the chinese economy in transition --challenges and ... · the chinese economy in transition...

TRANSCRIPT

The Chinese Economy in Transition --Challenges and Opportunities

Lawrence J. Lau, Ph. D. Ralph and Claire Landau Professor of Economics, The Chinese Univ. of Hong Kong

and Kwoh-Ting Li Professor in Economic Development, Emeritus, Stanford University

2013 Primavera Investor Conference

Beijing, 21st October 2013

Tel: (852)3550-7070; Fax: (852)2104-6938 Email: [email protected]; WebPages: www.igef.cuhk.edu.hk/ljl

*All opinions expressed herein are the author’s own and do not necessarily reflect the views of any of the organisations with which the author is affiliated.

2

Introduction The recent slowdown in the rate of growth of the Chinese

economy should be viewed as a positive development. After all, it is still above 7.5%.

The Chinese Government leaders aim to change the model of economic growth from (1) export and investment-led to consumption-led; and (2) from tangible inputs-driven to innovation-driven.

Will the Chinese economy be able to make these changes smoothly and successfully?

Yes, but it will take time.

3

Export-Led Growth There is a common mis-impression that the Chinese

economy is highly dependent on exports, and in particular, on its export surpluses, as a source of growth.

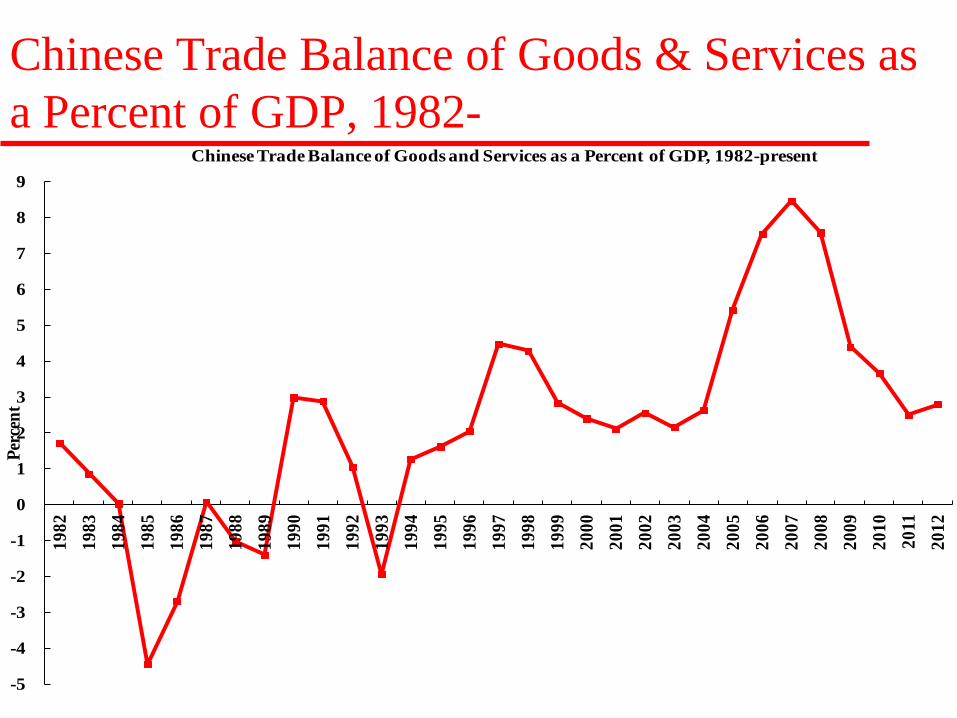

The facts are that China only began to have a significant trade surplus vis-a-vis the World in 2005, whereas the Chinese economy has been growing at an average real rate of almost 10 percent per annum since 1978.

It should therefore be clear that the trade surplus could not have been an important source of growth for the Chinese economy during the past three decades. Chinese economic growth does not depend on the Chinese trade surpluses.

4

Export-Led Growth In fact, Chinese economic growth has not been export-led

for quite some time now. First, China no longer has a large trade surplus. Second, Chinese exports have a low domestic-value-added

content. Third, export-oriented labour-intensive light manufacturing

has been relocating from China to other economies such as Bangladesh, Cambodia, Indonesia, Vietnam and even Myanmar where the wage rates are lower.

It is a goal in the Twelfth Five-Year (2011-2015) Plan for China to achieve balanced international trade.

Going forward, the gross value of exports may decline (they have already been declining in Renminbi terms) even as the domestic value-added content rises.

Chinese Trade Balance of Goods & Services as a Percent of GDP, 1982-

5 -5

-4

-3

-2

-1

0

1

2

3

4

5

6

7

8

9

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Perc

ent

Chinese Trade Balance of Goods and Services as a Percent of GDP, 1982-present

6

Export-Led Growth China both saves too much and invests too much. However,

the excessive savings and excessive investments were in approximate balance and hence there was little or no excess savings to be exported (in the form of a trade surplus).

China did not have a significant trade surplus vis-a-vis the World until 2005, even though it had had a large trade surplus vis-a-vis the United States.

Since 2008, the Chinese savings-investment gap has once again narrowed, resulting in a large reduction in the Chinese trade surplus relative to its GDP. The Chinese trade surplus has declined to 2% of its GDP by the end of 2012 and is expected to decline further during the next couple of years, reaching essentially balanced international trade by perhaps 2015.

7

Export-Led Growth The domestic value-added content of Chinese exports is no

more than 30 percent, that is: for every dollar of Chinese goods exported, less than 30 cents, on average, consist of domestic value-added. The rest consists of imported raw materials, intermediate goods, components, parts, semi-finished goods, etc. The domestic value-added percentage is even less for the so-called “Processing and Assembly” exports, which at one time accounted for more than half of total Chinese exports.

For example, Apple’s I-Pad, which is assembled in China, with an export value of approximately US$500, generates a value-added in China of only US$15.

8

Export-Led Growth In any case, it is unlikely that Chinese exports can resume

its rapid growth any time soon with the U.S. and European economies in recession. This is a principal reason for the shift in China from a policy of promotion of exports to a policy of promotion of internal demand, which is the only way to ensure sustained and sustainable economic growth in China. Such a policy shift has been incorporated in the Twelfth Five-Year Plan.

Chinese National Savings and Gross Domestic Investment as Percents of GDP

9 0

10

20

30

40

50

60

1952

1953

1954

1955

1956

1957

1958

1959

1960

1961

1962

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Perc

ent

Chinese National Savings and Gross Domestic Investment as a Percent of GDP since 1952

Savings Rate Investment Rate

10

Investment-Led Growth The national saving rate of China remains high—above

40%. The high national savings rate in turn had led to a high

investment rate, with the investment financed mostly with domestic savings.

The real rate of growth of gross fixed investment is around 20% per annum, much higher than the real rate of growth of household or personal consumption.

Chinese dependence on foreign capital inflows—whether direct investment or portfolio investment, is low. It has therefore insulated the Chinese economy from external disturbances. The existence of capital control has also helped to insulate the Chinese economy.

11 11

Monthly Rates of Growth of Chinese Fixed Assets Investment, Y-o-Y

0

10

20

30

40

50

60

Jan-

00Ap

r-00

Jul-0

0Oc

t-00

Jan-

01Ap

r-01

Jul-0

1Oc

t-01

Jan-

02Ap

r-02

Jul-0

2Oc

t-02

Jan-

03Ap

r-03

Jul- 0

3Oc

t-03

Jan-

04Ap

r-04

Jul-0

4Oc

t-04

Jan-

05Ap

r-05

Jul-0

5Oc

t-05

Jan-

06Ap

r-06

Jul-0

6Oc

t-06

Jan-

07Ap

r-07

Jul-0

7Oc

t -07

Jan-

08Ap

r-08

Jul-0

8Oc

t-08

Jan-

09Ap

r-09

Jul-0

9Oc

t-09

Jan-

10Ap

r-10

Jul-1

0Oc

t-10

Jan-

11Ap

r-11

Jul-1

1Oc

t-11

Jan-

12Ap

r-12

Jul-1

2Oc

t-12

Jan -

13Ap

r-13

Jul-1

3

Perc

ent

Monthly Rates of Growth of Chinese Fixed Assets Investment since 2000, Year-over-Year

12

Consumption-Led Growth The real rate of growth of household consumption has been

higher than the rate of growth of real GDP but not high enough to change the national saving rate.

Without a significant increase in the household income, household consumption is unlikely to increase at a significantly higher rate—it has already been increasing at 150% if the rate of growth of real GDP.

A potential source of a significant increase in household income as well as government revenue is a requirement for the publicly listed Chinese enterprises to declare and distribute significant cash dividends to their shareholders, which including households and the government. This should also help to reduce non-essential and non-productive investment on the part of publicly listed Chinese enterprises.

13

Consumption-Led Growth There is, however, significant room for the expansion of

public consumption, or consumption of public goods, financed by the government, for example, the cleaning up of air and water and the environment in general, which will require both new investments and continuing public expenditures.

The financing or provision of public goods such as education, health care, clean environment, by the government can greatly increase the welfare of the average people. It is also an effective means for redistribution, and for narrowing the degree of inequality of the effective income distribution, say between the urban and the rural areas.

14

Consumption-Led Growth Chinese household consumption is sometimes viewed as a

potential sustainable source of growth of Chinese domestic aggregate demand.

Chinese household consumption has actually been growing quite rapidly, as indicated by the double-digit monthly year-over-year rates of growth of real retail sales since the first quarter of 2009.

15 15

Monthly Rates of Growth of Chinese Real Retail Sales, Y-o-Y

0

5

10

15

20

25

30

35

Jan-

00Ap

r-00

Jul-0

0Oc

t-00

Jan-

01Ap

r-01

Jul-0

1Oc

t-01

Jan-

02Ap

r-02

Jul-0

2Oc

t-02

Jan-

03Ap

r-03

Jul-0

3Oc

t-03

Jan-

04Ap

r-04

Jul-0

4Oc

t-04

Jan-

05Ap

r-05

Jul-0

5Oc

t-05

Jan-

06Ap

r-06

Jul-0

6Oc

t-06

Jan-

07Ap

r-07

Jul-0

7Oc

t-07

Jan-

08Ap

r-08

Jul-0

8Oc

t-08

Jan-

09Ap

r-09

Jul-0

9Oc

t-09

Jan-

10Ap

r-10

Jul-1

0Oc

t-10

Jan-

11Ap

r-11

Jul-1

1Oc

t-11

Jan-

12Ap

r-12

Jul- 1

2Oc

t-12

Jan-

13Ap

r-13

Jul-1

3

Perc

ent

Monthly Rates of Growth of Chinese Real Retail Sales since 2000, Year-over-Year

16

Consumption-Led Growth The Chinese household saving rate, as distinct from the

much higher national saving rate, currently stands at approximately 30% (for urban households).

However, the consumption-savings behaviour of Chinese households on the Mainland today appears to be little different from ethnic Chinese households in Hong Kong and Taiwan at the same level of per capita household income, with an average saving rate of urban households of approximately 30%. Thus, the Chinese household saving rate is not likely to fall significantly in the foreseeable future. Increases in consumption must therefore come from increases in household income rather than decreases in the household saving rate.

Saving Rates of Urban and Rural Households

17 0

5

10

15

20

25

30

35

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Perc

ent

Savings Rates of Chinese Urban and Rural Households

Household Savings Rates: Rural

Household Savings Rates: Urban

18

Consumption-Led Growth Chinese household consumption can be expected to increase

significantly faster than GDP only if Chinese household (disposable) income as a share of GDP rises significantly. There are structural reasons why this is unlikely to occur in the short run even though in the longer run, the income share of labour, which currently stands at around 50%, is likely to rise in China.

Continuing Chinese economic growth beyond 2013 will therefore have to depend mostly on the growth of internal demand and not on exports, and, as analysed above, not on the growth of household consumption per se in the absence of a significant sustained increase in the share of household income in GDP.

Household income can be increased through wage increases but also through increases in the cash dividend payouts from publicly listed state-owned enterprises, as mentioned above. Recently, the Chinese Government has called for an increased cash dividend payouts from state-owned enterprises.

19

Consumption-Led Growth Increased cash dividend payouts have many advantages in addition to

increasing household income and thereby household consumption. They increase government revenue, both directly, as the government

is a major shareholder in many publicly listed enterprises and will receive the increased cash dividends, and indirectly, through the increased individual income taxes collected on the cash dividends paid to the other shareholders. The increased government revenue can in turn be used to increase public consumption—e.g., the provision of public services such as education and health care, the preservation and restoration of the environment, etc.

An increased cash dividend payout by the state-owned enterprises reduces their excess retained earnings so that they can no longer make investments at will—it will have to apply for loans and hence their investment projects will have to be justified to and evaluated by the lenders. This may help to reduce over-investment in certain industries.

20

Consumption-Led Growth Increased cash dividend payouts may make long-term

holding of shares more attractive and may attract a different breed of investors. It will encourage investors to hold their shares longer and hence indirectly improve corporate governance as only long-term shareholders pay any attention to corporate governance.

An increased cash dividend payout provides a support level for the price of the shares of a publicly listed enterprise. Thus, the government does not need to worry as much about supporting the market.

21

Consumption-Led Growth However, the high Chinese national saving rate is not due to an

exceptionally high household saving rate. In fact, the Chinese household saving rate is not significantly different from those of ethnically Chinese households in Hong Kong and Taiwan, both market economies and where the social safety nets are not completely adequate, particularly in Hong Kong.

The high Chinese national saving rate is due to the much lower share of GDP received by households as income; in particular, the share of labor is low in China, currently less than 50% of GDP, compared to approximately 70% in the developed economies of the World. The households’ share of national income is not much higher than 50%. Even if the households consume all of their income and do not save at all, household or personal consumption cannot be much more than 50% of GDP. The Chinese household saving rate is currently approximately 30%.

22

Consumption-Led Growth It is also due to the much higher Chinese corporate saving

rates—Chinese enterprises, state-owned as well as non-state-owned, typically reinvest their earnings and distribute little or no cash dividends to their shareholders. (For privately owned enterprises, this is done in part to avoid personal income taxation as cash dividends are taxed at a flat 20% rate.) Thus, the enterprise saving rate out of enterprise income (after taxes) is almost 100%.

The high Chinese national saving rate is thus the result of a weighted average between the household saving rate and the high enterprise saving rate (with the government saving rate—the budget surplus (deficit) as a percentage of GDP—being relatively insignificant until more recently).

23

Tangible Inputs-Driven Growth There will continue to be adequate investment in tangible

capital. The population is aging, and the working age population has

been predicted to fall. However, this is somewhat artificial. If retirement age is raised to 65 (perhaps with the requirement that no one above age 60 can hold senior administrative positions), there should continue to be sufficient labour over the next five to ten years.

The “one-child” population policy may be modified in the longer run.

24

Innovation-Driven Growth Innovation-driven growth depends on investments in

intangible capital such as human capital and R&D capital. China has been increasing its investment in R&D in recent

years, but it still lags behind the U.S. and other economies significantly, certainly as a percent of its GDP.

25

R&D Expenditure and Its Share of GDP: A Comparison of China and the U.S.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

0

50

100

150

200

250

300

350

400

450

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Perc

ent

USD

billio

ns

R&D Expenditure and Its Share of GDP, A Comparison of China and the U.S.

U.S. R&D Expenditure

Chinese R&D Expenditure

U.S.R&D Expenditure as a Percentage of GDP

Chinese R&D Expenditure as a Percentage of GDP

R&D Expenditures as a Ratio of GDP: G-7 Countries, 4 East Asian NIES & China

26

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Perc

ent

R&D Expenditures as a Percentage of GDP: G-7 Countries, 4 East Asian NIEs and China

U.S. Japan W. Germany U.K.

France Canada Italy South Korea

Singapore Taiwan China Hong Kong

27

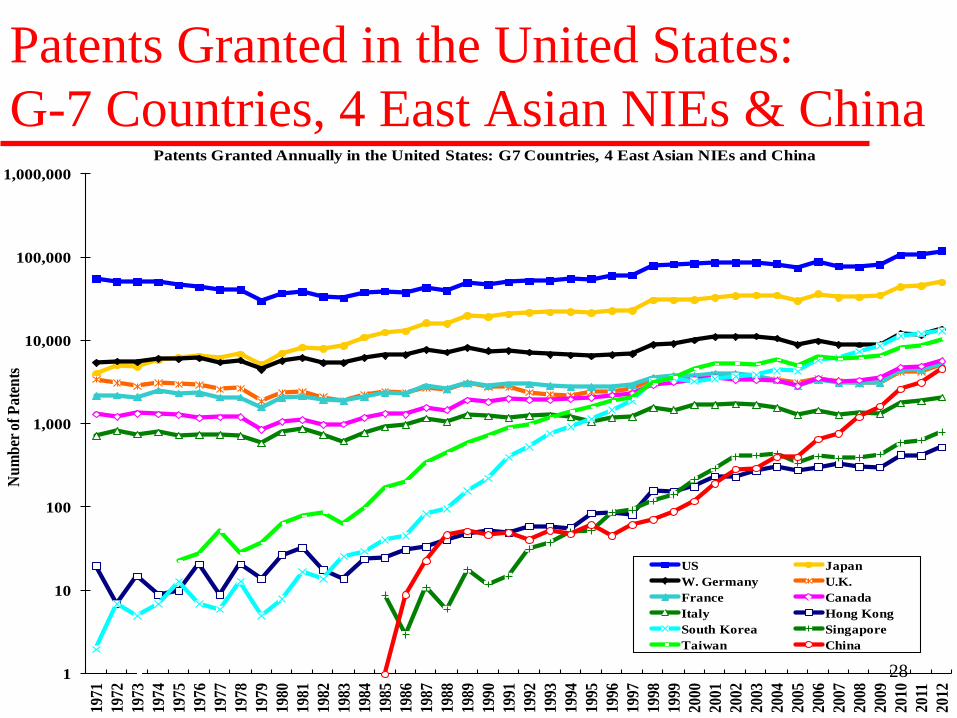

Innovation-Driven Growth One indicator of the potential for technical progress

(national innovative capacity) is the number of patents created each year. In the following chart, the number of patents granted in the United States each year to the nationals of different countries, including the U.S. itself, over time is presented.

The U.S. is the undisputed champion over the past forty years, with 121,026 patents granted in 2012, followed by Japan, with 50,677. The number of patents granted to Chinese applicants each year has increased from 1 in 1985 to 4,637 in 2012.

Patents Granted in the United States: G-7 Countries, 4 East Asian NIEs & China

28 1

10

100

1,000

10,000

100,000

1,000,000

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Num

ber o

f Pat

ents

Patents Granted Annually in the United States: G7 Countries, 4 East Asian NIEs and China

US JapanW. Germany U.K.France CanadaItaly Hong KongSouth Korea SingaporeTaiwan China

29

Innovation-Driven Growth The stock of R&D capital, defined as the cumulative past

real investment in R&D less depreciation of 10% per year, can be shown to have a direct causal relationship to the number of patents granted (see the following chart, in which the annual number of patents granted is plotted against the R&D capital stock of that year for each country or region).

The chart shows that the higher the stock of R&D capital of an economy, the higher is the number of patents granted to it by the U.S.

Patents Granted in the United States and R&D Capital Stocks, Selected Economies

The Number of U.S. Patents Granted Annually vs. R&D Capital Stocks

1

10

100

1,000

10,000

100,000

1,000,000

0 1 10 100 1,000 10,000Billions of 2005 Constant U.S. Dollars

Num

ber o

f Pat

ents

USJapanWest GermanyUKFranceCanadaItalySouth KoreaSingaporeChinaHong KongTaiwan

30

31

Innovation-Driven Growth The huge potential domestic market of 1.34 billion

consumers not only enables the realisation of economies of scale but also greatly enhances the productivity of intangible capital (e.g., R&D capital, goodwill). The fixed research and development costs of a new product or process can be easily amortised over a large market. The benefits of investment in goodwill, e.g., brand-building, are also much greater in a large market.

The huge potential domestic market also enables active Chinese participation in the setting of product and technology standards and sharing of the benefits of such standard-setting.

32

Innovation-Driven Growth However, innovation-driven growth also depends on

competition. Monopolies are not very good in innovation, or not very good in making full use of their innovation.

In order to encourage innovation, China also needs to protect intellectual property rights vigorously.

33

Sources of Sustainable Growth of Aggregate Demand The possible areas that have the potential of generating

sustainable increases in aggregate demand, in addition to household consumption and public infrastructural investment (e.g., high speed railroads, mass-transit systems, power plants, etc.), include:

(1) Acceleration of urbanisation; (2) Residential housing; (3) Education and health care and the application of high

technology in these sectors; and (4) Conservation of energy, environmental protection and

preservation (clean air and water), and promotion of the green economy.

34

The Partial De-Coupling Hypothesis Throughout the 2007-2009 global financial crisis, as well as

the subsequent European sovereign debt crisis, the East Asian economies and the economies of the BRICS countries (Brazil, Russia, India, China and South Africa) continued to do reasonably well. China, in particular, has been able to maintain its real rate of growth above 7.5% since 2007, lending credence to the “Partial De-Coupling Hypothesis”, that is, the Chinese and East Asian economies can continue to grow, albeit at slower rates, even as the U.S. and European economies go into economic recession.

This partial de-coupling can occur because of the gradual shift of the economic centre of gravity of the World from the United States and Western Europe to Asia (including both East Asia and South Asia) over the past three decades.

35

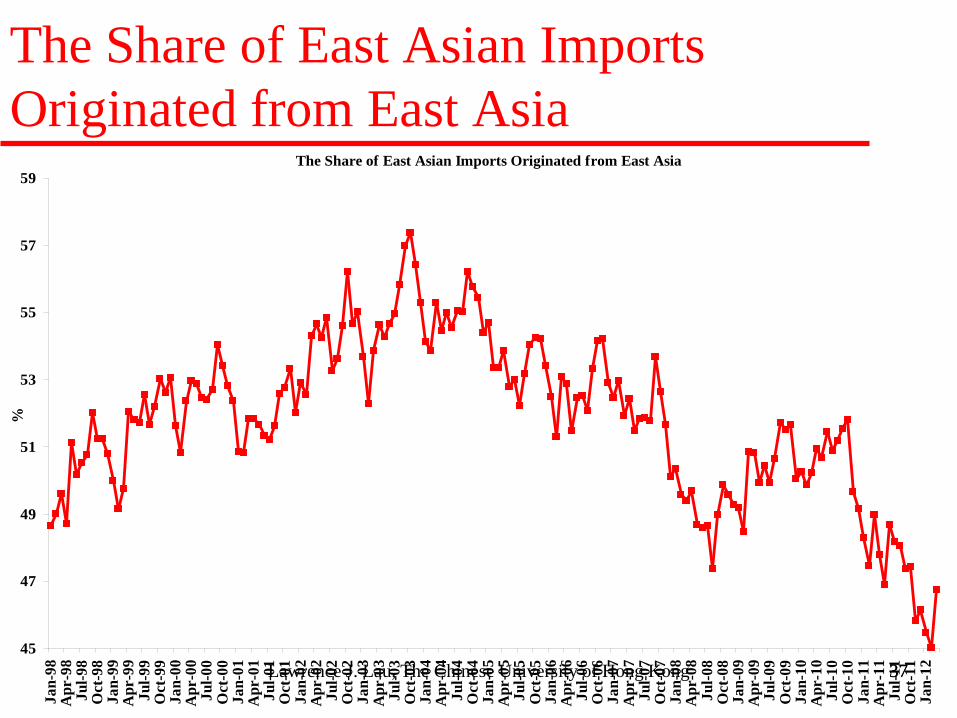

The Partial De-Coupling Hypothesis A particularly interesting development is the rise in intra-

East Asian international trade. The share of East Asian trade destined for East Asia has risen to over 50% in the past decade. This is a sea-change compared to 30 years ago when most of the East Asian exports was destined for either the United States or Western Europe.

Similarly, the share of East Asian imports originated from East Asia has remained above 45%.

36 36

The Share of East Asian Exports Destined for East Asia

The Share of East Asian Exports Destined for East Asia

35

37

39

41

43

45

47

49

51

53

Jan-

98A

pr-9

8Ju

l-98

Oct

-98

Jan-

99A

pr-9

9Ju

l-99

Oct

-99

Jan-

00A

pr-0

0Ju

l-00

Oct

-00

Jan-

01A

pr-0

1Ju

l-01

Oct

-01

Jan-

02A

pr-0

2Ju

l-02

Oct

-02

Jan-

03A

pr-0

3Ju

l-03

Oct

-03

Jan-

04A

pr-0

4Ju

l-04

Oct

-04

Jan-

05A

pr-0

5Ju

l-05

Oct

-05

Jan-

06A

pr-0

6Ju

l-06

Oct

-06

Jan-

07A

pr-0

7Ju

l-07

Oct

-07

Jan-

08A

pr-0

8Ju

l-08

Oct

-08

Jan-

09A

pr-0

9Ju

l-09

Oct

-09

Jan-

10A

pr-1

0Ju

l-10

Oct

-10

Jan-

11A

pr-1

1Ju

l-11

Oct

-11

Jan-

12

%

37 Lawrence J. Lau, The Chinese University of Hong Kong 37

The Share of East Asian Imports Originated from East Asia

The Share of East Asian Imports Originated from East Asia

45

47

49

51

53

55

57

59

Jan-

98A

pr-9

8Ju

l-98

Oct

-98

Jan-

99A

pr-9

9Ju

l-99

Oct

-99

Jan-

00A

pr-0

0Ju

l-00

Oct

-00

Jan-

01A

pr-0

1Ju

l-01

Oct

-01

Jan-

02A

pr-0

2Ju

l-02

Oct

-02

Jan-

03A

pr-0

3Ju

l-03

Oct

-03

Jan-

04A

pr-0

4Ju

l-04

Oct

-04

Jan-

05A

pr-0

5Ju

l-05

Oct

-05

Jan-

06A

pr-0

6Ju

l-06

Oct

-06

Jan-

07A

pr-0

7Ju

l-07

Oct

-07

Jan-

08A

pr-0

8Ju

l-08

Oct

-08

Jan-

09A

pr-0

9Ju

l-09

Oct

-09

Jan-

10A

pr-1

0Ju

l-10

Oct

-10

Jan-

11A

pr-1

1Ju

l-11

Oct

-11

Jan-

12

%

38

The Partial De-Coupling Hypothesis Any doubt that the Chinese economy can be partially de-

coupled from the World economy should be resolved by an examination of the following three charts. Even though Chinese exports and imports fluctuate like those of all the other East Asian economies, the rate of growth of real GDP of the Chinese economy has been relatively stable compared to those of the other East Asian economies.

39 39

Quarterly Rates of Growth of Exports of Goods: Selected East Asian Economies

-60

-50

-40

-30

-20

-10

0

10

20

30

40

50

60

70

Q1 19

97Q2

1997

Q3 19

97Q4

1997

Q1 19

98Q2

1998

Q3 19

98Q4

1998

Q1 19

99Q2

1999

Q3 19

99Q4

1999

Q1 20

00Q2

2000

Q3 20

00Q4

2000

Q1 20

01Q2

2001

Q3 20

01Q4

2001

Q1 20

02Q2

2002

Q3 20

02Q4

2002

Q1 20

03Q2

2003

Q3 20

03Q4

2003

Q1 20

04Q2

2004

Q3 20

04Q4

2004

Q1 20

05Q2

2005

Q3 20

05Q4

2005

Q1 20

06Q2

2006

Q3 20

06Q4

2006

Q1 20

07Q2

2007

Q3 20

07Q4

2007

Q1 20

08Q2

2008

Q3 20

08Q4

2008

Q1 20

09Q2

2009

Q3 20

09Q4

2009

Q1 20

10Q2

2010

Q3 20

10Q4

2010

Q1 20

11Q2

2011

Q3 20

11Q4

2011

Q1 20

12Q2

2012

Q3 20

12Q4

2012

Q1 20

13

Annu

alize

d Per

cent

per

annu

m

Year-over-Year Quarterly Rates of Growth of Exports of Goods in US$ (Percent)

China,P.R.:Hong Kong IndiaIndonesia KoreaMalaysia PhilippinesSingapore ThailandChina,P.R.: Mainland JapanTaiwan Prov.of China

40 40

Quarterly Rates of Growth of Imports of Goods: Selected East Asian Economies

-60

-50

-40

-30

-20

-10

0

10

20

30

40

50

60

70

80

90

Q1 19

97Q2

1997

Q3 19

97Q4

1997

Q1 19

98Q2

1998

Q3 19

98Q4

1998

Q1 19

99Q2

1999

Q3 19

99Q4

1999

Q1 20

00Q2

2000

Q3 20

00Q4

2000

Q1 20

01Q2

2001

Q3 20

01Q4

2001

Q1 20

02Q2

2002

Q3 20

02Q4

2002

Q1 20

03Q2

2003

Q3 20

03Q4

2003

Q1 20

04Q2

2004

Q3 20

04Q4

2004

Q1 20

05Q2

2005

Q3 20

05Q4

2005

Q1 20

06Q2

2006

Q3 20

06Q4

2006

Q1 20

07Q2

2007

Q3 20

07Q4

2007

Q1 20

08Q2

2008

Q3 20

08Q4

2008

Q1 20

09Q2

2009

Q3 20

09Q4

2009

Q1 20

10Q2

2010

Q3 20

10Q4

2010

Q1 20

11Q2

2011

Q3 20

11Q4

2011

Q1 20

12Q2

2012

Q3 20

12Q4

2012

Q1 20

13

Annu

alize

d Per

cent

per

annu

m

Year-over-Year Quarterly Rates of Growth of Imports of Goods in US$ (Percent)

China,P.R.:Hong Kong IndiaIndonesia KoreaMalaysia PhilippinesSingapore ThailandChina,P.R.: Mainland JapanTaiwan Prov.of China

41 41

Quarterly Rates of Growth of Real GDP, Y-o-Y: Selected East Asian Economies

-20

-15

-10

-5

0

5

10

15

20

Q1 19

94Q2

1994

Q3 19

94Q4

1994

Q1 19

95Q2

1995

Q3 19

95Q4

1995

Q1 19

96Q2

1996

Q3 19

96Q4

1996

Q1 19

97Q2

1997

Q3 19

97Q4

1997

Q1 19

98Q2

1998

Q3 19

98Q4

1998

Q1 19

99Q2

1999

Q3 19

99Q4

1999

Q1 20

00Q2

2000

Q3 20

00Q4

2000

Q1 20

01Q2

2001

Q3 20

01Q4

2001

Q1 20

02Q2

2002

Q3 20

02Q4

2002

Q1 20

03Q2

2003

Q3 20

03Q4

2003

Q1 20

04Q2

2004

Q3 20

04Q4

2004

Q1 20

05Q2

2005

Q3 20

05Q4

2005

Q1 20

06Q2

2006

Q3 20

06Q4

2006

Q1 20

07Q2

2007

Q3 20

07Q4

2007

Q1 20

08Q2

2008

Q3 20

08Q4

2008

Q1 20

09Q2

2009

Q3 20

09Q4

2009

Q1 20

10Q2

2010

Q3 20

10Q4

2010

Q1 20

11Q2

2011

Q3 20

11Q4

2011

Q1 20

12Q2

2012

Q3 20

12Q4

2012

Q1 20

13

Annu

alize

d Rat

es in

Per

cent

Quarterly Rates of Growth of Real GDP, Year-over-Year, Selected East Asian Economies

China,P.R.:Hong Kong IndiaIndonesia KoreaMalaysia PhilippinesSingapore ThailandChina,P.R.: Mainland JapanTaiwan Prov.of China

42

Projections of the Future If current trends continue, with the U.S. economy

recovering slowly but surely, Chinese real GDP is projected to catch up to U.S. real GDP in approximately 15 years’ time--around 2028, at which time both Chinese and U.S. real GDP will exceed US$28 trillion (in 2012 prices), almost four times the current Chinese GDP. (Bear in mind that in the meantime, the U.S. economy will also continue to grow, albeit at rates lower than those of the Chinese economy.)

By this time, China and the U.S. will each account for approximately 15% of World GDP.

Lawrence J. Lau 43 Lawrence J. Lau 43

Actual and Projected Chinese and U.S. Real GDPs and Their Rates of Growth

43

-4

-3

-2

-1

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

-9

-6

-3

0

3

6

9

12

15

18

21

24

27

30

33

36

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

2026

2028

2030

PercentU

SD tr

illio

ns, 2

012

price

s

Actual and Projected Real GDP of China and the U.S. and Their Rates of Growth

Growth Rate of U.S. Real GDP (right scale)Growth Rate of Chinese GDP (right scale)U.S. Real GDPChinese Real GDP

44

Concluding Remarks On the basis of its strong economic fundamentals, China should

be able to continue to grow at an average annual rate of at least 7% for the next couple of decades, more or less independently of what happens in the rest of the World.

Chinese economic growth will be marginally, but not critically, affected by a large decline in its exports, as demonstrated by its experience in the past several years as well as during the 1997-1998 East Asian currency crisis. Thus, it will be able to survive even prolonged economic recessions in the European and U.S. economies.

China will develop into a largely internal-demand driven economy like the United States. International trade and international investment will not have a decisive impact on the Chinese economy.

45

Concluding Remarks Exports as a share of Chinese GDP will probably continue

to decline over time, as befitting a large, continental economy. Chinese international trade will become approximately balanced with the rest of the World.

However, China may well become a net overseas direct as well as portfolio investor over the next decade.

46

Concluding Remarks The long-term sustainable sources of Chinese aggregate

demand will all be internal: urbanisation (building new cities), public infrastructure, mass-transit systems, household and public consumption, residential housing, investment in education and health care, environmental protection and preservation, energy conservation and renewable energy, and the green economy.

Chinese household consumption will rise, as GDP per capita and wage rate rise and the social safety net is gradually perfected. But the national saving rate may remain high for a long time.