the circular-flow diagram firms households market for factors of production market for goods and...

TRANSCRIPT

The Circular-Flow Diagram

Firms Households

Market for Factors

of Production

Market for Goods

and Services

SpendingRevenue

Wages, rent, and

profit

Income

Goods & Services

sold

Goods & Services bought

Labor, land, and capital

Inputs for production

Markets

A market is a group of buyers and sellers who interact to buy and sell a particular good or service.

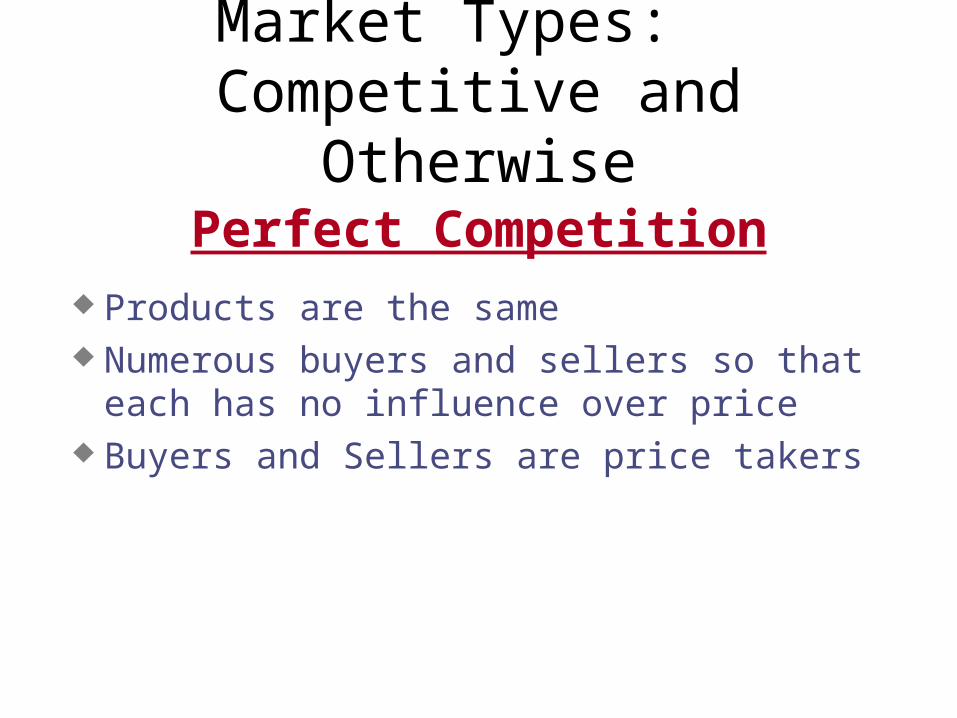

Market Types: Competitive and Otherwise

Products are the same Numerous buyers and sellers so that each

has no influence over price Buyers and Sellers are price takers

Perfect Competition

Market Types: Competitive and Otherwise

Monopoly One seller who controls price

Oligopoly Few sellers Not always aggressive competition

Monopolistic Competition Many sellers Slightly differentiated products Each seller may set price for its own product

The Circular-Flow Diagram

Firms Households

Market for Factors

of Production

Market for Goods

and Services

SpendingRevenue

Wages, rent, and

profit

Income

Goods & Services

sold

Goods & Services bought

Labor, land, and capital

Inputs for production

The quantity demanded is the amount of a good that a buyer is (buyers are)

willing and able to buy during a specified period of time.

Quantity demanded refers to a particular number of units.

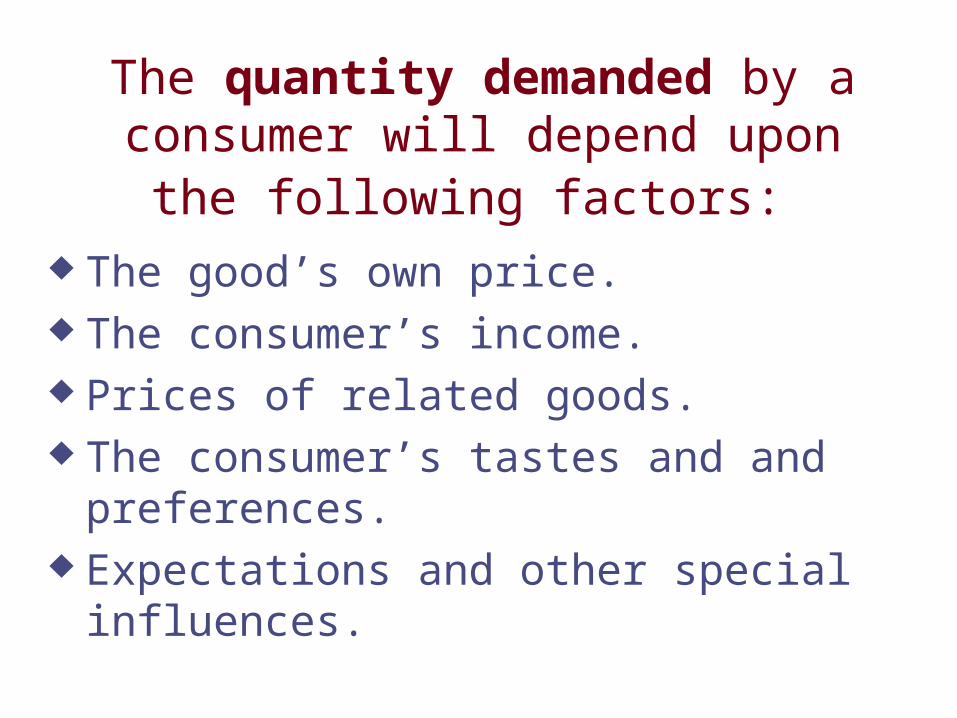

The quantity demanded by a consumer will depend upon the following factors:

The good’s own price. The consumer’s income. Prices of related goods. The consumer’s tastes and and preferences. Expectations and other special influences.

2 4 6 8 12 14

2

4

6

8

10

12

10

14

price

quantity

dv

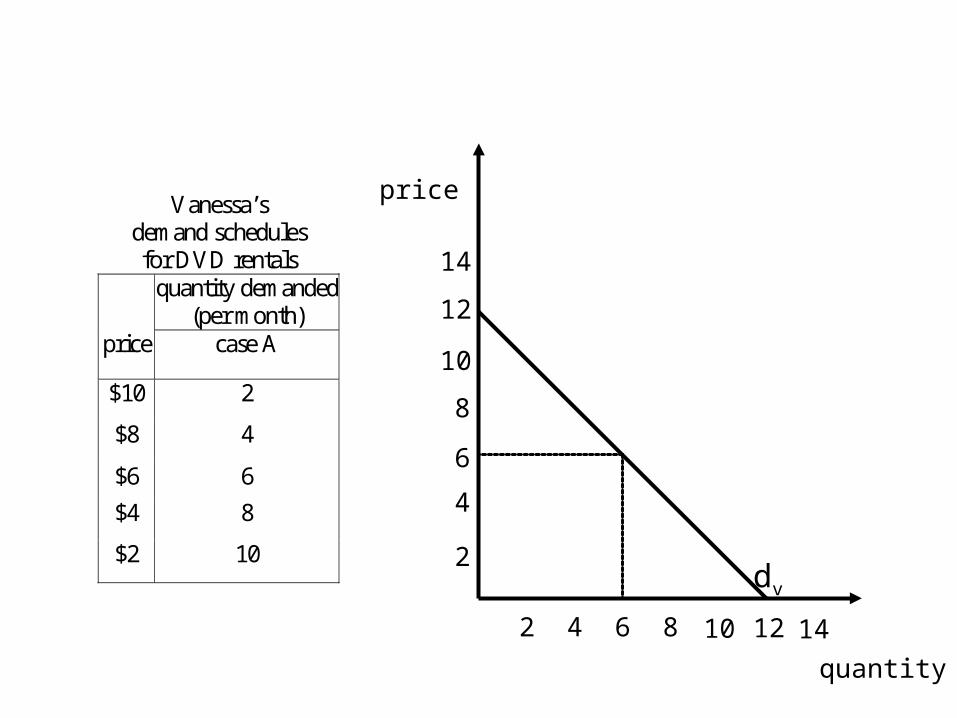

Vanessa’s demand schedules for DVD rentals

quantity demanded (per month)

price case A

$10 2

$8 4

$6 6

$4 8

$2 10

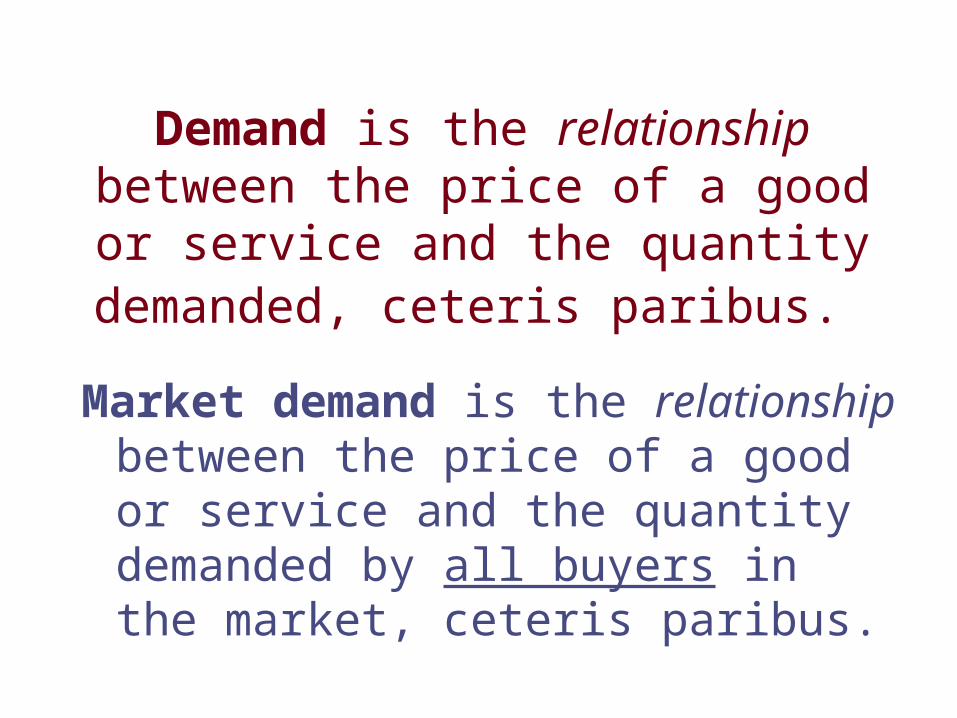

Demand is the relationship between the price of a good or service and the

quantity demanded, ceteris paribus.

Market demand is the relationship between the price of a good or service and the quantity demanded by all buyers in the market, ceteris paribus.

2 4 6 8 12 14 16

2

4

6

8

10

12

10

14

price

quantity

D

dkdD dv

a b c e

m n q r s

Demand Schedulesfor Video Rentals

quantity demanded(per month)

price Kim Derrek Van-essa

total

$10 1 0 2 3

$8 2 0 4 6

$6 3 1 6 10

$4 4 2 8 14

$2 5 3 10 18

The market demand curve is obtained by horizontally summing the demand curves for all buyers in the market.

Implication: An increase in the number of buyers will result in an increase in market demand, ceteris paribus.

Changes in Quantity Demanded

0

D1

Price of Cigarettes per Pack

Number of Cigarettes Smoked per Day

The price of cigarettes increases.

A

C

20

2.00

$4.00

12

Change in Quantity Demanded Movement along the demand curve. Caused by a change in the price of

the product.

Demand is the relationship between the quantity demanded and the good’s own

price, ceteris paribus.

Other factors being held constant: Income. Prices of related goods. Tastes and and preferences. Expectations and other special influences.

A change in demand is a change in the relationship between the quantity

demanded and price.

A shift in the demand curve, either to the left or right.

Caused by a change in a determinant other than the price.

2 4 6 8 12 14

2

4

6

8

10

12

10

14

price

quantity

dv

Vanessa’sdemand schedulesfor video rentals

quantity demanded(per month)

price case A case B

$10 2 0

$8 4 1

$6 6 2

$4 8 3

$2 10 4 d*v

Example of a Decrease in Demand

Changes in Demand

0

D1

Price of Ice-Cream Cone

Quantity of Ice-Cream Cones

D3

D2

Increase in demand

Decrease in demand

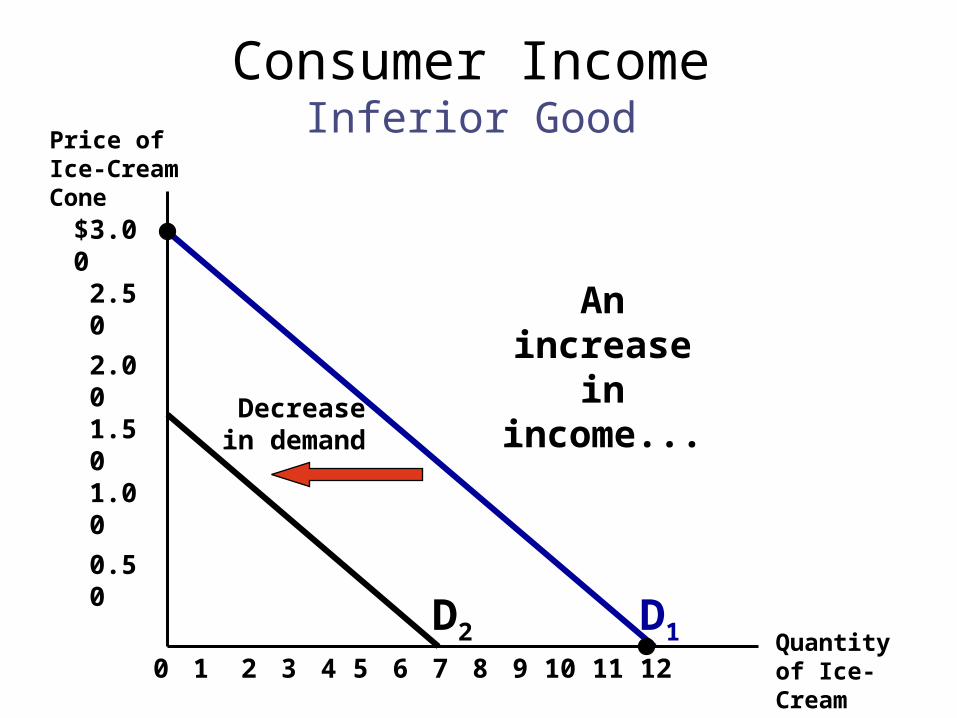

Consumer Income

As income increases the demand for a normal good will increase.

As income increases the demand for an inferior good will decrease.

Consumer IncomeNormal Good

$3.002.50

2.001.501.00

0.50

21 3 4 5 6 7 8 9 10

12

11

Price of Ice-Cream Cone

Quantity of Ice-Cream Cones

0

Increasein demand

An increase

in income...

D1

D2

Consumer IncomeInferior Good

$3.002.50

2.001.501.00

0.50

21 3 4 5 6 7 8 9 10

12

11

Price of Ice-Cream Cone

Quantity of Ice-Cream Cones

0

Decreasein demand

An increase

in income...

D1D2

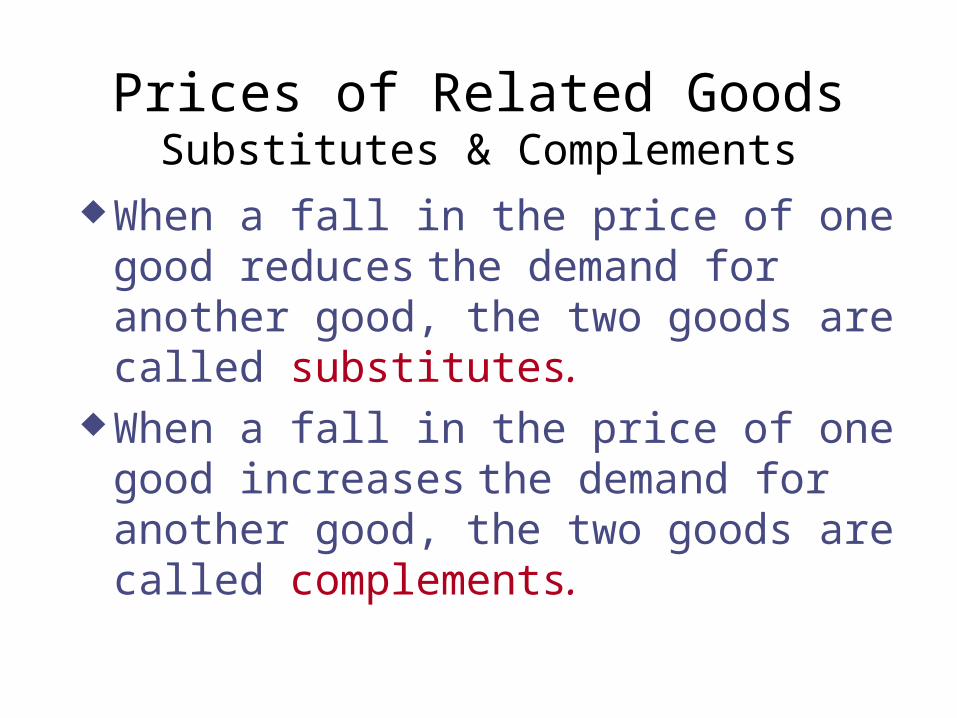

Prices of Related GoodsSubstitutes & Complements

When a fall in the price of one good reduces the demand for another good, the two goods are called substitutes.

When a fall in the price of one good increases the demand for another good, the two goods are called complements.

Show graphically and explain what will happen to the demand for gasoline

when:

The price of air travel increases. Automobile prices fall. Incomes rise. Highway tolls rise. The price of gasoline rises.

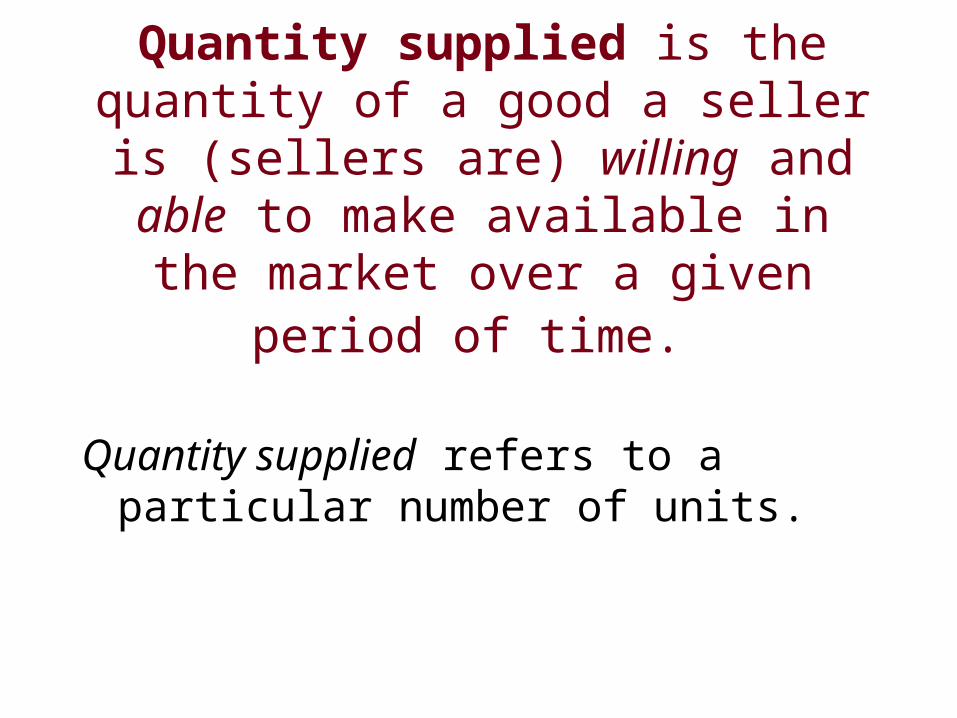

Quantity supplied is the quantity of a good a seller is (sellers are) willing and

able to make available in the market over a given period of time.

Quantity supplied refers to a particular number of units.

The quantity supplied will depend upon: the good’s own price prices of inputs used in producing the good technology prices of other goods the seller could supply expectations and other factors

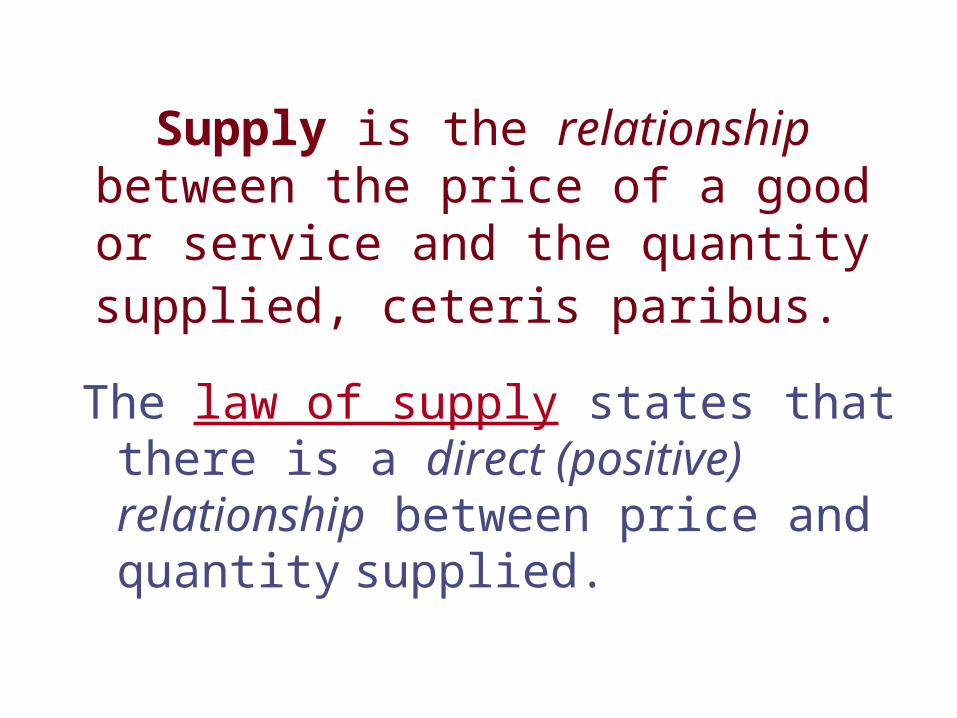

Supply is the relationship between the price of a good or service and the quantity supplied, ceteris paribus.

The law of supply states that there is a direct (positive) relationship between price and quantity supplied.

Supply Curve

$3.002.502.00

1.501.00

0.50

21 3 4 5 6 7 8 9 10

12

11

Price of Ice-Cream Cone

Quantity of Ice-Cream Cones

0

Price Quantity$0.00 00.50 01.00 11.50 22.00 32.50 43.00 5

Market Supply

Market supply refers to the sum of all individual supplies for all sellers in a market for a particular good or service.

Graphically, individual supply curves are summed horizontally to obtain the market supply curve.

Change in Quantity Supplied

1 5

Price of Ice-Cream Cone

Quantity of Ice-Cream Cones

0

S

1.00A

C$3.00

The price increases from $1.00 to $3.00

Change in Quantity Supplied

Movement along the supply curve.

Caused by a change in the market price of the product.

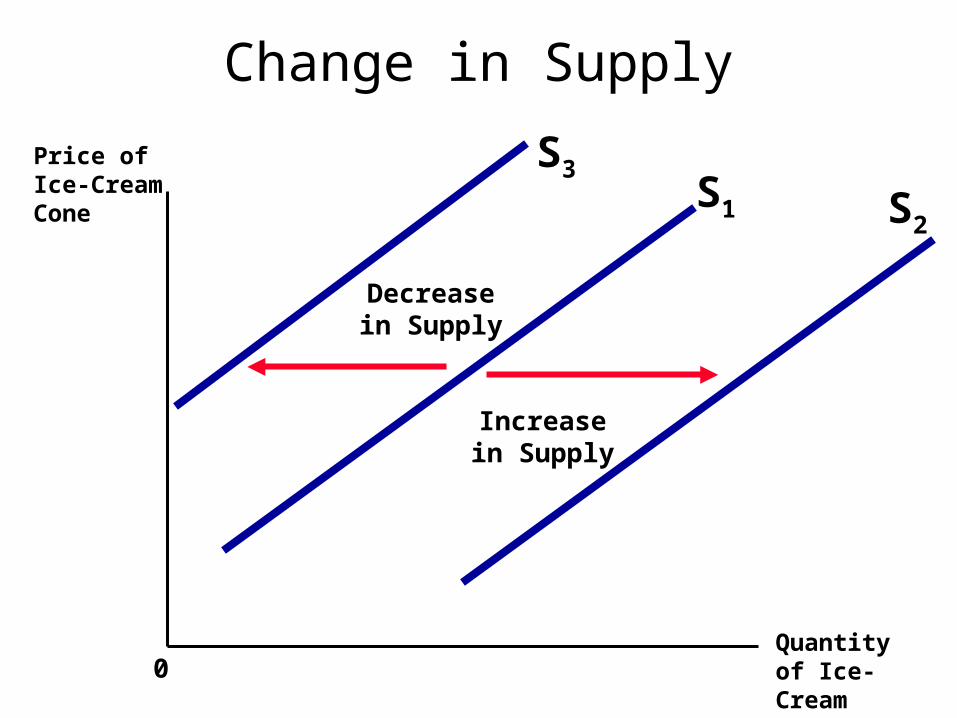

Change in Supply

Price of Ice-Cream Cone

Quantity of Ice-Cream Cones

0

S1 S2

S3

Increase in Supply

Decrease in Supply

Change in Supply

A shift in the supply curve, either to the left or right.

Caused by a change in a determinant other than price.

Factors that can cause a change in supply:

Changes in input prices. Changes in technology. Changes in prices of other goods that the seller

could supply. Changes in expectation and other factors.

How would the supply of personal computers be affected by:

A decline in the prices of a computer component. A faster method for assembling computers is

developed. Dell Corporation goes out of business. The price of personal computers declines.

Equilibrium Equilibrium is the state of balance between

opposing forces. In equilibrium, the system is in a state of rest

in that there is no tendency for change. In economics, there is an equilibrium when

economic forces are in balance so that economic variables have no tendency to change.

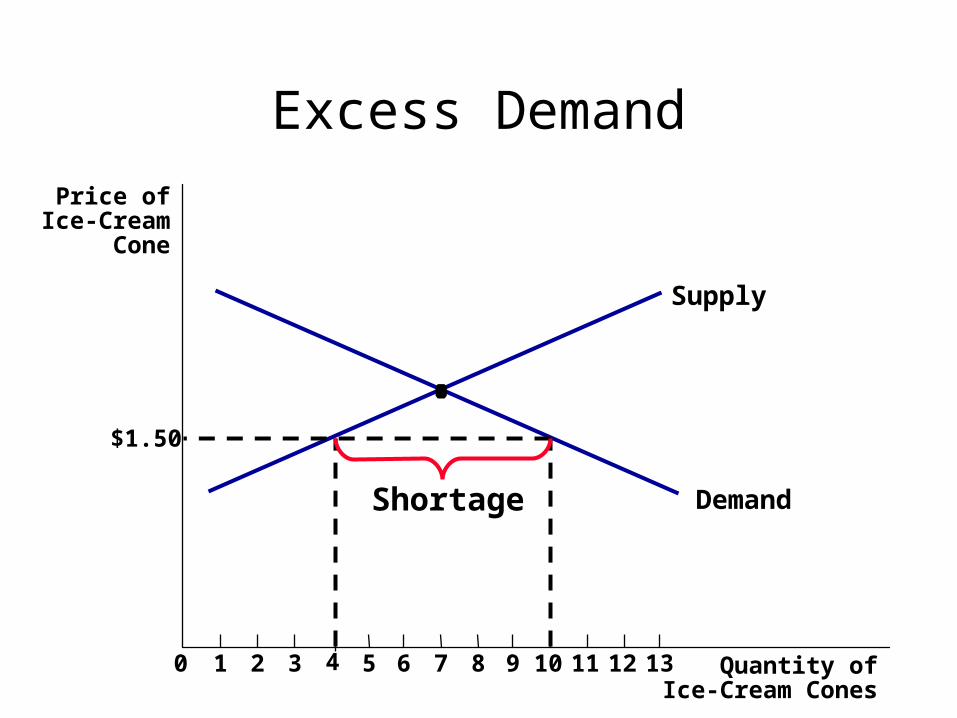

Excess Demand

Quantity ofIce-Cream Cones

Price ofIce-Cream

Cone

0 1 2 3 4 5 6 7 8 9 10 11 12 13

Supply

Demand

$1.50

Shortage

There is a shortage (excess demand) when the quantity demanded exceeds the quantity supplied.

A shortage will result in upward pressure on price.

Price of Ice-Cream Cone

Quantity of Ice-Cream Cones

21 3 4 5 6 7 8 9 10

12110

$3.002.50

2.00

1.501.00

0.50

Supply

Demand

Surplus

Excess Supply

There is a surplus (excess supply) when the quantity demanded is less than the quantity supplied.

A surplus will result in downward pressure on price.

Supply

Demand

Price of Ice-Cream Cone

Quantity of Ice-Cream Cones

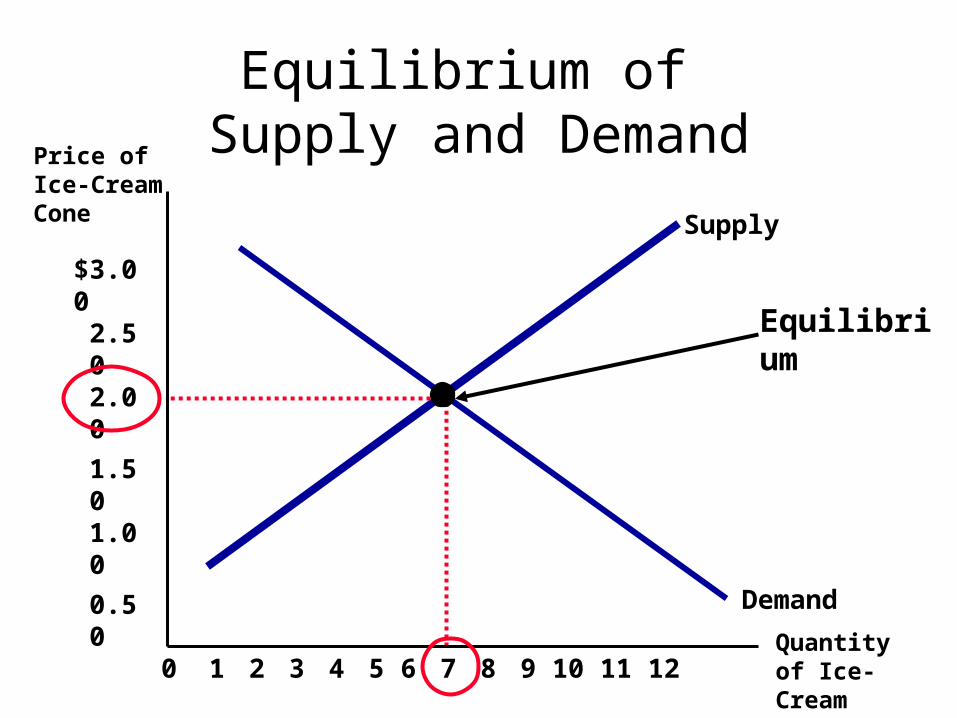

Equilibrium of Supply and Demand

21 3 4 5 6 7 8 9 10 12110

$3.002.502.00

1.501.00

0.50

Equilibrium

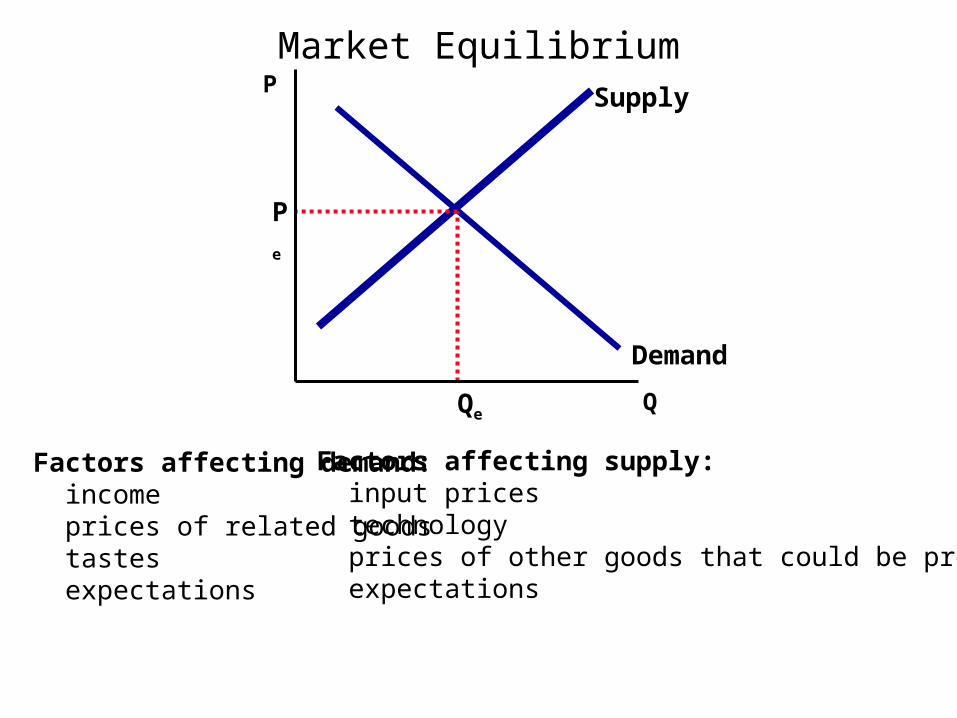

A market equilibrium exists when the price of a good is such that the quantity demanded equals the quantity supplied.

In equilibrium, the price and number of units traded will have no tendency to change.

Market EquilibriumSupply

Demand

P

QQe

Pe

Factors affecting demand: income prices of related goods tastes expectations

Factors affecting supply: input prices technology prices of other goods that could be produced expectations

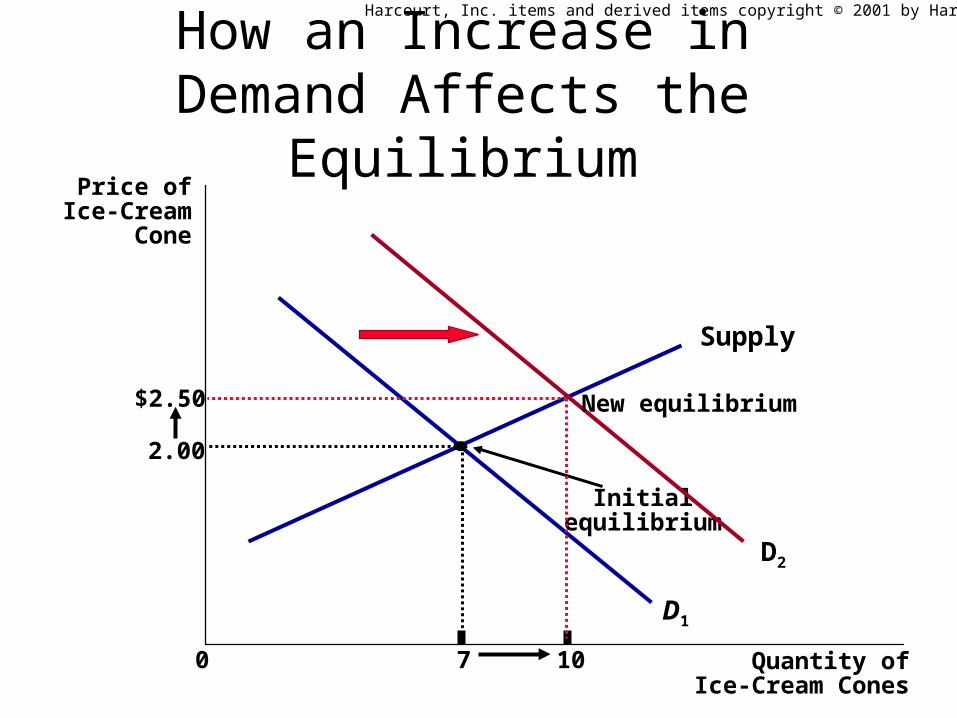

How an Increase in Demand Affects the Equilibrium

Price ofIce-Cream

Cone

2.00

0 7 Quantity ofIce-Cream Cones

Supply

Initialequilibrium

D1

D2

$2.50

10

New equilibrium

Harcourt, Inc. items and derived items copyright © 2001 by Harcourt, Inc.

Q

PD1 S

P1

Q1

Effect of an increase in demandwith supply unchanged

equil.demandeffect

Supplyeffect

neteffect

quantity up -- upprice up -- up

D2

P2

Q2 Q3

A. An increase in demand, ceteris paribus, will result in increases in both the equilibrium price and the equilibrium quantity.

Q

PD1 S

P1

Q1

Effect of an decrease in demandwith supply unchanged

equil.demandeffect

Supplyeffect

neteffect

quantity down -- downprice down -- down D5

P4

Q4Q5

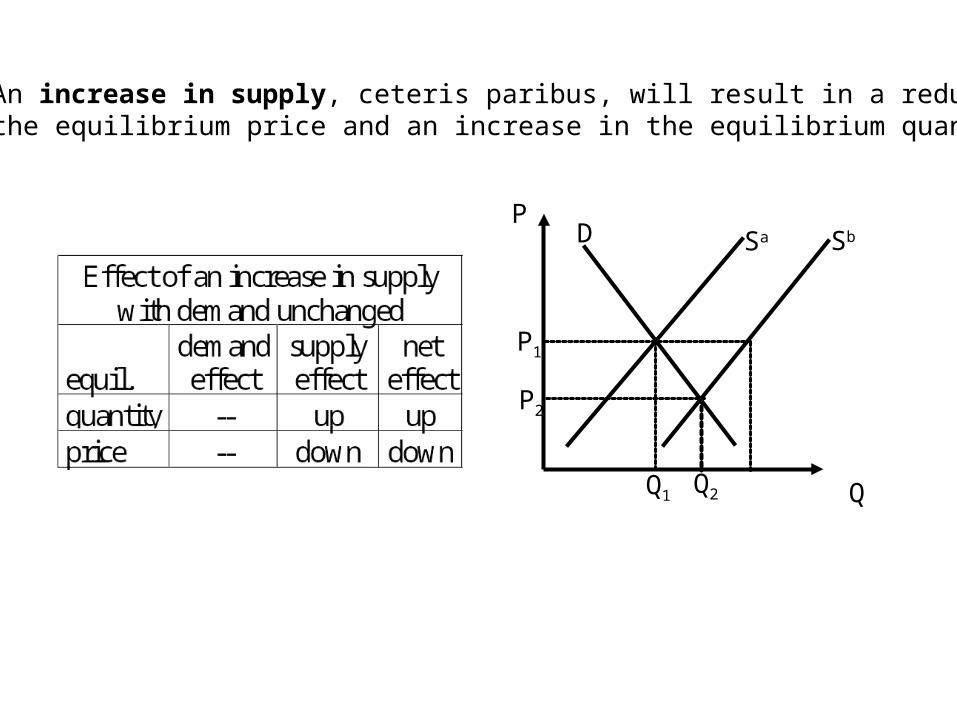

Q

PD Sa

P1

Q1 Q2

P2

Sb

C. An increase in supply, ceteris paribus, will result in a reductionin the equilibrium price and an increase in the equilibrium quantity.

Q

PD1 S1

P1

Q1

D2

P2

Q3

S2

Q

PD1 S1

P1

Q1

D2

P2

Q3

S2