the accounting framework and the · pdf file2 the accounting framework and the estimates the...

TRANSCRIPT

This PDF is a selection from an out-of-print volume from the NationalBureau of Economic Research

Volume Title: The Formation and Stocks of Total Capital

Volume Author/Editor: John W. Kendrick

Volume Publisher: NBER

Volume ISBN: 0-87014-271-2

Volume URL: http://www.nber.org/books/kend76-1

Publication Date: 1976

Chapter Title: The Accounting Framework and the Estimates

Chapter Author: John W. Kendrick

Chapter URL: http://www.nber.org/chapters/c3805

Chapter pages in book: (p. 22 - 64)

2The Accounting Framework and theEstimates

The estimates of total capital formation and stocks in the United States,by sector, presented in this study were made within an economicaccounting framework. Using a systematic framework of economicaccounts ensures consistency with the national income and product andsector income and outlay estimates, and facilitates analyses of invest-ment and stocks in relation to income and product and to the compo-nents of the accounts on a similarly consistent basis. Although it doesnot eliminate errors from the estimates, it reduces the likelihood oferrors because of the double-entry nature of accounts.

Our expansion of the concepts of saving, investment, and wealthbeyond those underlying the official U.S. national income accountsnecessitated our modifying the latter to a considerable extent. Thesemodifications will be described in the first section of this chapter withreference to the set of accounts presented in the tables. The sourcesand methods underlying the capital formation and stock estimatesand price deflators relative to the Appendix B tables are summarizedin the second section.

The Accounting Framework

Our economic accounts involve three major modifications of the U.S.Department of Commerce system. First, the broad concept of invest-ment developed in Chapter 1 requires the expansion of the nationalsaving-investment account and its deconsolidation by major sector.That is, since we include nonbusiness tangible capital formation aswell as the intangible investments of all sectors, investment is no22

THE ACCOUNTING FRAMEWORK AND THE ESTIMATES 23

longer confined largely to the tangible capital formation of the businesssector. Accordingly, capital accoUnts are set up for each sector, and theincome-outlay account of each sector is limited to the current outlays,including rental values of capital used by the nonbusiness sectors butexcluding the formation of capital, which is shifted to the capitalaccounts. By including intangible and human investments in the capitalaccounts we depart from the paradigm of business accounting.Research and development financed by business is typically chargedoff as a current expense. So are the human investments, as for trainingand health. In part, this is done because—to the extent these areembodied in workers and accrue to their benefit—they do not "belong"to the firm and are removed whenever the workers decide to changejobs. But from the broader socioeconomic viewpoint, it is clear that alloutlays that expand monetary or nonmarket income over severalaccounting periods should be capitalized.

Second, the scope of the income and product accounts has to bebroadened to include not only rental values of nonbusiness capital, butalso the imputed portions of capital formation which are charged tocurrent expense or are otherwise not included in the official estimates.

Finally, the capital stock estimates of the Commerce Department,which do not yet cover all sectors and all types of capital, have beenexpanded for our purposes to include all wealth, tangible and intangi-ble, human and nonhuman, resulting from the total investments of allsectors. In order to implement financial analysis, the capital accountscould also be expanded to include flows of funds, and the wealthstatements enlarged into complete balance sheets. We do show a com-bined national balance sheet below in order to demonstrate its relation-ship to the wealth estimates. But since our emphasis is on "real" ratherthan financial analysis, we confine the capital accounts and wealthstatements to productive capital outlays and stock. But the financialflows and levels could easily be added to the capital accounts andbalance sheets, respectively, for those who wish to do so.

Our system is close to the United Nations revised standard systemof national accounts, except that we include, and they exclude, intangi-ble capital formation and stocks. And, with the same exception, it iscloser to the Federal Reserve Board's flow-of-funds accounts than it isto the Commerce Department system, although the Federal ReserveBoard does not yet include public capital formation in the capitalaccount for the governments sector.1

1. For discussions of various systems of economic accounts, see Richard andNancy Ruggles, The Design of Economic Accounts, New York, NB ER, 1970; and JohnW. Kendrick, Economic Accounts and Their Uses, New York, McGraw-Hill Book Co.,1972.

24 FORMATION AND STOCKS OF TOTAL CAPITAL

The main features of the seven basic sets of accounts are reviewedbelow, with detailed notes on the derivation of the various entries inthe tables provided in Appendix A. Contra-entries to each line in theaccounts are indicated in the tables by the table and line numbers inparentheses.

THE PRODUCTION ACCOUNT

Before looking at the sector accounts, it is useful to examine theexpanded national income and product account (Table 2-1) in order toget an overview of the adjustments made to the conventional accounts.With respect to GNP, it will be noted that the domestic investmentcomponents are much larger than in the official accounts—43.1 per centagainst 15.7 per cent in 1929, and 50.6 per cent against 16.2 per cent in1966. In large part, the greater absolute and relative size of grossinvestment was due to reclassifications of items from current consump-tion to investment. In the case of gross tangible nonhuman investment(line 31), the Commerce Department still includes only business andinstitutional investment, plus new residential construction for owner-occupancy, whereas we also include the tangible investments by thenonbusiness sectors (households and governments) in new structures,durable equipment, additions to inventories, and natural resourcedevelopment. Gross tangible human investment (line 37), the cost ofrearing children to working age, is also a deduction from the CommerceDepartment's personal consumption expenditure estimates.

Gross intangible investment (line 38) consists of outlays for educa-tion and training, health and safety, labor mobility, and research anddevelopment (lines 39—42). All of these are human investment exceptR&D, which is largely directed toward new and improved products andprocesses. We therefore classify R&D as nonhuman intangible invest-ment, although it also acts to improve the productivity of human invest-ment and capital by adding to knowledge and know-how. To the extentthat R&D and certain other investments are charged to current expenseby business, our investment estimates require an upward adjustment tothe official GNP estimates (see Table 2-la).

Net exports (line 43) are the same as in the official accounts,comprising net foreign investment and unilateral transfer payments.

Both personal and government consumption (lines 29 and 30)begin with the official estimates, less the categories reclassified asinvestment, plus imputed rental values of the services provided by thetangible nonhuman capital stocks owned by each of the two nonbusi-ness sectors. The adjusted consumption estimates are below the official

THE ACCOUNTING FRAMEWORK AND THE ESTIMATES 25

U.S. estimates to the extent that the imputed rentals are less than thetangible capital outlays of each sector, and because of the deduction ofthe intangible capital outlays. But GNP and gross national income areenlarged by the imputed rental values which are not now includedexcept for owner-occupied residences. As shown in the reconciliationtable (2-la), the aggregate estimates are also larger to the extent offoregone earnings of students and of the frictionally unemployed,which are counted as part of intangible investments in education and inlabor mobility, respectively.

As a result of the various additions, our adjusted GNP estimates are23.5 per cent higher than the official estimates for 1929, and 34.3 percent higher for 1969. (See Table 2-la and Chart 2-1.) Note, however, thatthe adjustments were made purely for the sake of consistency with theexpanded investment and capital estimates. In another project we haveimputed values for all nonmarket production (indicated by parentheti-cal stub entries in the sector accounts). Other investigators have madefurther adjustments in an attempt to provide a still closer approximationto NEW (net economic welfare), as Samuelson has dubbed it in thelatest edition of his textbook.2 That was not our objective in making theadjustments shown in Table 2-la, although these items make a modestcontribution to broader welfare-oriented measures.

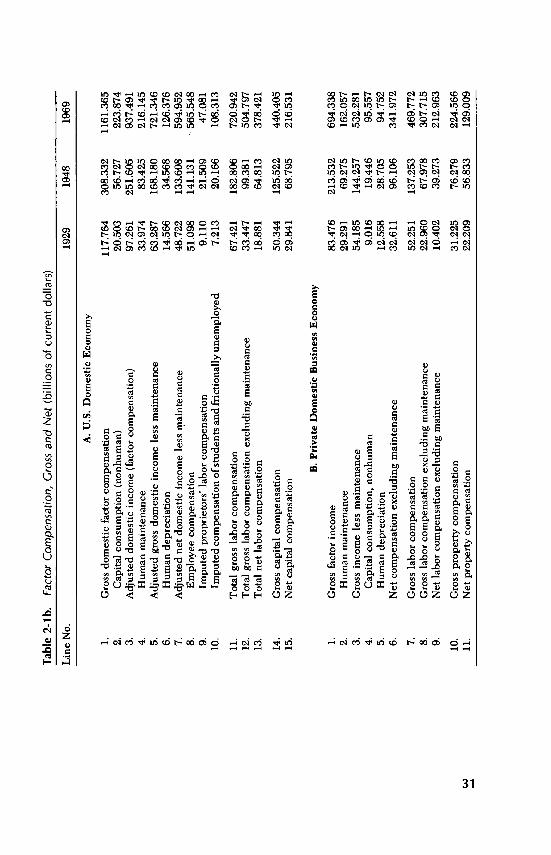

Turning to the debit side of the production account, which com-prises factor costs (national income) and other charges against product,adjustments were made for the additions to product just noted. Thus,labor compensation is increased by the imputed value of nonmarketservices involved in eduation and mobility (line 7), and net rentalincome includes the net rental value of household tangible wealth (line10) and of public sector wealth (line 12). We have also imputed thelabor value of proprietors' work (line 6) on the basis of the averagewage-salary of employees in the various industries, in order to isolatethe profit portion of proprietors' net income to be included with corpo-rate profits (line 11). This is necessary in order to estimate returns onhuman and nonhuman capital separately, as shown in Table 2-lb. Netinterest was modified by deducting from the official estimates con-sumer interest on brokerage loans and the excess of interest paid by thefederal government over and above the net rental value of that sector'sreal wealth. (See Appendix A for a more detailed discussion.)

It should be noted that we have not imputed a rental income for thehuman capital stock, tangible and intangible, since our view is that thelabor compensation estimates already represent the return on total

2. See William Nordhaus and James Tobin, "Is Growth Obsolete?," EconomicGrowth, Fiftieth Anniversary Colloquium V, New York, NBER, 1972.

Tab

le 2

-1.

Nat

iona

l Inc

ome

and

Pro

duct

Acc

ount

(bi

llion

s of

cur

rent

dol

lars

)

Lin

e N

o.19

2919

4819

66

DE

BIT

S

1.L

abor

com

pens

atio

n67

.42

182.

8154

7.58

2.W

age

and

sala

ry d

isbu

rsem

ents

(II

A-1

3)50

.44

135.

3439

4.50

3.W

age

accr

uals

less

dis

burs

emen

ts (

IIB

-73)

0.00

0.04

0.00

4.E

mpl

oyer

con

trib

utio

ns f

or s

ocia

l ins

uran

ce (

IVA

-19)

0.10

3.04

20.2

95.

Oth

er la

bor

inco

me

(IIA

-14)

0.56

2.71

20.7

16.

Impu

ted

labo

r co

mpe

nsat

ion

of p

ropi

etor

s (I

IA-1

5)9.

1121

.51

38.8

67.

Add

ition

al la

bor

com

pens

atio

n im

puta

tions

(II

A-1

6)7.

2120

.17

73.2

2

8.N

et r

enta

l inc

ome

of p

erso

ns a

nd in

stitu

tions

6.96

9.80

28.1

3

9.Fr

om a

uxili

ary

busi

ness

act

iviti

es (

lilA

-b)

3.08

5.36

8.72

10.

From

ow

ner-

used

cap

ital (

IIA

-22)

3.88

4.44

19.4

1

11.

Prof

its o

f bu

sine

ss e

nter

pris

es (

lilA

-li)

16.3

051

.95

116.

52

12.

Net

ren

tal i

ncom

e of

gov

ernm

ent (

IVA

-20)

0.78

1.95

6.17

13.

Net

inte

rest

6.61

6.07

45.7

9

14.

Pers

onal

inte

rest

inco

me

(IIA

-28)

7.22

7.88

43.6

415

.L

ess:

Unp

rodu

ctiv

e in

tere

st p

aid

by c

onsu

mer

s (h

A-l

i)0.

950.

030.

1916

.G

over

nmen

t int

eres

t inc

ome

(IV

A-2

1)0.

521.

364.

1517

.L

ess:

Unp

rodu

ctiv

e in

tere

st p

aid

by g

over

nmen

t (IV

A-1

1)0.

183.

141.

81

NA

TIO

NA

L I

NC

OM

E98

.07

252.

5874

4.19

18.

Les

s: H

uman

cap

ital c

onsu

mpt

ion

(IIA

-33)

14.5

734

.57

101.

15

NE

T N

AT

ION

AL

IN

CO

ME

83.5

021

8.01

643.

04

19.

Cap

ital c

onsu

mpt

ion

allo

wan

ces

35.0

791

.30

272.

57

20.

Pers

onal

(II

B-5

7)24

.33

54.5

316

9.44

21.

Non

hum

an9.

7719

.97

68.2

922

.H

uman

14.5

734

.57

101.

1523

.B

usin

ess

(III

B-3

8)9.

0219

.45

71.2

624

.G

over

nmen

t (IV

B-4

1)1.

7217

.32

31.8

7

GR

OSS

NA

TIO

NA

L I

NC

OM

E11

8.57

309.

3191

5.61

25.

Cur

rent

bus

ines

s tr

ansf

er p

aym

ents

(II

A-3

0)0.

590.

702.

99

26.

Indi

rect

tax

and

nont

ax c

harg

es (

IVA

-16)

7.34

20.5

167

.60

27.

Les

s: S

ubsi

dies

less

cur

rent

sur

plus

of

gove

rnm

ent

—0.

140.

862.

62en

terp

rise

s (I

VA

-12)

28.

Stat

istic

al d

iscr

epan

cy (

VI-

18)

0.70

—1.

99—

1.01

CH

AR

GE

S A

GA

INST

GR

OSS

NA

TIO

NA

L12

7.34

327.

6798

2.57

PRO

DU

CT

(con

tinue

d)

Tab

le 2

-1.

Nat

iona

l Inc

ome

and

Pro

duct

Acc

ount

of c

urre

nt d

olla

rs)

(con

dude

d)

Lin

e N

o.19

2919

4819

66

CR

ED

ITS

29.

Pers

onal

con

sum

ptio

n (I

IA-2

)64

.84

146.

0438

1.57

30.

Gov

ernm

ent c

onsu

mpt

ion

(IV

A-1

)6.

4335

.30

98.4

8

31.

Gro

ss ta

ngib

le n

onhu

man

inve

stm

ent (

VT

-i)

29.4

776

.63

244.

3632

.St

ruct

ures

11.4

827

.80

78.2

733

.Pr

ivat

e re

side

ntia

l3.

9514

.44

25.0

434

.O

ther

7.53

13.3

653

.23

35.

Dur

able

goo

ds15

.46

43.8

014

4.02

36.

Cha

nge

in in

vent

orie

s2.

535.

0322

.07

37.

Gro

ss ta

ngib

le h

uman

inve

stm

ent (

VI-

2)9.

7718

.28

54.6

2

38.

Gro

ss in

tang

ible

inve

stm

ent (

VI-

3)15

.69

44.9

819

8.26

39.

Edu

catio

n an

d tr

aini

ng11

.00

30.7

813

6.60

40.

Hea

lth1.

905.

2221

.47

41.

Mob

ility

2.53

6.61

17.4

142

.R

esea

rch

and

deve

lopm

ent

0.25

2.37

22.7

7

43.

Net

exp

orts

of

good

s an

d se

rvic

es1.

156.

445.

2844

.E

xpor

ts (

VA

-i)

7.03

16.7

943

.36

45.

Les

s: I

mpo

rts

(VA

-2)

5.89

10.3

538

.08

GR

OSS

NA

TIO

NA

L P

RO

DU

CT

127.

3432

7.67

982.

57

NO

TE

: Det

ail m

ay n

ot a

dd to

tota

ls d

ue to

rou

ndin

g.

Tab

le 2

-la.

Rec

onci

liatio

n of

Adj

uste

d G

NP

and

Com

mer

ce D

epar

tmen

t CN

P, 1

929,

194

8, a

nd 1

969

(bill

ions

of c

urre

nt d

olla

rs)

Lin

e N

o.19

2919

4819

69

1.G

NP,

Com

mer

ce c

once

pt10

3,09

525

7.56

292

9.09

5

Plus

Hou

seho

lds

and

inst

itutio

ns:

2.Im

pute

d st

uden

t com

pens

atio

n (l

ess

unem

ploy

men

t adj

ustm

ent)

5.14

115

.660

92.2

653.

Impu

ted

com

pens

atio

n of

fri

ctio

nally

une

mpl

oyed

2.07

24.

506

16.0

48(l

ess

subs

idie

s)4.

Impu

ted

rent

als

(exc

l. m

aint

enan

ce a

nd in

sura

nce)

on

10.4

0520

.499

100.

057

HH

dur

able

s an

d in

vent

orie

s5.

Impu

ted

rent

als

(exc

l. m

aint

enan

ce)

on in

stitu

tiona

l0.

337

0.54

45.

711

plan

t and

equ

ipm

ent a

nd la

nd, o

ver

OB

E d

epre

ciat

ion

and

inte

rest

pai

d

Bus

ines

s:6.

Tan

gibl

e in

vest

men

t con

vent

iona

lly c

harg

ed to

cur

rent

acc

ount

0.28

20.

899

2.34

07.

Inta

ngib

le in

vest

men

t con

vent

iona

lly c

harg

ed to

cur

rent

2.18

76.

953

35.3

87ac

coun

t

Gen

eral

gov

ernm

ent:

8.Im

pute

d re

ntal

s (e

xci.

mai

nten

ance

) on

land

, dur

able

s, a

nd3.

825

21.0

4866

.967

inve

ntor

ies

9.E

qual

s: G

NP,

adj

uste

d12

7.34

432

7.67

11,

247.

870

10.

Rat

io: A

djus

ted

to C

omm

erce

GN

P1.

235

1.27

21.

343

30 THE FORMATION AND STOCKS OF TOTAL CAPITAL

Chart 2-1. Relation of Adjusted to Official GNP Estimates, 1966

Billion dollars1,000

600

500

Equals:

Net exports

Investment, intangible

Investment, tangible

400

300

200

100

0

human capital employed.asymmetrIcal, however, in

Consumption, government

Consumption, personal

sumption allowances, while labor income is gross of human capitalconsumption. Accordingly, in line 18 we deduct human capital con-sumption allowances to arrive at "net national income" estimateswhich are symmetrical in that respect. The allowances represent thatportion of gross income which, from a theoretical social accountingviewpoint, must be invested in human capital in order to maintain itsproductive capacity intact.

Plus:

Business investment chargedto current expense

Imputed nonmarketlabor services

Imputed rentals

900

800

700

Tangible — — — —IntangibleFrictional unemployed

Student compensation

Government

Institution

Household

Government

Net exports

G .P. D. I.

Consumption

G N P Adjusted(USOC) G N P

The official national income estimatesthat property income is net of capital con-

are

Tab

le 2

-lb.

Fac

tor

Com

pens

atio

n, G

ross

and

Net

(bi

llion

s of

cur

rent

dol

lars

)

Line

No.

1929

1948

1969

A. U

.S. D

omes

tic E

cono

my

1,G

ross

dom

estic

fac

tor

com

pens

atio

n11

7.76

430

8.33

211

61.3

652.

Cap

ital c

onsu

mpt

ion

(non

hum

an)

20.5

0356

.727

223.

874

3.A

djus

ted

dom

estic

inco

me

(fac

tor

com

pens

atio

n)97

.261

251.

605

937.

491

4.H

uman

mai

nten

ance

33.9

7483

.425

216.

145

5.A

djus

ted

gros

s do

mes

tic in

com

e le

ss m

aint

enan

ce63

,287

168.

180

721.

346

6.H

uman

dep

reci

atio

n14

.566

34.5

6812

6.37

67.

Adj

uste

d ne

t dom

estic

inco

me

less

mai

nten

ance

48.7

2213

3.60

859

4.95

28.

Em

ploy

ee c

ompe

nsat

ion

51.0

9814

1.13

156

5.54

89.

Impu

ted

prop

riet

ors'

labo

r co

mpe

nsat

ion

9.11

021

.509

47.0

8110

.Im

pute

d co

mpe

nsat

ion

of s

tude

nts

and

fric

tiona

lly u

nem

ploy

ed7.

213

20. 1

6610

8.31

3

11.

Tot

al g

ross

labo

r co

mpe

nsat

ion

67.4

2118

2.80

672

0.94

212

.T

otal

gro

ss la

bor

com

pens

atio

n ex

clud

ing

mai

nten

ance

33.4

4799

.381

504.

797

13.

Tot

al n

et la

bor

com

pens

atio

n18

,881

64.8

1337

8.42

1

14.

Gro

ss c

apita

l com

pens

atio

n50

.344

125.

522

440.

405

15.

Net

cap

ital c

ompe

nsat

ion

29.8

4168

.795

216.

531

B. P

riva

te D

omes

tic B

usin

ess

Eco

nom

y

1.G

ross

fac

tor

inco

me

83.4

7621

3.53

269

4.33

82.

Hum

an m

aint

enan

ce29

.291

69.2

7516

2.05

73.

Gro

ss in

com

e le

ss m

aint

enan

ce54

.185

144.

257

532.

281

4.C

apita

l con

sum

ptio

n, n

onhu

man

9.01

619

.446

95.5

575.

Hum

an d

epre

ciat

ion

12.5

5828

.705

94.7

526.

Net

com

pens

atio

n ex

clud

ing

mai

nten

ance

32.6

1196

. 106

341.

972

7.G

ross

labo

r co

mpe

nsat

ion

52.2

5113

7.25

346

9.77

28.

Gro

ss la

bor

com

pens

atio

n ex

clud

ing

mai

nten

ance

22.9

6067

.978

307.

715

9.N

et la

bor

com

pens

atio

n ex

clud

ing

mai

nten

ance

10.4

0239

.273

212.

963

10.

Gro

ss p

rope

rty

com

pens

atio

n31

.225

76.2

7922

4.56

611

.N

et p

rope

rty

com

pens

atio

n22

.209

56.8

3312

9.00

9

32 THE FORMATION AND STOCKS OF TOTAL CAPITAL

It could be argued that even our net national income estimates areasymmetrical, since property income is considered net of maintenanceexpenditures while labor income is not. Most, but not all, economistsbelieve that, since the portion of current consumption representingmaintenance affords satisfaction, no deduction should be made if awelfare criterion is observed. We have followed this line in Table 2-1,recognizing a possible inconsistency with our treatment of humancapital consumption, although it can be argued that the current utilityportion of human investment is negligible in relation to the flow ofincome, psychic as well as monetary, deriving from human capitalcreation over future accounting periods. We do estimate maintenanceoutlays, as shown in Table 2-ib, as a basis for estimating rates of returnon human and nonhuman capital in a consistent manner, as discussedin the final section of this volume.

Once deducted, human capital consumption can be neatly com-bined with nonhuman capital consumption (line 19) and added to netnational income to obtain gross national income. Then the usual recon-ciliation items, chiefly indirect business taxes less subsidies, can beadded to arrive at total charges against GNP at market prices.

THE SECTOR ACCOUNTS, CURRENT AND CAPITAL

The basic design of sector accounts is well known. (See Tables 2-2through 2-5.) On the credit side, "primary" income flows from currentproduction plus transfer payments received (including tax revenues)are entered. To the official U.S. estimates we have added, in theappropriate sector accounts, the rental values of capital goods owned bythe household and government sectors, the imputed values of nonmar-ket time spent by persons on investment-in-self, and the several lesseritems discussed earlier. Note that we follow the Commerce Depart-ment in crediting total proprietors' profits to the personal sector, sincethere is no basis for estimating the proportion retained for investmentin unincorporated firms. Also, human capital consumption is deductedfrom personal income to arrive at "net personal income," so that per-sonal saving will be net of human as well as of nonhuman depreciationallowances.

In the business sector account (which the Commerce Departmentdoes not explicitly develop), we credit profits (before taxes) after thevarious valuation adjustments. Our foreign sector account is the same asthat of the Commerce Department.

On the debit side of the current accounts, both personal andgovernment consumption estimates are adjusted as described earlier; to

THE ACCOUNTING FRAMEWORK AND THE ESTIMATES 33

these are added transfer payments (including tax and nontax paymentsin the case of the personal sector) and "unproductive interest" pay-ments. In using the term "government consumption" we follow U.N.usage, and include noninvestment purchases presumably designed toproduce services for collective consumption. In the business sector, thedebits are for dividends, entrepreneurial withdrawals, and corporate taxliabilities. In all sectors, net saving is the balancing item obtained as theresidual after subtracting the various debits just described from the netsector incomes.

in the sector capital accounts, net saving becomes the initial credititem as a source of funds. Since the capital accounts are gross, in orderto explain the sources of funds to finance gross investment, capitalconsumption allowances—tangible and intangible—are credited to thesector accounts from the gross production account.

The final category of credits, intersectoral net capital transfers,requires some explanation. Whereas initial new investment is entered'according to the sector that finances it, we wish to show capital accumu-lation and stocks by the sector that controls and reaps the primarybenefit from the capital. Thus, we posit that the personal sector controlsall human capital, so the intangible human investments financed bybusiness and governments are transferred to the personal sector. Trans-fers are not necessary for rearing costs, which are both incurred by andaccrue to the benefit of households. We also posit that applied R&Daccrues to the benefit of the business sector, so nonbusiness R&D istransferred to business. Net capital transfers from abroad represent thechange in net human stock, calculated by age groups and adjusted foraccumulated depreciation, resulting from net immigration (immigrationless emigration). To simplify the estimation procedure, we assume thatimmigrants represent the same amounts of capital, in dollars, as personsof the same age groups already in the United States.

In this treatment, we have adopted the approach of the revisedSNA, although the capital transfers provided for there are intended tobe primarily financial. As a result of the productive capital transfers,sector stock estimates relate to the capital controlled, and it is on thisbasis that depreciation is estimated.

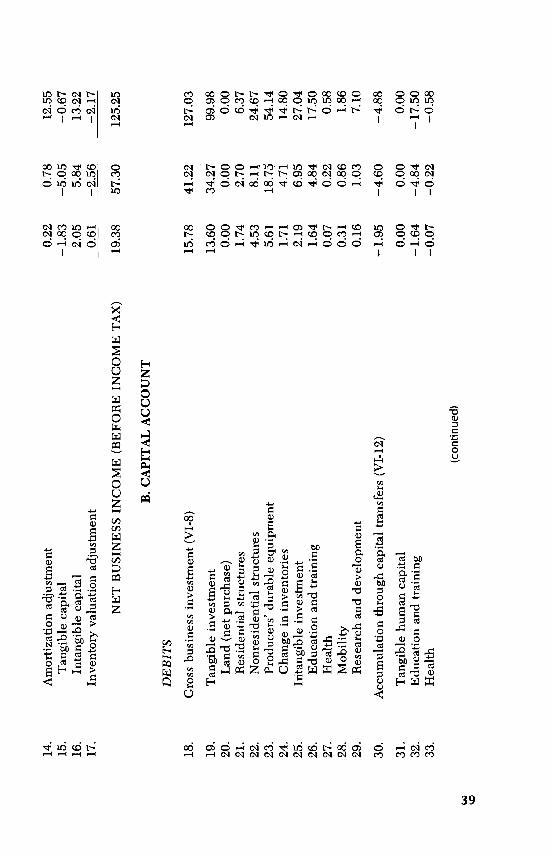

On the debit side of the domestic sector capital accounts, there arethree chief groupings of entries. First comes the productive tangibleand intangible investment financed, by type. Next, the capital accumu-lation from net capital transfers is detailed by type rather than by sectorof origin (as on the credit side). The third category, "net financialinvestment," is the balancing item in the capital accounts as the differ-ence between total credits and the sum of the other debits. If the capitalaccount were elaborated to show financial transactions, it would repre-

Tab

le 2

-2.

Per

sona

l Sec

tor

Acc

ount

s (b

illio

ns o

f cur

rent

dol

lars

)

Lirt

eNo.

1929

1948

1966

A. C

UR

RE

NT

AC

CO

UN

T (

Cas

h B

asis

)

DE

BIT

S1.

Pers

onal

tax

and

nont

ax p

aym

ents

(IV

A-1

4)2.

3120

.64

73.4

1

2.Pe

rson

al c

onsu

mpt

ion

(1-2

9)64

.84

146.

0438

1.57

3.Im

pute

d re

ntal

s fo

r se

rvic

es o

f ca

pita

l18

.47

35.3

013

8.41

4.O

wne

r-oc

cupi

ed r

esid

ence

s6.

4110

.80

46.2

85.

Inst

itutio

nal p

lant

0.41

0.75

5.50

6.C

onsu

mer

dur

able

goo

ds a

nd in

vent

orie

s11

.38

23.5

485

.65

7.In

stitu

tiona

l equ

ipm

ent

0.26

0.20

0.99

8.L

ess:

Im

pute

d re

ntal

s al

loca

ted

to in

tang

ible

and

hum

an in

vest

men

t2.

845.

4322

.75

(Con

sum

ptio

n pr

ovid

ed b

y bu

sine

ss to

em

ploy

ees)

(Cur

rent

con

sum

ptio

n tr

ansf

ers

from

bus

ines

s to

gene

ral p

ublic

)

9.O

ther

con

sum

ptio

n ex

pend

iture

s49

.22

116.

1826

5.91

10.

Pers

onal

tran

sfer

pay

men

ts to

res

t of

wor

ld (

net)

(V

A-3

)0.

340.

700.

56

11.

Unp

rodu

ctiv

e in

tere

st p

aid

by c

onsu

mer

s (1

-15)

0.95

0.03

0.19

12.

Net

per

sona

l sav

ings

(II

B-5

6)11

.12

30.0

711

1.22

DIS

POSA

L O

F N

ET

PE

RSO

NA

L I

NC

OM

E79

.56

197.

4856

6.95

CR

ED

iTS

13.

Wag

es a

nd s

alar

y di

sbur

sem

ents

(1-

2)50

.44

135.

3439

4.50

14.

Oth

er la

bor

inco

me

(1-5

)0.

562.

7120

.71

15.

Impu

ted

labo

r co

mpe

nsat

ion

of p

ropr

ieto

rs (

1-6)

16.

Add

ition

al la

bor

com

pens

atio

n im

puta

tions

(1-

7)

17.

Stud

ents

18.

Fric

tiona

lly u

nem

ploy

ed(H

ouse

hold

mem

bers

)(V

olun

teer

s)(E

mpl

oyee

s fo

r bu

sine

ss p

rovi

ded

cons

umpt

ion)

19.

With

draw

als

of p

ropr

ieto

rs' p

rofi

ts (

IIIA

-2)

20.

Net

ren

tal i

ncom

e

21.

From

aux

iliar

y bu

sine

ss a

ctiv

ities

(lil

A-i

)22

.Fr

om o

wne

r-us

ed c

apita

l (1-

10)

23.

Res

iden

ces

24.

Inst

itutio

nal p

lant

25.

Con

sum

er d

urab

le g

oods

and

inve

ntor

ies

26.

Inst

itutio

nal e

quip

men

t

27.

Div

iden

ds (

IIIA

-4)

28.

Pers

onal

inte

rest

inco

me

(1-1

4)

29.

Cur

rent

tran

sfer

s to

per

sons

30.

From

bus

ines

s (1

-25)

(Cas

h)(C

onsu

mpt

ion

prov

ided

to g

ener

al p

ublic

131

.Fr

om g

over

nmen

t (IV

A-9

)

32.

Les

s: P

erso

nal c

ontr

ibut

ions

for

soc

ial i

nsur

ance

(IV

A-1

8)

PER

SON

AL

IN

CO

ME

(con

tinue

d)

9.11

21.5

138

.86

7.21

20.1

773

.22

5.14

15.6

660

.89

2.07

4.51

12.3

4

5.47

18.5

421

.92

6.96

9.80

28.1

3

3.08

5.36

8.72

3.88

4.44

19.4

12.

130.

988.

330.

110.

272.

821.

613.

188.

060.

020.

020.

20

5.80

7.04

20.8

0

7.22

7.88

43.6

4

1.50

11.2

444

.06

0.59

0.70

2.99

0.91

10.5

441

.08

0.14

2.18

17.7

4

94.1

323

2.05

668.

10U

i

Tab

le 2

-2.

Per

sona

! Sec

tor

Acc

ount

s (b

illio

ns o

f cur

rent

dol

lars

) (c

ompl

eted

)

Line

No.

1929

1948

1966

33.

Les

s: H

uman

cap

ital c

onsu

mpt

ion

(1-1

8)14

.57

34.5

710

1.15

NE

T P

ER

SON

AL

IN

CO

ME

79.5

619

7.48

566.

95

B. C

API

TA

L A

CC

OU

NT

(A

ccru

al B

asis

)

DE

BiT

S

34.

Gro

ss p

erso

nal i

nves

tmen

t (V

I-7)

33.2

681

.20

260.

38

35.

Tan

gibl

e no

nhum

an in

vest

men

t12

.95

34.1

499

.41

36.

Lan

d (n

et p

urch

ase)

0.01

—0.

17—

1.63

37.

Res

iden

tial s

truc

ture

s2.

2111

.74

18.6

738

.In

stitu

tiona

l pla

nt0.

430.

713.

8239

.C

onsu

mer

dur

able

goo

ds9.

2122

.68

70.7

540

.In

stitu

tiona

l equ

ipm

ent

0.27

0.20

0.80

41.

Cha

nge

in h

ouse

hold

inve

ntor

ies

0.82

—1.

027.

0042

.T

angi

ble

hum

an in

vest

men

t9.

7718

.28

54.6

243

.In

tang

ible

inve

stm

ent

10.5

428

.78

106.

3544

.E

duca

tion

and

trai

ning

6.85

19.3

775

.29

45.

Hea

lth1.

473.

8215

.37

46.

Mob

ility

2.20

5.55

14.8

347

.R

esea

rch

and

deve

lopm

ent

0.02

0.04

0.86

48.

Acc

umul

atio

n th

roug

h ca

pita

l tra

nsfe

rs (

VI-

il)5.

8515

.10

75.2

2

49.

Tan

gibl

e no

nhum

an c

apita

l0.

000.

000.

0050

.T

angi

ble

hum

an c

apita

l0.

470.

511.

6851

.E

duca

tion

and

trai

ning

4.59

12.1

064

.84

52.

Hea

lth0.

461.

446.

38

53.

Mob

ility

0.33

1.06

2.58

54.

Res

earc

h an

d de

velo

pmen

t—

0.00

—0.

01—

0.25

55.

Net

fin

anci

al in

vest

men

t (V

I-15

)2.

193.

4420

.28

GR

OSS

AC

CU

MU

LA

TIO

N41

.30

99.7

435

5.88

CR

ED

iTS

56.

Net

per

sona

l sav

ing

(IIA

-12)

11.1

230

.07

111.

22

57.

Pers

onal

cap

ital c

onsu

mpt

ion

allo

wan

ces

(1-2

0)24

.33

54.5

316

9.44

58.

Tan

gibl

e no

nhum

an c

apita

l9.

7719

.97

68.2

959

.R

esid

entia

l str

uctu

res

1.51

4.10

11.7

460

.In

stitu

tiona

l pla

nt0.

170.

331.

6961

.C

onsu

mer

dur

able

goo

ds7.

8715

.39

54.2

062

.In

stitu

tiona

l equ

ipm

ent

0.21

0.15

0.65

63.

Tan

gibl

e hu

man

cap

ital

5.10

9.84

17.4

264

.In

tang

ible

cap

ital

9.46

24.7

383

.73

65.

Edu

catio

n an

d tr

aini

ng5.

2815

.55

54.6

766

.H

ealth

1.21

3.16

13.2

667

.M

obili

ty2.

986.

0215

.80

68.

Net

cap

ital t

rans

fers

5.85

15.1

075

.22

69.

Cap

ital t

rans

fers

fro

m b

usin

ess

(III

B-4

8)2.

025.

9219

.94

70.

Cap

ital t

rans

fers

fro

m g

over

nmen

t (IV

B-4

6)2.

907.

9450

.05

71.

Cap

ital t

rans

fers

fro

m r

est o

f w

orld

(V

B-8

)0.

931.

255.

4872

.L

ess:

Cap

ital t

rans

fers

to b

usin

ess

(III

B-4

5)0.

000.

010.

25

73.

Wag

e ac

crua

ls le

ss d

isbu

rsem

ents

(1-

3)0.

040.

00

FIN

AN

CE

OF

GR

OSS

AC

CU

MU

LA

TIO

N41

.30

99.7

435

5.88

Tab

le 2

-3.

Bus

ines

s S

ecto

r A

ccou

nts

(bill

ions

of c

urre

nt d

olla

rs)

Lin

e N

o.19

2919

4819

66

A. C

UR

RE

NT

AC

CO

UN

T

DE

BIT

S

1.W

ithdr

awal

s of

net

ren

tal i

ncom

e fr

om a

uxili

ary

busi

ness

3.08

5.36

8.72

activ

ities

(II

A-2

1)

2.W

ithdr

awal

s of

pro

prie

tors

' pro

fits

(II

A-1

9)5.

4718

.54

21.9

2

3.C

orpo

rate

pro

fits

tax

liabi

lity

(IV

A-1

5)1.

3712

.52

34.2

8

4.D

ivid

ends

(II

A-2

7)5.

807.

0420

.80

5.N

et b

usin

ess

savi

ng (

IIIB

-37)

3.66

13.8

639

.52

6.U

ninc

orpo

rate

d bu

sine

ss n

onw

ithdr

awn

prof

its b

efor

eN

AN

AN

Aad

just

men

t7.

Cor

pora

te u

ndis

trib

uted

pro

fits

bef

ore

adju

stm

ent

2.82

15.6

329

.15

8.A

mor

tizat

ion

adju

stm

ent

0.22

0.78

12.5

59.

Inve

ntor

y va

luat

ion

adju

stm

ent

0A31

2.56

2.17

DIS

POSA

L O

F N

ET

BU

SIN

ESS

IN

CO

ME

19.3

857

.30

125.

25

CR

ED

ITS

10.

Net

ren

tal f

rom

aux

iliar

y bu

sine

ss a

ctiv

ities

(1-

9)3.

085.

368.

72

11.

Prof

its o

f bu

sine

ss e

nter

pris

es (

I-li)

16.3

051

.95

116.

52

12.

Uni

ncor

pora

ted

busi

ness

pro

fits

bef

ore

adju

stm

ent

5.47

18.5

421

.92

13.

Cor

pora

te p

rofi

ts b

efor

e ad

just

men

t9.

9935

.19

84.2

2

DE

BIT

S

18.

Gro

ss b

usin

ess

inve

stm

ent (

VI-

8)

Tan

gibl

e in

vest

men

tL

and

(net

pur

chas

e)R

esid

entia

l str

uctu

res

Non

resi

dent

ial s

truc

ture

sPr

oduc

ers'

dur

able

equ

ipm

ent

Cha

nge

in in

vent

orie

sIn

tang

ible

inve

stm

ent

Edu

catio

n an

d tr

aini

ngH

ealth

Mob

ility

Res

earc

h an

d de

velo

pmen

t

30.

Acc

umul

atio

n th

roug

h ca

pita

l tra

nsfe

rs (

VI-

12)

31.

Tan

gibl

e hu

man

cap

ital

32.

Edu

catio

n an

d tr

aini

ng33

,H

ealth

2.19

6.95

1.64

4.84

0.07

0.22

0.31

0.86

0.16

1.03

—1.

95—

4.60

—4.

88

0.00

0.00

0.00

—1.

64—

4.84

—17

.50

—0.

07—

0.22

—0.

58

14.

Am

ortiz

atio

n ad

just

men

t15

.T

angi

ble

capi

tal

16.

Inta

ngib

le c

apita

l17

.In

vent

ory

valu

atio

n ad

just

men

t

NE

T B

USI

NE

SS I

NC

OM

E (

BE

FOR

E I

NC

OM

E T

AX

)

B. C

API

TA

L A

CC

OU

NT

0.22

0.78

—1.

83—

5.05

2.05

5.84

0.61

—2.

56

12.5

5—

0.67

13.2

2—

2.17

19.

20.

21.

22.

23.

24.

25.

26.

27.

28.

29.

19.3

857

.30

125.

25

15.7

841

.22

127.

03

13.6

034

.27

0.00

0.00

1.74

2.70

4.53

8.11

5.61

1.71

4.71

99.9

80.

006.

3724

.67

54.1

414

.80

27.0

417

.50

0.58

1.86

7.10

(con

tinue

d)

CT

able

2-3

.B

usin

ess

Sec

tor

Acc

ount

s (b

illio

ns o

f cur

rent

dol

lars

) (c

ompl

eted

)

Lin

e N

o.19

2919

4819

66

34.

Mob

ility

—0.

31—

0.86

—1.

86

35.

Res

earc

h an

d de

velo

pmen

t0.

071.

3215

.07

36.

Net

fin

anci

al in

vest

men

t (V

I-16

)—

3.11

—7.

92—

16.2

4

GR

OSS

AC

CU

MU

LA

TIO

N10

.72

28.7

010

5.91

CR

ED

ITS

37.

Net

bus

ines

s sa

ving

(II

IA-5

)3.

6613

.86

39.5

2

38.

Bus

ines

s ca

pita

l con

sum

ptio

n al

low

ance

s (1

-23)

9.02

19.4

571

.26

39.

Tan

gibl

e ca

pita

l8.

8818

.33

57.4

440

.R

esid

entia

l str

uctu

res

1.11

1.59

3.89

41.

Non

resi

dent

ial s

truc

ture

s3.

055.

2114

.76

42.

Prod

ucer

s' d

urab

le e

quip

men

t4.

7211

.53

38.7

943

.In

tang

ible

cap

ital,

rese

arch

and

dev

elop

men

t0.

141.

1213

.82

44.

Net

cap

ital t

rans

fers

—1.

95—

4.60

—4.

88

45.

Cap

ital t

rans

fers

fro

m p

erso

ns a

nd in

stitu

tions

(II

B-7

2)0.

000.

010.

2546

.C

apita

l tra

nsfe

rs f

rom

gov

ernm

ent (

IVB

-47)

0.07

1.31

14.8

147

.C

apita

l tra

nsfe

rs f

rom

res

t of

wor

ld (

VB

-9)

0.00

0.00

0.00

48.

Les

s: C

apita

l tra

nsfe

rs to

per

sons

(II

B-6

9)—

2.02

—5.

92—

19.9

4

FIN

AN

CE

OF

GR

OSS

AC

CU

MU

LA

TIO

N10

.72

28.7

010

5.91

Tab

le 2

-4.

Gov

ernm

ent S

ecto

r A

ccou

nts

(bill

ions

of c

urre

nt d

olla

rs)

Lin

e N

o.19

2919

4819

66

A. C

UR

RE

NT

AC

CO

UN

T

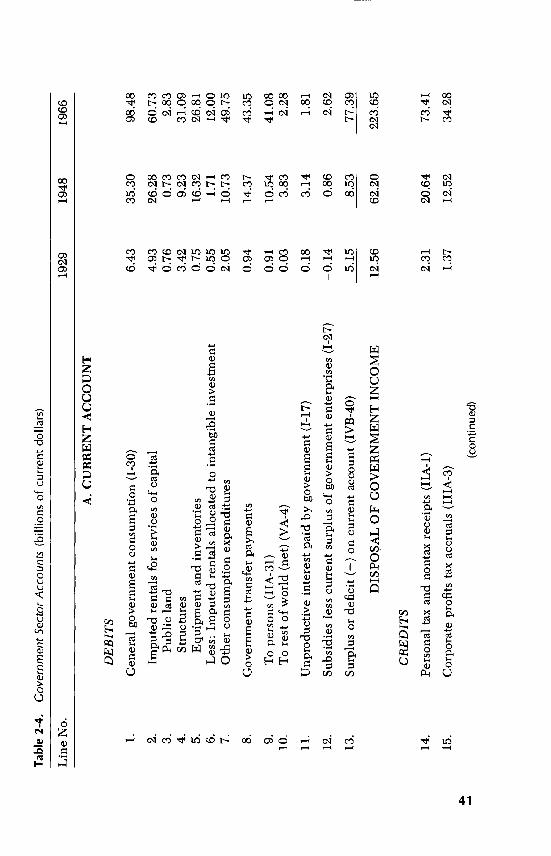

DE

BiT

S

1.G

ener

al g

over

nmen

t con

sum

ptio

n (1

-30)

6.43

35.3

098

.48

2.Im

pute

d re

ntal

s fo

r se

rvic

es o

f ca

pita

l4.

9326

.28

60.7

33.

Publ

ic la

nd0.

760.

732.

834.

Stru

ctur

es3.

429.

2331

.09

5.E

quip

men

t and

inve

ntor

ies

0.75

16.3

226

.81

6.L

ess:

Im

pute

d re

ntal

s al

loca

ted

to in

tang

ible

inve

stm

ent

0.55

1.71

12.0

07.

Oth

er c

onsu

mpt

ion

expe

nditu

res

2.05

10.7

349

.75

8.G

over

nmen

t tra

nsfe

r pa

ymen

ts0.

9414

.37

43.3

5

9.T

o pe

rson

s (H

A-3

1)0.

9110

.54

41.0

810

.T

o re

st o

f w

orld

(ne

t) (

VA

-4)

0.03

3.83

2.28

11.

Unp

rodu

ctiv

e in

tere

st p

aid

by g

over

nmen

t (1-

17)

0.18

3.14

1.81

12.

Subs

idie

s le

ss c

urre

nt s

urpl

us o

f go

vern

men

t ent

erpr

ises

(1-

27)

—0.

140.

862.

62

13.

Surp

lus

or d

efic

it (—

)on

curr

ent a

ccou

nt (

IVB

-40)

5.15

8.53

77.3

9

DIS

POSA

L O

F G

OV

ER

NM

EN

T I

NC

OM

E12

.56

62.2

022

3.65

CR

ED

ITS

14.

Pers

onal

tax

and

nont

ax r

ecei

pts

(hA

-i)

2.31

20.6

473

.41

15.

Cor

pora

te p

rofi

ts ta

x ac

crua

ls (

IIIA

-3)

1.37

12.5

234

.28

(con

tinue

d)

Tab

le 2

-4.

Gov

ernm

ent S

ecto

r A

ccou

nts

(bill

ions

of c

urre

nt d

olla

rs)

(com

plet

ed)

Lin

e N

o.19

2919

4819

66

16.

Indi

rect

tax

and

nont

ax c

harg

es (

1-26

)7.

3420

.51

67.6

0

17.

Con

trib

utio

ns f

or s

ocia

l ins

uran

ce0.

245.

2238

.04

18.

Pers

onal

(II

A-3

2)0.

142.

1817

.74

19.

Em

ploy

er (

1-4)

0.10

3.04

20.2

9

20.

Net

ren

tal i

ncom

e of

gov

ernm

ent (

1-12

)0.

781.

956.

17

21.

Gov

ernm

ent i

nter

est i

ncom

e (1

-16)

0.52

1.36

4.15

GO

VE

RN

ME

NT

IN

CO

ME

12.5

662

.20

223.

65

B. C

API

TA

L A

CC

OU

NT

DE

BIT

S

22.

Gro

ss g

over

nmen

t inv

estm

ent (

VI-

9)5.

8917

.47

109.

83

23.

Tan

gibl

e in

vest

men

t2.

928.

2344

.97

24.

Lan

d (n

et p

urch

ase)

—0.

010.

171.

6325

.St

ruct

ures

2.57

4.55

24.7

426

.E

quip

men

t0.

362.

1718

.33

27.

Cha

nge

in in

vent

orie

s0.

001.

340.

2728

.In

tang

ible

inve

stm

ent

2.96

9.24

64.8

629

.E

duca

tion

and

trai

ning

2.51

6.56

43.8

130

.H

ealth

0.36

1.18

5.52

31.

Mob

ility

0.02

0.20

0.71

.32

.R

esea

rch

and

deve

lopm

ent

0.07

1.31

14.8

1

33.

Acc

umul

atio

n th

roug

h ca

pita

l tra

nsfe

rs (

VI-

13)

—2.

96—

9.24

—64

.86

34.

Tan

gibl

e no

nhum

an c

apita

l0.

000.

000.

0035

.E

duca

tion

and

trai

ning

—2.

51—

6.56

—43

.81

36.

Hea

lth—

0.36

—1.

18—

5.52

37.

Mob

ility

—0.

02—

0.20

—0.

7138

.R

esea

rch

and

deve

lopm

ent

—0.

07—

1.31

—14

.81

39.

Net

fin

anci

al in

vest

men

t (V

I-17

)0.

988.

38—

0.57

GR

OSS

AC

CU

MU

LA

TIO

N3.

9116

.61

44.4

0

CR

ED

ITS

40.

Surp

lus

or d

efic

iton

curr

ent a

ccou

nt (

IVA

-13)

5.15

8.53

77.3

9

41.

Gov

ernm

ent c

apita

l con

sum

ptio

n al

low

ance

s (1

-24)

1.72

17.3

231

.87

42.

Stru

ctur

es1.

204.

7713

.76

43.

Equ

ipm

ent

0.52

12.5

518

.11

44.

Net

cap

ital t

rans

fers

—2.

96—

9.24

—64

.86

45.

Cap

ital t

rans

fers

fro

m r

est o

f w

orld

(yB

-b)

0.00

0.00

0.00

46.

Les

s: C

apita

l tra

nsfe

rs to

per

sons

(II

B-7

0)2.

907.

9450

.05

47.

Les

s: C

apita

l tra

nsfe

rs to

bus

ines

s (I

IIB

-46)

0.07

1.31

14.8

1

FIN

AN

CE

OF

GR

OSS

AC

CU

MU

LA

TIO

N3.

9116

.61

44.4

0

Tab

le 2

-5.

For

eign

Sec

tor

Acc

ount

s (b

illio

ns o

f cur

rent

dol

lars

)

Lin

e N

o.19

2919

4819

66

A. C

UR

RE

NT

AC

CO

UN

T

DE

BIT

S

1.E

xpor

ts o

f go

ods

and

serv

ices

(1-

44)

7.03

16.7

9-

43.3

6

RE

CE

IPT

S FR

OM

FO

RE

IGN

ER

S7.

0316

.79

43.3

6

CR

ED

ITS

2.Im

port

s of

goo

ds a

nd s

ervi

ces

(1-4

5)5,

8910

.35

38.0

8

3.Pe

rson

al tr

ansf

er p

aym

ents

to r

est o

f w

orld

(ne

t) (

hA-b

)0.

340.

700.

56

4.U

.S. G

over

nmen

t tra

nsfe

r pa

ymen

ts to

res

t of

wor

ld (

net)

(IV

A-l

O)

0.03

3.83

2.28

5.Su

rplu

s of

nat

ion

on c

urre

nt f

orei

gn a

ccou

nt (

VB

-6)

CU

RR

EN

T D

ISB

UR

SEM

EN

TS

AN

D S

UR

PLU

S O

N7.

0316

.79

43.3

6FO

RE

IGN

AC

CO

UN

T

B. C

API

TA

L A

CC

OU

NT

DE

BIT

S

6.Su

rplu

s of

nat

ion

on c

urre

nt f

orei

gn a

ccou

nt (

VA

-5)

0.77

1.92

2.45

7.N

et c

apita

l tra

nsfe

rs f

rom

res

t of

wor

ld0.

931.

255.

48

8.T

o pe

rson

s (I

IB-7

1)0.

931.

255.

489,

TO

bus

ines

s (I

IIB

-47)

0.00

0.00

0.00

10.

To

gove

rnm

ent (

IVB

-45)

SO

UR

CE

OF

AC

CU

MU

LA

TIO

N1.

703.

177.

92

CR

ED

ITS

11.

Acc

umul

atio

n th

roug

h ne

t cap

ital t

rans

fers

fro

m r

est o

f w

orld

(V

I-4)

0.93

1.25

5.48

12.

Net

for

eign

inve

stm

ent (

V1-

5)07

71.

922.

45

AC

CU

MU

LA

TIO

N O

N F

OR

EIG

N A

CC

OU

NT

1.70

3.17

7.92

Tab

le 2

-6.

Con

solid

ated

Cap

ital F

orm

atio

n A

ccou

nt (

billi

ons

of c

urre

nt d

olla

rs)

Lin

e N

o.19

2919

4819

66

DE

BIT

S

1.G

ross

tang

ible

non

hum

an in

vest

men

t (1-

31)

29.4

776

.63

244.

36

2.G

ross

tang

ible

hum

an in

vest

men

t (1-

37)

9.77

18.2

854

.62

3.G

ross

inta

ngib

le in

vest

men

t (1-

38)

15.6

944

.98

198.

26

4.A

ccum

ulat

ion

thro

ugh

net c

apita

l tra

nsfe

rs f

rom

of w

orld

(yB

-h)

rest

0.93

1.25

5.48

5.N

et f

orei

gn in

vest

men

t (V

B-1

2)0.

771.

922.

45

GR

OSS

AC

CU

MU

LA

TIO

N56

.63

143.

0550

5.16

CR

ED

ITS

6.G

ross

dom

estic

inve

stm

ent

54.9

313

9.89

497.

24

7. 8. 9.

By

pers

ons

and

inst

itutio

ns (

IIB

-34)

By

busi

ness

(II

IB-1

8)B

y go

vern

men

t (IV

B-2

2)

33.2

615

.78

5.89

81.2

041

.22

17.4

7

260.

3812

7.03

109.

83

10.

Acc

umul

atio

n th

roug

h ca

pita

l tra

nsfe

rs0.

931.

255.

48

11.

12.

13.

By

pers

ons

(IIB

-48)

By

busi

ness

(II

IB-3

0)B

y go

vern

men

t (IV

B-3

3)

5.85

—1.

95—

2.96

15.1

0—

4.60

—9.

24

75.2

2—

4.88

64.8

6

14.

Net

fin

anci

al in

vest

men

t.

0.07

3.90

3.46

15.

16.

17.

By

pers

ons

and

inst

itutio

ns (

IIB

-55)

By

busi

ness

(II

IB-3

6)B

y go

vern

men

t (IV

B-3

9)

2.19

—3.

110.

98

3.44

7.92

•8.3

8

20.2

816

.24

—0.

57

18.

Stat

istic

al d

iscr

epan

cy (

1-28

)0.

701.

99—

1.01

SOU

RC

E O

F G

RO

SS A

CC

UM

UL

AT

ION

56.6

314

3.05

505.

16

cji

Tab

le 2

-7.

Dis

posa

ble

Rec

eipt

s an

d E

xpen

ditu

res,

by

Sec

tor

(bill

ions

of c

urre

nt d

olla

rs)

Lin

e N

o.19

2919

4819

66

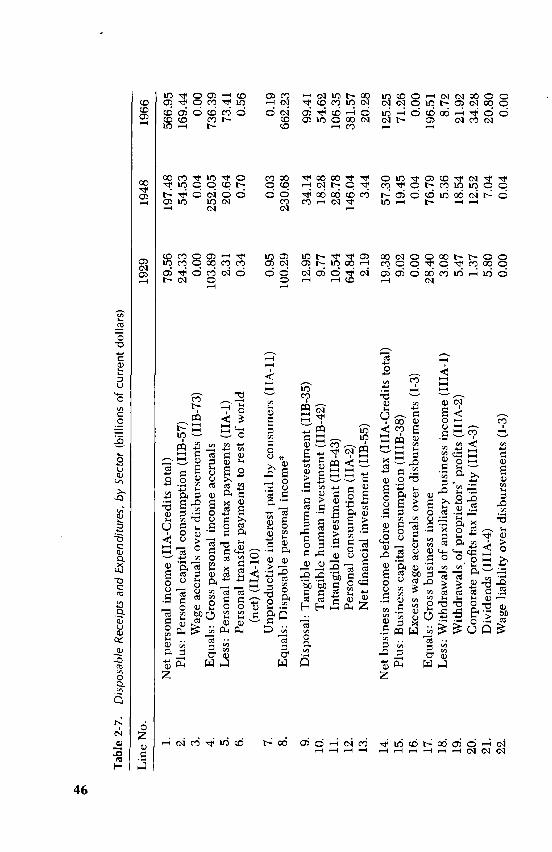

1.N

et p

erso

nal i

ncom

e (h

A-C

redi

ts to

tal)

79.5

619

7.48

566.

952.

Plus

: Per

sona

l cap

ital c

onsu

mpt

ion

(IIB

-57)

24.3

354

.53

169.

443.

Wag

e ac

crua

ls o

ver

disb

urse

men

ts (

IIB

-73)

0.00

0.04

0.00

4.E

qual

s: G

ross

per

sona

l inc

ome

accr

uals

103.

8925

2.05

736.

395.

Les

s: P

erso

nal t

ax a

nd n

onta

x pa

ymen

ts (

hA-i

)2.

3120

.64

73.4

16.

Pers

onal

tran

sfer

pay

men

ts to

res

t of

wor

ld0.

340.

700.

56(n

et)

(hA

-b)

7.U

npro

duct

ive

inte

rest

pai

d by

con

sum

ers

(hA

-il)

0.95

0.03

0.19

8.E

qual

s: D

ispo

sabl

e pe

rson

al in

com

e*10

0.29

230.

6866

2.23

9.D

ispo

sal:

Tan

gibl

e no

nhum

an in

vest

men

t (II

B-3

5)12

.95

34.1

499

.41

10.

Tan

gibl

e hu

man

inve

stm

ent (

IIB

-42)

9.77

18.2

854

.62

11.

Inta

ngib

le in

vest

men

t (11

13-4

3)10

.54

28.7

810

6.35

12.

Pers

onal

con

sum

ptio

n (I

IA-2

)64

.84

146.

0438

1.57

13.

Net

fin

anci

al in

vest

men

t (II

B-5

5)2.

193.

4420

.28

14.

Net

bus

ines

s in

com

e be

fore

inco

me

tax

(lilA

-Cre

dits

tota

l)19

.38

57.3

012

5.25

15.

Plus

: Bus

ines

s ca

pita

l con

sum

ptio

n (I

IIB

-38)

9.02

19.4

571

.26

16.

Exc

ess

wag

e ac

crua

ls o

ver

disb

urse

men

ts (

1-3)

0.00

0.04

0.00

17.

Equ

als:

Gro

ss b

usin

ess

inco

me

28.4

076

.79

196.

5118

.L

ess:

With

draw

als

of a

uxili

ary

busi

ness

inco

me

(lilA

-i)

3.08

5.36

8.72

19.

With

draw

als

of p

ropr

ieto

rs' p

rofi

ts (

IIIA

-2)

5.47

18.5

421

.92

20.

Cor

pora

te p

rofi

ts ta

x lia

bilit

y (I

IIA

-3)

1.37

12.5

234

.28

21.

Div

iden

ds (

IIIA

-4)

5.80

7.04

20.8

022

.W

age

liabi

lity

over

dis

burs

emen

ts (

1-3)

0.00

0.04

0.00

23.

Equ

als:

Gro

ss r

etai

ned

earn

ings

12.6

833

.29

110.

79

24.

Dis

posa

l: T

angi

ble

inve

stm

ent (

IIIB

-19)

13.6

034

.27

99.9

825

.In

tang

ible

inve

stm

ent (

IIIB

-25)

2.19

6.95

27.0

426

.N

et f

inan

cial

inve

stm

ent (

IIIB

-36)

—3.

11—

7.92

—16

.24

27.

Gov

ernm

ent i

ncom

e (I

VA

-Cre

dits

tota

l)12

.56

62.2

022

3.65

28.

Plus

: Gov

ernm

ent c

apita

l con

sum

ptio

n (I

VB

-41)

1.72

17.3

231

.87

29.

Equ

als:

Gro

ss g

over

nmen

t rec

eipt

s or

acc

rnal

s14

.28

79.5

225

5.52

30.

Les

s: G

over

nmen

t tra

nsfe

r pa

ymen

ts (

IVA

-8)

0.94

14.3

743

.35

31.

Unp

rodu

ctiv

e in

tere

st p

aid

by g

over

nmen

t (IV

A-i

l)0.

183.

141.

8132

.Su

bsid

ies

less

cur

rent

sur

plus

of

gove

rnm

ent

ente

rpri

ses

(IV

A-1

2)—

0.14

0.86

2.62

33.

Equ

als:

Dis

posa

ble

gove

rnm

ent i

ncom

ea13

.30

61.1

520

7.74

34.

Dis

posa

l: T

angi

ble

inte

rest

(IV

A-2

3)2.

928.

2344

.97

35.

Inta

ngib

le in

vest

men

t (IV

B-2

8)2.

969.

2464

.86

36.

Gen

eral

gov

ernm

ent c

onsu

mpt

ion(

I V

A-i

)6.

4335

.30

98.4

837

.N

et f

inan

cial

inve

stm

ent (

IVB

-39)

0.98

8.38

—0.

57

38.

Net

for

eign

tran

sfer

s (V

A-3

+ 4

)0.

384.

532.

8339

.L

ess:

Net

exp

orts

(1-

43)

1.15

6.44

5.28

40.

Equ

als:

Net

for

eign

cla

ims

—0.

77—

1.91

—2.

45

41.

Tot

al c

urre

nt in

com

e (l

ines

8 +

23

+ 3

3 +

38)

126.

6532

9.65

983.

5942

.PI

us: S

tatis

tical

dis

crep

ancy

(1-

28)

0.70

—1.

99—

1.01

43.

Equ

als:

Adj

uste

d G

NP

127.

3432

7.67

982.

57

aCro

ss o

f ca

pita

l con

sum

ptio

n an

d ca

pita

l tra

nsfe

rs, b

ut n

et o

f cu

rren

t tra

nsfe

rs to

oth

er s

ecto

rs.

48 THE FORMATION AND STOCKS OF TOTAL CAPITAL

sent the difference between net acquisition of assets (lending) and netincurrence of liabilities (borrowing), each of which could be detailedby type of financial instrument. But our interest here is not in the flowof funds.

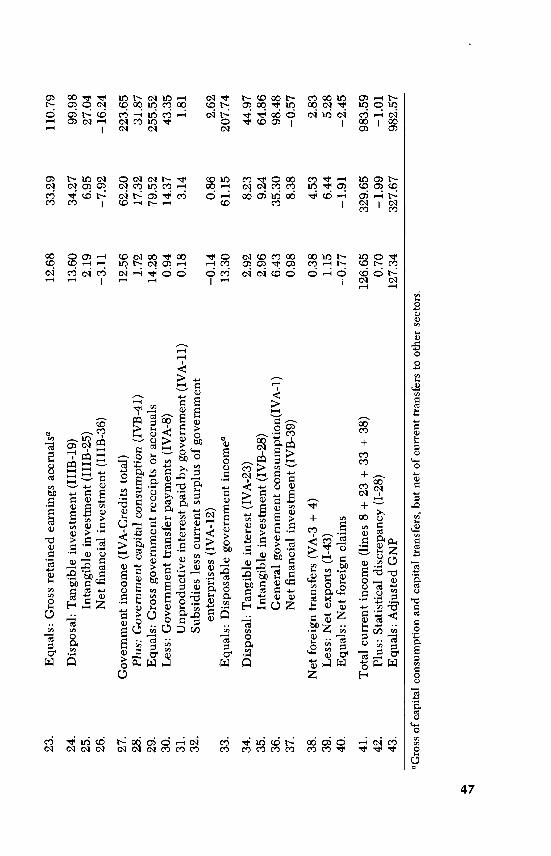

In the foreign sector capital account (Table 2-5), note that we addthe net capital transfers from the rest of the world (line 7), by recipientsector, to the surplus of the nation on current account (line 6).

The consolidated capital formation account (Table 2-6) contains thecontra-entries to the various investments and capital transfers of thesectors, and summarizes national investment, by sector and major type.Note that the capital transfers among the domestic sectors plus netcapital transfers from abroad sum to zero. So do net financial investmentof the domestic sectors plus net foreign investment, after allowance forthe statistical discrepancy. Or, to state it alternatively, the sum of netfinancial investment for the domestic sectors (line 14) equals net for-eign investment (line 5) less the statistical discrepancy (line 18).

Another useful summary is provided in Table 2-7, showing dispos-able income and its disposition, by sector. The disposable income foreach sector is derived as its gross income less transfers to other sectors,and it sums to GNP less statistical discrepancy. Disposable income isallocated by each sector to consumption, productive tangible and intan-gible investments, and net financial investment. Although savingequals investment for the nation, they are unequal for each sector to theextent of net financial investment. The sector disposable income series,and the channels of disposition, are necessary for an analysis of con-sumption, saving, and investment functions.

BALANCE SHEETS AND WEALTH STATEMENTS

The combined national balance sheets show the condition ofthe economy at the end of a period as a result of saving and borrowing,investing and lending, and (if stated in current prices) revaluations ofassets since the beginning of the period. In the balance sheet, produc-tive wealth, hitherto confined to tangibles, is added to the financialassets to obtain total assets, which are conventionally shown on the left-hand side. On the opposite side are liabilities (including stock andother equity if these are also carried on the asset side, as is usual innational and sector balance sheets).

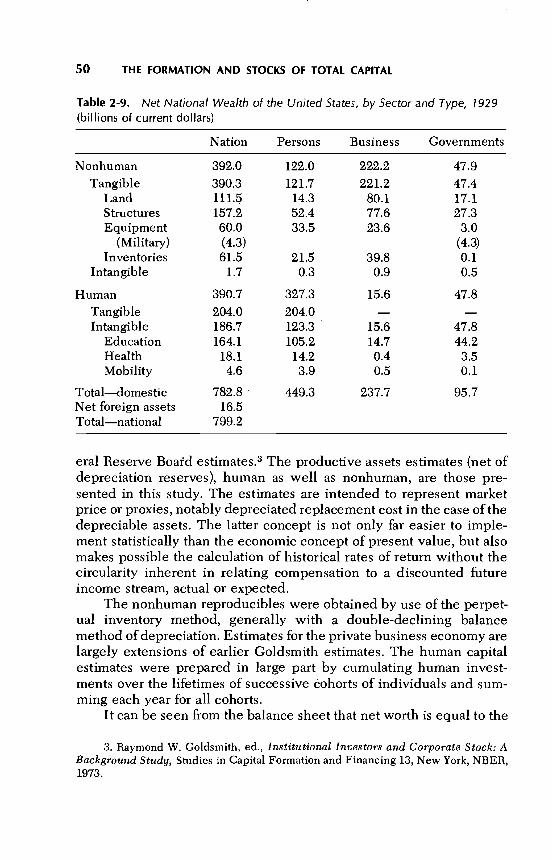

Table 2-8 below presents a combined national balance sheet forthe United States for the end of the year 1968. The financial assets andliabilities are taken from Goldsmith, who based them largely on Fed-

Tab

le 2

-8.

Com

bine

d B

alan

ce S

heet

of t

he U

nite

d S

tate

s, 1

968,

Incl

udin

g H

uman

Cap

ital (

bi I

lions

of c

urre

nt d

olla

rs)

Fin

anci

alas

sets

4,34

9L

iabi

litie

s—to

tal

2,79

1

Mon

etar

y re

serv

es22

Mon

etar

y re

serv

es5

Cur

renc

y an

d de

man

d de

posi

ts20

9C

urre

ncy

and

dem

and

depo

sits

211

Shor

t-te

rm c

laim

s1,

136

Shor

t-te

rm d