tft-lcd key components market update q4-2012. quarterly... · tft-lcd key components market update...

TRANSCRIPT

14 January 2013 | Page 1 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

Boyce Fan, Caroline Chen

TFT-LCD Key Components Market Update

Q4-2012

Display Division, Research Manager

Nov, 2012

Display Division, Analyst

14 January 2013 | Page 2 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

Outline

I. Summary

II. Key Component Status

IV. Mainstream Size Panel Cost

V. Panel Cost Analysis &

Financial Performance Analysis

VI. Large Size LCD Panel Supply

VII. Conclusion

III. Key Component Technical Trend

14 January 2013 | Page 3 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

Outline

I. Summary

14 January 2013 | Page 4 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

Summary

Key Components Status

Key Components Technical Trend

Mainstream Size Panel Cost Analysis

WW Large Size LCD Panel Supply

Component price decline – glass substrate: around 3~5%; polarizer: 1~2% on IT products and 2~3% on TV; BLU: 1~1.5% on CCFL

products and 1~5% on LED products.

As the demand for small & middle sized panels emerges, certain color filter(CF) makers have started to adopt Gen6 CF production lines

with new equipments to cut 4 pieces on large substrates to supply CFs of small generation in order meet high ppi requirement.

Meanwhile, the demand for large-sized panels recently heats up, slightly squeezing CF capacity in Gen6.

Affected by the rise of tablet demand, polarizers and driver ICs see capacity squeezed between large-sized and small mid-sized

products. Along with no expansion plans for polarizers and driver ICs in the near future, the balanced to slightly tight situation between

demand and supply would likely to extend to 2013.

After the CCFL models gradually disappear, the low-cost direct type model would possibly take the position of the entry-level model.

While manufacturers actively develop thin direct-type models, which is expected to be launched in 2013, attack the mainstream market,

and compete with the edge type.

Encouraged by tablets and smartphones, high resolution products have built the firm footstep in the small & middle sized product market

and moves toward the NB market. In the TV market, as the bottleneck of AMOLED TV development remains, 4K2K model development

and promotion in the immediate future would be a major point.

4K2K model development speed still depends on hardware makers’ activeness, in the condition of content and standard being immature

in the short term, the 4K2K models, touted with the price 1.2-1.3 times that of standard FHD models and providing low-cost

transformation solution, would be still appealing to certain manufacturers.

In 2012, the large-sized panel glass substrate input is expected to total 167.9Mn m2, growing 14.8% YoY from 2011.

Stirred by the demands for large-sized and new-sized products, the overall Q4 utilization in the industry remains above 80%, and panel

makers show an aggressive attitude on financial performances to swing from losses to profits, as a result, the utilization wouldn’t show

noticeable decline easily in the short term.

As makers are devoted actively to the developments of new technologies and new processes which consume the capacity to a certain

degree, the available glass substrate input area is projected to decline 5.2%.

In 4Q12, panel cost decline in mainstream sizes – NB is 3~4%; monitor is 2~3%; TV is around 3~5%.

The material cost and price ratio in mainstream sizes is around 66~86% in 4Q12. Since Monitor & TV panel price stopped dropping and

rebounded, the ratio of Monitor application decreases by 2% QoQ; TV application decreases by 2~3% QoQ.

15.6W NB are of the worst profitability level. The panel price has almost approached the cash cost level of that size.

14 January 2013 | Page 5 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

Outline

II. Key Component Status

14 January 2013 | Page 6 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

QoQ changes

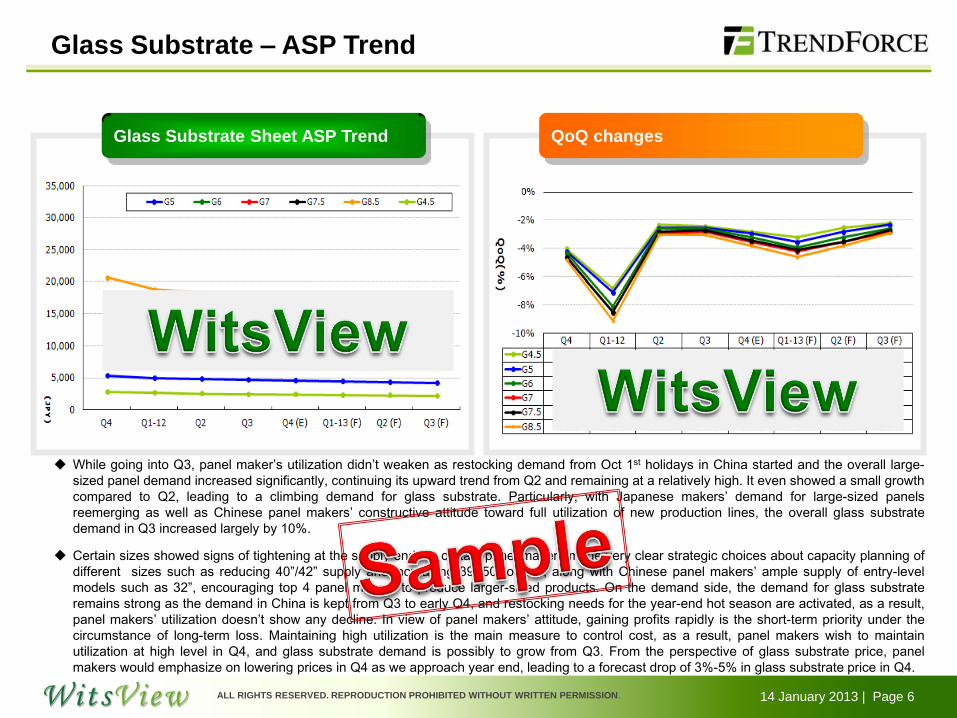

Glass Substrate – ASP Trend

While going into Q3, panel maker’s utilization didn’t weaken as restocking demand from Oct 1st holidays in China started and the overall large-

sized panel demand increased significantly, continuing its upward trend from Q2 and remaining at a relatively high. It even showed a small growth

compared to Q2, leading to a climbing demand for glass substrate. Particularly, with Japanese makers’ demand for large-sized panels

reemerging as well as Chinese panel makers’ constructive attitude toward full utilization of new production lines, the overall glass substrate

demand in Q3 increased largely by 10%.

Certain sizes showed signs of tightening at the supply end, as certain panel makers made very clear strategic choices about capacity planning of

different sizes such as reducing 40”/42” supply and increasing 39”/50” output, along with Chinese panel makers’ ample supply of entry-level

models such as 32”, encouraging top 4 panel makers to produce larger-sized products. On the demand side, the demand for glass substrate

remains strong as the demand in China is kept from Q3 to early Q4, and restocking needs for the year-end hot season are activated, as a result,

panel makers’ utilization doesn’t show any decline. In view of panel makers’ attitude, gaining profits rapidly is the short-term priority under the

circumstance of long-term loss. Maintaining high utilization is the main measure to control cost, as a result, panel makers wish to maintain

utilization at high level in Q4, and glass substrate demand is possibly to grow from Q3. From the perspective of glass substrate price, panel

makers would emphasize on lowering prices in Q4 as we approach year end, leading to a forecast drop of 3%-5% in glass substrate price in Q4.

Glass Substrate Sheet ASP Trend

14 January 2013 | Page 7 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

Color Filter Sheet ASP Trend QoQ changes

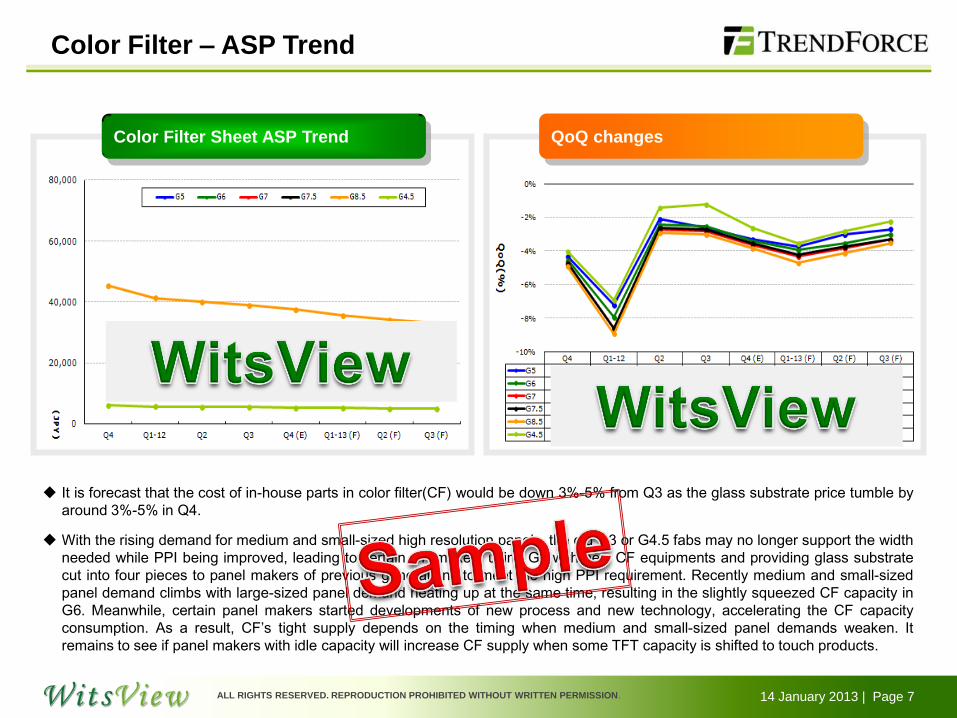

Color Filter – ASP Trend

It is forecast that the cost of in-house parts in color filter(CF) would be down 3%-5% from Q3 as the glass substrate price tumble by

around 3%-5% in Q4.

With the rising demand for medium and small-sized high resolution panels, the old G3 or G4.5 fabs may no longer support the width

needed while PPI being improved, leading to certain CF makers using G6 with new CF equipments and providing glass substrate

cut into four pieces to panel makers of previous generations to meet the high PPI requirement. Recently medium and small-sized

panel demand climbs with large-sized panel demand heating up at the same time, resulting in the slightly squeezed CF capacity in

G6. Meanwhile, certain panel makers started developments of new process and new technology, accelerating the CF capacity

consumption. As a result, CF’s tight supply depends on the timing when medium and small-sized panel demands weaken. It

remains to see if panel makers with idle capacity will increase CF supply when some TFT capacity is shifted to touch products.

14 January 2013 | Page 8 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

Polarizer ASP Trend QoQ changes

Polarizer – ASP Trend

In addition to 39” and 50”, the demands for new sizes developed by panel makers surge, including 58” and 28”. Along with the large-sized panel

demand heating up, the polarizer demand continues from Q3 to Q4. Based on makers’ estimations, the shipment peak would be in October, the

overall shipment in Q4 would grow by 5%-10% from Q3. The price decline would be 1%-3% due to demand growing recently and significant price

drops of certain sizes in previous quarters.

While going into the 2nd half of the year, the demand for the new generation of tablet surges. The film touch module, previously regarded as losing

its market, is revived on the concepts of thinness design and cost-saving. Of which ITO film materials and polarizer materials can share polarizer

capacity, with tablets also demanding for polarizers. As polarizer and ITO films used in tablets generate higher profits, makers would choose to

supply these items as priority, squeezing polarizer capacity globally. In addition to capacity squeezing effect, demands for large-sized and new

sized panel accelerate obviously the consumption of polarizer area. As different panel makers have distinct requirements for polarizer structure,

the higher complexity they demand causes higher capacity consumption. Besides, new size products have cutting efficiency concern in

accordance with the production width of polarizer capacity, leading to a polarizer supply-demand balance in the 2nd half of the year. For polarizer

makers, in consideration of the rising of AMOLED products, the polarizer demand would trim dramatically, causing polarizer makers’ relatively

conservative attitude toward expanding capacity in the short term. It is also foreseen the polarizer supply-demand balance could continue into

2013.

14 January 2013 | Page 9 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

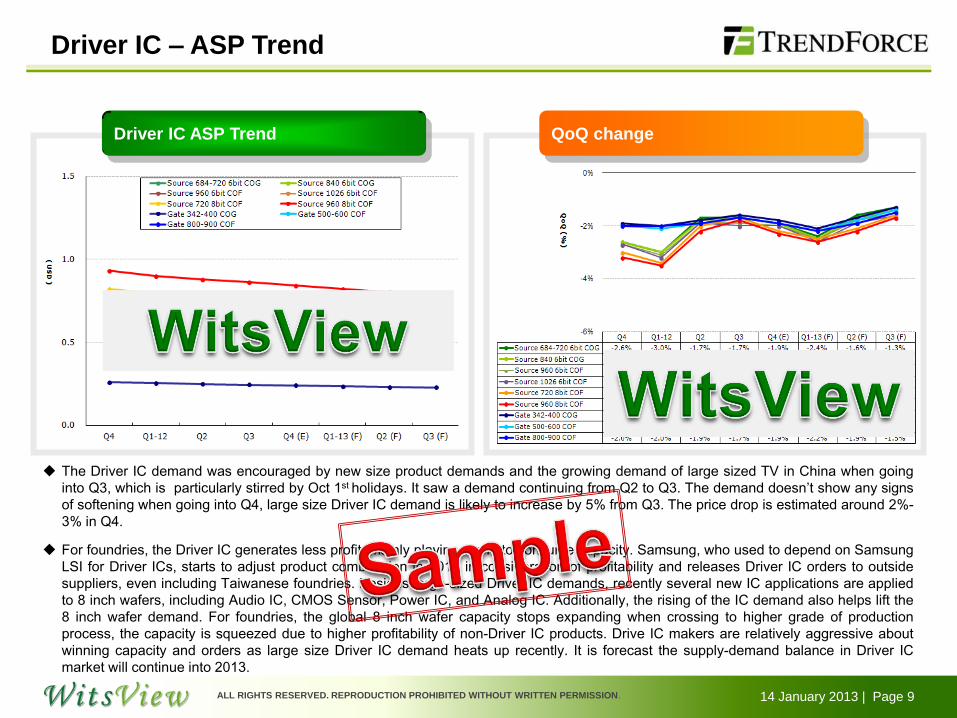

Driver IC – ASP Trend

Driver IC ASP Trend QoQ change

The Driver IC demand was encouraged by new size product demands and the growing demand of large sized TV in China when going

into Q3, which is particularly stirred by Oct 1st holidays. It saw a demand continuing from Q2 to Q3. The demand doesn’t show any signs

of softening when going into Q4, large size Driver IC demand is likely to increase by 5% from Q3. The price drop is estimated around 2%-

3% in Q4.

For foundries, the Driver IC generates less profit, mainly playing a role to consume capacity. Samsung, who used to depend on Samsung

LSI for Driver ICs, starts to adjust product combination in 2012 in consideration of profitability and releases Driver IC orders to outside

suppliers, even including Taiwanese foundries. Besides large-sized Driver IC demands, recently several new IC applications are applied

to 8 inch wafers, including Audio IC, CMOS Sensor, Power IC, and Analog IC. Additionally, the rising of the IC demand also helps lift the

8 inch wafer demand. For foundries, the global 8 inch wafer capacity stops expanding when crossing to higher grade of production

process, the capacity is squeezed due to higher profitability of non-Driver IC products. Drive IC makers are relatively aggressive about

winning capacity and orders as large size Driver IC demand heats up recently. It is forecast the supply-demand balance in Driver IC

market will continue into 2013.

14 January 2013 | Page 10 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

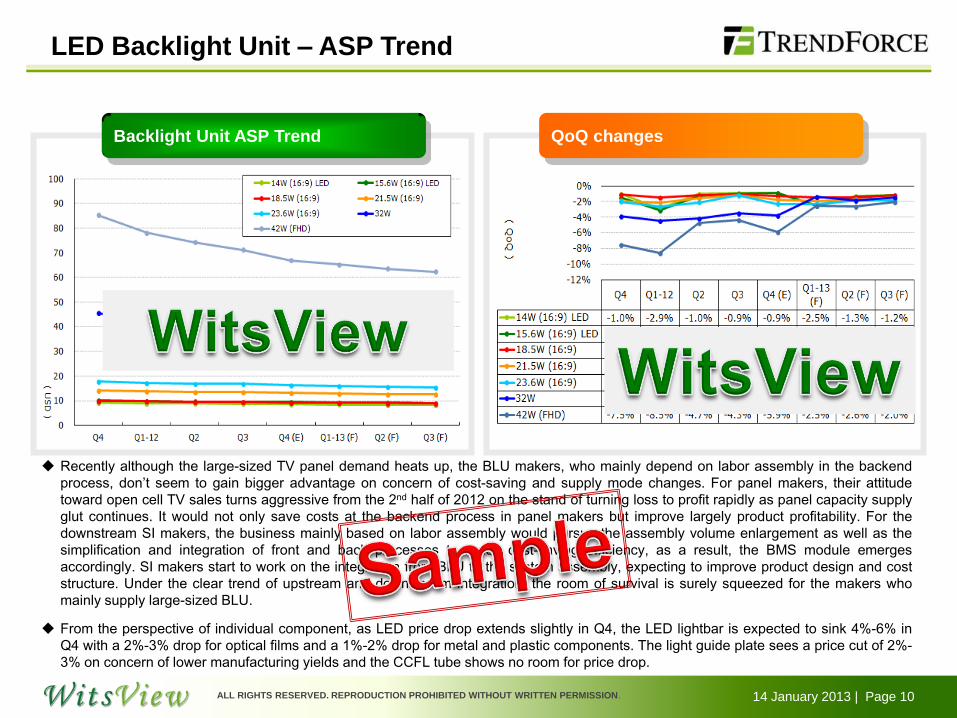

Backlight Unit ASP Trend QoQ changes

LED Backlight Unit – ASP Trend

Recently although the large-sized TV panel demand heats up, the BLU makers, who mainly depend on labor assembly in the backend

process, don’t seem to gain bigger advantage on concern of cost-saving and supply mode changes. For panel makers, their attitude

toward open cell TV sales turns aggressive from the 2nd half of 2012 on the stand of turning loss to profit rapidly as panel capacity supply

glut continues. It would not only save costs at the backend process in panel makers but improve largely product profitability. For the

downstream SI makers, the business mainly based on labor assembly would pursue the assembly volume enlargement as well as the

simplification and integration of front and back processes to reach cost-saving efficiency, as a result, the BMS module emerges

accordingly. SI makers start to work on the integration from BLU to the system assembly, expecting to improve product design and cost

structure. Under the clear trend of upstream and downstream integration, the room of survival is surely squeezed for the makers who

mainly supply large-sized BLU.

From the perspective of individual component, as LED price drop extends slightly in Q4, the LED lightbar is expected to sink 4%-6% in

Q4 with a 2%-3% drop for optical films and a 1%-2% drop for metal and plastic components. The light guide plate sees a price cut of 2%-

3% on concern of lower manufacturing yields and the CCFL tube shows no room for price drop.

14 January 2013 | Page 11 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

Outline

III. Key Component Technical Trend

14 January 2013 | Page 12 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

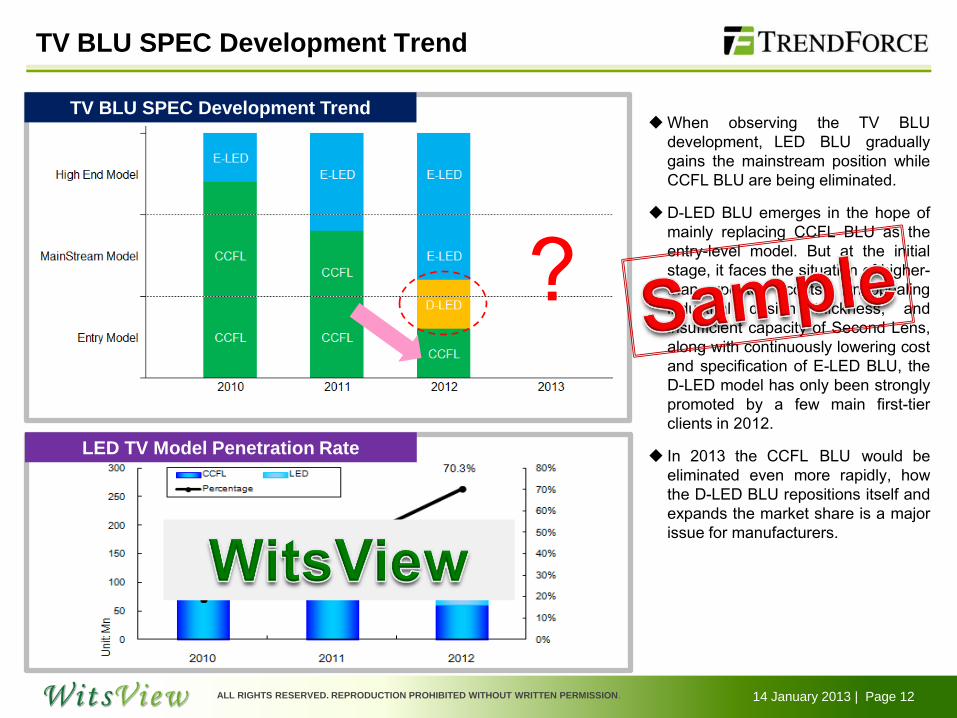

TV BLU SPEC Development Trend

TV BLU SPEC Development Trend

?

LED TV Model Penetration Rate

When observing the TV BLU

development, LED BLU gradually

gains the mainstream position while

CCFL BLU are being eliminated.

D-LED BLU emerges in the hope of

mainly replacing CCFL BLU as the

entry-level model. But at the initial

stage, it faces the situation of higher-

than-expected costs, unappealing

industrial design thickness, and

insufficient capacity of Second Lens,

along with continuously lowering cost

and specification of E-LED BLU, the

D-LED model has only been strongly

promoted by a few main first-tier

clients in 2012.

In 2013 the CCFL BLU would be

eliminated even more rapidly, how

the D-LED BLU repositions itself and

expands the market share is a major

issue for manufacturers.

14 January 2013 | Page 13 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

Challenge of D-LED Model : Thickness

CCFL STD Model Module Thickness

30~35mm

E-LED Model Module Thickness

20~25mm

D-LED Model Module Thickness

50~55mm

New D-LED Model Module Thickness

30~35mm

The number of LED Package increases,

reducing the height of mixing light area.

The structural diffuser plate replaces the

previous flat diffuser plate, strengthening

the mixing light uniformity.

LED Package arrangement is switched

from strip to diamond type, enforcing the

light mixing effect.

The old D-LED Model’s module

thickness reaches 50-55mm and

the industrial design is not

popular with consumers. The new

D-LED Model’s thickness is

expected to be reduced to

30~35mm, which is comparable

with the CCFL Standard Model

and increase the advantages to

compete with the E-LED Model.

The thickness reduction mainly

relies on increasing number of

LED Package, the adoption of

structural diffuser plates, the

change of LED Package

arrangement to reinforce the

mixing light uniformity.

BLU Thickness Comparison

14 January 2013 | Page 14 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

Challenge of D-LED Model: LED Package

Old LED Qty.

32” 30~36

39”/42” 60~70

46” 70~75

50” 85~90

55” 95~100

New LED Qty.

32” 40~50

39”/42” 65~70

46” 80~85

50” 100~105

55” 120~130

In 2013, certain makers would highly anticipate the D-

LED models in the hope that it can entirely replace CCFL

Model in the Entry Market and extend to the Mainstream

Market to compete with the E-LED Model.

It is projected that makers would attack the Entry Market

with the thicker D-LED Model while the cost declines Q

by Q and possibly reaches that of the CCFL Model.

Manufacturers have developed the thinner D-LED Model,

likely to be positioned in the Mainstream Market with the

increasing number of LED Packages and improving

industrial design and specification.

14 January 2013 | Page 15 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

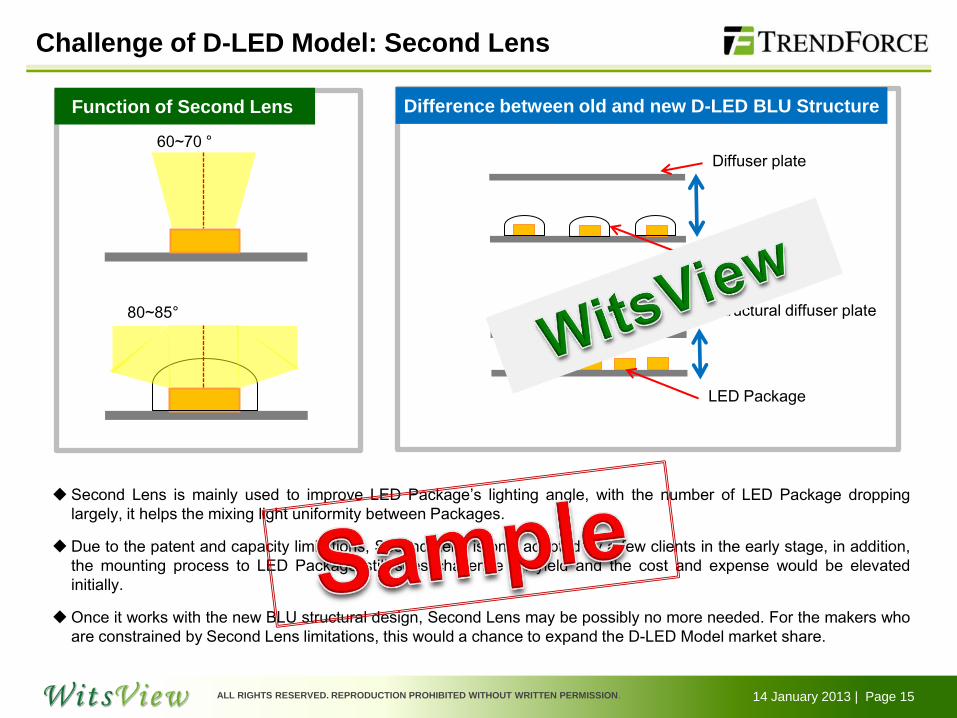

Challenge of D-LED Model: Second Lens

60~70 °

80~85°

Function of Second Lens Difference between old and new D-LED BLU Structure

Second Lens is mainly used to improve LED Package’s lighting angle, with the number of LED Package dropping

largely, it helps the mixing light uniformity between Packages.

Due to the patent and capacity limitations, Second Lens is only adopted by a few clients in the early stage, in addition,

the mounting process to LED Package still sees challenge on yield and the cost and expense would be elevated

initially.

Once it works with the new BLU structural design, Second Lens may be possibly no more needed. For the makers who

are constrained by Second Lens limitations, this would a chance to expand the D-LED Model market share.

Diffuser plate

Second Lens

Structural diffuser plate

LED Package

14 January 2013 | Page 16 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

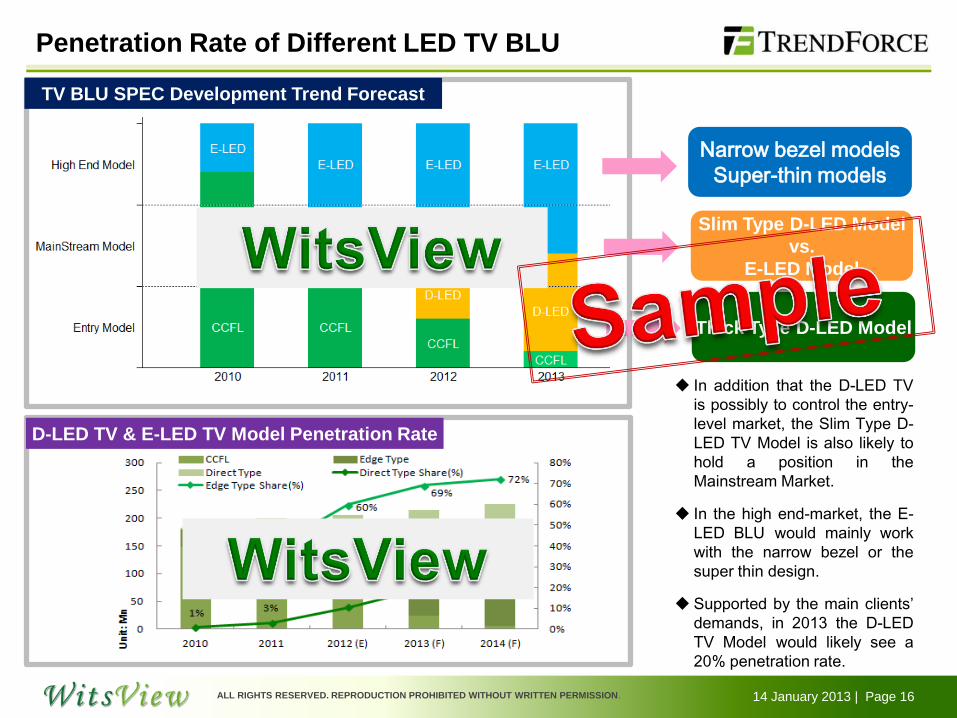

Penetration Rate of Different LED TV BLU

TV BLU SPEC Development Trend Forecast

Narrow bezel models

Super-thin models

Slim Type D-LED Model

vs.

E-LED Model

Thick Type D-LED Model

D-LED TV & E-LED TV Model Penetration Rate

In addition that the D-LED TV

is possibly to control the entry-

level market, the Slim Type D-

LED TV Model is also likely to

hold a position in the

Mainstream Market.

In the high end-market, the E-

LED BLU would mainly work

with the narrow bezel or the

super thin design.

Supported by the main clients’

demands, in 2013 the D-LED

TV Model would likely see a

20% penetration rate.

14 January 2013 | Page 17 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

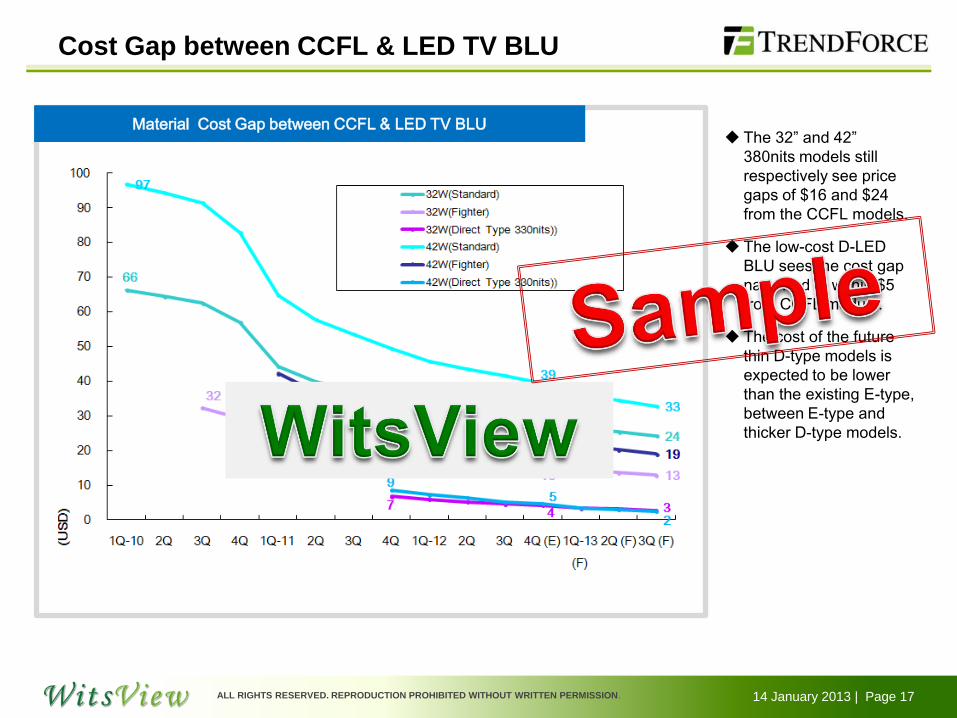

Cost Gap between CCFL & LED TV BLU

Material Cost Gap between CCFL & LED TV BLU The 32” and 42”

380nits models still

respectively see price

gaps of $16 and $24

from the CCFL models.

The low-cost D-LED

BLU sees the cost gap

narrowed to within $5

from CCFL module.

The cost of the future

thin D-type models is

expected to be lower

than the existing E-type,

between E-type and

thicker D-type models.

14 January 2013 | Page 18 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

QoQ changes

LED Lightbar – ASP Trend

LED Lightbar ASP Trend

From the perspective of individual components, LED’s price decline slightly enlarge in Q4, leading to an overall LED

Lightbar price decline of 4~6% expectedly in Q4.

As the Lightbar placement structure has reached maturity, the future main changes would be LED Package, shifted

from mid-power single chip 5630 or mid-power dual chip 7030 to mid-power dual chip 7020, to meet the LGP thickness

requirement developing toward 2mm from 3mm.

14 January 2013 | Page 19 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

Light Guide Plate ASP Trend

Diffuser Plate & Light Guide Plate – ASP Trend

Diffuser Plate ASP Trend

The diffuser plate demand is expected to decline along with the trimming CCFL model proportion, the diffuser plate

price decline is projected to be 1~2% in Q4.

The expectedly growing D-type model volume would compensate the loss from trimming CCFL models, and

manufacturers have chances to develop toward structural diffuser plates with high added values.

At the early stage of LED development, PMMA light guide plate once faced tight supply, leading to makers’ capacity

expansion. But along with LED model penetration rate raising slowly and the showcase of the new D-LED model,

PMMA light guide plate capacity sees risks of oversupply, and the Q4’12 PMMA light guide plate sees price drop

around 2~3%.

14 January 2013 | Page 20 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

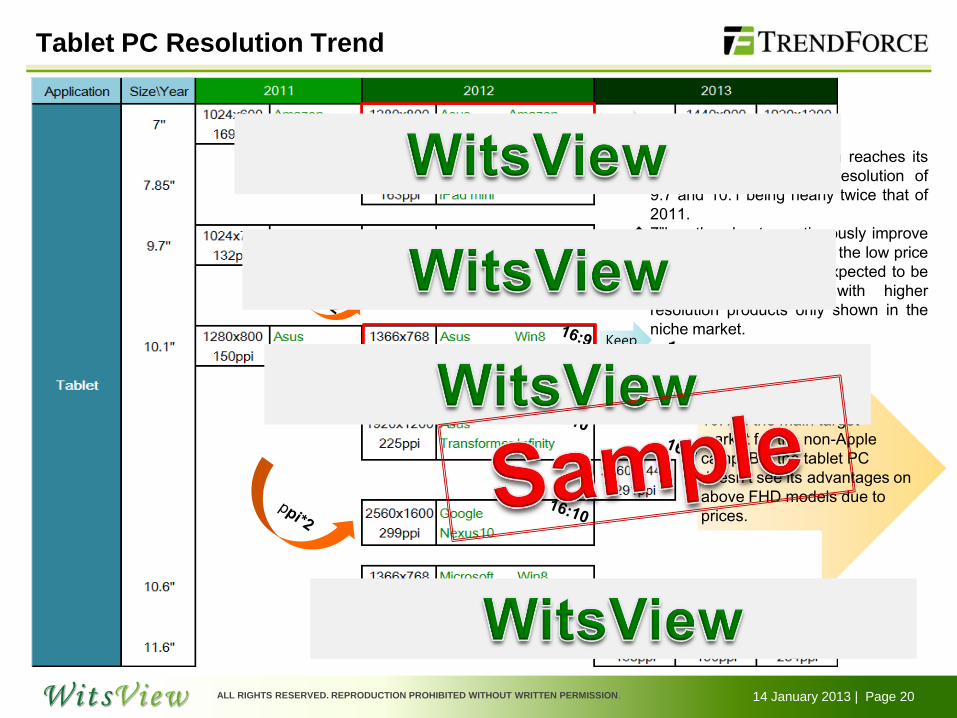

Tablet PC Resolution Trend

Keep

Keep

The lift of tablet resolution reaches its

peak in 2012 with the resolution of

9.7”and 10.1”being nearly twice that of

2011.

7”has the plan to continuously improve

resolution but is limited by the low price

trend. The 1280x800 is expected to be

mainstream in 2013 with higher

resolution products only shown in the

niche market.

10.1”is the main target

market for the non-Apple

camp. But the tablet PC

doesn’t see its advantages on

above FHD models due to

prices.

14 January 2013 | Page 21 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

Notebook Resolution Trend

NB doesn’t see many changes on resolution but mainly the changes on thickness, weight, power-consumption under the

same resolution.

The lifted resolution brings challenges to panel makers’ yields and costs, in the condition that NB prices see increases

difficultly , QHD high resolution is only expected on a few high-end NB models in 2013.

Panels carrying above

FHD resolutions are

developed only by

a few makers and didn’t

stimulate the market.

Macbook pro 13.3”2560x1600 16:10 227ppi

15.6”2880x1800 16:10 217ppi

Apple has extended the high resolution issue to the

NB market , launching the Retina display NB at

relatively high price.

14 January 2013 | Page 22 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

MNT & TV Resolution Trend

High resolution trend is

extended to TV market.

iMac FHD remains the

mainstream resolution.

Currently the monitor market

shows stagnant growth. Since

higher specification equals

higher price, the monitor lacks

the incentive to lift resolution.

14 January 2013 | Page 23 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

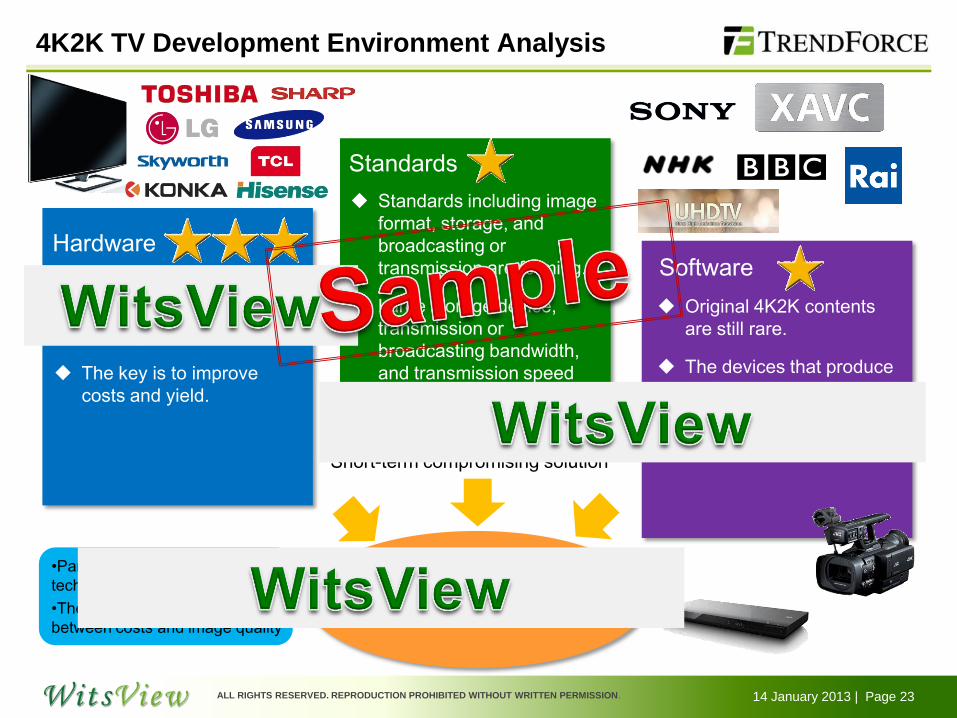

4K2K TV Development Environment Analysis

Hardware

Standards

Software Panels: makers are active

on 4K2K product

development.

The key is to improve

costs and yield.

Original 4K2K contents

are still rare.

The devices that produce

4K2K contents such as

cameras must be

common.

4K2K image transformation solution

built at system end or panel end??

Standards including image

format, storage, and

broadcasting or

transmission are forming.

Large storage device,

transmission or

broadcasting bandwidth,

and transmission speed

would be the future keys

to developments.

•Panel makers hold key

technologies

•There will be some trade-off

between costs and image quality

Short-term compromising solution

14 January 2013 | Page 24 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

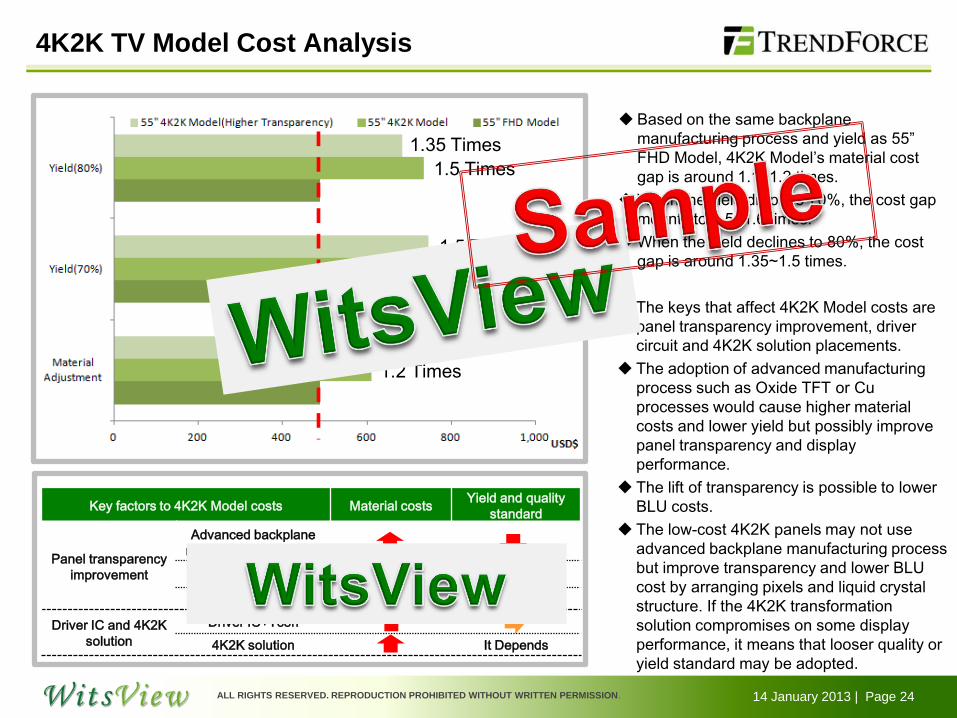

4K2K TV Model Cost Analysis

1.2 Times

1.1 Times

1.6 Times

1.5 Times

1.5 Times

1.35 Times

Based on the same backplane

manufacturing process and yield as 55”

FHD Model, 4K2K Model’s material cost

gap is around 1.1~1.2 times.

When the yield drops to 70%, the cost gap

mounts to 1.5~1.6 times.

When the yield declines to 80%, the cost

gap is around 1.35~1.5 times.

Key factors to 4K2K Model costs Material costs Yield and quality

standard

Panel transparency

improvement

Advanced backplane

manufacturing process

Pixel and LC structure

BLU cost

Driver IC and 4K2K

solution

Driver IC+Tcon

4K2K solution It Depends

The keys that affect 4K2K Model costs are

panel transparency improvement, driver

circuit and 4K2K solution placements.

The adoption of advanced manufacturing

process such as Oxide TFT or Cu

processes would cause higher material

costs and lower yield but possibly improve

panel transparency and display

performance.

The lift of transparency is possible to lower

BLU costs.

The low-cost 4K2K panels may not use

advanced backplane manufacturing process

but improve transparency and lower BLU

cost by arranging pixels and liquid crystal

structure. If the 4K2K transformation

solution compromises on some display

performance, it means that looser quality or

yield standard may be adopted.

14 January 2013 | Page 25 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

Outline

IV. Mainstream Size Panel Cost

14 January 2013 | Page 26 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

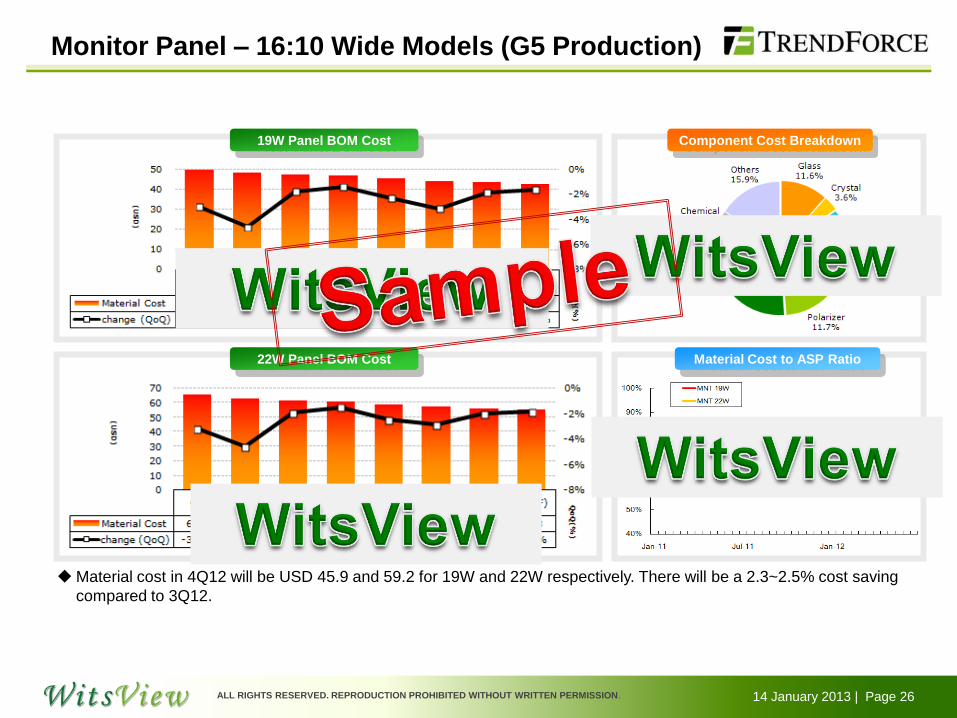

Monitor Panel – 16:10 Wide Models (G5 Production)

Component Cost Breakdown 19W Panel BOM Cost

22W Panel BOM Cost Material Cost to ASP Ratio

Material cost in 4Q12 will be USD 45.9 and 59.2 for 19W and 22W respectively. There will be a 2.3~2.5% cost saving

compared to 3Q12.

14 January 2013 | Page 27 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

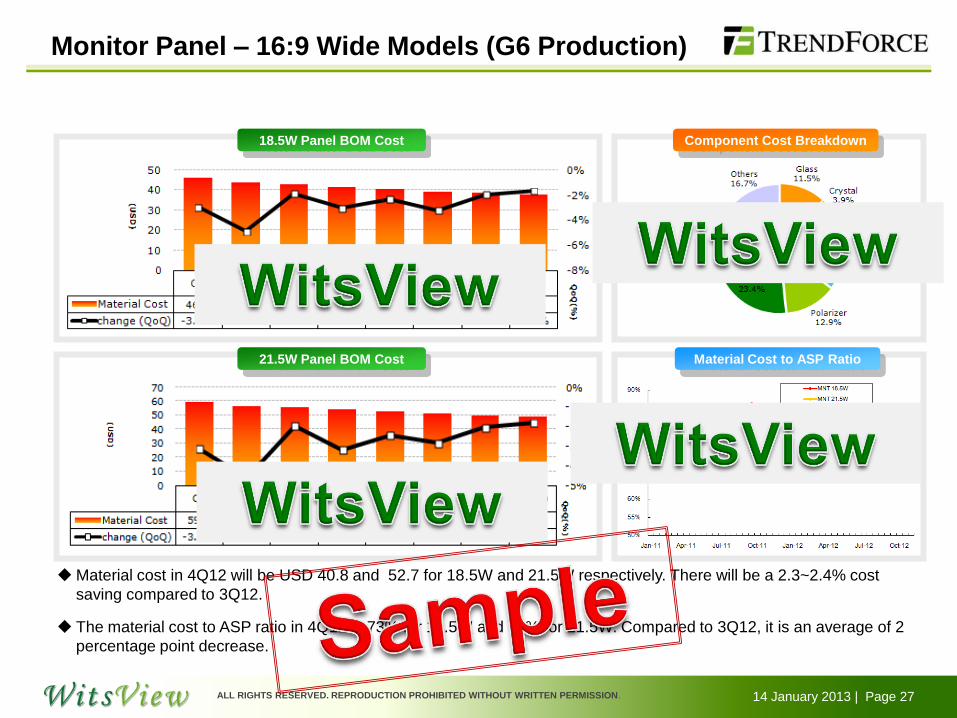

Monitor Panel – 16:9 Wide Models (G6 Production)

Component Cost Breakdown 18.5W Panel BOM Cost

21.5W Panel BOM Cost Material Cost to ASP Ratio

Material cost in 4Q12 will be USD 40.8 and 52.7 for 18.5W and 21.5W respectively. There will be a 2.3~2.4% cost

saving compared to 3Q12.

The material cost to ASP ratio in 4Q12 is 73% for 18.5W and 70% for 21.5W. Compared to 3Q12, it is an average of 2

percentage point decrease.

14 January 2013 | Page 28 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

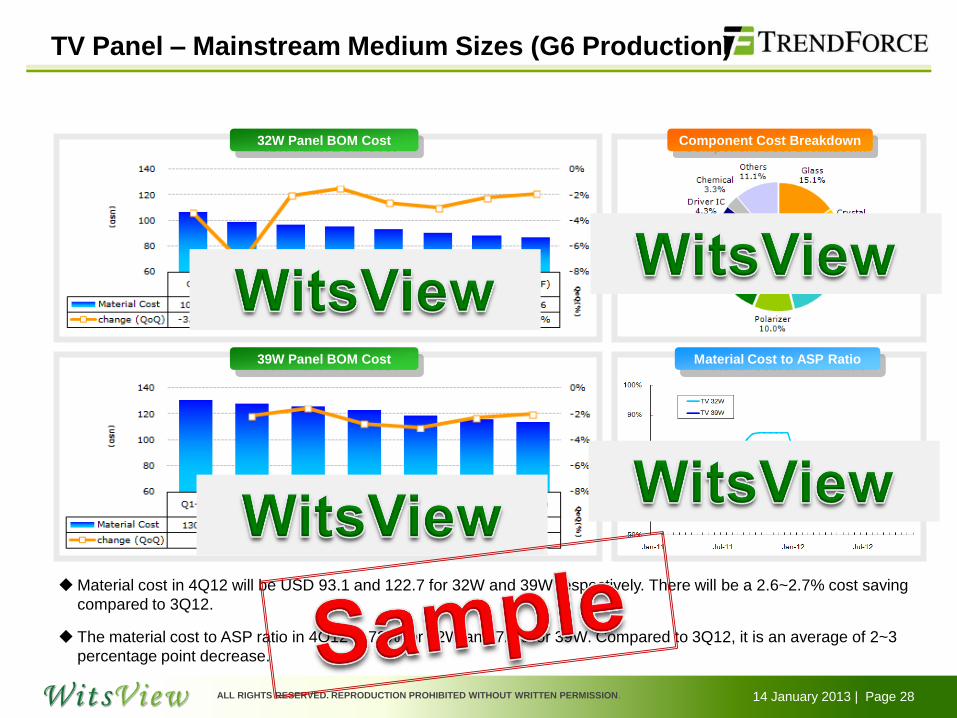

TV Panel – Mainstream Medium Sizes (G6 Production)

Component Cost Breakdown 32W Panel BOM Cost

39W Panel BOM Cost Material Cost to ASP Ratio

Material cost in 4Q12 will be USD 93.1 and 122.7 for 32W and 39W respectively. There will be a 2.6~2.7% cost saving

compared to 3Q12.

The material cost to ASP ratio in 4Q12 is 72% for 32W and 72% for 39W. Compared to 3Q12, it is an average of 2~3

percentage point decrease.

14 January 2013 | Page 29 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

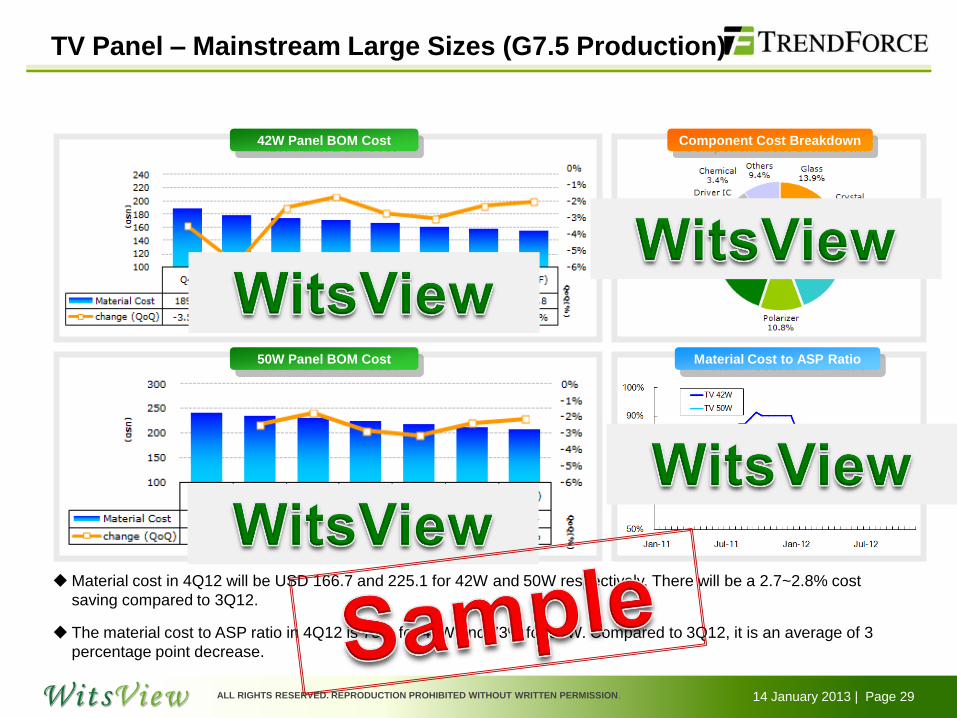

TV Panel – Mainstream Large Sizes (G7.5 Production)

Component Cost Breakdown

50W Panel BOM Cost

42W Panel BOM Cost

Material Cost to ASP Ratio

Material cost in 4Q12 will be USD 166.7 and 225.1 for 42W and 50W respectively. There will be a 2.7~2.8% cost

saving compared to 3Q12.

The material cost to ASP ratio in 4Q12 is 75% for 42W and 73% for 50W. Compared to 3Q12, it is an average of 3

percentage point decrease.

14 January 2013 | Page 30 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

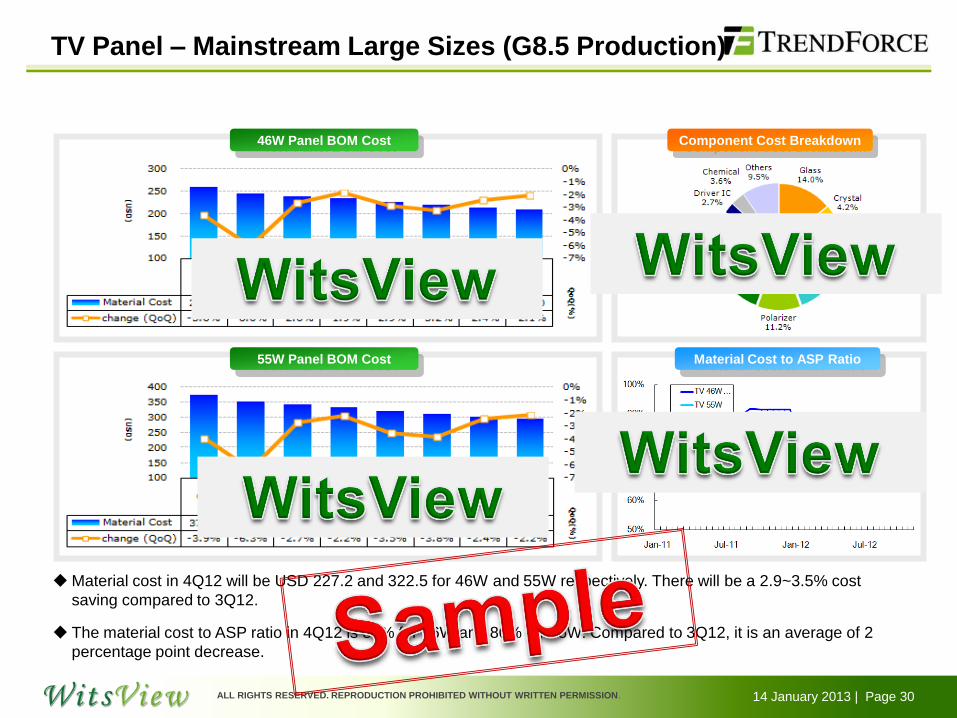

TV Panel – Mainstream Large Sizes (G8.5 Production)

Component Cost Breakdown

55W Panel BOM Cost

46W Panel BOM Cost

Material Cost to ASP Ratio

Material cost in 4Q12 will be USD 227.2 and 322.5 for 46W and 55W respectively. There will be a 2.9~3.5% cost

saving compared to 3Q12.

The material cost to ASP ratio in 4Q12 is 81% for 46W and 80% for 55W. Compared to 3Q12, it is an average of 2

percentage point decrease.

14 January 2013 | Page 31 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

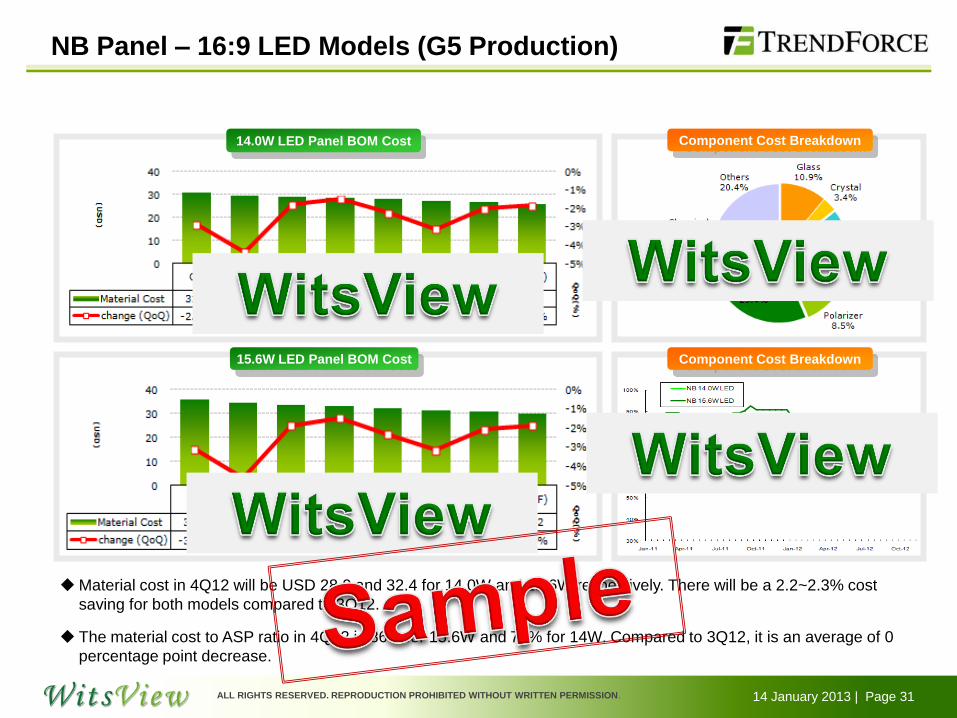

NB Panel – 16:9 LED Models (G5 Production)

Component Cost Breakdown 14.0W LED Panel BOM Cost

15.6W LED Panel BOM Cost Component Cost Breakdown

Material cost in 4Q12 will be USD 28.0 and 32.4 for 14.0W and 15.6W respectively. There will be a 2.2~2.3% cost

saving for both models compared to 3Q12.

The material cost to ASP ratio in 4Q12 is 86% for 15.6W and 77% for 14W. Compared to 3Q12, it is an average of 0

percentage point decrease.

14 January 2013 | Page 32 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

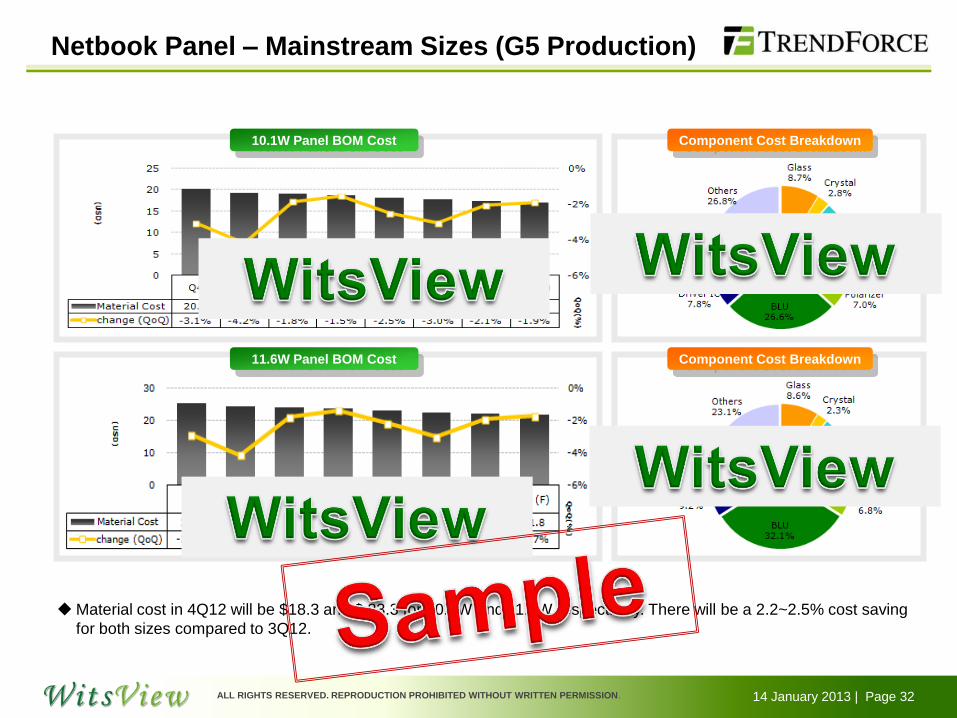

Netbook Panel – Mainstream Sizes (G5 Production)

Component Cost Breakdown

11.6W Panel BOM Cost Component Cost Breakdown

10.1W Panel BOM Cost

Material cost in 4Q12 will be $18.3 and $ 23.3 for 10.1W and 11.6W respectively. There will be a 2.2~2.5% cost saving

for both sizes compared to 3Q12.

14 January 2013 | Page 33 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

Outline

V. Panel Cost Analysis &

Financial Performance Analysis

14 January 2013 | Page 34 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

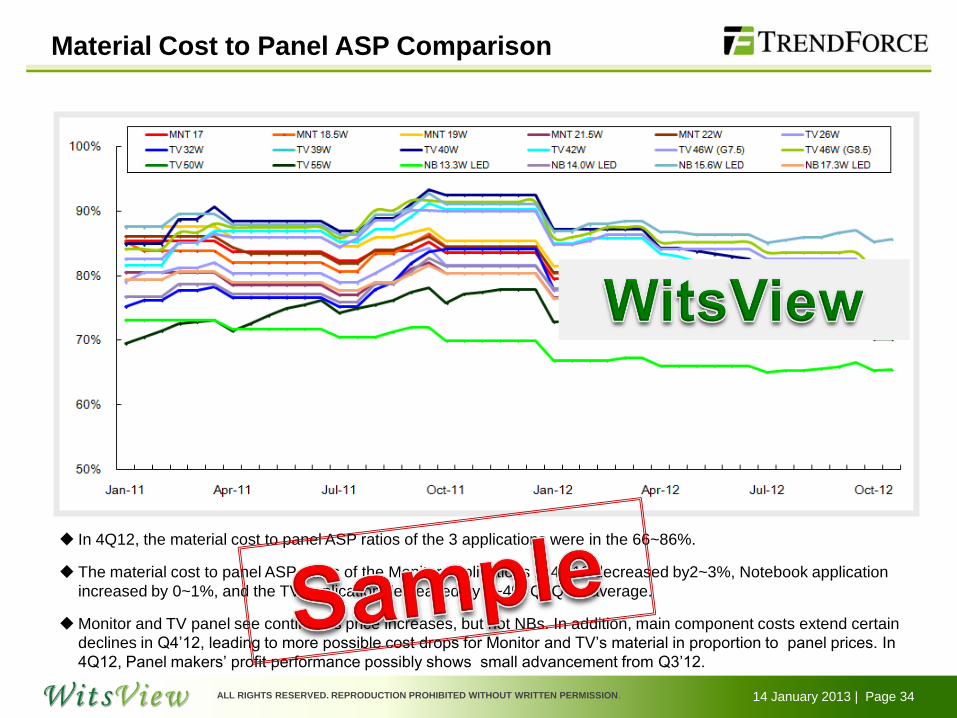

Material Cost to Panel ASP Comparison

In 4Q12, the material cost to panel ASP ratios of the 3 applications were in the 66~86%.

The material cost to panel ASP ratios of the Monitor applications in 4Q12 decreased by2~3%, Notebook application

increased by 0~1%, and the TV application decreased by 2~4% QoQ on average.

Monitor and TV panel see continuous price increases, but not NBs. In addition, main component costs extend certain

declines in Q4’12, leading to more possible cost drops for Monitor and TV’s material in proportion to panel prices. In

4Q12, Panel makers’ profit performance possibly shows small advancement from Q3’12.

14 January 2013 | Page 35 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

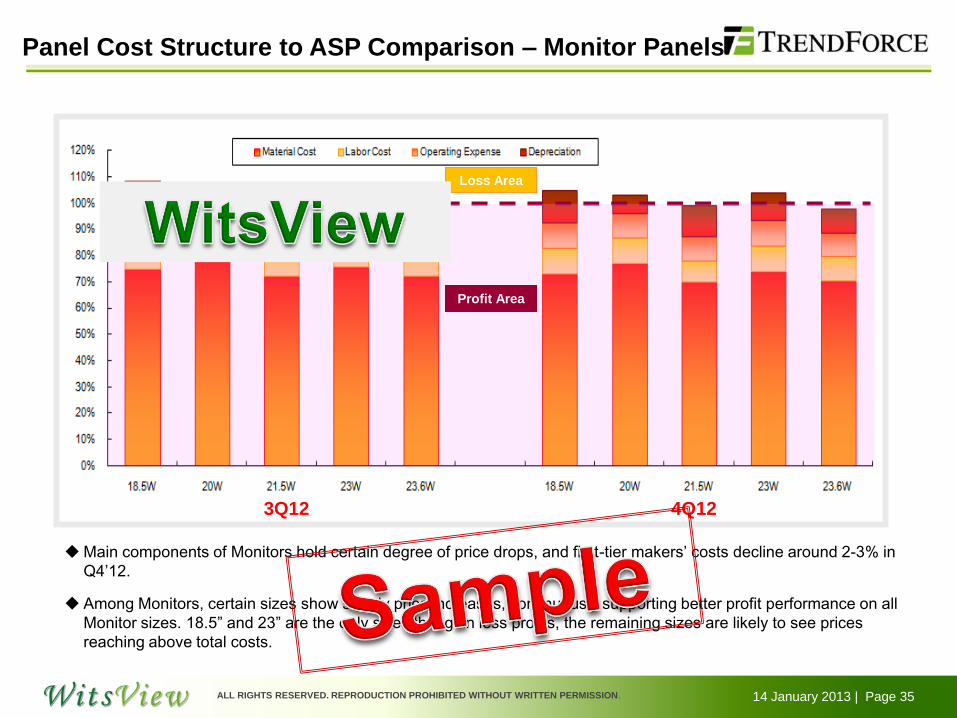

Panel Cost Structure to ASP Comparison – Monitor Panels

3Q12 4Q12

Profit Area

Loss Area

Main components of Monitors hold certain degree of price drops, and first-tier makers’ costs decline around 2-3% in

Q4’12.

Among Monitors, certain sizes show steady price increases, continuously supporting better profit performance on all

Monitor sizes. 18.5” and 23” are the only sizes that gain less profits, the remaining sizes are likely to see prices

reaching above total costs.

14 January 2013 | Page 36 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

Panel Cost Structure to ASP Comparison – TV Panels

3Q12 4Q12

Profit Area

Loss Area

In 4Q12, the TV panel cost is expected to decline by 3%-5%, as the price drop of LED BLU component starts to trim,

the decline gaps between LED and CCFL models are small.

TV panel price begins to stabilize from Q2’12, and certain sizes such as 32” and 42” see prices lifting, leading to a

further profit improvement on TV products with main sizes’ prices climbing back above cash costs.

14 January 2013 | Page 37 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

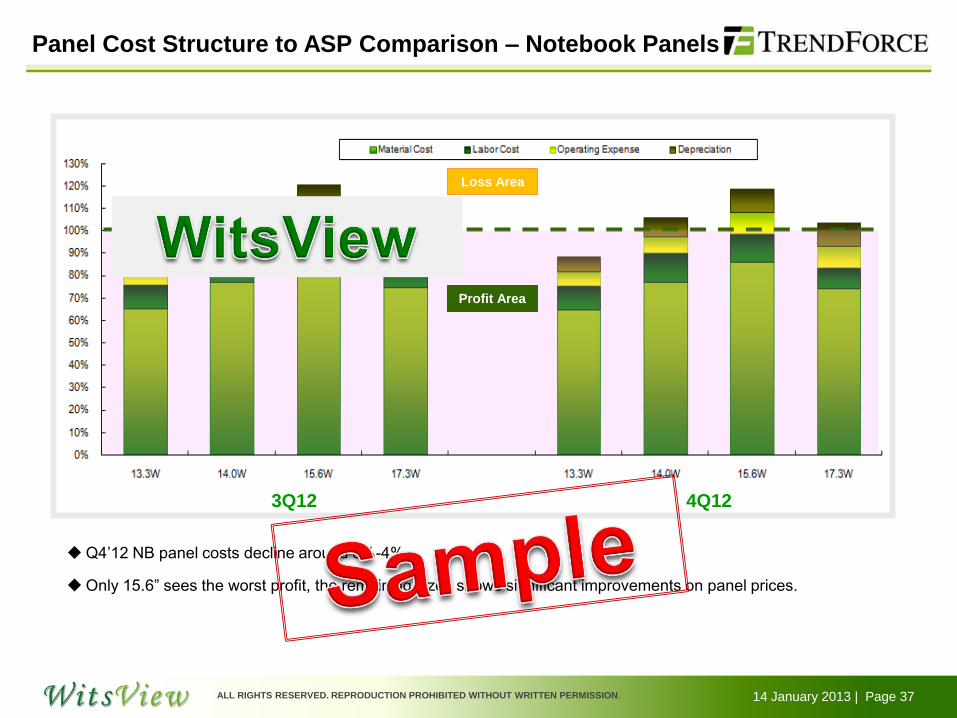

Panel Cost Structure to ASP Comparison – Notebook Panels

3Q12 4Q12

Profit Area

Loss Area

Q4’12 NB panel costs decline around 3%-4%.

Only 15.6” sees the worst profit, the remaining sizes shows significant improvements on panel prices.

14 January 2013 | Page 38 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

Outline

VI. Large Size LCD Panel Supply

14 January 2013 | Page 39 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

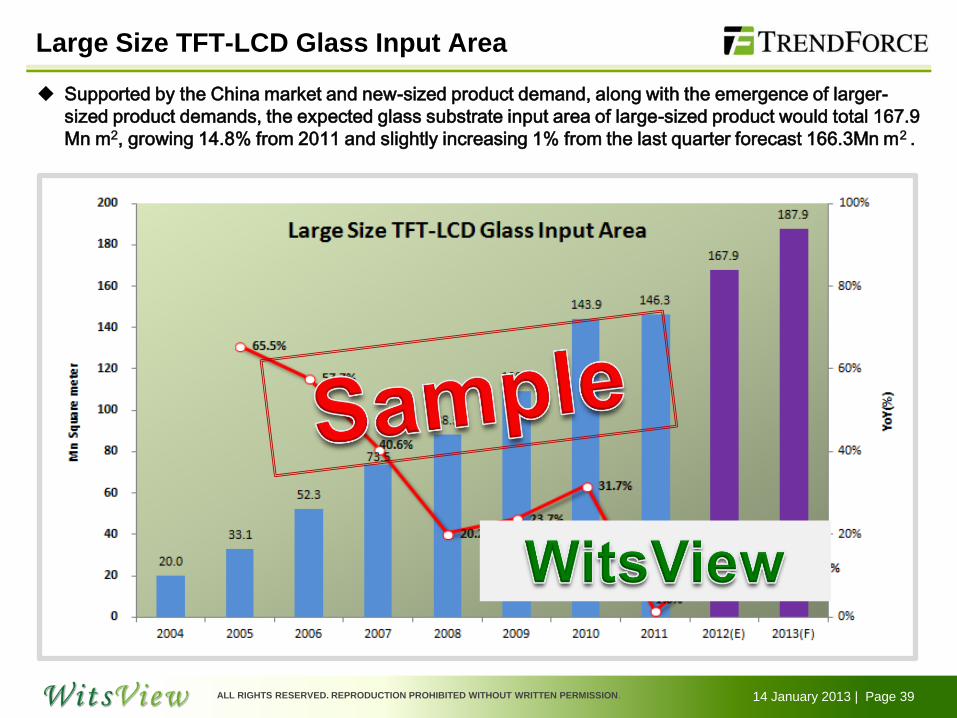

Supported by the China market and new-sized product demand, along with the emergence of larger-

sized product demands, the expected glass substrate input area of large-sized product would total 167.9

Mn m2, growing 14.8% from 2011 and slightly increasing 1% from the last quarter forecast 166.3Mn m2 .

Large Size TFT-LCD Glass Input Area

14 January 2013 | Page 40 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

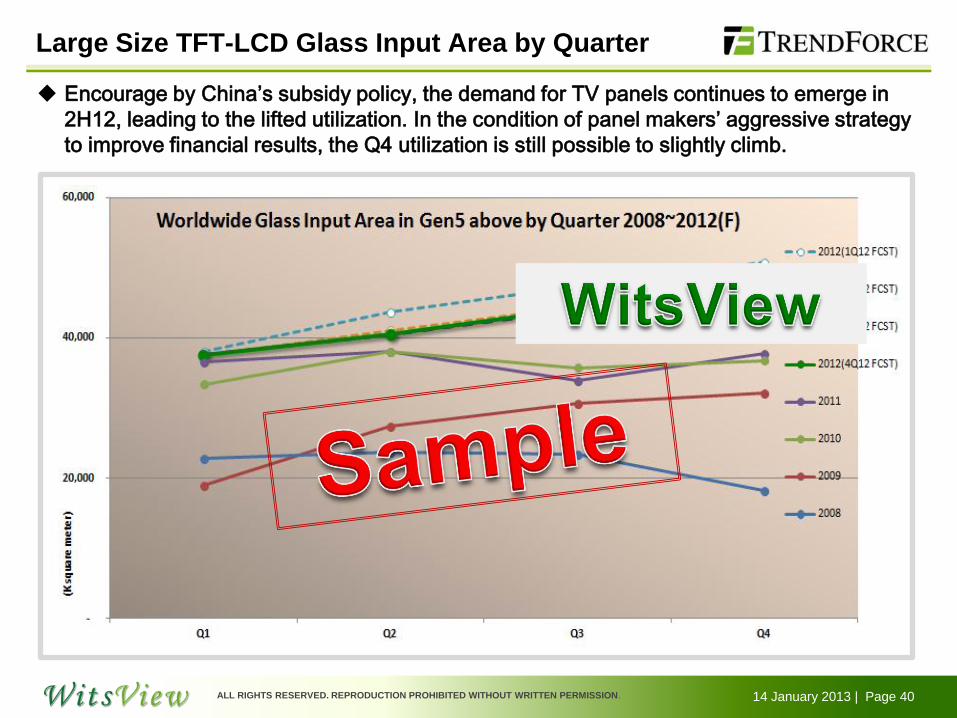

Encourage by China’s subsidy policy, the demand for TV panels continues to emerge in

2H12, leading to the lifted utilization. In the condition of panel makers’ aggressive strategy

to improve financial results, the Q4 utilization is still possible to slightly climb.

Large Size TFT-LCD Glass Input Area by Quarter

14 January 2013 | Page 41 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

Glass Input Area Trend

-22%

+4%

+5%

+4%

+3% -0.5% +11% -0.4%

+3%

Based on the observation of Q4’s growing tend from Q3, Q1 would show small decline.

From the view of largely rising input area in 2H12, the Q1’13 demand would noticeably weaken.

If panel makers wish to maintain high utilization to gain cost advantages, utilization drops may not be

obvious.

14 January 2013 | Page 42 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

WW UT by Generation

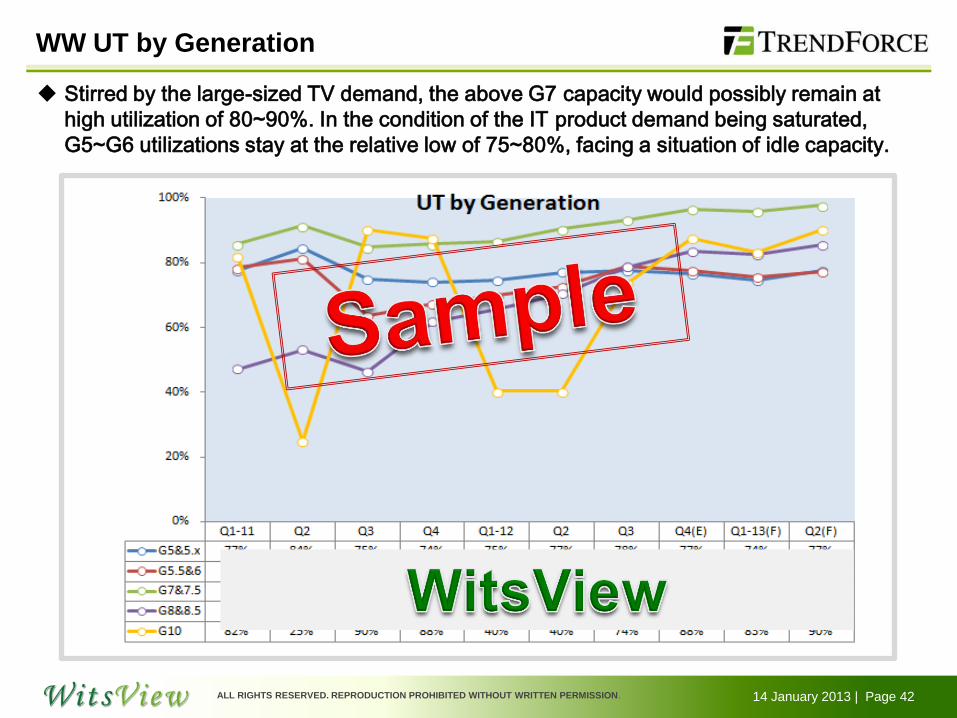

Stirred by the large-sized TV demand, the above G7 capacity would possibly remain at

high utilization of 80~90%. In the condition of the IT product demand being saturated,

G5~G6 utilizations stay at the relative low of 75~80%, facing a situation of idle capacity.

14 January 2013 | Page 43 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

Capacity Loss Forecast in 2013

IPS/FFS, Touch, LTPS

IPS/FFS, LTPS

IPS/FFS,

Slim Glass Substrate

Slim Glass Substrate,

Oxide TFT

-8.8%

-8.7%

-1.3%

-4.3% -5.2%

G5.x

G5.5&G6

G7&G7.5

G8 & above

2013 Capacity Loss Forecast

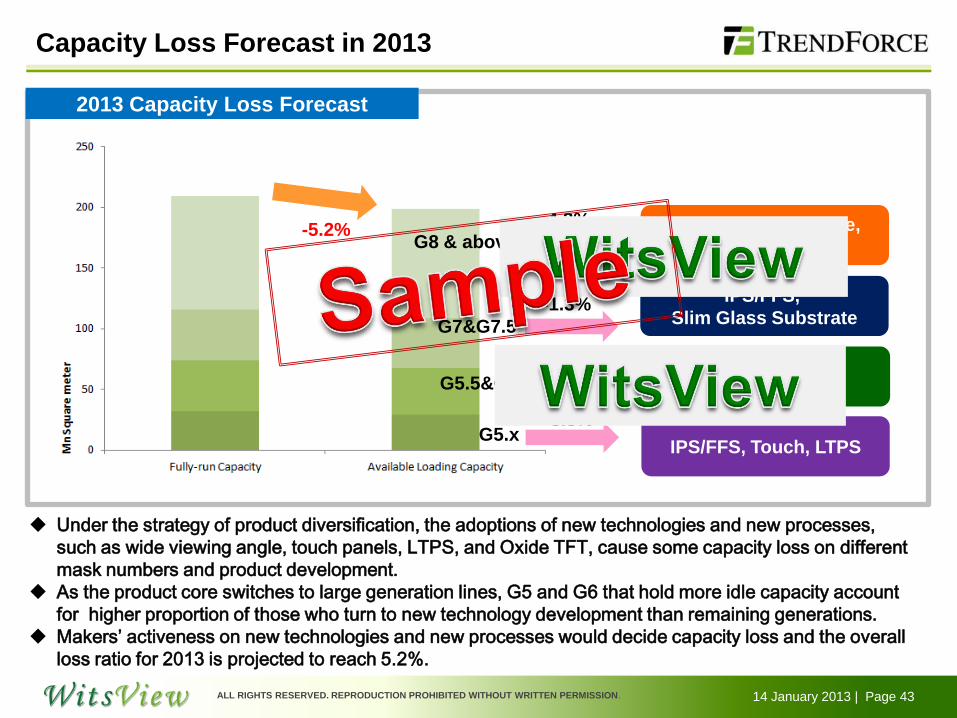

Under the strategy of product diversification, the adoptions of new technologies and new processes,

such as wide viewing angle, touch panels, LTPS, and Oxide TFT, cause some capacity loss on different

mask numbers and product development.

As the product core switches to large generation lines, G5 and G6 that hold more idle capacity account

for higher proportion of those who turn to new technology development than remaining generations.

Makers’ activeness on new technologies and new processes would decide capacity loss and the overall

loss ratio for 2013 is projected to reach 5.2%.

14 January 2013 | Page 44 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

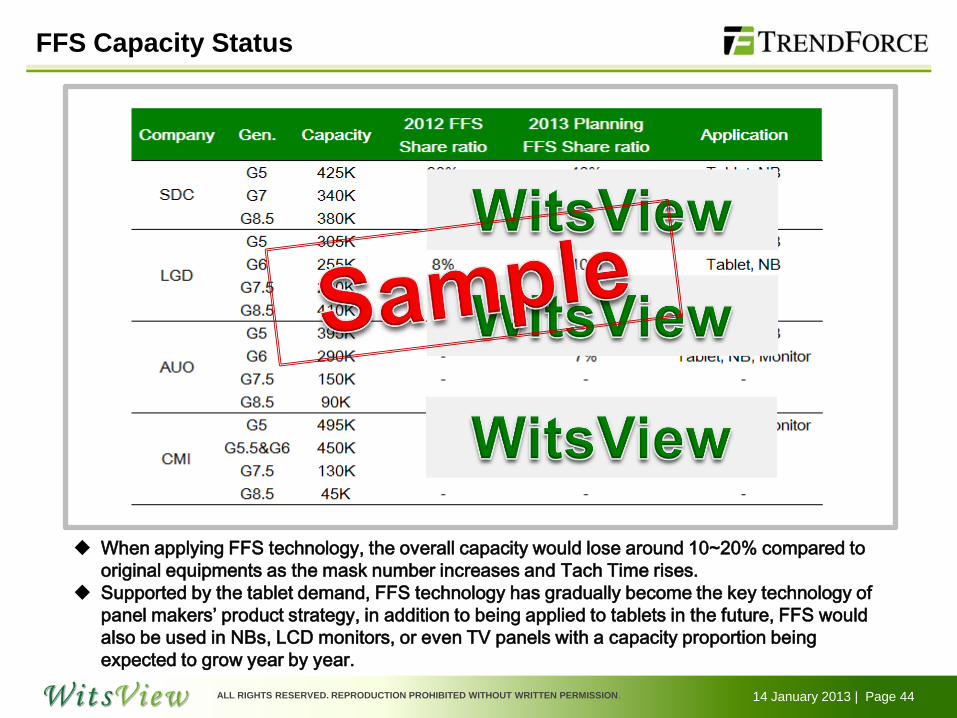

FFS Capacity Status

When applying FFS technology, the overall capacity would lose around 10~20% compared to

original equipments as the mask number increases and Tach Time rises.

Supported by the tablet demand, FFS technology has gradually become the key technology of

panel makers’ product strategy, in addition to being applied to tablets in the future, FFS would

also be used in NBs, LCD monitors, or even TV panels with a capacity proportion being

expected to grow year by year.

14 January 2013 | Page 45 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

Outline

VII. Conclusion

14 January 2013 | Page 46 ALL RIGHTS RESERVED. REPRODUCTION PROHIBITED WITHOUT WRITTEN PERMISSION.

Conclusion

As the demand for large-sized product increasingly grows, the area demand rises at the same time. For certain main

component suppliers that have no capacity expansion plans, they feel the gap between demand and supply obviously

trimming, and once the demand heats up, the demand and supply situation for some components is expected to be tight in

2013. Besides, how the adoptions of new materials such as new polarizer, structural diffuser plates help quotation to gain

cost advantages or change the upstream supply chain is also a key point to be observed on main component development

in 2013.

Due to the capacity limitation on key materials, the low-cost D-LED model development is not as good as expected in 2012,

only strongly promoted by the first-tier makers. Currently E-LED models show cost advantages with lower specifications.

Looking ahead to 2013, the successful launch of thin D-LED model depends not only on the industrial design that is close

to the E-LED Model but also if the quotation and price are appealing enough to compete with E-LED Model for the

mainstream position. This would be a key point to decide if the D-LED Model has chances to enlarge the market share.

As the hardware key technology is at the panel end, and 4K2K model development depends on panel makers’ activeness,

it may be the short term development direction for 4K2K model that panel end applies the solution of 4K2K signal

transformation which show lower display performance and cheaper prices.

As prices and shipments grow, panel makers’ profit performances improved largely in Q3’12. The utilization would remain

elevated with the Q4’12 demand remaining strong, in addition, panel makers tend to maintain utilization as high as possible

to improve profits. As a result, the utilization wouldn’t show noticeable decline through Q4’12 to Q1’13.

To lift the utilization continuously means to increase capacity and that implies a rising level of panel makers and clients’

inventory. When observing 2H12, the input area grew largely and clients’ overstocking was obvious, leading to a

reasonable expectation that the Q1’13 utilization must be obviously revised. If panel makers’ operation remains unchanged,

clients would need more time to digest the inventory and the panel demand would trim largely in 2H13.

Panel makers devote actively to the developments of new processes and new technologies and use the existing capacity

for transformation, meaning a certain degree of capacity loss. When observing conditions of all generation lines, G5-G6 see

idle capacity with weaker IT product demand, and G7-G8 see tighter capacity with strong TV product demand. But large-

sized panel demand cannot be shifted to G5-G6, and G5-G6 must make products with higher values such as high

resolution panels, wide viewing angle panels. How panel makers make good use of G5-G6 capacity is a key point to

observe in 2013.