taxes & the pampered chef by mckenzie rogers, c.p.a

TRANSCRIPT

Taxes & The Pampered Chef

by McKenzie Rogers, C.P.A.

Substantiation

Substantiate = ProofKeep everything!Receipts, invoices, checks, mileage log

Record RetentionAverage rule = 3 years

If you underreport income by 25% = 6 years

If you don’t file a return or commit fraud = Indefinitely Records related to assets = Keep as long as you own the asset

Business Deductions

Rule of thumb: “ordinary and necessary”

expenses

Ask yourself: Does any amount of this expense

benefit me or my family personally?

Fixed Assets & Depreciation

Tangible items: computers, desks, filing cabinets, machinery, equipment, furniture, computer software These items

are not expensed when purchased. They are capitalized and depreciated over a prescribed time period.

Business Deductions

Telephone- cannot deduct the cost of phone in your home if you only have 1 phone line- must have 2 to deduct 1

Cell Phone & Internet- only business use portion of the expense is deductible

Business DeductionsAdvertisingOffice SuppliesProfessional fees

(accounting, legal, consulting)RepairsTravel- leave town- hotel, plane tickets,

car rentalMileage* Groceries* Meals* Education*

Education & Training

Expenses for self improvement classes, courses ongrowing business, etc… probably not 100%deductible. Indirectly related to P.C. have toevaluate deductibility.

Training expenses directly related to P.C. productsand presentation and those courses offered by

P.C.,etc… probably 100% deductible.

Meals & Entertainment

Business meals and entertainment expenses incurred in the course of business are only 50% deductible

Receipt for meal should include the date, names of people at the meal or event, brief description of business purpose

Groceries

Groceries you buy to tests recipes that you feed

to your family for dinner are NOT deductible

Groceries you buy to prepare food for showsand show off products that are consumed atparties are deductible

Business use of home

• The business part of your home must be usedexclusively and regularly for your business• If you qualify you may be able to deductexpenses including mortgage interest,

insurance,utilities, repairs, depreciation• Deduction is based on sq. footage of office tothat of the house

Business use of your car

If you use your car for business and personal

purposes you must divide your expenses based on actual mileage

2 Choices: Standard mileage or actual costs

Once you choose you must use forever

Actual Expenses

• Depreciation or lease payments• Gas and oil• Tires• Repairs• Tune-ups• Insurance• Registration

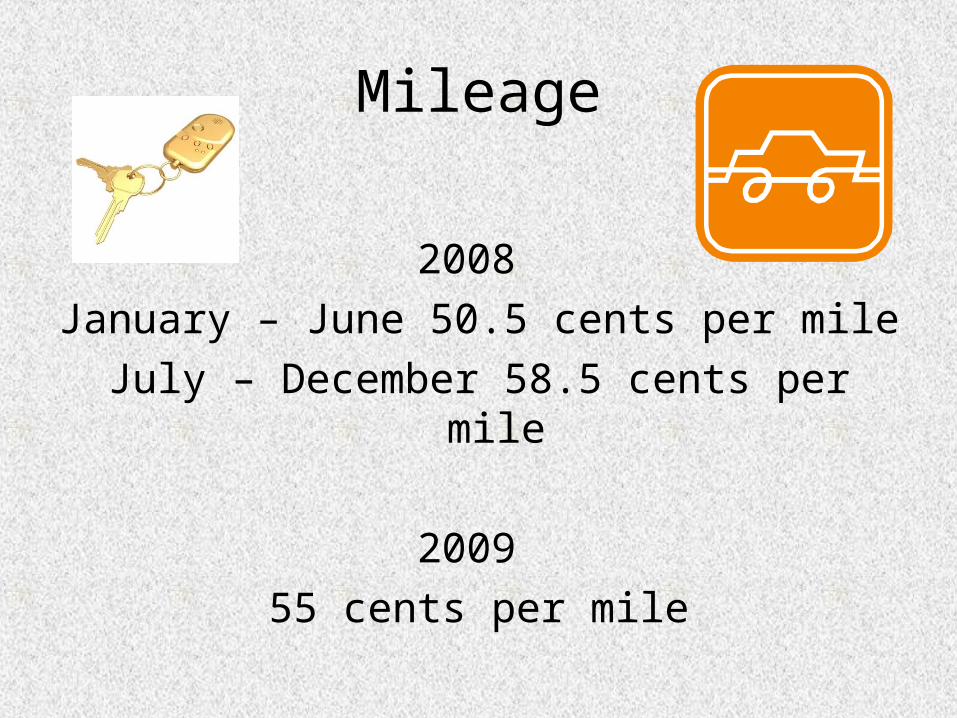

Mileage

2008 January – June 50.5 cents per mile

July – December 58.5 cents per mile

2009 55 cents per mile

Hobby Loss Rules

Your business must show a profitfor 3 out of every 5 consecutiveyears to be considered, “engaged in for profit” and there-fore not considered a hobby.

Losses from hobbies are not deductible.

Audit Risks

Direct Sales

Home in Office

Hobby Loss

Chances of being audited if you file Schedule C- about 1%

Sources of Assistance

www.irs.gov IRS Publications: 334 Tax Guide for Small Business463 Travel, Entertainment & Car

Expenses, 535 Business Expenses583 Starting a Business

& Keeping Records587 Business Use of Your Home

Questions?????