the classical monetary model - crei...2016/07/01 · the classical monetary model jordi galí crei,...

TRANSCRIPT

The Classical Monetary Model

Jordi Galí

CREI, UPF and Barcelona GSE

January 2019

Jordi Galí (CREI, UPF and Barcelona GSE) Classical Monetary Model January 2019 1 / 23

Assumptions

Perfect competition in goods and labor markets

Flexible prices and wages

Representative household

Money in the utility function

No capital accumulation

No fiscal sector

Closed economy

Jordi Galí (CREI, UPF and Barcelona GSE) Classical Monetary Model January 2019 2 / 23

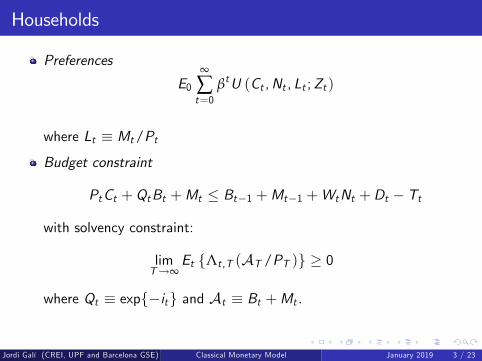

Households

Preferences

E0∞

∑t=0

βtU (Ct ,Nt , Lt ;Zt )

where Lt ≡ Mt/Pt

Budget constraint

PtCt +QtBt +Mt ≤ Bt−1 +Mt−1 +WtNt +Dt − Tt

with solvency constraint:

limT→∞

Et {Λt ,T (AT /PT )} ≥ 0

where Qt ≡ exp{−it} and At ≡ Bt +Mt .

Jordi Galí (CREI, UPF and Barcelona GSE) Classical Monetary Model January 2019 3 / 23

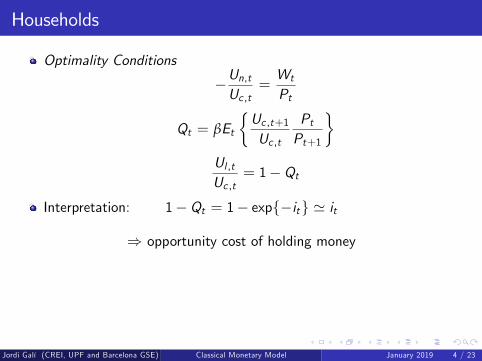

Households

Optimality Conditions

−Un,tUc ,t

=Wt

Pt

Qt = βEt

{Uc ,t+1Uc ,t

PtPt+1

}Ul ,tUc ,t

= 1−Qt

Interpretation: 1−Qt = 1− exp{−it} ' it

⇒ opportunity cost of holding money

Jordi Galí (CREI, UPF and Barcelona GSE) Classical Monetary Model January 2019 4 / 23

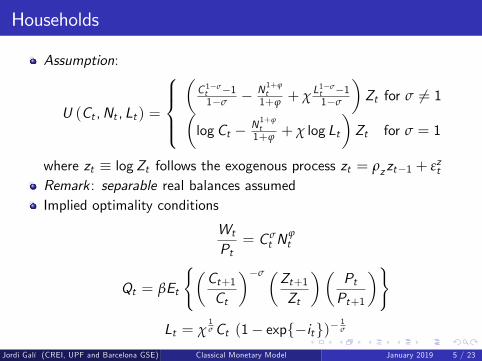

Households

Assumption:

U (Ct ,Nt , Lt ) =

(C 1−σt −11−σ − N 1+ϕ

t1+ϕ + χ L

1−σt −11−σ

)Zt for σ 6= 1(

logCt − N 1+ϕt1+ϕ + χ log Lt

)Zt for σ = 1

where zt ≡ logZt follows the exogenous process zt = ρzzt−1 + εztRemark : separable real balances assumedImplied optimality conditions

Wt

Pt= C σ

t Nϕt

Qt = βEt

{(Ct+1Ct

)−σ (Zt+1Zt

)(PtPt+1

)}Lt = χ

1σCt (1− exp{−it})−

1σ

Jordi Galí (CREI, UPF and Barcelona GSE) Classical Monetary Model January 2019 5 / 23

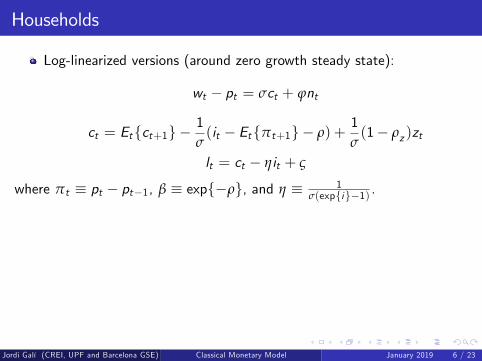

Households

Log-linearized versions (around zero growth steady state):

wt − pt = σct + ϕnt

ct = Et{ct+1} −1σ(it − Et{πt+1} − ρ) +

1σ(1− ρz )zt

lt = ct − ηit + ς

where πt ≡ pt − pt−1, β ≡ exp{−ρ}, and η ≡ 1σ(exp{i}−1) .

Jordi Galí (CREI, UPF and Barcelona GSE) Classical Monetary Model January 2019 6 / 23

Firms

TechnologyYt = AtN1−α

t (1)

where at ≡ logAt follows an exogenous process

at = ρaat−1 + εat

Profit maximization:max PtYt −WtNt

subject to (1), taking the price and wage as given

Optimality condition:

Wt

Pt= (1− α)AtN−α

t

Log linear version

wt − pt = at − αnt + log(1− α)

Jordi Galí (CREI, UPF and Barcelona GSE) Classical Monetary Model January 2019 7 / 23

Policy

Government budget constraint

PtGt + BGt−1 = Tt +QtBGt + ∆MS

t

Fiscal policy: rule determining {Gt ,BGt ,Tt}Monetary policy: rule determining {MS

t , it}

Jordi Galí (CREI, UPF and Barcelona GSE) Classical Monetary Model January 2019 8 / 23

Equilibrium: Market Clearing Conditions

Goods market clearingYt = Ct + Gt

Labor market clearing

(1− α)AtN−αt =

Wt

Pt= C σ

t Nϕt

Asset market clearingBt = BGt

Mt = MSt

Jordi Galí (CREI, UPF and Barcelona GSE) Classical Monetary Model January 2019 9 / 23

Equilibrium

Equilibrium values for real variables (assuming Gt = 0)

nt = ψnaat + ψn

yt = ψyaat + ψy

rt ≡ it − Et{πt+1} = ρ− σψya(1− ρa)at + (1− ρz )zt

ωt ≡ wt − pt = ψωaat + ψω

where ψna ≡ 1−σσ(1−α)+ϕ+α

; ψn ≡log(1−α)

σ(1−α)+ϕ+α; ψya ≡

1+ϕσ(1−α)+ϕ+α

;

ψy ≡(1−α) log(1−α)σ(1−α)+ϕ+α

; ψωa ≡σ+ϕ

σ(1−α)+ϕ+α; ψω ≡ −

α log(1−α)σ(1−α)+ϕ+α

Two neutrality results:

(i) non-fiscal variables independent of {BGt ,Tt} (Ricardianequivalence)

(ii) real variables independent of monetary policy

Monetary policy needed to determine nominal variables

Jordi Galí (CREI, UPF and Barcelona GSE) Classical Monetary Model January 2019 10 / 23

Price Level Determination

Example I: A Simple Interest Rate Rule

it = ρ+ π + φπ(πt − π) + vt

where φπ ≥ 0. Combined with definition of real rate:

φππ̂t = Et{π̂t+1}+ r̂t − vt

Case I: φπ > 1

π̂t =∞

∑k=0

φ−(k+1)π Et{r̂t+k − vt+k}

= −σψya(1− ρa)

φπ − ρaat +

1− ρzφπ − ρz

zt −1

φπ − ρvvt

=⇒ nominal determinacy

Jordi Galí (CREI, UPF and Barcelona GSE) Classical Monetary Model January 2019 11 / 23

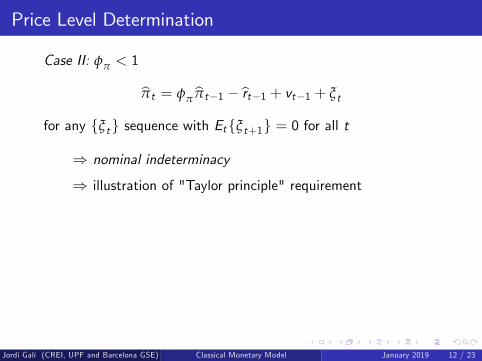

Price Level Determination

Case II: φπ < 1

π̂t = φππ̂t−1 − r̂t−1 + vt−1 + ξt

for any {ξt} sequence with Et{ξt+1} = 0 for all t

⇒ nominal indeterminacy

⇒ illustration of "Taylor principle" requirement

Jordi Galí (CREI, UPF and Barcelona GSE) Classical Monetary Model January 2019 12 / 23

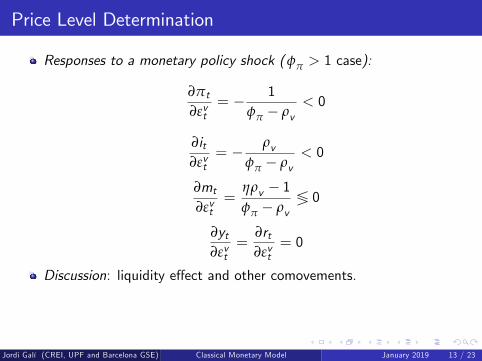

Price Level Determination

Responses to a monetary policy shock (φπ > 1 case):

∂πt∂εvt

= − 1φπ − ρv

< 0

∂it∂εvt

= − ρvφπ − ρv

< 0

∂mt∂εvt

=ηρv − 1φπ − ρv

≶ 0

∂yt∂εvt

=∂rt∂εvt

= 0

Discussion: liquidity effect and other comovements.

Jordi Galí (CREI, UPF and Barcelona GSE) Classical Monetary Model January 2019 13 / 23

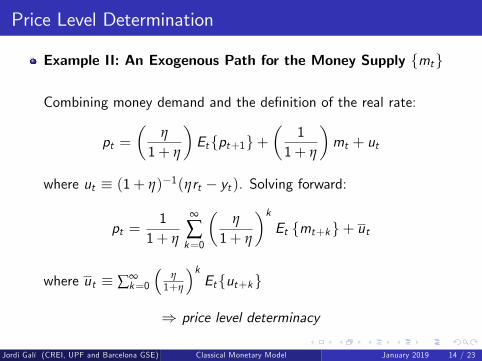

Price Level Determination

Example II: An Exogenous Path for the Money Supply {mt}

Combining money demand and the definition of the real rate:

pt =(

η

1+ η

)Et{pt+1}+

(1

1+ η

)mt + ut

where ut ≡ (1+ η)−1(ηrt − yt ). Solving forward:

pt =1

1+ η

∞

∑k=0

(η

1+ η

)kEt {mt+k}+ ut

where ut ≡ ∑∞k=0

(η1+η

)kEt{ut+k}

⇒ price level determinacy

Jordi Galí (CREI, UPF and Barcelona GSE) Classical Monetary Model January 2019 14 / 23

Price Level Determination

In terms of money growth rates:

pt = mt +∞

∑k=1

(η

1+ η

)kEt {∆mt+k}+ ut

Nominal interest rate:

it = η−1 (yt − (mt − pt ))

= η−1∞

∑k=1

(η

1+ η

)kEt {∆mt+k}+ ut

where ut ≡ η−1(ut + yt ) is independent of monetary policy.

Jordi Galí (CREI, UPF and Barcelona GSE) Classical Monetary Model January 2019 15 / 23

Price Level Determination

Assumption∆mt = ρm∆mt−1 + εmt

rt = yt = 0

Price response:

pt = mt +ηρm

1+ η(1− ρm)∆mt

⇒ large price response

Nominal interest rate response:

it =ρm

1+ η(1− ρm)∆mt

⇒ no liquidity effect

Jordi Galí (CREI, UPF and Barcelona GSE) Classical Monetary Model January 2019 16 / 23

The Case of Non-Separable Real Balances

Labor supply affected by monetary policy ⇒ non-neutralityExample:

U (Xt ,Nt ) =X 1−σt − 11− σ

− N1+ϕt

1+ ϕ

where

Xt ≡[(1− ϑ)C 1−ν

t + ϑL1−νt

] 11−v for ν 6= 1

≡ C 1−ϑt Lϑ

t for ν = 1

implying:Uc ,t = X ν−σ

t C−νt (1− ϑ)

Ul ,t = Xν−σt L−ν

t ϑ

Un,t = Nϕt

Remark: Ucl ,t > 0 ⇔ ν > σJordi Galí (CREI, UPF and Barcelona GSE) Classical Monetary Model January 2019 17 / 23

The Case of Non-Separable Real Balances

Optimality conditions:

Wt

Pt= Nϕ

t Xσ−νt C ν

t (1− ϑ)−1

Qt = βEt

{(Ct+1Ct

)−ν (Xt+1Xt

)ν−σ ( PtPt+1

)}

Lt = Ct (1− exp{−it})−1ν

(ϑ

1− ϑ

) 1ν

Log-linearized money demand equation:

lt = ct − ηit + ς

where η ≡ 1/[ν(exp{i} − 1)]

Jordi Galí (CREI, UPF and Barcelona GSE) Classical Monetary Model January 2019 18 / 23

The Case of Non-Separable Real Balances

Log-linearized labor supply equation (ignoring constants):

wt − pt = σct + ϕnt − (ν− σ)(xt − ct )= σct + ϕnt − χ(ν− σ) (lt − ct )= σct + ϕnt + ηχ(ν− σ)it

where χ ≡ θk 1−νm

1−θ+θk 1−νm

with km ≡ LC . In a zero inflation steady state,

km ≡ LC =

(ϑ

(1−β)(1−ϑ)

) 1ν, implying χ = km (1−β)

1+km (1−β). In addition,

η = βν(1−β)

.

Accordingly,wt − pt = σct + ϕnt +vit

where v ≡ ηχ(ν− σ) =kmβ(1− σ

ν )1+km (1−β)

≶ 0.

Jordi Galí (CREI, UPF and Barcelona GSE) Classical Monetary Model January 2019 19 / 23

The Case of Non-Separable Real Balances

Labor market clearing:

which combined with aggregate production function:

yt = ψyaat + ψyi it

where ψyi ≡ −v(1−α)

σ(1−α)+ϕ+αand ψya ≡

1+ϕσ(1−α)+ϕ+α

⇒ long run non-superneutrality

Jordi Galí (CREI, UPF and Barcelona GSE) Classical Monetary Model January 2019 20 / 23

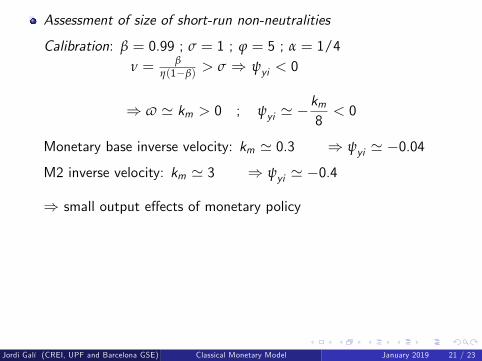

Assessment of size of short-run non-neutralities

Calibration: β = 0.99 ; σ = 1 ; ϕ = 5 ; α = 1/4ν = β

η(1−β)> σ ⇒ ψyi < 0

⇒ v ' km > 0 ; ψyi ' −km8< 0

Monetary base inverse velocity: km ' 0.3 ⇒ ψyi ' −0.04M2 inverse velocity: km ' 3 ⇒ ψyi ' −0.4

⇒ small output effects of monetary policy

Jordi Galí (CREI, UPF and Barcelona GSE) Classical Monetary Model January 2019 21 / 23

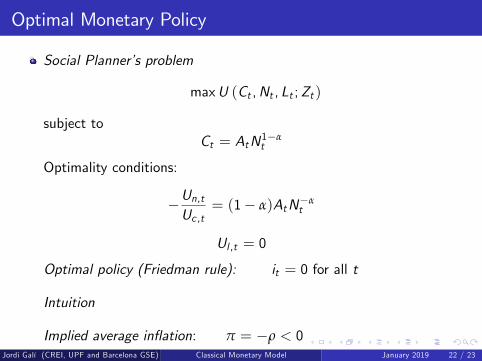

Optimal Monetary Policy

Social Planner’s problem

maxU (Ct ,Nt , Lt ;Zt )

subject toCt = AtN1−α

t

Optimality conditions:

−Un,tUc ,t

= (1− α)AtN−αt

Ul ,t = 0

Optimal policy (Friedman rule): it = 0 for all t

Intuition

Implied average inflation: π = −ρ < 0Jordi Galí (CREI, UPF and Barcelona GSE) Classical Monetary Model January 2019 22 / 23

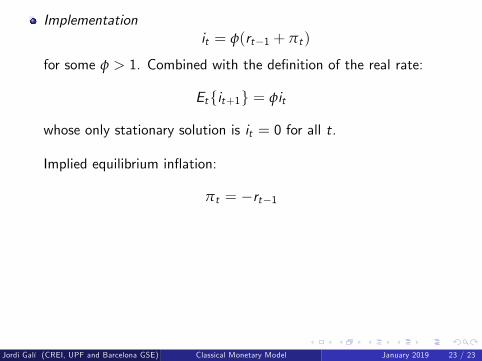

Implementationit = φ(rt−1 + πt )

for some φ > 1. Combined with the definition of the real rate:

Et{it+1} = φit

whose only stationary solution is it = 0 for all t.

Implied equilibrium inflation:

πt = −rt−1

Jordi Galí (CREI, UPF and Barcelona GSE) Classical Monetary Model January 2019 23 / 23