the caribbean fine cocoa industry 2013

TRANSCRIPT

Caribbean Fine Cocoa Industry

Vernon Patrick Barrett

The Fine Cocoa Industry – Global (UNCTAD 2010)

Western Hemisphere

• Trinidad & Tobago

• Jamaica

• Grenada

• St Lucia

• Dominica

• Dominican Republic

• Venezuela

• Colombia

• Peru

• Ecuador

• Costa Rica

Rest of World

• Madagascar

• Papua New Guinea

• São Tomé & Príncipe

• Indonesia

Above new entrants – could change market dynamics

2

What is Fine (or Flavoured) Cocoa?

• “Fine” Cocoa is recognised for its unique flavour and colour and is determined by an ICCO panel depending upon consumers and manufacturers – old Criollo and Trinitario varieties (5% of total) Tropical Plant Breeding (A. Charrier 2001)

• “Bulk” Cocoa is grown in large amounts mainly in South America (Brazil) and Africa (Cote d’Ivorie, Ghana, Cameroon)

Fine Cocoa attracts a substantial premium price to bulk cocoa – need to RETAIN this classification in Caribbean where some countries produce ONLY fine cocoa.

3

Jamaican Fine Cocoa Industry

The Jamaican Fine Cocoa Industry

• Brief History

– One of oldest crop exports - from 16th Century

– Sugar slump in mid 19th Century led to cocoa and bananas being actively promoted

– From 20 tons (1874) to 3,500 tons (1925)

– Early 20th century – prices slumped & large farmers exited the industry

– Thereafter, and now, cocoa is mainly in hands of small farmers (90% have less than 5 acres of land)

5

The Jamaican Fine Cocoa Industry

• First Renaissance – 1957 by Hon. Norman W Manley (then Chief Minister)

– Cocoa Marketing Board first then Cocoa Industry Board

– Built 4 Centralized Fermentaries across island

– By late 1960’s

• Distributed 9 million cocoa plants

• Cocoa acreage went from 14,000 to 30,000 acres

• Annual cocoa production averaged about 2,000 tons into 1980’s

However difficulties ensued from the 1990’s onwards

6

The Jamaican Fine Cocoa Industry

• Present Day Situation

– Still present across the island from east, central and west (only 3 or 4 parishes cannot grow cocoa)

– Thousands of small farmers grow it (< 5 acres)

– Mainly inter-cropping with cash crops

– Very few large farmers or cocoa mono-cropping

– Distributed Production but Centralised Processing

• Only 2 active Fermentaries remain (from 4 original)

7

The Jamaican Fine Cocoa Industry

• Structure of Industry

– Model of Operation

• Distributed Growing but Centralised Processing

– Advantages

• Economies of Scale - collection, processing, marketing

• Social Network support for rural communities

• Economic with centralised Quality Control

• Volume to negotiate with external buyers

• Visible pricing to farmers

• Diversified risk against hurricanes etc

8

The Jamaican Fine Cocoa Industry

The Jamaican Fine Cocoa Industry

The Jamaican Fine Cocoa Industry

• Required Key Success Factors - Interdependency – Trust and good working relationship between Cocoa Board

(sole buyer) and cocoa farmers

– Proper functioning of inter-linkages such as Lead Cocoa Agents, Cocoa Collectors, etc. in the network

– A critical mass of participation by small farmers to supply Cocoa Board processing plants

– Efficient and well functioning Cocoa Board • Proactive; investing for future;

• Good relationship management with farmers (customers)

• Honesty, fair play, competent staff

11

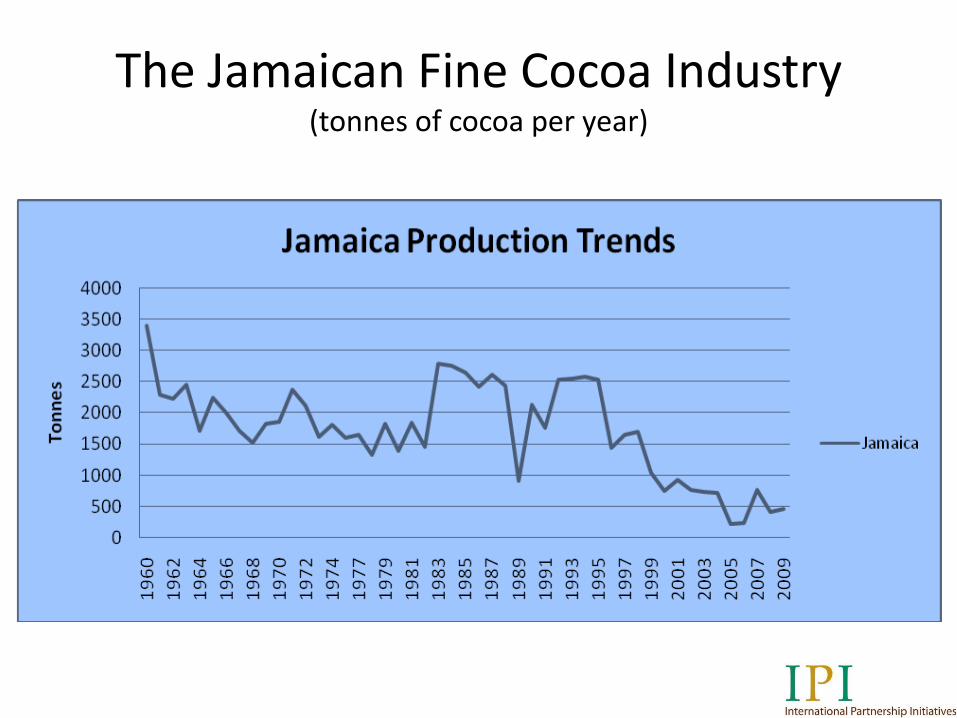

The Jamaican Fine Cocoa Industry (tonnes of cocoa per year)

12

The Jamaican Fine Cocoa Industry

• Current Issues - I

– Declining volumes of cocoa output (now reversing)

– Ageing demographics of rural farmer

– Farming not seen as a viable business

– Urban migration; stigma of farming re livelihood

– Competing crops with quicker returns

– Low price paid to small farmer by monopolistic buyer (but now improving)

– Informal land tenure (who owns what legally)

13

The Jamaican Fine Cocoa Industry

• Current Issues - II

– Loss of cocoa know-how across the generations

– Limited applications of technological innovations

• GIS /GPS; mobile telephony; transportation

– Cumulative lack of investment over the years

– Loss / Ageing of cocoa trees / Trees growing wild

– More extreme weather - possible low pollination

Host of Issues – is industry structured to address change in a pro-active manner?

14

The Jamaican Fine Cocoa Industry

• Current Status

– Government divesting its interest in Board and wants to liberalise market (ongoing new model)

– Significant EU Funding for project to rehabilitate 2,000 acres of cocoa (well underway - see Posters outside & CIB team here today)

– USAID support to the industry

– Jamaica Cocoa Farmers Association mobilising (also in attendance)

15

The Jamaican Fine Cocoa Industry

• Current Actions – EU project underway (CIB) – Capacity build the Cocoa Board (people, computers, power tools,

telecoms etc)

– Develop a methodology to rehabilitate the derelict cocoa fields with teams led by Change Agents

– Educate the Farmers in Business and Entrepreneurship (more from Prof Thompson UTT on that in her presentations)

– Use modern technology where beneficial to improve the productivity, efficiency and image of farming – BRING IT INTO THE 21st Century

– Promote the value add end of the value chain – not going to process all the beans immediately but we need to get into this part of the business!!

16

Trinidad & Tobago Fine Cocoa Industry

The Trinidad Fine Cocoa Industry (tonnes of cocoa per year)

18

0

500

1000

1500

2000

2500

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Comparison of Cocoa Industry Structures

TRINIDAD & TOBAGO

• Outside Hurricane Zone

• Several Large Farms (>200 acres) & many medium sized farms

• Complex industry structure of many buyers and traders

• Good cooca varieties research capability CRU

• Cocoa Assns strengthening

JAMAICA

• Multiple Hurricanes & Storms

• Some medium sized farms

• Majority are small farm sizes (2-5 acres)

• Centralised control by Cocoa Board – only buyer

• Need for improved technical capability in cocoa

• One main Cocoa Farmers Assn. JCFA

19

The Trinidad Fine Cocoa Industry

The Trinidad Fine Cocoa Industry

The Tobago Fine Cocoa Industry

The Trinidad Fine Cocoa Industry

• Current Challenges – Stagnating volumes of cocoa production

– Ageing demographics of rural farmer - generational memory loss & success crisis?

– Smaller farmers wanting support / incentives

– Wage inflation – hard to find labour / youth

– How to translate new cocoa varieties into the field (IP?)

– Supporting the small indigenous chocolate processors

– Increase value from the cocoa product

– Loss / Ageing of cocoa trees

– Possible low pollination with climatic change

23

Global Cocoa Based Industries

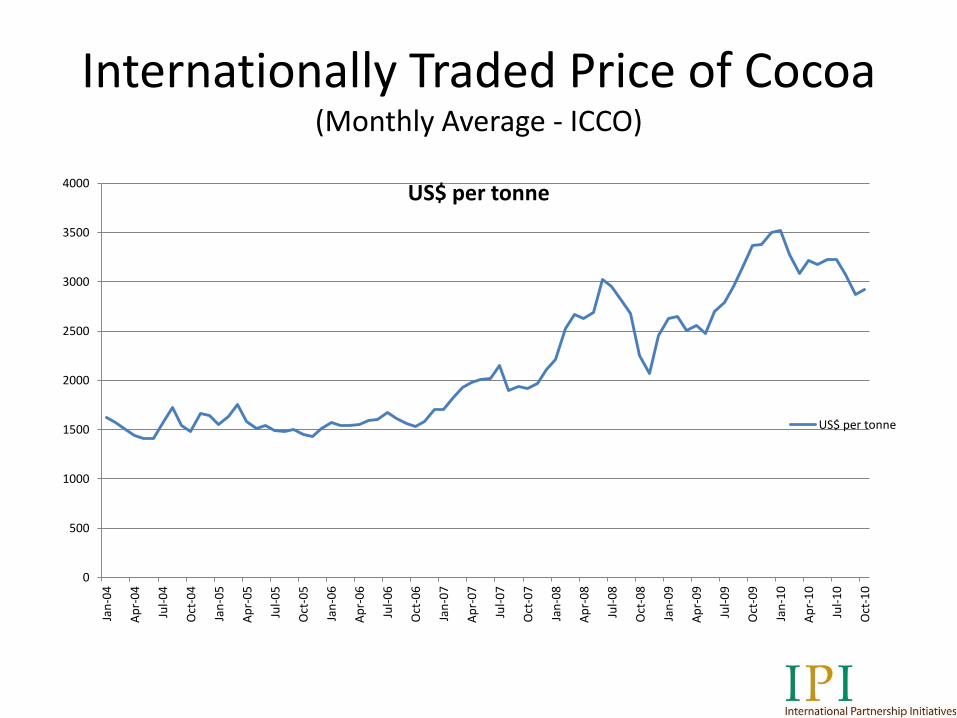

Internationally Traded Price of Cocoa (Monthly Average - ICCO)

25

0

500

1000

1500

2000

2500

3000

3500

4000

Jan

-04

Ap

r-0

4

Jul-

04

Oct

-04

Jan

-05

Ap

r-0

5

Jul-

05

Oct

-05

Jan

-06

Ap

r-0

6

Jul-

06

Oct

-06

Jan

-07

Ap

r-0

7

Jul-

07

Oct

-07

Jan

-08

Ap

r-0

8

Jul-

08

Oct

-08

Jan

-09

Ap

r-0

9

Jul-

09

Oct

-09

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

US$ per tonne

US$ per tonne

The Global Cocoa Processing Industry

• What happens to the cocoa beans exported?

– Value Add Players

• Cocoa grinders; blenders; traders;

• Chocolate makers; Confectionery makers;

– Value Add Products

• Cocoa Shells

• Powder / Cake

• Butter

• Paste / Liquor

• Chocolate & Chocolate Products

26

The Global Cocoa Processing Industry

• Favourable Trends

– Increasing specialisation / differentiation of end products; by country, region, taste etc.

– Growth in end consumer demand

– Higher world cocoa prices (Fine cocoa a premium)

– Small scale chocolatiers proliferating

– Health benefits of dark chocolate being promoted

– Miniaturization of technology in processing

– Dynamic changes in overseas processing structure

27

Caribbean Fine Cocoa Industry

THE FUTURE ?

The Caribbean Fine Cocoa Industry The Way Forward

• RETHINK THE VALUE CHAIN

– Most of the value is in the end product sales of confectionery AND in developed markets

– But without Cocoa Beans there is no Chocolate Bar

– Point of origin is a key selling point – branding

– Wine industry & premium coffee have analogies & lessons (Jamaica Blue Mountain Coffee)

– Move from a Value Chain to a Value Loop

29

The Caribbean Fine Cocoa Industry The Way Forward

• New Models for commercial success

– Caribbean Producers need to access / participate in wealth at end of value chain

• Partnership with intermediate or end producers (Joint Ventures, Sale Agreements etc)

• Growers get critical mass and economies of scale by collaboration amongst themselves (Assns. Co-ops etc)

• Incorporate other income streams via new products, markets and services – eco-tourism etc. (maximise revenue overall)

30

The Caribbean Fine Cocoa Industry The Way Forward

• Success Stories – Actions Underway

– Rehabilitation exercises in Trinidad & Tobago, Jamaica, St Lucia

– Renewed interest by land owners to get into cocoa growing & production

31

This project is funded

by the European Union

This project is funded

by the European Union

The Caribbean Fine Cocoa Industry The Way Forward

• Success Stories – New Models & Value Add

– Grenada (The Grenada Chocolate Company)

– St. Lucia (Hotel Chocolat)

32

The Caribbean Fine Cocoa Industry The Way Forward

• Success Stories – New Models & Value Add

– Trinidad

• Exotic Caribbean Mountain Pride

• Cocobel

• Brasso Seco

• House of Olando

• Rodco

33

The Caribbean Fine Cocoa Industry The Way Forward

• Success Stories – New Models & Value Add

– Tobago (Tobago Cocoa Estate)

– Jamaica (Chocolate Dreams)

34

The Caribbean Fine Cocoa Industry The Way Forward

• Policy Considerations - Trinidad

– Rural Labour availability (does TT need to formally import short term labour to get farm work done?)

– Need to stimulate and support the cocoa processing & value add sector

– Strengthen cross-linkages between Ministries of Food Production, Trade and Industry, Tourism

– Take the lead in regional approach for cocoa processing (cheap energy, close to other states,...)

35

The Caribbean Fine Cocoa Industry The Way Forward

• Policy Considerations - Jamaica

– Land tenure (legal issues) for generational transition so land ownership is secured

– Accessing cocoa growing on absentee land-holdings

– Use of All Terrain Vehicles (ATV’s or UTV’s) on public roads

– Collaboration between Government Departments in applying for external funding (EU etc.)

– Establishment of Project Office approach at CIB to proactively address industry issues

36

37

This project is funded

by the European Union

This project is funded

by the European Union

[email protected] www.caribbeanfinecocoa.net