the business environment in okinawa ... - okinawa-bank.co.jp › _files › 00023795 ›...

TRANSCRIPT

People’s Bank

The Bank of Okinawa,Ltd1

The Business Environment in Okinawa PrefectureThe Business Environment in Okinawa Prefecture

Outline of Business Results for FY2013Outline of Business Results for FY2013

Business StrategiesBusiness Strategies

The Bank of Okinawa,Ltd

People’s Bank

2

ContentsContents3

45678

9

10

11

1213141516171819202122232425

26

2728

The Business Environment in Okinawa

・Competitive Advantage of Okinawa’s Ideal Location…………・Future Development as International Distribution Base 1 ……・Future Development as International Distribution Base 2 ……・Population of Okinawa (Future Prospects)……………………・Number of Visitors to Okinawa…………………………………・Recent Economic Trends 1 (BOJ Tankan, Official land prices)…………………………………………………………………・ Recent Economic Trends 2 (Economic growth rate, Unemployment rate) ………………………………………………

Outline of Business Results for FY2013

・Highlights for FY2013 …………………………………………・Earnings …………………………………………………………・Deposits (Average Balance) …………………………………・Loans (Average Balance) ………………………………………・Loans to Individuals (Term-End Balance) ……………………・Fees and Commissions (Excluding Trust Fees) ……………・Loan / Deposit Interest Margin (Domestic)……………………・Loan / Deposit Spreads (Domestic)………………………..…・Securities (Term-End Balance) ………………………………・Securities Allocation…………………………. …………………・Expenses…………………………………………………………・Capital Ratio (Basel III Standard) ……………………………・Risk Management - Capital Allocation - ………………………・Credit Cost ………………………………………………………・Mandatory Disclosure of Bad Debt under the Financial Reconstruction Law ………………………………………………・Our Share of the Market Served by the Three Okinawan Regional Banks (FY2013) ………………………………………・Comparison with Other Okinawan Regional Banks…………

Business Strategies

・Business Performance Forecasts………………………………………・FY2013-2014 Medium-Term Business Plan…………………………. ・Numerical Targets …………………………………………………….…・Strategy for Consumer Loans……………………………………………・Strategy for Assets in Custody……………………………………………・Initiatives to Revitalize and Develop Local Communities………………・ Initiatives to Revitalize and Develop Local Communities (Foundation and Growth Support) …………………………………………………………・ Initiatives to Revitalize and Develop Local Communities (Management Improvement and Business Revitalization Support) ……・ Initiatives to Revitalize and Develop Local Communities (Business Succession and M&A Support) ……………………………………………・ Initiatives to Revitalize and Develop Local Communities (Cooperation Among Industry, Academia, Government and Financial Institutions)……・Branch Network Strategy and Shareholder Returns……………………

Supplemental Materials

・Business Performance ……………………………………………………・Term-End Balance, Average Balance, Yield, and Loan Balance by Industrial Segment ……………………………………………………………・Changes in Loan Balance by Assets Category (FY2012 and FY2013) ………………………………………………………・Interest Sensitivity …………………………………………………………・Major Economic Indicators in Okinawa Prefecture……………………

President : Yoshiaki Tamaki

Participant

29

303132333435

36

37

38

394041

42

43

444546

The Bank of Okinawa,Ltd

People’s Bank

3

The Business EnvironmentThe Business Environmentin Okinawa Prefecturein Okinawa Prefecture

The Bank of Okinawa,Ltd

People’s Bank

4

WithWith major Asian cities within range of 4 hours, located in the heartmajor Asian cities within range of 4 hours, located in the heart of East Asiaof East Asia

Narita 2h 25min

Haneda 2h 20min

Nagoya 2h 15min

Kansai 1h 50min

Seoul 2h 10min

Tsingtao 2h 50min

Shanghai 2h 5min

Taipei 1h 30min

Hong Kong 2h 35min

Bangkok 4h 25min

China (Population: 1.3 billion)

Japan (Population: 130 million)

ASEAN countries (Population: 600 million)

Okinawa

Locations within 4-hour travel from Okinawa

BeijingDalian

Seoul

Tsingtao

Shanghai

Guangzhou

Hanoi

Bangkok

Hong Kong

Manila

Located in the center of a massive market embracing a

population of 2 billion

Kuala Lumpur

Singapore

Jakarta

Taipei

Kansai NagoyaHaneda

Narita

Competitive Advantage of OkinawaCompetitive Advantage of Okinawa’’s Ideal Locations Ideal Location

The Bank of Okinawa,Ltd

People’s Bank

5

Shanghai

Taiwan

Southeast Asia

●Okinawa

Seoul

Bangkok

Delivery of nationwide specialties to the Asian market, ensuring their “added high-value and freshness”

Hong Kong

Direct shipments from producers to consumers using e-commerce site

malls!

Beef (Miyazaki)Beef (Miyazaki)

(Source: Okinawa Prefecture)

EchizenEchizen crabs (Fukui)crabs (Fukui)

Cherries (Yamagata)Cherries (Yamagata)

Horsehair crabs Horsehair crabs (Hokkaido)(Hokkaido)

Apples (Nagano)Apples (Nagano)

Sweet potatoes Sweet potatoes (Tokushima)(Tokushima) Achieving overwhelmingly advantageous lead times on the

back of the logistic infrastructures of ANA and Yamato Transport.The “Okinawa Great Trade Fair” provides assistance in business

matching for nationwide specialties suppliers and Japanese and overseas buyers.

◆

The export of nationwide specialty goods, including perishables, to the Asian market ◆

Rapid transport of high value-added products, e.g. electrical and precision apparatus

Okinawa

HanedaNagoya

Kansai Narita

Taipei

Singa pore

Bang kok

Hong Kong

Guan gzhou

Shan ghai

Tsing tao

Seoul

ANA domestic flights ANA international flights

North AmericaEurope

Other Asian cities

Other Asian cities

Other Asian cities

Other Asian cities

AsiaMiddle EastOceania

AsiaMiddle EastOceania

Inland areas in China

Inland areas in China

Inland areas in ChinaOther Asian cities

Future Development as International Distribution Base 1 Future Development as International Distribution Base 1 (Model of Distribution Relayed Through Okinawa(Model of Distribution Relayed Through Okinawa))

The Bank of Okinawa,Ltd

People’s Bank

6

(Source: Okinawa Prefecture)

Inventory center

Repair center

Shipping goods to Okinawa by air or marine transport

Perishable goods processing and distribution base

Storage and delivery base for catalog retailers

Dominant expansion into the Asian market by means of the Okinawa Distribution Depot

Future Development as International Distribution Base 2 Future Development as International Distribution Base 2 (Okinawa Warehousing Model) (Okinawa Warehousing Model)

The Bank of Okinawa,Ltd

People’s Bank

7

The population of Okinawa is expected to take a downward turn inThe population of Okinawa is expected to take a downward turn inand after 2025. Population is on the increase at this stage, and after 2025. Population is on the increase at this stage,

but active steps towards population growth are being taken now. but active steps towards population growth are being taken now.

沖縄県の人口推移

0

500

1,000

1,500

2,000

10 11 12 13 15 20 25 30 35 40 50 60 70 80 90 100

(出所)総務省 統計局 人口問題研究所、沖縄県

(単位:千人)

1,392千人(2010年)

1,415千人(2020年)

推 計 値

リスクシナリオに基づく人口予測

(2100)

2,030

(Creation of a society that allows people to marry, give birth to and raise children without undue worries)

Efforts to facilitate natural increase in population

◆

Higher marriage rates and birthrates ◆

Promotion of “health and longevity in Okinawa” campaign

(Creation of a dynamic society that is open to the world)

Efforts to enhancegrowth of society

◆

Job creation and securing diverse human resources ◆

Addressing to increase tourists and visitors

(Creation of a society that delivers well-balanced and sustainable population growth)

Aims to resolve challenges facedby isolated islands and

depopulated regions

◆

Improvement of conditions for long-term residence ◆

Industrial development by demonstrating attractive regional characteristics

(2050)

1,610(2035)

1,540

(2100)

840

(2024)

1,440

Population trends in Okinawa(in thousands)

1,392 (2010)

1,415 (2020)

Projected population curve based on risk

scenarios

Source: Statistics Bureau, Ministry of Internal Affairs and Communications of Japan, the National Institute of Population and Okinawa Prefecture

Projected population

Population of Okinawa (Future Prospects)Population of Okinawa (Future Prospects)

The Bank of Okinawa,Ltd

People’s Bank

8

FY2013 marked a record 6.58 million tourists visiting OkinawaFY2013 marked a record 6.58 million tourists visiting OkinawaBoth domestic and overseas tourists registered a new recordBoth domestic and overseas tourists registered a new record

入域観光客数と観光収入の推移

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

H15 H16 H17 H18 H19 H20 H21 H22 H23 H24 H25 H26 H33(年度)

(単位:人)

0

100,000

200,000

300,000

400,000

500,000

600,000

国内客(左軸) 外国人客(左軸) 観光収入(右軸)

(単位:百万円)

H25年度

入域観光客数658万人

(出所) 沖縄県「観光要覧」

26年度計画

690万人

33年度計画

1,000万人 Building of second runway at Naha Airport

(Scheduled for completion in 2019)

National Strategic Special Zone designated as bases for international tourism

(Designated in 2014)

Large-scale MICE (Facilities for international meetings, etc.)

(Scheduled to commence service in 2020)

Number of Visitors to OkinawaNumber of Visitors to Okinawa

Trends in the number of visitors and tourism revenues(Persons) (¥ million)

Target for FY20146,900,000

Number of visitors in FY2013

6,580,000

Target for FY2021

10,000,000

Source: Tourism Handbook, Okinawa Prefecture

Japanese visitors(left axis)

Overseas visitors(left axis)

Tourism revenues(right axis)

(fiscal year)20212003 04 05 06 07 08 09 10 11 12 13 14

The Bank of Okinawa,Ltd

People’s Bank

9

Official land pricesOfficial land prices

日銀短観 業況判断DI

▲ 30

▲ 20

▲ 10

0

10

20

30

40

H23.3 H23.9 H24.3 H24.9 H25.3 H25.9 H26.3

沖縄県

全国

商業地

-8

-7

-6

-5

-4

-3

-2

-1

0

1

22年 23年 24年 25年 26年

沖縄県

福岡県

熊本県

全国

・・Regarding official land prices for 2014, only Okinawa marked a rRegarding official land prices for 2014, only Okinawa marked a rise in land ise in land prices among prefectures in the Kyushu region. (6th highest rateprices among prefectures in the Kyushu region. (6th highest rate of rise in of rise in Japan)Japan)

・・BOJBOJ’’s Tankan survey also underlines greater improvement in Okinawas Tankan survey also underlines greater improvement in Okinawa’’s s business outlook compared to the national average.business outlook compared to the national average.

BOJ TankanBOJ Tankan

Source: Ministry of Land, Infrastructure and Transport

Source: BOJ Naha Branch

住宅地

-4.5

-4

-3.5

-3

-2.5

-2

-1.5

-1

-0.5

0

0.5

22年 23年 24年 25年 26年

沖縄県

福岡県

熊本県

全国

Highest value on record

¥209,000/sqm

Highest value on record

¥796,000/sqm

Recent Economic Trends 1Recent Economic Trends 1

Residential land prices

Commercial land prices

Okinawa

Fukuoka

KumamotoNational average

2010 2011 2012 2013 2014

2010 2011 2012 2013 2014

BOJ Tankan Business Confidence DI

Mar. 2011 Sep. 2011 Mar. 2012 Sep. 2012 Mar. 2013 Sep. 2013 Mar. 2014

Okinawa

Fukuoka

KumamotoNational average

OkinawaNational average

-

-

-

The Bank of Okinawa,Ltd

People’s Bank

10

・・Okinawa has maintained higher rates of economic growth than the Okinawa has maintained higher rates of economic growth than the national averagenational average・・In the past, Okinawa suffered nearly twice the unemployment rateIn the past, Okinawa suffered nearly twice the unemployment rate of the national average, but the of the national average, but the rates have steadily fallen, becoming closer to the national leverates have steadily fallen, becoming closer to the national level.l.

沖縄県と国の経済成長率の比較

▲ 5.0

▲ 4.0

▲ 3.0

▲ 2.0

▲ 1.0

0.0

1.0

2.0

3.0

4.0

H20 H21 H22 H23 H24見込

沖縄県 全国

県振興計画は平成33年まで年平均+2.0%を展望値としている

完全失業率の推移

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

H22 H23 H24 H25 H26.3 H33

差異 沖縄県 全国

(%) (%)

Economic growth rateEconomic growth rate(actual)(actual) Unemployment rateUnemployment rate

Source: Okinawa Prefecture, Cabinet Office, Government of Japan

Source: Okinawa Prefecture, Ministry of Internal Affairs and Communication

Recent Economic Trends 2Recent Economic Trends 2

Comparison of economic growth rate - Okinawa vs. National average Trends in unemployment rates

Okinawa National average National averageOkinawaDifference

2008 2009 2010 2011 2012 forecast 2010 2011 2012 2013 Mar. 2014 2021

-

-

-

-

-

The prefecture’s economic growth rate under the Okinawa Promotion Plan is expected to run at an annual average of +2.0% until 2021

The Bank of Okinawa,Ltd

People’s Bank

11

Outline of Business Results Outline of Business Results for FY2013for FY2013

The Bank of Okinawa,Ltd

People’s Bank

12

While interest income and commission revenues improved, credit costs increased substantially ⇒

resulting in increase in revenues and decrease earnings While interest income and commission revenues improved, credit costs increased substantially

⇒

resulting in increase in revenues and decrease earnings

●YoY comparison of business profit on core banking operations

Net gains on securities are posted as +0.9

Interest on securities

0.6

Interest paid on deposits

Others

Commissions

ExpensesTrust account

services

0.1

Interest on loans and bills discounted

IncreaseDecrease

Total 1.21.4

0.5

0.60.2

0.0

0.3

Highlights for FY2013Highlights for FY2013

* The capital ratio for FY13 was calculated according to the new standard, Basel III.

●Year-on-year changes(\ billion, %)

Average balance Yield InterestLoans and billsdiscounted

+48.6[+47.2]

(0.15)[(0.15)]

(0.6)[(0.7)]

Securities +1.8 +0.06 0.3

Deposits +39.4[+39.5]

(0.03)[(0.04)]

(0.5)[(0.6)]

Others - - 0.0[0.0]

Total - -0.2

[0.3]

(¥ billion)Non-consolidated

YoY changeOrdinary income 37.1 36.8 +0.3Gross business profit 30.0 30.2 (0.2)

Interest income 27.3 26.9 +0.3Fees and commissions 2.5 2.4 +0.1

Fees and commissions (excluding trust fees) 2.0 1.8 +0.2Trust account services 0.4 0.5 (0.1)

Other business profit 0.1 0.8 (0.7)Gains (losses) on bond trading (0.0) 0.7 (0.7)

Expenses (excluding non-recurrent items) 19.9 19.2 +0.6Business profit on core banking operations 10.1 10.3 (0.1)

Provision of general allowance for possible loan losses 0.6 (0.0) +0.7Net business profit 9.4 11.0 (1.5)

Non-recurrent items (0.9) (1.7) +0.8Net gains (losses) on equity securities 1.0 (0.5) +1.5Bad debt disposal (non-recurrent items) 2.2 1.6 +0.5

Ordinary profit 8.5 9.3 (0.7)Extraordinary gains (0.0) (0.0) (0.0)

Bad debt disposal (reversal of extraordinary losses) - - -Net income 4.5 5.4 (0.8)

Credit costs 2.8 1.6 +1.2Non-performing loan ratio 1.72% 1.64% 0.08%Capital ratio 11.66% 11.88% -

FY12FY13

The Bank of Okinawa,Ltd

People’s Bank

13

(¥ billion)

Business profit on core banking operations decreased due to higher expenses despite the rise in interest income

Business profit on core banking operations decreased due to higher expenses despite the rise in interest income

266

101

50

256

91

51

269

103

54

273

101

45

0

50

100

150

200

250

300

23/3期 24/3期 25/3期 26/3期

資金利益

コア業務純益

当期純利益

Earnings (Business profit on core banking operations Earnings (Business profit on core banking operations continued to exceed the continued to exceed the ¥¥10.0 billion level)10.0 billion level)

30.0

25.0

20.0

15.0

10.0

5.0

26.6 25.626.9

10.1

5.0

9.1

5.1

10.3

5.4

FY10 FY11 FY12 FY13

27.3

10.1

4.5

Interest income

Business profit on

core banking operations

Net income

The Bank of Okinawa,Ltd

People’s Bank

14

Deposits by individualsIncreased liquidity

Opening of new pension and salary payment accounts Decrease in time deposits

Maturity of deposits acquired through past promotional campaigns, etc.

Deposits by individualsIncreased liquidity

Opening of new pension and salary payment accountsDecrease in time deposits

Maturity of deposits acquired through past promotional campaigns, etc.

Deposits by corporationsIncreased liquidity

Enhanced function to trace funds

(¥ billion)

Deposits by corporations rose by ¥38.4 billion (+8.7%)Deposits by individuals rose by ¥24.1 billion (2.2%)Total deposits rose by ¥39.1 billion (+2.2%) to ¥1,745.6 billion

Deposits by corporations rose by ¥38.4 billion (+8.7%)Deposits by individuals rose by ¥24.1 billion (2.2%)Total deposits rose by ¥39.1 billion (+2.2%) to ¥1,745.6 billion

* Including trust accounts

9,724 10,718 11,000 11,242

4,7954,4114,3353,961

1,3461,5821,492

1,332

73

70158

104

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

23/3期 24/3期 25/3期 26/3期

個人

法人

公金

金融

15,12316,704 17,065 17,456

DepositsDeposits (Average Balance)(Average Balance)

FY10 FY11 FY12 FY13

1,800

1,600

1,400

1,200

1,000

800

600

400

200

1,512.31,670.4 1,706.5 1,745.6

133.2149.2 158.2 134.6

396.1433.5 441.1

479.5

972.41,071.8 1,100.0

1,124.2

10.4

15.8 7.0

7.3Financial

institutions

Public funds

Corporations

Individuals

The Bank of Okinawa,Ltd

People’s Bank

15

(¥ billion)

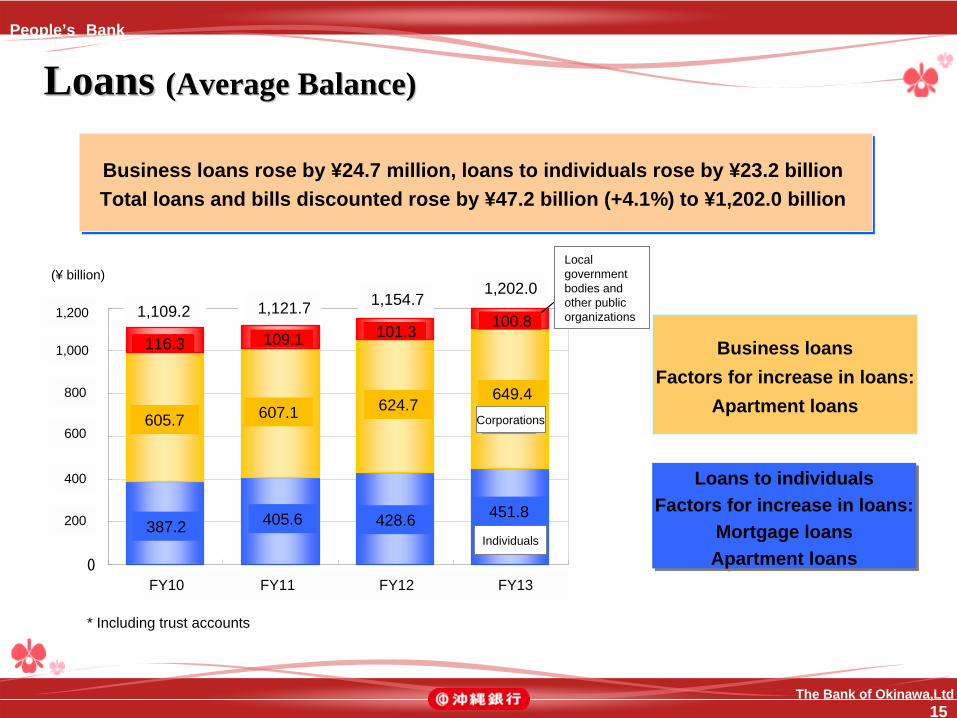

Business loans rose by ¥24.7 million, loans to individuals rose by ¥23.2 billionTotal loans and bills discounted rose by ¥47.2 billion (+4.1%) to ¥1,202.0 billionBusiness loans rose by ¥24.7 million, loans to individuals rose by ¥23.2 billionTotal loans and bills discounted rose by ¥47.2 billion (+4.1%) to ¥1,202.0 billion

* Including trust accounts

3,872 4,056 4,286 4,518

6,4946,2476,0716,057

1,0081,0131,0911,163

0

2,000

4,000

6,000

8,000

10,000

12,000

23/3期 24/3期 25/3期 26/3期

個人

法人

地公体11,092 11,217 11,547 12,020

Loans to individualsFactors for increase in loans:

Mortgage loansApartment loans

Loans to individualsFactors for increase in loans:

Mortgage loansApartment loans

Business loansFactors for increase in loans:

Apartment loans

1,200

1,000

800

600

400

200

FY10 FY11 FY12 FY13

Corporations

Individuals

1,109.2 1,121.7 1,154.71,202.0

116.3 109.1 101.3 100.8

605.7 607.1 624.7649.4

387.2 405.6 428.6 451.8

Local government bodies and other public organizations

Loans Loans (Average Balance)(Average Balance)

The Bank of Okinawa,Ltd

People’s Bank

16

(単位:億円)

Mortgage loans rose by ¥31.3 billion, other loans rose by ¥1.7 billionLoans to individuals rose by ¥33.0 billion (+6.6%) year on year to ¥529.8 billion

Mortgage loans rose by ¥31.3 billion, other loans rose by ¥1.7 billionLoans to individuals rose by ¥33.0 billion (+6.6%) year on year to ¥529.8 billion

※

信託勘定を含んでおります

3,883 4,121 4,3334,646

652635

611595

0

1,000

2,000

3,000

4,000

5,000

23/3期 24/3期 25/3期 26/3期

住宅ローン

4,4784,732

4,9685,298

その他ローン

Loans to IndividualsLoans to Individuals (Term(Term--End Balance)End Balance)

(¥ billion)

* Including trust accounts

447.8473.2

496.8529.8

FY10 FY11 FY12 FY13

59.561.1

63.565.2

388.3 412.1 433.3464.6

500

400

300

100

200

Mortgage loans

Other loans

The Bank of Okinawa,Ltd

People’s Bank

17

(¥ billion)

1415

1820

0

5

10

15

20

25

23/3期 24/3期 25/3期 26/3期

Major factors for increase (on a YoY basis)

・M&A fees・Investment trust sales

commissions

Fees and Commissions Fees and Commissions (Excluding Trust Fees)(Excluding Trust Fees)

2.5

2.0

1.5

0.5

1.0

1.4 1.5

1.82.0

FY10 FY11 FY12 FY13

The Bank of Okinawa,Ltd

People’s Bank

18

(単位:%)

0.26 0.14

1.121.13

1.061.05

0.110.29

1.211.12

1.01

0.94

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

23/3期 24/3期 25/3期 26/3期

2.51 2.442.32

2.17

預貸金利鞘

経費率

預金利回り

Yield on loans

Loan / Deposit Interest MarginLoan / Deposit Interest Margin

Loan / Deposit Interest Margin Loan / Deposit Interest Margin (Domestic) (Domestic)

(%)

FY10 FY11 FY12 FY13

Loan/deposit interest margin

Expense ratio

Yield on deposits

The Bank of Okinawa,Ltd

People’s Bank

19

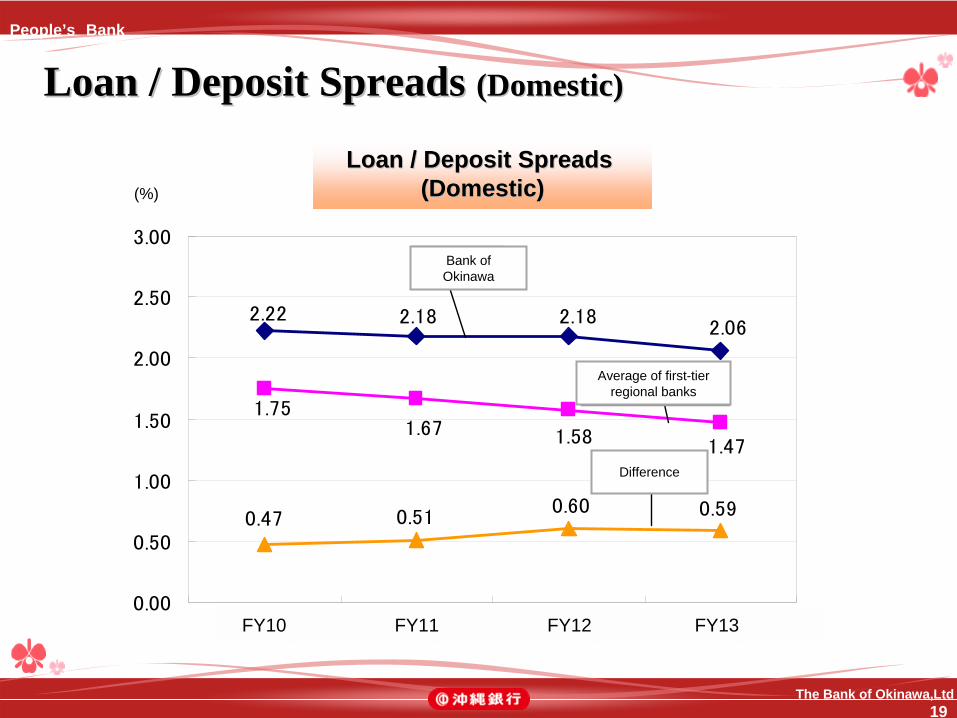

2.22 2.18 2.182.06

1.751.67 1.58 1.47

0.590.600.510.47

0.00

0.50

1.00

1.50

2.00

2.50

3.00

23/3期 24/3期 25/3期 26/3期

当行

第一地銀平均

差異

(%)

Loan / Deposit Spreads Loan / Deposit Spreads (Domestic)(Domestic)

Loan / Deposit Spreads Loan / Deposit Spreads (Domestic)(Domestic)

FY10 FY11 FY12 FY13

Bank of Okinawa

Average of first-tier regional banks

Difference

The Bank of Okinawa,Ltd

People’s Bank

20

(¥ billion) (%)

2,9213,604 3,625

3,111

280

324

196

209

1,235

1,146

854

1,084

953769216

181

214

203

251 258

3.28

2.87

1.982.00

0

1,000

2,000

3,000

4,000

5,000

6,000

23/3期 24/3期 25/3期 26/3期

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

国債

地方債

社債

株式

その他

デュレーション

4,466

5,3996,002

5,773

0.000

0.200

0.400

0.600

0.800

1.000

1.200

1.400

1.600

H20/3期 H21/3期 H22/3期 H23/3期 H24/3期 H25/3期 H26/3期 H27/3期計画

当行

地銀平均

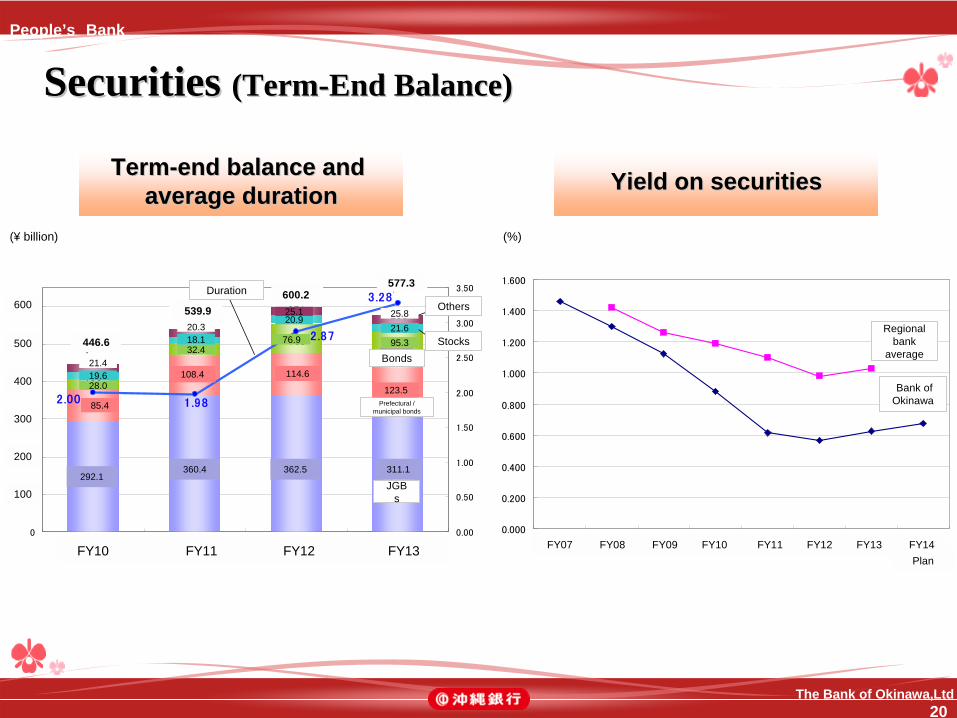

TermTerm--end balance and end balance and average durationaverage duration Yield on securitiesYield on securities

Securities Securities (Term(Term--End Balance)End Balance)

FY10 FY11 FY12 FY13

600

500

400

300

200

100

Others

Stocks

Prefectural / municipal bonds

Bonds

JGB s

FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 Plan

Bank of Okinawa

Regional bank

average

292.1360.4 362.5 311.1

85.4

108.4 114.6

123.528.0

32.476.9 95.3

19.6

18.1

20.921.6

25.1

21.4

20.325.8

446.6

539.9600.2

577.3Duration

The Bank of Okinawa,Ltd

People’s Bank

21

Review of allocation (improve allocation so it is notconcentrated on JGBs)Pursuing higher yields while controlling risks

Review of allocation (improve allocation so it is notconcentrated on JGBs)Pursuing higher yields while controlling risks

有価証券構成比率(期末簿価)

53.0%

66.5% 65.2% 66.8%61.1%

54.4%49.6%

13.6%

14.8% 19.3%20.1%

19.1%

21.5%

21.8%

14.7%

7.6%6.3%

6.1%13.0%

16.8%20.6%

10.1%

6.7% 4.3% 3.3% 2.9%0.8% 1.1%6.0% 3.4% 4.1% 2.9% 3.1% 3.3% 3.7%

3.0% 3.1%1.1%0.9%0.8%

1.0%

2.5%

0%

20%

40%

60%

80%

100%

H21/3末 H22/3末 H23/3末 H24/3末 H25/3末 H26/3末 H27/3末計画

国債

地方債

社債

株式

その他有価証券

外国証券

Investments to beemphasizedin the future

Securities AllocationSecurities Allocation

Securities composition percentage (carrying value at term-end)

Mar. 2009 Mar. 2010 Mar. 2011 Mar. 2012 Mar. 2013 Mar. 2014 Mar. 2015 Plan

Foreign securities

Other securities

Stocks

Bonds

Prefectural / municipal

bonds

JGB s

The Bank of Okinawa,Ltd

People’s Bank

22

¥19.9 billion (up ¥0.6 bn YoY)¥¥19.9 billion 19.9 billion (up (up ¥¥0.6 0.6 bnbn YoYYoY))

Non-personal expenses increased (up ¥0.5 billion)

mainly due to an increase in office consignment expenses

Personnel expenses increased (up ¥ 0.1 billion) owing partly to higher expenses incurred

by temporary hiring

(¥ billion) (%)

84 85 87 93

91 93 95 96

9 9 9 9

64.767.3

65.1 66.1

0

40

80

120

160

200

240

280

23/3期 24/3期 25/3期 26/3期

0

10

20

30

40

50

60

70

人件費

物件費

コアOHR

185 188 192 199税金

ExpensesExpenses

28.0

24.0

20.0

16.0

12.0

8.0

4.09.1 9.3 9.5 9.6

8.4 8.5 8.79.3

0.9 0.9 0.9 0.918.5 18.8 19.2 19.9

Core OHR

Non-personal expenses

Personnel expenses

Taxes

FY10 FY11 FY12 FY13

The Bank of Okinawa,Ltd

People’s Bank

23

Capital ratio (domestic standard) at 11.66%Capital ratio Capital ratio (domestic standard) (domestic standard) at 11.66%at 11.66%(%)

Outlier Ratio

Percentile standard

Core deposits are assumed to be 50% of the term-end balance of liquid deposits. The average maturity is assumed to be 2.5 years.

Average capital ratio of regional banksin the term ended March 2014

Capital ratio: 11.60%

Average capital ratio of regional banksin the term ended March 2014

Capital ratio: 11.60%

Source: Bank of Okinawa

12.7312.23 12.2512.01 11.88

11.66 11.66

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

23/3期 24/3期 25/3期 26/3期

自己資本比率 TierⅠ比率

コア資本

Calculated by new standard

Capital Ratio (Basel III Standard)Capital Ratio (Basel III Standard)

Core capital

FY10 FY11 FY12 FY13

Capital ratio Tier I ratio

Total interest rate risk Outlier ratioEnd of March 2014 \4,202 million 3.59%

The Bank of Okinawa,Ltd

People’s Bank

24

520

16073

198

190

375

120

48

102

43

50

0

200

400

600

800

1000

1200

配賦可能資本(Tier1資本)

25年度リスク資本内訳 25年度末リスク量

1,093

520

268

バッファー

未配賦資本

配賦リスク資本

Controlling risks within the scope of Tier IControlling risks within the scope of Tier I(¥ billion)

リスク量算定基準

信頼区間 99% 99% 99%

観測期間 1年 1年 1年

オペレーショナル・リスク

基礎的手法

保有区間

預貸等の金利リスク

信用リスク 市場リスク

1年 1年政策株 : 1年その他 : 1ヶ月

信用リスク 市場リスク預貸等の金利

リスクオペレーショナル・リスク

オペレーショナル・

リスク

預貸等の金利リスク

市場リスク

信用リスク

Risk Management Risk Management ―― Capital Allocation Capital Allocation ――

120

100

80

60

40

20

109.3

52.0

26.8

37.5

19.8

52.0

5.0

4.3

Operational risk

10.2

19.0

Market risk

16.07.3 Credit risk

4.8

12.0

Loan / deposit interest risk

Credit risk Market riskLoan / deposit

interest riskOperational

risk

Breakdown of risk capital in FY13

Risk amount (end of FY13)

Allocated economic capital (= Tier I)

Buffer

Unallocated capital

Allocated risk capital

Holding period

Confidence interval

Observation period

1 year

1 year

1 year

1 year 1 year

Basic indication approach (BIA)

Basis for risk calculation

Strategic share holdings: 1 year Others: 1 month

The Bank of Okinawa,Ltd

People’s Bank

25

Reflecting the rise in historical default rates of normal assets and assetsrequiring caution, and further drops in prime borrower rating,

credit cost amounted to ¥2.8 billion (up ¥1.2 bn YoY)

Reflecting the rise in historical default rates of normal assets and assetsrequiring caution, and further drops in prime borrower rating,

credit cost amounted to ¥¥2.8 billion 2.8 billion (up (up ¥¥1.2 1.2 bnbn YoYYoY))

(¥ billion)

26

16

22

17

6 0.23

0.140.14

0.09

0

5

10

15

20

25

30

24/3期 25/3期 26/3期 27/3期

0.00

0.05

0.10

0.15

0.20

0.25

0.30

不良債権処理額

計画

一般貸倒引当金繰入額

28(22+6)

11(26-15)

16 17

与信費用比率

▲15

Credit CostCredit Cost

3.0

2.5

2.0

1.5

1.0

0.5

(1.5)

0.6

2.6

1.6

2.2

1.7

1.71.6

1.1(2.6-1.5)

2.8(2.2+0.6)

Provision of general allowance for possible

loan losses

Bad debt disposal

Credit cost ratio

Plan

FY11 FY12 FY13 FY14

The Bank of Okinawa,Ltd

People’s Bank

26

¥21.7 billion (1.72%)Non-performing loan (NPL) ratio up 0.08% reflecting an increase in doubtful assets

¥¥21.7 billion 21.7 billion (1.72%)(1.72%)Non-performing loan (NPL) ratio up 0.08% reflecting an increase in doubtful assets

(¥ billion) (%)

20 1530

67 6764

82

36

210

107109115

99

1.68 1.63 1.64 1.721%台

3.042.95

3.073.02

0

100

200

300

23/3期 24/3期 25/3期 26/3期 27/3期

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

危険債権

破産更正債権及びこれに準ずる債権

開示債権比率 開示債権比率(地銀平均)

計画196 198 205

217 210

Mandatory Disclosure of Bad Debt Mandatory Disclosure of Bad Debt under the Financial Reconstruction Lawunder the Financial Reconstruction Law

30.0

20.0

10.0

19.6 19.8 20.5 21.7 21.0

10.7 11.5 10.99.9

6.7 6.76.4

8.2

2.0 1.5 3.0 3.6

21.0

FY10 FY11 FY12 FY13 FY14

1.00- 1.99%

Plan

NPL ratioNPL ratio

(regional bank average)

Bankrupt and quasi- bankrupt assets

Doubtful assets

The Bank of Okinawa,Ltd

People’s Bank

27

Increase in shares of loans; deterioration in shares of deposits

Loans: 42.74% (up 0.25 points YoY) Deposits: 41.97% (down 0.49 points YoY)

Increase in shares of loans; deterioration in shares of deposits

Loans: 42.74% Loans: 42.74% (up 0.25 points (up 0.25 points YoYYoY))

Deposits: 41.97%Deposits: 41.97% (down 0.49 points (down 0.49 points YoYYoY))

(%) (%)

貸出金(平残)貸出金(平残)貸出金(平残) 預金(平残)預金(平残)預金(平残)

41.79

42.14

42.7442.49

41.00

41.50

42.00

42.50

43.00

23/3期 24/3期 25/3期 26/3期

42.52 42.46

41.97

41.73

41.00

41.50

42.00

42.50

43.00

23/3期 24/3期 25/3期 26/3期

Our Share of the Market Served by the Three Our Share of the Market Served by the Three OkinawanOkinawan Regional Banks (FY2013) Regional Banks (FY2013)

Loans (average balance)

Deposits (average balance)

FY10 FY11 FY12 FY13 FY10 FY11 FY12 FY13

The Bank of Okinawa,Ltd

People’s Bank

28

Bank of Okinawa (Increase in revenues, decrease in earnings)

Bank A (Increase in revenues and

earnings)

Bank B (Decrease in revenues, increase in earnings)

Ordinary income ¥37.1 billion ¥37.9 billion ¥12.6 billionBusiness profit on core

banking operations ¥10.1 billion ¥8.4 billion ¥2.0 billion

Net income ¥4.5 billion ¥3.4 billion ¥1.3 billion

Capital ratio 11.66% 10.50% 9.83%

Loan/deposit spreads 2.06% 2.04% 2.39%

Core OHR 66.18% 71.87% 80.13%

ROE 4.13% 3.91% 4.06%

Loans (Average balance) ¥1,202.0 billion ¥1,247.7 billion ¥362.9 billionDeposits

(Average balance) ¥1,745.6 billion ¥1,836.4 billion ¥577.3 billion

Market capitalization ¥91.5 billion ¥52.9 billion -

PBR (consolidated) 0.72 times 0.6 times -

Comparison with Other Comparison with Other OkinawanOkinawan Regional Banks Regional Banks (FY2013)(FY2013)

The Bank of Okinawa,Ltd

People’s Bank

29

Business StrategiesBusiness Strategies

The Bank of Okinawa,Ltd

People’s Bank

30

Interest on securities

0.3Interest paid on deposits

Others

Commissions

ExpensesTrust account

services

0.6

Interest on loans and bills discounted

IncreaseDecrease

●コア業務純益の前期比

Total0.7 0.8

0.0

0.1

0.1

0.0

0.2

Business Performance ForecastsBusiness Performance Forecasts●Year-on-year changes forecast

Note) Figures in square brackets include trust accounts.

●YoY comparison of business profit on core banking operations

(\ billion, %)Average balance Yield Interest

Loans and billsdiscounted

+47.1[+45.7]

(0.069)[(0.069)]

0.1[0.1]

Securities (36.8) +0.052 +0.0

Deposits +32.0[+26.6]

(0.02)[(0.03)]

(0.3)[(0.5)]

Others - - (0.0)[(0.0)]

Total - - 0.5[+0.6]

(¥ billion)Non-consolidated

Ordinary income 37.1 36.4 (0.7)Gross business profit 30.0 31.0 +1.0

Interest income 27.3 27.9 +0.6Fees and commissions 2.5 2.7 +0.1

Fees and commissions (excluding trust fees) 2.0 2.3 +0.2Trust account services 0.4 0.4 (0.0)

Other business profit 0.1 0.3 +0.2Gains (losses) on bond trading (0.0) 0.2 +0.2

Expenses (excluding non-recurrent items) 19.9 20.5 +0.6Business profit on core banking operations 10.1 10.2 0.1

Provision of general allowance for possible loan losses 0.6 (0.0) (0.6)Net business profit 9.4 10.5 1.0

Non-recurrent items (0.9) (1.2) (0.3)Net gains (losses) on equity securities 1.0 0.2 (0.8)Bad debt disposal (non-recurrent items) 2.2 1.7 (0.4)

Ordinary profit 8.5 9.2 +0.7Extraordinary gains (0.0) (0.0) 0.0

Net income 4.5 5.7 +1.1

Credit costs 2.8 1.7 (1.1)

FY13 FY14 YoY change

The Bank of Okinawa,Ltd

People’s Bank

31

FY2013FY2013--2014 Medium2014 Medium--Term Business PlanTerm Business Plan

Improve the speed of management decision-making and evolve into a next-generation bank with customer focused strategy

BasicPolicy

Reinforcing our foundations as the top bank in OkinawaOkigin’s spirits make customers smile and revitalize the region

Customer focused strategy

Management Strategies Personnel Strategies Organizational Strategies

Regional Contribution Strategies

Strengthen sales and earning capabilities as well as promote retail sales from the customer’s point of view

Develop employees from the customer’s point of view and promote the principle: “small numbers, exceptional talent”

Build an organization from the customer’s point of view and pass along the “OKIGIN” culture

Leverage genuine value to revitalize business and the regional from the customer’s point of view

Leverage consulting functions

Introduce next-generation systems

Strengthen compliance systems

Build an organization from the customer’s point of view

Strategically assign employees

Develop employees able to make proposals suitable to each customer life stage

Develop employees from the customer’s point of view

Strengthen sales and earnings capabilities as well as promote retail sales

Promote IT marketing strategies

Improve the quality of loan assets

Customer Management Committee

Customer Service Department

Build an organization that helps improve customer and employee satisfaction by reflecting customer feedback and the needs of sales staff in management policies

Develop sales systems able to provide optimal financial services from the points of view of both individual and corporate customers

Build an organization by customer focused strategy

To become Okinawa’s No. 1 bank: aim→achieve→solidify→leverage our true value

Bank of Okinawa’s goal is to be the People’s Bank

A bank loved by people in Okinawa

Prefecture

The Bank of Okinawa,Ltd

People’s Bank

32

26/3期実績 27/3期目標

コア業務純益 101億円 100億円程度

コア業務純益ROE 9.16% 9%程度

資金量(平残) 1兆7,456億円 1兆7,700億円

融資量(平残) 1兆2,020億円 1兆2,200億円

開示債権比率 1.72% 1%台

コアOHR 66.1% 60%台

自己資本比率 11.66% 12%台

ROE(連結) 4.53% 5%程度

※ROE算式(期首株主資本+期末株主資本)÷2

当期純利益

Numerical TargetsNumerical Targets

Business profit on core banking operationsROE for core banking operations

Deposits (Average balance)

Loan assets (Average balance)

Non-performing loan ratio

Core OHR

Capital ratio

ROE (Consolidated)

FY13 Results FY14 Targets

¥10.1 billion Around ¥10.0 billion

Around 9%

¥1,745.6 billion

¥1,202.0 billion

¥1,770.0 billion

¥1,220.0 billion

1.00 - 1.99%

60.00 - 60.99%

12.00 - 12.99%

Around 5%

* ROE calculation formula

9.16%

1.72%

66.1%

11.66%

4.53%

Net income(Shareholders’ equity at the beginning of period + shareholders’ equity at the end of period) / 2

The Bank of Okinawa,Ltd

People’s Bank

33

(¥ billion)

Mortgage loans +¥30.7 billion, Other loans +¥2.3 billionConsumer loans ¥562.8 billion (+6.2% YoY)

Mortgage loans +¥30.7 billion, Other loans +¥2.3 billionConsumer loans ¥562.8 billion (+6.2% YoY)

4,953

675

3,883 4,121 4,3334,646

652635

611595

0

1,000

2,000

3,000

4,000

5,000

6,000

23/3期 24/3期 25/3期 26/3期 27/3期

計画

住宅ローン

4,4784,732 4,968

5,2985,628

その他ローン

・Solid housing demand・Higher personal spending on the back of improving economic outlook

Strategy for Consumer LoansStrategy for Consumer Loans

100

200

300

400

500

600

447.8473.2 496.8

529.8562.8

59.561.1

63.565.2

67.5

388.3 412.1 433.3 464.6 495.3

FY10 FY11 FY12 FY13 FY14

Other loans

Mortgage loans

Plan

The Bank of Okinawa,Ltd

People’s Bank

34

Pension insuranceTargeted sales volume

¥24.0 billion

Investment trustTargeted sales volume

¥14.0 billion

(¥ billion)

Boost sales focusing mainly on investment trusts and pension insuranceBoost sales focusing mainly on investment trusts and pension insurance

* Pension insurance totals are cumulative sums sold. * Sales target added to the balance as of the end of the previous fiscal year for the fiscal year ending March 31, 2015 excluding contract and other cancellations (Figures take into account redemption of JGBs)

244 201 194

390 452456

901

319460

403

415

1,141

445

524697

0

200

400

600

800

1000

1200

1400

1600

1800

2000

23/3期 24/3期 25/3期 26/3期 27/3期

計画

年金保険

投資信託

国債

1,321

1,233

1,394

1,507

1,791

Strategy for Assets in CustodyStrategy for Assets in Custody

100

200

120

140

160

180

80

132.1

20

40

60

179.1

123.3

139.4

150.7

44.5

52.4

69.7 90.1

114.1

39.0 45.2 40.345.6

41.5

31.924.4 20.1 19.4

46.0

Plan

FY10 FY11 FY12 FY13 FY14

Pension insurance

Investment trusts

JGBs

The Bank of Okinawa,Ltd

People’s Bank

35

Initial funding

(Foundation)

Working capital and capital expenditure

(Growth)Financing facilitation

Business revitalization

(Economic downturn)

M&A (Transition)

Working capital and capital expenditure

(Stabilization)

1 Matching business initiatives

Corporate customer growth and development

Financing deeply rooted in the community: making the most of consulting functions ― SR activities ―

2 International logistics initiatives

4 Management improvement support

3 Initiatives for business succession

Initiatives to Revitalize and Develop Local CommunitiesInitiatives to Revitalize and Develop Local Communities

The Bank of Okinawa’s operating activities (SR Activities) that match corporate customer lifecycles and needs

The Bank of Okinawa,Ltd

People’s Bank

36

Foundation Support

As an “authorized support organization” defined by the Act for Facilitating New Business Activities of Small and Medium-sized Enterprises, the Bank of Okinawa has implemented the following supporting services:Providing start-up business owners with useful information as well as assistance at the time of grant applicationsDispatch of professionals in cooperation with member organizations comprising the local SME platform

Initiatives for business growth (Support for the cultivation of markets)

Participation in the “Okinawa Great Trade Fair Pre- Trade Fair”The Bank of Okinawa co-hosted and participated in the “Okinawa Great Trade Fair Pre-Trade Fair”, a large, national-scale trade fair for visitors from around the world, with an eye to raising the status of “The Bank of Okinawa Churashima Trade Fair” to a prefectural level business fair.

Held on November 14 and 15, 2013Participation of 131 exhibitors and 102 buyersApproximately 1,600 individual business meetings took place in two days119 staff members from the Bank of Okinawa collaborated in the administration of the fair

Initiatives to Revitalize and Develop Local CommunitiesInitiatives to Revitalize and Develop Local Communities (Foundation and Growth Support)(Foundation and Growth Support)

(Results for FY13)Support item No. of cases

1. Foundation support for small-scale business owners, etc. (Assistance in the formulation of business or finance plans)

2. Assistance in the establishment of new medical businesses

3. Dispatch of professionals

The Bank of Okinawa,Ltd

People’s Bank

37

Customers

CreditScreeningDivision

CorporateBankingDivision

Authorized SupportOrganizations

Okinawa Prefectural Center forManagement Improvement Support

SME Revitalization Support Councils Professional business consultants for SMEs

Public support organizations certified by the governmentTax accountants, SME management consultants, lawyers and bankers from financial institutions, etc. practicing in Okinawa

Commencement of a project to provide assistance in the formulation of management improvement plans with collaboration from authorized support organizationsA designated window for businesses, which provides necessary funds to finance up to two-

thirds of relevant expenses (maximum ¥2 million)

Status of Application to SME Revitalization Support Councils

Current situation concerning the use of a “program implemented by authorized support organizations to assist in the formulation of management improvement plans”

Holding study sessions for authorized support organizations and briefing meetings at all the Bank’s branches inviting lecturers from the Small and Medium Enterprises Department, Economy, Trade and Industry Division, Okinawa General Bureau of the Cabinet Office.The Bank of Okinawa has received 44 applications, representing 63.7% of a total of 69 applications submitted in Okinawa Prefecture.

FY03-FY12 1H FY13 2H FY13 TotalNumber of applications submitted to Councils 84 8 12 104 (of which, submitted to the Bank of Okinawa) 50 6 6 62Percentage of applications submitted to the Bank of Okinawa 59.5% 75.0% 50.0% 59.6%

The Bank of Okinawa is committed to providing support for its customers in their management improvement and business revitalization, in proactive collaboration with

external professionals, etc., as necessary.

Initiatives to Revitalize and Develop Local CommunitiesInitiatives to Revitalize and Develop Local Communities (Corporate Management Improvement and Business Revitalization Su(Corporate Management Improvement and Business Revitalization Support)pport)

The Bank of Okinawa,Ltd

People’s Bank

38

□More than 65 years have passed since World War II ended and now many SMEs are managed by older founders [average age of 57.5].

□ [85%] of business owners in Okinawa have yet to name or decide upon their successors.

□Many of them often consult with [tax accountants] and [lawyers] for advice.□One of the critically important issues related to business succession is [finance].

□In 2008, the Bank of Okinawa established a division to promote business successions.

□In 2010, the Bank launched a business succession loan (the only provider of such loan in Okinawa).

□The Bank holds business succession seminars.

□It has run Okigin Business Successor School for five years in a row. 相談件数 契約件数

39

1

62

1

56

2

109

2

91

7

101

14

当行事業承継・M&A取組実績

20年 21年 22年 23年 24年 25年

急増中

Challenges faced by regional SMEs

Support system at the Bank of Okinawa

Initiatives to Revitalize and Develop Local CommunitiesInitiatives to Revitalize and Develop Local Communities(Business Succession and M&A Support)(Business Succession and M&A Support)

Number of business successions and M&A deals supported by the Bank of Okinawa

2008 2009 2010 2011 2012 2013

Number of consultations Number of signed contracts

Rapidly increasing

The Bank of Okinawa,Ltd

People’s Bank

39

Contribution to local community through cooperation among industry, academia, government and financial institutions

As a regional financial institution deeply rooted in local commuAs a regional financial institution deeply rooted in local communities, the Bank of Okinawa signed an agreement with the nities, the Bank of Okinawa signed an agreement with the University of the University of the RyukyusRyukyus to collaborate on the revitalization of local communities,to collaborate on the revitalization of local communities, by leveraging their combined capabilities, i.e. the by leveraging their combined capabilities, i.e. the BankBank’’s consulting function and corporate network and the universitys consulting function and corporate network and the university’’s personnel and intellectual resources. s personnel and intellectual resources. The Bank of Okinawa The Bank of Okinawa will strive to contribute to the realization of a selfwill strive to contribute to the realization of a self--supporting economy, envisaged by the 21st Century Vision of Okinsupporting economy, envisaged by the 21st Century Vision of Okinawa Prefecture.awa Prefecture.

Conclusion of an agreement to collaborate with the Integrated Innovation Center for Community, University of the Ryukyus

Initiatives to Revitalize and Develop Local CommunitiesInitiatives to Revitalize and Develop Local Communities (Cooperation Among Industry, Academia, Government and Financial (Cooperation Among Industry, Academia, Government and Financial Institutions)Institutions)

University of the Ryukyus

The Bank of Okinawa

Human resources development

Fostering of industries

Local revitalizationDispatch of lecturers

(endowed lectures)

Students’ business idea competition…etc.

Legal assistanceInternships Manufacturing, agricultural fields, etc.

Joint research and analysis, product development, market expansion, coordinated research matching

University side→Commercialization (utilizing developmental technologies, resources, etc.)Company side→Solution to problems

Human resources development

Manufacturing

Agriculture

Overall industries

Vision for the future (Undertaken by collaborative work)

Vision for the future (Consolidation of framework)

Incorporation of organizational

structure, mutual understanding,

human interaction, transmission of

information

Presentation of developmental

resources, specialized coordinator, matching,

commercialization support

Commercializatio n projects, results

recognition

Within 1 - 2 yearsWithin 2 - 3 years

Within 3 - 5 years

The Bank of Okinawa,Ltd

People’s Bank

40

Shareholder returnsShareholder returns

Branch network strategyBranch network strategy

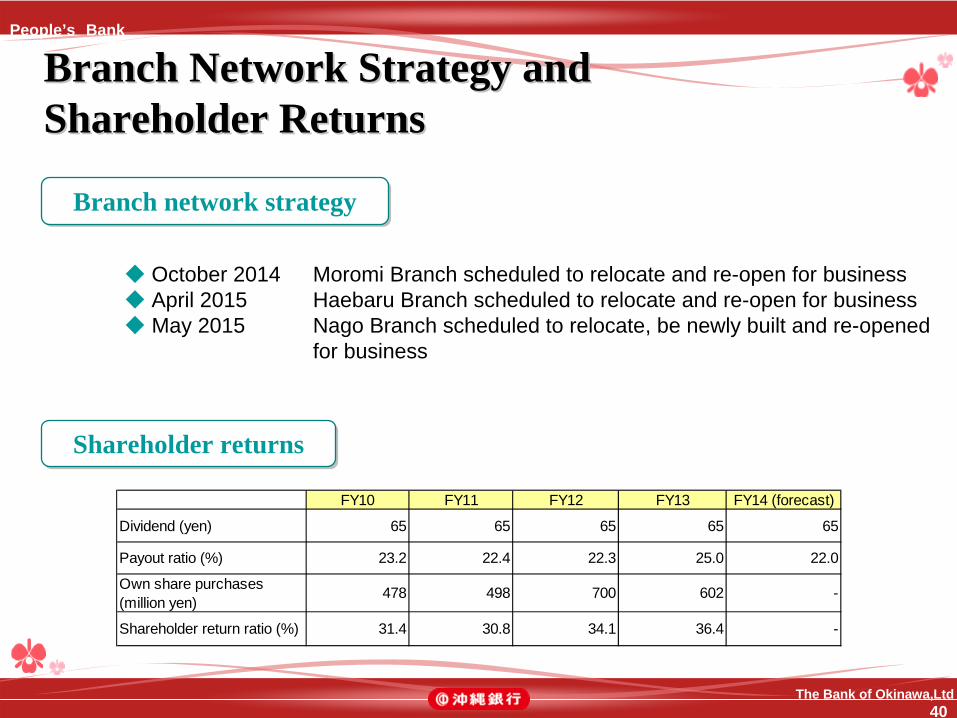

◆ October 2014◆ April 2015◆ May 2015

Moromi Branch scheduled to relocate and re-open for businessHaebaru Branch scheduled to relocate and re-open for businessNago Branch scheduled to relocate, be newly built and re-opened for business

Branch Network Strategy and Branch Network Strategy and Shareholder ReturnsShareholder Returns

FY10 FY11 FY12 FY13 FY14 (forecast)

Dividend (yen) 65 65 65 65 65

Payout ratio (%) 23.2 22.4 22.3 25.0 22.0

Own share purchases(million yen)

478 498 700 602 -

Shareholder return ratio (%) 31.4 30.8 34.1 36.4 -

The Bank of Okinawa,Ltd

People’s Bank

41

Supplemental MaterialsSupplemental Materials

The Bank of Okinawa,Ltd

People’s Bank

42

Business PerformanceBusiness Performance(¥ billion)

Non-consolidatedYoY change

Ordinary income 40.3 36.8 36.8 37.1 +0.3Gross business profit 30.3 28.5 30.2 30.0 (0.2)

Interest income 26.6 25.6 26.9 27.3 +0.3Fees and commissions 1.7 2.0 2.4 2.5 +0.1

Fees and commissions (excluding trust fees) 1.4 1.5 1.8 2.0 +0.2Trust account services 0.3 0.4 0.5 0.4 (0.1)

Other business profit 1.9 0.8 0.8 0.1 (0.7)Gains (losses) on bond trading 1.7 0.6 0.7 (0.0) (0.7)

Expenses (excluding non-recurrent items) 18.5 18.8 19.2 19.9 +0.6Business profit on core banking operations 10.1 9.1 10.3 10.1 (0.1)

Provision of general allowance for possible loan losses (0.2) (1.5) (0.0) 0.6 +0.7Net business profit 12.0 11.2 11.0 9.4 (1.5)

Non-recurrent items (2.4) (2.9) (1.7) (0.9) +0.8Net gains (losses) on equity securities (0.3) (0.6) (0.5) 1.0 +1.5Bad debt disposal (non-recurrent items) 1.8 2.5 1.6 2.2 +0.5

Ordinary profit 9.5 8.3 9.3 8.5 (0.7)Extraordinary gains (0.0) (0.0) (0.0) (0.0) +0.0

Bad debt disposal (amounts posted under extraordinary gains) 0.0 - - - -Net income 5.0 5.1 5.4 4.5 (0.8)

Credit costs 1.5 1.0 1.6 2.8 +1.2Non-performing loan ratio 1.68% 1.63% 1.64% 1.72% 0.08%Capital ratio (calculated under Basel III Standard for FY13) 12.73% 12.25% 11.88% 11.66% -

FY12 FY13FY10 FY11

The Bank of Okinawa,Ltd

People’s Bank

43

Term-end balance / Average balance / YieldTerm-end balance / Average balance / Yield

Loan balance by industrial segmentLoan balance by industrial segment

TermTerm--End Balance, Average Balance, Yield, End Balance, Average Balance, Yield, and Loan Balance by Industrial Segmentand Loan Balance by Industrial Segment

* Term-end and average balances are calculated on the basis of loan/deposit balances of the banking and trust accounts.

* Yields on loans and deposits are those used for domestic operations only.

* Including trust accounts

(\ billion, %)FY10 FY11 FY12 FY13

Loans Term-end balance 1,149.3 1,197.1 1,236.2 1,251.4Average balance 1,109.2 1,121.7 1,154.7 1,202.0Yield 2.51 2.44 2.32 2.17

Securities Term-end balance 446.6 539.9 600.2 577.3Average balance 416.7 509.6 581.8 583.6Yield 0.88 0.61 0.56 0.62

Deposits Term-end balance 1,592.8 1,714.8 1,789.8 1,755.1Average balance 1,512.3 1,670.4 1,706.5 1,745.6Yield 0.29 0.26 0.14 0.11

(\ billion)FY10 FY11 FY12 FY13

Manufacturing 41.2 40.5 37.9 36.6Agriculture and Forestry 0.5 0.5 0.4 0.5Fishery 0.5 0.5 0.5 0.5Mining and quarrying of stone and gravel 1.8 3.9 1.5 1.9Construction 54.4 49.7 47.3 44.7Electricity, gas, heat and water supply 4.0 4.0 2.5 3.5Telecommunications 9.4 10.0 7.9 7.2Transport and postal activities 15.7 16.4 15.0 14.8Wholesaling and Retailing 121.5 116.4 115.7 114.8Finance and insurance 19.2 18.9 22.1 25.0Real estate, and goods rental and leasing 206.2 227.4 261.9 294.8Miscellaneous services 133.9 137.1 137.2 129.5Local government bodies 111.0 123.8 127.3 98.3Others 429.4 447.3 458.4 478.6

Total 1,149.3 1,197.1 1,236.2 1,251.4

The Bank of Okinawa,Ltd

People’s Bank

44

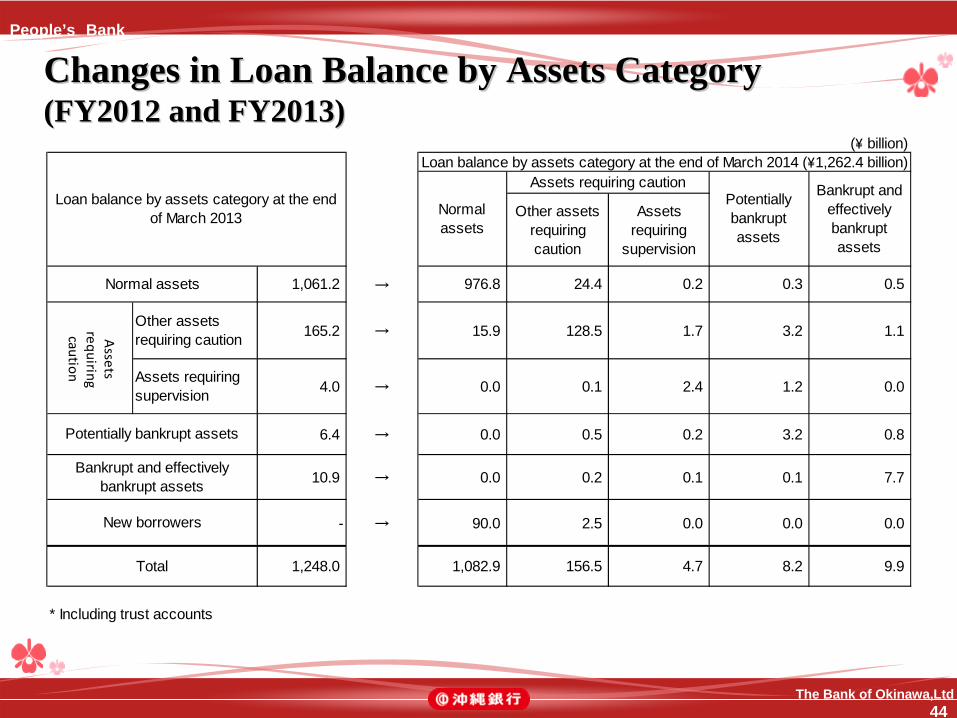

Changes in Loan Balance by Assets Category Changes in Loan Balance by Assets Category (FY2012 and FY2013)(FY2012 and FY2013)

(\ billion)

Other assetsrequiringcaution

Assetsrequiring

supervision

1,061.2 → 976.8 24.4 0.2 0.3 0.5

Other assetsrequiring caution 165.2 → 15.9 128.5 1.7 3.2 1.1

Assets requiringsupervision 4.0 → 0.0 0.1 2.4 1.2 0.0

6.4 → 0.0 0.5 0.2 3.2 0.8

10.9 → 0.0 0.2 0.1 0.1 7.7

- → 90.0 2.5 0.0 0.0 0.0

1,248.0 1,082.9 156.5 4.7 8.2 9.9

* Including trust accounts

Bankrupt andeffectivelybankruptassets

Loan balance by assets category at the end of March 2014 (\1,262.4 billion)

Total

Assets requiring caution

Normalassets

Potentiallybankruptassets

Loan balance by assets category at the endof March 2013

Normal assets

Potentially bankrupt assets

Bankrupt and effectivelybankrupt assets

New borrowers

Assets

requiring caution

The Bank of Okinawa,Ltd

People’s Bank

45

短プラ連動54.1%

固定金利32.9%

手貸、商手(固定分)

8.6%長プラ連動

1.1%

市場連動3.3%

定期性(1年超)

6.4%定期性(1年内)・金銭信

託41.5%

流動性52.1%

高い

低い高い低い

預金計17,898億円

貸出金(平残)貸出金貸出金預金(平残)預 金預 金

貸出計12,362億円

Interest SensitivityInterest Sensitivity

Deposit Loans

Time deposits (up to 1 year) and money in trust

Time deposits (over 1 year)

Current account deposits

HighLow

Total deposits: ¥1,789.8 billion Total loans: ¥1,236.2 billion

High

Low

Fixed interest Market-linkedShort-term prime

rate-linked

Long-term prime rate-linked

Loans on bills/ bills discounted (fixed

portion)8.6%

The Bank of Okinawa,Ltd

People’s Bank

46

Major Economic Indicators in Okinawa Major Economic Indicators in Okinawa PrefecturePrefecture

Unit FY10 FY11 FY12 FY13 FY13(nationwide)

Source

Population (Persons) 1,396,898 1,406,260 1,408,133 1,418,144 127.10 million Okinawa Prefecture, Ministry of Internal Affairs andCommunications (estimated population)

Number of households (Households) 537,981 533,982 541,280 553,958 54.17 million Okinawa Prefecture, Ministry of Internal Affairs andCommunications (The nationwide figure is as of March 2012)

GDP (nominal) (\ billion) 3,725.6 3,795.5 3,912.8 4,050.6 \529 trillion Okinawa Prefecture, (estimates for FY2012 and FY2013)

New car registration (Units) 39,266 38,170 40,506 50,686 5,692,000 Japan Automobile Dealers Association Value

Value of contractsfor public works

(\ million) 244,120 210,803 279,505 263,352 14,571,116 Hosho Jigyo Kaisha Kyokai (Association of guarantycompanies)

Housing starts (Houses) 10,914 11,737 12,713 17,173 987,254 Ministry of Land, Infrastructure and Transport

Number of touriststo the prefecture (Persons) 5,705,300 5,528,000 5,924,700 6,580,300 10,363,904 Okinawa Prefecture, Japan National Tourism Organization

Industrial production index(prior to seasonal adjustment)

(2005=100) 94.8 92.9 98.0 99.0 98.9 Okinawa Prefecture (Average for 11 months between Apr. 2013to Feb. 2014), Ministry of Economy, Trade and Industry

Job offers-to-seekers ratio (Times) 0.31 0.31 0.46 0.57 0.97 Okinawa Labor Bureau, Ministry of Health, Labour and Welfare

Land price change(residential land)

(%, YoY) (1.5) (1.1) (0.6) 0.1 (0.6) Ministry of Land, Infrastructure and Transport

Land price change(commercial land)

(%, YoY) (3.8) (1.4) (0.4) 0.5 (0.5) Ministry of Land, Infrastructure and Transport

* The number of tourists for FY2012 (nationwide) is the visitors from abroad (total number).

The Bank of Okinawa,Ltd

People’s Bank

47

Statements contained in these materials regarding forecasts of future events are based on information known to the management at the time of writing, and do not constitute any form of guarantee of the business performance of the Bank of Okinawa. These materials have been prepared to serve as a report on the settlement of accounts of the Bank for the fiscal 2013 term, ended March 2014, as well as to provide an explanation of the Bank’s future management vision: they are not intended as a solicitation of business.

For further details, please contact:The Bank of Okinawa, Ltd.

General Planning Department,Management Planning Group

Tel: 81-98-869-1253 / Fax: 81-98-869-1464