taxes and finance: structuring your horse business to succeed

TRANSCRIPT

February 25, 2012Lincoln, NE

Business Structures

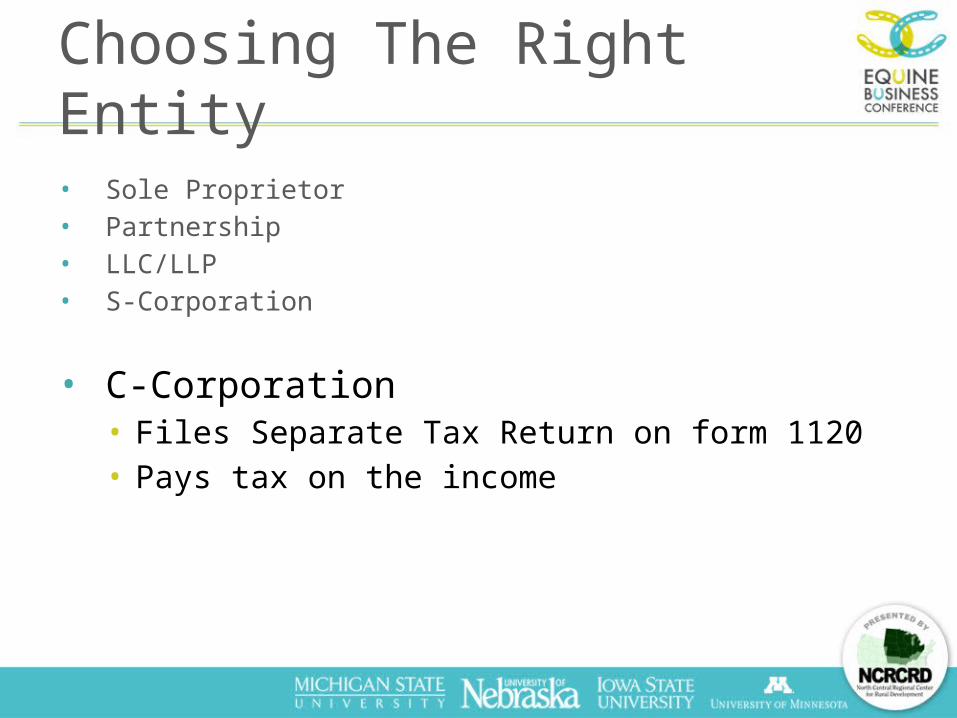

Choices of Entities

• Sole Proprietor • Partnership• LLC / LLP• S - Corporation • C - Corporation

Choosing The Right Entity

• Sole ProprietorFiles a Schedule F (On your Individual Tax Return)

• Partnership• LLC / LLP• S - Corporation • C - Corporation

Sole Proprietorship

Pros

• Most Common Entity

• Easy to Form, Easy to Quit

• Easiest Record Keeping Requirement

Sole Proprietorship

Cons

• Single Member Entity

• No Liability Protection

• Pays SE on All Income

Choosing The Right Entity

• Sole Proprietor

• PartnershipHistorically the most common entity for multiple membersFiles a 1065 Form (Separate Tax Return)

• LLC/LLP• S-Corporation• C-Corporation

Partnership

Pros

• Easy to Form, Easy to Quit

• Simple Way to Split Income and Expenses

• Easier Record Keeping (No Payroll), BUT The Books Must Balance.

Partnership

Cons

• No Liability Protection for General Partners

• Pays SE on All Income

• Can Not Provide Tax Free Benefits to Partners

Choosing The Right Entity

• Sole Proprietor• Partnership

• LLC/LLPConsidered a disregarded entity by the IRSCan Elect to be taxed as a partnership or corporationNo tax benefit to electing a corp status over just being a

corp.

• S-Corporation• C-Corporation

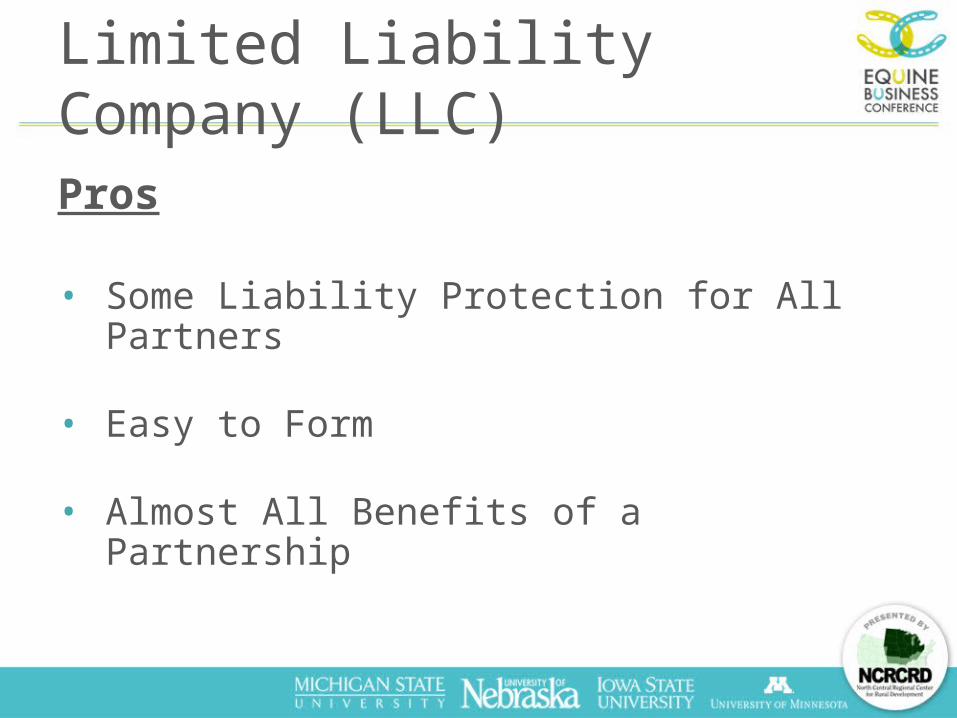

Limited Liability Company (LLC)

Pros

• Some Liability Protection for All Partners

• Easy to Form

• Almost All Benefits of a Partnership

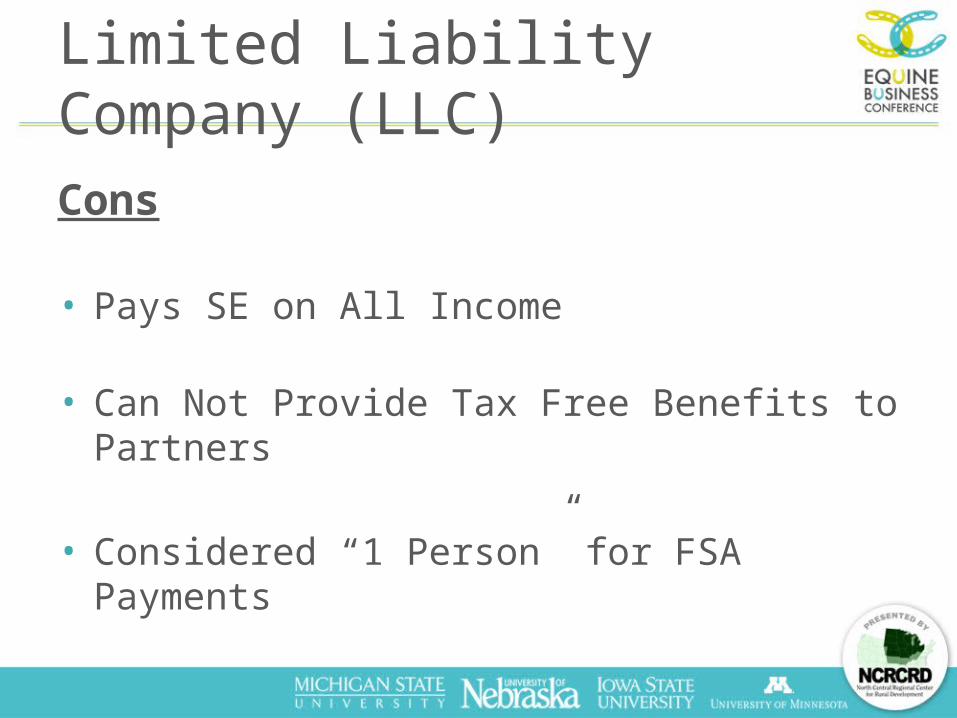

Limited Liability Company (LLC)

Cons

• Pays SE on All Income

• Can Not Provide Tax Free Benefits to Partners

• Considered “1 Person” for FSA Payments

Choosing The Right Entity

• Sole Proprietor• Partnership• LLC/LLP

• S-CorporationFiles separate tax return on form 1120-SSeparate entity, income flows through the corp tax return

to the personal return.

• C-Corporation

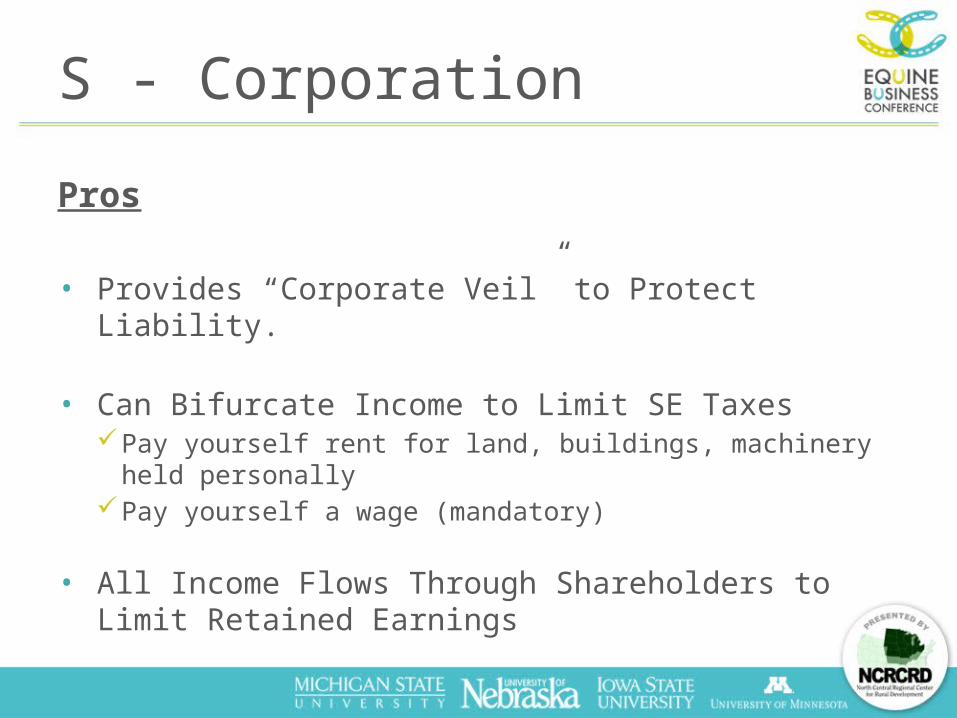

S - Corporation

Pros

• Provides “Corporate Veil” to Protect Liability.

• Can Bifurcate Income to Limit SE Taxes Pay yourself rent for land, buildings, machinery held personally Pay yourself a wage (mandatory)

• All Income Flows Through Shareholders to Limit Retained Earnings

S- Corporation

Cons

• Entity Debt > Basis Limits Deductions

• Tax Liability Due at Dissolution

• Benefits Not Allowed for Employee Owners of > 2%

Choosing The Right Entity

• Sole Proprietor• Partnership• LLC/LLP• S-Corporation

• C-Corporation• Files Separate Tax Return on form 1120• Pays tax on the income

Corporation

Pros

• Provides “Corporate Veil” to Protect Liability.

• Owners Receive Benefits

• SE Tax Limited to Wage

• Extra 15% Tax Bracket

Corporation

Cons

• Retained Earnings Double Taxed on Liquidation

• Cash Doesn’t Easily Flow Between Individual and Corp

• Record Keeping Work Increases.

Why Would You Change?

• Tax Reasons• Cooperative Farming• Generational Transfers• Estate Planning• Legal Protection

Why Would You Change?

• Tax ReasonsMainly Saving SE Taxes

S & C Corps: Pay yourself a reasonable wage(mandatory) Pay SE tax only on the wage.

Pay yourself rent on land, building, and machinery held personally No SE tax on rent

Some Income Tax Savings C-Corp 2012 pay capital gains tax on dividendsTax free benefits

Why Would You Change?

• Tax Reasons

• Cooperative Farming (Shared resources/operation)Share OperationShare EquipmentShare Land

• Generational Transfers• Estate Planning• Legal Protection

Why Would You Change?

• Tax Reasons• Cooperative Farming (Shared resources/operation)

• Generational Transfers Isolate Operational UnitShare EquipmentGift/Purchase Shares over Time

• Estate Planning• Legal Protection

Why Would You Change?

• Tax Reasons• Cooperative Farming (Shared resources/operation)• Generational Transfers

• Estate PlanningMinority DiscountsGift/Purchase in Partial Amounts

• Legal Protection

Why Would You Change?

• Tax Reasons• Cooperative Farming (Shared resources/operation)• Generational Transfers• Estate Planning

• Legal Protection Insurance is no longer sufficientOperation is more at risk

When To Change?

• For Income Taxes?Net Farm Income is consistently $100,000 for MFJ

• A change to the business A child returning to the farmA new entity or enterprise added

When’s To Change?

• Liability issues changeLivestock operationsNet worth is at a point where insurance is not sufficient.

• Reaching Net Worth levels that need an estate plan. Individuals with net worth’s over $5 million ($10 million if

married)For 2012 only (Returns to $1 million each in 2013)

Potential Pitfalls - S-Corp

• Possible legislation to make all earnings from an S-Corp subject to Self-Employment TaxesNegates almost all benefits to S-Corp status.

• Regardless of action taken by Congress to change this, the issue of “Reasonable Wage” has been a HOT audit area.MUST be paying at least some wage!

• Must have basis to take money out of the corporation. Problem if the corporation is not profitable.

Pitfalls - C-Corp

• Double Taxation:Earnings from C-Corp belong to the corpOnly way to have access personally is through dividends

(ordinary income after 2012) or wages (subject to employment taxes)

Dissolution of entity is expensive with corp paying tax on sale of assets and double taxation.

Potential tax penalty if retained earnings become “too high” inside the corp.Not to hard in agriculture to explain that we are

saving for investment

Tax Drawbacks to Entities

• Loss of Step-Up in Basis

Machinery contributed to a corporation goes in at your basis (No tax consequences)

Machinery in a corporation does not receive a step-up in basis at the time of death, the stock owned receives the step-up.

Nebraska Farm Business, Inc

3815 Touzalin AveSuite 105

Lincoln, NE 68507-1600(402) [email protected]