the ancaar audit quality project phase 3 quality of ... · the ancaar audit quality project phase 3...

TRANSCRIPT

1

THEANCAARAUDITQUALITYPROJECTPHASE3

QUALITYOFASSURANCESERVICESFORNON-FINANCIALDISCLOSURES

A report prepared by the 2015-16 Summer Scholars in the Research School of Accounting and Business

Information Systems

Jianyang (Justin) Li Wei (Grace) Li Ziqi (Julian) Gao

15 February 2016

Australian National Centre for Audit and Assurance Research Hanna Neumann Building #21 Canberra ACT 0200 Australia

Contact: [email protected]

1

1. Introduction The rate of non-financial information disclosure is growing in a staggering rate, for over the

last decade, corporate responsibility reporting has become a common practice for the biggest

companies in the world (non-financial information reporting, corporate social responsibility

reporting and sustainability reporting means providing information in terms of economic,

environmental, social and governance performance. In this paper, these terms are used

interchangeably).

According to the survey conducted by KPMG (2015), 64% of the G250 (top 250 of Fortune

500) companies published corporate responsibility reports in 2005, while the rate of corporate

responsibility reporting has reached 92% in 2015.

As corporate responsibility reporting continues to grow in importance, the demand for

external assurance on non-financial information also increased dramatically. Third-party

assurance of corporate responsibility information has been established as a standard practice

for large multinational corporations in the world. More specifically, only 30% of the G250

firms have their non-financial information independently assured in 2005, but the percentage

has increased to 63% in 2015 (KPMG 2015).

Although assurance on sustainability reports has become so important, few people really

understand what “assurance quality” means in terms of non-financial information, and

research in non-financial information assurance quality is relatively sparse. Unlike financial

information assurance, auditing professions do not have a monopoly position on non-

financial information assurance, even though major accountancy organizations currently

dominates the market, the competition with other professions will be fierce in the future.

Therefore, it is important for practitioners and researchers to understand what non-financial

information assurance quality really means. It is also very important to know how the

emergence of greenhouse gas (GHG) reporting and internet-based non-financial disclosure

will affect the auditing profession.

The paper proceeds as follows. The next section provides a brief summary of some of the

literature that deals with non-financial information assurance quality. The relevant auditing

standards for non-financial disclosures are subsequently analyzed and compared. The

following section discusses GHG emissions disclosures: the reporting regulations and

1

schemes for GHG emissions, the assurance providers and standards used for this disclosure

and most importantly, the reason for the need of independent assurance standards for GHG

emissions disclosures. This is succeeded by discussion of the emergence of internet-based

non-financial disclosure, and how it may affect auditing profession. The final part

concludes.

2. Key points of assurance quality literature

• A brief summary Previous research has pointed out the problem in the assurance of non-financial disclosures,

managerial capture. The content analysis conducted by Ball et al. (2000), O’Dwyer (2003),

O’Dwyer and Owen (2005, 2007) and Manurung and Basuki (2010) indicates that managerial

capture is prevailed in the assurance process. For instance, Hasan et al. (2003) find managers

take control of the assurance process by frequently nominating themselves as addressees of

assurance statements.

As for the assurance providers for non-financial disclosures, FEE (2002) identifies five major

assurance providers for non-financial disclosures including experts, rating agents,

accountants/auditors, consultants and social auditors. Considerable differences exist in

presentation formats and contents (Deegan et al 2006), the level of assurance (Mock et al

2007) and quality of assurance (Perego and Kolk, 2012). Thus, choice of assurance providers

should have a significant influence on the overall assurance quality of non-financial

disclosures. Simnett et al (2009) find that a positive relationship exists between company size

and the choice of the auditor. Different assurance providers’ work is perceived to have

different quality. Owen and O’Dwyer (2004) finds the difference between professional and

specialist auditors’ assurance approach results form their different conception of

accountability. Both Pflugrath (2011) and Fernandez-Feijoo et al. (2012) agree that

professional auditors provide higher quality assurance statements. Among professional

auditors, Big Four auditors are perceived to provide even higher quality assurance services

(Hasan et al. 2005; Perego 2009). Different countries have different preferences for the two

types of assurance providers. Deegan et al. (2006) find that European countries except the

UK tend to choose professional auditor as assurers. The professional auditors also dominate

1

assurance engagement for non-financial disclosures in Spanish (Sierra et al. 2013; Zorio et al.

2013). In contrast, Australia and the UK prefer to have CSR reports audited by specialist

auditors (Deegan et al., 2006; Perego, 2009; Moroney, et al. 2011). To increase the assurance

quality, Dando and Swift (2003) argue that stakeholders’ concerns should be included in CSR

auditing process. As Bebbington et al. (2007) state, materiality and relevance of information

presented in the assurance statements can be improved with more stakeholder involvement in

assurance engagement.

• Content analysis

Assurance quality is a complex concept. In the context of non-financial information, it is even

harder to define. Although we did not find a generally accepted definition of assurance

quality in terms of non-financial information, we found that many researchers attempted to

measure assurance quality quantitatively, and the most popular approach was content analysis

of assurance statements.

In order to assess assurance quality on sustainability reports, O’Dwyer and Owen (2005)

constructed an index based on recommended minimum contents of three standards –

AA1000AS, FEE and GRI. Perego and Kolk (2012) and Segui-Mas, Bollas-Araya and Polo-

Garrido (2015) used almost the same sets of index, but they also assign a number to each item

in the index, so that the assurance quality can be measured numerically. For example, if the

finishing date of an assurance exercise is mentioned, one score will be awarded to that

assurance statement (Perego & Kolk 2012). Zorio, Benau and Sierra (2012) developed an

index which was also based on content analysis of assurance statements, but the contents

were based on ISAE 3000 and AA1000AS. Sethi, Martell and Demir 2015 (2015) analyzed

assurance quality based on a structural framework called the CSR-S Monitor, which utilized

content analysis approach as well. The CSR-S Monitor divides the content of sustainability

reports into 11 quantifiable elements, which is very similar to Perego and Kolk’s (2012)

method. The most frequently used items that are included in the assurance quality index are

listed in Table 1.

1

Table 1: Commonly used items in content analysis of assurance quality

(O’Dwyer & Owen 2005), (Perego & Kolk 2012), (Segui-Mas, Bollas-Araya & Polo-Garrido 2015)

Item Explanation

Title Title of assurance statement

Addressee Which stakeholder group the assurance statement is addressed to

Name and location of assuror Name and location of the assurance provider

Report date The finishing date of assurance exercise

Responsibility A statement of what the reporter is responsible to

Independence A statement of independence of assuror

Scope Assurance statement coverage

Objective Objective of assurance engagement

Competencies A description of professional skills

Criteria A statement of what reporting criteria is used (e.g. GRI)

Assurance standard A statement of what assurance standard is used (e.g. AA1000AS or ISAE 3000)

Materiality Indicating if the report satisfies the AA1000 principle of "materiality"

Completeness Indicating if the report satisfies the AA1000 principle of "completeness"

Responsiveness Indicating if the report satisfies the AA1000 principle of "responsiveness"

Conclusion A statement expressing the result of the assurance exercise

In most of the studies mentioned above, researchers did not explain why they chose the index

to measure assurance quality, nor did they evaluate whether the index was a good proxy of

assurance quality. In many cases, researchers focused on the question “what factors may

affect assurance quality” without discussing the meaning of assurance quality. For example,

Perego and Kolk (2012) found accounting firms provided assurance service with higher

quality, because the assurance statements produced by accountants received higher scores

than specialists and certificate bodies. However, they only mentioned that the quality of

1

assurance statement was based on O’Dwyer and Owen’s (2005) work, without evaluating if it

was appropriate to measure assurance quality.

• The problem of not addressing assurance statement to external stakeholders

Sustainability reports are aimed to provide useful information to a wide range of

stakeholders, however, assurance providers are reluctant to address assurance statements to

external stakeholders. In financial information reporting, there is a requirement that the audit

report must be addressed to shareholders, but in terms of non-financial information reporting,

specifying an addressee is not required. In most of the sustainability reporting assurance

statements, no addressee is identified (Deegan, Cooper & Shelly 2006). On the few occasions

that an addressee is identified, it is usually management of the reporting companies (Owen &

O’Dwyer 2004).

The reluctance to address assurance statements to external stakeholders may imply that the

assurance providers are ultimately accountable to management of the reporting entities

(O’Dwyer & Owen 2005), thus auditors who provide assurance service on non-financial

information may not be truly independent. Reporting in financial information is heavily

regulated, however, all aspects in non-financial information reporting are controlled by the

reporting organization (Sethi, Martell & Demir 2015). Therefore, there might be a significant

degree of management control over reporting and assurance process (Owen & O’Dwyer

2004). If assurance providers are only responsible to the management, they will potentially

avoid auditing information that may damage the reputation of the reporting organization.

Due to auditors’ lack of independence, the assurance quality on non-financial information

will not be high.

Not addressing stakeholders as main users of assurance statements also has implications on

materiality of the information provided (Owen & O’Dwyer 2005). According to AA1000AS

(AccountAbility 2008), a piece of information is deemed material if its omission or

misstatement will affect stakeholders’ decision making. Without considering stakeholders’

information needs, materiality cannot be defined properly, and thus the assurance quality will

be negatively affected. In order to enhance assurance quality in sustainability reporting,

stakeholders must be involved in the assurance process, and they should be identified clearly

in the assurance statement as key users.

1

• Audit quality indicators In financial information assurance, many different audit quality indicators have been

developed, which help people to gain insight into financial statement audit quality. For

example, PCAOB uses audit quality indicators such as “training hours per audit

professional”, “average compensation to ensure adequate financial incentive” and “frequency

of financial statement restatement for errors” (PCAOB 2013).

However, in the context of non-financial information assurance, no such assurance indicator

has been developed. Cohen (2014) pointed out that some of the financial information

assurance quality indicators are also appropriate to non-financial information auditing, while

others are not very relevant. The extent to which the indicators are relevant to non-financial

information assurance is shown in table 2 (Cohen 2014). It is an interesting question for

researchers to investigate further in the future.

Table 2. (Cohen 2014)

Common proxies for financial

statement audit quality Relevance for assurance quality for CSR

Material misstatement Can observe restatement, relevant

Going concern opinions Not relevant

Discretionary accruals Not relevant

Accrual quality Not relevant

Market reactions Relevant

PCAOB inspections Not relevant

Audit fees Audit fees to CSR assurance are generally not publicly observable

3. Standards for assurance of non-financial disclosures

1

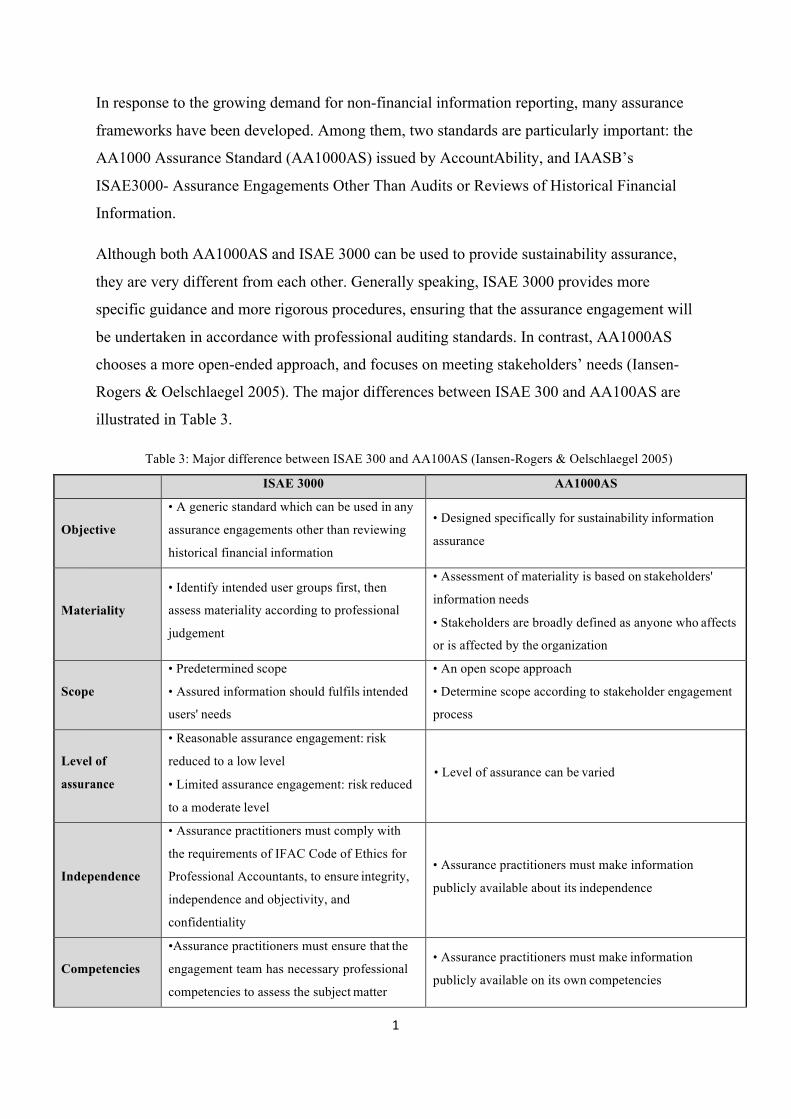

In response to the growing demand for non-financial information reporting, many assurance

frameworks have been developed. Among them, two standards are particularly important: the

AA1000 Assurance Standard (AA1000AS) issued by AccountAbility, and IAASB’s

ISAE3000- Assurance Engagements Other Than Audits or Reviews of Historical Financial

Information.

Although both AA1000AS and ISAE 3000 can be used to provide sustainability assurance,

they are very different from each other. Generally speaking, ISAE 3000 provides more

specific guidance and more rigorous procedures, ensuring that the assurance engagement will

be undertaken in accordance with professional auditing standards. In contrast, AA1000AS

chooses a more open-ended approach, and focuses on meeting stakeholders’ needs (Iansen-

Rogers & Oelschlaegel 2005). The major differences between ISAE 300 and AA100AS are

illustrated in Table 3.

Table 3: Major difference between ISAE 300 and AA100AS (Iansen-Rogers & Oelschlaegel 2005)

ISAE 3000 AA1000AS

Objective

• A generic standard which can be used in any

assurance engagements other than reviewing

historical financial information

• Designed specifically for sustainability information

assurance

Materiality

• Identify intended user groups first, then

assess materiality according to professional

judgement

• Assessment of materiality is based on stakeholders'

information needs

• Stakeholders are broadly defined as anyone who affects

or is affected by the organization

Scope

• Predetermined scope

• Assured information should fulfils intended

users' needs

• An open scope approach

• Determine scope according to stakeholder engagement

process

Level of

assurance

• Reasonable assurance engagement: risk

reduced to a low level

• Limited assurance engagement: risk reduced

to a moderate level

• Level of assurance can be varied

Independence

• Assurance practitioners must comply with

the requirements of IFAC Code of Ethics for

Professional Accountants, to ensure integrity,

independence and objectivity, and

confidentiality

• Assurance practitioners must make information

publicly available about its independence

Competencies

•Assurance practitioners must ensure that the

engagement team has necessary professional

competencies to assess the subject matter

• Assurance practitioners must make information

publicly available on its own competencies

1

Responsiveness

• Focuses on historical performance

information

• A more futuristic perspective

• Besides historical information, practitioners should also

assess if an organization is able to respond to future

challenges

Mandatory • Yes • No

ISAE 300 and AA100AS are complementary and research shows that a large proportion of

assurance engagements use both ISAE 300 and AA100AS at the same time.

As to assurance standards for carbon emissions disclosures, there are two internationally

recognized standards ISO 14064-3:2006 Specification with Guidance for the Validation and

Verification of Greenhouse Gas Assertions, and ISAE 3410 Assurance on greenhouse Gas

Statements. ISO 14064-3:2006 provides, for the first time, a standardized process for

conducting a verification of a GHG inventory. It establishes four principles for conducting

GHG verification: independence, ethical conduct, fair presentation, and due professional care.

This standard also establishes the “fundamentals” for the verification, including the

verification level of assurance, objectives, criteria, scope, and definition of materiality under

the verification (Wintergreen and Delaney, 2007).

Compared to ISO 14064-3: 2006, ISAE 3410 is a relatively new assurance standard for

carbon emissions disclosures. It was released in 2012 by IAASB to enhance the quality and

consistency of assurance engagements on GHG emissions disclosures. The objective of an

engagement under ISAE 3410 is to obtain either limited or reasonable assurance, as

applicable, about whether the GHG statement is free from material misstatement, whether

due to fraud or error. An ISAE 3410 engagement adopts a risk-based approach, regardless of

whether it is a reasonable or limited assurance engagement. This standard applies to

assurance procedures performed with respect to the GHG statement other than when the

GHG statement is a relatively minor part of the overall information subject to assurance

(Ifac.org, 2016).

Huggins et al (2011) points out that the materiality level for different types of assurance and

the amount of detail about the assurance plan revealed to the client are the main differences

between the two standards. ISO 14064-3 states the agreed level of assurance decides the

materiality level while ISAE 3410 states that the materiality level is the same in both limited

and reasonable level of assurance. ISO 14064-3 states that the client needs to know how the

10

assurer will conduct the assurance engagement, while ISAE 3410 states that the assurer must

not discuss the details of the assurance procedures with the client. Different assurance

providers tend to use different assurance standards to conduct the assurance of GHG

emissions disclosures. Audit and assurance services firm providers use the ISAE 3410 more

often while the ISO 1404-3 is the commonly used by specialist auditors.

4. Assurance for GHG emissions disclosures As the global climate warming is drawing more attention worldwide, there has been research

on the specific issue of assurance of GHG emissions disclosures. Simnett and Nugent (2007)

and Simnett et al (2009a) point out that a specific assurance standard for GHG emission

disclosures is necessary as the world is paying more attention to the economic and

environmental impacts of global climate warming and a specific assurance standards can

increase the credibility of this disclosure and any associated trading scheme. Huggins et al.

(2011) suggests that GHG emissions disclosures be included in the financial statements of the

annual report. Green and Li (2011) finds that an expectation gap exists between emissions

preparers, emissions assurers and shareholders in relation to relative responsibilities of

assurers and management, as well as in relation to the assurers’ objectivity. By examining the

assurance practices of 3008 companies across 43 countries between 2006 and 2008, Green

and Zhou (2013) finds that the assurance services for carbon emissions disclosures were

demanded mainly in Europe and companies from carbon intensive industries.

The demand for the disclosure of GHG emissions has increased because of mandatory

Emissions Trading Schemes (ETSs) and Emissions Reporting Schemes (ERSs) in some

countries, including the European Union Emissions Trading Scheme, the United States

Environmental Protection Agency’s Mandatory Greenhouse Gas Reporting Program,

California’s Regulation for the Mandatory Reporting of Greenhouse Gas Emissions,

Alberta’s Climate Change and Emissions Management Act, Australia’s National Greenhouse

and Energy Reporting Scheme, and the New Zealand Emissions Trading Scheme (Green and

Zhou, 2013). There has also been an increase in voluntary reporting of GHG emissions from

entities participating in voluntary ETTs and reporting schemes. Organizations voluntarily

disclose GHG emissions to show that they are good corporate citizens. That can send a signal

to their customers that they are moving towards carbon neutrality and helps differentiate them

11

from their competitors. The assurance of GHG emissions disclosures is largely voluntary

even for entities covered in mandatory ETSs. Only Alberta’s Climate Change and Emissions

Management Act in Canada requires GHG reporting to have a limited level of assurance.

Before 2006, there was no specific assurance standard for GHG emissions disclosures. Just

like other non-financial information, GHG emissions disclosures were audited using AA

1000 Assurance Standard or ISAE 3000 Assurance Engagements Other than Audits or

Reviews of Historical Financial Information.

4.1 the need for independent assurance standards for GHG emissions.

Simnett and Nugent (2007) points out that a specific assurance standard for GHG emission

disclosures is necessary as the economic and environmental impacts of global climate

warming is drawing more attention and a specific assurance standard can increase the

credibility of this disclosure and any associated trading scheme. In fact, the regulatory

requirements in each country that aim to control global warming are the driving force for the

specific assurance standards for GHG emissions. For example, entities covered in Australia’s

National Greenhouse and Energy Reporting (NGER) Act of 2007 will face potential fines

reaching six figures for non-compliance in their GHG emissions reporting. Therefore the

credibility of the GHG emissions disclosures becomes very important. Besides, as the

emission trading schemes are introduced in more countries, the credibility of GHG emissions

disclosures become more significant because organizations can buy or sell carbon permits,

which is based on whether they have exceeded or fallen below their permitted emissions

level. But before 2012, there was no specific assurance standards for GHG emissions

disclosures developed by the international accounting bodies. Therefore this type of

disclosure was audited using the same assurance standards as other non-financial information

and usually only a limited assurance level was provided for GHG emissions disclosures. But

unlike other non-financial information, the GHG emissions include three types and each

requires different auditing procedures and not all three can have the same level of assurance.

Because of the unique nature of GHG emissions disclosure and the importance stakeholders

place on its credibility, an independent assurance standard for GHG carbon disclosures is

necessary.

4.2 the assurance provider

12

Green and Zhou (2013) identify two broad types of assurance providers, audit and assurance

services firm providers and specialist providers. There are differences in the assurance

practices between the two types of assurance providers, including: the scope of the assurance,

the type of report conveying the assurance, the level of the assurance as well as the standards

used for the assurance. When the subject matter is the whole sustainability report, the

assurance service for the GHG emissions disclosures is mainly provided by audit and

assurance services firms. Companies appear to be more willing to choose the assurance

services from specialist providers if the subject assured is GHG only. There are two

internationally recognized assurance standards for carbon emissions disclosures, ISO 14064-

3:2006 Specification with Guidance for the Validation and Verification of Greenhouse Gas

Assertions, and ISAE 3410 Assurance on greenhouse Gas Statements.

4.3 Future development for the assurance of GHG emissions. To increase the level of assurance provided for carbon emissions disclosures, some

researchers suggest that this type of information be included in the financial statements of the

annual report. This can ensure that “these disclosures be subject to the same rigorous level of

assurance as other aspects of the financial report” (Simnett et al. 2007; Huggins et al. 2011).

In fact there are two developments occurring that will make this suggestion possible. One

trend is the integrated reporting, which aims to combine non-financial information with

financial information. The other is the emissions trading schemes. When these schemes issue

tradable securities that will have the characteristics of assets or liabilities, these securities will

need to be included in financial statements (Huggins et al. 2011).

5 Assurance of non-financial disclosure on website

Using internet as a channel to disseminate non-financial information has become a common

practice for many companies in recent years, because it is widely believed that internet-based

reporting has many advantages. However, disclosing information on websites also presents

new challenges to auditors. Online reporting will potentially widen the expectation gap

between auditors and users, and increases auditing risk. Since internet based non-financial

information reporting will grow in importance in the future, it is important for practitioners

and researchers understand the implications of internet-based reporting.

13

5.1 Advantages of internet-based non-financial information disclosure (1) Lower information costs:

Disclosing non-financial information on internet will reduce information costs (Herzig &

Godemann 2010). For example, storing information on a company’s website saves printing

and dissemination costs. In addition, by utilizing XBRL (extensible Business Reporting

Language), a piece of information that is used in multiple ways only need to be prepared for

once, thus avoiding the cost of transferring the information into different formats

(Wagenhofer 2003). Moreover, users of the non-financial information can access specific

information more easily. Sustainability reports usually has a very broad scope, and users have

heterogeneous information demands. If the sustainability report is only provided in printed

format, it will be difficult for users to find the specific information they want. Fortunately,

internet-based reporting provides search engines and hyperlinks, which help users to locate

the information they need (Herzig & Godemann, 2010).

(2) Larger amount of relevant information: At the beginning stage of internet-based reporting, information disclosed on internet is

identical to the printed version, usually in HTML and PDF format. However, in recent years,

it is believed larger amount of information should be incorporated in digital format than in

the printed version (Lymer & Debreceny 2003). First, a printed sustainability report has finite

number of pages, so it only contains limited amount of information. However, all relevant

information can be disclosed on internet. Second, publishing and disseminating printed report

is time consuming, thus some information in the hardcopy is outdated. In contrast, new

information can be updated immediately on a company’s website. As a result, internet-based

sustainability reporting provides users a more complete vision of a company’s sustainability

performance (Herzig & Godemann, 2010).

(3) Customized information: Information needs of different stakeholders are heterogeneous, therefore it would be better

for sustainability report preparers to identify some critical stakeholder groups, and provide

them with relevant and customized information. However, the traditional printed

sustainability report is designed to meet all stakeholders’ needs, thus the information

14

provided may be too general to meet any stakeholder’s real needs (Isenmann 2004). Internet-

based technology will enable organizations to provide more customised information to

important stakeholders. For example, information preparers can develop a so-called XML

schema, and each XML schema can be used to produce customised information for a target

stakeholder group (Isenmann, Bey and Welter 2007).

(4) More interaction with stakeholders: Stakeholder involvement is very important for sustainability reporting. In order to decide

what information is relevant and material, companies must communicate to stakeholders.

AA1000AS emphasizes that an organization must be responsive to stakeholders’ concerns.

To prepare printed report, organizations usually only contact stakeholders before the

production of report. By disclosing information on internet, companies are able to contact

stakeholders continuously. Stakeholders can contact the company in various ways, for

example by email, on internet chat room or through video conference. It will help companies

to better understand stakeholders’ needs, and provide information with more relevance and

higher quality (Herzig & Godemann 2010).

5.2 Challenges to auditors (1) Professional pronouncement:

The emergence of internet-based reporting presents new challenges to auditors. Currently, it

is still unclear whether auditors have responsibilities to examine information provided on

corporate websites. The existing standards and guidance on internet reporting assurance are

sometimes ambiguous, and standards in different countries are very different from each other.

According to International Standard on Auditing (ISA) 720: The Auditor’s Responsibilities

Relating to Other Information which is issued by International Federation of Accountants

(IFAC), auditors are responsible to make sure that there is no material inconsistency between

audited information and “other information”. However, ISA 720 excludes information

disclosed on websites from the definition of “other information”. Although IAASB

considered if ISA 720 should include internet-reporting issues, they eventually concluded that

it was impractical for auditors to monitor online information continuously (Fisher & Naylor

2015).

15

In the US, according to Statement of Auditing Standards No.8 “Other Information in

Documents Containing Audited Financial Statements”, auditors have no responsibilities to

read information on their client’s websites, nor do they need to consider consistency between

audited information and online information (Fisher & Naylor 2015).

In contrast to the US standard, Australian standard (Auditing Guidance Statement 1050)

suggests that auditors do have responsibilities in examining electronic data on the internet.

However, AGS 1050 does not provide specific guidance on how to conduct assurance

engagements on information presented on corporate websites. The guidance suggests that

auditors should use their professional judgement to determine what information disclosed on

the internet should be examined (Lymer & Debreceny 2003). Interestingly, AGS 1050

suggests that “Engagements to provide assurance in respect of matters relating to the entity’s

web site do not form part of the financial report auditing engagement, but may be agreed with

management as a separate engagement” (AUASB 2002, AGS 1050, para. 20), because

Australian standard setters believe that the current audit report is not suitable to internet-

based reporting (Lymer & Debreceny 2003).

(2) Inappropriate association of audited and non-audited information: When a company disclose information on its websites, unaudited information is sometimes

presented alongside audited information. Moreover, hyperlinks connect audited information

to web pages which contains unaudited information. As a result, it is difficult for users to

distinguish between audited and non-audited information (Fisher & Naylor 2015). Hodge

(2001) finds if a company connect audited financial report with unaudited information by

hyperlinks, users are highly likely to perceive the unaudited information as audited.

Therefore, firms can potentially manipulate users’ perception by using hyperlinks. In order to

protect their reputation, it is important for auditors to make sure that their clients have made

adequate steps to prevent inappropriate association of audited and non-audited information

(Fisher, Oyelere & Laswad 2004).

The most commonly used method to distinguish audited information from unaudited

information is to making audited report into PDF files, while keeping unaudited information

in other formats. Since many users are not sophisticated enough, complicated hyperlinks can

still confuse them. Auditors should ask their clients to make audited information which is

presented on internet more visually distinctive, for example using watermarks or intermediate

warning web pages (Fisher, Oyelere & Laswad 2004).

16

(3) Omission of audit report: A large proportion of companies publish their financial reports on the internet do not include

the corresponding audit reports (Fisher, Oyelere & Laswad 2004). Ettredge (2000) finds that

compare to companies receive unqualified audit opinions, companies receive qualified

opinions or going concern modifications are more likely to omit the auditors’ reports on

websites. Therefore, users cannot decide if the information on internet has been audited, and

they cannot see the auditor’s opinions. In terms of non-financial reporting, although external

assurance is not mandatory, it is still important for auditors to make sure that their clients

who report on the internet also include the assurance report on their websites.

(4) Continuous monitoring: To provide users more timely information, companies often release real-time information on

their websites. To make sure that all material information updated is true and fair, auditors

will have to monitor the information published on websites continuously. Furthermore, online

information is susceptible to unauthorized alteration, for example corporate websites may be

attacked by hackers. Many people believe it is auditors’ responsibility to protect the integrity

of the information disclosed online, they suggest that all material modification of information

on the internet must be authorized by auditors (Khadaroo 2005).

(5) Expectation gap: Since corporate websites have become a major source of information, many users will expect

auditors to protect the integrity of information provided online. However, auditors are slow to

adapt the internet reporting environment. As can be seen, the emergence of internet-based

reporting makes auditors’ work more difficult, but professional pronouncement and auditing

standards do not provide auditors clear guidance on how to examine information presented on

corporate websites. Therefore, the audit expectation gap will become wider.

Fisher and Naylor (2015) conducted a survey in New Zealand, and concluded that the

expectation gap of auditors’ responsibilities in internet reporting related issues does exist.

More specifically, auditors in New Zealand were unsure (or did not want to acknowledge)

their internet reporting related responsibilities, while shareholders and sophisticated

information users could identify many auditor’s existing responsibilities. In order to reduce

auditors’ expectation gap, Fisher and Naylor (2015) suggested the overall expectation gap

should be decomposed into different parts, and each part should be managed differently.

17

According to Porter (1993), audit expectation gap can be divided into three parts: deficient

standard gap, deficient performance gap, and reasonableness gap.

Reasonableness gap - the gap between society’s expectation and what auditors can

reasonably be expected. Some of the users’ expectations are unrealistic, for example many

shareholders thought auditors should monitor the change in information on websites

continuously to protect the integrity of online information. However, continuous monitoring

online information is too costly and impractical. Therefore, auditors should educate the users

so that their expectations will not be unrealistic (Fisher & Naylor 2015).

Deficient standard gap - the gap between society’s reasonable expectation and auditor’s

existing legal responsibilities. Although in New Zealand, the assurance standard does not

require auditors to check if there is any inappropriate omission of auditor’s report on the

internet, according to the survey, both auditors and users believed that auditors should accept

this responsibility. Obviously, it helps users to better understand whether information

disclosed on a website has been audited, while the incremental cost for auditors is minimal.

Assurance standard should specify more auditors’ responsibilities in internet reporting issues

if they pass the cost-benefit test (Fisher & Naylor 2015).

Deficient performance gap - the gap between auditor’s existing legal responsibilities and

auditors’ performance perceived by society. It reflects how well auditors have performed

their existing internet reporting related responsibilities. For example, in New Zealand

auditors are responsible to make sure that there is no material inconsistency between audited

information and information disclosed on companies’ websites. However, most users thought

auditors did not do very well in this job. To reduce expectation gap, auditors should improve

their performance (Fisher & Naylor 2015).

5.3 Future of the internet-based non-financial information assurance In my opinion, internet based non-financial information assurance service has three main

trends. First, as the internet based reporting continue to grow in importance, new assurance

standards and approaches need to be developed, so that auditors can better adapt online

reporting environment. Second, rather than verifying the accuracy of data, auditors should put

more efforts in reviewing the overall information system. Third, integrated reporting which

combines financial and non-financial information in a single report might become important

18

in the future, so researchers and practitioners should start to consider how to conduct

assurance engagements in relation to integrated reporting.

(1) New auditing approaches: As far as I am concerned, some traditional auditing approaches might not be appropriate for

internet-based non-financial information reporting, so auditors and regulators should develop

new standards and techniques to better assure information disclosed electronically.

The Australian auditing standard AGS 105 suggests disclosing information on the internet

may require auditors to consider new approaches, and it points out that some factors may

affect the electronic presentation of the audit report. First, in printed format, audit report links

the financial report which has been audited by reference to page numbers. However, page

numbers are not suitable in digital format (AUASB 2002, AGS 1050, para. 25). I think the

audit report can also be made into digital format, so that the audit report and relevant sections

of financial report can be connected by hyperlinks. Second, auditor’s signature traditionally

provides authentic identification of the auditor, but on the internet, signatures may not be able

to protected information from unauthorized changes (AUASB 2002, AGS 1050, para. 25). It

is suggested that auditors should apply cryptographic techniques and digital signatures on the

internet (Fisher, Oyelere & Laswad 2004). Furthermore, the content of audit report can also

be changed in order to decrease audit risk. For example, auditors can indicate in the audit

report that they have not provide assurance on information disclosed on their client’s website,

or they do not provide any opinion on information that is hyperlinked (Fisher, Oyelere &

Laswad 2004). In addition, some people suggest better control will be achieved if auditors

host the website which contains audited information for their clients (Khadaroo 2005).

It is important to develop assurance standards which provide clear guidance on how to audit

non-financial information disclosed on the internet. Currently, there is a lack of generally

accepted assurance guidance on internet reporting and sustainability reporting. However, as

more and more companies start to disclose non-financial information on the internet, auditors

will need more specific guidance to meet this demand. Unlike financial reporting, auditing

profession does not have a monopoly position in sustainability reporting. If auditors do not

respond quickly to the internet reporting environment, they will be placed at a competitive

disadvantage relative to other professions (Xiao, Jones & Lymer 2002).

19

(2) WebTrust and SysTrust: Due to the innovation of internet technology, verifying the accuracy of particular information

will become less practical and less important. Internet-based reporting enables more

information to be produced and disseminated in a lower cost on a continuous basis.

Therefore, asking auditors to assume an ongoing responsibility to monitor such a large

amount of information is unrealistic. More importantly, the format of internet reporting is too

flexible and customised. For example, XBRL allows users to define the structure of the

online reports, and put their own assumptions to produce the information they want

(Wagenhofer 2003). As a result, it will be impossible to examine all customised reports.

In the future, the service on auditing the overall soundness of the information system will

become more important, therefore trust services such as WebTrust and SysTrust will be more

popular. In a SysTrust engagement, auditors evaluate the reliability of a company’s

information system, and test if the system can operate efficiently without material error.

SysTrust increases the credibility of information presented on a website, and reduces the

likelihood of business interruptions due to system breakdown (Bedard, Jackson & Graham

2005). By comparison, WebTrust is more focused on E-commerce. If an internet vendor

discloses and follows its business practices, completes and bills transaction as agreed, and

protects clients’ privacy, a WebTrust seal will be provided on the vendor’s website, thereby

increasing his trustworthiness (Houston & Taylor 1999).

(3) Integrating financial and non-financial information: Some researchers believe that stand-alone environmental, social and financial reports should

be integrated into one report which shows interrelations between financial and non-financial

information (Eccles & Krzus 2010). Since an organisation’s economic and social

performance may affect its long-term profitability, showing the relationship between

economic and non-economic factors will better inform investors and other stakeholders how

an organization creates value in a sustainable manner (Eccles, Schulschenk & Serafeim

2011). The relationship between environmental, social and financial performance can be

more clearly illustrated in an internet-reporting environment, because internet provides

hyperlinks between different parts of the report, and connects non-financial information to

financial factors it affects (Isenmann 2004). For example, in integrated online report, users

will more easily understand how waste reduction affects productivity and future income of a

manufacturer.

20

Assurance of integrated reports is not mandatory, but assurance service does increase

credibility of the information in integrated reports. Currently, there is a lack of assurance

guidance or standard for auditing integrated reports (Cohen & Simnett 2015). Since internet

facilitates integrated reporting, many companies will present both financial and non-financial

information online in the future, and guidance for integrated reporting should be developed in

the future.

6. Conclusion In this report, we first find that in the context of non-financial information, currently there is

no generally accepted definition of assurance quality. The most commonly used method to

measure assurance quality by researchers is content analysis of assurance statement. Second,

we discuss the implication of greenhouse gas emissions disclosures. Third, although internet

based non-financial information reporting has many advantages, it also presents many

challenges.

REFERENCES Auditing & Assurance Standards Board, 2002, AGS 1050 Audit Issues Relating to the

Electronic Presentation of Financial Reports, AUASB, Canberra, viewed 2016-1-28, <

http://www.auasb.gov.au/admin/file/content102/c3/AGS1050_07-02.pdf>

Ball, A., Owen, D. and Gray, R. 2000. External transparency or internal capture? The

role of third-party statements in adding value to corporate environmental reports.

Business Strategy and the Environment, 9(1), pp.1-23.

Bebbington, J., Brown, J., Frame, B. and Thomson, I. (2007). Theorizing engagement: the

potential of a critical dialogic approach. Accounting, Auditing & Accountability Journal,

20(3), pp.356-381.

21

Bedard, J., Jackson, C. and Graham, L. 2005. Issues and risks in performing SysTrust®

engagements: implications for research and practice. International Journal of Accounting

Information Systems, 6(1), pp.55-79.

Cohen, J. and Simnett, R. 2015. CSR and Assurance Services: A Research Agenda.

AUDITING: A Journal of Practice & Theory, 34(1), pp.59-74.

Deegan, C., Cooper, B. and Shelly, M. 2006. An Investigation of TBL Report

Assurance Statements: Australian Evidence. Australian Accounting Review, 16(39),

pp.2-18.

Deegan, C., Cooper, B. and Shelly, M., 2006, An investigation of TBL report assurance

statements: UK and European evidence, Managerial Auditing Journal, 21(4), 329–71.

Eccles, R. and Krzus, M. 2010. One report. Hoboken, N.J.: John Wiley & Sons.

FEE. 2002. Providing assurance on sustainability reports. Fedération des Experts Comptables

Européens: Brussels.

Ferna´ndez-feijo´ o-souto B.; Romero S. and Ruiz-blanco S., 2012, Measuring quality of

sustainability reports and assurance statements: characteristics of the high quality reporting

companies, International Journal of Society Systems Science (IJSSS), 4(1), 5–27.

Fisher, R. and Naylor, S. 2015. Corporate reporting on the Internet and the expectations gap:

new face of an old problem. Accounting and Business Research, pp.1-25.

Fisher, R., Oyelere, P. and Laswad, F. 2004. Corporate reporting on the Internet. Managerial

Auditing Journal, 19(3), pp.412-439.

Gray, R.: 2000, Current Developments and Trends in Social and Environmental Auditing,

Reporting and Attestation: A Review and Comment, International Journaol f Auditing4 (3),

247-268.

Green, W., A. Huggins, and R. Simnett. 2011. An International Review of Assurance

Regulations and standards for Greenhouse gas Emissions Report. Working paper, University

of New South Wales.

22

Green, W. and Li, Q. 2011. Evidence of an expectation gap for greenhouse gas emissions

assurance. Accounting, Auditing & Accountability Journal, 25(1), pp.146-173.

Green, W. and Zhou, S. 2013. An International Examination of Assurance Practices on

Carbon Emissions Disclosures. Australian Accounting Review, 23(1), pp.54-66.

Hasan, M., Roebuck, P.J. and Simnett, R. 2003, An investigation of alternative report formats

for communicating moderate levels of assurance, Auditing, Vol. 22 No. 2, pp. 171-187.

Hasan M, Maijoor S, Mock TJ, Roebuck P, Simnett R, Vanstraelen A. 2005. The different

types of assurance services and levels of assurance provided. International Journal of

Auditing 9: 91–102

Herzig, C. and Godemann, J. 2010. Internet-supported sustainability reporting: developments

in Germany. Management Research Review, 33(11), pp.1064-1082.

Huggins, A., Green, W. and Simnett, R. 2011. The Competitive Market for Assurance

Engagements on Greenhouse Gas Statements: Is There a Role for Assurers from the

Accounting Profession? Current Issues in Auditing, 5(2), pp.A1-A12.

Ifac.org, (2016). At a Glance: International Standard on Assurance Engagements (ISAE)

3410, Assurance Engagements on Greenhouse Gas Statements | IFAC. [online] Available at:

http://www.ifac.org/publications-resources/glance-international-standard-assurance-

engagements-isae-3410-assurance-engag [Accessed 1 Feb. 2016].

International Auditing and Assurance Standards Board (IAASB) (2013), ISAE 3410

Assurance on Greenhouse gas Statements.

Institute for Social and Ethical AccountAbility 2008, AA1000 AccountAbility principles

standard 2008, AccountAbility, London International Organization for Standardization (ISO), 2006, “ISO 14064-3: Greenhouse

Gases – Part 3: Specification with Guidance for the Validation and Verification of

Greenhouse Gas Assertions”, Geneva.

Isenmann, R. 2004. Internet-based sustainability reporting. International Journal of

Environment and Sustainable Development, 3(2), p.145.

23

Isenmann, R., Bey, C. and Welter, M. 2007. Online reporting for sustainability

issues. Business Strategy and the Environment, 16(7), pp.487-501.

Khadaroo, I. 2005. Corporate reporting on the internet: some implications for the auditing

profession. Managerial Auditing Journal, 20(6), pp.578-591.

Lymer, A. and Debreceny, R. 2003. The Auditor and Corporate Reporting on the Internet:

Challenges and Institutional Responses. International Journal of Auditing, 7(2), pp.103-120.

Manurung, A.M. and Basuki, H. 2010, An analytical assessment of assurance practices in

social environmental and sustainable reporting in the United Kingdom and North America,.

International Journal of Business, Vol. 12 No. 1, pp. 75-115.

Manetti, G. and Toccafondi, S. 2011. The Role of Stakeholders in Sustainability Reporting

Assurance. J Bus Ethics, 107(3), pp.363-377.

Mock T. J., Strohm C. and Swartz K. M., 2007, An examination of worldwide assured

sustainability reporting, Australian Accounting Review, 17(41), 67–77

Moroney R,Windsor C, Ting Aw Y. 2011. Evidence of assurance enhancing the quality of

voluntary environmental disclosures: an empirical analysis. Accounting and Finance.

O’Dwyer, B.: 2003, Conceptions of Corporate Social Responsibility: The Nature of

Managerial Capture, Accounting, Auditing and Accountability Journal 16(4), 523–557.

O'Dwyer, B. and Owen, D. 2005. Assurance statement practice in environmental, social and

sustainability reporting: a critical evaluation. The British Accounting Review, 37(2), pp.205-

229.

O’Dwyer, B. and Owen, D. 2007, Seeking stakeholder-centric sustainability assurance: an

examination of recent sustainability assurance practice, Journal of Corporate Citizenship,

Vol. 25, pp. 77-94

Olson, E. 2010. Challenges and opportunities from greenhouse gas emissions reporting and

independent auditing. Managerial Auditing Journal, 25(9), pp.934-942.

24

Owen, D. L., T. A. Swift, C. Humphrey and M. Bowerman: 2000, The New Social Audits:

Accountability, Managerial Capture or the Agenda of Social Champions?, European

Accounting Review 9(1), 81–98.

Owen, D., Swift, T. and Hunt, K. 2001. Questioning the Role of Stakeholder Engagement in

Social and Ethical Accounting, Auditing and Reporting. Accounting Forum, 25(3), pp.264-

282.

Owen DL, O’Dwyer B. 2004. Assurance Statement Quality in Environmental, Social and

Sustainability Reporting: A Critical Evaluation of Leading Edge Practice. International

Centre for Corporate Social Responsibility: Nottingham.

Perego P. M., 2009, Causes and consequences of choosing different assurance providers: An

international study of sustainability reporting, International Journal of Management, 26(3),

412–25.

Perego P. and Kolk A., 2012, Multinationals’ accountability on sustainability: the evolution

of third-party assurance of sustainability reports, Journal of Business Ethics, 110, 173–90.

Porter, B. 1993. An Empirical Study of the Audit Expectation-Performance Gap. Accounting

and Business Research, 24(93), pp.49-68.

Public Company Accounting Oversight Board 2013, PCAOB Discussion – Audit Quality

Indicators, PCAOB, Washington D.C. Sierra L., Zorio A. and Garc´ia-benau M. A., 2013, Sustainable development and assurance

of corporate social responsibility reports published by Ibex-35 Companies, Corporate Social

Responsibility and Environmental Management, 20(6), 359–370.

Simnett, R. and Nugent, M. 2007. Developing an Assurance Standard for Carbon Emissions

Disclosures. Australian Accounting Review, 17(42), pp.37-47.

Simnett, R., Nugent, M. and Huggins, A.L. 2009, Developing an international assurance

standard on carbon emissions disclosures, Accounting Horizons, Vol. 23 No. 4, pp. 347-63.

Simnett, R., Vanstraelen, A. and Chua, W. 2009. Assurance on Sustainability Reports: An

International Comparison. The Accounting Review, 84(3), pp.937-967.

2

Smith, J., Haniffa, R. and Fairbrass, J. 2010. A Conceptual Framework for Investigating

‘Capture’ in Corporate Sustainability Reporting Assurance. J Bus Ethics, 99(3), pp.425-439.

Wagenhofer, A. 2003. Economic Consequences of Internet Financial Reporting.

Schmalenbach Business Review, Vol. 55, pp. 262-279

Wintergreen J, Delaney T. 2007. ISO 14064, International Standard for GHG Emissions

Inventories and Verification. Raleigh, NC: 16th Annual International Emissions Inventory

Conference.

Xiao, Z., Jones, M. and Lymer, A. 2002. Immediate trends in Internet reporting. European

Accounting Review, 11(2), pp.245-275.

Zorio, A., García-Benau, M. and Sierra, L. 2012. Sustainability Development and the Quality

of Assurance Reports: Empirical Evidence. Business Strategy and the Environment, 22(7),

pp.484-500.

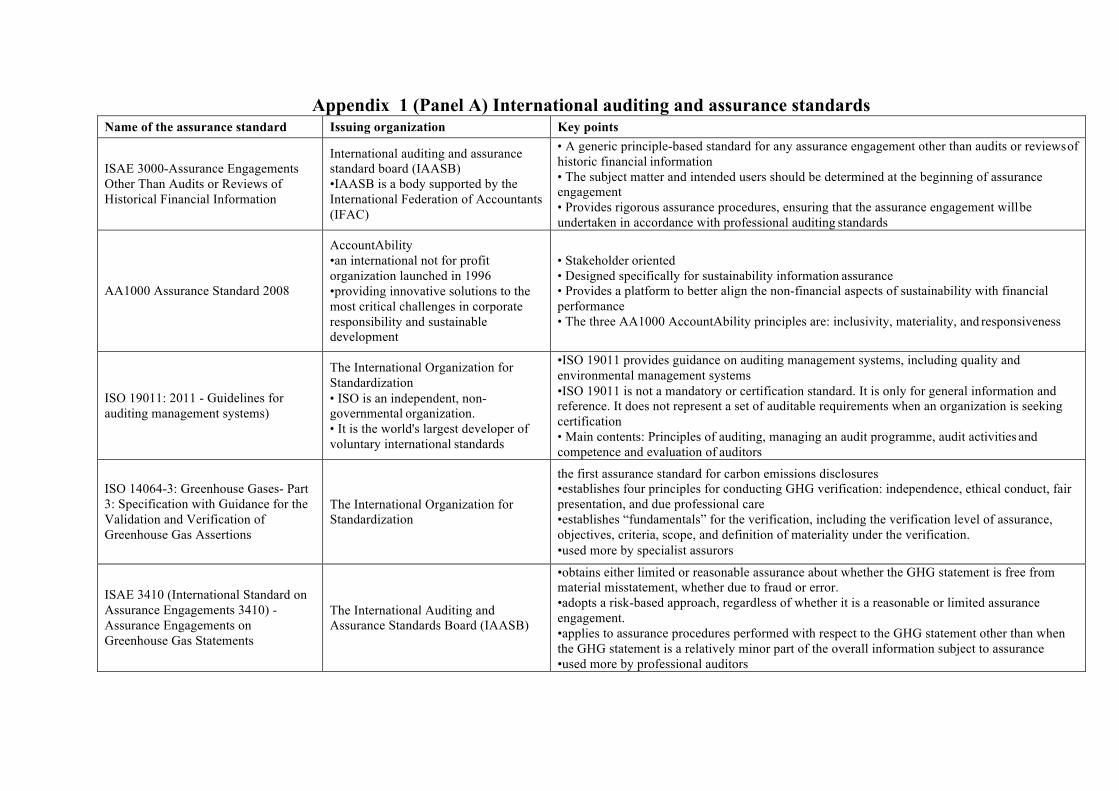

Appendix 1 (Panel A) International auditing and assurance standards Name of the assurance standard Issuing organization Key points

ISAE 3000-Assurance Engagements Other Than Audits or Reviews of Historical Financial Information

International auditing and assurance standard board (IAASB) •IAASB is a body supported by the International Federation of Accountants (IFAC)

• A generic principle-based standard for any assurance engagement other than audits or reviews of historic financial information • The subject matter and intended users should be determined at the beginning of assurance engagement • Provides rigorous assurance procedures, ensuring that the assurance engagement will be undertaken in accordance with professional auditing standards

AA1000 Assurance Standard 2008

AccountAbility •an international not for profit organization launched in 1996 •providing innovative solutions to the most critical challenges in corporate responsibility and sustainable development

• Stakeholder oriented • Designed specifically for sustainability information assurance • Provides a platform to better align the non-financial aspects of sustainability with financial performance • The three AA1000 AccountAbility principles are: inclusivity, materiality, and responsiveness

ISO 19011: 2011 - Guidelines for auditing management systems)

The International Organization for Standardization • ISO is an independent, non- governmental organization. • It is the world's largest developer of voluntary international standards

•ISO 19011 provides guidance on auditing management systems, including quality and environmental management systems •ISO 19011 is not a mandatory or certification standard. It is only for general information and reference. It does not represent a set of auditable requirements when an organization is seeking certification • Main contents: Principles of auditing, managing an audit programme, audit activities and competence and evaluation of auditors

ISO 14064-3: Greenhouse Gases- Part 3: Specification with Guidance for the Validation and Verification of Greenhouse Gas Assertions

The International Organization for Standardization

the first assurance standard for carbon emissions disclosures •establishes four principles for conducting GHG verification: independence, ethical conduct, fair presentation, and due professional care •establishes “fundamentals” for the verification, including the verification level of assurance, objectives, criteria, scope, and definition of materiality under the verification. •used more by specialist assurors

ISAE 3410 (International Standard on Assurance Engagements 3410) - Assurance Engagements on Greenhouse Gas Statements

The International Auditing and Assurance Standards Board (IAASB)

•obtains either limited or reasonable assurance about whether the GHG statement is free from material misstatement, whether due to fraud or error. •adopts a risk-based approach, regardless of whether it is a reasonable or limited assurance engagement. •applies to assurance procedures performed with respect to the GHG statement other than when the GHG statement is a relatively minor part of the overall information subject to assurance •used more by professional auditors

Appendix 1 (Panel B) Individual country's auditing standards

Country or Region Name of the standard

Australia General Guidelines on the Verification, Validation and Assurance of Environmental and Sustainability Reports.

Australia Standard on Assurance Engagements ASAE 3410 Assurance Engagements on Greenhouse Gas Statements

New Zealand General Guidelines on the Verification, Validation and Assurance of Environmental and Sustainability Reports.

US Attest Engagements on Greenhouse Gas Emissions Information Europe EU Emissions Trading System Guidance on Annual Verification for emissions from stationary installations emitted before 1 January 2013 Germany Germany Generally Accepted Assurance Principles for Audit or Review of Sustainability Reports (ED As).

Sweden Proposed Recommendation on Independent Review of Voluntary Separate Sustainability Report.

The Netherlands Practitioners Working with Subject Matter Experts from other Disciplines on Non-Financial Assurance Engagements (ED 3010) .

The Netherlands Assurance Engagements Relating to Sustainability Reports (ED 3410). Italy Linee guida per l’asseverazione dei report di sostenibilita`.

France

Informal Guidance on Pratique professionnelle relative au rapport du Commissaire aux Comptes sur certaines donne´es ou informations environnementales et sociales ou sur les proce´dures d’e´tablissement de ces donne´es ou informations, contenus dans le rapport rendant compte en matie`re de de´veloppement durable.

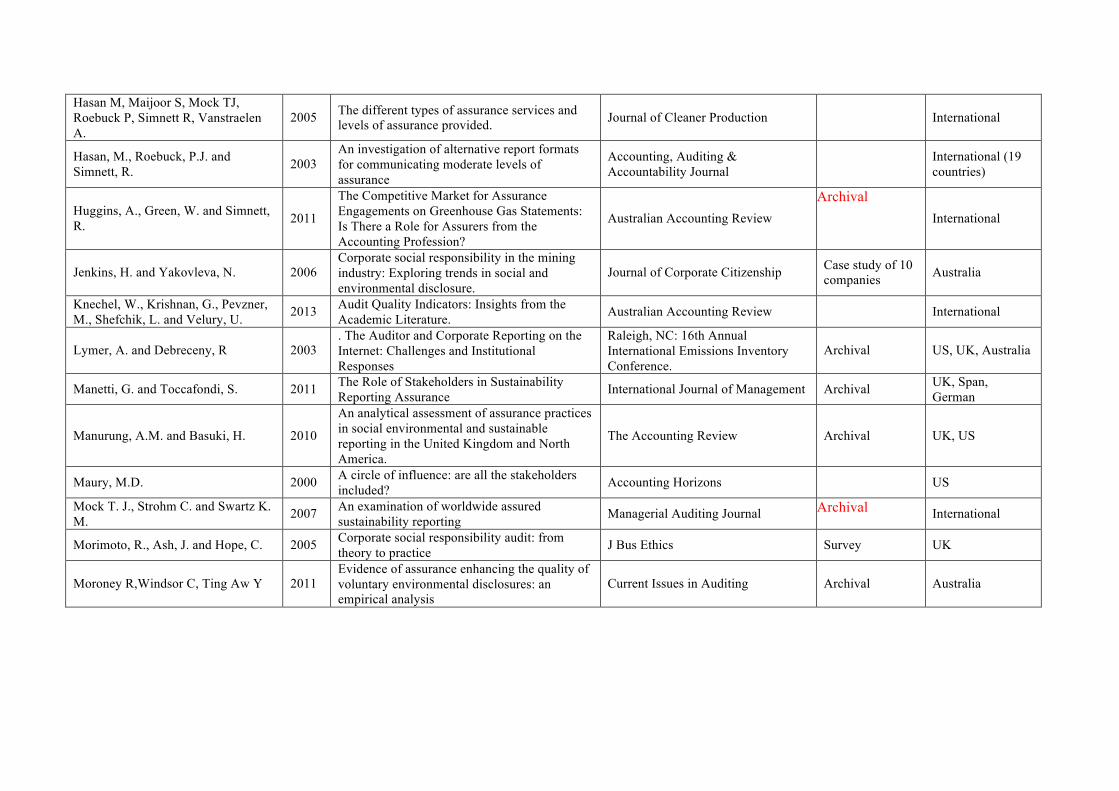

Appendix 2 Academic literature Author Year Title Journal Research

Method Country

Ball, A., Owen, D. and Gray, R.

2000

External transparency or internal capture? The role of third-party statements in adding value to corporate environmental reports.

Business Strategy and the Environment

Archival 13 European

countries

Bebbington, J., Brown, J., Frame, B. and Thomson, I. 2007 Theorizing engagement: the potential of a

critical dialogic approach. International Journal f Auditing International

Cohen, J. and Simnett, R. 2015 CSR and Assurance Services: A Research Agenda. Journal of Business Ethics International

Dando, N. and Swift, T. 2003 Transparency and assurance: minding the credibility gap European Accounting Review UK

Deegan, C., Cooper, B. and Shelly, M. 2006 An Investigation of TBL Report Assurance

Statements: Australian Evidence Critical Perspectives on Accounting Archival Australia

Deegan, C., Cooper, B. and Shelly, M.

2006 An investigation of TBL report assurance

statements: UK and European evidence

Accounting Forum

Archival

UK and 9 European countries

Ferna´ndez-feijo´ o-souto B.; Romero S. and Ruiz-blanco S.

2012

Measuring quality of sustainability reports and assurance statements: characteristics of the high quality reporting companies

Journal of Business Ethics

International

Fisher, R. and Naylor, S 2015 Corporate reporting on the Internet and the expectations gap: new face of an old problem Auditing Survey New Zealand

Fisher, R., Oyelere, P. and Laswad, F 2004 Corporate reporting on the Internet Accounting, Auditing and Accountability Journal Survey New Zealand

Gendron, Y. and J. Be´dard 2001 Academic Accounting Research: An Exploratory Investigation into its Usefulness

International Centre for Corporate Social Responsibility: Nottingham

US, Canada

Gray, R.

2000

Current Developments and Trends in Social and Environmental Auditing, Reporting and Attestation: A Review and Comment

International Journal of Auditing

Not mentioned

Green, W. and Li, Q. 2011 Evidence of an expectation gap for greenhouse gas emissions assurance Journal of Business Ethics Survey Australia

Green, W. and Taylor, S. 2013 Factors that Influence Perceptions of Greenhouse Gas Assurance Provider Quality. The British Accounting Review Survey Australia

Green, W. and Zhou, S. 2013 An International Examination of Assurance Practices on Carbon Emissions Disclosures Australian Accounting Review Archival 43 countries

Hasan M, Maijoor S, Mock TJ, Roebuck P, Simnett R, Vanstraelen A.

2005 The different types of assurance services and

levels of assurance provided.

Journal of Cleaner Production

International

Hasan, M., Roebuck, P.J. and Simnett, R.

2003

An investigation of alternative report formats for communicating moderate levels of assurance

Accounting, Auditing & Accountability Journal

International (19 countries)

Huggins, A., Green, W. and Simnett, R.

2011

The Competitive Market for Assurance Engagements on Greenhouse Gas Statements: Is There a Role for Assurers from the Accounting Profession?

Australian Accounting Review

Archival International

Jenkins, H. and Yakovleva, N.

2006

Corporate social responsibility in the mining industry: Exploring trends in social and environmental disclosure.

Journal of Corporate Citizenship Case study of 10

companies

Australia

Knechel, W., Krishnan, G., Pevzner, M., Shefchik, L. and Velury, U. 2013 Audit Quality Indicators: Insights from the

Academic Literature. Australian Accounting Review International

Lymer, A. and Debreceny, R

2003

. The Auditor and Corporate Reporting on the Internet: Challenges and Institutional Responses

Raleigh, NC: 16th Annual International Emissions Inventory Conference.

Archival

US, UK, Australia

Manetti, G. and Toccafondi, S. 2011 The Role of Stakeholders in Sustainability Reporting Assurance International Journal of Management Archival UK, Span,

German

Manurung, A.M. and Basuki, H.

2010

An analytical assessment of assurance practices in social environmental and sustainable reporting in the United Kingdom and North America.

The Accounting Review

Archival

UK, US

Maury, M.D. 2000 A circle of influence: are all the stakeholders included? Accounting Horizons US

Mock T. J., Strohm C. and Swartz K. M. 2007 An examination of worldwide assured

sustainability reporting Managerial Auditing Journal Archival International

Morimoto, R., Ash, J. and Hope, C. 2005 Corporate social responsibility audit: from theory to practice J Bus Ethics Survey UK

Moroney R,Windsor C, Ting Aw Y

2011

Evidence of assurance enhancing the quality of voluntary environmental disclosures: an empirical analysis

Current Issues in Auditing

Archival

Australia

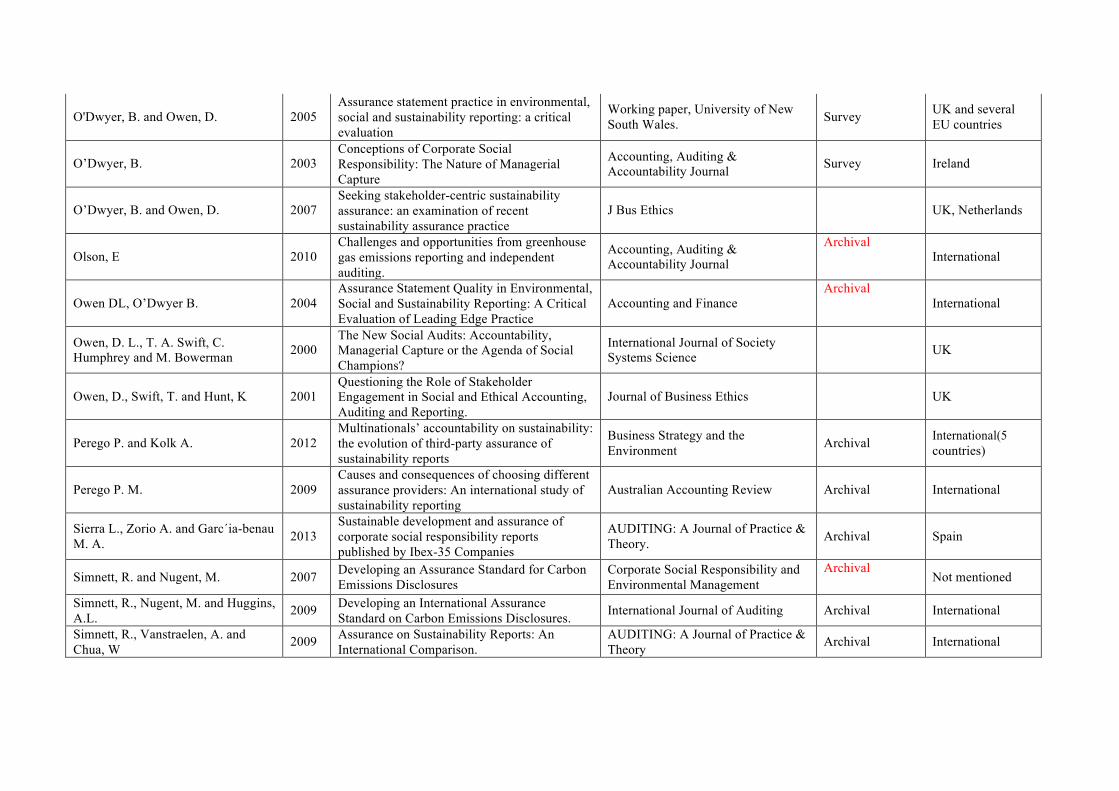

O'Dwyer, B. and Owen, D.

2005 Assurance statement practice in environmental, social and sustainability reporting: a critical evaluation

Working paper, University of New South Wales.

Survey UK and several

EU countries

O’Dwyer, B.

2003

Conceptions of Corporate Social Responsibility: The Nature of Managerial Capture

Accounting, Auditing & Accountability Journal

Survey

Ireland

O’Dwyer, B. and Owen, D.

2007

Seeking stakeholder-centric sustainability assurance: an examination of recent sustainability assurance practice

J Bus Ethics

UK, Netherlands

Olson, E

2010

Challenges and opportunities from greenhouse gas emissions reporting and independent auditing.

Accounting, Auditing & Accountability Journal

Archival International

Owen DL, O’Dwyer B.

2004

Assurance Statement Quality in Environmental, Social and Sustainability Reporting: A Critical Evaluation of Leading Edge Practice

Accounting and Finance

Archival International

Owen, D. L., T. A. Swift, C. Humphrey and M. Bowerman

2000

The New Social Audits: Accountability, Managerial Capture or the Agenda of Social Champions?

International Journal of Society Systems Science

UK

Owen, D., Swift, T. and Hunt, K

2001

Questioning the Role of Stakeholder Engagement in Social and Ethical Accounting, Auditing and Reporting.

Journal of Business Ethics

UK

Perego P. and Kolk A.

2012

Multinationals’ accountability on sustainability: the evolution of third-party assurance of sustainability reports

Business Strategy and the Environment

Archival International(5

countries)

Perego P. M.

2009

Causes and consequences of choosing different assurance providers: An international study of sustainability reporting

Australian Accounting Review

Archival

International

Sierra L., Zorio A. and Garc´ia-benau M. A.

2013

Sustainable development and assurance of corporate social responsibility reports published by Ibex-35 Companies

AUDITING: A Journal of Practice & Theory.

Archival

Spain

Simnett, R. and Nugent, M. 2007 Developing an Assurance Standard for Carbon Emissions Disclosures

Corporate Social Responsibility and Environmental Management

Archival Not mentioned

Simnett, R., Nugent, M. and Huggins, A.L. 2009 Developing an International Assurance

Standard on Carbon Emissions Disclosures. International Journal of Auditing Archival International

Simnett, R., Vanstraelen, A. and Chua, W 2009 Assurance on Sustainability Reports: An

International Comparison. AUDITING: A Journal of Practice & Theory Archival International

Smith, J., Haniffa, R. and Fairbrass, J.

2010

A Conceptual Framework for Investigating ‘Capture’ in Corporate Sustainability Reporting Assurance.

Accounting and Business Research

International

Wintergreen J, Delaney T 2007 ISO 14064, International Standard for GHG Emissions Inventories and Verification. International Journal of Auditing Archival Not mentioned

Xiao, Z., Jones, M. and Lymer, A. 2002 Immediate trends in Internet reporting Managerial Auditing Journal Survey UK Zorio, A., García-Benau, M. and Sierra, L. 2012 Sustainability Development and the Quality of

Assurance Reports: Empirical Evidence. European Accounting Review Archival Spain