telecom italia group · s.p.a. business or acquisition strategy or planned capital expenditures or...

TRANSCRIPT

0

TELECOM ITALIA GROUP

Telecom Italia Group

Investor Meetings – Paris, July 3-4 2012

Franco Bernabè – Chairman and Group CEO

1

TELECOM ITALIA GROUP

Safe Harbour

These presentations contain statements that constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements appear in a number of places in this presentation and include statements regarding the intent, belief or current expectations of the customer base, estimates regarding future growth in the different business lines and the global business, market share, financial results and other aspects of the activities and situation relating to the Company and the Group. Such forward looking statements are not guarantees of future performance and involve risks and uncertainties, and actual results may differ materially from those projected or implied in the forward looking statements as a result of various factors. Consequently, Telecom Italia S.p.A. makes no representation, whether expressed or implied, as to the conformity of the actual results with those projected in the forward looking statement.Forward-looking information is based on certain key assumptions which we believe to be reasonable as of the date hereof, but forward looking information by its nature involves risks and uncertainties, which are outside our control, and could significantly affect expected results.Analysts are cautioned not to place undue reliance on those forward looking statements, which speak only as of the date of this presentation. Telecom Italia S.p.A. undertakes no obligation to release publicly the results of any revisions to these forward looking statements which may be made to reflect events and circumstances after the date of this presentation, including, without limitation, changes in Telecom Italia S.p.A. business or acquisition strategy or planned capital expenditures or to reflect the occurrence of unanticipated events. Analysts and investors are encouraged to consult the Company's Annual Report on Form 20-F as well as periodic filings made on Form 6-K, which are on file with the United States Securities and Exchange Commission.

2

TELECOM ITALIA GROUP

Agenda

Telecom Italia Group Overview

1Q12 Results

Focus on UBB

Financial Position and Group Targets

Sustainability at TI

3

TELECOM ITALIA GROUP

* Revenues based on net contributions

Euro mln, Organic Data

TI Group

FY 11 Δ% yoy FY 11 Δ% yoy

Brazil

FY 11 Δ% yoy

Argentina

FY 11 Δ% yoy

Revenues* 35%29,958 +2.7% 7,343 +18.2% 3,220 +26.5%19,033 -4.8%

EBITDA-CAPEX 7,467 -0.4% 708 +20.7% 479 +23.3 %6,374 -3.7%

85%

Domestic

EBITDA 25%12,339 Flat 1,998 +10.7% 1,035 +24.1%9,351 -3.9%

Cash Generation

for the Group

Engine of Growth

for the Group

Weight in TI Group

FY2011 Group Key Figures

4

TELECOM ITALIA GROUP

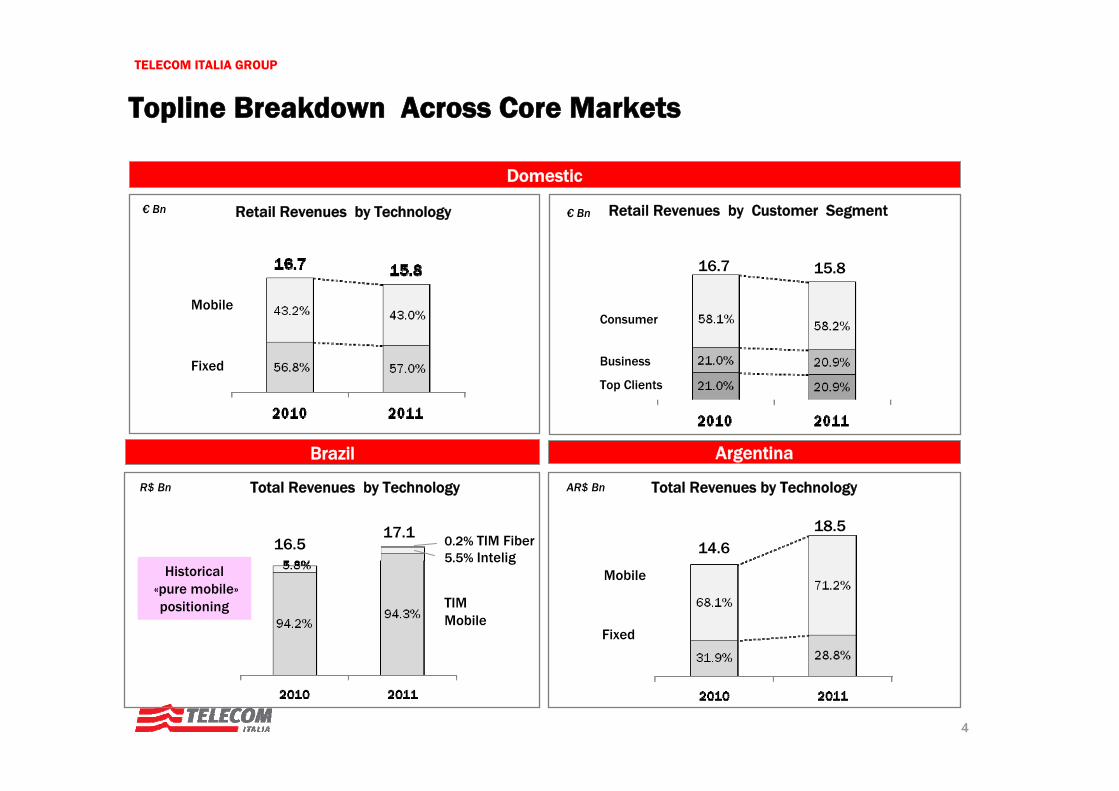

Topline Breakdown Across Core Markets

Brazil Argentina

Domestic

€ Bn

Fixed

Mobile

16.7 15.8

Consumer

Business

Top Clients

Retail Revenues by Customer Segment

18.514.6

Mobile

Fixed

AR$ Bn Total Revenues by Technology

17.116.5

TIM Mobile

0.2% TIM Fiber5.5% Intelig

Total Revenues by Technology R$ Bn

Historical«pure mobile»positioning

Retail Revenues by Technology € Bn

5

TELECOM ITALIA GROUP

TI’s Domestic Market: the Growing Importance of Innovation

FixedDomestic Retail Revenues

Mobile

16.715.8

€bn

Innovative

Traditional

€bn

Innovative

Traditional

7.4Innovative

Traditional

€bn

• Broadband• Web Contents• ICT (products

and services)

• Mobile browsing (Large & Small Screen)

• Contents (premium services, donwloads, games, ringtones, Infotainment)

6

TELECOM ITALIA GROUP

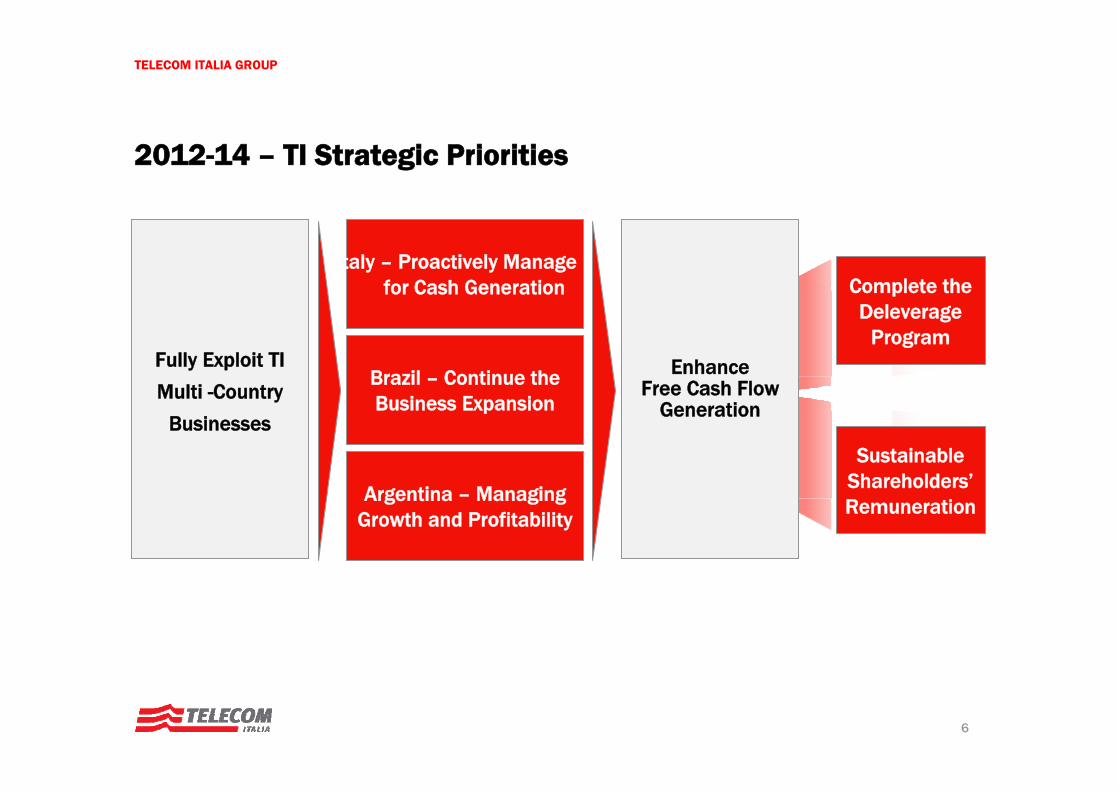

Fully Exploit TI

Multi -Country

Businesses

Brazil – Continue the Business Expansion

Argentina – Managing Growth and Profitability

Italy – Proactively Manage for Cash Generation

Enhance Free Cash Flow

Generation

Sustainable Shareholders’Remuneration

Complete the Deleverage

Program

2012-14 – TI Strategic Priorities

7

TELECOM ITALIA GROUP

** excluding Latam spectrum licences

TI Group – FY 2012 Key Guidance

Revenues

Ebitda

Capexcum ’12-’14

NFP Adj.**

NFP Adj. 2012-’14

Stable

Broadly Stable

>15 € bln

∼ 27.5 € bln

FY 2012: ∼ 27.5 € bln

FY 2013: ∼ 25 € bln

From FY 2014: < 2x Net Debt/Ebitda***

Organic Data*

TI Group – 2012-14 Plan Key Guidance **Ebitda-Capexcum ’12-’14

>22 € bln

Organic Data*

*exchange rates 2011 (R$/€ 2.33; ARS/€5.74), excluding impact from non-organic items

*** reported figure

Telecom Italia Group – FY 2012 and 2012-14 Plan Key Guidance

8

TELECOM ITALIA GROUP

Agenda

Telecom Italia Group Overview

1Q12 Results

Focus on UBB

Financial Position and Group Targets

Sustainability at TI

9

TELECOM ITALIA GROUP

Revenues EBITDA

42.0% 40.1%% on Revenues -1.9 p.p.

Revenues Trend YoY EBITDA-CAPEX

Euro mln, Organic data, %

27.2%-2.1 p.p.29.3%

+15 M€+0.5%

-43 M€-2.1%

TI Group Key Results

+373 M€+5.3%7,019

7,392

1Q11 1Q12

2,055 2,012

1Q11 1Q12

2,951 2,966

1Q11 1Q12

-0,2%

2.1%

3.7%

5.0%5.3%

1Q11 2Q11 3Q11 4Q11 1Q12

% on Revenues

10

TELECOM ITALIA GROUP

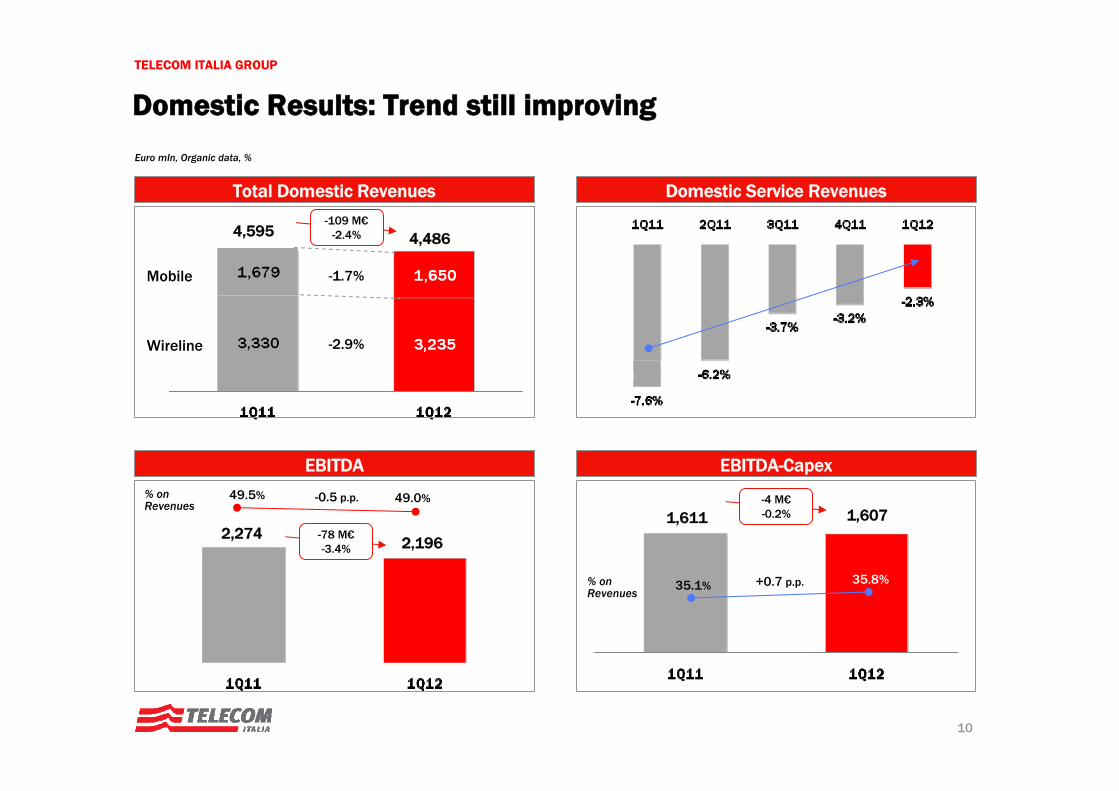

Domestic Results: Trend still improving

Euro mln, Organic data, %

4,595 4,486-109 M€

-2.4%

-1.7%

-2.9%Wireline

Mobile

Total Domestic Revenues Domestic Service Revenues

EBITDA

-78 M€-3.4%

49.5% 49.0%-0.5 p.p.% on Revenues

2,2742,196

EBITDA-Capex

1,611 1,607

35.8%+0.7 p.p.% on Revenues 35.1%

-4 M€-0.2%

11

TELECOM ITALIA GROUP

Euro mln, Organic Data

Mobile Revenues: 1Q12 Results at a Glance

Total Mobile Revenues

Mobile Service Revenues Trend – YoY % change

Handset revenues

Service revenues

1,650-29

-1.7%1,679

Normalized (*)

~-2.5%

Total Mobile

-3.7%

Normalized (*)

~-4.5%

+71.1%

(*) Leap year

Mobile Handsets Revenues Trend – YoY % change

12

TELECOM ITALIA GROUP

Domestic Mobile – Surfing the Data Wave

Increasing Smartphone Penetration in All Segments

Smartphones increasingly Service-Driven

Bri

ngin

g In

nova

tion

to t

he

Mas

s M

arke

t Operating Systems on TIM ‘s Network - The Android Growth

Dou

blin

g sm

artp

hone

pe

netr

atio

n on

C

B

Furt

her

roo

m fo

r gr

owth

Smartphone Penetration on Customer Base

~1,3 mln

May 2012 Dealer Convention

Of which >75% Smartphones

Data Bundle users and Renewal Rate

Number of Data connections by Device (*)

+~20%

2.2mln1.9mln

Renewal rate 79%87%

+1,9X

* Peak of traffic on the average day of the second week of each month

Dec’11 Jan’12 Feb’12 Mar’12 Apr’12

13

TELECOM ITALIA GROUP

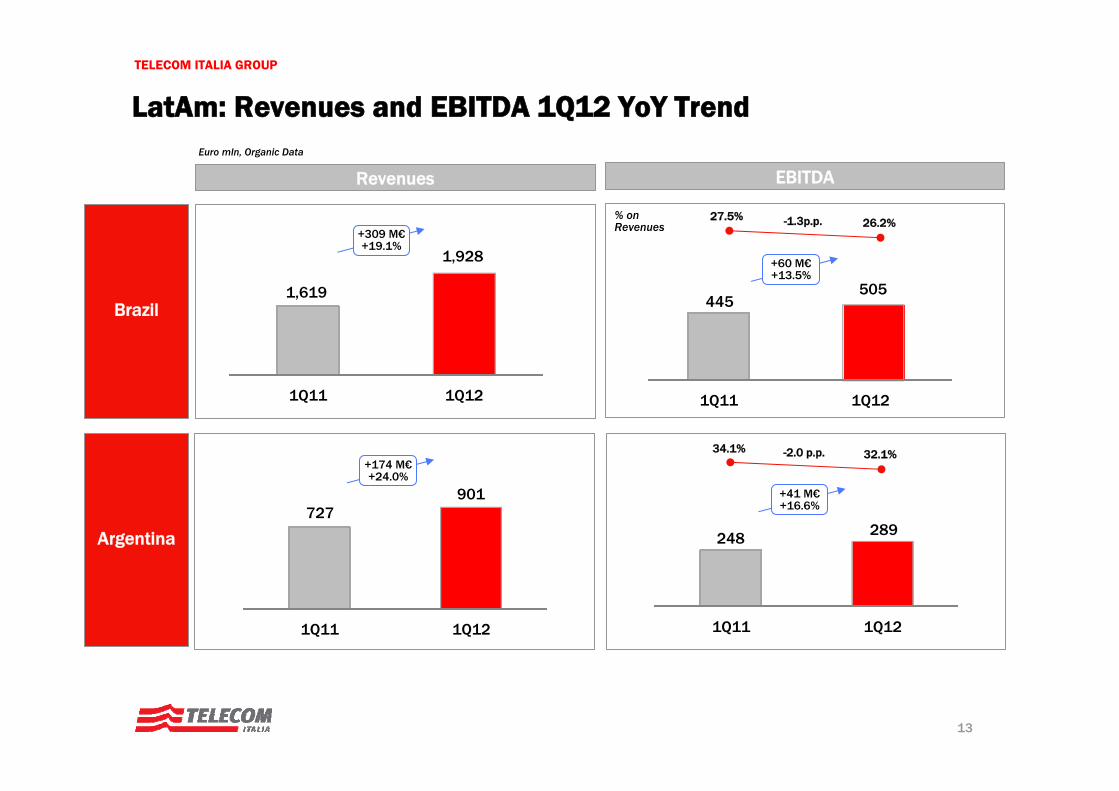

Euro mln, Organic Data

Revenues EBITDA

LatAm: Revenues and EBITDA 1Q12 YoY Trend

% on Revenues

+309 M€+19.1%

+60 M€+13.5%

27.5% 26.2%-1.3p.p.

1,619

1,928

1Q11 1Q12

445 505

1Q11 1Q12

Brazil

Argentina

+174 M€+24.0%

+41 M€+16.6%727

901

1Q11 1Q12

248 289

1Q11 1Q12

32.1%-2.0 p.p.34.1%

14

TELECOM ITALIA GROUP

Market Leaders In Our Footprint (March 2012)

Brazil ArgentinaDomestic

Mobile

Fixed

Broadband

#1 position - 32.3 mln lines

#1 position - 7.1 mln accesses

#1 position - 14.46 mln accesses

#2 position - 57.6 mln lines #2 position - 18.5 mln lines

#2 position - 1.56 mln accesses

#2 position - 4.14 mln accesses

A Competitive and still Healthy Market where TI remains the

Leading Operator

Customer base expansionacross all segments, driven by mobile rebranding of Personal

and the successful proposition of Arnet on broadband TV

Successful «Challenger «strategy and leadership in growth . TIM re-gained the

second position during 2011.

52.7%

34.9%

66.2%

26.8% 33.6%

47%

35%

Tim Brasil acquiredrelevant fiber infrastructure

through the Intelig and AES purchases,to further profitably develop

its mobile business.AES now offers the opportunity to enter the Fixed BB business

15

TELECOM ITALIA GROUP

Agenda

Telecom Italia Group Overview

1Q12 Results

Focus on UBB

Financial Position and Group Targets

Sustainability at TI

16

TELECOM ITALIA GROUP

% families

Families(mln)

23.9 24.3 24.6 24.9 25.2 25.4

Source: Between

UBB Networks allow TI to further tap growing BB demand:Mobile BB is complementary to Fixed BB

29%32% 30%

22%

18%

15%2%

7%18%

24% 28%

2%8% 12%

16%

71%66%

61%

52%

45%41%

2006 2007 2008 2009 2010 2011

FBB‐only families FBB & MBB families

MBB‐only families "No‐BB" families

Source: <Osservatorio Banda Larga

Italian Families - Broadband Penetration Italian Soho & SME - Broadband Penetration

17

TELECOM ITALIA GROUP

Capex Allocation

Strengthen the Network for a Technological Leadership

UltraBB Roadmap

Customer Service& Traffic Driven

Network Development

Network Maintainance

Acceleration

Decrease

HSPDA 42 Mbps LTE

NGAN Roll-out

Mobile Coverage

Optimize Network Investment to maintain excellent quality in TLC services

Increase the effort in Network Development and Innovation to confirm Technological Leadership and grant the Best Experience on the Net

2014100 Cities (including all

main ones) covered throughFTTH&Cab Technology

~¼ of Housing units passed with >30 Mb/s

Speed

2014More than 40% of

population covered by LTE

Optimization

Network Capex

2012-2014 Plan

18

TELECOM ITALIA GROUP

TI’s Convergent Approach to Fixed and Mobile UBB

The Value of our Core Asset A

cces

sN

etw

ork Key asset both for fixed and mobile

Huge capital and time already fruitfully investedHigh CapillarityStrategic asset in the economic , social & regulatory landscape

Yesterday Today: Pervasive Ultra Broadband

UBB

Super Internet +

NGAN Fttx HSPA+ LTE

NGN

Fixed Network

Fixed & Mobile Network

19

TELECOM ITALIA GROUP

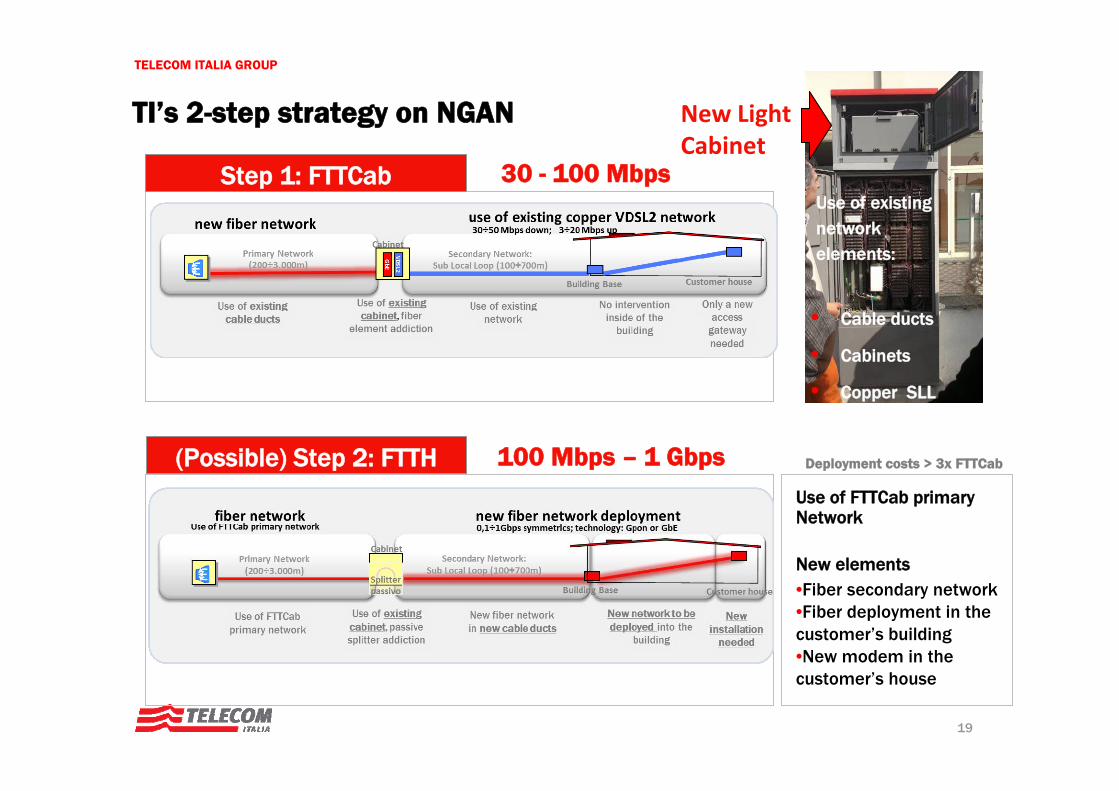

TI’s 2-step strategy on NGAN

Step 1: FTTCab

(Possible) Step 2: FTTH

30 - 100 Mbps

100 Mbps – 1 Gbps

• Cable ducts

• Cabinets

• Copper SLL

Use of FTTCab primary Network

New elements•Fiber secondary network•Fiber deployment in the customer’s building•New modem in the customer’s house

Deployment costs > 3x FTTCab

New Light Cabinet

Use of existing network elements:

20

TELECOM ITALIA GROUP

TI Fixed UBB Plan: 2012-2014 and beyond

About 60% cities target in the North (i.e. Milan, Turin, Genoa); NewCo Trentino NGN for Trento region

About 20% cities located in the Central part of the country (i.e. Rome, Florence)

About 20% cities located in the South(i.e. Naples, Bari, Palermo)

2014 within 20202012 - 1H13

30 cities 100 cities

Driver for NGAN Plan:

Density of population;

Leverage on existing infrastructure (i.e. ducts already in place in most of 100 targeted cities)

Moving towards DAE

Targets

21

TELECOM ITALIA GROUP

Agenda

Telecom Italia Group Overview

1Q12 Results

Focus on UBB

Financial Position and Group Targets

Sustainability at TI

22

TELECOM ITALIA GROUP

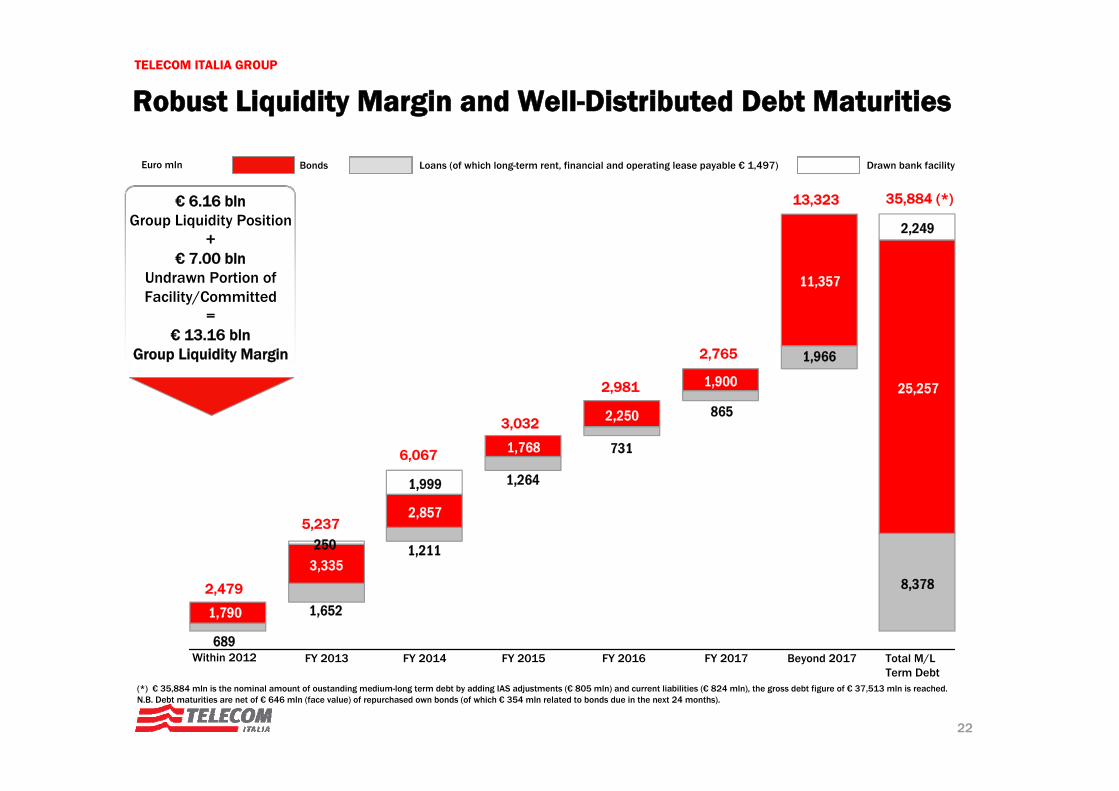

Bonds Loans (of which long-term rent, financial and operating lease payable € 1,497) Drawn bank facilityEuro mln

€ 6.16 bln Group Liquidity Position

+€ 7.00 bln

Undrawn Portion of Facility/Committed

=€ 13.16 bln

Group Liquidity Margin

Robust Liquidity Margin and Well-Distributed Debt Maturities

689

1,652

1,211

1,264

731

865

1,966

8,378

1,790

3,335

2,857

1,768

2,250

1,900

11,357

25,257

250

1,999

2,249

2,479

5,237

6,067

3,032

2,981

2,765

13,323 35,884 (*)

(*) € 35,884 mln is the nominal amount of oustanding medium-long term debt by adding IAS adjustments (€ 805 mln) and current liabilities (€ 824 mln), the gross debt figure of € 37,513 mln is reached.N.B. Debt maturities are net of € 646 mln (face value) of repurchased own bonds (of which € 354 mln related to bonds due in the next 24 months).

Within 2012 FY 2013 FY 2014 FY 2015 FY 2016 FY 2017 Beyond 2017 Total M/LTerm Debt

23

TELECOM ITALIA GROUP

2011-2013 Deleverage Targets Confirmed

Cash Flow Generation (EBITDA- Capex) Net Financial Position Adjusted**

New Dividend Policy (as announced on Feb. 24 2012)

Euro Bln

35.930.4

2007 2011 2012

∼27.5

-5.5 Bln € Net Debt

2013

∼25

2014

Latam

Domestic

Financial Discipline

2012 and 2013 targets confirmed

~20%

~80%

>22 Bln €

Cum. ‘12-’14

Organic Data*

*Organic: same perimeter, 2011 FX rates, excluding spectrum licences acquisitions.** Excluding Latam spectrum licences acquisitions.

24

TELECOM ITALIA GROUP

Agenda

Telecom Italia Group Overview

1Q12 Results

Focus on UBB

Financial Position and Group Targets

Sustainability at TI

25

TELECOM ITALIA GROUP

TI is part of all main global and European sustainability indexes

Electricity consumption and Greenhouse Gas emissions have been curbed downwards (respectively, -6,3% and -6,2% versus 2010)

TI delivers a wide range of Green and Social telecommunications solutions for the Public Administration and private Customers, improving their environmental footprint and lifestyle

Relations with Trade Unions are excellent. This is key to deliver agreements which are considered satisfactory by all involved parties (e.g the one of August 4, 2010)

A wide range of projects aimed at bridging the social digital divide are under way, sometimes with the involvement of the Public Administration

Telecom Italia is a founding member of a joint auditing project on suppliers' production sites in developing countries, carried out in partnership with other leading Telecom operators. As of December 2011, 33 sites were audited involving 155,000 workers

Sustainability at TI: Key Actions and Results