temasek review 2014- our journey has just begun (media conference presentation)

TRANSCRIPT

Tuesday, 8 July 2014

Our journey has just begun

Forward Looking

Institution

Trusted Steward

Active Investor

Tuesday, 8 July 2014

Our journey has just begun

4

Portfolio Value since Inception

Resilient Portfolio

1 Incorporation of Temasek on 25 June 1974. 2 Financial year 75 began 25 June 1974 and ended 31 December 1975. 3 Financial year-end was changed from 31 December before 1993 to 31 March from 1994 onwards. 4 FRS39 Financial Instruments: Recognition and Measurement, introduced during year ended 31 March 2006, requires available-for-sale financial assets to be

measured at fair value.

223

187

172

S$b

5

Long Term Returns to Shareholder

16% Compounded Annualised S$ Return since Inception

18

16

7

12

15

4

16

14

6

9

11

4

2

TSR1 in US$ (%) TSR1 in S$ (%)

Period (in years)

Since inception

(1974)

30

20

10

5

3

1

(as at 31 March 2014) 1 Total Shareholder Return

0

6

One, 10, & 20-Year S$ Returns to Shareholder

Stable Long Term Performance

Rolling TSR (%)

20-year

10-year

One-year

18 16 18 17

13 16 15 15 14

6 5 6 8 10

6 6 9 10 13 9

16

25 27

7

(30)

43

5 1

9

2

05 06 07 08 09 10 11 12 13 14(as at 31 March)

7

16

14

6

9

11

4

2

9

9

9

9

9

8

8

TSR and Risk-Adjusted Cost of Capital

S$ Total Shareholder Return (TSR) and Risk-adjusted Hurdle Rate (%)

Since inception (1974)

TSR in S$ terms

Risk-adjusted hurdle rate

Period (in years)

20

30

1

3

5

10

(as at 31 March 2014)

8

16

14

6

9

11

2

8

6

5

9

16

(1)

4

7

12

4

9

8

6

4

15

21

TSR and MSCI Indices

N/A

N/A

20

30

1

Since inception (1974)

5

10

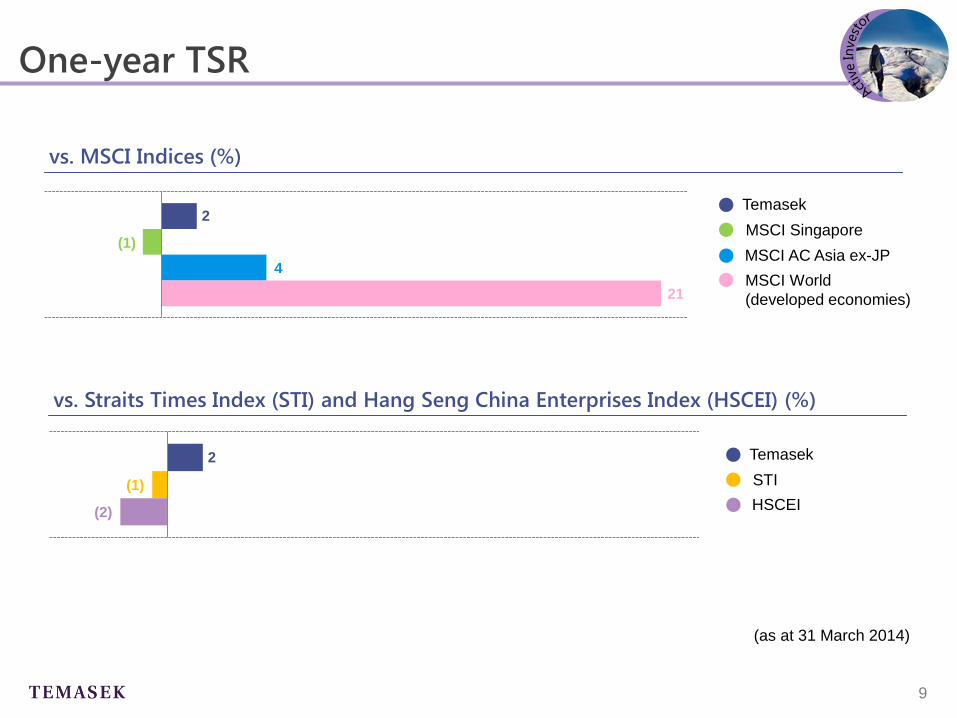

Temasek

MSCI Singapore

MSCI AC Asia ex-JP

MSCI World

(developed economies)

Period (in years)

(as at 31 March 2014)

S$ Total Shareholder Return (TSR) and MSCI Indices (%)

9

One-year TSR

vs. MSCI Indices (%)

(as at 31 March 2014)

2

(1)

4

21

2

(1)

(2)

Temasek

STI

HSCEI

Temasek

MSCI Singapore

MSCI AC Asia ex-JP

MSCI World

(developed economies)

vs. Straits Times Index (STI) and Hang Seng China Enterprises Index (HSCEI) (%)

10

Group Income Statements

Steady Group Net Profit

(S$b)

For year ended 31 Mar 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Revenue 67.5 79.8 74.6 83.3 79.6 76.7 83.5 83.5 83.8 81.1

Profit before income tax 12.2 19.0 14.3 25.5 10.4 8.5 17.8 14.8 15.2 15.8

Profit attributable to equity

holder of the Company 7.5 12.8 9.1 18.2 6.2 4.6 12.7 10.7 10.6 10.9

8

11 13

5 6

18

9

13 11 11

11

(S$b)

As at 31 Mar 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Total assets 199.1 213.7 242.4 295.5 247.9 284.8 297.9 302.6 317.4 319.0

Shareholder equity

before fair value

reserve

70.9 83.6 92.9 120.2 119.9 127.8 134.6 146.4 155.9 172.4

Fair value reserve1 - 7.0 21.1 23.9 (1.5) 21.9 20.9 11.8 13.2 14.9

Shareholder equity 70.9 90.6 114.0 144.1 118.4 149.7 155.5 158.2 169.1 187.3

Net debt2 26.9 16.7 23.6 33.8 22.1 17.8 9.5 16.1 13.3 3.7

Group Balance Sheets

Strong Foundation Built Over Decades

1 FRS39 Financial Instruments: Recognition and Measurement, introduced during year ended 31 March 2006, requires available-for-sale financial

assets to be measured at fair value. 2 Total debt less cash and cash equivalents.

Steady growth Group Shareholder Equity: S$187b

Up S$18b

from last year

12

(S$b)

As at 31 Mar 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Total assets 199.1 213.7 242.4 295.5 247.9 284.8 297.9 302.6 317.4 319.0

Shareholder equity

before fair value

reserve

70.9 83.6 92.9 120.2 119.9 127.8 134.6 146.4 155.9 172.4

Fair value reserve1 - 7.0 21.1 23.9 (1.5) 21.9 20.9 11.8 13.2 14.9

Shareholder equity 70.9 90.6 114.0 144.1 118.4 149.7 155.5 158.2 169.1 187.3

Net debt2 26.9 16.7 23.6 33.8 22.1 17.8 9.5 16.1 13.3 3.7

Full financial flexibility Temasek ended the year in a net cash position

Group Balance Sheets

Strong Foundation Built Over Decades

1 FRS39 Financial Instruments: Recognition and Measurement, introduced during year ended 31 March 2006, requires available-for-sale financial

assets to be measured at fair value. 2 Total debt less cash and cash equivalents.

Modest one-year returns

Robust longer term returns

Opportunities ahead

Full flexibility with strong

balance sheet and liquidity

14

Investment Themes

Growing

Middle Income

Populations

Transforming

Economies

Deepening

Comparative

Advantages

Emerging

Champions

emphasise future

long term trends

15

Investment Themes

Strong home base, at inflexion points

Tapping potential of transforming economies

Leveraging growing consumer demands

Economies, businesses with distinctive edge

Growing

Middle Income

Populations

Transforming

Economies

Deepening

Comparative

Advantages

Emerging

Champions

16

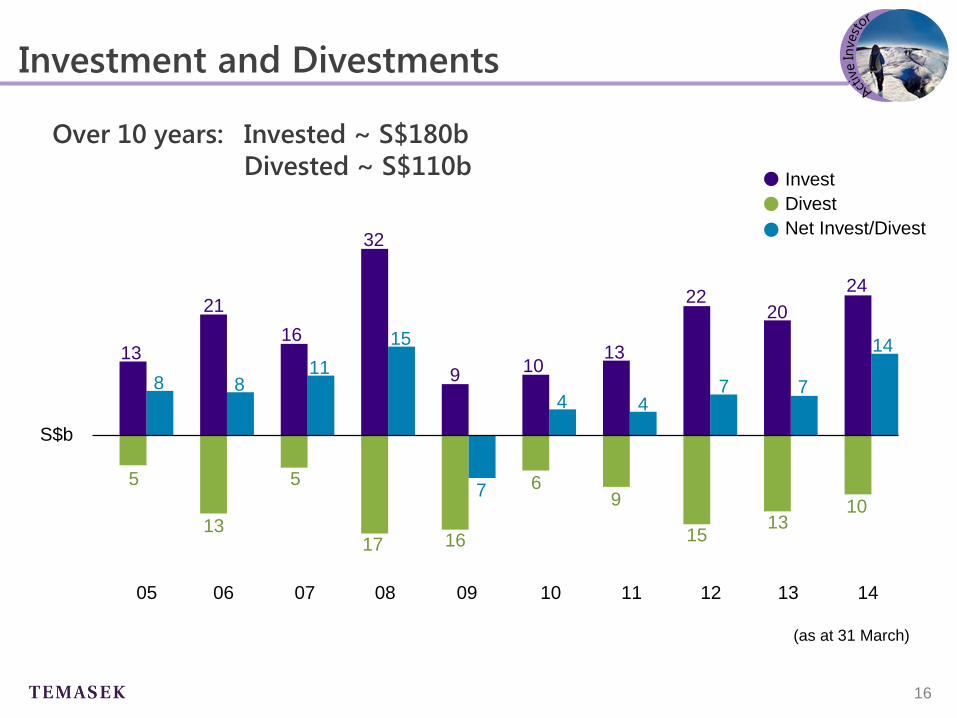

Investment and Divestments

10 11 14 13 12 09 08 07 05 06

Invest

Net Invest/Divest

Divest

5

13

5

17 16

6 9

15 13

13

21

16

32

9 10

13

22 20

S$b

(as at 31 March)

10

24

8 8 11

15

4 4 7 7

14

7

Over 10 years: Invested ~ S$180b

Divested ~ S$110b

17

Active Investor

Invested

S$24b

Divested

S$10b

Post

Mar 2014

Investments

18

41

31

14

10

2 2

Geographic Mix

Asia weighted portfolio at 72%

(%) 2014 2013

Asia ex-Singapore 41 41

Singapore 31 30

North America & Europe 14 12

Australia & New Zealand 10 13

Latin America 2 2

Africa, Central Asia

& the Middle East 2 2

Note: Distribution based on underlying assets. (as at 31 March)

S$223b 31 Mar 14

19

41

31

14

10

2 2

Geographic Mix

60:40 exposure to mature : growth

(%) 2014 2013

Asia ex-Singapore 41 41

Singapore 31 30

North America & Europe 14 12

Australia & New Zealand 10 13

Latin America 2 2

Africa, Central Asia

& the Middle East 2 2

Growth regions – 40%

Mature economies – 60%

Note: Distribution based on underlying assets. (as at 31 March)

60%

40%

20

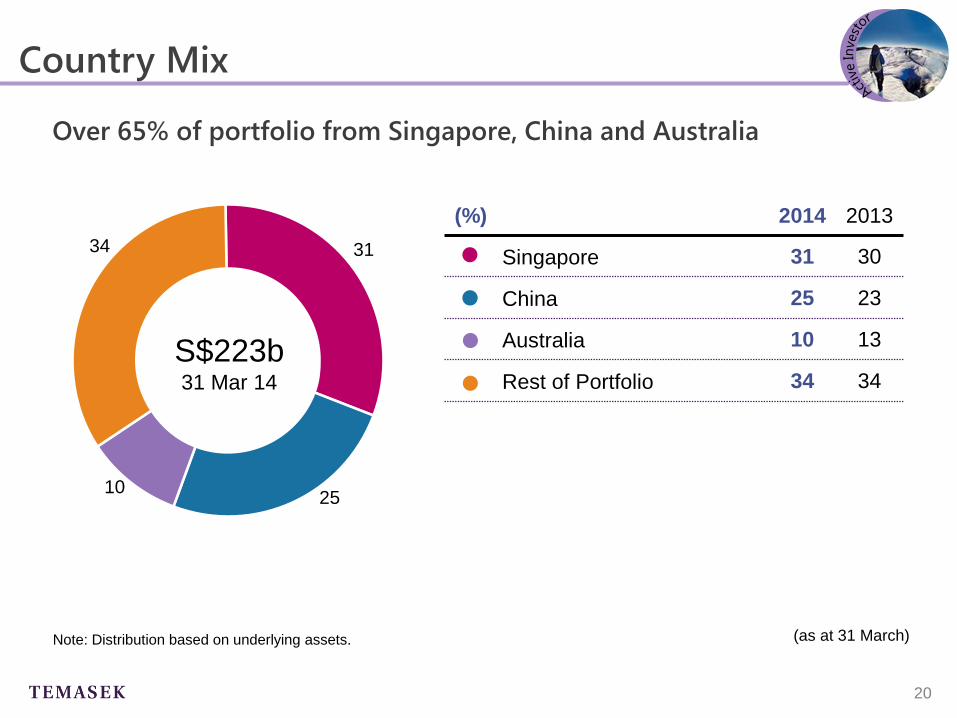

Country Mix

Over 65% of portfolio from Singapore, China and Australia

31

25 10

34

(%) 2014 2013

Singapore 31 30

China 25 23

Australia 10 13

Rest of Portfolio 34 34

S$223b 31 Mar 14

(as at 31 March) Note: Distribution based on underlying assets.

21

Sector Mix

Tracking growth opportunities

30

23

20

14

6

7 (%) 2014 2013

Financial Services 30 31

Telecommunications,

Media & Technology 23 24

Transportation & Industrials 20 20

Life Sciences, Consumer &

Real Estate 14 12

Energy & Resources 6 6

Others 7 7

Note: Distribution based on underlying assets.

S$223b 31 Mar 14

(as at 31 March)

22

Liquidity

A liquid portfolio with full flexibility

36

34

30

(%) 2014 2013

Liquid & sub-20%

listed assets 36 35

Listed large blocs

(≥ 20%share) 34 38

Unlisted assets 30 27 S$223b 31 Mar 14

(as at 31 March)

23

Currency Mix

Strong base in Singapore

61

12

12

4

3

8 (%) 2014 2013

Singapore dollars 61 65

Hong Kong dollars 12 11

US dollars 12 6

British pounds sterling 4 6

Euros 3 2

Others 8 10

Note: Distribution based on currency of denomination.

S$223b 31 Mar 14

(as at 31 March)

24

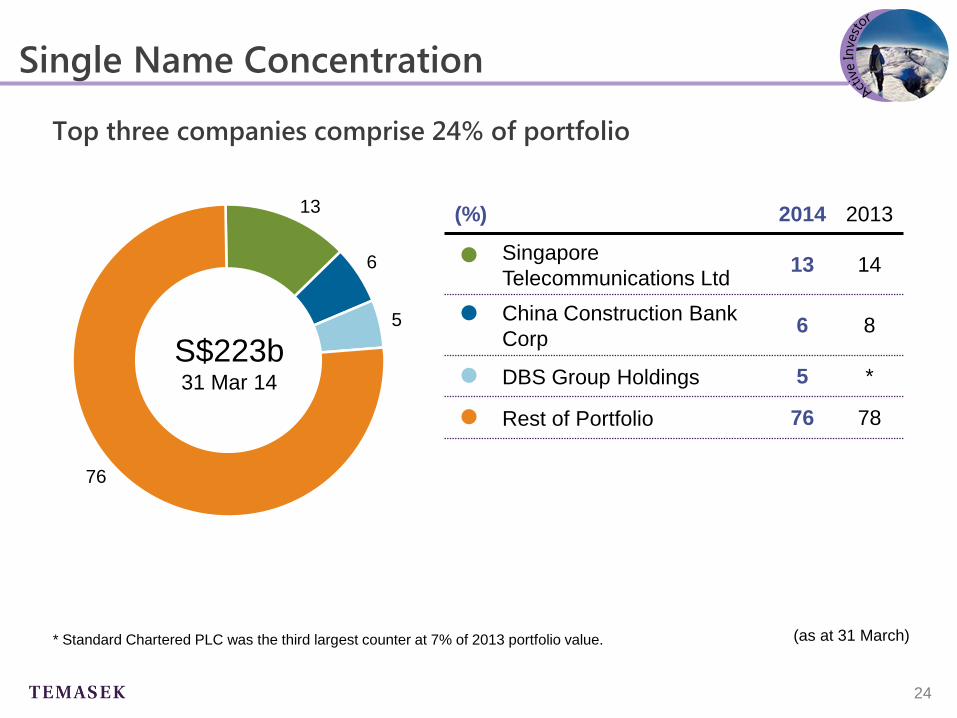

Single Name Concentration

Top three companies comprise 24% of portfolio

13

6

5

76

(%) 2014 2013

Singapore

Telecommunications Ltd 13 14

China Construction Bank

Corp 6 8

DBS Group Holdings 5 *

Rest of Portfolio 76 78

S$223b 31 Mar 14

(as at 31 March) * Standard Chartered PLC was the third largest counter at 7% of 2013 portfolio value.

25

Near Term Global Outlook

Outlook slower-growth environment

26

Near Term Global Outlook

USA on recovery path

global implications of monetary policy

27

Near Term Global Outlook

China slowing growth

potential financial system risks

ample policy room

28

Near Term Global Outlook

Euro zone mixed prospects

uneven reforms

29

Near Term Global Outlook

Global imbalances improving…

30

Near Term Global Outlook

gradual recovery

active year of investment

USA

China

Euro zone

- recovering

- adjusting

- mixed

31

Opportunities

Asia-focused

North America and Europe – Recovering

Innovation –

Partnership for growth

Energy

Life sciences

Consumer

Technology

32

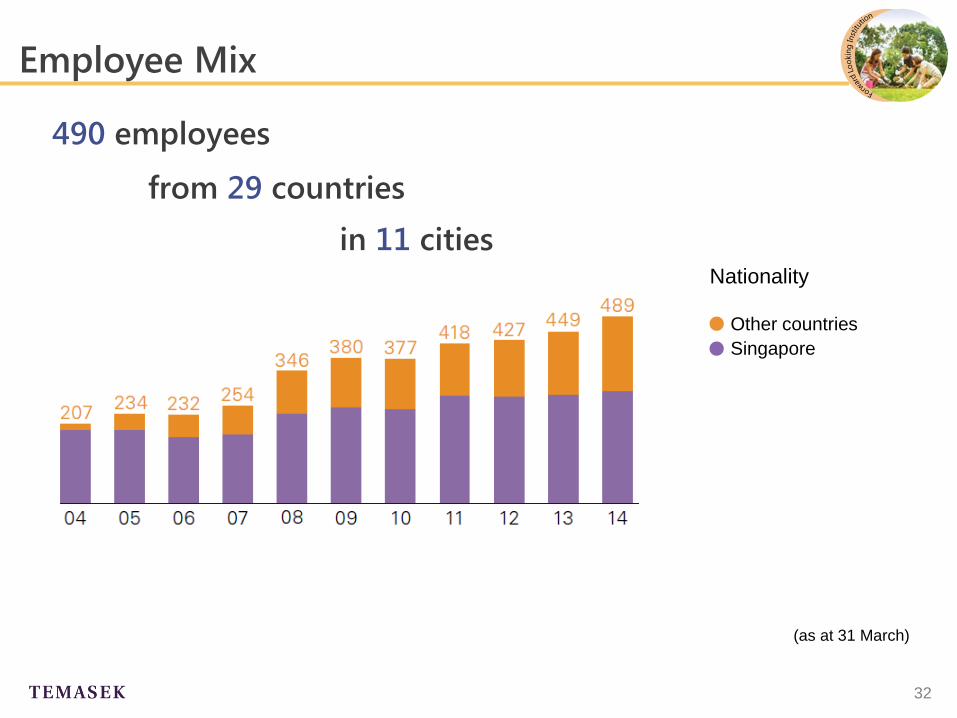

Employee Mix

(as at 31 March)

Other countries

Singapore

490 employees

from 29 countries

in 11 cities Nationality

33

Trusted steward Communities across generations

Active investor Sustainable long term value

Forward looking institution Ownership culture

The Temasek Charter

34

Our MERITT Values

Meritocracy Respect Teamwork

Excellence Integrity Trust

35

Delivering

returns over

risk-adjusted

hurdles

An Ownership Mindset

Investment Strategy

Capital Allocation

Performance Management

Incentive Framework

Delivering Sustainable Returns over the Long Term

36

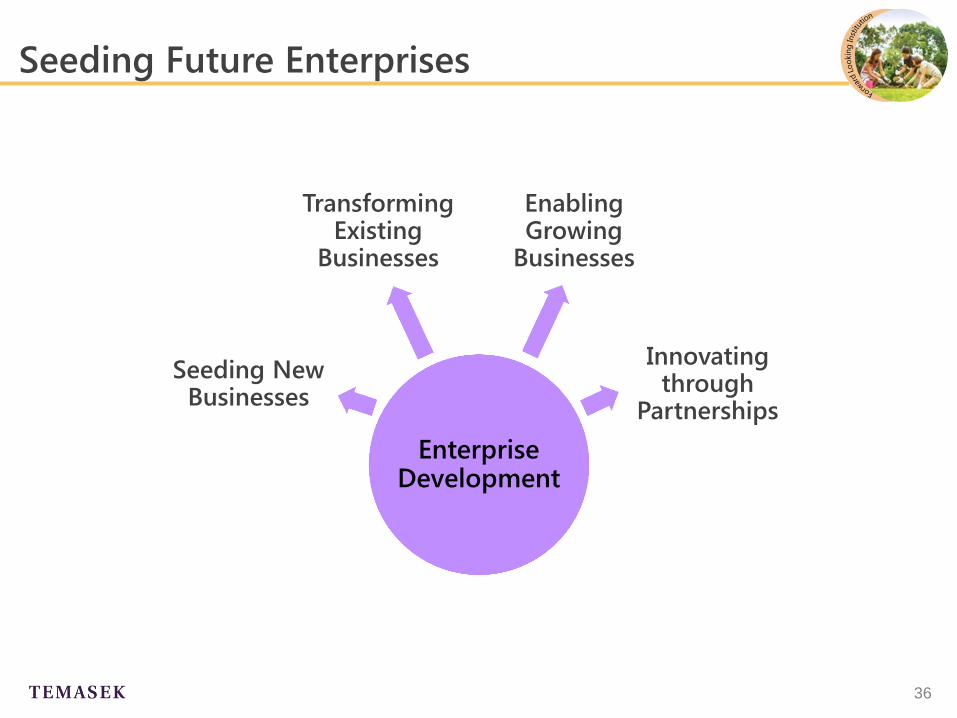

Seeding Future Enterprises

Enterprise Development

Seeding New Businesses

Enabling Growing

Businesses

Transforming Existing

Businesses

Innovating through

Partnerships

37

Seeding Future Enterprises

38

A Trusted Steward

16 endowments

39

Touched lives of

over 170,000 over past 10 years

A Trusted Steward

40

Fostering Stewardship and Governance

41

Our Temasek DNA

Tuesday, 8 July 2014

Our journey has just begun

A journey of a thousand miles, begins with a single step.

千里之行,始于足下 Lao Zi

Q&A

Tuesday, 8 July

Temasek Review 2014 Our journey has just begun

ANNEX

Tuesday, 8 July

Temasek Review 2014 Our journey has just begun

45

TSRs and MSCI Indices

18

16

7

12

15

0

10

7

6

12

20

(2)

5

10

17

3

11

10

8

7

19

20

N/A

N/A

Temasek

MSCI Singapore

MSCI AC Asia ex-JP

MSCI World

(developed economies)

Period (in years)

20

30

1

Since inception (1974)

5

10

US$ Total Shareholder Return (TSR) and MSCI Indices (%)

(as at 31 March 2014)