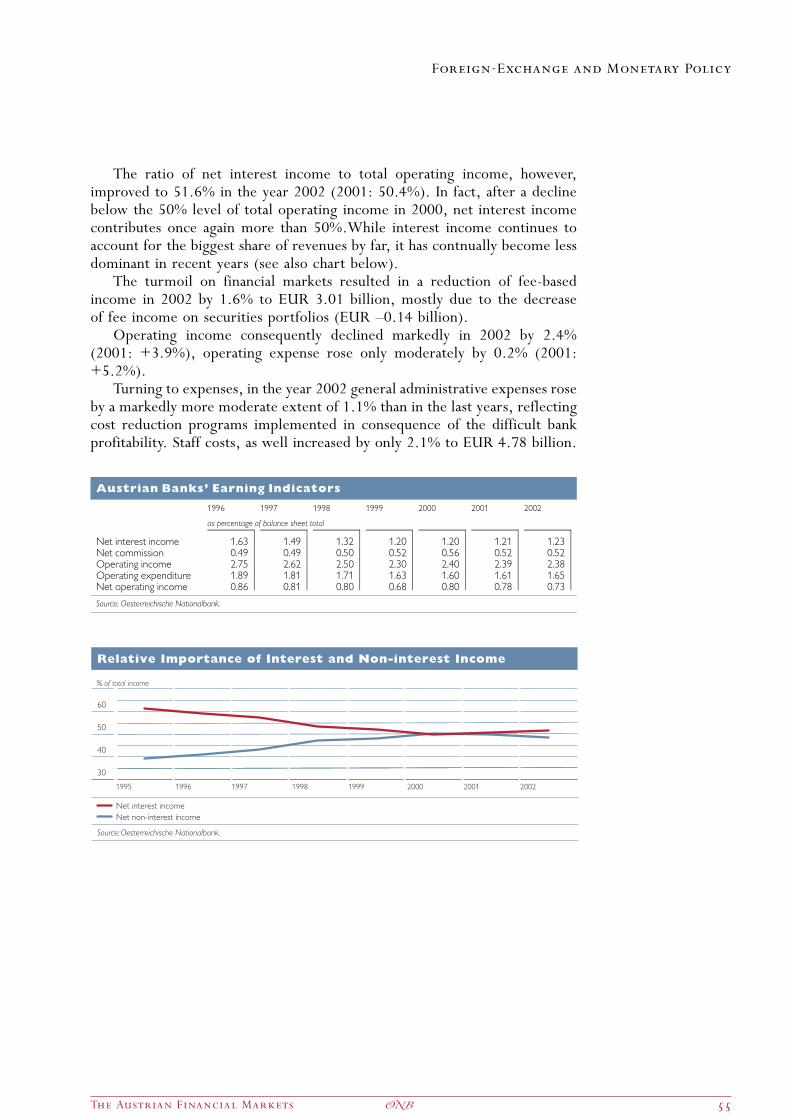

the austrian fianancial markets - startseite847bfb6d-7c14-4075-a666-9b9fdd66eff3/... · financial...

TRANSCRIPT

Oesterre i ch i s che Nat ionalbank

&

Financial Markets Austria Services Ltd.

The Austrian Fianancial Markets

A Survey of Austria�s Capital Markets

Facts and Figures

Revised Edit ion 2003

Published and produced by:Oesterreichische Nationalbank in cooperation

with Financial Markets Austria Services Ltd.

Editor in chief:Wolfdietrich Grau

Secretariat of the Governing Board and Public Relations

Oesterreichische Nationalbank

Edited by:Ulrike Oschischnig

Financial Markets Analysis and Surveillance Division

Oesterreichische Nationalbank

Karl Wagner

Oesterreichische Kontrollbank AG / Financial Markets Austria Services Ltd.

Printed and produced by:Oesterreichische Nationalbank

Printing Office

Inquiries:Oesterreichische Nationalbank

Secretariat of the Governing Board and Public Relations

Otto-Wagner-Platz 3, A-1090 Vienna, Austria

Postal address: P. O. Box 61, A-1011 Vienna, Austria

Telephone: +43-1-404 20, ext. 6666

Fax: +43-1-404 20, ext. 6696

http://www.oenb.at

Orders:Financial Markets Austria Services Ltd.

attn. Karl Wagner

Am Hof 4, A-1010 Vienna, Austria

Telephone: +43-1-531 27, ext. 2512

Fax: +43-1-531 27, ext. 5816

e-mail: [email protected]

Oesterreichische Nationalbank

Secretariat of the Governing Board and Public Relations

Otto-Wagner-Platz 3, A-1090 Vienna, Austria

Postal address: P. O. Box 61, A-1011 Vienna, Austria

Telephone: +43-1-404 20, ext. 6666

Fax: +43-1-404 20, ext. 6696

http://www.oenb.at

This publication is designed to provide accurate information in regard to the subject matters covered. The information has been

carefully prepared and has been drawn from the most reliable sources available. Nevertheless, the publishers cannot be held responsible

for its accuracy. It is distributed with the understanding that the publishers are not engaged in rendering legal, accounting or other

professional service.

Copy deadline: May 2003

The publication of a brochure providing easy access to continuously updatedinformation on the Austrian capital markets to the international investmentcommunity was one of the first suggestions developed within the frameworkof the reform initiative currently undertaken by participants in the Austrianfinancial market. This brochure, jointly edited by the Oesterreichische Natio-nalbank and Financial Markets Austria Ltd., a subsidiary of OesterreichischeKontrollbank AG (OeKB), is the result of continuous efforts and the commitmentof a number of contributors.

We would like to express our sincere appreciation for their contributionsto the Federal Ministry of Finance, OMV Aktiengesellschaft, The FinancialMarket Authority, the Austrian Institute of Economic Research, O‹IAG O‹ sterrei-chische Industrieholding AG, O‹VFA O‹ sterreichische Vereinigung fu‹r Finanzanalyse undAnlageberatung (Austrian Association of Financial Analysis and Asset Manage-ment), KPMG Alpen-Treuhand Gesellschaft mbH and Dr. Po‹ch, legal counselorto OeKB.

A lot of input and expertise have been provided by the Wiener Bo‹rse AG (theVienna securities and derivatives exchange) and numerous banking and finan-cial institutions active in the Austrian and international capital markets, as wellas the experts who contributed to the brochure and are named in the brochureas contacts for further details.

The Austrian Financial Markets 3�

Acknowledgment

1 Preface by:

The Austrian Federal Minister of Finance 8The Governor of the Oesterreichische Nationalbank 10The Government Representative for the Capital Market 12

2 Focus on Special Topics

2.1 Cross Border Settlement in the EU 162.2 The Financial Market Authority (FMA) 182.3 Wiener Bo‹rse AG 212.4 Austria in Central Europe 22

3The Economy

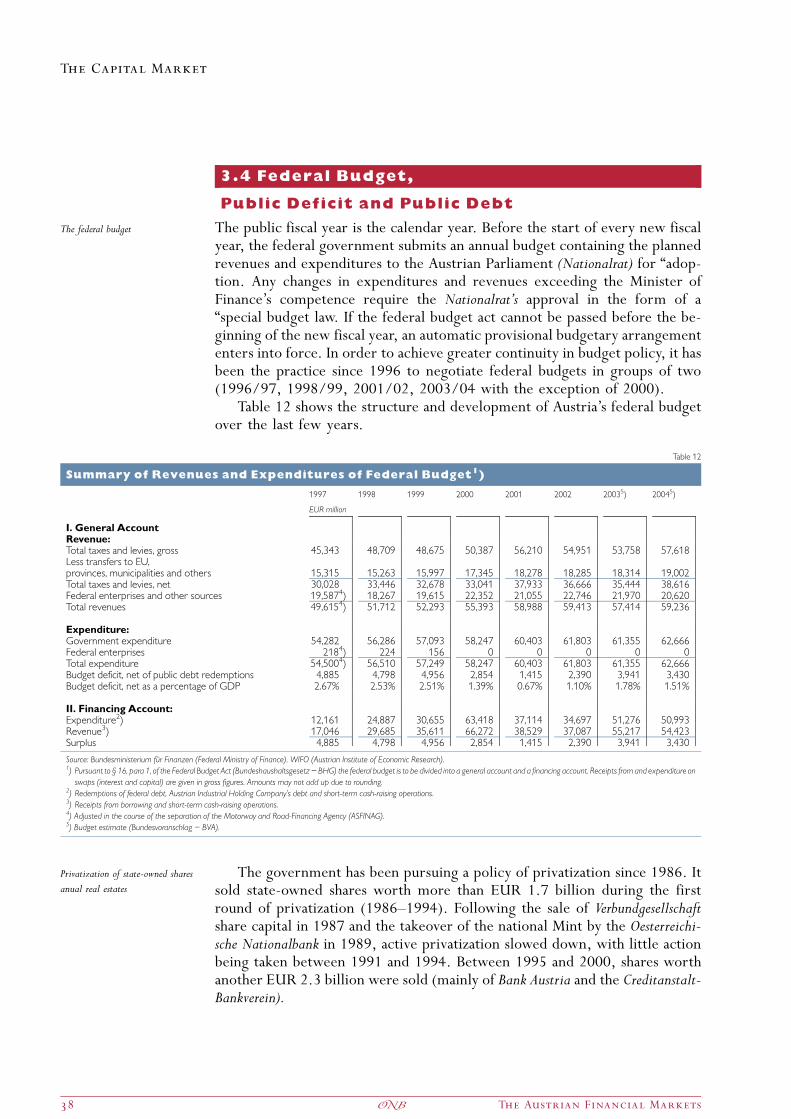

3.1 Economic Structure and Selected Indicators 283.2 Foreign Trade and the Balance of Payments 333.3 Labor, Education and Social Services 363.4 Federal Budget, Public Deficit and Public Debt 38

4Monetary Policy

4.1 The Oesterreichische Nationalbank — Central Bank of Austria 444.2 Monetary Policy 464.3 The Banking System 48

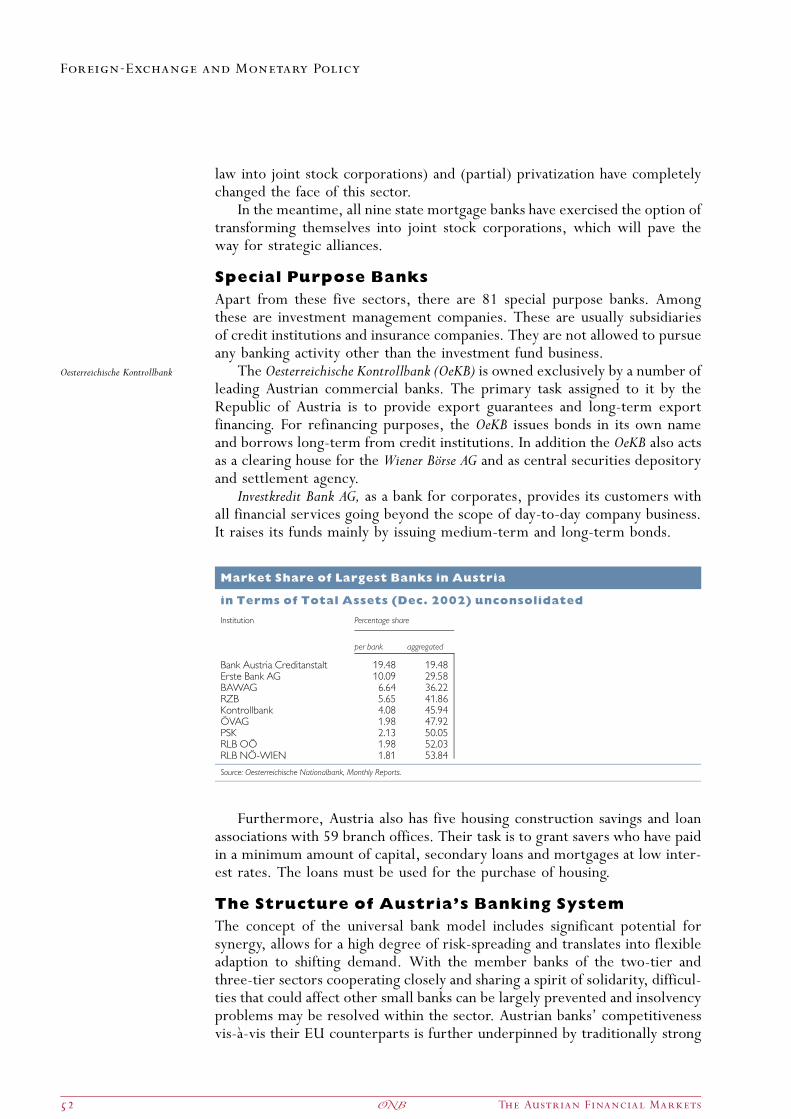

Introduction 48Joint Stock Banks 49Savings Banks 49Cooperative Banks 50State Mortgage Banks 51Special Purpose Banks 52The Structure of Austria�s Banking System 52

4.4 Supervisory Requirements 56Capital Requirements for Credit and Market Risks 56Future Capital Framework 56Risk Weighting 57Other Risks 57Supervisory Review Process 58Market Discipline 58

5The Capital Markets

5.1 Wiener Bo‹rse AG 60The Central Role of Wiener Bo‹rse in the Austrian Capital Market 60Future Strategy of Wiener Bo‹rse 60Added Value Services based on Competence and Know-how 60The New Market Segmentation of Wiener Bo‹rse 60New CECE indices in Euro on the otob market 60Campaign Targeting Private Investors 61Investor Relations Campaign of the Listed Companies of Wiener Bo‹rse 61Cooperation with Banks 61Initiative to Promote the New Retirement Product 61Initial Public Offering Campaign 61

4 The Austrian Financial Markets�

Table of Contents

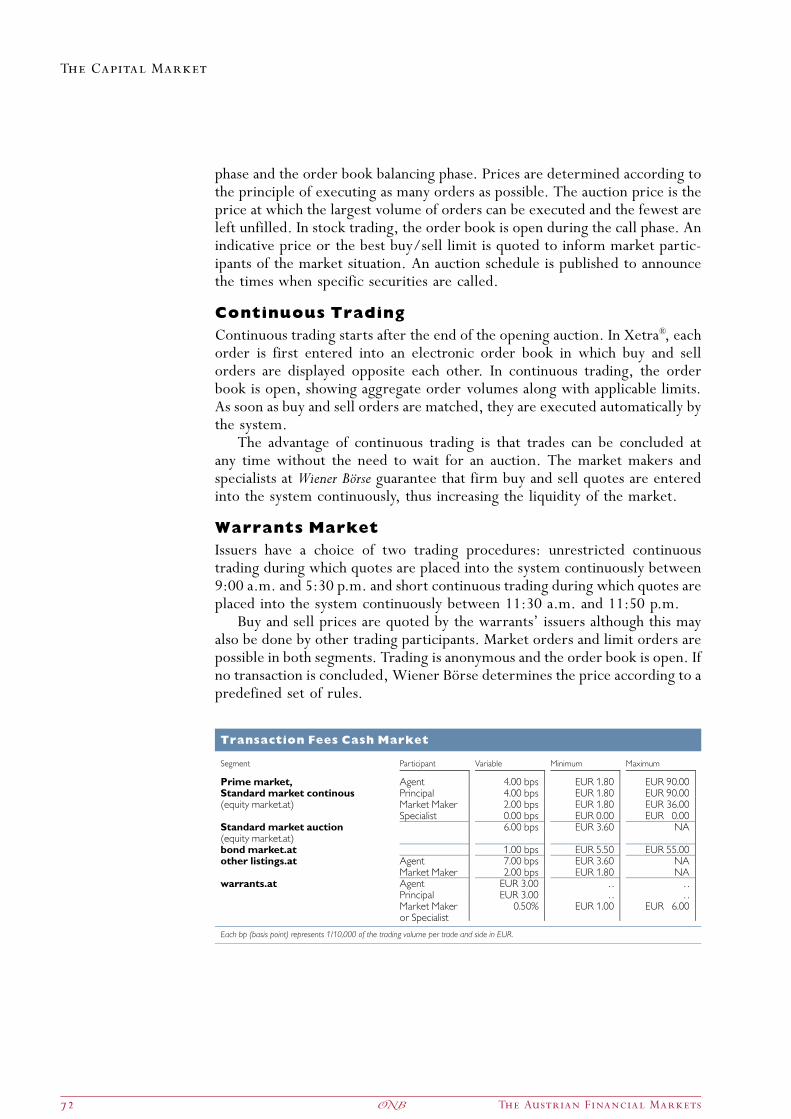

Initiative for the Development of Austrian Investment Funds 62The Committee for the Austrian Capital Market 62Austrian Code of Corporate Governance 62EXAA 62Outlook 62The Market Segmentation on Wiener Bo‹rse 63A. equity market.at 63B. bond market.at 65C. otob market.at 65D. warrants.at 65E. other listings.at 65Listing on Wiener Bo‹rse 66Xetra¤ — The Trading System on the Cash and Warrants Market 71Cash Market 71Auction 71Continuous Trading 72Warrants Market 72The Clearing and Settlement System (Arrangement) 73The Depository System 74Wiener Bo‹rse Membership 77Membership Fees 78List of Members of Wiener Bo‹rse AG 79

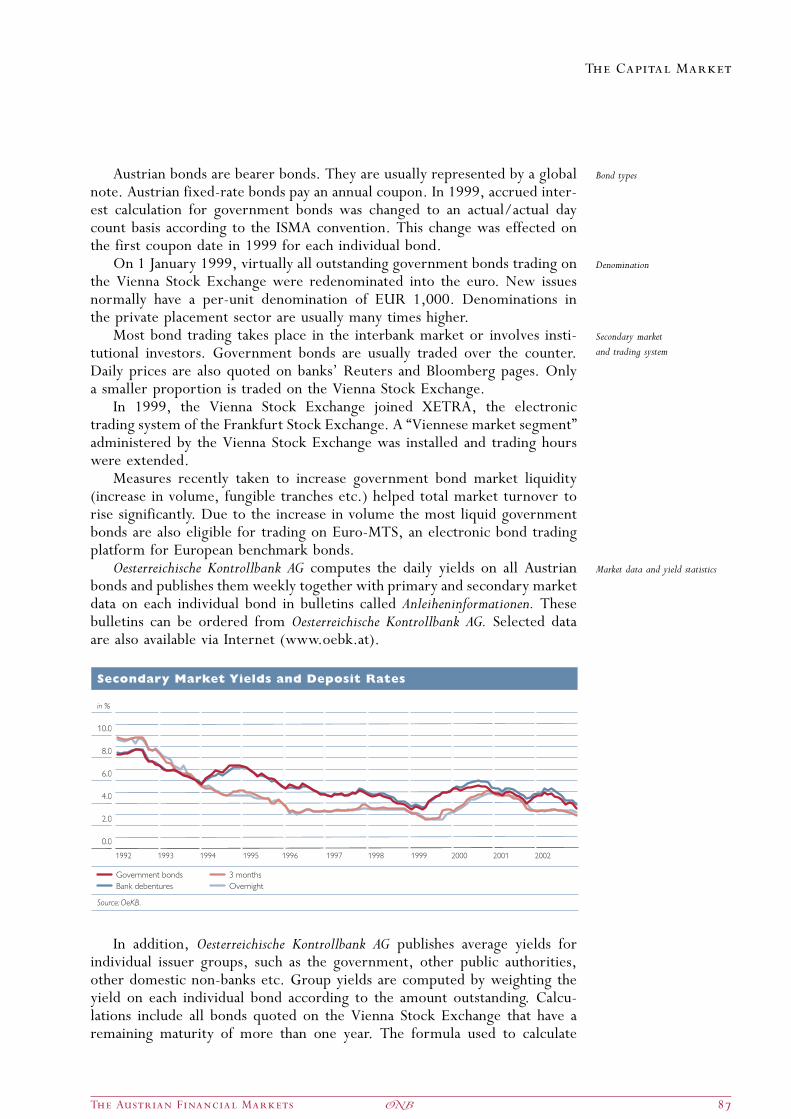

5.2 The Austrian Bond Market 83Recent Performance and Developments 83The Characteristics and Scale of the Market 83Market Structure 84The Auction System for Government Bonds 88Bond-Market Indices 91

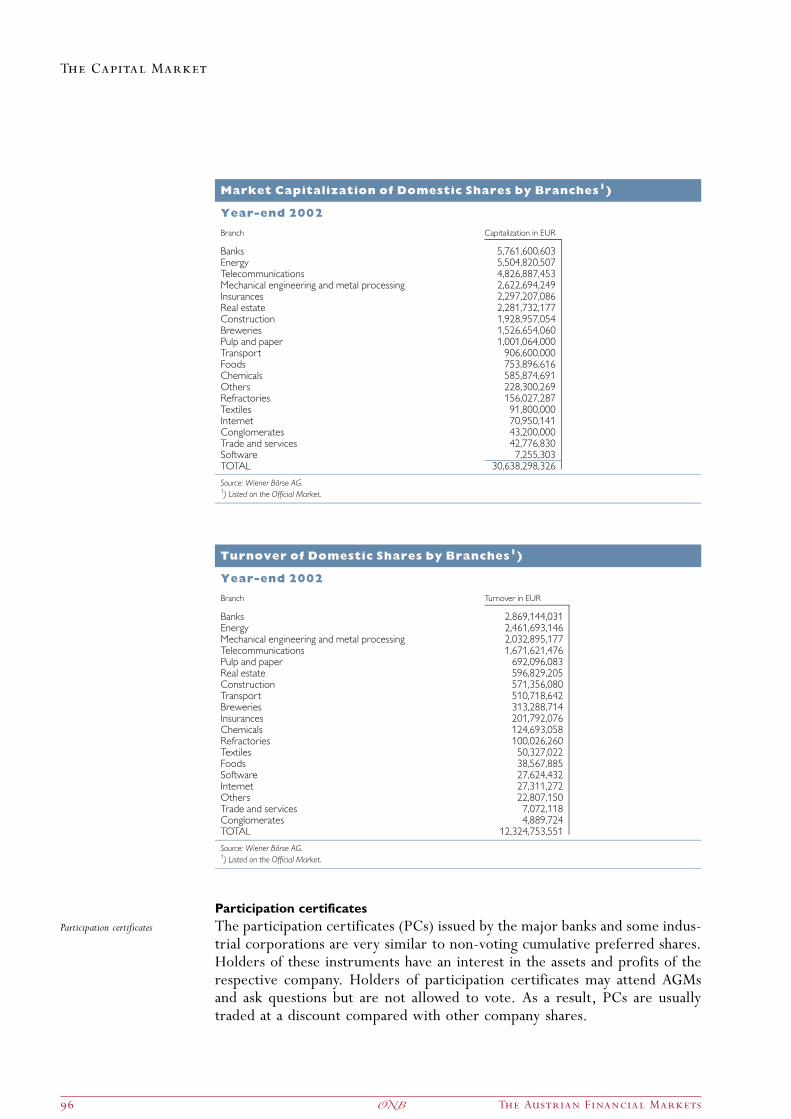

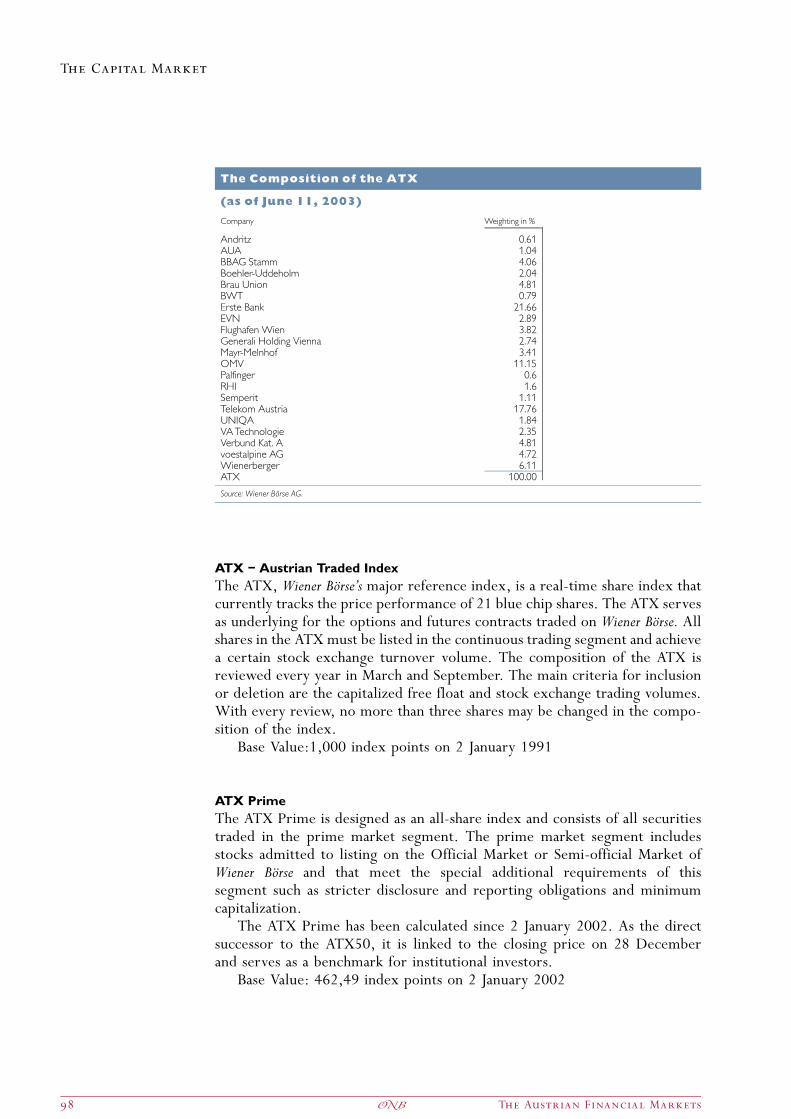

5.3 The Austrian Equity Market 92Index Performance 2002 92The Structure and Scale of the Equity Market in 2002 93The Different Types of Shares Traded on Wiener Bo‹rse AG 95Austrian Shareholders 97The Indices Traded at Wiener Bo‹rse 97

5.4 otob market.at — Wiener Bo‹rse�s Derivatives Market 101A. Austrian Derivatives 101B. The CECE Index Family 101Trading and Clearing on the otob market 102

5.5 Privatizations in Austria 1045.6 The Capital Markets Act 108

General 108Public Offer 108Prospectus 108Notification Office 108

The Austrian Financial Markets 5�

Table of Contents

Annex

Facts and FiguresA. Key Facts on the Republic of Austria 112B. Recent Economic Developments and Outlook 117C. Capital Market Data 119

C.1 The Bond Market 119C.2 The Equity Market 122C.3 OTOB — Derivatives Market 124

D. Financial Data Service by Oesterreichische Kontrollbank AG 126E. Exchange Data Provided by Wiener Bo‹rse 128F. Accounting Standards for Austrian Companies 129G. Taxation 131H. Useful Addresses and Telephone Numbers 145I. List of Sources and Bibliography

Pertaining to Austria�s Capital Markets 147

6 The Austrian Financial Markets�

Table of Contents

I

Preface

Nowadays financial markets are becoming more and more important for thereal economy: dynamic developments such as globalisation, liberalisationand product innovation are leading without doubt to a more efficient alloca-tion of capital. The other side of the coin is the higher financial vulnerabilitydue to steady integration of the markets.

In this respect much more emphasis has been laid lately on preserving andimproving the stability of the financial markets. On national level we havealready taken important steps by creating the new Financial Market Authority(FMA) which assumed all operative tasks of the supervision of the banking,insurance, securities and pension funds. Due to the integration of all sectorswithin a single authority, close examination of cross-sector aspects, whichoften impose higher threats to financial stability, is therefore granted. Further-more, the close co-operation between the FMA and the OesterreichischeNationalbank in certain fields of supervision is an important aspect of guaran-teeing the stability of the finance markets. This relatively new level playingfield for supervision is currently being assessed by an IMF/Worldbank-initia-tive (FSAP — Financial Sector Assessment Programme), which will provide auseful check of the organisation and functioning of the Austrian supervision ofthe financial system in practical terms. Recommendations by the IMF will behelpful for further improvements of the supervisory framework and finally ofthe stability of the Austrian financial markets.

As to the EU level, the importance of further convergence of supervisorymethods and of closer co-operation amongst the competent authorities hasbeen recognised by the EU-Member States. Experience has shown, that acountry can not take isolated measures any more in case of severe problems.In order to lay the ground for common activities, EU-Member have thereforeagreed to apply the �Lamfalussy framework� to all financial sectors in order tomake EU arrangements for financial regulation, supervision and stability moreefficient, effective and flexible. In addition regular intense discussions offinancial market developments with special emphasis on cross-sector andcross-border aspects take place in order to gain good oversight and a coherentview on the situation on the markets.

The new capital adequacy regulation (�Basle II�) will certainly contributeas well to the goal of increasing the stability in financial markets by demandinga more comprehensive treatment of risks and by strengthening the supervisorybodies. The discussions here are in a final stage, the recommendations by theBasle Committee are expected to be published in October 2003.

The severe correction in stock market valuations and the increased risk-aversion we can observe since the last years were amongst others caused bya series of corporate governance scandals world wide. In order to restorethe investor�s confidence the Austrian Corporate Governance Code has beendrawn up, addressing specifically enterprises that raise funds through capitalmarkets. It consists of a set of rules, which lay down the principles of goodcorporate governance and which can therefore be said to constitute an impor-tance source of guidance for investors. It is a voluntary self-regulatory initia-tive laying emphasis on reporting transparency, quality of co-operationbetween supervisory board, management board and shareholders, and alsotaking into account long-term value creation. On EU-level the EU Commis-

Karl-Heinz GrasserAustrian Federal Ministerof Finance

8 The Austrian Financial Markets�

Preface

sion has also published an action plan in spring 2003 to improve the corporategovernance in the European Union.

To strengthen the Austrian Capital Market, the special governmentrepresentative, Mr. Schenz, has drawn up an Action Plan by bundling variousinitiatives into a common strategy. Emphasis is being laid on creating a highervolume of securities traded on the Vienna stock exchange and on improvingthe investor�s confidence in the Austrian Markets. Some initiatives have alreadybeen realised, such as the above mentioned Corporate Governance code andthe equity-based private pension scheme (�Zukunftsvorsorge�). This productis aimed at fostering the so-called �third pillar� of pension schemes but alsoat promoting the Austrian capital market and it has been very well receivedby the public giving the capital market a new impetus.

In spring 2003 discussions on some other important topics were finalised:amongst these the agreement with the European Commission on Stateguarantees granted by regional or local authorities to certain credit institu-tions, the transposition of the second EU-anti-money laundry directive inthe field of the financial sector and the passing of the Act on real-estate invest-ment trusts are worth mentioning here.

All these developments demonstrate clearly, that the Austrian FinancialMarket is in a permanent change in order to cope with the challenges. Thevery same will apply for the future.

The Austrian Financial Markets 9�

Preface

The year 2002 was marked by global economic cooling and turmoil in inter-national stock markets. Moreover, geopolitical tension exacerbated uncer-tainty on future global economic developments.

In this difficult environment, European monetary policymakers faced newchallenges. However, pursuing a prudent monetary policy, the GoverningCouncil of the ECB continued to maintain price stability and interest ratesreached a very low level both in nominal and real terms, which — from amonetary point of view — has paved the way for a gradual recovery of theeconomy. To be able to fully utilize the potential of the stability-orientedmonetary policy, the euro area also needs an economic policy aimed atsafeguarding stability in the long run. Thus, fiscal policies must be drivenby adherence to the provisions of the Treaty establishing the EuropeanCommunity and the Stability and Growth Pact as well as the vigorouscontinuation of the structural reforms of the labor, goods and financial marketswhich have already been initiated.

The worldwide downturn has dampened economic growth also in Austria.The slowdown in growth and higher volatility in international financialmarkets are reflected, inter alia, in the performance of the Austrian financialsector. Yet the Austrian banking system proved fairly robust by internationalcomparison, which is attributable mainly to the flourishing business in Centraland Eastern Europe. Austrian banks continue to utilize their extraordinaryknow-how on these markets to step up their already very successful activitiesin Central and Eastern Europe.

After the successful implementation of monetary union, the EU is nowsetting its sights on the next milestone of integration: its enlargement byten new Member States. The acceding countries� progress in economic tran-sition and catching-up over the past ten years has been impressive.

The gradual monetary integration of the new Member States following EUaccession will further enhance the efficiency of the European financialmarkets, thus making a crucial contribution to financial stability.

The increasing integration of the European financial markets highlights theneed for an EU-wide financial stability perspective. The Eurosystem�s policy ofcentralized decision-making and decentralized implementation gives theparticipating national central banks — depending on their individual degreeof integration into financial market and banking supervision — the opportunityto provide valuable contributions to systemic financial stability.

Austria has responded to the increased international challenges in financialmarkets by establishing a new independent regulatory body, the FinancialMarket Authority (FMA). Regardless of the transfer of prudential respon-sibilities to the FMA, which now represents the statutory integrated financialsector supervisory agency, the OeNB�s previously existing tasks and rights ofparticipation as laid down in the Austrian Banking Act have not only beenpreserved; in fact, they have been augmented, which significantly enhancedcooperation between the statutory supervisory body and the OeNB. Further-more, payment systems oversight was conferred on the OeNB from April 1,2002. Thus, another crucial step towards creating supervisory structures inline with Eurosystem standards was successfully completed.

Under the guidance of the Special Government Representative for theCapital Market appointed by the federal government, experts drew up an

Klaus LiebscherGovernorOesterreichischeNationalbank

10 The Austrian Financial Markets�

Preface

action plan to strengthen the competitiveness of the Austrian capital market inthe new European environment. In addition, a Board for the Promotion of theAustrian Capital Market1) was established in cooperation with the OeNB andWiener Bo‹rse AG. The primary objective of this initiative is to sustainablystimulate the Austrian capital market and to strategically strengthen its posi-tion in Europe.

Monetary union and the euro have already considerably strengthened theeuro area�s position in the dynamic process of globalization. In the future, theywill continue to drive reform and act as a catalyst for further economic andpolitical integration in Europe. Internationally competitive and efficientfinancial markets and banking systems in the euro area play a pivotal role inthis development.

1 Kuratorium fu‹r den o‹sterreichischen Kapitalmarkt.

The Austrian Financial Markets 11�

Preface

Optimism takes hold of Austrian capital marketThe global environment for capital markets has deteriorated in the course ofthe year. Still, despite the adverse situation, Austria�s capital market achievedexcellent performance in international comparison. This remarkable perfor-mance is also the outcome of the consistent capital market policy pursuedin the past few years. Policymakers in Austria have been quick to take adequateand effective measures after having clearly recognised the need for an efficientand well-functioning national capital market to provide the domestic economywith the capital it requires, in particular, in the light of the Basle II Accord andto meet the challenges of ensuring old age provisions.

The action plan for the Austrian capital marketAs the Special Government Representative for the Capital Market, it is my jobto bundle the positive forces best suited to strengthen the Austrian capitalmarket and to coordinate the measures needed for its revival. To this end,I have drafted an action plan for the Austrian capital market jointly withrecognised capital market experts. This action plan has defined two majorareas of focus: increasing confidence and increasing volume. It definesprecisely those measures called for to eliminate the weak spots in Austria�scapital market. Considering the special situation in Austria, a completelynew approach is needed that bundles a large number of measures designedto promote the capital market. Two core elements of the action plan havealready been implemented: the Austrian Code of Corporate Governanceand the creation of a new state-subsidised retirement product.

Austrian Code of Corporate Governance to bolster confidenceThe adoption of the Austrian Code of Corporate Governance marks theachievement of a balanced, internationally acceptable and viable frameworkthat defines rules of good practice for companies. This voluntary, self-regu-latory step has met with wide acceptance and approval, and will contributeto reinforcing the confidence of investors.

State-subsidised retirement product to stimulate investment activityThe creation of a state-subsidised retirement product is a milestone achieve-ment in the promotion of retirement provisions and has been specificallydesigned to strengthen the Austrian capital market. On the one hand, it is aretirement scheme outside the mandatory system that offers attractive taxadvantages and safe investments through capital guarantees, and on the otherhand, it encourages a focus on investments in Austria that will benefit WienerBo‹rse and provide it with the crucial impulses needed for growth. At least40% of the capital must be invested in stocks listed on markets in the EEAwhose market capitalization is lower than 30% of GDP. This provision encour-ages investments in Austria�s stock market and after the enlargement of the EUalso in the stock markets of the accession countries.

The public relations and campaign work of the Committee for the AustrianCapital MarketAnother major step forward in the endeavour to revive the capital market hasbeen the establishment of a Committee for the Austrian Capital Market which

Richard SchenzSpecial GovernmentRepresentativefor the Capital Market

12 The Austrian Financial Markets�

Preface

boasts top decision-makers from Austria�s business community. This bodyplays an especially important role for the work of raising awareness andproviding information to the population and business sector on investmentsin Austrian securities.

Further activitiesIn this encouraging environment, we expect to see new listings and the home-coming of Austrian companies to Wiener Bo‹rse. Nonetheless, it remains a factthat the still low level of capitalisation of the Austrian capital market does notcorrespond to the economic performance capacity of our country. The globalcrisis of confidence in stock markets has also left its mark on Austria. For thecapital market campaign to achieve sustainable success, we need concertedaction to increase investor confidence in Austria�s capital market and to raisethe volume of trading. In my opinion, the following measures of the action planmust be implemented quickly to achieve success:� Expansion of employee participation schemes� Exploitation of the potential of securitisation� Tax incentives to reinforce the equity base of companies and encourage

public offerings� Development of Austrian investment funds� Creation of a Central European financial marketplace� Specialisation as a market for SMEs� Strengthening the pre-IPO risk capital market (venture capital and private

equity)� Dissemination of comprehensive information on the Austrian capital

market

The Austrian Financial Markets 13�

Preface

2

Focus on Special Topics

2.1 Cross Border Settlement in the EU

OeKB to ensure highly efficient clearingand settlement in the Austrian securities marketOesterreichische Kontrollbank AG (OeKB) is highly committed and invests greatefforts in further developing the Austrian financial market — among otherthings, also as a member of the Committee for the Austrian Capital Market.In its role as an established Clearing House for Wiener Bo‹rse and as theCentral Securities Depository with an excellent international network, itserves as the competence centre for the Austrian capital market and contri-butes enormously to optimising cross-border securities dealings.

The globalisation of capital markets has led to the steady rise of cross-border securities trading in Europe and between continents. Since 1999, thisdevelopment has accelerated even more with the introduction of the Euro.

The European Central Securities Depositories have responded to thechallenges arising from this development and have worked closely togetherto define standards for the interoperability of the individual clearing andsettlement organisations. To this end they founded the European CentralSecurities Depository Association (ECSDA) in 1997 with the main goal ofimplementing a secure and efficient process for the cross-border settlementof securities dealings in Europe. In its function as the Central SecuritiesDepository for Austria, Oesterreichische Kontrollbank AG is one of thefounding members of the ECSDA and contributes major and valuable inputsto the attainment of the goals of the ECSDA.

In the past two years, the European Union intensified its efforts to com-plete the internal market for financial services and has defined as a focus ofwork the creation of an integrated European securities market and theelimination of barriers to cross-border securities settlement. Already inNovember 2001, a group of experts headed by Alberto Giovannini identifiedin the �Report on Cross Border Clearing and Settlement Arrangements in theEU� fifteen barriers that are still hindering cross-border securities settlementin Europe.

On the basis of this report, the commission drafted a Communication tothe Council and to the European Parliament in May 2002 in which it formu-lated as policy goals the elimination of barriers to settlement in the form ofnational difference and the abolishment of distortions to competition due tothe unequal treatment of clearing institutions and settlement agencies. Allmajor market participants, associations and interest group representatives aswell as the European Parliament made statements on the proposals of theCommission that varied widely and some of which were highly controversial.Jointly with the other 15 Central Securities Depositories in Europe, we for-mulated a comprehensive statement within the scope of the ECSDA, whichincorporates the position of Austrian market participants, and sent it to theCommission. Furthermore, the ECSDA has addressed all elected officials ofthe European Parliament in a joint paper.

In the past few months, further proposals have been presented for theimprovement of the clearing and settlement of cross-border securities dealingswithin the scope of the diverse initiatives:

Johannes AttemsMember of the Boardof Executive Directors,OesterreichischeKontrollbank AG

Giovannini Group

EU Commission

16 The Austrian Financial Markets�

Focus on Special Topics

� The Group of Thirty (G 30), a consultative group on internationaleconomics and monetary affairs composed of senior representatives ofthe private and public sectors and academia released a report with 20 re-commendations to significantly improve the safety and efficiency ofinternational securities markets. The recommendations aim at creating astrengthened, interoperable global network, mitigating risk and improvinggovernance. Their implementation shall take place within a 5 to 7 yearperiod and will be monitored by the G30.

� In a joint project, the ECB and CESR (Committee of European SecuritiesRegulators) formulated in more detail and concretely the 19 recommen-dations drafted by the CPSS (Committee of Payment and SettlementSystems) and the IOSCO (International Organisation of Securities Com-missions) for their optimised application in the sophisticated Europeanmarkets. Apart from improved cooperation among the diverse publicauthorities, security and transparency within the European markets areto be raised and a level playing field is to be secured for the diverse serviceproviders.

� Meanwhile, the second report of the Giovannini group has been completedthat contains concrete proposals stating who is to be responsible foreliminating each of the 15 barriers to settlement and up to what time.The ECSDA (European Central Securities Depositories Association) willbe responsible for eliminating three of these barriers (operating hours &settlement deadlines, corporate actions, intraday settlement) and thecorresponding working groups have already been established in the ECSDAin which we are represented by experts.As the Austrian Central Securities Depository and Clearing House for

Wiener Bo‹rse, Oesterreichische Kontrollbank AG has been offering highquality clearing and settlement services to market participants in the Austriancapital market for many years. Our efficiently organised team of specialistswork with the most modern systems and the close collaboration with theEuropean authorities and the ECSDA ensures that business processes areconstantly and flexibly adjusted to the future challenges of an integrated Euro-pean securities market.

For more detailed information please contact:Oesterreichische Kontrollbank AGAttn.: Mr. Georg ZinnerAm Hof 4, A-1010 ViennaPhone: +43-1-531 27-2353Fax: +43-1-531 27-5826e-mail: [email protected]

G 30

ECB-CESR

15 Barriers

The Austrian Financial Markets 17�

Focus on Special Topics

2.2 The Financial Market Authority (FMA)

The FMA was established as an integrated financial supervisory authority on1 April 2002 under the Austrian Financial Market Authority Act. The super-visory tasks concerning banking, insurance and pension funds were transferredto the FMA from the Federal Ministry of Finance. In addition, also theAustrian Securities Authority became part of the FMA. The FMA is nowthe single statutory supervisory body directly responsible for banking,insurance, pension funds, securities and stock exchange supervision.

The reorganisation, which is also a reaction to the altered internationalregulatory conditions and the growing globalization of the financial markets,has led to the disappearance of the institutional segmentation of the oldsystem. One of the most important projects of the FMA for the forthcomingyears in the context of new international standards is the preparation for theimplementation of the Basel II principles with their new distinct capitalprovisions.

The FMA is an institution under public law and forms a legal entity of itsown. In performing its tasks it is not bound by any directives. The status of theFMA is secured by constitutional provision which was unanimously supportedby all parties represented in the Austrian Parliament in February 2002. Thisamendment to the Financial Market Authority Act guarantees the status ofthe FMA as an integrated and independent supervisory authority.

The FMA�s independence is a strong asset for the credibility of the plans ofthe Austrian government to provide the Austrian financial markets with atransparent, effective and efficient supervisory framework. The FMA aimsto take advantage of the synergies of being an integrated financial supervisoryauthority and to be an open, transparent and consistent supervisor. With theabolishment of the old institutional segregation there is considerable potentialfor increased cost efficiency.

The Austrian approach to financial market supervision is concentrating onthe core functions performed within the financial system rather than on insti-tutions or sectors and is thus in line with a functional approach to supervision.The new system is sector neutral and ensures a level playing field for allfinancial institutions doing business in Austria.

The main objectives of the Austrian Financial Market Authority are tostrengthen the stability and performance of the Austrian financial market,to ensure that financial legislation is observed and to guarantee fairness inthe Austrian financial market.

Besides, the FMA is concerned with the implementation of relevant EU-directives and actively participates in the elaboration of financial legislation.International co-operation and the fostering of bilateral and multilateralcontacts form another major task (Memoranda of Understanding).

The FMA supervises 906 credit institutions, 115 insurance companies,20 Pensionskassen (pension funds) and 339 investment services providers(date of survey: 31 December 2002).

On 1 January 2003 a new system for severance payments came into forcein Austria. This amendment to the legal situation required the establishment ofthe �Mitarbeitervorsorgekassen� (institutions authorised to conduct the business of

Andreas Gru‹nbichlerExecutive Directorof the FinancialMarket Authority

18 The Austrian Financial Markets�

Focus on Special Topics

investment-based statutory severance payments). The FMA is responsible forthe licensing and the supervision of these institutions.

The costs for banking, insurance, pension funds and securities supervisionare primarily borne by the supervised institutions themselves. In addition, thefederal government contributes a flat amount of EUR 3.5 million per fiscalyear. The total budget of the FMA for the year 2003 amounts to aboutEUR 21.8 million.

The �Directive on Insider Dealing and Market Manipulation� (MarketAbuse Directive) of the European Parliament and of the Council was publishedin the Official Journal of the European Union on 12 April 2003. Austria like allother member states shall bring into force the laws, regulations and adminis-trative provisions necessary to comply with this Directive until 12 October2004. This new directive strengthens the position of the FMA as supervisoryauthority, e.g. it enables the FMA to carry out on-site inspections at issuers ofsecurities. Furthermore, it harmonizes the definitions of �inside information�,�market manipulation� and the different �financial instruments� for allEuropean financial markets. After the implementation of the directive intonational law, the senior management of companies issuing securities will berequired to disclose their own trading in securities. According to the AustrianCode of Corporate Governance there has not been a disclosure obligation sofar. On the whole, the Market Abuse Directive is an important step forwardsfor the combat against insider trading and market manipulation of securitieslisted on the stock exchange. In the future the FMA aims to be vested withthe legal power to pursue insider trading in administrative penalty proceed-ings.

To enhance the enforceability of supervisory measures, the FMA is vestedwith administrative penal power and the power to enforce its supervisoryadministrative decisions. No appeal of any kind is possible against rulingsissued by the FMA except in administrative penalty proceedings.

Furthermore, the FMA has the power to issue ordinances in order tospecify the general obligations stated by law. Regulations of the FMA arepublished in the Federal Law Gazette.

The FMA�s accountability is clearly defined. The FMA is accountable to theFinancial Committee of the National Assembly and the Federal Minister ofFinance. According to the Austrian Financial Market Authority Act, theFederal Minister of Finance supervises the FMA in order to ensure that itfulfils its statutory duties, does not breach the laws and regulations whenperforming its functions and does not exceed its scope of authority. For thispurpose, the Federal Minister of Finance is authorized to seek informationfrom the FMA on all matters relating to the supervision of the financialmarket.

The FMA has two executive directors, Andreas Gruenbichler, who isProfessor for Finance at the University of St. Gallen and Kurt Pribil, formerHead of the Foreign Research Division of the Oesterreichische Nationalbank(Austrian Central Bank). The Executive Board is appointed by and reporting toa Supervisory Board.

The Supervisory Board of the FMA consists of a Chairman, a Vice-Chair-man, four additional members and two co-opted members. The Chairman,the Vice-Chairman and the other members of the Supervisory Board with

The Austrian Financial Markets 19�

Focus on Special Topics

the exception of the two co-opted members are appointed by the FederalMinister of Finance. The Oesterreichische Nationalbank submits nominationsfor the functions of the Vice-Chairman and two additional members of theSupervisory Board. In addition, the Supervisory Board co-opts two membersnominated by the Austrian Federal Economic Chamber. However, they have novoting rights.

To promote co-operation, the exchange of ideas and to provide advice onissues of the financial markets, the financial market stability and supervisorymatters the Financial Market Committee has been set up at the FederalMinister of Finance. It consists of one representative of the FMA, the Oester-reichische Nationalbank as well as of one representative of the Federal Ministryof Finance. This committee is meant to serve as a platform for the institutionsjointly responsible for financial stability, i.e. Oesterreichische Nationalbank, FMAand the Federal Ministry of Finance. It is convened at least four times a year.External experts may be called in as consultants. However, the FinancialMarket Committee is no decision making body of the FMA.

Complementing the establishment of the FMA as the single, statutorysupervisory body, there is a close co-operation between the FMA and theOesterreichische Nationalbank and also the Federal Ministry of Finance.

There is a close involvement of the Oesterreichische Nationalbank in thesupervision of the banking system. The Oesterreichische Nationalbank has tobe entrusted with on-site inspections regarding the examination of creditand market risk of banks and is to be consulted in certain matters. Inparticular, the FMA continuously entrusts the Oesterreichische Nationalbankwith the collection and processing of money and banking statistics (e.g.monthly returns, quarterly reports, major loans register).

The Federal Ministry of Finance, on the other hand, safeguards thecorrectness of the FMA�s conduct of business and remains the major authorityfor drafting legislation in this field.

With the establishment of the FMA, there is an independent and efficientAustrian supervisory regime in line with recent international developments.The FMA will continue striving to obtain material improvements in super-visory instruments and to further benefit the stability of the Austrian financialmarket. The FMA has budgetary independence, autonomy in employment andthe resources to recruit highly qualified staff. The number of employees rosesignificantly throughout the last year and currently amounts to 155 (April2003).

Keep yourself informed about the developments of financial supervisionpolicies on our website www.fma.gv.at. The FMA plans to restructure andextend its existing website and to implement an English version in summer2003.

FMA — Finanzmarktaufsicht(The Austrian Financial Market Authority)Praterstrasse 23A-1020 Vienna, AustriaPhone: +43-1-249 59-0Fax: +43-1-249 59-4499e-mail: [email protected]://www.fma.gv.at

20 The Austrian Financial Markets�

Focus on Special Topics

2.3 Wiener Bo‹ rse AG

Wiener Bo‹rse is a modern, customer- and market-oriented financial servicescompany, which plays a central role in the Austrian capital market. However,the sustained support of the latter and the retention of its competitiveness in aEuropean context can only be achieved in teamwork with all market players.With this objective in view, during 2002 Wiener Bo‹rse began to set up theCommittee for the Austrian Capital Market. In view of the internationalmarket situation, which is characterised by a general lack of optimism, it isextremely pleasing that important protagonists from Austrian industryspontaneously declared their readiness to assist in shaping this project.

The most significant aspect of the Committee�s activities is the creation of anetwork at management and expert level, which above and beyond theexchange of ideas, initiates numerous individual measures and is of major im-portance to the Austrian economy. The first result of this co-operation withthe Government Representative for the Capital Market, Richard Schenz, isan innovation for Austria in the form of a pensions product containing a highlevel of Austrian stock and offering an advantageous premium.

In the meantime, numerous national companies have recognised thebenefits of the domestic stock exchange, not least due to the stable pricedevelopment of the ATX and the ATX prime indices. Several companies,which up to now were listed on other exchanges, are already quoted inVienna, or are in the process of preparing such a listing.

The future strategy of Wiener Bo‹rse has two focal points:— On the one hand, the creation of all the technical and organisational

prerequisites required for smooth trading and the positioning of WienerBo‹rse AG as a modern services company.

— On the other hand, the motivation of all market players to make activecontributions to the development of the Austrian financial market.As an intermediary between all the market participants, Wiener Bo‹rse AG has

been actively involved in the development and support of the Austrian capitalmarket for many years. Even in an increasingly integrated European economiczone, regional institutions retain their importance and are indispensable forthe upholding of certain quality standards. In the medium-term, Wiener Bo‹rseAG intends to fully exploit the potential for small and mid-cap issues and,above all, to interest retail investors in the purchase of domestic stocks.

Furthermore, Wiener Bo‹rse has steadily expanded its range of services andmodified them to match the needs of the modern market. Among other items,via data vendors, Wiener Bo‹rse Information Products supplies real time priceinformation to professional market players and retail investors. As a specialinformation service, Wiener Bo‹rse AG issues and calculates 19 real time shareindexes, which have established themselves as benchmarks for the Austrianand the CEE markets.

In terms of an international comparison, despite the negative, generalsituation, the ATX, the leading index of Wiener Bo‹rse, was able to performwell. At the year-end 2002, the ATX closed at 1,150.05 points, which repre-sented a slight 0.85% improvement in performance over the year-end 2001(1,140.36 points).

Stefan ZapotockyMember of theManagement BoardWiener Bo‹rse AG

Erich ObersteinerMember of theManagement BoardWiener Bo‹rse AG

The Austrian Financial Markets 21�

Focus on Special Topics

2.4 Austria in Central Europe

At the European Council meeting held in Copenhagen in December 2002, aresolution was passed to admit eight Central and East European countries aswell as Cyprus and Malta to the EU.

The EU accession treaty was signed at the Acropolis on 16 April 2003, andaccession is scheduled for May 2004. The EU enlargement will provide amajor impetus to growth in the new and old member countries and willincrease Austria�s appeal as a business location. The enlargement is fullysupportive of Austria�s economic and political interests. Due to its geograph-ical location and historical relations, Austria has always had close economic tiesto Eastern Europe, but at the same time it has also been firmly integrated inthe West European economy. In 2002, 60.2% of Austria�s exports went to theEU (euro area countries accounted for 53.7%), and 17.7% went to East Euro-pean countries (8 EU accession countries accounted for 12.4%). The EUaccounted for a 35.0% share of Austria�s direct investments abroad in mid-2002, while East European countries accounted for a 36.7% share.

Economic relations boostedsince the transformation of 1989The political transformation in the Eastern European countries in the autumnof 1989 radically changed the political and economic relations between Austriaand Eastern Europe. Eastern Europe�s transition to democracy and free marketeconomy has not only eliminated the latent threat along the long easternborder (1,300 km), it has also resulted in considerable economic advantages.Austria shifted from a peripheral location at the border between the West andthe East to the heart of a converging continent. Real economic growth hasincreased considerably since 1989 as a result of the opening up of EasternEurope (liberalisation) and an estimated number of 60,000 new jobs have beencreated. Austria took advantage of the opportunities in Eastern Europe earlierthan its competition.

The growing economic relations with Eastern Europe were based on thegradual integration of the region under the Europe Agreements and on signi-ficant economic aid. Austrian exports to the East European countries soared to4.4 times the 1989 figure by 2002 and even by as much as 5.8 times in thesuccessful transition countries of Eastern Central Europe (Hungary, CzechRepublic, Slovakia, Poland). Exports to South-eastern Europe also developedvery well after the end of the Balkan crisis. Although exports to Russia and theother states that emerged from the former USSR lost significance during thenineties, they recovered perceptibly in 2000 and 2001. As a result of thisdynamic development, the amount of exports to the East increased from lessthan 10% in 1989 to almost 18% of total exports in 2002, while those to East-ern Central Europe rose from 4.5% to over 10%. Austria�s most importanttrade partners in the East in 2002 were Hungary, which was 4.3% ahead ofthe Czech Republic and Slovenia. Eight of Austria�s 20 most important tradepartners were located in Eastern Europe.

In 2002, the volume of Austrian exports to Eastern Europe rose +6.8%,which was less than the years before, but still far above that of the EU (+3.1%)and most other regions. Exports to the economically more advanced countries

Jan StankovskyAustrian Instituteof Economic Research(WIFO)

22 The Austrian Financial Markets�

Focus on Special Topics

in Eastern Central Europe have only shown moderate growth (+4.0%, ofwhich Hungary is responsible for +0.9%), since these countries are feelingthe effects of the continuing economic stagnation within the EU (particularlyin Germany) due to their high degree of integration in the West. Exports toRussia and the Ukraine have also stagnated. Remarkable results were achievedin South-eastern Europe (+14.3%) — a region that has recovered from thedestruction of the last years and has also made progress in the transformationprocess.

Overall Austrian imports may have dropped by 2.2% in 2002 due tocyclical factors, but exports to Eastern Europe rose by 2.1%. Thanks to lowerprices and improved quality, East European suppliers have been able to steadilyenlarge their market share in Austria and the percentage that East Europeancountries account for in total imports (13.8%) today is over twice as highas in 1989. A significant share of the imports from Eastern Europe comes fromthe subsidiaries of Austrian and international corporations. Austria�s balance oftrade for 2002 with the East European countries reported a surplus ofEUR 3 billion.

The significance of foreign trade with Eastern Europe for Austria is two tothree times greater than for the other Western countries. Austria accountedfor 6.6% of the exports from industrialized countries (OECD) to EasternEurope and for 7.5% of the exports to Eastern Central Europe as well asfor 10.2% of exports to South-eastern Europe. Austria is one of the mostimportant trade partners for its neighbouring countries to the East. AlthoughAustria lost some market shares in Eastern Europe in 2001, it maintained itsposition and even achieved slight gains in 2002 according to the resultscurrently available. Austria�s strong position in Eastern Europe is remarkable,since it is a relatively small country with a population of 8 million and accountsfor only 1.7% of the OECD�s exports worldwide.

Austria�s ties to Eastern Europe are also based on the intensive cooperationamong businesses relating to direct investments. Takeovers and acquisitions ofstakes in companies in Eastern Europe have helped Austrian companies tosecure market shares in the region. The outsourcing of wage-intensive produc-tion has helped to improve the Austrian economy�s competitive position at theinternational level. The subsidiaries in Eastern Europe are generally highlyprofitable and make significant contributions to the good results of the parentcompanies in some sectors (e.g. banks). The excellent position of Austriancompanies in Eastern Europe has enhanced their appeal for international jointventures. Vienna has become one of the preferred sites for the Eastern Euro-pean headquarters of multinational companies.

Austrian companies have expanded their position as investors in EasternEurope over the last years. New investments doubled from EUR 1 billionin 1999 to EUR 2.1 billion by 2000 and rose further to EUR 2.6 billion by2001, reaching a new high of EUR 1.6 billion by mid-year 2002. The invest-ment boom also continued during the second half of 2002. The Austrianmarket share in terms of new investments in Eastern Europe rose from8.3% in 2001 to over 10% in the first half of 2002. Austria accounted for over12% of new investments in Central Europe1). The share of direct investments1 Cf. Hunya, G., Stankovsky, J., WIIW-WIFO Database, Foreign direct investment in CEECS and the former Soviet Union,

WIIW-WIFO, February 2003.

The Austrian Financial Markets 23�

Focus on Special Topics

by Austrian investors in Eastern Europe was EUR 10.6 billion at the end of2001, and had risen to EUR 12.2 billion by mid-2002. Austria accountedfor 6.0% of the existing foreign investments in Eastern Europe by mid-2002. Around 30% of the total foreign investment capital in Slovakia andthe Slovenia, and 10% in the Czech Republic, Hungary and Croatia come fromAustria.

The Czech Republic is currently of the focus of interest of Austrian invest-ors. The geographical proximity, the population�s relatively high purchasingpower and the country�s industrial tradition as well as the companiesscheduled for privatisation are behind this trend. Croatia came in second placerecently, which is somewhat surprising since it is not a candidate for EUmembership. The political and economical consolidation of Croatia hasobviously convinced Austrian investors of its attractiveness.

The total number of Austrian �East European companies� was estimated tobe somewhere between 11,000 and 12,000 by the Austrian Federal EconomicChamber in 2000. A number of 162,000 persons were employed in the sub-sidiaries of Austrian companies in Eastern Europe in the year 2000, 50,000each in the Czech Republic and Hungary and 21,000 in Poland. Austria wasalso a major employer in Slovakia.

Austrian direct investments in Eastern Europe are for the most part profit-able. After a difficult transition phase in the mid-1990s, the majority of theAustrian subsidiary companies in East Europe have started generating highreturns. In 2000, Austrian subsidiaries in East European countries achieveda net income of EUR 654 million. The restructured companies posted a profitof EUR 878 million, but the figure contrasts with losses of EUR 224 millionreported by local branches. The improved earnings situation becomes parti-cularly clear when we look at the profitability (net income as a percentageof equity). The profitability of Austrian companies was extremely low andeven negative during the restructuring phase between 1992 and 1995. Earningpower has increased significantly since 1996 and recently it surpassed the 10%level. Since a relatively large number of East European companies — mostlyacquisitions or newly founded enterprises — are posting losses, the profitabilityof the restructured companies is high and is probably quite frequently around20% of the invested capital. The earning power of the East European sub-sidiaries was roughly twice as high as those in other countries in the pastfew years.

The increasingly closer economic ties with Eastern Europe ahead of theaccession to the EU were to be expected and the experience is similar tothe one made during the southern EU enlargement. The successful conclusionof the EU enlargement negotiations will give foreign direct investment in East-ern Europe a major boost.

Economic cooperation with Eastern Europein the enlarged EUAustria became a member of the European Union in 1995, a move whichenabled it to secure its economic interests in this important market. EUmembership did not have a negative effect on Austria�s trade relations withEastern Europe; on the contrary, Austrian exports have shown above averagegrowth ever since.

24 The Austrian Financial Markets�

Focus on Special Topics

East European countries have close economic ties with the EU. In Decem-ber 2002, the European Council in Copenhagen passed a resolution to admiteight European countries (Poland, Czech Republic, Slovakia, Slovenia,Hungary and three Baltic countries) as well as Cyprus and Malta to the EU.The EU membership of these countries will add further depth to the economiccooperation and will widen the flow of foreign capital from West to East. EUmembership will accelerate growth in the new EU states. These states havecommitted themselves to adopt the aquis communautaire of the EuropeanUnion, a move which will substantially lower the export and investment risk.At the same time, existing trade barriers (e. g. border checks) between the oldand the new EU members are being eliminated, which will reduce trade costsand facilitate foreign trade as well as cross-border cooperation among busi-nesses. The new members will receive considerable financial support fromthe EU. According to a recent EU study (�Kok Report�), the advantages ofthe EU enlargement and the resulting opportunities outweigh the possiblecosts and risks by far1). EU membership will heighten Eastern Europe�s appealas an export market and investment location. Austria has good chances ofstaking its claim among competitors in Eastern Europe. Austrian exports toEastern Europe will grow at above average rates and Austria�s share in the totalexports could rise to almost 20% by 20102). The flow of foreign capital intoEastern Europe will increase. The capital invested in Eastern Europe hasresulted mainly in advantages for Austria and will also have a positive effectin the future. The upcoming enlargement of the Union will create majoropportunities for Austria. The economic advantages resulting from theenlargement will probably not be as great as those related to the openingup of Eastern Europe, but they will be positive in any case. Economic growthwill increase almost one percentage point by 2010, inflation will be curbed,the unemployment rate will drop slightly and the burden on the governmentbudget will drop. Austria stands to gain more from the EU�s enlargement toEastern Europe than other EU countries3). In Austria, the closer economicrelations with Eastern Europe have already started to exert — often painful —pressure to adjust existing structures, and it will still increase in some sectors.The pressure is unevenly distributed across regions, sectors and social groups.The liberalisation of current restrictions relating to the job market and transittraffic could (temporarily) lead to problems, but Austria has been concededtransitional measures in these areas (temporary job market protection, amongothers). The border regions will receive substantial help under the EUassistance programmes.

1 �Die Erweiterung der Europa‹ischen Union: Errungenschaften und Herausforderungen�, EU March 2003,http://europa.eu.int/comm/enlargement/communication/index.htm/kok_report.

2 Cf., Stankovsky, J., EU-Erweiterung: Chancen und Herausforderungen fu‹r die o‹sterreichische Wirtschaft, in: Neisser, H. undPuntscher Riekmann S. (Hg.), Europa‹isierung der o‹sterreichischen Politik, Universita‹tsverlag, Vienna, 2002.

3 Cf. Breuss, F. , �Teilprojekt 12: Makroo‹konomische Auswirkungen der EU-Erweiterung auf alte und neue Mitglieder�, in:Mayerhofer, P. und Palme, G. (Koordination) (2000/01), Strukturpolitik und Raumplanung in den Regionen an dermitteleuropa‹ischen EU-Au§engrenze zur Vorbereitung auf die EU-Osterweiterung (Preparity); Breuss, F. und Lehner, G.�Teilprojekt 12/2: Die Auswirkungen der EU-Erweiterung auf den o‹sterreichischen Staatshaushalt�, in: Mayerhofer, P.,Palme, G. (Coordination).

The Austrian Financial Markets 25�

Focus on Special Topics

For more detailed information please contact:Austrian Institute of Economic ResearchAttn.: Mr. Jan StankovskyP. O. Box 91, A-1103 ViennaPhone: +43-1-798 26 01Fax: +43-1-798 93 86e-mail: [email protected]://www.wifo.ac.at

Austria�s economic relations with East European countries

2001 20021)

Value Dynamic Significance2) Value Dynamic Significance2)

in EUR million Change in % Share in % in EUR million Change in % Share in %

Foreign tradeExports 12.8 10.9 17.2 13.6 6.8 17.7Imports 10.4 5.7 13.2 10.6 2.1 13.8Balance of trade 2.4 . . . . 3.0 . . . .

Direct investmentExisting investments 10.6 31.9 35.2 12.2 . . 36.7New investments 2.6 22.7 75.1 1.6 . . 50.71) Direct investment in first half-year.2) Share accounted for by Eastern European countries in total foreign trade.

26 The Austrian Financial Markets�

Focus on Special Topics

3

The Economy

3.1 Economic Structure and Selected Indicators

Robust economic growth and a strengthening labor market, stable prices,moderate unit labor costs and high price competitiveness, heightened attrac-tiveness for foreign investment, a firm commitment to sound public finances,a track record of monetary stability, and social partners� responsible policy-making have proved big assets for Austria and have clearly reinforced itsinternational competitiveness since its entry into the European Union (EU)in 1995 and by its participation in the first wave of EMU in 1999, as reflectedby highly favorable economic conditions that prevail in Austria.

In an international comparison of business locations, Austria claims aremarkably strong position. For one thing, Austria provides a sound businessclimate for industrial enterprises, which is underscored by the substantialamount of direct investment the country has attracted and by the better exportperformance it has achieved in recent years. The economic integration withinthe EU as well as the progressive integration of southeastern and eastern Euro-pean countries — both of which guarantee access to large, more highly inter-linked markets — are also seen as important competitive advantages. Moreover,a high standard of living and stable macroeconomic and legal frameworkconditions contribute to the favorable assessment of Austria as a businesslocation. Last but not least, Austria boasts a workforce whose qualificationsand motivation are well above the European average. Austria will maintainits appeal as a business location against international competition also in thelong term. To this effect, the reforms that have been started to eliminateexisting structural weaknesses will have to be advanced energetically. Enlarge-ment opens up new chances and challenges for Austria as a business location.According to the most recent �World Competitiveness Yearbook 2003� andespecially to the World Competitiveness Scoreboard (which presents theoverall ranking for 49 countries) Austria moved to rank 10 (2002: 8). Eco-nomic giants like Germany, France and Japan lie either just ahead of orbehind Austria. The following review of Austria�s performance highlightsthe headway Austria has made in terms of economic growth, budget consol-idation and competitiveness.

Almost half of Austria�s land area is used for agriculture and animalfarming. Domestic agricultural production satisfies about 80% of the country�sfood needs. In 2002, almost 25,800 people were employed in agriculture andforestry, or 0.8% of Austria�s jobholders. This sector accounted for 2.0% ofAustria�s GDP.

Austria is a highly industrialized country with efficient and diversifiedindustrial and services sectors. Austria�s industries — which include manu-facturing and mining, power generation and water supply — accounted forabout 21.9% of GDP in 2002. In terms of output, the country�s most impor-tant industrial sectors are metals (machinery and tools, iron and steel, motorvehicles, nonferrous metals), chemicals, electrical equipment and electronics,food and beverages, forestry products (production and processing of paper andwood), oil, textiles and clothing.

In 2002, the construction industry employed about 240,000 persons, or7.6% of Austria�s jobholders, and accounted for 6.9% of Austria�s GDP.

Introduction

Austria attractive Business Location

Agriculture and forestry

Industry

Construction sector

28 The Austrian Financial Markets�

The Capital Market

The sector trade and services as a whole accounted for about 63.4% ofGDP in 2002. Services have become the biggest single contributor to theAustrian economy. The country�s services sector comprises high-performancetransport and telecommunication industries, banking and insurance, com-merce and a wide variety of production-related services. Tourism is an impor-tant service industry, making a major contribution to Austria�s currentaccount.

The GDP generated by all these sectors in 2002 totalled EUR 216.6 billionat current prices. This represents a nominal 2.2% increase on 2001. Allowingfor inflation, Austria�s GDP increased by 1.0%. Real GDP is expected to growby 0.7% in 2003 and by 1.2% in 2004 (most recent WIFO-forecast of June2003).

An international comparison of key economic indicators shows that Austriaperforms very well across the board. Over the long term, the country�seconomy has grown in line with that of most European countries. Moreover,Austria has an extremely good employment and inflation record.

Average gross unadjusted per-capita income equaled EUR 2,400 a monthin 2001 (there are no data available for 2002 yet). After deducting payroll tax,social insurance contributions, etc., jobholders had average monthly take-home pay of EUR 1,620, which represents a 1.25% increase on 2001.

The productivity of Austrian employees has grown steadily during the pastfew years but weakening in 2001 (it remained unchanged year on year). In2002, productivity (measured as real GDP per employee) climbed by 1.5%.

Table 1

Gross Domestic Product

Sector 1996 1997 1998 1999 2000 2001 2002 2002

EUR billion % of GDP

Agriculture, hunting and forestry 4.2 4.2 4.3 4.3 4.3 4.5 4.3 2.0

ManufacturingMining and quarrying 0.6 0.6 0.6 0.6 0.7 0.8 0.8 0.4Manufacturing 32.8 34.3 36.2 37.5 40.4 41.3 41.9 19.3Electricity, gas and water supply 4.8 4.5 4.7 4.8 4.4 4.2 4.7 2.2Construction 13.5 13.8 14.5 14.9 15.1 14.7 14.9 6.9Total manufacturing 51.7 53.2 56.0 57.8 60.6 61.0 62.3 28.8

Trade and servicesWholesale and retail trade1) 21.4 22.0 22.8 23.3 24.9 25.1 25.5 11.8Hotels and restaurants 6.5 6.6 7.0 7.3 7.9 8.6 9.0 4.2Transport, storage and communication 12.2 12.5 12.8 12.9 13.4 13.9 13.9 6.4Financial intermediation 11.4 12.2 12.2 11.7 13.2 13.1 12.7 5.9Real estate, renting and business activities 24.3 25.7 27.6 29.1 31.4 33.8 34.9 16.1Public administration and defence; compulsory social security 11.2 11.4 11.7 12.2 12.5 12.8 12.9 6.0Other services 25.6 24.3 25.2 25.3 26.5 27.4 28.4 13.1Total trade and services 112.6 114.7 119.3 121.8 129.8 134.7 137.3 63.4

Less financial intermediation services indirectly measured 8.5 9.1 9.1 8.4 9.6 10.3 9.9 4.6Taxes less subsidies on products 17.9 19.5 20.0 21.5 21.8 21.8 22.7 10.5GDP at current prices 178.0 182.5 190.6 197.2 207.0 211.9 216.6 100.0GDP at 1995 prices 175.7 178.5 185.5 190.6 197.4 198.7 200.8 x

%-change in GDP vs. previous yearat current prices 3.3 2.5 4.5 3.4 5.0 2.3 2.2 xat 1995 prices 2.0 1.6 3.9 2.7 3.5 0.7 1.0 x

Source: Statistics Austria, OeNB.1) Inclusive repair of motor vehicles, motorcycles and personal and household goods.

Services, Tourism

GDP

International comparison

Per-Capita income

Productivity

The Austrian Financial Markets 29�

The Capital Market

Over the longer term, Austria has a good inflation record. Stability-oriented and competitiveness-oriented wage moderation has contributedsignificantly to the favorable price environment. Due to stagnant unit laborconstant increasing competition especially in the service sector (deregulation,liberalization), the HICP-inflation dropped to a low of 0.5% in 1999. In 2002,inflation came to 1.7% (and therefore clearly fell behind the 2001 figure of2.3%). Inflation was largely carried by services and food including alcoholicbeverages and tobacco. Prices of unprocessed food, by contrast, decelerated.In 2002, the Austrian price increase was below the average in the Euro area(2.2%) and in the European Union (2.1%).

Table 2

The Austrian Economy in an International Context

Austria Euro Area European Union

1999 2000 2001 2002 1999 2000 2001 2002 1999 2000 2001 2002absolute or % vs. previous year

GDP at constant prices 2.7 3.5 0.7 1.1 2.8 3.5 1.5 0.8 2.8 3.5 1.6 1.0Consumer prices 0.6 2.3 2.7 1.8 x x x x x x x xHarmonized consumer prices 0.5 2.0 2.3 1.7 1.1 2.3 2.3 2.2 1.2 1.9 2.2 2.1Unemployment rate(EUROSTAT-Definition) 3.9 3.7 3.6 4.3 9.4 8.5 8.0 8.3 8.7 7.8 7.3 7.6Budget deficit(general government) as % of GDP —2.3 —1.5 0.3 —0.6 —1.3 0.1 —1.6 —2.3 —0.7 0.9 —0.9 —1.9Gross fixed capital formationat constant prices 2.1 5.9 —2.2 —4.6 5.9 4.9 —0.6 —2.6 5.2 4.7 —0.3 —2.4Exports at constant prices 8.5 13.4 7.4 2.7 5.3 12.6 3.0 1.3 5.5 12.2 2.6 1.0Imports at constant prices 9.0 11.6 5.9 —1.3 7.4 11.3 1.7 —0.4 7.4 11.4 1.6 —0.1Current account deficit/surplus as % of GDP —3.2 —2.6 —1.9 0.4 0.6 0.0 0.3 0.9 0.2 —0.3 0.2 0.7

Sources: Statistics Austria, EUROSTAT, EU-Commission.

Table 3

The Austrian Productivity, Wage and Price Indices

Year GDP per employee Negotiated minimum wage rate Wholesale prices Harmonized consumer price index

Index(1995=100)

–% vs.previous year

Index(1986=100)

–% vs.previous year

Index(1996=100)

–% vs.previous year

Index(1996=100)

–% vs.previous year

1997 103.7 1.1 153.3 1.8 100.4 0.4 101.2 1.21998 106.7 2.9 156.7 2.2 99.9 —0.5 102.0 0.81999 108.1 1.3 160.6 2.5 99.0 —0.8 102.5 0.52000 111.1 2.8 163.9 2.1 103.0 4.0 104.5 2.02001 111.1 0.0 168.3 2.7 104.5 1.5 106.9 2.32002 112.7 1.5 172.3 2.4 104.2 —0.4 108.8 1.7

Source: Statistics Austria.

Prices

30 The Austrian Financial Markets�

The Capital Market

Unit labor costs are an important criterion of international competitive-ness. Austria has been performing well in this respect for many years. Austria�srelative industrial labor costs have been improved Austria�s competitivenessvis-a‘-vis both Germany and (on average) its trading partners (weighted onthe basis of their share in foreign trade).

Table 4

Harmonized Index of Consumer Prices — International Comparison

Selected Countries 1998 1999 2000 2001 2002

Change in % vs. previous year

Belgium 0.9 1.1 2.7 2.4 1.6Germany 0.6 0.6 1.4 1.9 1.3Greece 4.5 2.1 2.9 3.7 3.9Spain 1.8 2.2 3.5 2.8 3.6France 0.7 0.6 1.8 1.8 1.9Ireland 2.1 2.5 5.3 4.0 4.7Italy 2.0 1.7 2.6 2.3 2.6Luxembourg 1.0 1.0 3.8 2.4 2.1Netherlands 1.8 2.0 2.3 5.1 3.9Austria 0.8 0.5 2.0 2.3 1.7Portugal 2.2 2.2 2.8 4.4 3.7Finland 1.4 1.3 3.0 2.7 2.0

Euro Area 1.2 1.1 2.3 2.3 2.2

Denmark 1.3 2.1 2.7 2.3 2.4Sweden 1.0 0.6 1.3 2.7 2.0United Kingdom 1.6 1.3 0.8 1.2 1.3

EU-15 1.3 1.2 1.9 2.2 2.1

Switzerland1) 0.0 0.8 1.6 1.0 0.6Norway1) 2.3 2.3 3.1 3.0 1.3

USA1) 1.5 2.2 3.4 2.8 1.6Japan1) 0.7 —0.3 —0.7 —0.6 —0.9Canada1) 1.0 1.7 2.7 2.5 2.3

Total OECD1) 4.0 3.4 4.0 3.4 2.5

Sources: EUROSTAT, OECD.1) National CPI.

��������������� ����������� ��� ������ �

���

���

���

����

����

����

���� ������������������������������� ����������������� ��������������������������������������������������������� ��������������� ��!��"��

�##�

����������������

��������������������������������������������

�##� �##$ �##� �##% �##� �##& �##' �### ���� ����

���������������������������������������������������� �������!"� #�$�%����&&'��

�##� ���� ���$�� ������

()�����

Unit labor costs

The Austrian Financial Markets 31�

The Capital Market

During 2002 Austrians spent 57.6% of income earned within Austria onprivate consumption and 18.7% on public consumption. However, the levelof investment expenditure on industrial modernization and the infrastructurewas also high. Austria�s gross fixed capital formation reached 21.8%, whichwas ahead of the OECD average.

Table 5

Relative Labor Costs in Manufacturing in Austria

Labor costsper unitof output

Relative labor costs1)

Austria versustradingpartners

Austria versusGermany

Annual change in %

1990 �0.9 �2.2 �3.41991 þ2.2 �2.7 �1.81992 þ3.8 þ2.3 �0.91993 þ0.9 þ1.1 �2.71994 �3.6 þ0.8 þ2.91995 �0.6 þ3.0 �0.21996 �0.8 �1.6 þ1.21997 �4.4 �4.8 þ0.81998 �2.0 �1.2 þ0.11999 �1.2 �2.1 �0.82000 �4.5 �5.4 �1.82001 þ1.8 �0.3 þ0.12002 �0.2 �0.2 þ0.020032) �0.5 þ1.4 �1.420042) �0.6 �0.7 �1.2

Sources: Statistics Austria, WIFO (Austrian Institute of Economic Research).1) Negative values indicate an increase in competitiveness.2) Forecast (WIFO — June 2003).

Table 6

Domestic Expenditure in Austria

1996 1997 1998 1999 2000 2001 2002 2002

EUR billion % of GDP

Private consumption 101.8 105.0 108.5 112.0 117.4 121.6 124.9 57.6Public consumption 36.1 35.9 37.3 39.0 39.8 40.5 40.6 18.7Total consumption 137.9 141.0 145.7 151.0 157.2 162.1 165.4 76.4Gross fixed capital formation 41.5 43.0 45.0 46.2 49.4 49.1 47.2 21.8Changes in inventories andacquisitions less disposals of valuables 0.7 1.2 1.2 2.1 0.9 0.0 — 0.5 — 0.2Gross capital formation 42.2 44.1 46.2 48.4 50.3 49.1 46.7 21.6Errors and omissions — 0.1 0.2 — 0.2 — 0.5 0.8 0.7 — 0.5 — 0.2Total domestic expenditure 180.0 185.3 191.8 198.9 208.3 211.9 211.7 97.7

Source: Statistics Austria.

Domestic expenditure

32 The Austrian Financial Markets�

The Capital Market

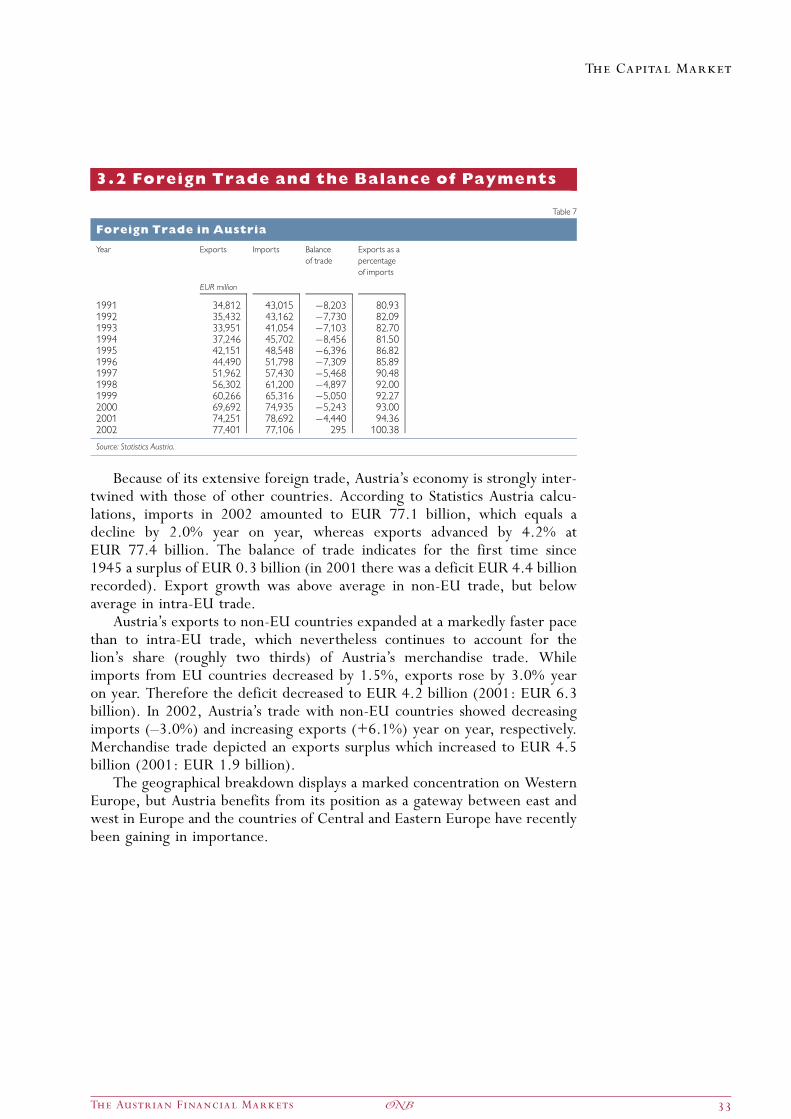

3.2 Foreign Trade and the Balance of Payments

Because of its extensive foreign trade, Austria�s economy is strongly inter-twined with those of other countries. According to Statistics Austria calcu-lations, imports in 2002 amounted to EUR 77.1 billion, which equals adecline by 2.0% year on year, whereas exports advanced by 4.2% atEUR 77.4 billion. The balance of trade indicates for the first time since1945 a surplus of EUR 0.3 billion (in 2001 there was a deficit EUR 4.4 billionrecorded). Export growth was above average in non-EU trade, but belowaverage in intra-EU trade.

Austria�s exports to non-EU countries expanded at a markedly faster pacethan to intra-EU trade, which nevertheless continues to account for thelion�s share (roughly two thirds) of Austria�s merchandise trade. Whileimports from EU countries decreased by 1.5%, exports rose by 3.0% yearon year. Therefore the deficit decreased to EUR 4.2 billion (2001: EUR 6.3billion). In 2002, Austria�s trade with non-EU countries showed decreasingimports (—3.0%) and increasing exports (+6.1%) year on year, respectively.Merchandise trade depicted an exports surplus which increased to EUR 4.5billion (2001: EUR 1.9 billion).

The geographical breakdown displays a marked concentration on WesternEurope, but Austria benefits from its position as a gateway between east andwest in Europe and the countries of Central and Eastern Europe have recentlybeen gaining in importance.

Table 7

Foreign Trade in Austria

Year Exports Imports Balanceof trade

Exports as apercentageof imports

EUR million

1991 34,812 43,015 �8,203 80.931992 35,432 43,162 �7,730 82.091993 33,951 41,054 �7,103 82.701994 37,246 45,702 �8,456 81.501995 42,151 48,548 �6,396 86.821996 44,490 51,798 �7,309 85.891997 51,962 57,430 �5,468 90.481998 56,302 61,200 �4,897 92.001999 60,266 65,316 �5,050 92.272000 69,692 74,935 �5,243 93.002001 74,251 78,692 �4,440 94.362002 77,401 77,106 295 100.38

Source: Statistics Austria.

The Austrian Financial Markets 33�

The Capital Market

The commodity breakdown of Austria�s foreign trade has becomeconsiderably more balanced over the past few years. There is a clear trendtowards manufactured products and capital goods on both the export andimport sides.

An evaluation of the Austrian current account for 2002 shows a balancedresult — a noticeable improvement that is ascribable to a rise in Austrianexports and to lower income outflows. For the first time in ten years, theAustrian current account recorded a surplus of EUR 0,949 million or 0.4%of GDP in 2002 — a substantial improvement by EUR 5,063 million against2001.

According to the transaction principle the current account recorded forthe first quarter 2003 a surplus of EUR 1.4 billion, a slightly lower surplusthan in the like period of 2002. This development is due to the lower net flowsfrom the position merchandise and service payments and to the betterdevelopment of the income position.

Table 8

Exports and Imports in Austria — According to Product Group1)

1994 1995 1996 1997 1998 1999 2000 2001 2002 2002

EUR million % of total

Exports (f.o.b):Food and live animals 1,088 1,395 1,666 1,968 2,108 2,309 2,478 2,803 3,075 3.97Beverages and tobacco 258 288 283 358 431 641 780 974 975 1.26Raw materials, inedible,other than fuels 1,597 1,749 1,616 1,869 1,903 2,142 2,396 2,388 2,511 3.24Fossil fuels, lubricants andrelated substances 484 423 547 623 561 656 911 1,452 1,840 2.38Animal and vegetable oils, fats 25 35 28 39 45 52 54 53 66 0.08Chemical products 3,407 3,877 4,156 5,038 5,242 5,655 6,427 7,077 7,929 10.24Processed goods2) 10,752 12,274 12,085 13,468 14,868 14,439 16,363 17,187 17,309 22.36Machinery and vehicles 14,511 16,447 18,083 21,301 23,344 25,982 30,612 32,137 33,069 42.72Miscellaneous manufactured goods 5,102 5,626 5,897 7,222 7,722 8,338 9,089 9,910 10,092 13.04Goods not classed by kind 23 36 127 76 78 51 581 270 535 0.69Total exports3) 37,246 42,151 44,490 51,962 56,302 60,266 69,692 74,251 77,400 100.00

Imports (c.i.f):Food and live animals 2,207 2,562 2,806 3,218 3,311 3,427 3,553 3,937 4,030 5.23Beverages and tobacco 179 195 201 270 319 336 376 437 497 0.64Raw materials, inedible,other than fuels 1,931 2,256 1,947 2,356 2,378 2,487 3,014 2,930 2,960 3.84Fossil fuels, lubricants andrelated substances 2,014 2,151 2,767 3,030 2,565 2,881 4,899 5,500 5,731 7.43Animal and vegetable oils, fats 83 88 101 127 133 116 111 110 126 0.16Chemical products 4,742 5,189 5,359 6,089 6,546 6,749 7,572 8,229 8,683 11.26Processed goods2) 8,744 9,385 9,412 10,507 11,056 11,135 12,501 13,264 12,507 16.22Machinery and vehicles 17,365 17,896 19,613 21,916 24,320 26,947 30,818 31,612 30,020 38.93Miscellaneous manufactured goods 8,415 8,515 9,214 9,725 10,229 11,044 11,814 12,431 12,184 15.80Goods not classed by kind 23 310 377 191 343 193 278 241 368 0.48Total imports3) 45,702 48,548 51,798 57,430 61,200 65,316 74,935 78,692 77,104 100.00

Source: Statistics Austria.1) Based on movements of goods.2) Semi-finished and finished products.3) Amounts may not add up due to rounding.

34 The Austrian Financial Markets�

The Capital Market

���� ������� �������� ������������ ������������� �������

(��������������

��� ���� ���� $��� ���� %��� ���� &��� '��� #���

�����

���

����� �������������

*+��,������

����

-������.����!

/��� �

0���"

��!��"

��

������

12����0!����

������ ������������������

���

%��

�&��

%�$

���

��&

���

'�%

$���

����

'���

���

��'

�$��

$�$

$�&

���

$�#

&��

���$

�%�&

'$��

()�����

Table 9

Balance of Payments1)

1994 1995 1996 1997 1998 1999 2000 20012) 20023)

EUR million

Current account � 2,717 � 4,490 � 4,180 � 5,758 � 4,685 � 6,330 � 5,357 � 4,114 949

Goods � 6,557 � 4,874 � 5,598 � 3,777 � 3,289 � 3,377 � 2,990 � 1,403 3,749Exports - f.o.b. 37,340 42,253 44,615 52,038 56,413 60,504 70,187 74,722 78,031Imports - c.i.f 43,897 47,127 50,213 55,816 59,702 63,881 73,177 76,125 74,282Services 6,108 3,379 3,501 874 2,122 1,648 1,743 2,045 1,069of which travel 2,873 1,925 1,354 788 1,502 1,730 1,536 1,423 1,952Income � 1,373 � 1,741 � 715 � 1,349 � 1,779 � 2,698 � 2,661 � 3,404 -2,134Current transfers � 896 � 1,254 � 1,367 � 1,506 � 1,738 � 1,902 � 1,449 � 1,352 -1,735

Financial account 3,147 5,047 3,812 5,448 5,531 6,614 4,679 4,599 -4,623

Capital account � 232 � 203 � 75 � 111 � 308 � 248 � 475 � 592 -580

Foreign direct investment abroad � 1,043 � 828 � 1,488 � 1,762 � 2,469 � 3,098 � 6,230 � 3,506 -6,001Foreign direct investment in Austria 1,745 1,395 3,405 2,354 4,078 2,792 9,595 6,574 1,612Portfolio investment assets � 3,744 � 2,073 � 6,396 � 8,800 �10,116 �27,207 �29,167 �11,882 -25,151Portfolio investment liabilities 4,036 9,418 4,764 10,174 16,018 24,654 32,395 18,603 19,992Other investment assets � 2,311 � 7,414 651 � 4,526 � 825 �10,571 �17,187 � 9,520 11,320Other investment liabilities 5,260 5,336 3,369 4,572 1,566 18,496 14,698 2,334 -7,795Change in official reserves � 768 � 1,001 � 809 2,608 � 2,914 1,963 838 2,067 1,810

Errors and omissions � 197 � 354 443 421 � 539 � 36 1,152 108 4,254

Source: Oesterreichische Nationalbank.1) Amounts may not add up due to rounding.2) Revised data.3) Provisional data.

The Austrian Financial Markets 35�

The Capital Market

3.3 Labor, Education and Social Services

During 2002, Austria�s total work force (jobholders, the self-employed andthe unemployed) averaged 4.29 million. The number of jobholders (depend-ent employment) averaged 3.16 million, 28% of whom worked in industryand construction, 68% in commerce and other service sectors and 1% inagriculture and forestry.

Unemployment has been increasing in recent years. In 2002 it averaged232,400, compared with 203,900 in 2001. Job vacancies averaged 23,200during 2002. The unemployment rate (Eurostat definition) was 4.3%, whichwas well blow the euro area average (8.3%). This rate is putting Austria inthird place within the Euro area, namely behind Luxemburg and the Nether-lands. The national unemployment rate (not seasonally adjusted) came to6.9% in 2002.

The past few years have also seen the employment of a substantial numberof foreigners. Their number peaked in 2002 with an average of 334,000, or10.6% of all jobholders. At that time, 48.3% of the foreign workers werecitizens of former Yugoslavia, 16.8% of Turkey and 11.7% of EU countries.

Thanks to its well-developed and comprehensive educational system,Austria has a highly-qualified work force. Children have to attend school fromthe age of six, and compulsory schooling lasts for nine years. After four yearsat elementary school, ten-year-old pupils can choose between two systems ofschooling: extended elementary school or secondary school. Pupils whocomplete their studies at a secondary or higher vocational school are awardeda graduation certificate that entitles them to attend university.

In 2002, the federal government�s expenditure on education amounted toEUR 5.66 billion. The system provides pupils with excellent facilities. Thegovernment is continuing to improve the country�s school system by makingclasses smaller and introducing new subjects such as computer science andelectronic data processing. In the 2001/2002 school year, 1.231,000 pupilsattended Austria�s 6,800 schools.

Table 10

Employment and Unemployment in Austria

Dependent employment Registeredunemployment

Unemployment rate Vacancies

in 1,000 annualchange in %

in 1,000 NationalDefinition1)

EUDefinition2)

in 1,000

1991 2,997.4 þ2.3 185.0 5.8 3.4 49.41992 3,055.8 þ2.0 193.1 6.0 3.3 44.11993 3,054.9 �0.0 222.3 6.8 3.9 32.91994 3,070.7 þ0.5 214.9 6.5 3.8 30.21995 3,068.2 �0.1 215.7 6.6 3.9 25.01996 3,047.3 �0.7 230.5 7.0 4.4 19.41997 3,055.6 þ0.3 233.3 7.1 4.4 19.01998 3,076.7 þ0.7 237.8 7.2 4.5 23.11999 3,107.9 þ1.0 221.7 6.7 3.9 31.22000 3,133.7 þ0.8 194.3 5.8 3.7 35.52001 3,148.2 þ0.5 203.9 6.1 3.6 29.72002 3,155.2 þ0.2 232.4 6.9 4.3 23.2

Sources: Austrian Public Employment Service, EUROSTAT, Austrian Institute of Economic Research, Main Association of Austrian Social SecurityInstitutions.1) Registered unemployed in % of dependent employment and registered unemployed.2) Sample survey according to EUROSTAT criteria.