the 2015 uk reputation dividend report€¦ · the 2015 uk reputation dividend report ... by...

TRANSCRIPT

The 2015 UK Reputation Dividend Report

What’s your reputation worth?

...studies like this should focus the minds of all those in positions of corporate power

Sunday Telegraph - Rainmaker

“

What’s your reputation worth?

Reputation Value: Money on the Ball or Left on the Table

u� UK corporate reputations worth over £620bn

u� At best, reputation contributes £1 in every £2 of market cap; at worst, it is ‘destroying’ £1 of value in £7.

u� Unilever and Diageo hang on to the top spots with highest reputation values; Next leaps to 3rd place, and HSBC appears among top ten

u� More companies showing declines in Reputation Contribution than rises for the first time in six years suggesting a creeping complacency with regard to their reputation assets.

u� FTSE 100 companies are, on average, leaving £490m on the table by companies not addressing reputation sufficiently; FTSE 250s, £23m.

Introduction

The 2015 UK Reputation Dividend Report summarises the current state of corporate reputation and how it

impacts shareholder value in the UK. It is the eighth annual study and is based on analysis of more than 200

of the country’s largest public companies.

The Reputation Dividend Report provides a fresh perspective on how well, or not, corporate reputations are

working, and specifically, to the advantage of their investors. It combines headline measures of reputation

strength with financial metrics to explain the economic impact of each individual company’s reputation asset.

This is the Reputation Contribution – the proportion of a company’s market capitalisation that is directly attrib-

utable to the confidence instilled by its reputation. (See www.reputationdividend.com/what-we-do for details of

the analysis)

This is critical insight for reputation stewards, not only in the shape of explanation as to how much financial

value this intangible asset is delivering but also, into the communications and messaging priorities to secure

and grow them further.

This year’s report was launched on February 24th, 2015.

1

Overview

At their most effective the corporate reputations of UK companies are contributing one pound in everytwo of market capitalisation. At their least effective, they are destroying one pound of value in seven.

2014 was a year in which many of the economic signals remained firmly mixed. UK employment appeared to

be on the up but wage growth was poor; interest rates stayed low but the longer term effects of quantitative

easing remained to be understood; recovery beckoned for many UK companies but concerns for the impact of

Eurozone slowness and a Chinese slowdown grew.

Against that backdrop corporate reputations at the start of 2015 were, in the main, continuing to work hard to

secure investor confidence. At their most significant, Reputation Contributions - the proportion of market cap-

italisation attributable to reputation - were approaching 50%. In a small minority of cases however the impact

was such that market capitalisation was up to 14% lower because reputations were undermining confidence.

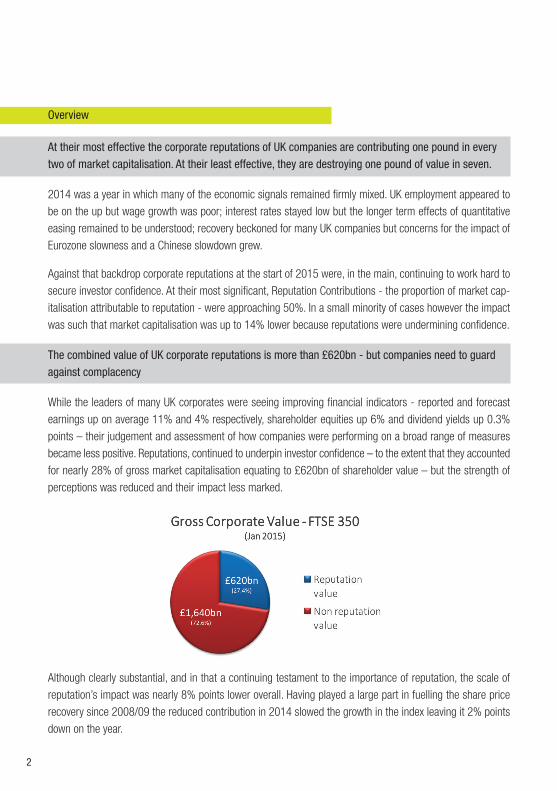

The combined value of UK corporate reputations is more than £620bn - but companies need to guardagainst complacency

While the leaders of many UK corporates were seeing improving financial indicators - reported and forecast

earnings up on average 11% and 4% respectively, shareholder equities up 6% and dividend yields up 0.3%

points – their judgement and assessment of how companies were performing on a broad range of measures

became less positive. Reputations, continued to underpin investor confidence – to the extent that they accounted

for nearly 28% of gross market capitalisation equating to £620bn of shareholder value – but the strength of

perceptions was reduced and their impact less marked.

Although clearly substantial, and in that a continuing testament to the importance of reputation, the scale of

reputation’s impact was nearly 8% points lower overall. Having played a large part in fuelling the share price

recovery since 2008/09 the reduced contribution in 2014 slowed the growth in the index leaving it 2% points

down on the year.

2

The set back was, on the whole, more apparent in larger companies. Although their reputations continued to

be more influential, and thus proportionately more valuable, the declines in 2014 were larger. Reputation Con-

tributions across the FTSE 100 slipped nearly 9% points to an average of 30%, while the decline across the

FTSE 250 was a more modest 3% points to just 16%. As a result, the combined value of FTSE 100 companies

at the end of 2014 was 1.7% lower over the year compared with the FTSE 250 where it was 0.4% up.

It would seem that some reputation owners did not fully appreciate just how hard their reputations were working

for them and took their foot off the pedal too soon. Either they relied too much on the improving financial results,

assuming they would speak for themselves, or they failed to fully direct their messaging and corporate

communications to play to the components of their reputations that mattered most.

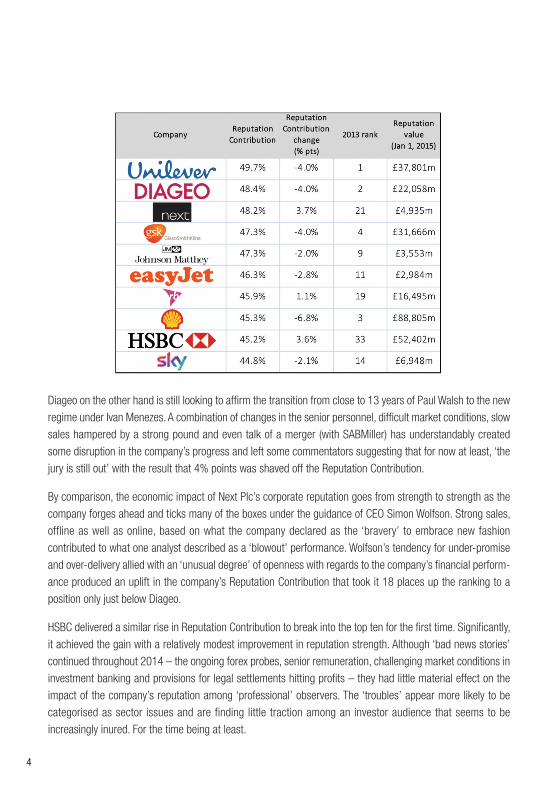

Unilever and Diageo hold on to the top spots but the momentum is elsewhere

Standing out at the top of the Reputation Contribution table, but only just, are Unilever and Diageo. They held

on to the lead established in 2013 but their previously blue chip reputations undoubtedly lost some impact as

their momentum stalled.

Although keeping the number one position, Unilever’s Reputation Contribution slipped 4% points and is now

below 50% for the first time in five years. The company’s strategic ambitions appear to be both understood

and appreciated by commentators, but there were growing signs of pressure for reassurance. 2014 was

arguably the company’s ‘weakest’ year for a decade and the combination of slow US recovery, poor European

outlook and strong sterling is doing little to reward Paul Polman’s increased emphasis on personal care and

emerging markets. As a result, perceptions of the company’s leadership prowess lost a little of its shine as too

did its much championed community and environmental credentials.

What’s your reputation worth?

3

Diageo on the other hand is still looking to affirm the transition from close to 13 years of Paul Walsh to the new

regime under Ivan Menezes. A combination of changes in the senior personnel, difficult market conditions, slow

sales hampered by a strong pound and even talk of a merger (with SABMiller) has understandably created

some disruption in the company’s progress and left some commentators suggesting that for now at least, ‘the

jury is still out’ with the result that 4% points was shaved off the Reputation Contribution.

By comparison, the economic impact of Next Plc’s corporate reputation goes from strength to strength as the

company forges ahead and ticks many of the boxes under the guidance of CEO Simon Wolfson. Strong sales,

offline as well as online, based on what the company declared as the ‘bravery’ to embrace new fashion

contributed to what one analyst described as a ‘blowout’ performance. Wolfson’s tendency for under-promise

and over-delivery allied with an ‘unusual degree’ of openness with regards to the company’s financial perform-

ance produced an uplift in the company’s Reputation Contribution that took it 18 places up the ranking to a

position only just below Diageo.

HSBC delivered a similar rise in Reputation Contribution to break into the top ten for the first time. Significantly,

it achieved the gain with a relatively modest improvement in reputation strength. Although ‘bad news stories’

continued throughout 2014 – the ongoing forex probes, senior remuneration, challenging market conditions in

investment banking and provisions for legal settlements hitting profits – they had little material effect on the

impact of the company’s reputation among ‘professional’ observers. The ‘troubles’ appear more likely to be

categorised as sector issues and are finding little traction among an investor audience that seems to be

increasingly inured. For the time being at least.

4

The one company meriting particular attention for its reputational performance in 2014 has to be AstraZeneca.

While the main story was without question its robust and ultimately successful defence of the bid from American

giant Pfizer, a number of other factors conspired to confirm the company in the most favourable light for some

time. CEO Pascal Soriot has raised investor hopes as the turnaround progresses and, while aspects such as

innovation are yet to be as well regarded as might be hoped, there were notable improvements in revenues

and the all important pipeline. As a result the company’s reputation asset recovered to the point where the

confidence it is supporting registered a 26% point rise to 40% to become the 13th highest of all the companies

tracked in 2014.

Industry sector continues to have a bearing on the influence of reputation

One factor governing the economic impact of corporate reputation is company sector with average Reputation

Contributions ranging from the low teens (Technology and Telecommunications) to the mid 30s (Basic Materials).

Individual company ratings will vary within the averages but standards undoubtedly become rules by which

companies of a type can be judged.

Investors looking at companies in Basic Materials, Consumer Goods and Oil & Gas tend to be guided in part by

both the economic cycle and faith in market indicators for their assessments putting greater emphasis on what

amounts to company reputation. Within that a stronger reputation will inure a company from sector issues. For

example, Shell’s substantially more potent reputation has been more effective in reducing the decline in share

price triggered by the falling oil price (-11% in six months to January 2015) than BP’s (share price down -

19%). By contrast, the prospects for companies in ‘newer’ sectors like Telecommunications and Technology

are sometimes easier to illustrate and evidence with the result that the dependence on reputation is lower.

What’s your reputation worth?

5

Value depends most on what companies are known for

While the overall strength of any two companies’ reputations may be the same the economic contribution of

their reputations can be quite different. Different reputations will display different strengths and weaknesses

and these will support different levels of investor confidence and so value.

At the beginning of 2015 the most valuable components of corporate reputations in the FTSE 350 were per-

ceptions of companies’ financial soundness and long term potential. Together they accounted for 30% of all

reputation value. ‘Softer’ qualities such as quality of the leadership and how well the company was thought to

be deploying its assets were the next most important accounting for 27% of the value. Least impactful but by

no means insignificant are companies’ corporate and environmental credentials. These alone contributed a

total of £22bn of shareholder value and an answer to the perennial question ‘what are companies’ CSR

programmes actually worth?’

As well as being a repository of value corporate reputations retain potential to grow it further

Reputation Leverage is the extent to which growth in reputation strength is likely to increase investor confidence

and thus market capitalisation. It varies considerably from company to company but provides important insight

into the potential for returns on reputation building investment.

At the beginning of 2015, the average Reputation Leverage across the FTSE 350 was 1.4%. As such, a 1%

improvement in the underlying strength of a company’s reputation would be expected to deliver a 1.4% uplift

in market capitalisation.

6

That suggests that the average FTSE 100 company looking to grow the strength of its corporate reputation by

just 1% would expect a return on the investment of close to £266m. By the same measure the average FTSE

250 with a market capitalisation of £1.25bn would expect to see a return of £17m.

The messaging priorities for optimising value growth

While the broad requirements of messaging delivered through corporate communications and investor relations

may be well known it is clear that the needs of the investment community are movable. A company’s reputation

can be a complex beast and different elements will work harder than others to drive confidence to build value.

In short, companies will achieve disproportionately greater returns on their communications investment by

ensuring they are promoting the messages that matter most at the time.

Financially orientated ‘harder’ messages remain motivating, but so too are many of the apparently ‘softer’ qualities.

Perceptions of how companies are seen to be deploying their assets emerged as the single most influential

driver in 2015. Investors are in two minds as to the precise shape of future demands and are marking up com-

panies showing adaptability and application.

Long term investment potential and financial soundness continues to be key given the volatile world as does a

company’s ability to attract talent and thus compete as the upswing gathers pace.

Innovation and product quality continue to be important but marginally less so as UK consumer expenditure

remains tight for the foreseeable future. On the other hand, community and environmental credentials continue

to grow in importance as investors increasingly recognise the commercial benefits they provide.

What’s your reputation worth?

7

How Reputation Dividend Can Help

Analytics are applied on two levels.

Level 1: Dedicated company reports

Analysis of your company’s reputation based on data and analysis from our 2014 study.

A report includes:

u� Your company’s Reputation Contribution – the value of your company’s corporate reputation – along with historical trend data.

u� Comparisons to defined competitors and peer group companies.

u� A breakdown of the sources of your company’s reputation value and their individual contribution to market capitalisation - your company’s ‘Reputation Risk Profile’.

u� The incremental value potential of each reputational driver and likely ROI – ‘what if’ analysis exploring different messaging possibilities.

u� Pointers on reputational messaging priorities as they relate to securing and growing shareholder value.

Individual company reports include a meeting to present the findings and opportunity to discuss their

implications.

Level 2: Ad-hoc research and consulting

For any company wishing to make a deeper dive investigation we offer a second level of research and analy-

sis. This provides a more comprehensive and bespoke examination of the drivers of a company’s reputation

and its capacity to drive shareholder value.

This service is for organizations that wish to assess the impact of corporate reputation in more detail and

against company-specific reputational drivers or against a particular timeframe (for example in the run up to

financial results).

Level 2 reports take account of reputational and financial data from a mix of your own internal and external

sources. We can also undertake additional custom research as required. We use our own research resources

and can complement these with any additional sources of your choice.

These engagements often involve interviews with senior management, investment and industry analysts and

communications specialists to ensure that existing strategies are factored into our analysis.

8

In addition to everything in a Level 1 report, a Level 2 report will provide:

u� The information necessary to inform executive management teams how to allocate resources and budget more effectively.

u� A framework to align and adjust communications, messaging channels and budgets.

u� Guidelines for revising the internal strategies to support the reputation opportunities.

u� A basis to improve the coordination of communications and operational strategies.

u� The insight and knowledge to better align corporate, internal and customer brand management.

u� The basis of a fully integrated and on-going reputation value management programme.

Level 2 engagements include regular client liaison and findings review throughout the process and culminate

in a presentation to and discussion with your senior leadership team.

6For further information about the 2015 UK study and how reputation value analytics can help your company

please contact either;

Simon Cole – Founding Partner Sandra Macleod – [email protected] [email protected]

Or visit our website : www.reputationdividend.com

What’s your reputation worth?

9

What’s your reputation worth?

Valuing Corporate Reputation to Secure and Build Shareholder Value

© 2015 Reputation Dividend