tcns clothing company ltd.€¦ · it sold products through 541 ebos, 1,623 lfs stores and 1,428...

TRANSCRIPT

June 28, 2019

TCNS Clothing Company Ltd. Initiating Coverage

Restyling India’s ethnic-wear landscape

June 28, 2019 Before reading this report, you must refer to the disclaimer on the last page. Page 1 of 26

TCNS Clothing Ltd. Absolute: ADD

Relative: Overweight

Initiating Note Regular Coverage 8% ATR in 18 Months

Restyling India’s ethnic-wear landscape – Initiate with ADD Textiles

© 2019 Equirus All rights reserved

Rating Information

Price (Rs) 781

Target Price (Rs) 872

Target Date 31st Dec'20

Target Set On 27th Jun'19

Implied yrs of growth (DCF) 20

Fair Value (DCF) 790

Fair Value (DDM) 26

Ind Benchmark SPBSMIP

Model Portfolio Position NA

Stock Information

Market Cap (Rs Mn) 47,893

Free Float (%) 38.37 %

52 Wk H/L (Rs) 870/515

Avg Daily Volume (1yr) 1,26,003

Avg Daily Value (Rs Mn) 91

Equity Cap (Rs Mn) 123

Face Value (Rs) 2

Bloomberg Code TCNSBR IN

Ownership Recent 3M 12M

Promoters 32.4 % 0.0 % -

DII 4.6 % 0.3 % -

FII 16.4 % 0.2 % -

Public 46.6 % -0.5 % -

Price % 1M 3M 12M

Absolute 5.0 % -4.8 % -

Vs Industry 6.7 % -2.7 % -

ABFRL 0.9 % -3.9 % 54.4 %

Trent 18.9 % 21.2 % 48.4 %

Consolidated Quarterly EPS forecast

Rs/Share 1Q 2Q 3Q 4Q

EPS (19A) 3.2 6.4 5.7 5.1

EPS (20E) 4.4 6.0 5.2 4.8

TCNS Clothing (TCNS), India’s leading women’s ethnic wear player has emerged as a key

beneficiary from a shift in preference from unbranded to branded apparels. Its leadership

in a growing branded ethnic wear market stems from USPs like (1) a differentiated brand

portfolio (W, Aurelia & Wishful) across price points, (2) an extensive store network with a

robust supply chain, and (3) an institutionalized and feedback-oriented design process.

TCNS is set to deliver a ~17% revenue CAGR over FY19-FY22E; with better operating

efficiencies driving an ~18% adj. EBITDA CAGR in this period. However, current softness in

demand and muted airport store revenues could hurt near-term performance. We are mid-

to-long-term positive on TCNS and its ability to outpace peers and gain market share.

Initiate with ADD at a TP of Rs 872 set at 35x Dec’20 TTM EPS of Rs 25.

Differentiated portfolio, rapid store network expansion to drive ~17% revenue

CAGR over FY19-FY22E: Over the years, TCNS has developed a differentiated brand

portfolio (W, Aurelia & Wishful) with offerings across price points, leading to a strong

brand recall. A rapidly expanding store network with 23%/30%/18% CAGR in EBO/LFS/

MBO store counts over the last 4 years has strengthened the company’s foothold in

the women’s branded ethnic wear market. We feel that a combination of factors

including (1) A unique product portfolio, (2) strong revenue growth from existing

stores, and (3) addition of 70-75 EBO stores per annum would drive a 17% revenue

CAGR over FY19-FY22E. This along with better operating efficiencies from scale

benefits would lead to an ~18% adj. EBITDA CAGR over this period.

Innovative & institutionalized design process = finger on consumer pulse: TCNS has

developed a highly innovate and feedback-oriented design process that helps it come

up with latest designs post filtration at both the company and dealer-distributor level

(at trade shows organized by TCNS bi-annually). This filtration significantly reduces

chances of design failure, thus ensures high acceptance levels for the company’s brands.

Strict WC control, strong FCF generation to continue: Despite continuous store

additions, TCNS has maintained a strict control on WC requirements; this along with

high profitability has helped generate strong cash flows for the company. With limited

capex requirements (Rs 450mn-500mn per annum) for the next 2-3 years, TCNS should

generate a FCFF of ~Rs 2bn over the next three years. Limited capex and largely stable

WC turns should improve adj. core ROIC by ~160bps to ~26% over FY19-FY22E.

Initiate with ADD, Dec’20 TP of Rs 870: At CMP of Rs 781, TCNS trades at 38x/33x

FY20E/FY21E EPS, which we feel is expensive when compared to peers and given the

near-term uncertainties. Initiate with ADD and a TP of Rs 872 set at 35x Dec’20 TTM EPS

of Rs 25.

Consolidated Financials

Rs. Mn YE Mar FY19A FY20E FY21E FY22E

Sales 11,480 13,369 15,675 18,427

EBITDA 1,768 2,193 2,614 3,162

Depreciation 222 293 382 475

Interest Expense 5 7 7 7

Other Income 75 120 141 166

Reported PAT 1,314 1,318 1,549 1,864

Recurring PAT 1,314 1,318 1,549 1,864

Total Equity 6,186 7,511 9,021 10,827

Gross Debt 0 0 0 0

Cash 1,608 1,937 2,651 3,602

Rs. Mn YE Mar FY19A FY20E FY21E FY22E

Earnings 20.3 20.4 24.0 28.9

Book Value 101 116 140 168

Dividends 0.0 0.0 0.5 0.8

FCFF 8.5 4.7 11.3 15.3

P/E (x) 38.4 38.3 32.6 27.1

P/B (x) 7.7 6.7 5.6 4.7

EV/EBITDA (x) 26.3 21.0 17.4 14.1

ROE (%) 25 % 19 % 19 % 19 %

Core ROIC (%) 30 % 25 % 25 % 26 %

EBITDA Margin (%) 15 % 16 % 17 % 17 %

Net Margin (%) 11 % 10 % 10 % 10 %

TCNS Clothing Ltd. Absolute – ADD Relative – Overweight 8% ATR in 18 Months

June 28, 2019 Page 2 of 24

Company Snapshot

How we differ from Consensus

- Equirus Consensus % Diff Comment

EPS FY20E 20.4 20.0 2 % In-line with consensus

FY21E 24.0 23.9 0 %

Sales FY20E 13,369 13,334 0 %

FY21E 15,675 15,685 0 %

PAT FY20E 1,318 1,286 3 %

FY21E 1,549 1,555 0 %

Our Key Investment arguments:

• Differentiated brand portfolio across price points, huge store network & robust supply

chain are key USPs for a leader in the organized women’s ethnic wear market.

• Highly penetrated store network and continuous stores additions to drive a ~17%

revenue CAGR over FY19-FY22E. This along with rise in operating efficiencies on scale

benefits will lead to ~18% adj. EBITDA CAGR over this period.

• Innovative and institutionalized design process helps in coming up with highly

acceptable designs.

• Strict control over WC and strong FCFF generation would improve return ratios.

Key Assumptions:

Particulars (In Rs Mn) FY19 FY20E FY21E FY22E

W Revenues 6,888 8,093 9,550 11,297

Aurelia Revenues 3,903 4,449 5,117 5,900

Wishful Revenues 689 827 1,008 1,230

Capex 217 450 420 420

NWC Days 103 108 108 109

Risk to Our View

Continued demand slowdown, design failure for many seasons in a row, longer breakeven

time of new stores.

Key Triggers

• Robust demand growth; increase in share of organized ethnic wear & faster break-even

of new stores.

Sensitivity to Key Variables % Change % Impact on EPS

Revenue 1 % 1 %

EBITDA 1 % 1 %

- - -

DCF Valuations & Assumptions

Rf Beta Ke Term. Growth Debt/IC in Term. Yr

7.5 % 1.2 14.7 % 2.5 % 0.0 %

- FY20E FY21E FY22-24E FY25-29E FY30-39E

Sales Growth 16 % 17 % 11 % 14 % 16 %

NOPAT Margin 9 % 9 % 10 % 11 % 12 %

IC Turnover 2.42 2.47 2.65 2.73 2.87

RoIC 24.8 % 24.6 % 29.0 % 31.7 % 37.3 %

Years of strong growth 1 2 5 10 20

Valuation as on date (Rs) 160 171 239 330 642

Valuation as of Mar'20 197 211 294 406 790

Based on DCF, assuming 20 years of 16% CAGR and 37% average ROIC, we derive our current

fair value of Rs 642 and a 31st Dec’20 fair value of Rs 790.

Company Description:

TCNS is one of the India’s leading manufacturers that designs, manufactures, markets and

retails a wide portfolio of women’s branded apparels across multiple brands. As on Mar’19,

it sold products through 541 EBOs, 1,623 LFS stores and 1,428 MBO stores located in 31

states and UTs in India. It also sold its products through 6 EBO stores in Nepal, Mauritius

and Sri Lanka.

Comparable valuation Mkt Cap

Rs. Mn.

Price

Target

Target

Date

EPS P/E BPS P/B RoE Div Yield

Company Reco. CMP FY19A FY20E FY21E FY19A FY20E FY21E FY19A FY20E FY19A FY20E FY21E FY19A FY20E

TCNS Clothing ADD 781 47,893 872 31st Dec'20 20.3 20.4 24.0 38.4 38.3 32.6 100.9 6.7 25 % 19 % 19 % 0.0 % 0.0 %

ABFRL NR 213 1,64,717 NR NR 4.2 3.4 5.0 51.3 62.7 42.3 18.5 9.9 25 % 17 % 21 % 0.0 % 0.0 %

Trent NR 445 1,48,014 NR NR 2.9 5.5 6.9 156.1 80.7 64.6 49.5 8.0 6 % 12 % 14 % 0.2 % 0.4 %

TCNS Clothing Ltd. Absolute – ADD Relative – Overweight 8% ATR in 18 Months

June 28, 2019 Page 3 of 24

Favorable industry dynamics = Huge market opportunities

India’s women’s apparel industry witnessing robust growth

India’s total apparel market was pegged at US$ 51bn in FY17, of which women’s apparel

contributed ~37% or US$ 19bn. Rising digitization and urbanization, supported by increasing

brand consciousness and greater purchasing power will lead to above-GDP growth for

apparel consumption. India’s women apparel market is expected to touch US$ 42bn by FY25,

growing at a healthy 10.3% CAGR driven by (a) an increase in number of working women,

(b) a shift towards aspiration rather than need-based buying, and (c) emergence of many

home-grown national brands with unique design innovations that appeal to Indian

sensibilities.

Exhibit 1: Women’s apparel market to continue to grow at ~10.3% CAGR (FY20E-25E)

Source: Technopak Analysis, TCNS RHP, Equirus Securities

Of the total women’s apparel market, Indian apparels account for 71% of the market and is

dominated by a few national brands along with many regional players. The disproportionate

size of Indian wear for women is attributable to its distinct positioning vis-à-vis that of men

in India.

Particulars For Women For Men

Indian & Ethnic wear Daily wear incl. occasions wear utility

Largely restricted to occasion wear viz. weddings & festivals

Western Wear Occasionally however ratio growing rapidly

Daily wear except for occasions

For Indian women, Indian and ethnic fashion is a mainstream daily-wear use requirement

(in addition to strong occasion-wear utility); for men, it is largely restricted to occasion-

wear alone. viz weddings and festivals.

Exhibit 2: Indian wear accounts for ~71% or US$ 13.5bn of women’s apparel market

Source: Technopak Analysis, TCNS RHP, Equirus Securities

Exhibit 3: Of US$ 13.5bn women’s Indian wear market, ethnic wear has a 48% share

Source: Technopak Analysis, TCNS RHP, Equirus Securities

12.1

19.3

25.7

41.9

0

5

10

15

20

25

30

35

40

45

FY12 FY17 FY20E FY25E

Indian Women's apparel market (In US $ bn) 71%

15%

3%

3%

3%

3%

2%

Indian Wear

Innerwear

Winterwear

Sleepwear

Tops/Shirts/T-Shirts

Denim/Trousers/Skirts

Others

48%45%

7%

Ethnic wear

Sarees

Blouse Petticot

TCNS Clothing Ltd. Absolute – ADD Relative – Overweight 8% ATR in 18 Months

June 28, 2019 Page 4 of 24

Women’s ethnic apparel market in India stood at US$ 6.5bn as of FY17 and is expected to

grow at 14% CAGR to reach US$ 9.5bn by FY20E-end. Factors such as rising disposable

incomes, better design, quality and fit assurance, growing aspiration levels and increasing

acceptance of ethnic wear as work wear are triggering a shift from traditional apparel

(sarees) to ethnic wear (salwar kameez, kurtas).

Rise of organized and branded ethnic wear players

Until a decade ago, ethnic wear ― largely constituting sarees and their clothing accessories

― was looked at as old-age wear that was catered to by neighborhood tailors. However, an

influx of new entrants that sell a fusion of modern and traditional wear has altered mindsets

and attracted the younger generation towards ethnic wear. This shift was further boosted

by (a) a rising share of organized and branded players in the segment, and (b) an aspiration

to be associated with brands that provide features of design, fit, comfort and convenience.

Exhibit 4: At 29% CAGR, organized retail is set to grow at 3x unorganized retail growth

Source: TCNS RHP, Equirus Securities. Figures in chart are average nos. of range provided.

As of FY17, the share of organized retail in women’s ethnic apparel stood at 20%; however,

with changing consumer preferences fueled by a large-scale presence of organized players,

this should touch 33% by FY20-end. Thus, with a growth rate of 29.4% over FY17-FY20E,

organized retail would grow ~3x that of unorganized retail in this period.

Exhibit 5: Branded ethnic wear to grow at 31% CAGR with a ~35% market share in 2020

Source: TCNS RHP, Equirus Securities.

High growth in organized retail in ethnic women’s wear will also be reflected in high growth

of branded women’s ethnic apparels. Branded ethnic wear, at US$ 1.5bn with a 23% market

share in FY17, is expected to grow at a 31% CAGR (to US$ 3.4bn in FY20) with women’s

ethnic wear constituting a 35% share. Though the ethnic wear market is dominated by

unbranded women’s wear, a large part of it is moving towards branded apparels on account

of the following:

- Increase in variety that meets the tastes and preferences of various age groups

- Standardization of designs available in many sizes and fits

- Wide range available at various price points

Institutionalization of the design process, use of unique fabrics as well as modern

production processes are the key growth drivers of women’s wear brands. Growth of the

branded and organized ethnic apparel segment will be driven by significant investments by

industry leaders in building capabilities around design and sourcing coupled with strong

demand dynamics of the category.

Women’s ethnic wear market can be segregated into four distinct phases (Exhibit 6). It is

noteworthy that the proportion of branded wear in organized retail has been steadily

increasing.

7%9%

13.5%

20%

33%

Pre 2000 2001-2007 2008-15 2015-2017 FY20E

Share of Organized retail in women's apparel market

56.1

1.5

3.4

0

2

4

6

8

10

2017 2020

Unbranded Branded

TCNS Clothing Ltd. Absolute – ADD Relative – Overweight 8% ATR in 18 Months

June 28, 2019 Page 5 of 24

Exhibit 6: Rising share of organized retail in every phase of evolution

Pre-2000 2001-2007 2008-2015 2015-Present

Dominance of Unorganized Players

Initiation of Organized Retail

Growth of Organized Retail Emergence of Industry Leaders

Organized Retail Share: 5%-8% Organized Retail Share: 8%-10% Organized Retail Share: 12%-15% Organized Retail Share: 20%

1. Local boutiques serve captive customers

2. Daily apparel needs served through customized

tailoring or limited functional ready to apparel

offering

3. Readymade offering limited to occasion

apparel

4. Retail footprint of organized retailers

(Fabindia, Biba) restricted to EBOs in few cities

and clusters

5. Ethnic apparel private label of Westside

1. BIBA and Fab India expand retail

footprints

2. W opens its first EBO

3. Westside expands its retail footprints

1. Retail brands scale up penetration of EBOs in metros

and mini-metros

2. Emergence of regional brands

3. Growth of LFS formats as an important organized retail

channel for women’s ethnic apparel both as private

labels and as destination for retail brands

4. Launch of sub-brands or retail store segmentation by

ethnic apparel retail brands to cater to different needs.

5. Initiation and growth of e-commerce

1. Retail brands expand beyond metros

and mini-metros to other urban

clusters

2. Online retail starts gaining traction as

a complimentary retail channel

3. Emergence of industry leaders on

product differentiation, designs and

positioning

Domestic players clearly dominate branded apparel ethnic wear market

Overall size of India’s ethnic fashion market is neither big enough not broad enough (in

terms of appeal outside India) for the global supply chain of western apparel to align itself

on raw materials, sourcing and merchandising for ethnic apparel. Raw materials and

sourcing for Indian ethnic fashion is a mix of artisanal skills, machines, handlooms and

power looms. This poses a challenge for the scale of global fashion brands. Additionally,

the global design response that interprets trends into products for global brands requires

interpretation of Indian ethos, fabric and colors into products; this becomes difficult for

global players to respond to in light of international presence and unique design philosophy

of India and other foreign countries.

Therefore, ethnic apparel in India is a domestic-focused opportunity and one which provides

home-grown players with a natural and sustainable advantage to seize. This advantage is

reflected in the structure of the ethnic apparel category that comprises home grown

entities only.

TCNS Clothing Ltd. Absolute – ADD Relative – Overweight 8% ATR in 18 Months

June 28, 2019 Page 6 of 24

Exhibit 7: Competitive landscape in women’s ethnic apparel retailing in India

National Players Regional Player Private Label Local Players

Ethnic Lifestyle & Fashion Retailers

Ethnic Apparel led Retail Brands Ethnic Apparel led

Retail Brands In-store apparel brands of Multi-

brand retailers Neighbourhood stores/Boutique

shops

Example FabIndia, Anokhi W, Aurelia, BIBA, Global Desi Kiara, Ibadat, Harra Rangmanch, Akriti, Morpankh, Navras

-

Share of women's ethnic apparel in total business

40-60% ~90% ~95% < 90% 100%

Sales Breakup by channel EBO: 100%

EBO: 40-50% LFS: 30-40% MBO: 5-10%

Online: 5-10%

EBO: 70-80% LFS: 10-20%

LFS: 100% Within store: 100%

Retail Presence PAN India, strong presence in

Tier 2 & below towns PAN India, strong presence in Tier

2 & below towns Region focused PAN India presence Limited to a city/cluster

Price point ~Rs 1000-5,000 ~Rs 800-5,000 ~Rs 1,000-2,500 ~Rs 700-1,500 ~Rs 500-1,200

Design Focus Specific prints & designs Strong design philosophy catering

to PAN India taste Regional designs &

prints Wide range of designs with high

focus on core products Limited for ready to wear but premium for made to order

Source: Technopak, TCNS RHP, Equirus Securities

Depending on the scale of operations and product offerings, India’s ethnic wear segment

can be divided into three broad categories:

National brands: These can be further classified into two types of retailers:

- Ethnic lifestyle-led fashion retailers: Small retailers that have grown big to national

levels and sell multiple categories on ethnic fashion ethos like women’s apparel, men’s

apparel, home furnishing (FabIndia, Anokhi).

- Ethnic apparel-led retail brands: Women’s ethnic apparel comprises ~90% of the sales

mix. Strengths include product design differentiation, pan-India reach, store network of

owned & franchisee stores (Biba, W, Aurelia, Global Desi).

Regional brands: These retailers try to imitate national brands on EBO formats and product

offerings. While they have an advantage of being closer to regional tastes of their

consumers, their product designing abilities or retail reach restrict them to expand beyond

their region (Mebaaz, Harra, Prafull, Ibadat, Kiara).

Private labels: Private labels are the in-store ethnic apparel brands of large format stores

(LFS). Leading LFS stores have created in-store label brands and sell them exclusively along

with other national or regional brands and thus carry an image of quality equivalent to

other brands. These private label brands are attractively priced in comparison to

national/regional brands and thus generate interest from a larger audience. Stop of

Shoppers Stop, Melange of Lifestyle, Rangmanch, Akriti and Trisha of Pantaloons, Morpankh,

Navras and Ateesha of Central are leading private label brands in women’s ethnic apparel

space.

Exhibit 8: Fab India & BIBA ― Pioneers of branded women’s ethnic retailing in India

Brand Year of Inception Focus Area

W 2002 All-India

Aurelia 2009 All-India

Wishful 2006 All-India

BIBA 1988 North, South, West

Global Desi 2007 North & West

Fab India 1960 All-India

Soch 2005 South

Source: TCNS RHP, Equirus Securities

TCNS Clothing Ltd. Absolute – ADD Relative – Overweight 8% ATR in 18 Months

June 28, 2019 Page 7 of 24

Investment Rationale

Differentiated brand portfolio across price points ― a key USP

In India’s women ethnic wear market, a number of players offer products to specific apparel

categories like western wear, occasion wear, office wear and daily wear, or cater to specific

price points and thus restrict themselves to a limited group of target customers.

Few national players like TCNS have differentiated themselves from other players through

a multi-brand platform strategy by offering products across price points and catering to

various customer segments. A diversified brand portfolio (W, Aurelia and Wishful) helps

TCNS to cater to customer needs with its extensive product range and thus increase brand

loyalty.

TCNS is India’s leading women’s branded apparel company that designs, manufactures and

retails a wide portfolio of women’s branded apparel across multiple brands. Its product

portfolio includes top-wear, bottom-wear, drapes, combination sets and accessories that

cater to a wide variety of wardrobe requirements of Indian women, including daily wear,

casual wear, office wear and occasion wear.

Backed by the strong understanding of Indian women’s needs and aspirations, TCNS has a

track record of developing home-grown brands over the years that cater to the needs of

ethnic wear with a blend of western sensibilities as well. Brands of TCNS include:

W is a premium fusion wear brand that is a blend of Indian and

western fashion sensibilities with emphasis on distinctive design

and styling and is targeted primarily at the modern Indian

women’s work and casual wear requirements.

Aurelia is a contemporary ethnic wear brand targeted at women

looking for great design, fit, and quality for casual and work wear

requirements.

Wishful is a premium occasion wear brand, with elegant designs

catering to women’s apparel requirements for evening wear and

occasions such as weddings, events and festivals.

TCNS Clothing Ltd. Absolute – ADD Relative – Overweight 8% ATR in 18 Months

June 28, 2019 Page 8 of 24

W ― Plugging the gap between Indian and western wear

W is the first and the most successful brand for the company that bridged the gap between

Indian wear and western wear apparels. There existed a large set of consumers wanting to

rise above traditional sarees, blouses and conventional dresses but did not want to switch

entirely to western wear. This need for the fusion of both Indian and western sensibilities

was well identified and catered to along with innovative fusion prints and fabric; this in

turn led to the success of the brand W for the company. Majority of the top-wear under this

brand sells at maximum retail prices ranging from Rs 1,299 to Rs 1,899. W currently is the

largest brand for TCNS and contributes ~60% of revenues. Revenues from this brand have

seen phenomenal growth of ~30% CAGR over FY16-FY19 driven by rising brand loyalty and

increased penetration in both newer and existing markets.

Exhibit 9: W revenues have grown at a robust 30% CAGR over FY16-19 (In Rs Bn)

Source: Company, Equirus Securities.

Aurelia ― Focusing on quality & fit; price point lower than W

Aurelia, almost a similar brand to W, is a contemporary ethnic wear brand specially targeted

to women looking for a great fit, quality and design for casual and workwear requirements.

The focus here is more towards fit and quality vs. innovative design and styling for W. The

price point of Aurelia is also lower than W, at Rs 799 to Rs 1,499 and at Rs 1,999 to Rs 4,499

for combination sets. Both these features segregate target customers of W and Aurelia.

Aurelia has also seen robust growth of 35% CAGR over FY16-FY19 with ~34% contribution to

revenues.

Exhibit 10: Aurelia revenues have grown at phenomenal 35% CAGR over FY16-19 (In

Rs Bn)

Source: Company, Equirus Securities.

Wishful ― Premium occasion wear brand

Wishful is a premium occasion-wear brand with elegant designs catering to women’s apparel

requirements for evening wear and occasions such as weddings, events and festivals. Under

Wishful, the company also sells a higher-end premium range brand, Wishlist, that is made

up from premium clothing and has high-quality work and embellishments. While Wishful

products are sold in the range of Rs 2,999 to Rs 4,999, Wishlist products range between

Rs 12,000 – Rs 29,000. With ~6% revenue contribution in FY19, TCNS has not been able to

scale up Wishful revenues over the last three years mainly due to manufacturing constraints

and supply chain issues.

Exhibit 11: Wishful, due to manufacturing & supply constraints, grew at just 4% CAGR

over FY16-19 (In Rs Bn)

Source: Company, Equirus Securities.

3.2

4.3

5.7

6.9

0

2

4

6

8

FY16 FY17 FY18 FY19

1.6

2.2

3.4

3.9

0.0

1.0

2.0

3.0

4.0

5.0

FY16 FY17 FY18 FY19

0.60.6

0.9

0.7

0.0

0.2

0.4

0.6

0.8

1.0

FY16 FY17 FY18 FY19

TCNS Clothing Ltd. Absolute – ADD Relative – Overweight 8% ATR in 18 Months

June 28, 2019 Page 9 of 24

Exhibit 12: TCNS has a different brand at different price points

Brand Price Point Style Offerings Peers

W Rs 1,299-1,899 Premium fusion wear brand

Top wear, bottom wear, drapes

Global Desi, BIBA, STOP, etc.

Aurelia

Rs 799-1499, combination sets from Rs 1,999-4,499

Contemporary Ethnic wear

Top wear, bottom wear, drapes, combination sets

Soch, Melange, Rangmanch, etc.

Wishful Rs 2,999-4,999 Premium occasion wear brand

Top wear, bottom wear, drapes

Fbb, Miraaya, SPAR, Prafful, etc.

Wishlist (sub-brand of Wishful)

Rs 12,000 – 29,000

High premium occasion wear

Combination sets of Top wear, bottom wear and drape sold together

Designer boutique & fashion houses

Source: Company, Equirus Securities

Multi-channel retail network with pan-India presence lends competitive edge

In the branded and organized women’s ethnic wear market, Exclusive Brand Outlets (EBO)

and Large format stores (LFS) are the leading retail channels preferred by majority of

national and regional brands. While EBOs are the building blocks that provide brand value

proposition to customers, LFS ensures higher reach of the brand across cities in an

affordable manner. Not surprisingly, most players have ~70-90% of presence through

these routes.

Exhibit 13: EBO & LFS is the most preferred channel for most national players

Source: Technopak, TCNS RHP, Equirus Securities.

Over the years, TCNS has successfully set up a wide-scale multi-channel retail network

spread across India by investing heavily in establishing processes, teams and technology and

infrastructure. As of 31st Mar’19, the company sold its products through 3,598 points of sale

comprising EBOs, LFS and MBOs located across 108 cities in 31 states and UTs in India. TCNS

enters into lease agreements with property owners or into franchises agreements with third

parties for its franchise-owned EBO stores; at present, ~60% of its EBO stores are franchise-

owned stores. In addition, the company has a small international presence with 3 EBO stores

in Sri Lanka, 2 EBO stores in Mauritius and 1 EBO store in Nepal with ~0.5% contribution to

revenues.

Exhibit 14: TCNS has a wide-spread distribution network with a pan India presence

Source: TCNS RHP, Equirus Securities

EBOs41%

LFS47%

MBOs6% Online

6%EBO: 49

LFS: 238

EBO: 50

LFS: 184

EBO: 54

LFS: 68

EBO: 38

LFS: 138EBO: 29

LFS: 39

EBO: 30

LFS: 99

EBO: 21

LFS: 151

EBO: 25

LFS: 113

EBO: 17

LFS: 26

EBO: 19

LFS: 77

EBO: 20

LFS: 49

EBO: 12

LFS: 25

EBO: 11

LFS: 22

EBO: 9

LFS: 30

EBO: 10

LFS: 17

EBO: 10

LFS: 23

EBO: 6

LFS: 54

EBO: 11

LFS: 32

EBO: 7

LFS: 44

EBO: 6

LFS: 10

EBO: 5

LFS: 3

EBO: 5

LFS: 12

EBO: 5

EBO: 3

EBO: 2

LFS: 3

EBO: 1

LFS: 2

EBO: 1

LFS: 1

EBO: 2

LFS: 3

EBO: 2

LFS: 4

EBO: 2

LFS: 1

EBO: 3

LFS: 1

TCNS Clothing Ltd. Absolute – ADD Relative – Overweight 8% ATR in 18 Months

June 28, 2019 Page 10 of 24

TCNS (W & Aurelia combined) has the highest number of stores than any other brands in

the country. Also, it is well spread across the country, unlike other players like Fab India,

BIBA, AND, Global Desi and others which are concentrated and region focused. The top

eight cities, viz. Delhi/NCR, Greater Mumbai, Kolkata, Chennai, Bangalore, Hyderabad,

Ahmedabad and Pune have the highest penetration levels as majority of the consumption

happens in these cities. Apart from these cities, TCNS is also increasing its penetration in

tier 2, 3 and 4 cities because of its high growth potential and a preference shift towards

branded apparels.

Exhibit 15: TCNS (W, Aurelia) has highest number of stores than any other Indian player

Source: Technopak, TCNS RHP, Equirus Securities. *FY19 end numbers

Exhibit 16: Fairly wide presence in all Indian regions

Source: Company, TCNS RHP, Equirus Securities

Expansion in new markets, rising share in existing markets to drive revenue growth

A key driver of the strong 47% revenue CAGR over the last five years for TCNS has been the

rapid expansion of its stores in both new and existing markets. The company had opened

its first EBO in New Delhi in 2002. Since then, it has added its store count at a significant

rate; in the last four years ending FY19, TCNS has more than doubled its store count for

both W and Aurelia brands from a total of 235 stores in FY15 to 541 stores in FY19.

Simultaneously, it has also entered many new markets by EBO and LFS routes to cater to

the unmet demand of smaller towns and cities.

Exhibit 17: Robust store expansion in last four years

Store Counts FY15 FY16 FY17 FY18 FY19 CAGR (FY15-19)

W

EBO 166 202 233 281 321 18%

LFS 302 426 535 717 - -

International Outlets 2 2 5 5 5 26%

Aurelia

EBO 69 103 148 183 215 33%

LFS 263 368 456 752 - -

International Outlets 0 0 1 1 1 -

Wishful

EBO 0 0 0 1 5 -

Total

EBO 235 305 381 465 541 23%

LFS 565 794 991 1,469 1,623 28%

International Outlets 2 2 6 6 6 32%

Multi Brand Outlets 748 960 1,109 1,522 1,428 18%

Source: Company, Equirus Securities.

While the company has a decent presence in most parts of the country, there are many

small pockets or cities in tier 2, 3 and 4 states which are seeing a massive shift towards

branded women’s ethnic wear; this is a major area where the company expects its future

growth to come from. Additionally, there are many areas with very high growth potential

but are served with either few stores or smaller-sized stores and as a result are not able to

realize their full potential. In such areas, the company plans to increase its presence either

through addition of new stores or upgrading stores to bigger sizes with high product

varieties.

321

215

256

141123

276

98

28

0

50

100

150

200

250

300

350

W* Aurelia* BIBA Global Desi AND FabIndia Soch Anokhi

No. of EBO stores

North40%

South25%

East15%

West20%

W

North30%

South35%

East15%

West20%

Aurelia

TCNS Clothing Ltd. Absolute – ADD Relative – Overweight 8% ATR in 18 Months

June 28, 2019 Page 11 of 24

Innovative & institutionalized product design process = Finger on consumer pulse

An inherent threat to any company related to the fashion industry is its inability to respond

to rapidly changing consumer preferences. With a keen focus on design aesthetics and

expertise in identifying a trend, TCNS has been able to align to consumer preferences and

introduce new brands at regular time intervals and managed to scale them successfully.

Trade shows help keep tab on changing consumer preferences

TCNS organizes its own trade shows twice a year, showcasing new offerings for all brands

in the upcoming season. These trade shows are attended by more than 400 channel partners

including distributors, EBO store owners, LFS store managers and MBO stores owners. In

contrast to other trade shows that are organized primarily to secure orders, TCNS’s trade

shows intend to gather feedback on designs, quality, material and fit, and thus accordingly

make changes to its offerings for the new season.

Brainstorming of designs, subsequent screening lead to most preferred designs

A design team of 40-45 members (separate teams of ~12-13 members for Aurelia & ~27-30

members for W/Wishful) starts working around two months prior to the trade week in

bringing out new designs inspired by new stories/events across the world in the fashion

industry. Extensive discussions are carried out on every design story among the team, which

includes members from the design, production, sales and marketing teams, and valuable

inputs are incorporated into the designs. Before these designs are displayed in the trade

show, based on the feedback from the previous season, ~20% of internal dropping happens.

For the rest of the designs, 30-40% of fabric ordering is done and production is started. Rest

of the fabric ordering and production is done on considering feedback from the channel

partners in the trade show.

During the trade show, extensive feedbacks are collected on various designs from the channel

partners & modifications are carried out based on it. Based on the feedback and ratings, the

company finalizes the quantity and season for the product rollout. Such feedback-oriented

design process differentiates TCNS from peers & helps them come up with designs with high

acceptance levels. The final products are then rolled out in phases according to seasons like

monsoon (Jun-Aug), festive (Sep-Oct), winter (Nov-Dec) and summer (Mar-April).

Robust supply chain network provides strong back-end support

TCNS uses raw materials like printed fabrics, unprocessed fabrics and trim materials, which

are sourced from ~181 suppliers across India. It does not enter into long-term sourcing

agreements with supplies, rather issues purchase orders in line with sourcing needs. Based

on the supplier’s production capacity and quantities supplied in the previous season, the

company places orders for the upcoming season. TCNS also assists suppliers in developing

infrastructure and increasing productivity. To maintain standards at each step of sourcing

and the production cycle, it has implemented several quality-control mechanisms, and

regularly conducts inspections of fabrics sourced from suppliers, while supervising the

manufacturing plants. The company’s supply-chain strength is demonstrated from the fact

that it has not faced any attrition in its top-10 suppliers in the last decade.

Constantly refreshed product offerings provide a sense of novelty

It remains the company’s constant endeavor to refresh its product offerings through

innovative designs and optimizing the fit and sizing while adhering to higher quality and

latest trends. On an average, TCNS refreshes product offerings at an average interval of

2-3 weeks, which provides a sense of novelty every time a customer visits a store. Over a

year, the company launches ~2,000 products in various sizes, product materials and designs;

these tend to be widely acceptable as a lot of work is carried out in bringing a new design

including the R&D analysis to emphasize the fit and comfort of its products.

Capital efficient business model, low payback period ensures higher returns

Renting retail outlets & job work manufacturing limit upfront capex requirements

TCNS enters into lease or franchisee agreements for putting up new EBO stores and thus

cuts down on its upfront capex requirements on acquiring a real estate, building the

property and other installation expenses. As of 31st Mar’19, ~40% of its total 541 EBO stores

was on franchisee basis. This business model is also scalable as the company can expand its

geographical reach without locking capital and impacting the existing business and

cashflows. It also helps TCNS minimize losses and costs incurred at the time of shutting

down the non-performing outlets.

Additionally, TCNS completely outsources its production to third-party job workers with

whom it enters into contractual agreements on regular intervals and books the capacity in

advance. This helps the company increase its production capacity as required without

incurring additional capex. To ensure good quality, TCNS conducts regular supervision at

facilities of job workers through supervisors that are either stationed at such facilities or

visit these facilities for inspection at regular intervals.

Store-level breakeven achieved in 18-24 months of operations

Our rough calculation suggests a store-level EBITDA margin of ~28%. On an average,

depending upon the size & area of the store, it is expected to break even anywhere between

18-24 months; this is upon taking into consideration the ramp-up of revenues from the

store.

TCNS Clothing Ltd. Absolute – ADD Relative – Overweight 8% ATR in 18 Months

June 28, 2019 Page 12 of 24

Exhibit 18: Rough calculation suggests an average EBO store breaks even at 18-24

months from start of operations

Particulars Comments

Capex per store

Store Area (sq. ft) 1,000

Capex per sq. ft 3,000 Includes furniture & fixtures

Fixed Assets (Rs mn) 3.0

Inventory Requirement (Rs mn) 3.2 ~4 months inventory stocked

Total upfront capex needed (Rs mn) 6.2

Store level EBITDA

Revenues from EBO stores (FY19;

(Rs mn)) 5,625

EBO store count 503 Avg. store count of FY18 & FY19

Revenue per store (Rs mn) 11.2

Gross Profit (Rs mn) 7.4 Assumed company level gross margins

Rental Expenses (Rs mn) 2.2 Assumed total rental exp as % of EBO

sales for FY19

Employee & other expenses (Rs mn) 2.0 Assumed employee & other exp at 18% of

sales

EBITDA per store (Rs mn) 3.2

EBITDA margin 28%

Estimated Payback period 1.5 -2 years

Source: Company, Equirus Securities.

Like for other players in the industry, MBOs are the most profitable channel for TCNS while

LFS the least profitable. MBOs lead to outright sale to a channel partner without any

investments in capex or inventory; in contrast, LFS ― because of its contractual agreements

of revenue sharing and carrying of inventory on the company’s books ― has the least

margins.

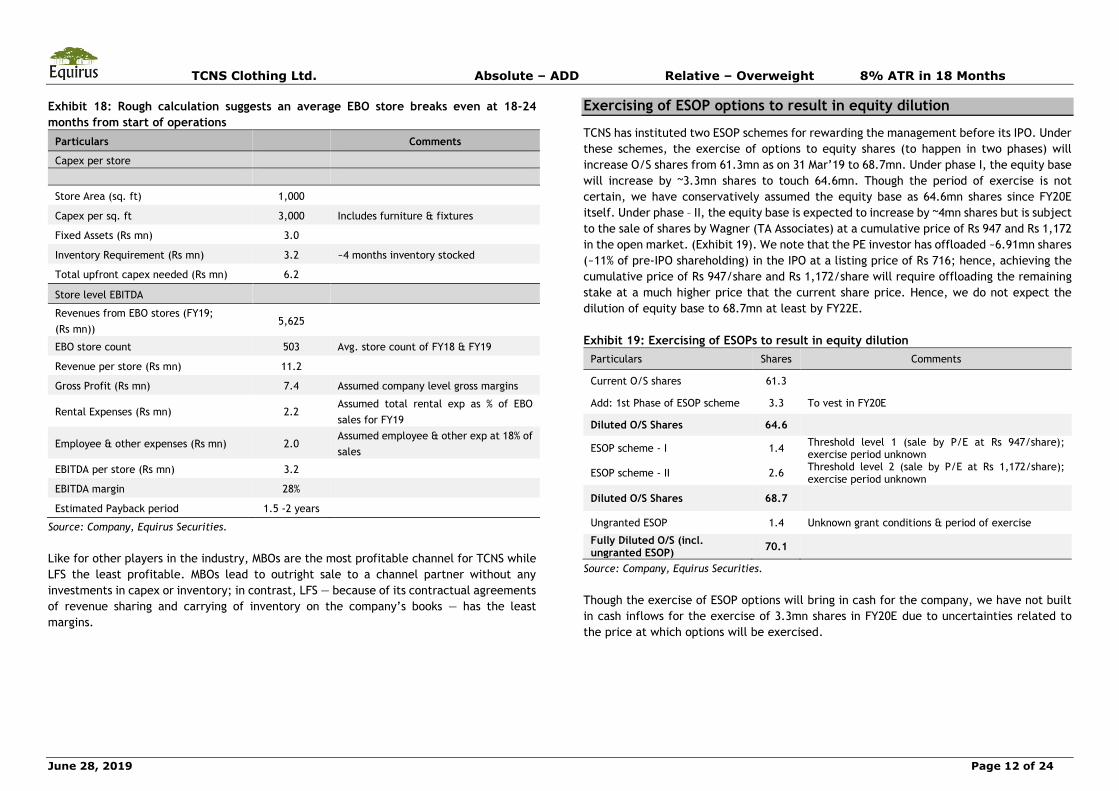

Exercising of ESOP options to result in equity dilution

TCNS has instituted two ESOP schemes for rewarding the management before its IPO. Under

these schemes, the exercise of options to equity shares (to happen in two phases) will

increase O/S shares from 61.3mn as on 31 Mar’19 to 68.7mn. Under phase I, the equity base

will increase by ~3.3mn shares to touch 64.6mn. Though the period of exercise is not

certain, we have conservatively assumed the equity base as 64.6mn shares since FY20E

itself. Under phase – II, the equity base is expected to increase by ~4mn shares but is subject

to the sale of shares by Wagner (TA Associates) at a cumulative price of Rs 947 and Rs 1,172

in the open market. (Exhibit 19). We note that the PE investor has offloaded ~6.91mn shares

(~11% of pre-IPO shareholding) in the IPO at a listing price of Rs 716; hence, achieving the

cumulative price of Rs 947/share and Rs 1,172/share will require offloading the remaining

stake at a much higher price that the current share price. Hence, we do not expect the

dilution of equity base to 68.7mn at least by FY22E.

Exhibit 19: Exercising of ESOPs to result in equity dilution

Particulars Shares Comments

Current O/S shares 61.3

Add: 1st Phase of ESOP scheme 3.3 To vest in FY20E

Diluted O/S Shares 64.6

ESOP scheme - I 1.4 Threshold level 1 (sale by P/E at Rs 947/share); exercise period unknown

ESOP scheme - II 2.6 Threshold level 2 (sale by P/E at Rs 1,172/share); exercise period unknown

Diluted O/S Shares 68.7

Ungranted ESOP 1.4 Unknown grant conditions & period of exercise

Fully Diluted O/S (incl. ungranted ESOP)

70.1

Source: Company, Equirus Securities.

Though the exercise of ESOP options will bring in cash for the company, we have not built

in cash inflows for the exercise of 3.3mn shares in FY20E due to uncertainties related to

the price at which options will be exercised.

TCNS Clothing Ltd. Absolute – ADD Relative – Overweight 8% ATR in 18 Months

June 28, 2019 Page 13 of 24

Financial Profile

Expansion of physical & online presence to drive 17% rev. CAGR over FY19-22E

TCNS has been astute in focusing on markets where demand for its products has been

picking up and was quick to add stores here much before competition. It has more-than-

doubled its EBO store count in the last five years to 541 stores at FY19-end. Going ahead,

we build in 70-75 store additions each over next 2-3 years in tier 2,3 & 4 cities which will

drive the future revenue growth. Additionally, backed by the experience of operating stores

in Nepal, Sri Lanka and Mauritius, the company plans to enhance its international presence

to other Asian countries which are largely similar to Indian markets. However, these

currently form a very small portion of revenues and adding stores in foreign countries would

not add meaningfully to the topline.

Exhibit 20: EBO store additions to continue at same pace as in the past

Source: Company, Equirus Securities

Online medium ― A platform to reach undiscovered places

Apart from its brick & mortar presence, TCNS sells products through online retailers like

Myntra, Jabong and Amazon and also through its own websites wforwoman.com and

shopforaurelia.com. There is a massive surge seen in demand for branded women’s ethnic

wear products in smaller cities and towns which is catered to through online channels.

Presence on the online platform helps the company identify demand trends of a particular

region, thus providing key inputs for opening a new store in a specific region. Online

revenues for TCNS have grown at a robust ~70% CAGR over FY16-FY19, albeit off a low base,

and contributed ~14% of its overall revenues in FY19 (FY16: ~7%). We expect strong growth

in online revenues to continue ahead as well given the rising preferences of online shopping

and an enhanced consumer base that online channels provide to the company.

Blocks falling in place for Wishful

TCNS has seen strong growth in its W and Aurelia brand revenues over the last 5 years;

however, it could not scale up in its Wishful brand due to lack of quality suppliers which

can manufacture complex products like Wishful. The company has recently tied up with 3-

4 manufacturing units that match the required skillset and manufacturing capabilities

required to produce Wishful garments. With supply constraints resolved, we expect Wishful

revenues to pick up as management plans to increase the brand’s presence in its W stores.

TCNS opened four new Wishful stores in FY19, taking the total to 5 stores. The shop-in-shop

concept within W stores is working better than exclusive Wishful stores; hence, the

company is not likely to open exclusive Wishful stores going ahead.

Complementary product line extension ― a new growth driver

TCNS has recently added jewelry as a category extension to its product offerings. These

include finger rings, earrings & necklaces with a price range of Rs 300 to Rs 2,000. It has

also added footwear on pilot basis in some stores. These complementary products being a

very small part of revenues cannot be a significant growth diver for total revenues but can

surely provide some boost to overall revenue growth.

New brands acquisition ― Looking for inorganic growth

Apart from organic growth coming from scaling up existing brands, the company is also

actively looking for inorganic growth opportunities in the form of new brand acquisitions or

acquiring a new business. The company’s target is to acquire business that has high

customer traction; but lacks in terms of either management bandwidth or financial strength

or inefficiencies in managing the scale and thus are not able to ramp up. Such businesses

have the potential of ramping up quickly and thus match the value proposition of the

company’s existing brands. While the potential business necessarily needs to be a women’s

wear segment, it could be in the category of western wear, footwear, or even women

undergarments.

Overall revenues to 17% CAGR over FY19-22E

TCNS saw some slowdown in FY19 revenues due to the following: (1) 1H was impacted by a

high base of H1FY18 (pre-GST sales) and ERP implementation. (2) 2H was hit by a sharp dip

in its sales of airport stores due to Jet Airways crisis (N.B.: Airport stores contribute ~10%

of EBO revenues) and a reduction in EOSS period which somewhat impacted sales.

305 381 465 541 616 686 756

7076

84

76 75 7070

0

10

20

30

40

50

60

70

80

90

0

100

200

300

400

500

600

700

800

FY16 FY17 FY18 FY19 FY20E FY21E FY22E

EBO stores LHS Store Additions - RHS

TCNS Clothing Ltd. Absolute – ADD Relative – Overweight 8% ATR in 18 Months

June 28, 2019 Page 14 of 24

Going ahead, we expect revenues to be impacted in near term due to prevailing demand

sluggishness & muted recovery of airport store revenues. However, these issues seem to be

temporary & are expected to be resolved soon. We expect overall revenues to grow at a

17% CAGR over FY19-FY22E driven by (1) rising revenues from existing stores, (2) addition

of 70-75 stores each year over the next two years, (3) continued robust growth in online

revenues, (4) resolution of supply constraints for Wishful products leading to strong growth

in the brand’s revenues, and (5) additional revenue stream coming from complementary

products. At a brand level, we expect W/Aurelia/Wishful revenues to grow at 18%/15%/21%

CAGR over FY19-FY22E.

Exhibit 21: Brand-wise revenue growth estimates

Particulars (In Rs Mn) FY18 FY19 FY20E FY21E FY22E CAGR (19-22E)

W Revenues 5,748 6,888 8,093 9,550 11,297 18%

Growth YoY 34% 20% 18% 18% 18%

Aurelia Revenues 3,358 3,903 4,449 5,117 5,900 15%

Growth YoY 55% 16% 14% 15% 15%

Wishful Revenues 865 689 827 1,008 1,230 21%

Growth YoY 54% -20% 20% 22% 22%

Source: Company, Equirus Securities

Exhibit 22: Overall revenues to grow at 17% CAGR over FY19-22E

Source: Company, Equirus Securities

Rise in operational efficiencies to drive 18% adj. EBITDA CAGR over FY19-

FY22E

In the past, TCNS’s gross margins have remained very volatile driven by GST-related

changes, implementation of Ind-AS 115 and reclassification of some line items. Gross

margins expanded ~480bps over FY15-FY17 to reach ~81% driven by effective sourcing,

better terms for job work and scale benefits coming in. However, in FY18, implementation

of GST ― that taxed apparels below MRP of Rs 1,000 at 5% and above MRP of Rs 1,000 at

12% ― led to a major reshuffling in apparel prices, resulting in some gross margin

contraction. Additionally, in FY19, some costs like fabrication charges, product

development charges and consumption of packaging materials were moved from other

expenses to COGS, leading to stabilization of gross margins at 66%.

Going ahead, we expect flattish gross margins over FY19-22E as benefits of shifting of

production out of the NCR region (currently ~10% manufacturing has shifted out of NCR);

will take some time to accrue.

Exhibit 23: Modest gross margin expansion ahead as gains from shifting production

out of NCR will take time to accrue

Source: Company, Equirus Securities

4.9 7.0 10.0 11.5 13.4 15.7 18.4

61%

44%42%

15% 16%17% 18%

0%

10%

20%

30%

40%

50%

60%

70%

0

2

4

6

8

10

12

14

16

18

20

FY16 FY17 FY18 FY19 FY20E FY21E FY22E

Revenues (In Rs Bn) Growth YoY

3.8 5.7 6.5 7.6 8.8 10.4 12.2

78.6% 81.1%

65.7% 66.0% 66.1% 66.2% 66.2%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0

2

4

6

8

10

12

14

FY16 FY17 FY18 FY19 FY20E FY21E FY22E

Gross Profit (In Rs Bn) Gross Margin

TCNS Clothing Ltd. Absolute – ADD Relative – Overweight 8% ATR in 18 Months

June 28, 2019 Page 15 of 24

Lower discounting, better operating efficiencies largely drive EBITDA growth

Reduction in EOSS: TCNS is making constant efforts to reduce its EOSS period and increase

the share of full-price sales as heavy discounts offered in EOSS hurt its margins. For the

monsoon season in FY19, it reduced its EOSS period by one week; this did hurt its sales

somewhat but was beneficial to its margins. Going ahead, it plans to reduce the EOSS period

by a week for both seasons, which will aid margins to some extent.

Rise in operating efficiencies: TCNS has added ~160 EBO stores and ~632 LFS stores in last

two years, which are expected to achieve higher operating efficiencies with rising footfalls

and increasing sales. Additionally, several new stores to be added in the near future will be

in tier 2,3, 4 cities that will have lower rent and other fixed costs, resulting in faster

breakeven and higher profitability.

In the past, due to ESOP expenses, employee costs have remained very volatile. A major

part of ESOP-related expenses have been incurred in the past, and hence such expenses are

unlikely to significantly hurt margins in the future. Adjusted for ESOP expenses, EBITDA has

grown at a 31% CAGR over FY16-FY19. We expect adj. EBITDA/reported EBITDA to grow at

18%/21% CAGR over FY19-FY22E mainly driven by a rise in operating efficiencies.

Exhibit 24: ESOP expenses have hit profitability in the past; less impact to be felt in

future

Source: Company, Equirus Securities

Exhibit 25: Adj. EBITDA to grow at ~18% CAGR with ~60bps EBITDAM expansion over

FY19-22E

Source: Company, Equirus Securities

Strong cashflow generation to continue

Despite continuous store addition in the past, TCNS has consistently generated positive

operating cashflows mainly due to improving profitability and a strict control over working

capital. Except for FY17, where higher tax payment on account of share-based payments

resulted in lower OCF generation, the company’s operating cashflows have continuously

seen an uptrend, in line with revenue growth. Going ahead, with normalization of the tax

rate at ~35% (as tax benefits of ESOP were largely taken in FY19), capex pegged at

~Rs 450-500mn each for next 3 years, and limited growth in WC requirements, we expect

strong OCF generation of Rs 0.9bn/1.2bn in FY20E/FY21E. With nil debt on books, FCF

generation too will remain stronger at Rs 0.3/0.7bn in FY20E/FY21E.

898

737

215165

100 9050

0

100

200

300

400

500

600

700

800

900

1,000

FY16 FY17 FY18 FY19 FY20E FY21E FY22E

ESOP Expenses (In Rs Mn)

0.9 1.5 1.8 1.9 2.3 2.7 3.2

17.7%

21.4%

17.7%16.8% 17.2%

17.3%17.4%

0%

5%

10%

15%

20%

25%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

FY16 FY17 FY18 FY19 FY20E FY21E FY22E

Adj. EBITDA (In Rs Bn) EBITDAM

TCNS Clothing Ltd. Absolute – ADD Relative – Overweight 8% ATR in 18 Months

June 28, 2019 Page 16 of 24

Exhibit 26: Limited capex & strict control on WC will lead to strong cashflow generation

Source: Company, Equirus Securities

Increase in equity base, high cash balance to drag ROE; core ROIC to say strong at ~26%

Apart from a marginal increase in the equity base (due to increase in equity base from

61.3mn shares to 64.6mn on exercise of ESOP options), ROE will be impacted by high

cashflow generation and no plans of declaring dividend as TCNS is looking for inorganic

growth opportunities (some brand/business acquisition). We expect ROE to normalize from

25% in FY19 to 20% in FY20 & FY21 each while adj. core ROIC is expected to remain strong

at ~26% over next 3 years.

Exhibit 27: ROE/Adj. core ROIC to normalize to 20%/26% in FY20 & FY21 resp.

Source: Company, Equirus Securities

Working capital days to increase marginally

TCNS has very strict control over its working capital ― a key concern for most peers in the

fashion industry. There was a marginal increase in WC days in FY19 due to (1) some rise in

its RM inventory on account of shifting of production out of NCR and (2) a decline in payable

days as early payment was made to creditors to gain some extra benefits. We have built in

some increase in WC days going ahead owing to (a) the current liquidity crunch in the

market and (b) a marginal increase in receivable days with some leeway given to

distributors to boost sales. Though the increase would be temporary, we expect WC days

to rise from 103 in FY19 to ~108 in FY20E-21E each.

Exhibit 28: Marginal increase in NWC days

Source: Company, Equirus Securities

344251

413

906 894

1,248

1,505

154

-13

142

521

302

732

989

-200

0

200

400

600

800

1,000

1,200

1,400

1,600

FY16 FY17 FY18 FY19 FY20E FY21E FY22E

OCF (In Rs Mn) FCF (In Rs Mn)

10%

28%25%

20% 20% 20%

10%

29%

25% 26% 26%28%

0%

5%

10%

15%

20%

25%

30%

35%

FY17 FY18 FY19 FY20E FY21E FY22E

ROE Core ROIC

1.7 2.6 3.2 4.0 4.7 5.6

9096

103108 108 109

0

20

40

60

80

100

120

0

1

2

3

4

5

6

FY17 FY18 FY19 FY20E FY21E FY22E

NWC (in Rs Bn) NWC days - RHS

TCNS Clothing Ltd. Absolute – ADD Relative – Overweight 8% ATR in 18 Months

June 28, 2019 Page 17 of 24

Forecast & key assumptions

• Overall revenues to grow at 17% CAGR over FY19-FY22E.

• W/Aurelia/Wishful revenues expected to grow at 18%/15%/21% CAGR over FY19-FY22E.

• We expect 75 EBO stores addition in FY20E and 70 stores in FY21E. Capex would be in

the range of Rs 420-450mn per annum over next 3 years.

• Gross margins are expected to see remain flattish while adj. EBITDA margin, on account

of operational efficiencies, is expected to grow by ~60bps over FY19-FY22E to reach

17.4% in FY22E.

Exhibit 29: Key Assumptions

Particulars (In Rs Mn) FY19 FY20E FY21E FY22E

W Revenues 6,888 8,093 9,550 11,297

Aurelia Revenues 3,903 4,449 5,117 5,900

Wishful Revenues 689 827 1,008 1,230

Capex 217 450 420 420

NWC Days 103 108 108 109

Source: Company, Equirus Securities

Investment risk & concerns

Inability to anticipate & respond to change in fashion trends & consumer preferences:

TCNS has a strong track record of bringing innovative designs across its brands in an ever-

changing fashion market, leading to high acceptance levels. However, any failure to

anticipate or respond to such changing customer preferences and design new products can

hurt revenues & margins.

Concentration of job work manufacturing units: TCNS outsources its entire manufacturing

to third party job work manufacturing units. Despite shifting ~10% of manufacturing out of

the NCR region in FY19, ~90% of manufacturing is still carried out in the region. Any

political, economic or natural unrest in the NCR region can disrupt manufacturing and thus

adversely hit revenues and margins.

Delay in stores expansion & sales pickup: A major part of future revenue growth will come

from store expansion in tier 2,3, 4 cities and a subsequent pick up in sales from these stores.

Any delay in expansion of retail outlets and corresponding pickup in sales from newer and

existing outlets can negatively affect TCNS’s revenue growth.

Corporate Governance

Key highlights on corporate governance based on TCNS’s RHP:

• Company accounts are audited by M/s. Deloitte Haskins & Sells, CA. The reports and

findings of the Internal Auditor and the internal control system are periodically

reviewed.

• TCNS is a professionally managed company. Onkar Singh Pasricha and Arvinder Singh

Pasricha are promoters of the company, with more than 20 years of experience in the

apparel industry.

• Anant Daga, the MD, has been associated with TCNS for more than seven years, and

prior to that worked with Reebok India. TCNS’ other senior leadership team comprising

nine heads of department have an average of 15 years of experience in the apparel

and clothing industry.

• The Board of Directors has an optimum combination of Executive, Non-Executive and

Independent Directors, including women directors. The Board comprises one whole-

time directors (MD), one Non-Executive Director and three Independent Directors.

Except for the non-executive Director, all other directors (including MD) are liable to

retire by rotation.

• TCNS has not paid any dividend till date as, with the accumulated cash, it plans to

acquire a new brand or a business in the women’s wear industry. Also, it continues to

expand its presence by adding 70-75 stores per annum in new areas/geographies. All

these will utilize existing cash with the company & might even necessitate TCNS to

take on some debt.

• Related Party Transactions: The company has entered into related party transactions

with TCNS Ltd., a group company which is into the business of providing job work

activities for production of women’s ethnic wear apparels, lease of EBO stores & sale

and purchase of goods. The following table elaborates the payments made by the

company to TCNS Ltd. from FY15 to FY18 for fabrication services provided.

Exhibit 30: Fabrication charges paid by TCNS to group company

Particulars (In Rs Mn) FY15 FY16 FY17 FY18

Fabrication costs paid to group co. 284 331 379 393

as % of total fabrication costs 50% 39% 30% 26%

as % of total expenses 20% 6.6% 5.8% 5.6%

Trade Payables to TCNS Ltd. 30 25 70 80

as % of total trade payables 4% 2% 6% 7%

Source: TCNS RHP, Equirus Securities

TCNS Clothing Ltd. Absolute – ADD Relative – Overweight 8% ATR in 18 Months

June 28, 2019 Page 18 of 24

Peer Analysis

No listed peer in women’s ethnic wear space; BIBA, Fab India, Global Desi ―

the closest unlisted peers

TCNS is the only listed player in the women’s ethnic wear apparel market. Its closest peers would be BIBA, Fab India and Global Desi.

Revenue growth for TCNS has been the highest amongst its peers over FY16-FY18. TCNS,

BIBA and Global Desi (HAD) generated almost similar revenues in FY16; however, over the

next two years, TCNS’s revenues grew at staggering rate of 43% CAGR while BIBA/Global

Desi grew at 13%/8%. Fab India, which was almost double the size of TCNS in revenues in

FY16, grew at 8% CAGR; TCNS with a robust 43% CAGR almost reached the size of Fab India

in FY18.

Return ratios for TCNS have been higher than its peers driven by strict control on working

capital and lower invested capital than peers.

Exhibit 31: TCNS has superior financials amongst its peers

Particulars (In Rs Mn) TCNS Clothing BIBA Fab India Global Desi

Comments FY16 FY17 FY18 FY19 FY16 FY17 FY18 FY16 FY17 FY18 FY16 FY17 FY18

Revenue 4,854 7,009 9,971 11,480 4,278 4,573 5,435 9,105 10,277 10,576 4,139 4,521 4,819 For the period of FY16-18, TCNS had the highest growth amongst peers Growth (%) 61% 44% 42% 15% 13% 7% 19% 20% 13% 3% 29% 9% 7%

EBITDA 860 1,499 1,769 1,933 1,059 492 983 1,637 1,754 1,812 631 532 427

EBITDA Margin (%) 18% 21% 18% 17% 25% 11% 18% 18% 17% 17% 15% 12% 9% TCNS' EBITDA margins in-line with peers

PAT -415 158 981 1,314 608 206 478 931 901 1,181 315 236 126

PAT Margin (%) - 2% 10% 11% 14% 4% 9% 10% 9% 11% 8% 5% 3%

CFO 344 251 413 906 418 -325 -106 837 1,259 1,363 326 87 229 CFO & CFO/EBITDA (%) highest for FabIndia. TCNS has a scope of improvement in reducing its WC days. CFO/EBITDA (%) 40% 17% 23% 47% 40% NA NA 51% 72% 75% 52% 16% 54%

Receivable Days 48 52 57 57 19 21 23 3 2 4 15 17 24

Payable Days 64 57 42 37 20 35 25 12 9 12 28 41 40

Inventory Days 103 101 82 87 140 185 187 100 95 92 75 107 96

Cash Conversion Cycle 88 96 98 108 139 171 185 91 88 84 63 83 79 Cash conversion cycle largely in-line with peers

Total Debt 382 88 2 0 7 465 929 337 922 544 87 328 317

Cash & Cash Equivalents 103 132 512 1,608 126 21 61 136 137 166 376 456 471

Net D/E 0.6 0.0 -0.1 -0.3 0.0 0.2 0.3 0.1 0.1 0.1 -0.1 0.0 -0.1

ROE (%) -52% 10% 28% 25% 28% 8% 17% 25% 18% 19% 14% 9% 5% Despite high cash, ROE ratio highest for TCNS

ROIC (%) -26% 8% 27% 24% 28% 8% 15% 23% 17% 18% 13% 9% 5% ROIC ratio highest for TCNS

Source: MCA, Equirus Securities

TCNS Clothing Ltd. Absolute – ADD Relative – Overweight 8% ATR in 18 Months

June 28, 2019 Page 19 of 24

Valuations

We like TCNS because of (1) its leadership position in branded women’s ethnic wear market,

(2) strong and highly penetrated retail network with a pan-India presence, (3) robust supply

chain network (4) debt-free balance sheet, (5) highly-controlled working capital, and (6)

superior return ratios.

At CMP of Rs 781, the stock trades at 38x/33x P/E of FY20E/21E. When compared with the

closest listed industry peers, on an EV/EBITDA basis (as P/E ratio will be distorted due to

different capital structure and number of O/S shares of peer companies), TCNS trades at

an EV/EBITDA of 21x/17.4x for FY20E/FY21E, which is much higher than the median industry

EV/EBITDA of 14x/11x for Indian peers & 9.5x/9x for global peers for FY20E/21E.

We believe that the stock is expensive in light of a few concerns related to the overall

sluggish demand, liquidity crunch in the market and a slowdown in airport sales (~10% of

revenues) with Jet Airways shutting shop. However, acquisition of a brand/business with a

strong growth potential and subsequent scale up in line with its existing brands remains an

upside risk to our estimates.

We initiate coverage on the stock with ADD with a PT of Rs 872 and value it at 35x P/E to

Dec’20 TTM EPS of Rs 25.

Some of the P/E deals in the sector in the past

Attracted by the women’s apparel industry growth, TCNS Ltd. & other industry players have

seen some private equity investors infusing funds in the past. The following table shows

some of such P/E deals in TCNS & other industry players:

Date Target Trans. Type

Buyer Seller Deal Value

($ Mn)

18-10-2011 TCNS Clothing P/E Matrix Partners India LLC - 12

09-07-2013 TCNS Clothing P/E Matrix Partners India LLC - 4.9

08-08-2016 TCNS Clothing P/E TA Associates Advisory Pvt Ltd.

Matrix Partners India LLC

139.1

04-09-2013 Biba Apparels Pvt. Ltd.

P/E Warburg Pincus India Pvt. Ltd., Faering Capital India Evolving Fund

Future Consumer Ent. Investment Arm

51.1

01-04-2014 Ritu Kumar P/E Everstone Cap. Ritu Kumar 16.6

01-09-2015 Creative Lifestyle Pvt. Ltd.

P/E Aditya Birla P/E Sunrise Fund

- 5.3

Source: VCCEdge, Equirus Securities

Exhibit 32: Relative valuation of TCNS with other closest listed Indian & global peers

Company Unit Price (Rs.) M Cap (Bn) Sales CAGR

EBITDA Margin (%) EPS CAGR Net D/E P/E EV/EBITDA ROE ROIC

Indian Peers (FY19-21E) FY19 FY20E FY21E (FY19-21E) FY19 FY19 FY20E FY21E FY19 FY20E FY21E FY19 FY20E FY21E FY19

Page Ind. INR 20,470 2,28 10.0% 21.6% 21.8% 22.1% 11.6% 0.0 58.0 49.8 41.7 37.1 32.1 27.2 49% 51% 50% 43%

ABFRL INR 205 158 8.9% 6.8% 7.8% 8.6% 6.7% 0.8 49.3 56.8 60.3 30.6 23.4 18.8 25% 17% 21% 15%

Arvind fashions INR 689 40 17.2% 6.2% 7.1% 7.7% 144.8% 0.7 242 43.5 31.0 16.9 13.3 10.3 2% 8% 10% 13%

Future Lifestyle INR 445 86 24.8% 9.2% 9.2% 7.9% 16.0% 0.4 45.8 39.6 29.4 17.7 14.4 9.9 11% 12% 14% 11%

Shoppers Stop INR 475 42 7.8% 6.9% 7.6% 8.1% 33.9% 0.0 64.3 33.3 26.8 16.9 13.5 11.0 7% 12% 13% 6%

Kewal Kiran INR 1,150 14 4.7% 22.4% 23.1% 23.7% 6.2% -0.1 17.7 16.2 14.7 12.2 11.1 10.0 19% 20% 21% 14%

Median 9.5% 8.0% 8.5% 8.3% 13.8% 0.2 53.6 41.6 30.2 17.3 13.9 10.6 15% 15% 17% 14%

Global Peers

H&M SEK 147 2,43 3.9% 12.0% 11.9% 12.1% 2.5% 0.1 19.3 19.6 18.3 10.0 9.5 9.0 20% 22% 24% 16%

Inditex EUR 25 77 4.4% 20.7% 27.3% 27.4% 9.2% 0.0 22.8 20.5 19.1 13.3 9.3 8.6 27% 25% 26% 21%

Median 4.2% 16.3% 19.6% 19.8% 5.8% 0.1 21.0 20.1 18.7 11.7 9.4 8.8 23% 24% 25% 18%

TCNS Clothing 782 49 17.2% 15.4% 16.4% 16.7% 8.6% 0.0 38.4 38.3 32.6 26.3 21.0 17.4 25% 19% 19% 30%

Source: Bloomberg consensus figures, Equirus Securities

TCNS Clothing Ltd. Absolute – ADD Relative – Overweight 8% ATR in 18 Months

June 28, 2019 Page 20 of 24

Exhibit 33:TTM P/E vs. 1 year forward EPS Growth

Exhibit 34:TTM EV/EBITDA vs. 1 year forward EBITDA Growth

Source: Equirus Securities

Exhibit 35:TTM P/B vs. 2 year forward RoE

Source: Equirus Securities

Key Management profile

Onkar Singh Pasricha, aged 68 years, is the Chairman, executive Director and one of the

Promoters of our Company. He holds a bachelor’s degree in technology in electrical

engineering from Indian Institute of Technology, Delhi. He has been on our Board since

December 3, 1997 and was last re-appointed on January 5, 2018. He has more than 40 years

of experience in the apparel industry.

Anant Kumar Daga, aged 42 years, is the Managing Director of our Company. He holds a

bachelor’s degree in commerce from the University of Calcutta and a post-graduate diploma

in management from Indian Institute of Management, Ahmedabad. He joined our Company

as a Chief Executive Officer with effect from March 16, 2010 and has been on the Board

since September 7, 2016. Prior to joining our Company, Anant Kumar Daga has worked with

Reebok, India as director (sales) and with ICICI bank. He also features in the Economic

Times’ 40 under 40 list of India’s hottest business leaders for 2017 and has been awarded

the “Brand Professional of the Year Award” at the CMAI Apex Awards 2017.

26x

34x

30x

38x

42x

7%

8%

9%

10%

400

500

600

700

800

900

1,000

1,100

Jul-

18

Sep-1

8

Nov-

18

Jan-1

9

Mar

-19

May

-19

Jul-

19

Sep-1

9

Nov-

19

Jan-2

0

Mar

-20

May

-20

Jul-

20

Sep-2

0

Nov-

20

EPS Growth

20%

22%

24%

26%

28%

30%

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Aug-

18

Oct

-18

Dec

-18

Feb

-19

Apr-

19

Jun-1

9

Aug-

19

Oct

-19

Dec

-19

Feb

-20

Apr-

20

Jun-2

0

Aug-

20

Oct

-20

Dec

-20

24x

18x

21x

27x

30xEBITDAGrowth

0%

5%

10%

15%

20%

25%

30%

400

600

800

1,000

1,200

1,400

Aug-

18

Oct

-18

Dec

-18

Feb

-19

Apr-

19

Jun-1

9

Aug-

19

Oct

-19

Dec

-19

Feb

-20

Apr-

20

Jun-2

0

Aug-

20

Oct

-20

Dec

-20

RoE

6x

7x

8x

10x

9x

TCNS Clothing Ltd. Absolute – ADD Relative – Overweight 8% ATR in 18 Months

June 28, 2019 Page 21 of 24

Consolidated Quarterly Earnings Forecast and Key Drivers Rs in Mn 1Q19A 2Q19A 3Q19A 4Q19A 1Q20E 2Q20E 3Q20E 4Q20E 1Q21E 2Q21E 3Q21E 4Q21E FY19A FY20E FY21E FY22E

Revenue 2,366 3,205 3,002 2,907 3,142 3,543 3,449 3,235 3,840 4,154 4,013 3,668 11,480 13,369 15,675 18,427 Raw Material 757 1,098 946 1,099 1,052 1,205 1,155 1,120 1,279 1,421 1,344 1,254 3,899 4,532 5,298 6,214

Employee Cost 339 374 379 346 389 393 415 373 441 459 456 459 1,438 1,571 1,814 2,068

Other Expenditure 979 1,163 1,170 1,062 1,219 1,306 1,323 1,226 1,472 1,480 1,487 1,510 4,374 5,074 5,949 6,984 EBITDA 292 570 507 400 481 639 556 517 648 795 725 445 1,768 2,193 2,614 3,162 Depreciation 51 53 55 63 73 73 73 73 96 96 96 96 222 293 382 475 EBIT 241 517 452 336 408 565 483 444 553 699 630 350 1,546 1,900 2,232 2,687 Interest 1 1 0 3 2 2 2 2 2 2 2 2 5 7 7 7 Other Income 18 19 21 16 28 32 31 29 35 37 36 33 75 120 141 166 PBT 259 536 472 350 434 595 512 471 586 735 664 381 1,616 2,013 2,366 2,846 Tax 54 123 102 23 150 205 177 163 202 254 229 131 302 694 816 982 PAT bef. MI & Assoc. 205 412 371 327 284 390 335 309 384 481 435 249 1,314 1,318 1,549 1,864 Minority Interest 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 Profit from Assoc. 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 Recurring PAT 205 412 371 327 284 390 335 309 384 481 435 249 1,314 1,318 1,549 1,864 Extraordinaries 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 Reported PAT 205 412 371 327 284 390 335 309 384 481 435 249 1,314 1,318 1,549 1,864

EPS (Rs) 3.17 6.38 5.74 5.06 4.40 6.04 5.19 4.78 5.94 7.45 6.74 3.86 20.35 20.41 23.99 28.86

Key Drivers

W revenues - - - - - - - - - - - - 6,888 8,093 9,550 11,297 Aurelia Revenues - - - - - - - - - - - - 3,903 4,449 5,117 5,900 Wishful revenues - - - - - - - - - - - - 689 827 1,008 1,230 - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

- - - - - - - - - - - - - - - - -

Sequential Growth (%)

Revenue -8 % 35 % -6 % -3 % 8 % 13 % -3 % -6 % 19 % 8 % -3 % -9 % - - - - Raw Material -24 % 45 % -14 % 16 % -4 % 14 % -4 % -3 % 14 % 11 % -5 % -7 % - - - - EBITDA -10 % 95 % -11 % -21 % 20 % 33 % -13 % -7 % 25 % 23 % -9 % -39 % - - - - EBIT -12 % 115 % -13 % -26 % 21 % 39 % -15 % -8 % 25 % 27 % -10 % -44 % - - - - Recurring PAT -17 % 102 % -10 % -12 % -13 % 37 % -14 % -8 % 24 % 26 % -10 % -43 % - - - -

EPS -23 % 102 % -10 % -12 % -13 % 37 % -14 % -8 % 24 % 26 % -10 % -43 % - - - -

Yearly Growth (%)

Revenue 4 % 20 % 22 % 13 % 33 % 11 % 15 % 11 % 22 % 17 % 16 % 13 % 15 % 16 % 17 % 18 % EBITDA -28 % 35 % 26 % 24 % 65 % 12 % 10 % 29 % 35 % 25 % 30 % -14 % 14 % 24 % 19 % 21 % EBIT -35 % 35 % 25 % 24 % 69 % 9 % 7 % 32 % 36 % 24 % 30 % -21 % 11 % 23 % 17 % 20 % Recurring PAT 1 % 82 % 36 % 32 % 39 % -5 % -10 % -6 % 35 % 23 % 30 % -19 % 44 % 0 % 18 % 20 %

EPS -18 % 64 % 35 % 24 % 39 % -5 % -10 % -6 % 35 % 23 % 30 % -19 % 34 % 0 % 18 % 20 %

Margin (%)

EBITDA 12 % 18 % 17 % 14 % 15 % 18 % 16 % 16 % 17 % 19 % 18 % 12 % 15 % 16 % 17 % 17 % EBIT 10 % 16 % 15 % 12 % 13 % 16 % 14 % 14 % 14 % 17 % 16 % 10 % 13 % 14 % 14 % 15 % PBT 11 % 17 % 16 % 12 % 14 % 17 % 15 % 15 % 15 % 18 % 17 % 10 % 14 % 15 % 15 % 15 %

PAT 9 % 13 % 12 % 11 % 9 % 11 % 10 % 10 % 10 % 12 % 11 % 7 % 11 % 10 % 10 % 10 %

TCNS Clothing Ltd. Absolute – ADD Relative – Overweight 8% ATR in 18 Months

June 28, 2019 Page 22 of 24

Consolidated Financials

P&L (Rs Mn) FY19A FY20E FY21E FY22E Balance Sheet (Rs Mn) FY19A FY20E FY21E FY22E Cash Flow (Rs Mn) FY19A FY20E FY21E FY22E

Revenue 11,480 13,369 15,675 18,427 Equity Capital 123 129 129 129 PBT 1,616 2,013 2,366 2,846

Op. Expenditure 9,711 11,176 13,061 15,266 Reserve 6,063 7,381 8,892 10,698 Depreciation 222 293 382 475

EBITDA 1,768 2,193 2,614 3,162 Networth 6,186 7,511 9,021 10,827 Others 0 0 0 0

Depreciation 222 293 382 475 Long Term Debt 0 0 0 0 Taxes Paid 302 694 816 982

EBIT 1,546 1,900 2,232 2,687 Def Tax Liability 144 169 194 219 Change in WC (630) (717) (684) (834)

Interest Expense 5 7 7 7 Minority Interest 0 0 0 0 Operating C/F 906 894 1,248 1,505

Other Income 75 120 141 166 Account Payables 1,150 1,392 1,632 1,918 Capex (273) (547) (470) (470)

PBT 1,616 2,013 2,366 2,846 Other Curr Liabi 379 418 490 558 Change in Invest (116) (50) (50) (50)

Tax 302 694 816 982 Total Liabilities & Equity 7,859 9,489 11,337 13,523 Others 0 0 0 0

PAT bef. MI & Assoc. 1,314 1,318 1,549 1,864 Net Fixed Assets 592 749 787 732 Investing C/F (389) (597) (520) (520)

Minority Interest 0 0 0 0 Capital WIP 3 50 50 50 Change in Debt (2) 0 0 0

Profit from Assoc. 0 0 0 0 Others 877 977 1,077 1,177 Change in Equity 557 7 0 0

Recurring PAT 1,314 1,318 1,549 1,864 Inventory 2,741 3,296 3,865 4,544 Others 25 25 (14) (33)

Extraordinaires 0 0 0 0 Account Receivables 1,807 2,198 2,577 3,029 Financing C/F 580 32 (14) (33)

Reported PAT 1,314 1,318 1,549 1,864 Other Current Assets 230 282 331 389 Net change in cash 1,097 329 714 952

FDEPS (Rs) 20.3 20.4 24.0 28.9 Cash 1,608 1,937 2,651 3,602 RoE (%) 25 % 19 % 19 % 19 %

DPS (Rs) 0.0 0.0 0.5 0.8 Total Assets 7,859 9,489 11,337 13,523 RoIC (%) 24 % 19 % 18 % 18 %

CEPS (Rs) 25.1 25.0 29.9 36.2 Non-cash Working Capital 3,249 3,967 4,651 5,485 Core RoIC (%) 30 % 25 % 25 % 26 %

FCFPS (Rs) 8.5 4.7 11.3 15.3 Cash Conv Cycle 103.3 108.3 108.3 108.6 Div Payout (%) 0 % 0 % 3 % 3 %

BVPS (Rs) 100.9 116.3 139.7 167.6 WC Turnover 3.5 3.4 3.4 3.4 P/E 38.4 38.3 32.6 27.1

EBITDAM (%) 15 % 16 % 17 % 17 % FA Turnover 19.3 16.7 18.7 23.6 P/B 7.7 6.7 5.6 4.7

PATM (%) 11 % 10 % 10 % 10 % Net D/E (0.3) (0.3) (0.3) (0.3) P/FCFF 91.8 167.2 68.9 51.0

Tax Rate (%) 19 % 35 % 35 % 35 % Revenue/Capital

Employed 2.1 1.9 1.9 1.8 EV/EBITDA 26.3 21.0 17.4 14.1

Sales Growth (%) 15 % 16 % 17 % 18 % Capital Employed/Equity 1.0 1.0 1.0 1.0 EV/Sales 4.0 3.5 2.9 2.4

FDEPS Growth (%) 34 % 0 % 18 % 20 % Dividend Yield (%) 0.0 % 0.0 % 0.1 % 0.1 %

TTM P/E vs. 2 yr forward EPS growth

TTM EV/EBITDA vs. 2 yr forward EBITDA growth

TTM P/B vs. 2 yr forward RoE

26x

34x

30x

38x

42x

7%

8%

9%

10%

400

500

600

700

800

900

1,000

1,100

Aug-

18

Oct

-18

Dec

-18

Feb-

19

Apr-

19

Jun-

19

Aug-

19

Oct

-19

Dec

-19

Feb-

20

Apr-

20

Jun-

20

Aug-

20

Oct

-20

Dec

-20

EPS Growth

20%

22%

24%

26%

28%

30%

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Aug-

18

Oct

-18

Dec

-18

Feb

-19

Apr-

19

Jun-1

9

Aug-

19

Oct

-19

Dec

-19