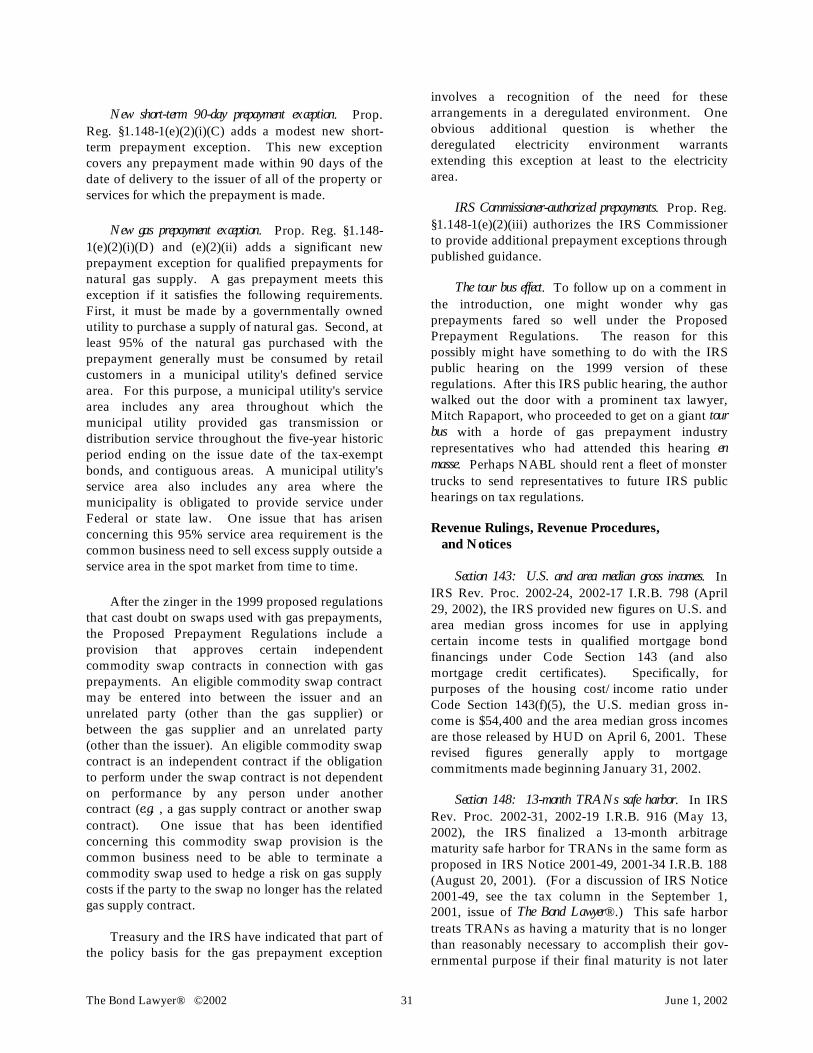

the bond lawyer - nabl · the bond lawyer® ©2002 june 1, ... intended to reflect any position of...

TRANSCRIPT

President's Column (William J. Noth) 1 Washington Saga (William L. Larsen) 2 Friel Medal Nominations Sought 7 Actions by the Board of Directors on March 7 and 8, 2002 (W. Jackson Williams) 7 Actions by the Board of Directors on January 28 and 29, 2002 (W. Jackson Williams) 12 Actions by the Board of Directors on December 4, 2001 (W. Jackson Williams) 13 2002 Washington Seminar (Jeffrey C. Nave) 14 National Office News (Kenneth J. Luurs) 19 Federal Securities Regulation (Paul S. Maco) 20 "Pray to Play" Revisited (Griffith F.Pitcher) 23 Voice From the Past (Manly W. Mumford) 24 Tax Developments at the Crossroads (John J. Cross III) 26 Legal Assistants' Corner (Nancy Mendenhall) 39 Letter to the Editor 41 Book Review 41 Editor's Notes 42

The Bond Lawyer®: The Journal of the National Association of Bond Lawyers ("NABL") is published on or about March 1, June 1, September 1, and December 1 of each year, for distribution to members

and associate members of the Association. Membership information may be obtained by writing to Kenneth J. Luurs, Executive Director, NABL, 250 S. Wacker Drive, Suite 1550, Chicago,

IL 60606-5886, by calling 312/648-9590, or e-mailing [email protected], or at www.nabl.org. ©2002, NABL. Copyright is not claimed for any portion hereof prepared by any official or

employee of the United States of America in the course of his or her official duties, nor for articles or other items separately copyrighted by their authors.

THE BOND LAWYER®

°° °° The Journal of the National Association of Bond Lawyers Volume 23, No. 2 June 1, 2002

The Bond Lawyer® ©2002 June 1, 2002

National Association of Bond Lawyers Officers and Directors William J. Noth ................................................................................................................................................................ President Ahlers, Cooney, Dorweiler, Haynie, Smith & Allbee, P.C.

Des Moines, Iowa Helen C. Atkeson .................................................................................................................................................... President-Elect Hogan & Hartson L.L.P.

Denver, Colorado W. Jackson Williams ......................................................................................................................................................... Secretary Williams & Anderson LLP

Little Rock, Arkansas Linda B. Schakel ............................................................................................................................................................. Treasurer Ballard Spahr Andrews & Ingersoll, LLP

Washington, D.C. Virginia D. Benjamin......................................................................................................................................................... Director Calfee, Halter & Griswold LLP

Cleveland, Ohio John J. Cross III ................................................................................................................................................................ Director Hawkins, Delafield & Wood

Washington, D.C. Meredith L. Hathorn ......................................................................................................................................................... Director Foley & Judell, L.L.P.

New Orleans, Louisiana Monty G. Humble ............................................................................................................................................................. Director Vinson & Elkins

Dallas, Texas G. Mark Mamantov ........................................................................................................................................................... Director Bass, Berry & Sims PLC

Knoxville, Tennessee Jeffrey M. McHugh............................................................................................................................................................ Director Miller, Canfield, Paddock and Stone, P.L.C.

Detroit, Michigan Walter J. St. Onge III..........................................................................................................................................................Director Palmer & Dodge LLP

Boston, Massachusetts J. Hobson Presley, Jr.......................................................................................................................................................... Director Maynard, Cooper & Gale, P.C. Immediate Past President

Birmingham, Alabama Frederick O. Kiel .............................................................................................................................................. Honorary Director Cincinnati, Ohio Editor of The Bond Lawyer® ° ° Kenneth J. Luurs................................................................................................................................................ Executive Director

Chicago, Illinois Publisher of The Bond Lawyer® William L. Larsen ...................................................................................................................... Director of Governmental Affairs Washington, D.C.

Because opinions with respect to the interpretation of state and federal laws relating to municipal obligations frequently differ, the National Association of Bond Lawyers ("NABL") has given the authors who contribute to The Bond Lawyer® , and its editor, the opportunity to express

their individual legal interpretations, opinions, and positions. These interpretations, opinions, and positions, whether explicit or implicit, are not intended to reflect any position of NABL or the law firms, branches of government, or organizations with which the authors and editor are associated, unless they have been specifically adopted by such organizations. For educational purposes, the authors and editor may employ hyperbole or offer suggested interpretations for the purpose of stimulating discussion. Neither the authors, the editor, nor NABL can take responsibility for the completeness or accuracy of the materials contained herein; readers are encouraged to conduct independent research of original sources of authority. The Bond Lawyer® is not intended to provide legal advice or counsel as to any particular situation. Errors or

omissions should be called to the editor's attention: mail to 1095 Nimitzview Drive, Suite 103, Cincinnati, Ohio 45230-4341, or e-mail to [email protected].

The Bond Lawyer® ©2002 June 1, 2002

PRESIDENT'S COLUMN The education of our members and others in the practice of public finance has been part of the Association's mission since its inception in 1979. Many of our volunteer members have devoted tremendous amounts of time over the years to that cause, and we are better lawyers because of their efforts. Our educational program today is second to none in the quality of its offerings for bond lawyers. For many years, NABL's educational program has consisted of four annual seminars: the Bond Attorneys' Workshop, the Tax Seminar, the Fundamentals of Municipal Bond Law Seminar and the Washington Seminar. More recently, NABL has also conducted a handful of teleconferences on selected topics, including the Ethics Teleconference. Each of these has developed its own following among our members, with BAW recently attracting almost one-third of our membership. No organization, however, can afford to put things on automatic pilot, and NABL is no exception. If we are to stay com-mitted to presenting timely, effective and useful programs, it is necessary to reassess our educational programs periodically to determine whether adjust-ments are necessary to better meet the changing needs of our members. Over the past several months, the Board of Directors and our Education Committee (Scott Lilienthal, Chair; Bruce Weisenthal, Vice-Chair) have been doing just that. As the minutes of our March meeting (printed infra) reflect, the Board has determined to "merge" our Tax Seminar and Washington Seminar into a new seminar, to be held for the first time in Fort Lauderdale in February, 2003. Although many of the details are still in flux, we expect the new seminar to address advanced tax and securities law topics both in concurrent general sessions and in smaller break-out sessions on narrower topics. Two co-chairs, one drawn from the tax side of our membership and one from the securities side, will oversee the new seminar, rather than the traditional chair/vice-chair format. David Miller and Jeff Nave (who served as Vice-Chairs of the 2002 Tax Seminar and Washington Seminar, respectively) have agreed to serve as Co-Chairs for the new 2003 seminar. Our March minutes reflect much of the rationale that led to this decision, and I will not repeat it all here. Suffice it to say that the decision was motivated by the desire to use our member and staff resources wisely, and to ensure that our educational programs

are meeting the needs of as many of our members as possible. The new seminar, we think, strikes the appropriate balance in our program and should be a good fit. We hope you are able to attend it. The Board also intends to increase the use of teleconferences in the future. Holding four annual seminars has served to constrain our use of teleconferences a bit, since there has been a natural tendency to want to highlight any significant new developments or guidance at one of our seminars (particularly Tax or Washington). That should be less of a concern with our revamped seminar schedule, and give us more opportunities to address relatively narrow topics through teleconferences. Again, the goal here is a more focused and useful educational program for our members. In closing, I also want to mention that it is time for nominations for next year's officers and directors of the Association. The 2002 Nominating Committee was approved by the Board of Directors at its May 16-17, 2002, meeting, and consists of Hobby Presley (Chair), Cynthia Weed, Foster Clark, Kathleen Crum McKinney and me. (Please see the June 1, 1999, edition of The Bond Lawyer® — on the Website — for a description of the role, responsibility and functions of the Nominating Committee.) This year, I have been truly fortunate to be surrounded by volunteers who have brought a great deal of insight and energy to the tasks at hand. We need your input to ensure that this continues in the future, so please contact any one of the Committee members (by July 15th) with your suggestions for nominees. William J. Noth May 17, 2002 WASHINGTON SAGA

[Noth photo]

The Bond Lawyer® ©2002 2 June 1, 2002

Greetings from Washington. Of course, it

couldn’t last. Not in an election year with control of Congress hanging in the balance. The post-9/11 bipartisan spirit that had Democrats and Republicans singing together on the Capitol steps and showing a united front behind their President began to fray around the edges on domestic issues as early as last October and has continued to unravel. Democrats sensed that, despite the public’s near-unanimous sup-port for the President’s handling of the war on terror-ism, they could criticize his domestic initiatives and advance their own priorities without suffering in the polls. Perhaps the best recent example of this occurred when the Senate rejected oil drilling in the Arctic National Wildlife Refuge as part of major energy legislation passed on April 25. President

Bush had long advocated opening the ANWR to oil exploration as a matter with national security

implications. Moreover, the Senate failed fully to embrace more drilling and production of fossil fuels, a key element of the President’s energy policy, choosing instead to

emphasize increased renew-able resources.

Even though administration energy priorities may yet prevail in the conference committee that will begin work in June to reconcile the House and Senate energy bills, many observers considered the loss in the Senate a major domestic policy defeat for the President and a confirmation that big bipartisan victories such as the 2001 tax cut will be difficult to come by again. In recent days, questions have surfaced about the administration’s handling of early warnings of impending terrorist attacks and flawed intelligence sharing among counter-terrorist and law enforcement agencies. Again sensing election year vulnerability, Democrats have begun to criticize, mostly indirectly, aspects of the administration war against terrorism. Partisan criticism of the White House on this issue would have been unthinkable not long ago. Democrats must still be wary of a patriotic backlash if

they go too far in criticizing the White House, but the Bush administration must also be more careful than in the months immediately following September 11 to avoid overplaying what Senator Richard Durbin (D-Ill.) recently called “the wartime White House defense” as an answer to Congressional inquiries. With bipartisanship fast becoming a distant memory, the Bush administration is all but abandoning post-2000 election rhetoric about cooperation with the Democrats and focusing on regaining Republican control of the Senate and preserving Republican control of the House. As the elections approach, the White House will increase its political involvement, using the President’s continued popularity and the public’s support of his handling of the war on terrorism to keep Democrats on the defensive. Heeding their strategists, Democrats will retreat from criticism of the war on terror and focus on domestic issues where they believe they have an edge over Republicans. Stimulus Bill On March 8, after failing for several months to agree on an economic stimulus package and in spite of widespread forecasts of broadening economic recovery, Congress passed a streamlined stimulus bill. The President signed the Job Creation and Worker Assistance Act (P.L. 107-147) on March 9. The economic stimulus package includes some bond-related measures, in particular a number of provisions designed to provide relief for New York City in the aftermath of last September’s terrorist attacks. The legislation authorizes issuance of up to $8 billion in tax-exempt private activity bonds from 2002-2004 primarily for reconstruction and renovation of both residential and non-residential real property in lower Manhattan. The bonds are not subject to the annual state volume cap, and are exempt from use-of-proceeds restrictions and tenant-targeting rules, as well as the alternative minimum tax. The stimulus legislation provides for an additional advance refunding for the bonds of certain New York City issuers in an amount up to $9 billion. In addition to the New York City relief measures, the stimulus bill extended the Qualified Zone Academy Bond program (which had technically expired last December 31) through the end of 2003. The QZAB program allows issuance of up to $400 million a year of taxable tax credit bonds to renovate schools in poor neighborhoods. Enron Update

[Larsen photo]

The Bond Lawyer® ©2002 3 June 1, 2002

The Enron scandal has faded somewhat from the headlines and nightly comedic monologues. No longer are the eleven Congressional committees which initiated probes into the Enron collapse holding hearings almost daily. However, as a direct result of Enron, Congress is seriously pursuing legislation designed to reform the audit process, improve corporate responsibility, and prevent future abuses. It is still too soon to tell how much Enron will affect regulation and practice in the municipal securities marketplace, but Enron-related reform legislation bears watching, particularly in the area of corporate and auditing accountability. On April 15, 2002, the House passed the Corporate and Auditing Accountability, Respon-sibility, and Transparency Act of 2002 (H.R. 3763). This comprehensive legislation creates a new audit oversight mechanism, consisting of a public regulatory organization to be established under SEC rules. H.R. 3763 also prohibits auditors from offering financial systems consulting and internal auditing services to clients. With respect to disclosure, the bill attempts to improve transparency, move disclosure to “real time,” and improve disclo-sure oversight mechanisms. In an attempt to prevent future corporate abuses, the legislation also prohibits insider trades during pension-fund blackout periods, permits the removal of insider trading profits from trades prior to correction of erroneous financial statements, permits the SEC to bar individuals from serving as officers/directors, and sets forth rules concerning the retention of records. The legislation also requires SEC and GAO studies and recommen-dations in several areas, including rules relating to analyst conflicts of interest, corporate governance practices, enforcement actions, credit rating agencies, investment banks, and model rules for attorneys of issuers. Democrats have criticized the House-passed bill as not being tough enough. A separate, more stringent, accounting reform bill, the Public Company Accounting Reform and Investor Protection Act of 2002, is now under consideration in the Senate. The bill, in the form of a committee print draft, was scheduled for Senate Banking Committee markup this week, but Chairman Sarbanes (D. Md.) postponed the markup until after the Memorial Day recess to give Committee Republicans more time to examine the issues. The Sarbanes measure has drawn heavy opposition from the accounting profession and the business community. In addition to establishing an independently funded Public Company Accounting Oversight Board, the

committee print requires the SEC to promulgate rules to prevent analyst conflicts of interest, and substantially increases the SEC budget. Other Legislative Items Effective May 15, the Treasury suspended sales of State and Local Government series (SLGS) nonmarketable Treasury securities until further notice. Treasury took this action because the statutory debt ceiling has not been raised. The House is considering supplemental appropriations legisla-tion that will likely include language raising the debt ceiling. The Senate also is expected to raise the debt ceiling in its supplemental bill. Raising the debt ceiling is not without controversy, however, and it may be mid to late June before both houses agree to the terms of the supplemental appropriation legislation that will also raise the debt ceiling, thus allowing the Treasury to resume selling SLGS. Both houses have passed comprehensive energy bills (each designated H.R. 4), which are now in conference committee. If approved by the conference committee, certain provisions would affect tax-exempt bonds issued for public power facilities. The House bill includes provisions clarifying the law in the areas of public power participation in competitive electricity markets and the tax-exempt status of bonds issued to purchase prepaid natural gas contracts. The Senate bill includes a provision calling for the Treasury to conduct an ongoing study of tax issues resulting from restructuring of the electric service industry, including the proposed output regulations released in January 2001. With a combined bill totaling over 1500 pages, conferees will literally have their hands full, while focusing on contentious issues such as ANWR drilling, climate change, an ethanol mandate, and electric industry reform. Conference committee negotiations on H.R. 4 are likely to continue through the summer. There is legislation pending in both houses of Congress to repeal the 10-year rule for mortgage revenue bonds. This rule limits the ability of mortgage revenue bond issuers to use the proceeds of mortgage prepayments and repayments to make new home loans. Support for repeal is steadily growing. S. 677 has 60 co-sponsors and H.R. 951 has 320 co-sponsors. Notwithstanding this high level of support, 10-year rule reform still needs a vehicle to advance in the legislative process. Further, repeal of the 10-year rule would cost the Treasury money. In this season of ever-tightening budgetary constraints, Congress may hesitate to act, leaving efforts to reform the 10-

The Bond Lawyer® ©2002 4 June 1, 2002

year rule to carry over to next year. Bankruptcy Reform Currently in conference committee, bankruptcy reform legislation (H.R. 333) faces slow going. Both houses of Congress passed bankruptcy reform bills in March, 2001. The major obstacle for the conference committee is language in the Senate version that would bar the discharge of debts incurred as a result of acts of violence and other protest activities directed at abortion clinics and other targets. The municipal market’s interest in this legislation is in provisions affecting municipal bankruptcy, including a requirement that a municipality receive a court order for relief after filing a petition under Chapter 9 and an enlargement of the scope of section 901 of the Code. Conferees are apparently prepared to continue negotiating for the rest of the 107th Congress. NABL Legislative Proposal Update On November 28, 2001, NABL introduced its legislative proposal for reform of the IRS enforcement program. NABL continues its efforts to broaden understanding and support of the legislative proposal in the issuer community by meeting with industry associations and public interest groups. In the last several months, NABL has met with a variety of groups in various forums. President Bill Noth briefed members of the Muni Council regarding the proposal during the Council’s meeting on March 14. Also in March, I introduced the proposal at a workshop panel at the National League of Cities’ Congressional City Conference in Washington and updated the Public Finance Network on the proposal. In April, Bill Noth spoke about the proposal before the National Association of Higher Education Facilities Authorities. On the same day, Bill Noth, Helen Atkeson, Linda Schakel, Neil Arkuss, John Cross, and I participated in a follow-up conference call regarding the proposal with the Government Finance Officers Association Debt Committee. Several other NABL presentations on the legislative proposal took place in May. Bill Noth addressed the National Federation of Municipal Analysts and the State Debt Management Network Conference of the National Association of State Treasurers. Linda Schakel appeared before the Council of Infrastructure Financing Authorities and chaired a panel discussion on the legislative proposal at the Washington Seminar. Hobby Presley spoke at the spring conference of the National Council of Health Facilities Finance Authorities. Other members of the NABL Board and ADR Task Force will be speaking

to various industry groups in the near future as NABL continues to solicit feedback and get the word out on this proposal. Spring Meetings with Regulators We usually schedule meetings with our Washington-based regulators to coincide with NABL’s May Washington Seminar. This year, NABL leaders again visited the IRS and the SEC. On May 8, NABL met with regulators from the IRS and Treasury. Attending for NABL were President Bill Noth, President-Elect Helen Atkeson, Treasurer Linda Schakel, Board Member John Cross, Tax Committee Vice-Chair Mitch Rapaport, Washington Seminar Chair Ed Oswald and Vice-Chair Jeff Nave, and I. IRS/Treasury attendees included Sarah Hall Ingram of the Office of Chief Counsel, Rebecca Harrigal, Tim Jones, and Rose Weber of the Bond Branch, Charlie Anderson, Cliff Gannett, and Sunita Lough of the Tax Exempt Bond unit of TEGE, Tom Louthan of Appeals, and Steve Watson of Treasury. Discussion centered generally on various guidance and enforcement-related topics. On May 8 at the SEC, President Bill Noth, President-Elect Helen Atkeson, Board Member Walter St. Onge, Securities Committee Chair John McNally and Vice Chair Ken Artin, Washington Seminar Vice Chair Jeff Nave, and I met with Caite McGuire and Josh Kans of the Office of Chief Counsel of the Division of Market Regulation, Martha Haines, Peg Henry, Mary Simpkins, and Alexandra Albright of the Office of Municipal Securities, and Amy Starr of the Division of Corporation Finance. Among other topics, the meeting focused on the OMS’ evaluation of the general condition of the NRMSIR system and various other disclosure topics. Muni Council Meets The Muni Council, an informal coalition of a number of industry groups, including the American Bankers Association, GFOA, ICI, the National Council of State Housing Agencies, NFMA, and TBMA met on March 14-15 in Washington at the Investment Company Institute (ICI). NABL’s representatives to the Council are President Bill Noth and President-Elect Helen Atkeson. Hosted and chaired by the ICI, the March meeting was the first meeting of the group outside the auspices of the MSRB. The Muni Council heard presentations from, among others, the NRMSIRs and the SEC. Bill Noth described NABL’s current projects,

The Bond Lawyer® ©2002 5 June 1, 2002

including our legislative proposal, model opinion, and Article 9 projects. The Council generally identified disclosure improvement goals, including moving toward all-electronic filing of disclosure information by issuers, a central index or repository for disclosure filings, and one-stop filing of disclosure documents. The Muni Council will meet again on September 26-27, 2002. TBMA will chair and host the meeting in New York City. UCC Article 9 Survey Posted and Updated On February 28, NABL posted on its Website schedules developed by the Article 9 Subcommittee of NABL’s Committee on Opinions and Documents that track which states have adopted UCC Article 9 as proposed, and which have in some way preserved their municipal transaction exemption. Since the posting of the original survey, the Article 9 subcommittee received various comments, additions, and corrections from members. Based on this member feedback, Joan Stern, chair of the subcommittee, revised and updated the original schedules, merging two schedules into one and making a number of additions and corrections. On April 30, we posted the updated NABL “scorecard” of state action on amended Article 9 and the municipal transaction exemption. The NABL Article 9 survey was featured in a Bond Buyer article on March 19, and has been well received by members and other industry participants. The Article 9 subcommittee encourages members to continue to send timely corrections and supplemental information so that the information for each state remains complete and current. The subcommittee will continue to update the survey. IRS Advisory Committee for TE/GE Formerly known as the Tax Exempt/Gov-ernment Entities Advisory Committee (TEAC), the IRS advisory committee established to serve as an organized public forum for the IRS and repre-sentatives who deal with employee plans, exempt organizations, tax-exempt bonds, and federal, state, local, and Indian tribal governments now has a new name. The committee is now called the Advisory Committee for TE/GE (ACT). NABL member Perry Israel, of Orrick, Herrington, and Sutcliffe, is one of the two TEAC members appointed to represent the tax-exempt bond community. Perry reports that the ACT will hold a public meeting on June 21 in Washington. At that meeting, there will be a report on voluntary self-correction. Perry continues to encourage people having procedural

problems with the IRS/TEGE to contact him so that he can bring such problems to the attention of the committee and the IRS. NABL Representative to GASAC John Overdorff of Greenberg Traurig is NABL’s new representative on the Governmental Accounting Standards Advisory Council (GASAC). GASAC provides counsel on technical projects, priorities and accounting issues to the Governmental Accounting Standards Board (GASB). GASB recently issued Statement 34, which significantly changed the financial reporting of governments. In upcoming meetings, GASAC will be considering projects related to reporting and disclosure issues. Mr. Overdorff welcomes input from NABL members regarding issues on GASB’s agenda. Notes on the Regulators Three nominations for SEC Commissioner are pending before the Senate Banking Committee. They include Republican Paul Atkins, an accountant; Democrat Harvey Goldschmid, a lawyer and law professor who was SEC general counsel under former Chairman Levitt; and Democrat Roel Campos, a lawyer. Mr. Campos would replace current holdover commissioner Isaac Hunt. Mr. Atkins and Mr. Goldschmid would fill currently vacant positions on the Commission. The three new nominees would join Republican Chairman Harvey Pitt and Republican Commissioner Cynthia Glassman. Hats off to the IRS for developing a Website page devoted to tax-exempt bonds. You can find the IRS bond page at www.irs.gov/bonds. It is a work in progress, but contains a variety of useful information, including a Tax Exempt Bonds Essentials Tax Kit, various forms and publications, selected Internal Revenue Manual materials, Revenue Procedures, PLRs, TAMs, FSAs, Notices, Regulations and other resources. Website/NABLNET Update Speaking of Websites, please visit the NABL Website at www.nabl.org, where we post legislative, regulatory, and other materials that are substantively pertinent to bond law practice. We also send members NABLNET Alerts of significant developments. Our recent NABLNET Alerts have included notice of the NABL Website postings of the NABL Article 9 Subcommittee Survey of State Treatment of Governmental Transfers under Revised

The Bond Lawyer® ©2002 6 June 1, 2002

UCC Article 9; H.R. 3090, the Job Creation and Worker Assistance Act of 2002; SEC Rules regarding Requirements for Arthur Andersen LLP Auditing Clients; IRS Proposed Regulations and An-nouncement regarding Hospital Acquisition Financing Bonds; IRS Proposed Regulations regarding Arbitrage, Investment-Type Property, and Prepayment; and Treasury’s Suspension of Sales of State and Local Government Series Securities. If you are not receiving the Alerts and you would like to, please send your e-mail address to [email protected] with SUBSCRIBE in the subject line. Also, if you change e-mail addresses, please let us know so we can update our records. We welcome your feedback as we continue our efforts to improve the Website as a useful resource for members. Mr. Osbourne Goes to Washington It is not unusual for Hollywood and Washington to cross paths. Politicians love to bask in the reflected limelight of Hollywood celebrities. Nor is it unusual for politicians to get a little starstruck. For example, when Oscar-winning actress Julia Roberts testified on the Hill recently, there was no question of obtaining a quorum of House Appropriations Committee members. Votes were postponed, schedules rearranged, and the hearing room packed with Congressmen eager to be in the same room with Ms. Roberts. Still, when one thinks of official Washington going a little crazy over a Hollywood star, it is not former Black Sabbath frontman Ozzy Osbourne who comes to mind. Yet this same bat-chewing rocker charmed the Washington Establishment, captivated the press, and got considerably more attention than President Bush at the annual White House Correspondents’ Dinner. The Washington Post quotes the following exchange between MTV’s latest star and the President. Ozzy (grabbing his brown and pink

hair): “You should wear your hair like mine!”

President Bush (hesitating): “Second term, Ozzy!”

Now there’s a reason to look forward to a Bush victory in 2004. Bill Larsen Washington, D.C. May 24, 2002

FRIEL MEDAL NOMINATIONS SOUGHT Nominations of recipients of the Association's Bernard P. Friel Medal should be submitted not later than July 1 to Director of Governmental Affairs William L. Larsen, 601 Thirteenth Street, N.W., Suite 800 South, Washington, DC 20005-3875, or by e-mail to [email protected]. The Friel Medal, a high-relief bronze cast of the Association's original seal, may be awarded annually for distinguished service in public finance. Nominees need not be members of the Association, or lawyers, and may not be members of the current Board of Directors. Prior recipients (some posthumous) are Charles P. Carlson (1983), Russell C. Dikeman (1984), Daniel B. Goldberg (1985), Catherine L. Spain (1986), Manly W. Mumford (1987), Huger Sinkler (1987), James W. Perkins (1988), Robert S. Amdursky (1990), Thomas S. Currier (1991), Beryl Anthony, Jr. (1992), Sharon Stanton White (1993), Robert Dean Pope (1994), Joseph H. Johnson, Jr. (1997), Austin V. Koenen (1998), Amy K. Dunbar (1998), Julianna Ebert (1999), Richard H. Nicholls (2000), Robert J. Kutak (2000), and Harold B. Judell (2001). No Friel Medal was awarded in 1989, 1995, or 1996.

ACTIONS BY THE BOARD OF DIRECTORS ON MARCH 7 AND 8, 2002 The Board of Directors met on March 7 and 8, 2002, in Naples, Florida. President William J. Noth presided. Also present were Helen C. Atkeson, President-Elect; W. Jackson Williams, Secretary; Linda B. Schakel, Treasurer; Directors Virginia D. Benjamin, John J. Cross III, Meredith L. Hathorn, Monty G. Humble, G. Mark Mamantov, Jeffrey M. McHugh, and Walter J. St. Onge III; Immediate Past President, J. Hobson Presley, Jr.; Honorary Director Frederick O. Kiel; Kenneth J. Luurs, Executive Director; and William L. Larsen, Director of Governmental Affairs. Report of Director of Governmental Affairs William L. Larsen, Director of Governmental Affairs, made the following report: Legislative Proposal: Since the Board's January meeting in Washington with a number of municipal

The Bond Lawyer® ©2002 7 June 1, 2002

market groups and regulators, outreach and education efforts continue with respect to the Association's legislative proposal. On January 29, 2002, President Noth, President-Elect Atkeson and Governmental Affairs Director Larsen met with the GFOA Debt Committee for a general presentation and questions and answers on the proposal. On February 11, 2002, Treasurer Schakel gave a presen-tation to the annual Washington Legislative Conference of the National Association of State Treasurers. Mr. Larsen is scheduled to appear on a workshop panel at the National League of Cities' upcoming Congressional City Conference in Washington on March 11. In May, Past President Presley is scheduled to speak at the Spring Conference of the National Council of Health Facility Finance Authorities. Also in May, President Noth will be addressing the National Federation of Municipal Analysts and Treasurer Schakel will appear before the Council of Infrastructure Financing Authorities. The Washington office has sent letters to a number of public interest groups that represent issuers offering to meet with group leadership in order to provide speakers on the Association's legisla-tive proposal. The Washington office has received expressions of interest from the Council of Development Finance Agencies and the Health Care Finance Management Association. MSRB Muni Council: President Noth and President-Elect Atkeson will represent the Association at the next Muni Council meeting on March 14-15, 2002. The Muni Council is an outgrowth of an MSRB proposal that public finance interest groups work together to improve municipal securities disclosure. The March meeting will be the first meeting of the group outside the auspices of the MSRB. Both the MSRB and the SEC have been invited to the meeting, which the ICI will hold and chair. UCC Article 9: Opinions and Documents Committee member Ms. Joan Stern has just completed work on a "scorecard" of state action on Amended Article 9 and the municipal transaction exemption. The "scorecard" is now posted on the NABL website. Seminar and Projects: Mr. Larsen reported he is assisting the Washington Seminar panel chairs to obtain government and outside group panelists and to coordinate their participation. In connection with the Washington Seminar, Mr. Larsen will be organizing the meetings with the Internal Revenue Service and Securities and Exchange Commission.

Further, Mr. Larsen was assisting Chair Kristin Franceschi with the pending Model Opinion Review Project and as needed with the Tax and Securities Committee projects. Report of Executive Director Executive Director Luurs made the following report to the Board: Tax Seminar: The recently completed Tax Seminar was well-received, albeit with some reduction in the number of participants compared to the last two years. Attendance was in line with budgeted expectations and it is anticipated that costs have been well contained within budget. Comments from attendees were very positive. Directory: The Association Directory for 2002 is in preparation and is expected to be distributed shortly. Additional Revenue Sources: Mr. Luurs reported on the possibility of several new sources of revenue to help offset increased costs. Mr. Luurs reported that many associations have created partnerships with for-profit organizations, developed new lines of products and services/or expanded the audience for the pro-grams. Thereafter he described a number of possibilities of new sources of revenue, and described their potential utility to the Association. Following this discussion, the Board agreed to request the Membership Committee to consider this matter and to report to the Board its recommendations. Further, the Membership Committee was asked to consider how the Association should plan its 25th anniversary year meeting.

Visit your Website: www.nabl.org

The Bond Lawyer® ©2002 8 June 1, 2002

Strategic Plan President-Elect Atkeson reported to the Board the status of the Strategic Plan and the Board reviewed the most recent draft, including amendments suggested at the December meeting of the Board. During the discussion, several Board members suggested certain language changes which were approved and the Strategic Plan as so modified was unanimously approved, upon motion by Director Humble and seconded by Director Hathorn. As revised and approved, the Strategic Plan will be presented to the Board at its next meeting. By-Laws President-Elect Atkeson presented to the Board a draft of the current By-Laws of the Association and suggested several revisions. The suggested revisions and current draft of By-Laws were discussed extensively without any final action taken. President-Elect Atkeson was requested to prepare another draft of proposed By-Laws revisions consistent with the discussion at this meeting. She was also requested to review the Illinois Non-Profit Corporation statute in making a new proposal with the goal that new revised By-Laws could be considered at a subsequent Board meeting. Expense Guidelines President-Elect Atkeson reported on expense guidelines utilized by the Association and the Board considered current expense guidelines used for seminars, committees, invitees to Association meetings, employees, Bond Attorneys' Workshop Steering Committee members, and Directors. After an extensive discussion concerning expense guide-lines in an effort to create uniformity within the expense guidelines where appropriate, the Board then deferred the matter to be again reviewed and reconsidered at the Board's May, 2002, meeting. Bond Attorneys' Workshop Chairman Mamantov of the Bond Attorneys' Workshop reported on plans for the September, 2002, Bond Attorneys' Workshop. He advised that the Steering Committee would hold its meeting April 8-9, 2002, and hoped to complete plans for the Workshop at that meeting. Chairman Mamantov reported that the current arrangements with the Palmer House extend to 2005 and that the Association should begin plans now for where and at what hotel it wishes to continue the Bond Attorneys'

Workshop in 2006 and subsequent years. President Noth advised that the Board would consider this matter at its May, 2002, meeting. Opinions and Documents Committee The Board liaison, Jack Williams, reported on the current status of the Opinions and Documents Committee's work on the Model Bond Opinion Project. The Committee plans to meet on May 8, 2002, and hopes to submit a report to the Board by June 30, 2002. There followed an extensive discussion of this project; Director Williams was directed to advise the Committee to continue its work and to report progress at the May, 2002, meeting of the Board. Treasurer's Report Treasurer Schakel presented to the Board for its review the final budget of the Association for 2002. Task Force on Alternate Dispute Resolution Past President Presley reported on the status of the Task Force and its work to produce a legislative proposal which is now being considered by the Association. The Task Force had requested that it hold a meeting this year to evaluate the proposal further and see if it should be revised in any respects. Upon motion by Secretary Williams, seconded by Director Benjamin, the Board approved payment of expenses for a meeting of the Task Force. The Task Force was further requested to assess the view of the Association's own membership concerning the legislative proposal and to further discuss means and methods of moving the proposal forward. Would you like to serve on a NABL Committee? Call Executive Director Ken Luurs, 312/648-9590.

The Bond Lawyer® ©2002 9 June 1, 2002

Report of Education Committee Director Benjamin, liaison to the Education Committee, reported to the Board the activities of the Education Committee. The Education Committee had prepared an extensive report and made specific recommendations to modify the current education program of the Association. The Education Committee pointed out that for many years the Association's schedule of education events has primarily consisted of four annual seminars: The Bond Attorneys' Workshop, the Tax Seminar, the Fundamentals of Municipal Bonds Seminar and the Washington Seminar. Most recently, the Association has also conducted several teleconferences on selected topics, including ethics. The Committee had received reports both formally and informally from a number of Association mem-bers, including President Noth, President-Elect Atkeson and members of the Board, raising certain concerns regarding the Association's educational program. Analysis of the Current Program: Major concern has been raised relating to the future of the Washington Seminar. Attendance at this seminar has always been somewhat low, and member interest in the event seems to have declined even further in recent years. The Washington Seminar was originally intended to provide members with an opportunity to interact with regulators from the Internal Revenue Service, U.S. Treasury, and the Securities and Exchange Commission. In recent years, however, these regulators have been participating significantly in other Associations seminars. In addition, the Internal Revenue Service and the Securities and Exchange Commission have significantly expanded their own outreach efforts, including numerous "roundtables" and similar events. Further, there has been a decrease in the output of published guidance and other newsworthy announcements from regula-tors. This combination of factors indicates that the Washington Seminar, as presently constituted, may have outlived its usefulness. Together, the Washing-ton and Tax Seminars typically are attended by approximately 10% of the Association's members each year. Further, it has been suggested that the resources of the Association and its members may be more effectively utilized by reducing the number of annual seminars from four to three. Each seminar requires significant commitments of time and effort from both the Association staff and the members who volunteer

their time. By reducing the number of seminars by one, even if that involves combining aspects of the two previously held seminars, the Association staff can more effectively focus their efforts in organizing the seminars and also be able to devote more time to the additional tasks for which they are responsible. Also, reducing the number of seminars to three would reduce the burden placed on many Asso-ciation members who serve in the critical roles of Chair, Vice-Chair and faculty members for Association seminars. Further, in the current environment of reduced travel budgets, it seems prudent to cut back on the number of times each year that the Association asks members to travel to Association educational events. Proposed New Seminar: In response to the concerns described above, the Education Committee recommended that the Association expand the scope of the current Tax Seminar to include securities law and other topics. Like the Tax Seminar, the new seminar would be targeted toward practitioners who already have achieved a certain level of expertise in the subject matter so that sessions can focus on more advanced topics and issues. The Board discussed the proposal of the Education Committee at some length. Thereupon, Director Benjamin moved, seconded by Director Hathorn, that there be no Washington Seminar in 2003, and that the current Tax Seminar and Washington Seminar be replaced by a new seminar, as described in the Education Committee's report and to be planned by and implemented by the Education Committee and as approved by the Board, to commence in 2003, the site to be Fort Lauderdale, Florida, the planned site for the 2003 Tax Seminar. Director Benjamin also reported that the Educa-tion Committee report recommended that the Association expand its use of teleconferences to be primarily focused on narrowly targeted subjects of special interests to the Association. Upon motion by Secretary Williams, seconded by Director Cross, it was unanimously approved that the Association hold up to two new teleconferences on timely topics of interest to Association members, the planning to commence immediately, the subject matter of each teleconference to be approved by the Education Committee, the Board Advisor to the Education Committee, and the President of the Association. Report of the Securities Law Publication Task Force

The Bond Lawyer® ©2002 10 June 1, 2002

Director St. Onge reported on the Securities Law Desk Book Project. Director St. Onge reported that the Editorial Board, composed of Drew Kintzinger, John McNally, Paul Maco and Thomas Harding, had commenced its activities. Initially, they are working with LexisNexis to develop market data concerning demand for such a volume. LexisNexis has indicated that it would be comfortable moving forward if it could be demonstrated there was demand for at least 400 copies. Consideration will be given to a survey of the membership via NABLNET to test interest for a securities law desk book, similar to the Federal Taxation of Municipal Bonds desk book. Report of the Securities Law and Disclosure Committee Director St. Onge, liaison to the Securities Law and Disclosure Committee, reported that the Committee was moving forward with plans for the Washington Seminar. Among other features, Director Humble will lead a discussion on initial disclosure and Director St. Onge will lead a discus-sion on continuing disclosure. Director Humble advised that he was working on a paper concerning disclosure for variable rate demand bond transactions which would include market perceptions. Director Humble advised that some at the Securities and Ex-change Commission take the view that there should be a disclosure of the underlying credit in variable rate demand transactions, but according to Director Humble the corporate experience in this regard had been different. Report of General Tax Committee Director McHugh, liaison to the General Tax Committee, reported on the status of the Committee's projects. The active substantive guidance projects of the Tax Committee relate to (1) the project on allocation accounting rules under Code Section 141, (2) followup work (including negotiations with the Internal Revenue Service and U.S. Treasury and drafting) relating to Charles Henck's solid waste report, (3) a project, suggested and headed up by Jeanette Bond, on the definition of manufacturing facilities under Code Section 144(a), (4) a project regarding the tax treatment of "naming rights" transactions, and (5) a project regarding tax simplification proposals. On item (1), representatives of the Treasury reported that the Treasury and the Internal Revenue Service are again actively working on this gap in the

regulations and, consistent with the Committee's approach, are going to begin working on smaller, discrete areas of the reserved regulations. The first discrete topic for the Committee is the effect of partnerships on tax-exemption, focusing largely on partnerships between non-profit corporations and partnerships between non-profit and for-profit enti-ties. On (2), the Association representatives met with a number of Internal Revenue Service and U.S. Treasury representatives to discuss the solid waste report in more detail and submitted additional proposals in response to the issues raised at the meeting. At this point, the Committee is waiting for the Internal Revenue Service and U.S. Treasury to move forward on this project. On (3), Ms. Bond has circulated a second draft of her report on the definition of manufacturing facilities under Code Section 144(a). There is no current activity to report on (4), the project concerning "naming rights" transactions. On (5), tax simplification, Director Cross has indicated a willingness to take the lead in writing a proposal on tax simplification in regard to municipal bonds. This paper will go to the Committee for review, and the Committee will report further on this project at the May, 2002, Board meeting. The concept is that this report would be the Committee's project for contribution to ongoing discussions with the Internal Revenue Service and the U.S. Treasury. Report of Legal Assistants Committee Director Mamantov, liaison to the Legal Assistants Committee, provided the report on this committee to the Board. Mr. Eric Ballou has agreed to be the "coordinator" for the completion of the Legal Assistants Handbook. The goal is to complete the handbook this year. The plans for the current panel to be presented at the Fundamentals Seminar will be modified to add more substance to the presentation. If it can be arranged, President Noth and Director Benjamin will meet with the Legal Assistants Committee at the Fundamentals Seminar to discuss its panel and activities generally. The Board discussed the possibility of a teleconference for legal assistants and new attorneys in public finance on selected topics. Report of Membership Committee

The Bond Lawyer® ©2002 11 June 1, 2002

Director Hathorn reported on the activities of the Membership Committee. She reported that consistent with the Board's earlier discussion concerning membership enhancements, the Committee will have a conference call on these issues and would be making its report to the Board at the May, 2002, meeting. The Committee will also discuss possibilities for the Association's 25th anniversary meeting. Ms. Hathorn also reported that in this connection the Membership Committee will utilize the Association's website as part of its efforts. NABL has a JOB BANK for members and public

sector lawyers seeking employment opportunities with private law firms. Contact Executive Director Ken Luurs at 312/648-9590.

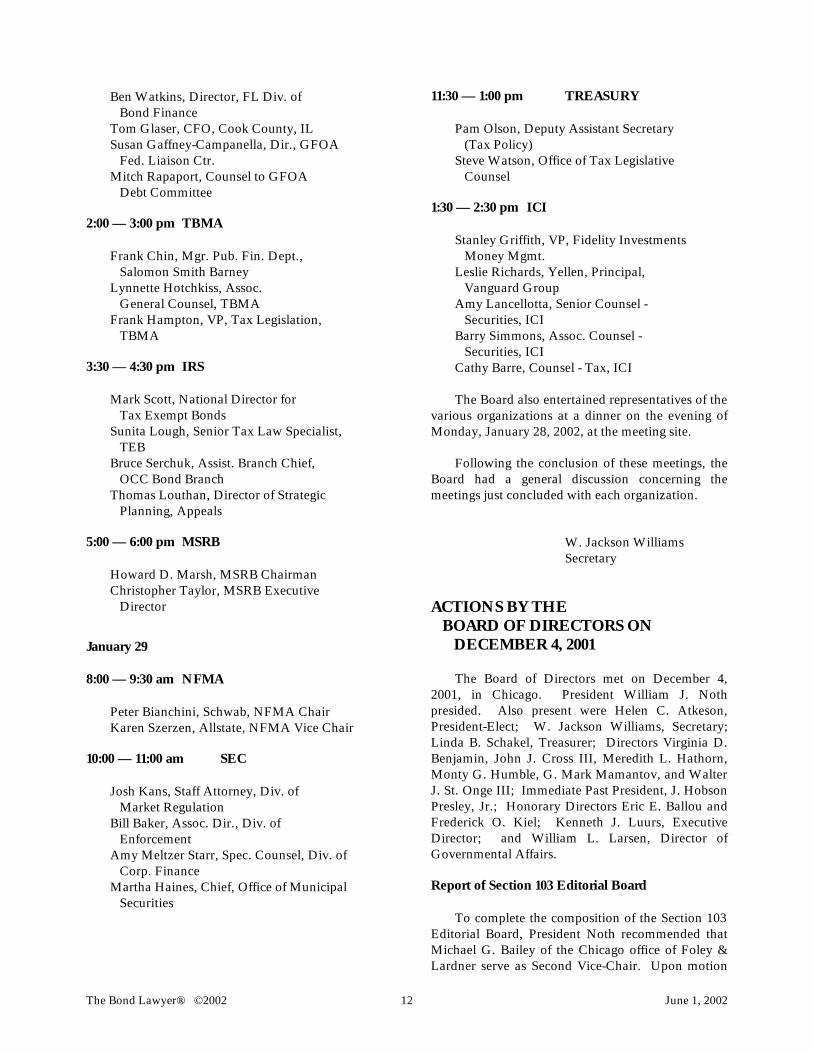

Report of Professional Responsibility Committee Director Humble reported that Mr. Thomas Downs was working on a paper on indemnification requests of bond counsel and that he would have a further report to make on the activities of the Committee at subsequent Board meetings. W. Jackson Williams Secretary ACTIONS BY THE BOARD OF DIRECTORS ON JANUARY 28 AND 29, 2002 The Board of Directors met on January 28 and 29, 2002, in Washington, D.C. President William J. Noth presided. Also present were Helen C. Atkeson, President-Elect; W. Jackson Williams, Secretary; Linda B. Schakel, Treasurer; Directors Virginia D. Benjamin, John J. Cross III, Meredith L. Hathorn, Monty G. Humble, G. Mark Mamantov, Jeffrey M. McHugh, and Walter J. St. Onge III; Immediate Past President J. Hobson Presley, Jr.; Kenneth J. Luurs, Executive Director; and William L. Larsen, Director of Governmental Affairs. Also present was former President Neil Arkuss, Chair of the Task Force on Alternate Dispute Resolution, for portions of the meeting attended by representatives of the Internal Revenue Service and the U.S. Department of the Treasury. Meetings with Representatives of Various Government Agencies and Municipal Finance Organizations President Noth called the meeting to order and advised that a full schedule for the next two days was arranged for the Board to meet with representatives of several government agencies and public finance organizations. The meetings with the respective groups then followed at the various times shown below and with the representatives of each organization as so identified: January 28 Noon — 1:30 pm GFOA Alan Anders, Dir. of Financing Policy, NYC/OMB

The Bond Lawyer® ©2002 12 June 1, 2002

Ben Watkins, Director, FL Div. of Bond Finance Tom Glaser, CFO, Cook County, IL Susan Gaffney-Campanella, Dir., GFOA Fed. Liaison Ctr. Mitch Rapaport, Counsel to GFOA Debt Committee 2:00 — 3:00 pm TBMA Frank Chin, Mgr. Pub. Fin. Dept., Salomon Smith Barney Lynnette Hotchkiss, Assoc. General Counsel, TBMA Frank Hampton, VP, Tax Legislation, TBMA 3:30 — 4:30 pm IRS Mark Scott, National Director for Tax Exempt Bonds Sunita Lough, Senior Tax Law Specialist, TEB Bruce Serchuk, Assist. Branch Chief, OCC Bond Branch Thomas Louthan, Director of Strategic Planning, Appeals 5:00 — 6:00 pm MSRB Howard D. Marsh, MSRB Chairman Christopher Taylor, MSRB Executive Director

January 29 8:00 — 9:30 am NFMA Peter Bianchini, Schwab, NFMA Chair Karen Szerzen, Allstate, NFMA Vice Chair 10:00 — 11:00 am SEC Josh Kans, Staff Attorney, Div. of Market Regulation Bill Baker, Assoc. Dir., Div. of Enforcement Amy Meltzer Starr, Spec. Counsel, Div. of Corp. Finance Martha Haines, Chief, Office of Municipal Securities

11:30 — 1:00 pm TREASURY Pam Olson, Deputy Assistant Secretary (Tax Policy) Steve Watson, Office of Tax Legislative Counsel 1:30 — 2:30 pm ICI Stanley Griffith, VP, Fidelity Investments Money Mgmt. Leslie Richards, Yellen, Principal, Vanguard Group Amy Lancellotta, Senior Counsel - Securities, ICI Barry Simmons, Assoc. Counsel - Securities, ICI Cathy Barre, Counsel - Tax, ICI The Board also entertained representatives of the various organizations at a dinner on the evening of Monday, January 28, 2002, at the meeting site. Following the conclusion of these meetings, the Board had a general discussion concerning the meetings just concluded with each organization. W. Jackson Williams Secretary ACTIONS BY THE BOARD OF DIRECTORS ON DECEMBER 4, 2001 The Board of Directors met on December 4, 2001, in Chicago. President William J. Noth presided. Also present were Helen C. Atkeson, President-Elect; W. Jackson Williams, Secretary; Linda B. Schakel, Treasurer; Directors Virginia D. Benjamin, John J. Cross III, Meredith L. Hathorn, Monty G. Humble, G. Mark Mamantov, and Walter J. St. Onge III; Immediate Past President, J. Hobson Presley, Jr.; Honorary Directors Eric E. Ballou and Frederick O. Kiel; Kenneth J. Luurs, Executive Director; and William L. Larsen, Director of Governmental Affairs. Report of Section 103 Editorial Board To complete the composition of the Section 103 Editorial Board, President Noth recommended that Michael G. Bailey of the Chicago office of Foley & Lardner serve as Second Vice-Chair. Upon motion

The Bond Lawyer® ©2002 13 June 1, 2002

made by Director Hathorn, seconded by Director Onge, the Board resolved that Mr. Bailey be appointed Second Vice-Chair of the Section 103 Editorial Board for 2001 – 2002. Strategic Plan and By-Laws President-Elect Atkeson distributed the memorandum she had prepared describing suggested revisions to the Strategic Plan. There ensued a general discussion concerning the suggested revisions to the Strategic Plan, and suggestions were made for the Strategic Plan to include the concept of encouraging new products and new techniques. There was also discussion concerning leadership issues, and it was understood that those types of changes would require amendments to the By-Laws. At the conclusion of this discussion, President-Elect Atkeson was requested to continue her revisions to the Strategic Plan and also to make recommendations concerning amendments to the By-Laws. The revisions to the Strategic Plan and By-Laws would again be reviewed by the Board at its next opportunity. Washington, D.C., Board Meeting Director of Governmental Affairs Larsen reviewed with the Board the proposed schedule of the Washington Board meeting with various agencies and interest groups in Washington, D.C., January 28 – 29, 2002. All the groups invited to participate in this meeting have committed to participate. President Noth assigned respective Board members to each respective group to coordinate that group’s participation with the Board. President Noth advised that he will initiate a conference call of the Board in mid-January, 2002, to review final arrangements for the Washington, D.C., Board meeting. See you at the Bond Attorneys' Workshop? Tax Seminar President Noth advised that in order for Neil P. Arkuss, Palmer & Dodge, Boston, Chair of the Task Force on Alternate Dispute Resolution, to participate in the 2002 Tax Seminar, Board approval would be required, since he had appeared as a participant in the last three consecutive tax seminars. Upon motion by Director Humble, seconded by Director Benjamin, the Board resolved that Mr. Arkuss be approved to participate fully in the 2002 Tax Seminar to be held in February, 2002, in San Antonio, Texas. W. Jackson Williams

Secretary 2002 WASHINGTON SEMINAR NABL presented its 2002 Washington Seminar on May 9th and 10th under the leadership of Chair Ed Oswald (Orrick Herrington & Sutcliffe LLP) and with a strong slate of panelists and panel topics. The Seminar featured officials from the Securities and Exchange Commission, the Internal Revenue Service and the U.S. Treasury Department, who discussed regulatory and enforcement issues facing the municipal securities industry. In all aspects, the Seminar was a great success. Hollace Cohen (Jenkins Gilchrist Parker Chapin LLP) chaired the Seminar’s lead-off panel, which explored some of the lessons that the municipal securities market can extrapolate from the Enron crisis. After Hollace briefly summarized the bankruptcy proceedings, she turned the discussion over to Bill Doyle (Orrick Herrington & Sutcliffe LLP). Bill provided insight into the due diligence challenges facing counsel in public power financings. Many of these challenges — such as determining the extent to which a municipal power utility may be engaged in power marketing activities, or be exposed to counterparty risks, or be involved in off-balance-sheet financing transactions — have arisen in recent years as municipal utilities have sought to remain competitive during the era of industry deregulation. Bill was followed on the panel by Claire Cohen of Fitch Investors Service, Inc. Claire offered an analyst’s perspective on Enron’s relevance in the context of municipal securities. Enron’s collapse does underscore the analyst’s need to “always be suspicious” and to fully understand a financing structure. Claire touched on the differences between the equity market and municipal debt market, especially in the treatment of off-balance-sheet debt. The SEC’s Release No. 33-8070 was addressed by Martha Haines (Chief, Office of Municipal Securities, Division of Market Regulation). The release suggests that the late filing of annual financial statements audited by Arthur Andersen not be considered as a material breach of a continuing disclosure undertaking if certain conditions are met. Martha also indicated that disclosure regarding special purpose entities (SPEs) was a hot issue that may deserve greater attention by counsel. Paul Saltzman of The Bond Market Association

The Bond Lawyer® ©2002 14 June 1, 2002

highlighted the legislative and regulatory initiatives that the Enron collapse has spawned. These included initiatives regarding the quality and timeliness of financial information (with the suggestion that the Internet will become the preferred means of disseminating information), bankruptcy reform, and greater oversight of rating agencies. While final action is not expected in all of these areas, Paul expected to see some “spill-over” into the municipal marketplace. Paul concluded his comments by observing that investment bankers must continue to be able to rely on professionals, such as accountants and counsel. Monty Humble (Vinson & Elkins LLP) moderated the morning’s second panel, which featured a lively discussion of the disclosure obligations arising in the context of variable rate demand obligations (VRDO) supported by direct-pay letters of credit. This topic has been a perennial favorite at the Bond Attorneys' Workshop, and recently has been aired in The Bond Buyer. Monty offered the money market funds an opportunity to discuss their need for information in the context of VRDO offerings. Stephanie Peterson (Charles Schwab & Co.) and Ruth Levine (Vanguard Investments), both representing the “buy” side on the panel, jointly announced the pending release of the National Federation of Municipal Analysts’ “Best Practices” disclosure guideline for short term obliga-tions. That document is now posted on the NFMA’s Website (www.nfma.org). They also described the lack of disclosure that often accompanies public offerings of bond anticipation notes (e.g., sometimes the investor receives only a notice of sale and must track down at the NRMSIRs other information regarding the issuer), that VRDOs are purchased as long-term investments, and that commercial paper has a very limited secondary market. With respect to new issue disclosure for VRDOs backed by a direct-pay letter of credit, the market fund panelists stated they were most interested in information showing the issuer has a justifiable reason for issuing the debt and that the issuer understands its obligations. They also underscored their need for continuing information in order to comply with Rule 2a-7 under the Investment Company Act of 1940, a topic that was discussed in greater detail during an afternoon session at the Seminar. Monty offered the SEC panelists an opportunity to state their positions regarding the disclosure

practices relating to VRDO offerings. Amy Starr (Special Counsel, Office of Chief Counsel, Division of Corporate Finance) commented on disclosure practices regarding the credit enhancer and the underlying issuer in the context of corporate offerings. She observed that the 1989 and 1994 releases relating to Rule 15c2-12 are noteworthy in the context of municipal offerings. Martha Haines engaged the audience when she queried why disclosure practices regarding insured bonds should differ from disclosure practices relating to VRDOs supported by direct-pay letters of credit. She then closed the morning session by asking bond lawyers to help educate issuers regarding Rule 15c2-12 compliance and to draft more user-friendly continuing disclosure undertakings. John Podesta — President Clinton’s Assistant and Chief of Staff — treated Seminar attendees to an insider’s view of the West Wing and the Washington political scene. His speech dealt with humorous topics, like President Clinton’s ambitions to be a television talk-show host, and sobering topics, such as the inability to achieve a Middle East peace settlement at Camp David. And for those of you who did not attend the Seminar, the television series “The West Wing” received high marks from Mr. Podesta for its relatively accurate portrayal of life within the White House. Continuing with the disclosure theme, Walter St. Onge (Palmer & Dodge LLP) launched the post-lunch crowd into a lively discussion regarding continuing disclosure topics. Walter, Ken Artin (Bryant, Miller & Olive, P.A.) and the other panelists highlighted problems that currently exist in this area. Peg Henry (Attorney-Fellow, Office of Municipal Securities, Division of Market Regulation) presented the audience with findings from the SEC’s examination of continuing disclosure compliance in 30 selected transactions. A handout that accompanied her comments is posted on NABL’s Website (www.nabl.org). Following up on the com-ments made earlier in the day, attorneys on the finance team were encouraged to educate transaction participants, at closing, of their on-going disclosure responsibilities. Stanley Griffith (Vice President/Associate General Counsel, Fidelity Investments Money Management, Inc.) observed that the NRMSIR system, in his view, is ineffective primarily because information cannot be accessed in sufficient time to make investment decisions (which often must be made with little notice). He explained that better

The Bond Lawyer® ©2002 15 June 1, 2002

continuing disclosure is necessary so that money market fund investors can meet regulatory require-ments (e.g., Rule 2a-7 requirements) and their own liquidity, diversity and credit risk requirements. He also mentioned that the Investment Company Insti-tute is looking for a disclosure system that provides free access to information in electronic format and keyed to CUSIP numbers (with CUSIP numbers being included in the preliminary official statement, if possible). Peg Henry offered the Municipal Advisory Council of Texas as an example of a state information depository that satisfied many of these criteria. An issuer’s perspective regarding continuing disclosure was provided by Ben Watkins, the Director of Florida’s Division of Bond Finance. Ben discussed a number of initiatives undertaken by the Government Finance Officers Association. He emphasized the use of CUSIP numbers and The Bond Market Association’s cover sheets when making NRMSIR filings, and suggested that a single depository would be more user-friendly than four depositories. The Seminar turned to tax matters with a panel on NABL’s legislative proposal and IRS appeals, chaired by Linda Schakel (Ballard Spahr Andrews & Ingersoll, LLP). Linda briefed the audience regarding the current status of NABL’s legislative proposal (which is posted on NABL’s Website) and its purpose. She noted that the proposal still is in draft form. Mitch Rapaport (Nixon Peabody LLP) briefly discussed concerns issuer groups have regarding the fact the proposal assigns ultimate liability to the issuer. Bradley Waterman, who has represented clients in tax proceedings relating to municipal bonds, questioned why the IRS would give up its right to commence proceedings against bondholders. Not only would the IRS relinquish a tool it could use to compel issuers to settle, it also might relinquish the ability to collect full tax liability (especially under those circumstances where the issuer is not well funded). On the other hand, Brad expressed the view that the greatest market inefficiency today is the drastic market reaction to news reports that a transaction is under audit (i.e., bonds are liquidated). He believes this is addressed by NABL’s legislative proposal. The regulators on the panel did not comment on the NABL proposal. However, Thomas Louthan (Director, Office of Strategic Planning &

Communications, IRS) related that the IRS is very interested in settling disputes expediently through arbitration. Tom and Mark Scott (Director for Tax-Exempt Bonds, Tax-Exempt and Governmental Entities Division, IRS) closed the panel by informally announcing a new pilot program for mediation of factual disputes in audit situations. The IRS envisions that IRS appeals officers will serve as mediators. As envisioned, the mediation process is expected to result in a factual determination within a 60-day period. The final panel during Thursday’s session of the Seminar explored ethical considerations that arise for tax counsel. Vicky Tsilas (Ballard Spahr Andrews & Ingersoll, LLP) skillfully guided the panel — which also included Thomas Morgan (George Washington University Law School), William Freivogel (formerly of ALAS) and Lloyd Mayer (Caplin & Drysdale Chartered) — through a series of hypothetical sce-narios. Topics discussed included whether ethics rules might be violated if a tax opinion is rendered that does not meet NABL’s opinion standard; whether bond counsel can represent an issuer in a subsequent audit of a transaction for which such counsel rendered the tax opinion; when a new engagement letter may be appropriate for post-issuance guidance regarding tax issues; the degree to which bond counsel might be liable for providing casual post-issuance advice to issuers; and what counsel should do if a client refuses to follow counsel’s advice regarding the need to disclose adverse tax determinations. Friday’s session opened with a panel on federal tax developments, which was chaired by Mike Bailey (Foley & Lardner). The Seminar attendees were treated to a discussion of the recently proposed prepayment and acquisition financing regulations by the principal authors of those regulations — Rebecca Harrigal (Branch Chief, Tax Exempt Bond Branch, IRS), Bruce Serchuk (Senior Technician Reviewer, Office of the Chief Counsel, IRS) and Stephen Watson (Associate Tax Legislative Counsel, Office of Tax Policy, U.S. Treasury Department). The government representatives discussed the proposed prepayment regulations, with a special focus on the natural gas prepayment exception and its relationship to the business purpose and customary exceptions. The natural gas exception, they noted, was intended to address a specific fact pattern that had come to the IRS’ attention. The proposed regulations regarding acquisition financings were summarized by Bruce Serchuk. He

The Bond Lawyer® ©2002 16 June 1, 2002

discussed certain hospital acquisition transactions that provided a backdrop for the regulations. The examples contained in the proposed regulations also were examined by the panelists. The panel session closed with a discussion of regulatory projects the IRS and Treasury Department are likely to undertake in the upcoming year. These included finalizing the output regulations, proposing allocation and accounting rules for output facilities, proposing regulations relating to refunding issues under Section 141 of the Code, and finalizing broker fee regulations for GICs and defeasance escrows under Section 148 of the Code. No Washington Seminar would be complete without a discussion of IRS enforcement initiatives. Mary Reichart (Bryan Cave LLP) presided over a panel that included Cliff Gannett (Manager, Outreach, Planning and Review, IRS), Charles Anderson (Manager of Tax-Exempt Bonds, Field Operations, IRS), Mark Scott and Timothy Firestine (Director of Finance, Montgomery County, Maryland). The panelists discussed the IRS’ new audit guidelines that are likely to be released soon in the form of an Internal Revenue Memorandum. The guidelines will provide procedures for following the IRS work plan, will address the audit “referral” process (i.e., audit “snitch” letters from inside and outside the agency), among other things. It is expected that IRS audit letters will indicate whether an audit is triggered by a “referral” or whether the audit is a targeted area compliance audit. The new policy guidelines also are expected to provide clearer guidelines on settlement of enforcement actions. The panelists also discussed the difference between the IRS’ Outreach Program and the Voluntary Closing Agreement Program (VCAP). The Outreach Program is intended to provide an opportunity to have dialogue between IRS and industry groups, whereas VCAP is intended to be used where an issuer wants to fix the problem but self-correction remedies (e.g., yield reduction payments) are not available. Change in use is the most prevalent issue arising in VCAP proceedings, followed by advance refunding escrows failing to roll into zero-coupon SLGs. The VCAP process is intended to result in a settlement agreement between the issuer and the IRS. The IRS representatives suggested that an issuer should commence the VCAP process by offering the

IRS some form of consideration (e.g., be willing to pay something or redeem outstanding obligations). If no consideration is offered, the IRS will refer the matter out of VCAP on the grounds that the issuer is looking for resolution of a legal issue. Legal issues are resolved through the private letter ruling process. Mark Scott briefly discussed the special closing agreement program for hospital affiliation transactions announced in IRS Announcement 2002-43, and asked for comments on the issue of how interest on variable rate bonds should be calculated for purposes of determining the closing amount. (The IRS informally had adopted the practice of determining tax liability based on the variable rate applicable at the time of settlement. In hospital acquisition/affiliation VCAP proceedings under Announcement 2002-43, the hospitals have suggested that the IRS calculate interest based on a rate that could be achieved had the issuer entered into a fixed rate swap for its variable rate bonds, which amount usually is higher than the variable rate on the settlement date. This would lower the amount of tax exposure for these transactions because the settlement amount under Announcement 2002-43 is a percentage of the arbitrage profits on the escrow investments purchased in such transactions.) The panelists also discussed “Round Two” of the IRS’ yield-burning audits, in which the IRS is targeting investment banking firms. The IRS apparently has found that certain firms involved in yield-burning audits settled through 1994 had yield burning problems for later deals. With respect to TRANs under audit, concerns were noted with TRAN pools that apparently borrowed for entities that indicated no need for working capital financing. The panelists also observed that the IRS’ solid waste audits have raised generic Section 142 issues beyond whether the targeted waste stream has value. Other issues arising on audit include: qualified 501(c)(3) bonds being threatened by unrelated business income; the reasonableness of issuer expectations in the context of loan pools involving poor origination history on multiple deals; “telephone book TEFRAs” (i.e., the practice of including a laundry list of potential borrowers/projects in TEFRA notices where money is not originated for those projects); and, for multi-family housing projects, the IRS is finding that tenants are not meeting the income requirements of Section 142(d) of the Code. The panelists turned their attention to issuer liability for tax exposure and the wisdom of NABL’s legislative proposal. The global settlement of the

The Bond Lawyer® ©2002 17 June 1, 2002

yield-burning audits was offered as a prime example of a situation where the IRS was able to pressure investment bankers into settlement because issuers did not have statutory tax liability. Mark Scott concluded the Seminar by officially announcing the IRS’ proposed mediation program. The pilot program probably will last for one to two years and will involve factual issues only. The IRS envisions that the mediation process will occur after an initial audit letter is received by the issuer and before the preliminary determination letter is mailed. The issuer will have the discretion to elect into the mediation process. The issuer and the IRS agent will jointly select the mediator and the Office of Appeals will fund the process. The Office of Appeals has committed to completing the mediation process within 45 to 60 days.

Through the tireless work of Ed Oswald, Seminar Chair, and Bill Larsen, Director of

Governmental Affairs, as well as the panel chairs and NABL’s dedicated staff in Chicago and Washington, D.C., NABL pulled off another great

Washington Seminar. Limited supplies of the written materials for

the Seminar may be purchased from NABL’s Chicago office. Jeffrey C. Nave Foster Pepper & Shefelman PLLC Vice-Chair Washington Seminar

NATIONAL OFFICE NEWS

We have enjoyed nearly a year in our new offices. Normally, our year has some ebbs and flows in workload. This year has been one of constant activity. My thanks to everyone for their patience.

This summer will be spent making plans for locations for some of our upcoming meetings. This fall's Bond Attorneys' Workshop will be held at the Palmer House Hilton in Chicago on September 18-20. The Capital Steps will be performing at this year's luncheon, providing insightful humor and comment on the latest happenings in our nation's capital. We hope to be able to open a members-only section of the NABL website and have materials available for download there that have only been available via print in the past. We hope to forward information to you later this year. Finally, for subscribers to Federal Taxation of Municipal Bonds, you now have free access to a new component: a web-based version, which contains all of the material included in the 9-volume loose-leaf set plus the full texts of the IRS' Private Letter Rulings and Technical Advice Memoranda, which are summarized in the loose-leaf set. This product offers access to all this material via your internet browser (Internet Explorer or Netscape Navigator); easily locate the material you need by browsing, full-text search or citation cite, tables of contents, or tables of authorities. You can perform a simple search or quickly focus your research with advanced search techniques. On-line help is available along with search tips and there are frequent updates. Finally, you can print information out in very printer-friendly formats. Access to the content on the site is exclusively available to subscribers to the complete set of FTMB products at no additional charge. The public home page for this new product is located at www.lexisnexis.com/ municipalbonds. To access the content on the site, you must have a username and password provided by LexisNexis. (Note: your Lexis .com ID is not compatible with this product.) To obtain your username and password, send a brief e-mail message to llp.clp@ lexisnexis.com with "FTMB" in the subject line and the following required information in the message body: Firm or organization name Account number User's first name User's last name User's e-mail address User's phone number User's fax number

[Luurs photo]

The Bond Lawyer® ©2002 18 June 1, 2002

No other information is required in the body of the e-mail message. Upon receipt of the e-mail, LexisNexis will send the username and password to the user's registered e-mail address. Your subscription to Federal Taxation of Municipal Bonds includes a single-user license to this new site. Please contact LexisNexis at [email protected] for multi-user pricing and to order additional licenses. If you have any questions about the new site, please contact LexisNexis at [email protected]. If you have any questions about your subscription, please contact LexisNexis Customer Service at 1-800-833-9844, Option 5. Kenneth J. Luurs May 24, 2002

FEDERAL SECURITIES

REGULA-TION

TURNED

AROUND BY UP-DATE AND BRING-DOWN? PERHAPS THIS WILL

HELP. A continuing disclosure topic that from time to time