).

In the year of 1990s, The Indonesian Ulema Council (MUI) established a

working team with aim to form Islamic Banks in Indonesia. As the result of it,

PT. Bank Muamalat Indonesia was established as the first Islamic bank in

Indonesia on November 1, 1991 accordance to its establishment certificate and

officially operated with an initial capital IDR 106,126,382,000 on May 1,

1992 (Laucereno, 2018). When the economic and monetary crisis occurred in

1997-1998, financial institutions such as banks experienced a difficult period

due to high interest rates due to high inflation. During the economic crisis

Islamic banks were not affected and still showed relatively better performance

because Islamic banks did not refer to interest rates but profit sharing.

Accordance to Bambang Brodjonegoro, former of Finance Minister of

Indonesia, there are several studies that say that Islamic banks have a stronger

resistance to dealing with crises than conventional banks because Islamic

banks tend to play “safe”. In every transaction in Islamic finance must be

based on underlying assets, unlike the conventional banks that tend to be

speculative (detikfinance, 2015).

2

Islamic finance in Indonesia has developed more than two decades since the

operation of Bank Muamalat Indonesia, as the first Islamic bank in Indonesia.

Even in global markets, Indonesia is among the top ten countries that have the

largest Islamic financial index in the world. Accordance to the study by

Rahman (2015) which The Test of Crisis Resilience to Islamic Banking in

Indonesia with the Index Banking Crisis (IBC) for the period of 2006 to 2012

shows that Islamic finance system could give contributions toward the

monetary condition of the country, which Islamic banks in Indonesia does not

significantly influenced by the global crisis happened in 2006 to 2012.

Figure 1.1 Market Shares of Islamic Banks in Indonesia Source: Snapshot Perbankan Syariah Indonesia per June 2018

However, the growth of Islamic finance has not been able to keep up with

conventional financial growth. This can be seen from the Islamic financial

market share which is still 5.70% per June 2018 with 0.14% is from Sharia

rural bank which is the lowest compared to Sharia commercial banks and

Sharia business unit (Otoritas Jasa Keuangan, 2018).

Sharia Rural Bank; 0,14% Sharia

Business Unit;

1,78% Sharia

Commercial Bank,

3.77%

3

Figure 1.2 Top 10 Countries in Islamic Banking Assets Source: Thomson Reuters Islamic Finance Development Report, 2017

Moreover, by looking at the assets, Indonesia has the lowest Islamic banking

assets compared to the top 10 countries in Islamic banking asset with only

USD 26,220 Million. It is quite contrast to the fact that Indonesia has the most

Muslim population in the world, which has more than 87% of the population

or 222 million are Muslim (Muslim Pro, 2018).

Islamic bank is carrying out its business activities which align with Sharia

principles. According with its type, it divided into three types of bank which

are Sharia commercial bank, Sharia business unit and Sharia rural banks. In

Indonesia as per July 2018, there are 13 Sharia commercial banks, 21 Sharia

business units and 168 Sharia rural banks are operating. Meanwhile, Sharia

rural banks have always decreases ROA in almost every year yet increasing its

NPF at in almost every year (Otoritas Jasa Keuangan, 2017).

4

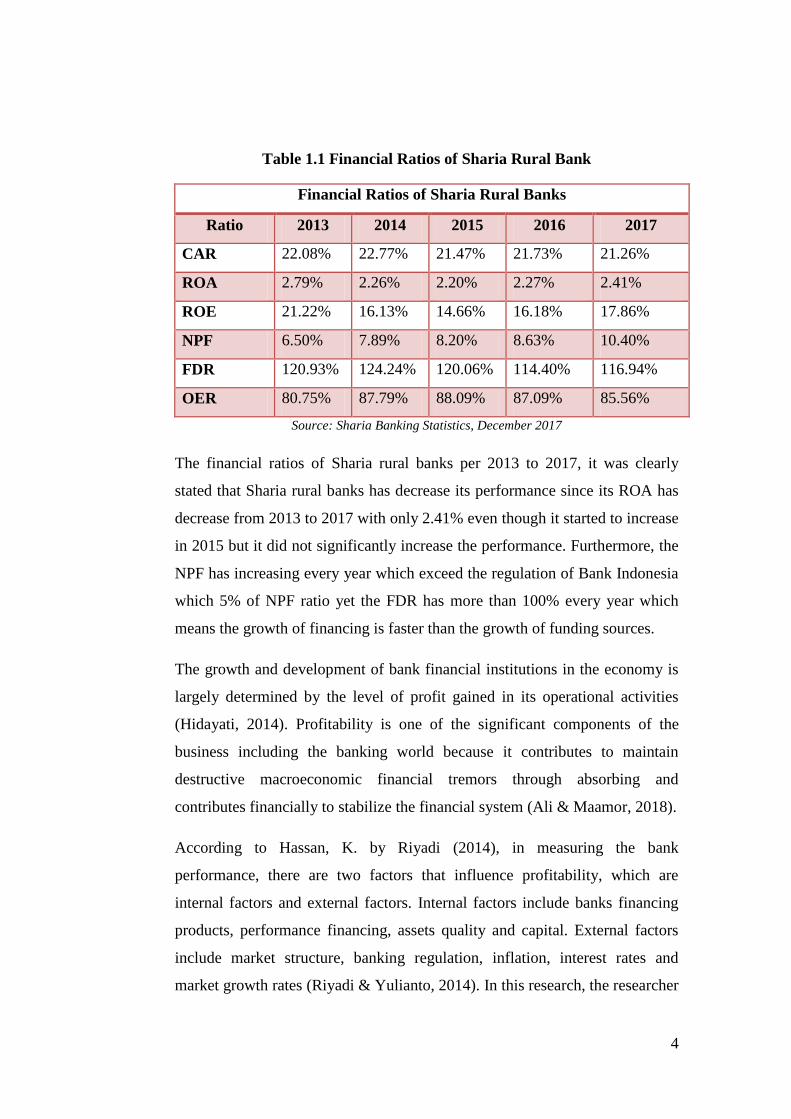

Table 1.1 Financial Ratios of Sharia Rural Bank

Financial Ratios of Sharia Rural Banks

Ratio 2013 2014 2015 2016 2017

CAR 22.08% 22.77% 21.47% 21.73% 21.26%

ROA 2.79% 2.26% 2.20% 2.27% 2.41%

ROE 21.22% 16.13% 14.66% 16.18% 17.86%

NPF 6.50% 7.89% 8.20% 8.63% 10.40%

FDR 120.93% 124.24% 120.06% 114.40% 116.94%

OER 80.75% 87.79% 88.09% 87.09% 85.56%

Source: Sharia Banking Statistics, December 2017

The financial ratios of Sharia rural banks per 2013 to 2017, it was clearly

stated that Sharia rural banks has decrease its performance since its ROA has

decrease from 2013 to 2017 with only 2.41% even though it started to increase

in 2015 but it did not significantly increase the performance. Furthermore, the

NPF has increasing every year which exceed the regulation of Bank Indonesia

which 5% of NPF ratio yet the FDR has more than 100% every year which

means the growth of financing is faster than the growth of funding sources.

The growth and development of bank financial institutions in the economy is

largely determined by the level of profit gained in its operational activities

(Hidayati, 2014). Profitability is one of the significant components of the

business including the banking world because it contributes to maintain

destructive macroeconomic financial tremors through absorbing and

contributes financially to stabilize the financial system (Ali & Maamor, 2018).

According to Hassan, K. by Riyadi (2014), in measuring the bank

performance, there are two factors that influence profitability, which are

internal factors and external factors. Internal factors include banks financing

products, performance financing, assets quality and capital. External factors

include market structure, banking regulation, inflation, interest rates and

market growth rates (Riyadi & Yulianto, 2014). In this research, the researcher

5

use both external factors and internal factors to analyze its influence toward

the profitability of Sharia rural bank in Indonesia.

The researcher uses 2 (two) external factors which are Gross Domestic

Product and inflation. While for internal factors, the researcher uses CAR,

FDR, NPF and OER. Those factors are the measures that are used to analyze

whether these external factors and internal factors have any impact over the

profitability which will be examined by ROA of Sharia rural banks in

Indonesia.

1.2 Problem Identification

The Islamic financial industry globally shows quite rapid development. Based

on data from the IFSB Financial Stability Report 2016, the assets of the world

Islamic financial industry have grown from around USD150 billion in the

1990s to around USD 2 trillion at the end of 2015 and are predicted to reach

USD 6.5 trillion in 2020. In Indonesia, the existence of Islamic banks has 20

years old and has given its own color to Indonesian financial industry. On the

other hand, despite the development of Islamic banks the fact shows Islamic

financial market share still moves in the range of 5% (Otoritas Jasa

Keuangan, 2017).

According to Islamic Banking Statistics by Financial Service Authority (OJK),

Sharia rural banks has the lowest market share compared with Sharia

commercial banks and Sharia business units which only 2,53% of the total

Islamic banking market share. Moreover, the financial ratio of Sharia rural

banks in Indonesia did not show the good condition for the past 5 years started

from 2013 to 2017, to be specified for the ROA as a common measurement of

bank’s financial performance which mostly shows the decreasing every year.

6

1.3 Statement of Problems

Accordance with the previous explanation, this study will emphasize on the

variables that affect profitability of Sharia rural banks in Indonesia. The

researcher has modified research questions which will be analyzed in this

research, as follows:

1. Is there any significant partial influences of:

a. GDP towards profitability of Sharia rural banks in Indonesia?

b. Inflation towards profitability of Sharia rural banks in Indonesia?

c. CAR towards profitability of Sharia rural banks in Indonesia?

d. FDR towards profitability of Sharia rural banks in Indonesia?

e. NPF towards profitability of Sharia rural banks in Indonesia?

f. OER towards profitability of Sharia rural banks in Indonesia?

2. Is there any simultaneous significance influence of GDP, inflation, CAR,

FDR, NPF and OER towards profitability of Sharia rural banks in

Indonesia?

3. Which variable that has the most significant influence towards

profitability of Sharia rural banks in Indonesia?

1.4 Research Objectives

As it has been explained in problem identification, the objectives of this

research by concentrate to Sharia rural banks in Indonesia, as follows:

1. To find out whether there is significant partial influence of:

a. GDP towards profitability of Sharia rural banks in Indonesia.

b. Inflation towards profitability of Sharia rural banks in Indonesia.

c. CAR towards profitability of Sharia rural banks in Indonesia.

d. FDR towards profitability of Sharia rural banks in Indonesia.

e. NPF towards profitability of Sharia rural banks in Indonesia.

f. OER towards profitability of Sharia rural banks in Indonesia.

2. To find out whether there any simultaneous significant influence of

External factors (GDP and inflation) and Internal Factors (CAR, FDR,

7

NPF, OER) towards profitability and its impact to Sharia rural bank in

Indonesia.

3. To find out the variable that has the most significant influence towards

profitability of Sharia rural banks in Indonesia.

1.5 Significance of the Study

Banking holds crucial role in the country since it influences the economics

conditions which affects to every aspect in the country. Indonesia which has

the most Muslim population in the world also conducts the business based on

Sharia principal. On the other hand, the growth of banks with Sharia principal

is way left behind than the conventional one. Therefore through this study, the

researcher aims to support and develop insight of how influential external and

internal variables in relation to banks profitability. This purpose is addressed

for:

1. Sharia banking industry

The results of the study are expected to give input for Sharia banking

Industry to be specified for Sharia rural bank in Indonesia in order to

increase the profitability of the bank that could help the bank to develop.

2. Academic community

This research expected to complement existing Sharia rural bank

profitability evaluation and to deepen knowledge of students and

academicians regarding Sharia rural banks.

3. The next researcher

The results of the study are expected to give reference and knowledge

regarding profitability of Sharia rural banks influenced by external factors

and internal factors of the economic for further analyst.

8

4. The researcher

This research is arranged to expand as well as to obtain comprehensive

knowledges of the application of several factors in measuring banks

profitability and being a prerequisite to accomplish Bachelor Degree in

Business in President University.

1.6 Scope and Limitations of the Study

1. Scope

This research is aim to determine the influence of GDP, inflation, CAR,

FDR, NPF and OER towards banks profitability which represented by

ROA. The study is intended for Sharia rural banking sector in Indonesia,

which are listed in Bank Indonesia and OJK during observation period

consisted of 168 Sharia rural banks in Indonesia as per September 2018.

2. Limitation

This research have only focused on Sharia rural banks in Indonesia which

have total assets >100 Billion IDR. In addition, the data limitation of this

research from 2014Q1 – 2018Q3 by using quarterly basis from the

financial report of every Sharia rural banks which list in Bank Indonesia

and OJK.

1.7 Thesis Organization

In order to obtain a systematic arrangement and discussion, this research is

arranged in the following systematics which divided into 5 different parts such

as:

CHAPTER I INTRODUCTION

In this section, it contains the background of the study, the formulated

problem, purpose of research, usefulness of research, limitation of research

and systematics writing.

9

CHAPTER II LITERATURE REVIEW

Chapter II contains theoretical foundations on matters relating to research and

research models. As well as some previous research that will support this

research in developing hypotheses.

CHAPTER III METHODOLOGY

This section contains the variables research and definitions operational

variables, population and samples, types and sources of data, data collection

methods, and analytical methods.

CHAPTER IV ANALYSIS OF DATA AND INTERPRETATION OF

RESULT

Chapter IV contains the results of data processing and analysis of the results

processing of such data. The researcher will collect and arrange the data in

Microsoft Excel to be run in IBM SPSS Statistics 22. The data will be

processed by SPSS 22 by using descriptive analysis, classical assumption test,

multiple regression analysis and hypothesis testing. In addition, the relevant

theories and literature must be included to support the research.

CHAPTER V CONCLUSIONS AND RECOMMENDATIONS

This section contains the summary of analysis result in accordance to the

research objectives. Also, the researcher will provide the recommendation for

the related parties.

10

CHAPTER II

LITERATURE REVIEW

2.1 Sharia Bank

Economic development activities cannot be separated from the banking sector,

because banks have an important role in the growth of economic stability

within every country. Bank one of the financial institutions, have functions as

a financial intermediary of two parties, namely those who are over-funded and

those who lack funds (Otoritas Jasa Keuangan, 2017). Based on basic

principle in conducting its business activities, banking industry divided into

two types; which are conventional bank and Sharia bank. Both conventional

and Sharia banks are having the same function which as a financial

intermediary between who are over-funded and who lack of funds but have

different principle in processing the fund. In this study, we focus on Sharia

rural banks that are exist in Indonesia.

Banks are entities which collecting funds in the form of financing or in other

words carry out the financial intermediary function. As stipulated in Law No.

10 of 1998, banks have the function of collecting and channeling public funds,

as well as banking objectives to support national development. In the banking

system in Indonesia there are two types of banking operational system, which

are conventional banks and Islamic banks (Sharia banks).

In accordance to Sharia Banking Law No. 21 of 2008, Sharia bank is bank that

runs business according with the Sharia principles, or the principle of Islamic

law that is regulated in the fatwa of the Indonesian Ulema Council (MUI) such

as the justice and equality principles ('adl wa tawazun), benefits (maslahah),

universalism (alamiyah), and does not contain gharar, maysir, riba (usury),

zalim (cruel) and obscene (objects). In conducting its businesses, Sharia

banking should follow the Sharia Principles, economic democracy also

prudential principles. Sharia banking has objective to support the

11

implementation of national development with aims to improve justice,

togetherness and equality of people's welfare.

Based on its activities Sharia banks are differentiated into BUS, UUS, and

BPRS. BUS has the same institutional form with conventional commercial

banks, while Sharia rural banks have the same institutional form with

conventional rural banks. The legal entity of Sharia commercial banks and

Sharia rural Banks can be in the form of a limited liability company, regional

company, or cooperative. Meanwhile, Sharia business unit is not a separate

legal entity, but is a unit or part of a conventional commercial bank.

2.1.1 Sharia Rural Bank

Sharia rural bank is carrying out their business activities based on Sharia

policies which in its activities are not providing the services in payment

traffic. The legal form could be as limited liability company, cooperative or

regional company (Article 2 PBI No. 6/17 / PBI / 2004). Accordance with the

Law No. 21 of 2008 stated that sharia rural bank is a bank with Sharia system

which its activities do not provide services in traffic payment.

Sharia rural banks’ business activities essentially are similar to the activities of

the Sharia commercial banks, namely in the form of fund raising, distribution

of funds, and activities in the service sector. What distinguishes it is that

Sharia rural banks is not permitted to provide services in payment traffic, for

example participating in clearing activities, collection, and curbing demand

deposits.

2.2 Macroeconomics

Macroeconomics is the economy as a whole which has involve to the overall

economic performance of the nation such as production growth, unemploye

number, price increase by the inflationary, deficits of government, exports and

imports level (OpenStax College, 2014). Additionally, according to

(Andolfatto, 2008), there are 9 (nine) indicators of macroeconomic such as

GDP, output and employment, unemployment, uncertainty and expectations,

12

consumption and saving, capital and investment, money and inflation, fiscal

policy, and growth and development. This study focuses on two

macroeconomics indicators to be analyzed which GDP and Inflation.

2.2.1 Gross Domestic Product

Gross Domestic Product is one of the important indicators to determine the

economic growth in a country in a given period, both at current prices and at

constant prices (Badan Pusat Statistik, 2016). Basically, GDP is the amount of

added value generated by all business units in a particular country in a certain

period. The value of goods used should be equal to the total value of the final

goods and services provided from the production. GDP is considered as one of

the most significant macroeconomic variables to represent profitability (Ali &

Maamor, 2018).

To determine GDP, it can be generated by summing up all domestic and

foreign effective demand for national goods. Things that considered as

domestic demands are government, household, and firm expenditure (public

expenditure, consumption, and investment) while exports are when foreign

customers buy national good. Additionally, the GDP sum could be decrease

since imports also attracts the domestic demand (Kira, 2013).

According to (Garin, et al., 2018) GDP can be calculated by using expenditure

approach which based on expenditures incurred in given period with the

formula as follows:

(Eq. 1)

With:

C = sum of consumption

I = Investment

G = Government Expenditure

X = Net Export or export

IM = Imports

GDPt = Ct + It + Gt + (Xt − IMt)

13

2.2.2 Inflation

Inflation is one of the serious matters in the economics of a country or even

globally. Accordance to the study by Amadeo in 2012, inflation is when the

price’s condition of most goods and services continue increasing and it may

cause the decreasing of the standard of living cost as the effect of spending a

lot of money to get the same amount of goods and/or services we bought

previous time (Islam et al., 2017). The impact of inflation is not only on

corporate’s pricing but also has influence on bank customers and financial

resources significantly (Ali & Maamor, 2018).

Inflation happens because of several causes which are where number of

demand increases faster than number of supply thus it affects to the cost of

goods and services. The imbalance of number of supply and number of

demand are lead to the inflation and causes of deficits of government, interest

rate expansion by banks and the increase of foreign demand (Semuel &

Nurina, 2015).

According to Bank Indonesia, Consumer Price Index is the indicator that is

common to be used to measure the inflation. Changes in CPI over the time

will indicate the movements in price of goods package and services consumed.

In the CPI basket, to determine the goods and services are carried out on the

basis of the cost of living survey carried out by the BPS. Then, BPS will

monitor the growth of price and services in a monthly basis within several

cities, in traditional also modern markets for several types of goods or services

within every city (Bank Indonesia, 2018).

In accordance to (Tennant, 2009), the change in CPI from preceding year is

considered as inflation. It can be formulated with:

Inflationyear 2 = CPI2 – CPI1 X 100%

CPI1

(Eq.2)

14

2.3 Financial Performance

Financial performance is the barometer of the operation of the company.

Financial performance can be used as the measurement of financial health of

the company (Matar & Eneizan, 2018). To assess the financial performance, it

can be done by analyzing the financial statement of the company to determine

its stability, viability and profitability (Sultan, 2014). This study focuses on 5

(five) information which provided in financial statement such as ROA, CAR,

FDR, NPF and OER.

2.3.1 Capital Adequacy Ratio

Capital is a very important factor for the development and progress of the

bank while maintaining public trust. Every fund comes, has potential to

generate profits also has the potential to cause risk. Therefore capital must also

be used to maintain the possibility of risk of loss of assets and investments in

assets, especially those originating from third party funds or the public. When

banks do their operations, capital is one of important factors for the

development of the business and overcome the risk of loss.

CAR is the capital to risk-weighted assets ratio. This ratio shows how far all

risk-bearing assets come from being financed from the own capital fund of

banks. It also to incur source of funds from outside the bank such as public

funds, loans, etc. (Rahim, 2014). Accordance to Rahim, CAR is the ratio to

measure the bank’s capital adequacy of in order to support risk-bearing assets.

Ideally by Edy Setiady as Head of Sharia banking department of OJK, Sharia

rural banks should have CAR for more than 14%. If the CAR is low, the

maximum FDR of banks should be in 99% while if the CAR is 20%, is not

consider as a problem if FDR number is more than 100% (Agustiyani, 2014).

In accordance with Bank Indonesia, capital adequacy ratio is showing how far

all risk-bearing bank assets (credit, participation, and bill securities in other

banks) are also financed from capital funds of bank. Additionally, it has aim to

15

obtain source of funds from outside the bank, such as funds from public, loans

(debt), etc. In other words, capital adequacy ratio is the banks’ ratio to

measure its performance in order to support the assets that contain or produce

risks, for example the loans given.

Capital adequacy ratio can be defined as an important parameter for judging

the strength and soundness of the bank (Fatima, 2014). Based on Circular

Letter from Bank Indonesia with the issuance of the regulation of Bank

Indonesia No. 8/18/PBI/2006 dated 5 October 2006 concerning obligation to

provide minimum capital of rural credit banks (Official Gazette of the

Republic of Indonesia No. 75 of 2006, Supplement to the Official Gazette of

the Republic of Indonesia No. 4644) hereinafter referred to as PBI, it is

necessary to stipulate implementing provisions concerning the minimum

capital requirement for rural credit banks.

Which according to Article 2 (two) of regulation of Bank Indonesia, rural banks

required to provide capital minimum of 8% (eight percent) from Risk Weighted

Assets (ATMR). By having minimum 8% of CAR it will lead to: (a) Maintain

public’s trust in bank, (b) Protecting third party funds of the bank concerned, (c)

To fulfill standardize of BIS (Bank for International Settlement) (Rahim,

2014).

To calculate the CAR in accordance with Basel II is using core capital and

supplementary capital and both should be added together then divided by risk

weighted assets (RWA) (El-Ansary & Hafez, 2015) which is used in

regulation of Indonesian Financial Ministry Number 140/PMK.010/2009

about Coaching and Supervision Indonesian Export Financing Agency related

with capital adequacy ratio, formulated with:

CAR =

Capital x 100%

Risk-Weighted

Assets

(Eq. 3)

16

Based on the regulation of Indonesian Financial Ministry, the capital used for

calculating the capital adequacy ratio divided into 3 tiers which consists of

core capital as 1st tier, supplementary capital as 2

nd tier and additional

supplementary capital as 3rd

tier.

2.3.2 Financing to Deposit Ratio

In accordance with Bank Indonesia, FDR is the ratio between financing

provided with total third party funds. Financing to deposit ratio is a ratio used

to determine the bank’s liquidity in repaying funds withdrawals made by

depositors by relying on financing provided as a source of liquidity, which is

by dividing the amount of financing provided by banks to third party funds

(DPK) (Wahyu, 2016). The higher the FDR, the higher the funds channeled to

DPK. By channeling third party funds, the bank's income is large which

examined by the increasing of ROA, so FDR is positively influencing the

ROA.

According to the study of Mohammed in (Amelia, 2015), FDR is released for

financing Islamic banks to determine the third party funds. FDR is also can be

used to measure the liquidity of the banks (Wahyu, 2016). In addition, to

determine the bank performance in term of financing, the bank can use FDR

as a tool (Nahar & Prawoto, 2017).

Based on Regulation of Bank Indonesia Number 6/23/DPNP/2004, the amount

of FDR to achieve the profit target, the bank should maintain its FDR in

between 85% to 100% (Sriyana, 2015). In other words, FDR shows the

capability of bank in paying bank the third party funds. In accordance to

(Firmansyah, 2014) in which also used by Bank Indonesia, the ratio between

total financing and total third party funds can be determined as FDR of the

bank.

FDR = Total Financing

x 100%

Total third party fund

(Eq. 4)

17

2.3.3 Non Performing Financing

Financing as main activity of Sharia banks because it is the main source of

income for Sharia banks come from this activity. Non-Performing Financing

is one of the risks since the greater the amount of funding compared to the

third party fund in a bank bring consequences of the greater the risk must be

borne by the banks (Solihatun, 2014). In other words, NPF used as the

measurement level of financing problems in Islamic banks (Amelia, 2015).

Non-Performing Financing is the ratio to determine risk in financing of banks

(Nahar & Prawoto, 2017). Non-Performing Financing shows the inability of

the customer to return the loan in the specific period of time. The higher NPF

indicates the bad performance of banks in term of financing while the lower

NPF indicates the good performance of banks in term of financing since the

bank guarantees the lower credit risk.

In accordance with (Lemiyana & Litriani, 2016) which also used in regulation

of OJK No. 15/POJK.03/2017, the maximum limit of NPF is more than 5% of

total credit or total financing. According to Nahar & Prawoto (2017) also

based on the regulation of Bank Indonesia, NPF is the ratio can be calculated

between non-performing financing and total financing, with the formula as

follows:

NPF =

Non-Performing Financing

(Substandard, doubtful and loss) x100%

Total Financing

(Eq. 5)

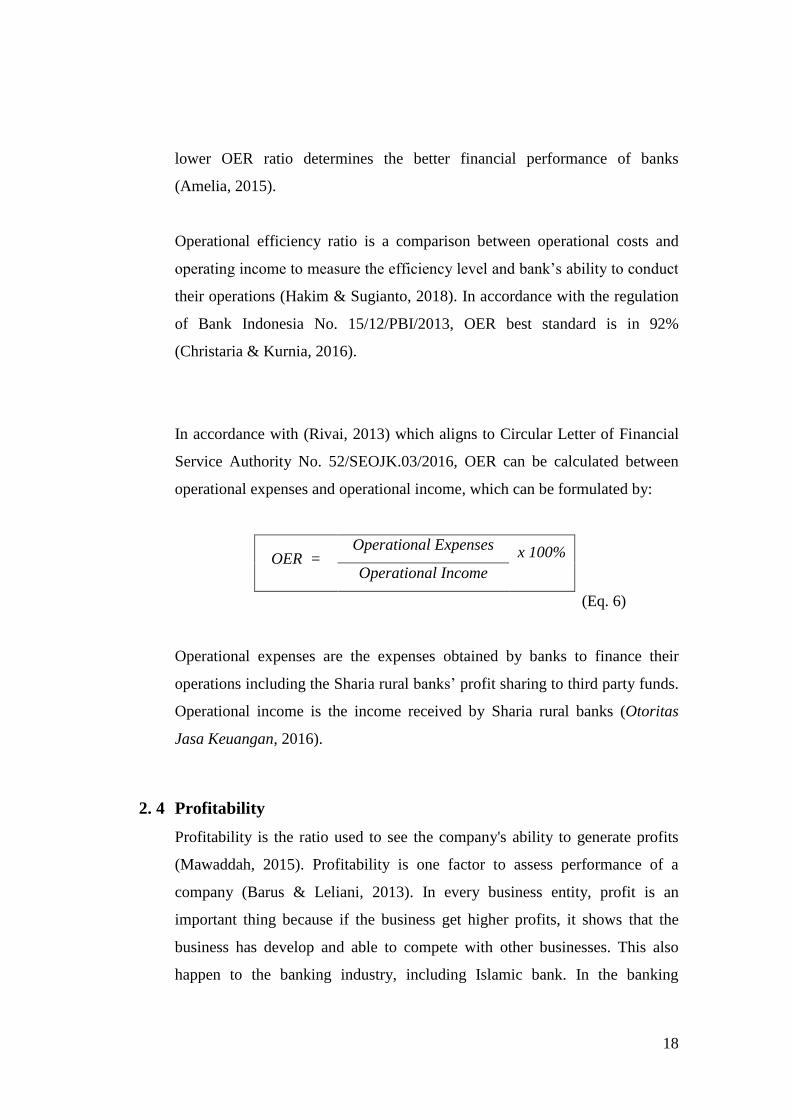

2.3.4 Operational Efficiency Ratio

OER determines the bank’s efficiency in carrying out its operations (Yogianta,

2013). Bank’s efficient determined by the amount of OER, thus the higher

OER, the greater inefficient operating cost of the bank. On the other hand, the

18

lower OER ratio determines the better financial performance of banks

(Amelia, 2015).

Operational efficiency ratio is a comparison between operational costs and

operating income to measure the efficiency level and bank’s ability to conduct

their operations (Hakim & Sugianto, 2018). In accordance with the regulation

of Bank Indonesia No. 15/12/PBI/2013, OER best standard is in 92%

(Christaria & Kurnia, 2016).

In accordance with (Rivai, 2013) which aligns to Circular Letter of Financial

Service Authority No. 52/SEOJK.03/2016, OER can be calculated between

operational expenses and operational income, which can be formulated by:

OER = Operational Expenses

x 100%

Operational Income

(Eq. 6)

Operational expenses are the expenses obtained by banks to finance their

operations including the Sharia rural banks’ profit sharing to third party funds.

Operational income is the income received by Sharia rural banks (Otoritas

Jasa Keuangan, 2016).

2. 4 Profitability

Profitability is the ratio used to see the company's ability to generate profits

(Mawaddah, 2015). Profitability is one factor to assess performance of a

company (Barus & Leliani, 2013). In every business entity, profit is an

important thing because if the business get higher profits, it shows that the

business has develop and able to compete with other businesses. This also

happen to the banking industry, including Islamic bank. In the banking

19

industry, to indicate the performance of the bank’s profitability can be

determined by calculating the return on assets and return on equity which the

ratio that indicates the ability of the entire existing assets and both are used to

generate the bank’s profit (Hosen & Rahmawati, 2016).

Profitability is defined as a condition produces financial gain or profit through

exchange of potential risks (Ali & Maamor, 2018). Profitability is considered

as a significant component in the banking industry since the profitability

contributes to sustain destructive macroeconomics financial tremors and it

contributes financially to stabilize the financial system of the country. The

level of profitability of the bank is influenced by several factors both internal

and external. Some of these factors are bank characteristics, macro indicators,

taxation, financial structure, asset quality, capital and liquidity (Anto &

Wibowo, 2012).

According to Bank Indonesia, to measures the profitability of banks in

Indonesia based on 2 (two) indicators which are return on assets and

operational efficiency ratio (Mawaddah, 2015). The greater the bank’s return

on assets, the greater the profit level achieved by the bank. It concludes that

the bank has better the position in terms of asset use. The return on assets was

developed by DuPont which used by many firms to evaluate how effectively

assets of the firms are used. In accordance with DuPont analysis, it combined

effect of profit margins and assets turnover (Groppelli & Nikbakht, 2000).

Profitability as one of the references in measuring the magnitude is so

important to know whether the company has run its business efficiently. The

efficiency of a new business can be known after comparing the profit obtained

with the capital or assets that generate the profit.

20

2.5 Previous Research

Table 2.1 Previous Researches

No Researcher/Year/Title Variables Research Design

1 Paulin and Wiryono

(2015)

Determinants of

Islamic Bank’s

Profitability in

Indonesia for 2009-

2013

Independent:

a. NPF

b. OER

c. NIM

d. FDR

e. PPAP Compliance

f. NPA

g. EA

h. LIQD

Dependent: ROA

a. Population: 11 Islamic

commercial banks in

Indonesia

b. Sample: 8 Islamic banks in

Indonesia

c. Data analysis: multiple linear

regression

d. Result: NPF, FDR, NPA, EA,

and LIQD does not partially

influence ROA, the rest of

variables are vice versa.

2 Ali, Maamor, Yaacob,

and Gill (2018)

Impact of

Macroeconomic

Variables on Islamic

Banks Profitability

Independent:

a. GDP

b. Interest Rate

c. Inflation

d. Exchange Rate

e. Oil Prices

f. Competition

g. Money Supply

Dependent:

Profitability

a. Population: Islamic Banks of

Brunei Darussalam

b. Sample: DEPD, AMBD and

IMF annual reports

c. Data analysis: Panel data

analysis

d. Result: GDP growth rate,

inflation, exchange rate, oil

prices and money supply have

positive significant impact on

profitability. While, oil

prices, GDP and inflation

were the most significant and

exchange rate and money

supply were the least

significant determinants of

profitability.

3 Nahar and Prawoto

(2017)

Bank’s Profitability in

Indonesia: Case study

of Islamic Banks

Independent:

a. Inflation

b. GDP

c. CAR

d. FDR

a. Population: Islamic Banks in

Indonesia

b. Sample: 3 Islamic

commercial banks

c. Data analysis: Panel data

d. Result: All the independent

21

period 2008-2012 e. NPF

f. OER

Dependent: ROA

variables are significantly

influence the dependent

variables. In terms of the

significance, inflation, GDP

and NPF are positively

significant, CAR, FDR and

OER, vice versa.

4 Aslam, Inamullah

and Ismail (2016)

Determinants Affecting

the Profitability of

Islamic Banks:

Evidence from

Pakistan

Independent:

a. Size

b. Deposits

c. Financing

d. GDP

e. Inflation

f. Market share

Dependent:

a. ROA

b. ROE

a. Population: Islamic banks in

Pakistan

b. Sample: 5 full-fledged

Islamic banks and 17 Islamic

banking branches of

conventional banks

c. Data analysis: panel data

d. Result: the determinants of

both ROA and ROE are not

same. But the factors used in

this article have the same

impact over ROA and ROE.

Size, deposits, financing,

market shares, GDP and

Inflation are insignificantly

affect ROA and ROE. Size,

financing and market share

positively impact ROA and

ROE whereas Deposits, GDP

and Inflation negatively

impact over ROA and ROE.

5 Ashraful and

Chowdhury (2015)

Which is more

important in terms of

Profitability of Islamic

Banks: Bank Specific

factors or

Macroeconomic

factors? An Empirical

Study on Malaysian

Independent:

a. Asset quality ratio

b. CAR

c. Overheard ratio

d. Liquidity Risk

e. GDP growth rate

f. Inflation

g. Money Supply

h. Savings on GNI

a. Population: Islamic banks in

Malaysia

b. Sample: 11 Islamic banks in

Malaysia

c. Data analysis: The pooled

ordinary least square

d. Result: Overhead costs and

GNI are negatively influence

the bank’s profitability, while

equity financing and inflation

are positively influence the

22

Islamic Banks

Dependent:

Profitability

bank’s performance. On the

other hand, the Credit risks

and Liquidity risks factors are

insignificant towards bank’s

profitability.

6 Amzal (2016)

The Impact of

Macroeconomic

Variables on Indonesia

Islamic Banks

Profitability

Independent:

a. GDP

b. Inflation rate

c. BI rate

d. NPF

Dependent:

Profitability

a. Population: Islamic banks in

Indonesia

b. Sample: Indonesian banking

sectors during the period

2016Q1 – 2014Q4

c. Data analysis: Time series

d. Result: All independent

variables are significantly

influence the profitability.

7 Asadullah (2017)

Banks Determinants of

Profitability of Islamic

Banks of Pakistan – A

case Study on

Pakistan’s Islamic

Banking Sector

Independent:

a. GDP

b. Size

c. Inflation

d. Liquidity

e. Exchange rate

Dependent:

Profitability

a. Population: Islamic banks in

Pakistan

b. Sample: Five Islamic banks

over a period of ten years, i.e.

2006-2015 in Pakistan

c. Data analysis: Panel

regression

d. Result: Liquidity has positive

whereas size has negative

effect on bank’s profitability.

On the other hand, there are

three variables have no

influence toward profitability.

8 Amelia (2015)

Financial Ratio and Its

Influence to

Profitability in Islamic

Banks

Independent:

a. CAR

b. NPF

c. FDR

d. OER

Dependent: ROA

a. Population: Islamic banks in

Indonesia

b. Sample: 2 Islamic banks

2005-2012 quarterly

c. Data analysis: Multiple

regression analysis

d. Result: CAR, NPF, and FDR

partially no significant effect

to ROA, while OER partially

significant effect to ROA.

23

9 Sutrisno (2016)

Risk, Efficiency and

Performance of Islamic

Banking: Empirical

Study on Islamic Bank

in Indonesia

Independent:

a. FDR

b. RR

c. CAR

d. NPF

e. OEOI (OER)

Dependent:

a. ROA

b. NPM

a. Population: Islamic bank in

Indonesia

b. Sample: 8 Islamic banks in

Indonesia using quarterly data

c. Data analysis: Multiple

regression analysis

d. Result: It found that FDR,

CAR. OEOI and size are

significantly influence the

performance the performance

of Islamic banks while the

other two variables, RR and

NPF insignificant in affecting

the performance of the banks.

10 Ullah (2016)

Influencing Factors of

Profitability on the

Banking Industry: A

case study of GCC

countries.

Independent:

a. Total Assets

b. EA

c. NLA

d. Growth

e. Inflation

Dependent:

a. ROA

b. ROE

a. Population: Islamic banks in

GCC region

b. Sample: 26 Islamic Banks

and 46 conventional banks

c. Data analysis: least square

d. Result: All internal factors

significantly influence the

bank’s profitability. On the

other hand, external factors

insignificantly influence the

profitability.

11 Chokri and Anis

(2018)

Measuring the

Financial Performance

of Islamic Banks in

Selected Countries

Independent:

a. CTA

b. PTA

c. ASITA

d. ALCC

e. FGTA

f. Inflation rate

g. Growth rate

Dependent: ROA

a. Population: Islamic banks

b. Sample: 10 Islamic banks in

10 selected countries over the

period of 2012 - 2014

c. Data analysis: multiple

regression

d. Result: It found that CTA,

PTA, ALCC and growth rate

are positively influence the

bank’s performance contrary

to ASITA, FGTA and

inflation rate which influence

negatively the bank’s

performance. On the other

24

hand, growth rate and

inflation are not significantly

influence the bank’s

performance.

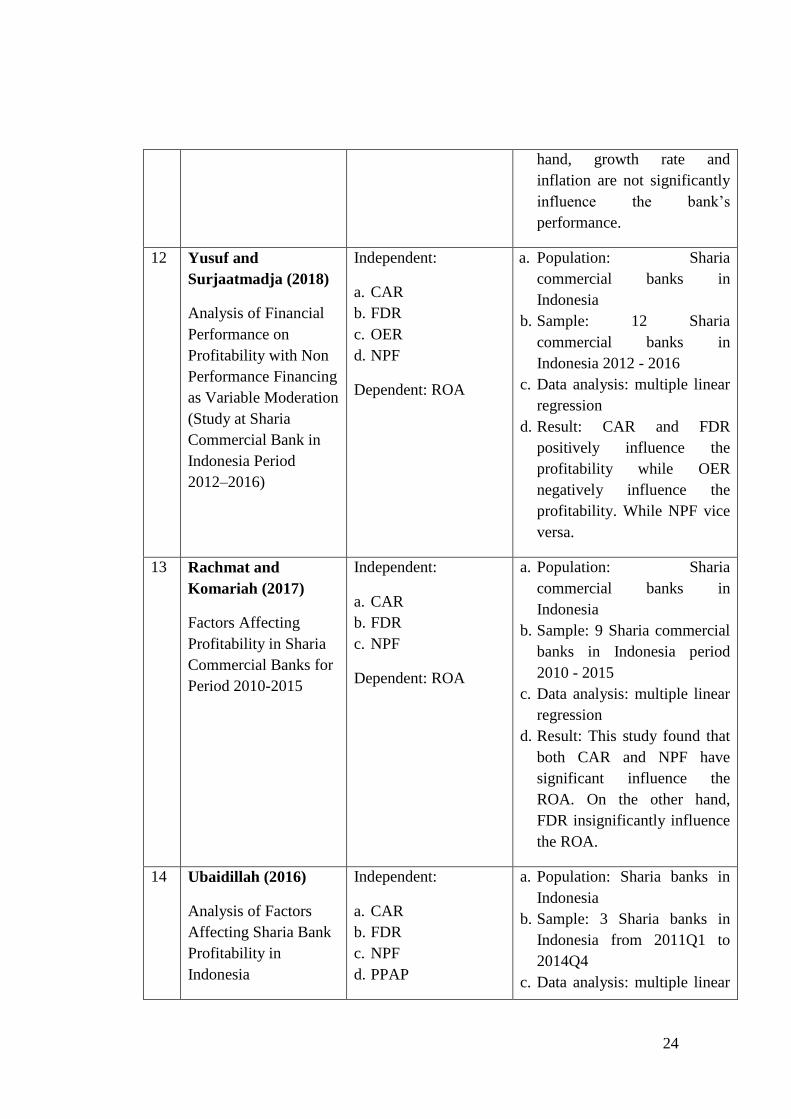

12 Yusuf and

Surjaatmadja (2018)

Analysis of Financial

Performance on

Profitability with Non

Performance Financing

as Variable Moderation

(Study at Sharia

Commercial Bank in

Indonesia Period

2012–2016)

Independent:

a. CAR

b. FDR

c. OER

d. NPF

Dependent: ROA

a. Population: Sharia

commercial banks in

Indonesia

b. Sample: 12 Sharia

commercial banks in

Indonesia 2012 - 2016

c. Data analysis: multiple linear

regression

d. Result: CAR and FDR

positively influence the

profitability while OER

negatively influence the

profitability. While NPF vice

versa.

13 Rachmat and

Komariah (2017)

Factors Affecting

Profitability in Sharia

Commercial Banks for

Period 2010-2015

Independent:

a. CAR

b. FDR

c. NPF

Dependent: ROA

a. Population: Sharia

commercial banks in

Indonesia

b. Sample: 9 Sharia commercial

banks in Indonesia period

2010 - 2015

c. Data analysis: multiple linear

regression

d. Result: This study found that

both CAR and NPF have

significant influence the

ROA. On the other hand,

FDR insignificantly influence

the ROA.

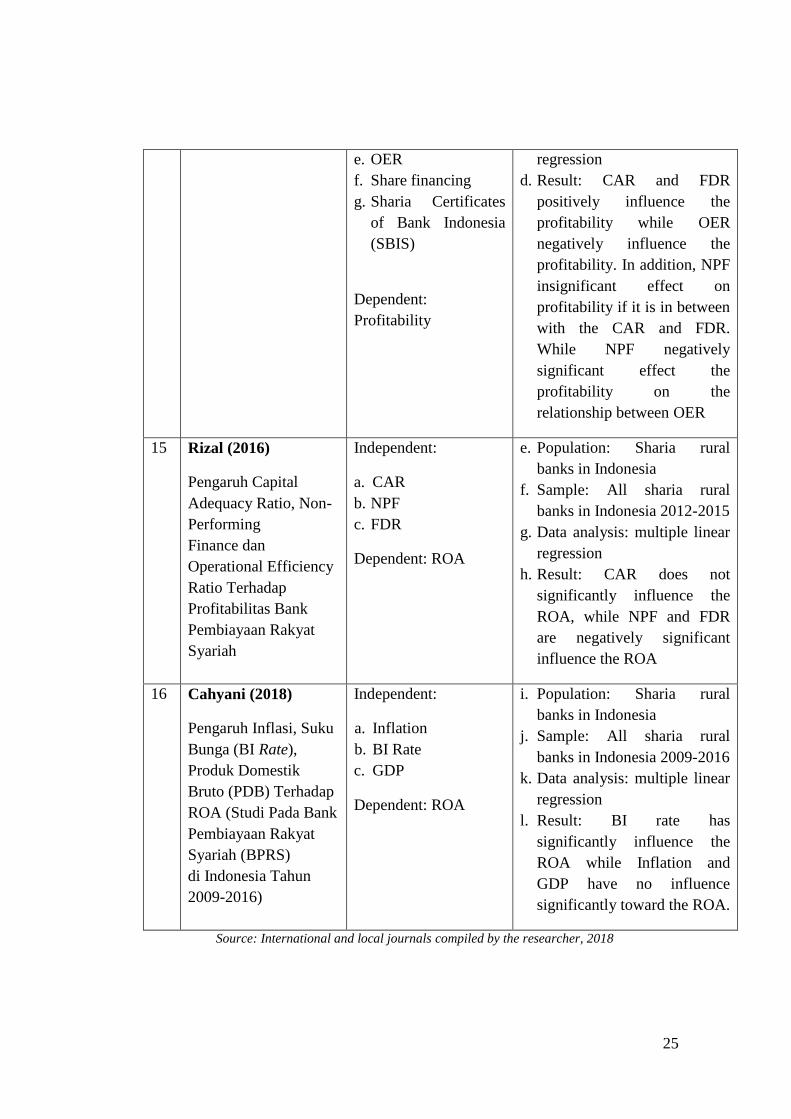

14 Ubaidillah (2016)

Analysis of Factors

Affecting Sharia Bank

Profitability in

Indonesia

Independent:

a. CAR

b. FDR

c. NPF

d. PPAP

a. Population: Sharia banks in

Indonesia

b. Sample: 3 Sharia banks in

Indonesia from 2011Q1 to

2014Q4

c. Data analysis: multiple linear

25

e. OER

f. Share financing

g. Sharia Certificates

of Bank Indonesia

(SBIS)

Dependent:

Profitability

regression

d. Result: CAR and FDR

positively influence the

profitability while OER

negatively influence the

profitability. In addition, NPF

insignificant effect on

profitability if it is in between

with the CAR and FDR.

While NPF negatively

significant effect the

profitability on the

relationship between OER

15 Rizal (2016)

Pengaruh Capital

Adequacy Ratio, Non-

Performing

Finance dan

Operational Efficiency

Ratio Terhadap

Profitabilitas Bank

Pembiayaan Rakyat

Syariah

Independent:

a. CAR

b. NPF

c. FDR

Dependent: ROA

e. Population: Sharia rural

banks in Indonesia

f. Sample: All sharia rural

banks in Indonesia 2012-2015

g. Data analysis: multiple linear

regression

h. Result: CAR does not

significantly influence the

ROA, while NPF and FDR

are negatively significant

influence the ROA

16 Cahyani (2018)

Pengaruh Inflasi, Suku

Bunga (BI Rate),

Produk Domestik

Bruto (PDB) Terhadap

ROA (Studi Pada Bank

Pembiayaan Rakyat

Syariah (BPRS)

di Indonesia Tahun

2009-2016)

Independent:

a. Inflation

b. BI Rate

c. GDP

Dependent: ROA

i. Population: Sharia rural

banks in Indonesia

j. Sample: All sharia rural

banks in Indonesia 2009-2016

k. Data analysis: multiple linear

regression

l. Result: BI rate has

significantly influence the

ROA while Inflation and

GDP have no influence

significantly toward the ROA.

Source: International and local journals compiled by the researcher, 2018

26

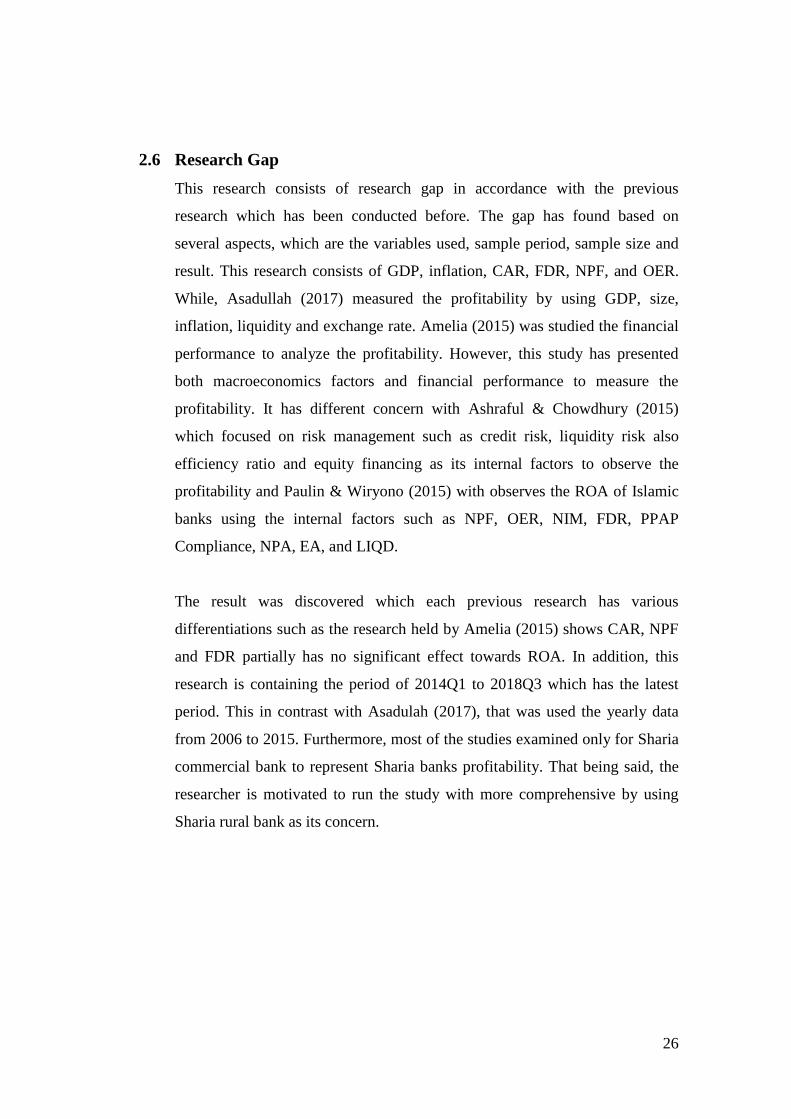

2.6 Research Gap

This research consists of research gap in accordance with the previous

research which has been conducted before. The gap has found based on

several aspects, which are the variables used, sample period, sample size and

result. This research consists of GDP, inflation, CAR, FDR, NPF, and OER.

While, Asadullah (2017) measured the profitability by using GDP, size,

inflation, liquidity and exchange rate. Amelia (2015) was studied the financial

performance to analyze the profitability. However, this study has presented

both macroeconomics factors and financial performance to measure the

profitability. It has different concern with Ashraful & Chowdhury (2015)

which focused on risk management such as credit risk, liquidity risk also

efficiency ratio and equity financing as its internal factors to observe the

profitability and Paulin & Wiryono (2015) with observes the ROA of Islamic

banks using the internal factors such as NPF, OER, NIM, FDR, PPAP

Compliance, NPA, EA, and LIQD.

The result was discovered which each previous research has various

differentiations such as the research held by Amelia (2015) shows CAR, NPF

and FDR partially has no significant effect towards ROA. In addition, this

research is containing the period of 2014Q1 to 2018Q3 which has the latest

period. This in contrast with Asadulah (2017), that was used the yearly data

from 2006 to 2015. Furthermore, most of the studies examined only for Sharia

commercial bank to represent Sharia banks profitability. That being said, the

researcher is motivated to run the study with more comprehensive by using

Sharia rural bank as its concern.

27

2.7 Theoretical Framework

To represent the beliefs on how certain variables are related to each other

along with the explanation of why the research believes that variables used are

associated with each other (Sekaran & Bougie, 2011). In this research, the

theoretical framework is described by Figure 2.1.

Figure 2.1 Theoretical Framework Source: Adjusted by Researcher, 2018

In this study, based on its relationship, the variables are segregated into two

types which are dependent variables and independent variables. Dependent

variable uses ROA to represent the profitability. While, independent variables

represented by GDP (X1), inflation (X2), CAR (X3), FDR (X4), NPF (X5), and

OER (X6). The researcher is aim to see any partial influence from each

independent variables toward dependent variables which expressed by H1 to

H6. Correspondingly, the simultaneous influence from all independent

variables which have been expressed by H7 in the Figure 2.1.

GDP

Inflation

CAR

FDR

NPF

OER

Profitability

H1 H2

H3

H4

H5 H6

H7

28

2.8 Hypothesis

In accordance with the literature review and research framework, the

researcher constructed the following hypothesis:

H1: There is significant influence of GDP towards profitability of Sharia

rural banks in Indonesia.

H2: There is significant influence of inflation towards profitability of

Sharia rural banks in Indonesia.

H3: There is significant influence of CAR towards profitability of Sharia

rural banks in Indonesia.

H4: There is significant influence of FDR towards profitability of Sharia

rural banks in Indonesia.

H5: There is significant influence of NPF towards profitability of Sharia

rural banks in Indonesia.

H6: There is significant influence of OER towards profitability of Sharia

rural banks in Indonesia.

H7: There is significant simultaneous influence of GDP, inflation, CAR,

FDR, NPF, and OER towards profitability of Sharia rural banks in

Indonesia.

29

CHAPTER III

METHODOLOGY

3.1 Research Method

Research method or those methods that are used in conducting the research to

achieve its objectives is different with research methodology. Research

methodology can be determined as the way to systematically solve the

research problem (Kothari, 2004). By having the research method, it will help

the researcher to have a clear understanding regarding the topic since it builds

the awareness of the topic (Neuman, 2014).

3.2 Research Framework

Figure 3.1 Theoretical Framework Source: Adjusted by Researcher, 2018

Understand problem and specify

research objective

Find and gather the theory

By using

Microsoft Excel

2010 and IBM

SPSS Statistics 22

Accessed from Bank

Indonesia, Financial

Service Authority

and Central

Statistics Agency

Develop theoretical framework

Define the methodology

Collect the data needed

Input and process the data

Data analysis and interpretation of results

Conclusions and recommendation

30

3.3 Sampling Design

In conducting the research, a sample design is a certain plan in order to obtain

a sample from given population. The researcher has to set up a sample design

that must be reliable and appropriate with the study (Kothari, 2004). In

accordance to (Sekaran & Bougie, 2011), the process of selecting number of

subjects from population as the representatives of the research is sampling.

This study uses non-probability sampling to collect the data from the

population. By having the right sample, it can be used to conclude a whole

population of the study.

3.3.1 Size of Population

Population can be determined as the whole individuals or objects within group

which interested to be analyzed by the researcher (Sekaran & Bougie, 2011).

It is not feasible to analyze the population because of its size. Thus, in this

study, we select some of population to achieve the research purpose. The

population of this study consists of Sharia rural banks in Indonesia which in

Indonesia based on Sharia Banking Statistics as per September 2018 by OJK,

there are 168 Sharia rural banks listed in Indonesia.

3.3.2 Size of Sample

In accordance to Sekaran & Bougie (2011), sampling design is divided into

two types, which are probability and non-probability sampling. The study is

using non-probability sampling with focus in purposive sampling with criteria

as follow:

1. Sharia rural banks in Indonesia which has listed and published in Bank

Indonesia and OJK

2. Sharia rural banks in Indonesia with minimum assets of IDR 100

Billion

3. Have provided its financial report in quarterly for the period of

2014Q1 to 2018Q3.

31

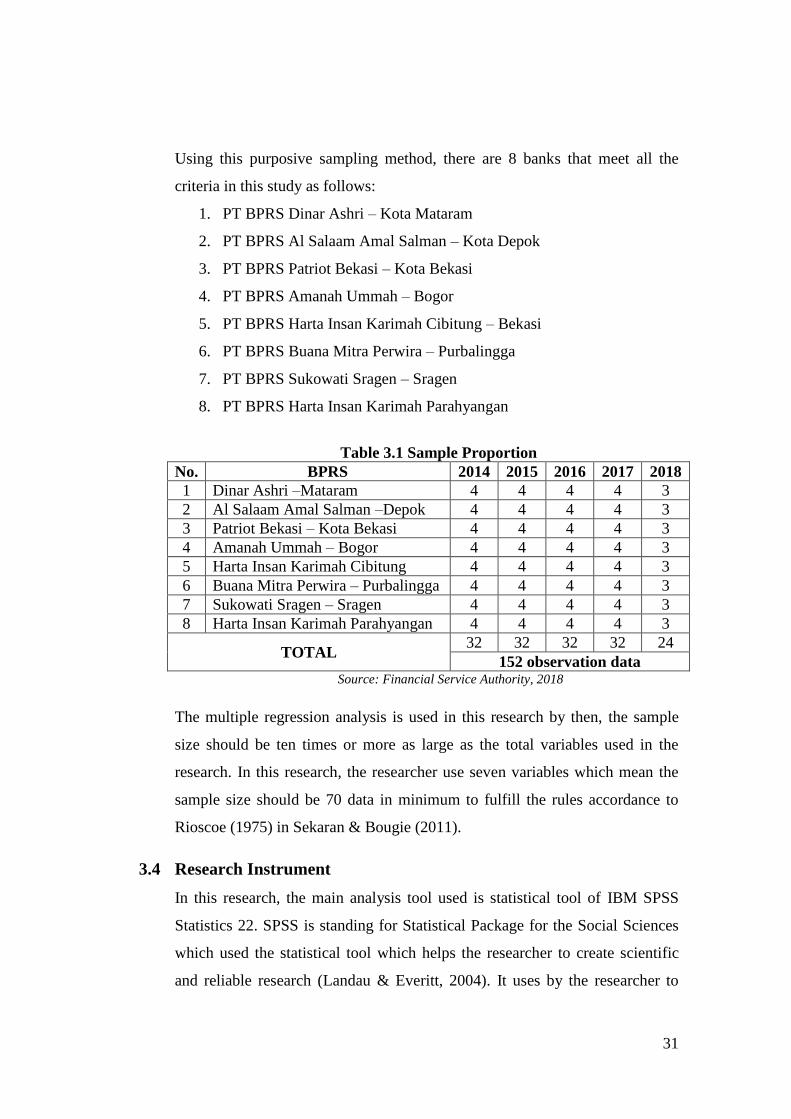

Using this purposive sampling method, there are 8 banks that meet all the

criteria in this study as follows:

1. PT BPRS Dinar Ashri – Kota Mataram

2. PT BPRS Al Salaam Amal Salman – Kota Depok

3. PT BPRS Patriot Bekasi – Kota Bekasi

4. PT BPRS Amanah Ummah – Bogor

5. PT BPRS Harta Insan Karimah Cibitung – Bekasi

6. PT BPRS Buana Mitra Perwira – Purbalingga

7. PT BPRS Sukowati Sragen – Sragen

8. PT BPRS Harta Insan Karimah Parahyangan

Table 3.1 Sample Proportion

No. BPRS 2014 2015 2016 2017 2018

1 Dinar Ashri –Mataram 4 4 4 4 3

2 Al Salaam Amal Salman –Depok 4 4 4 4 3

3 Patriot Bekasi – Kota Bekasi 4 4 4 4 3

4 Amanah Ummah – Bogor 4 4 4 4 3

5 Harta Insan Karimah Cibitung 4 4 4 4 3

6 Buana Mitra Perwira – Purbalingga 4 4 4 4 3

7 Sukowati Sragen – Sragen 4 4 4 4 3

8 Harta Insan Karimah Parahyangan 4 4 4 4 3

TOTAL 32 32 32 32 24

152 observation data Source: Financial Service Authority, 2018

The multiple regression analysis is used in this research by then, the sample

size should be ten times or more as large as the total variables used in the

research. In this research, the researcher use seven variables which mean the

sample size should be 70 data in minimum to fulfill the rules accordance to

Rioscoe (1975) in Sekaran & Bougie (2011).

3.4 Research Instrument

In this research, the main analysis tool used is statistical tool of IBM SPSS

Statistics 22. SPSS is standing for Statistical Package for the Social Sciences

which used the statistical tool which helps the researcher to create scientific

and reliable research (Landau & Everitt, 2004). It uses by the researcher to

32

processing the raw data in statistic way with aim to get the result that will be

interpreted, such as normality, descriptive, heteroscedasticity, autocorrelation,

multicollinearity and multiple regression.

SPSS is statistics software which helps to provide advanced data analysis,

regression and forecasting tools (Landau & Everitt, 2004). Additionally, the

researcher also use the Microsoft Excel 2010 in transforming the raw data

obtained from financial reports of Sharia rural banks in Indonesia quarterly

and BPS data portal, to categorize the data and to create charts and tables. The

other relevant instrument used in this research is Microsoft Word 2010 to

compose the research.

3.5 Data Collection Method

In conducting a study, data holds an important role in proving the hypothesis

has been set and achieve objectives of the research. Every study must have

known what data needs to be provided and how to collect, identify and process

the data. This study is using secondary data which means the collection of data

which collected by someone else earlier which has no relation to the research

study but collected these data for any other purposes at the different time in

the past (Johnston, 2014).

The data collection method in this research is financial report, which in

quarterly report of Sharia rural bank in Indonesia which has the total assets

minimum of IDR 100 Billion based on the Infobank Sharia Awards in 2018.

For microeconomics, the data collected from financial report of each banks

where have been provided in website of Bank Indonesia and OJK. While

macroeconomics collected from central agency on statistics which both data

macroeconomics and microeconomics taken quarterly from 2014Q1 to

2018Q3.

33

3.6 Operational Definitions

In this study, there are 6 (six) independent variables, which are GDP, inflation,

CAR, FDR, NPF, and OER. While, ROA to represent the profitability is the

dependent variable in this research. Meanwhile, the conceptual definitions and

measurements are follows:

Table 3.2 Operational Definitions

Research

Variable

Operational

Definition Equation Scale

Dependent Variable

Profitability Profitability is the ratio

which developed by

DuPont in order to

evaluate how effectively

assets are used by the

firms (Groppelli &

Nikbakht, 2000).

ROA =

Net Income x 100 Total Asset

Ratio

Independent Variables

Gross

Domestic

Product

GDP is the amount of

added value generated by

all business units in a

particular country in a

certain period (OpenStax

College, 2014)

GDPt = Ct + It + Gt + (Xt − IMt)

Ratio

Inflation Inflation is when the

price’s condition of most

goods and services

continue increasing and it

may cause the decreasing

of the standard of living

cost as the effect of

spending a lot of money

Inflationyear2 = CPI2 – CPI1 x 100

CPI1 Ratio

34

to get the same amount

of goods and/or services

we bought previous time

(OpenStax College,

2014)

Capital

Adequacy

Ratio

CAR is the ratio that

helps to measure the

capital adequacy of a

bank to support risk-

bearing assets (Rahim,

2014).

CAR =

Capital x 100% Risk-

Weighted

Assets

Ratio

Financing

Deposit

Ratio

FDR is the ratio that

helps to measure the

bank’s liquidity in

repaying funds

withdrawals made by

depositors by relying on

financing provided as a

liquidity source, which

by dividing the amount

of financing provided by

banks to third party funds

(Wahyu, 2016).

FDR =

Total

Financing

x 100% Total Third

Party Fund Ratio

Non-

Performing

Financing

NPF is show the inability

of the customer to return

the loan in the specific

period of time (Nahar &

Prawoto, 2017).

NPF =

NPF

(Substandard,

doubtful

and loss)

x 100% Total

Financing

Ratio

35

Operational

Efficiency

Ratio

OER is a comparison

between operational costs

and operating income to

measure the level of

efficiency and bank’s

ability in conducting

their operations (Hakim

& Sugianto, 2018).

OER =

Operational

Expenses x 100%

Operational

Income

Ratio

Source: Adjusted by Researcher, 2018 according to Ali & Maamor (2018), Islam, et al.

(2017), Rahim (2014), Wahyu (2016), Nahar & Prawoto (2017), Hakim & Sugianto (2018),

3.7 Data Analysis Method

3.7.1 Descriptive Statistics Analysis

According to (Sugiyono, 2010), descriptive analysis is analysis used to

analyze data by describing the collected data as they are without intending to

make conclusions that apply to the general or generalizations. Descriptive

analysis analyzes data by giving a description or characteristic of data seen

from the mean, standard deviation, maximum, and minimum (Weiss, 2012).

The mean is used to estimate the magnitude of the population average

estimated from the sample which can be formulated as follows (Schwert,

2010):

(Eq. 7)

Where:

N = perceptions quantity in the present test

The maximum and minimum are used to see the current sample of maximum

and minimum values (Schwert, 2010).

36

Standard deviation is used to determine how the data is spread in the sample

or data around average which can be formulated as follows (Schwert, 2010):

(Eq. 8)

Where:

N = number of observations in the current sample

y mean of the series

Descriptive statistics need to be done to see the overall picture of the samples

collected and fulfill the requirements as samples.

3.7.2 Classical Assumption Test

In accordance to William (2015), it is important to conduct the classical

assumption test since it utilizes the multiple regressions or indeed any

statistical technique. There are several test used for classical assumption test

which explained as follows:

1. Normality Test

The first step to do the multivariate analysis is doing the normality test. This

test has objective to test the regressions model and the residual confounding

variable has a normal distribution or not (Sugiyono, 2010). The t and F tests

are assuming that the residual value follows a normal distribution. In

accordance with (Ghozali, 2016), in order to detect the residuals are normally

distributed or not, it can be analyzed by using graph. The graphical analysis

can be seen from histogram graph and probability-probability plot (p-p plot).

The basics to decide the normality test can be done by graphical analysis. If

the dots in P-P plot graph are spreading around the diagonal line or following

the direction of the line, it concluded that the regression model has met the

assumption of normality, or normality distribution. In addition, if the curve of

histogram is concentrated in the middle and declined in both left and right side

37

or the curve shaped like a bell shape, it can be conclude that the data has

normally distributed (Totton & White, 2011).

2. Heteroscedasticity Test

Heteroscedasticity determined as the variance of the error term for probability

(Williams, 2015). Heteroscedasticity happens if the variance error is not

constant which means the dispersion is not the same in all observations. On

the other hand, when the variance error is constant which means the dispersion

also remains the same in all observation is called as Homoscedasticity (Gau &

Stadtherr, 2002). A good regression model will show there is no issue for

heteroscedasticity in which only show homoscedasticity, means the regression

model is acceptable (Santoso, 2010).

Heteroscedasticity can be found by graph techniques in which seeing the

scatter plot. In the scatter plot, it shows the pattern of dots formed between

dependent variable (ZPRED) and the residuals (SRESID). It is a good way to

find out the homoscedasticity or an error along the regression line.

Accordance to Santoso (2012), the basic criteria for heteroscedasticity can be

seen through scatter plot as follows:

1) Heteroscedasticity can be found if there are certain patterns or dots

forms a regular pattern (wavy, widened, and/or narrowed).

2) Homoscedasticity can be found if there are no certain patterns which

the dots are spreading above and below the zero and Y axis.

3. Autocorrelation Test

Autocorrelation aims to clarify correlations in data collection among time

series data in the same cross sectional unit on the same variable (Meko, 2013).

Violation of this requirement exists when there is correlation error between

observations. Autocorrelation refers to the correlations of the time series with

its own past and future values and among members of a series of number

which compiled in time (Meko, 2013).

38

The Durbin-Watson statistic is measuring the autocorrelation in the residuals