taxation (business taxation and remedial matters) act...

TRANSCRIPT

Examined and certified:

Clerk of the House of Representatives

In the name and on behalf of Her Majesty Queen Elizabeth

the Second I hereby assent to this Act this 19th day

of December 2007

Governor-General.

Taxation (Business Taxation and RemedialMatters) Act 2007

Public Act 2007 No 109

Contents

Page

1 24Title2 24Commencement

Part 1Amendments to Income Tax Act 2004

3 26Income Tax Act 20044 26Withholding liabilities5 27Section CB 4B replaced

CB 4B 27Disposal of certain shares by portfolio invest-ment entity or New Zealand SuperannuationFund after declaration of dividend

6 28New section CB 5A insertedCB 5A 28Land partially sold or sold with other land

7 28Disposal: amount from major development or divisionand not already in income

8 29Residential exclusion from sections CB 10 and CB 119 29Business exclusion from section CB 1010 29Investment exclusion from section CB 1011 30Foreign investment fund income12 30Determination of amount of credit in certain cases13 30When does a person have attributed repatriation from a

CFC?

1

Taxation (Business Taxation and RemedialMatters) Act 2007 2007 No 109

14 30New heading and section CE 12 inserted

Tax credits

CE 12 31Tax credits under section LD 1B added toprovider’s income

15 31Benefits, pensions, compensation, and government grants16 31When FIF income arises17 32Exclusions of withdrawals of various kinds18 32Meaning of petroleum miner19 32New section CT 6B inserted

CT 6B 32Meaning of petroleum mining operations20 33Proceeds of share disposal by qualified foreign equity

investor21 35New section CW 28B inserted

CW 28B Payment of certain accident compensation 35payments

22 35Local authorities23 35Charities: non-business income24 36Charities: business income25 36New heading and sections CW 49C and CW 49D

inserted

Income of, and distributions by, certaininternational funds

CW 49C Income of certain international funds 36CW 49D Distributions by certain international funds 36

26 37Heading above section CX 42 replaced27 37New section CX 42B inserted

CX 42B Contributions to retirement savings scheme 3728 38Proceeds from disposal of certain shares by portfolio

investment entities or New Zealand SuperannuationFund

29 38Portfolio investor allocated income and distributions ofincome by portfolio investment entities

30 39Cost of revenue account property31 39Research or development32 40Some definitions33 41Gifts of money by company34 41Certain investors have deduction for portfolio investor

allocated loss35 41Sale of business: transferred employment income

obligations36 42Heading to subpart DF37 42New section DF 4 added

2

Taxation (Business Taxation and RemedialMatters) Act 20072007 No 109

DF 4 42Payment by claimant receiving personal servicerehabilitation payment

38 43When FIF loss arises39 43Acquiring film rights40 44Film production expenditure41 44New section DS 2B inserted

DS 2B 45Expenditure in acquiring film, or film right,intended for disposal

42 45Maori authorities: donations43 45Cost44 46Discounted selling price45 46Valuing closing stock consistently46 47Discounted selling price for low-turnover traders47 47Valuing closing stock consistently for low-turnover

traders48 47Reduction: bloodstock not previously used for breeding

in New Zealand49 48Valuation of excepted financial arrangements50 49Special rate or provisional rate51 49Meaning of adjusted tax value52 49Meaning of annual rate53 49Allocation of income and deductions by portfolio tax

rate entity54 49Expenditure incurred in acquiring film rights in feature

films55 50Expenditure incurred in acquiring film rights in films

other than feature films56 50Film production expenditure for New Zealand films57 51Film production expenditure for films other than New

Zealand films58 51What spreading methods do59 52What is included when spreading methods used60 52New sections EW 15B to EW 15E inserted

EW 15B IFRS taxpayer method 52EW 15C IFRS method 55EW 15D Determination alternatives to IFRS 56EW 15E Expected value method and equity-free fair 58

value method61 59Yield to maturity method or alternative62 60Straight-line method63 60Market valuation method64 61Choice among first 3 spreading methods65 61Determination method or alternative66 62Section EW 21 repealed

3

Taxation (Business Taxation and RemedialMatters) Act 2007 2007 No 109

67 62Default method68 63Failure to use method for financial reporting purposes69 63Consistency of use of spreading method70 64New section EW 25B inserted

EW 25B Consistency of use of specific individual 64methods under IFRS taxpayer method

71 65Change of spreading method72 66When calculation of base price adjustment required73 67Base price adjustment formula74 68New heading and new section EW 48B inserted

Consideration when change from fair valuemethod under IFRS method

EW 48B Consideration when change from fair value 68method under IFRS method

75 68Meaning of CFC76 69Options and similar rights in certain cases77 69Associates and 10% threshold78 69Branch equivalent income or loss: calculation rules79 69CFC rules exemption80 69Exemptions: direct income interests in FIF in grey list

country81 71Exemptions limited by income years: shares in certain

grey list companies82 72Exemption: shares in listed Australian company83 74Exemption: units in certain Australian unit trusts84 75Limits on choice of calculation methods85 77Use of particular calculation methods required86 77Default calculation method87 77Comparative value method88 77Fair dividend rate method89 78Fair dividend rate method: usual method90 79Fair dividend rate method: method for entities that value

investors’ units91 80Fair dividend rate method and cost method: calculating

items in formulas for periods affected by sharereorganisations

92 81Cost method93 82Codes: comparative value method, deemed rate of return

method, fair dividend rate method, and cost method94 82Limits on changes of method95 82Consequences of changes in method96 83FIF rules first applying to interest for income year

beginning on or after 1 April 2007

4

Taxation (Business Taxation and RemedialMatters) Act 20072007 No 109

97 84Measurement of cost98 84Policyholder income formula99 85New sections EY 42B and EY 42C inserted

EY 42B Policyholder income formula: FDR 85adjustment

EY 42C Policyholder income formula: PILF 86adjustment

100 89New section EZ 50 insertedEZ 50 89Transitional rule for IFRS financial reporting

method101 89Sections FC 8H and FC 8I replaced

FC 8H 89Adjustment required if lease becomes financelease

FC 8I 91Adjustment required for certain operating leasesentered before 20 June 2007

102 92Variations in control or income interests in foreigncompanies

103 92New section GC 14EB insertedGC 14EB Treatment of dividends as if from qualifying 92

company104 93Tax credits for family support and family plus105 93Dividends from qualifying company106 93Scheme of subpart107 94Section HL 3 replaced

HL 3 94Eligibility requirements for entities108 96Effect of failure to meet eligibility requirements for

entities109 96New sections HL 5B and HL 5C inserted

HL 5B 96Meaning of investor and portfolio investor classHL 5C 98Income interest requirement

110 98Investor membership requirement111 99Further eligibility requirements relating to investments112 100Investor interest size requirement113 100Further eligibility requirements relating to investments114 100Election to become portfolio investment entity and

cancellation of election115 101Unlisted company may choose to become portfolio listed

company116 101Becoming portfolio investment entity117 102Tax consequences from transition118 102Treatment of income from interest if no investor entitled

or investor has conditional entitlement

5

Taxation (Business Taxation and RemedialMatters) Act 2007 2007 No 109

119 102Credits received by portfolio tax rate entity or portfolioinvestor proxy

120 103Payments of tax by portfolio tax rate entity making noelection

121 103Payments of tax by portfolio tax rate entity choosing tomake payments when investor leaves

122 104Optional payments of tax by portfolio tax rate entities123 104Portfolio investor allocated income and portfolio investor

allocated loss124 104Treatment of portfolio investor allocated loss for zero-

rated portfolio investors and investors with portfolioinvestor exit period

125 105Credits received by portfolio tax rate entity or portfolioinvestor proxy

126 106Portfolio investor proxies127 106Companies included in group of companies128 106Net loss offset between group companies129 106Rebate in respect of gifts of money130 107New section KC 6 inserted

KC 6 107Rebate in respect of redundancy payment131 108Amendments to subpart KD made in schedule 1132 108Determination of net income133 108Calculation of subpart KD credit134 109Determination of amount of credit in certain cases135 109Credit of tax for imputation credit136 109New section LB 3 inserted

LB 3 109Credit of retirement scheme contribution with-holding tax for imputation credit

137 110New sections LD 1B and LD 1C insertedLD 1B 110Tax deductions from certain accident compensa-

tion payments: credit allowed to providerLD 1C 111Tax deductions from certain accident compensa-

tion payments: credit allowed to claimant138 112New section LD 4 inserted

LD 4 112Credit of retirement scheme contribution with-holding tax for Maori authority credit

139 112Credit of tax for dividend withholding payment credit inhands of shareholder

140 113New section LD 12 addedLD 12 113Credit for retirement scheme contribution with-

holding tax if retirement scheme contributionnot excluded income

141 114Credits in respect of dividends to non-resident investors

6

Taxation (Business Taxation and RemedialMatters) Act 20072007 No 109

142 114Special rules for holding companies143 114Estimation method144 114GST ratio method145 116Provisional tax payable in instalments146 116Calculating amount of instalment under standard and

estimation methods147 117Who may use GST ratio?148 117Changing determination method149 117Disposal of assets150 118Paying provisional tax in transitional years151 118Consequences of change in balance date152 119Registering for GST or cancelling registration153 119Refund of excess tax154 119Companies required to maintain imputation credit

account155 119Companies electing to maintain imputation credit

account156 120Credits arising to imputation credit account157 120Allocation rules for imputation credits158 120Further tax payable where end of year debit balance or

when company ceases to be imputation credit accountcompany

159 120Amount of imputation credit to be attached to cashdistribution

160 121Notional distribution deemed to be dividend161 121Amount of imputation credit to be attached to cash

distribution162 121Notional distribution deemed to be dividend or taxable

Maori authority distribution163 121Branch equivalent tax account of company164 121Credits and debits arising to branch equivalent tax

account of company165 121Use of credit to reduce dividend withholding payment,

or use of debit to satisfy income tax liability166 122Debits and credits arising to group branch equivalent tax

account167 122Use of consolidated group credit to reduce dividend

withholding payment, or use of group or individual debitto satisfy income tax liability

168 123Allocation rules for dividend withholding paymentcredits

169 123Dividend with both imputation credit and dividend with-holding payment credit attached

170 123Conduit tax relief account171 123Credits arising to conduit tax relief account

7

Taxation (Business Taxation and RemedialMatters) Act 2007 2007 No 109

172 123Debits arising to conduit tax relief account173 123Consolidated group conduit tax relief account174 124Credits arising to group conduit tax relief account175 124Debits arising to group conduit tax relief account176 124Private use of motor vehicle: when schedular value not

used177 124Private use of motor vehicle: when schedular value used178 124New subpart NEB inserted

Subpart NEB—Retirement scheme contributionwithholding tax

NEB 1 124Retirement scheme contribution withholding taximposed

NEB 2 125Retirement scheme contribution withholding taxto be deducted

NEB 3 125Payment and notice of deductionsNEB 4 126Failure to deductNEB 5 127Retirement savings schemesNEB 6 128Retirement scheme contributorsNEB 7 129Application of other provisions to retirement

scheme contribution withholding tax179 129Application of RWT rules180 130Resident withholding tax deductions from dividends

deemed to be dividend withholding payment credits181 130New section NG 16B inserted

NG 16B Person withholding amount as retirement 130scheme contribution withholding tax whenliable for non-resident withholding tax

182 131Definitions183 141Meaning of source deduction payment: shareholder-

employees of close companies184 141Meaning of income tax185 141Further definitions of associated persons186 142Schedule 13—Months for payment of provisional tax

and terminal tax

Part 2Amendments to Tax Administration Act 1994

187 142Tax Administration Act 1994188 142Interpretation189 144Keeping of business records190 145Section 28B repealed191 145New section 28B inserted

8

Taxation (Business Taxation and RemedialMatters) Act 20072007 No 109

28B 145Investor to advise portfolio tax rate entity ofinvestor’s tax file number

192 145New section 28C inserted28C 145Person advising retirement savings scheme of

retirement scheme prescribed rate193 145Shareholder dividend statement to be provided by

company194 146Maori authority to give notice of amounts distributed195 147Portfolio tax rate entity to give statement to investors

and request information196 147Annual returns of income197 147Annual returns of income not required198 148New section 33C inserted

33C 148Return not required for certain providers of per-sonal services

199 149New section 34B inserted34B 149Commissioner to list tax agents

200 151Dates by which annual returns to be furnished201 151Returns to annual balance date202 152Annual returns by persons who receive subpart KD

credit203 152New section 41B inserted

41B 152Return by person claiming rebate on redundancypayment

204 153Non-active companies may be excused from filingreturns

205 153New section 47B inserted47B 153RSCT statements provided by retirement

scheme contributor or retirement savingsscheme

206 153New section 48B inserted48B 154Reconciliation statement for retirement scheme

contribution withholding tax207 156Portfolio tax rate entities and portfolio investor proxies

to make returns, file annual reconciliation statement208 158Disclosure of interest in foreign company or foreign

investment fund209 158New sections 68D and 68E inserted

68D 158Statements in relation to research and develop-ment tax credits: single persons

9

Taxation (Business Taxation and RemedialMatters) Act 2007 2007 No 109

68E 159Statements in relation to research and develop-ment tax credits: internal software developmentgroups and partnerships

210 160Particulars to be included in income statement211 160What Commissioner must do on receipt of application212 160Payment by instalment of family support (without

abatement)213 160Payment of tax credit by chief executive214 160Determining family assistance credit215 161When entitlement to income-tested benefit ends216 161No authority to pay family assistance credit217 161Request by chief executive to stop payment of family

assistance credit218 161Payment of tax credit taken over by Commissioner219 161Effect of extra instalment on entitlement to tax credit220 162Officers to maintain secrecy221 162Disclosure of information concerning actions of tax

advisor222 163Disclosure of information for purposes of entitlement

card223 163Disclosure of information for family support double pay-

ment identification224 163Disclosure of information in relation to family income

assistance225 164Use of information supplied under section 85GA226 164Where Commissioner accepts adjustment proposed by

disputant227 164Determinations relating to financial arrangements228 165Determination on type of interest in FIF and use of fair

dividend rate method229 166New heading and section 91AAP inserted

Determinations relating to research anddevelopment tax credits

91AAP 166Determinations relating to requirements forresearch and development tax credits

230 167Taxation laws in respect of which binding rulings maybe made

231 168New section 98B inserted98B 168Assessment of retirement scheme contribution

withholding tax232 169Time bar for amendment of income tax assessment233 169Extension of time bars234 169Commissioner may at any time amend assessments

10

Taxation (Business Taxation and RemedialMatters) Act 20072007 No 109

235 169New section 113D inserted113D 170Amended assessments for research and develop-

ment tax credits236 170Residual income tax of new provisional taxpayer237 170Heading to example replaced238 170Provisional tax instalments in transitional years239 170Heading to example replaced240 170Provisional tax and rules on use of money interest241 171Late filing penalties242 172New section 139AAA inserted

139AAA Late filing penalty for GST returns 172243 173Late payment penalty244 174Imposition of late payment penalties when financial

relief sought245 174Late payment penalty and provisional tax246 175Imputation penalty tax payable where end of year debit

balance247 175New section 140BB inserted

140BB 175Imputation penalty tax payable in somecircumstances

248 176Dividend withholding payment penalty tax payablewhere end of year debit balance

249 176New section 140CA inserted140CA 176FDP penalty tax payable in some circumstances

250 176Tax shortfalls251 178Not taking reasonable care252 178Unacceptable tax position253 179Abusive tax position254 180Evasion or similar act255 180New section 141ED inserted

141ED 180Not paying employer monthly schedule amount256 182Reduction in penalty for voluntary disclosure of tax

shortfall257 182Reduction where temporary shortfall258 183Limitation on reduction of shortfall penalty259 184Section 141KB repealed260 184Due date for payment of late filing penalty261 184New due date for payment of tax that is not penalty262 185Knowledge offences263 185Imposition of civil and criminal penalties264 186Remission for reasonable cause265 186Remission consistent with collection of highest net

revenue over time

11

Taxation (Business Taxation and RemedialMatters) Act 2007 2007 No 109

266 186Small amounts of penalties and interest not to becharged

267 186Power to make interim payments of family assistancecredit

268 186New section 226B inserted226B 186Business group amnesties

Part 3Amendments to other Acts and Regulations

Estate and Gift Duties Act 1968269 189Exemption for gifts to charities and certain bodies

Goods and Services Tax Act 1985270 190Goods and Services Tax Act 1985271 190Interpretation272 190Value of supply of goods and services273 190Zero-rating of goods274 191Zero-rating of services275 192Special returns276 192Calculation of tax payable277 192New section 24BA inserted

24BA 192Shared tax invoices278 193Relief from tax where new start grant made279 193Group of companies

Income Tax Act 1994280 194Income Tax Act 1994281 194Public and local authorities’ exempt income282 194Non-profit bodies’ and charities’ exempt income283 195Other exempt income284 195What constitutes an interest in a foreign investment fund285 195Companies required to maintain imputation credit

account286 195Use of credit to reduce dividend withholding payment,

or use of debit to satisfy income tax liability287 196Use of consolidated group credit to reduce dividend

withholding payment or use of group or individual debitto satisfy income tax liability

288 197Definitions

Taxation Review Authorities Act 1994289 198Taxation Review Authorities Act 1994290 198New section 22B inserted

22B 198Power to order costs for filing fees291 198Regulations

12

Taxation (Business Taxation and RemedialMatters) Act 20072007 No 109

Taxation (Depreciation, Payment Dates Alignment,FBT, and Miscellaneous Provisions) Act 2006

292 198Taxation (Depreciation, Payment Dates Alignment, FBT,and Miscellaneous Provisions) Act 2006

Customs and Excise Act 1996293 199New sections 280J, 280K, and 280L inserted

280J 199Defined terms for sections 280K and 280L280K 199Disclosure of arrival and departure information

for purposes of Child Support Act 1991280L 200Direct access to arrival and departure informa-

tion for purposes of Child Support Act 1991

Health (Drinking Water) Amendment Act 2007294 201New Part 2A inserted

Housing Restructuring and Tenancy Matters Act 1992295 202Amendments to Housing Restructuring and Tenancy

Matters Act 1992 made in schedule 2

Privacy Act 1993296 202Privacy Act 1993297 202Notice of adverse action proposed298 202Schedule 3—Information matching provisions

Rates Rebate Act 1973299 202Amendments to Rates Rebate Act 1973 made in

schedule 2

Social Security Act 1964300 202Amendments to Social Security Act 1964 made in

schedule 2

Goods and Services Tax (Grants and Subsidies) Order1992

301 203Schedule—Goods and Services Tax (Grants and Subsi-dies) Order 1992

Health Entitlement Cards Regulations 1993302 203Amendments to Health Entitlement Cards Regulations

1993 made in schedule 2

Income Tax (Withholding Payments) Regulations 1979303 203Schedule—Tax deductions from withholding payments

Social Security (Temporary Additional Support)Regulations 2005

304 203Amendments to Social Security (Temporary AdditionalSupport) Regulations 2005 made in schedule 2

13

Taxation (Business Taxation and RemedialMatters) Act 2007 2007 No 109

Student Allowances Regulations 1998305 204Amendments to Student Allowances Regulations 1998

made in schedule 2

Amendments to Income Tax Act 2007306 204Income Tax Act 2007307 204Commencement308 204Withholding liabilities309 204Disposal: amount from major development or division

and not already in income310 205Residential exclusion from sections CB 12 and CB 13311 205Business exclusion from section CB 12312 205Investment exclusion from section CB 12313 205New section CB 23B added

CB 23B Land partially sold or sold with other land 205314 205Certain disposals by portfolio investment entities

CB 26 205Certain disposals by portfolio investmententities

315 206Foreign investment fund income316 207Available subscribed capital (ASC) amount317 207When does person have attributed repatriation from

controlled foreign company?318 207Prevention of double taxation of share cancellation

dividends319 207Tax credits added to caregiver’s income

CE 12 207Tax credits for personal service rehabilitationpayments

320 208Benefits, pensions, compensation, and government grants321 208Adjustments under consecutive or successive finance

leasesCH 6 208Adjustments for certain finance and operating

leases322 208When FIF income arises323 209New section CQ 7 added

CQ 7 209Treatment of attributing interests subject toreturning share transfer

324 209Withdrawals325 209Exclusions of withdrawals of various kinds326 209Meaning of petroleum miner327 210New section CT 6B inserted

CT 6B 210Meaning of petroleum mining operations328 210Proceeds of share disposal by qualifying foreign equity

investor

14

Taxation (Business Taxation and RemedialMatters) Act 20072007 No 109

329 212Payment to claimant of certain accident compensationpaymentsCW 35 212Personal service rehabilitation payments

330 212Local authorities331 213Charities: non-business income332 213Charities: business income333 213New section CW 59B inserted

CW 59B Income of and distributions by certain 213international funds

334 214New section CX 50B insertedCX 50B Contributions to retirement savings schemes 214

335 215Proceeds from certain disposals by portfolio investmententities or New Zealand Superannuation Fund

336 215Portfolio investor allocated income and distributions ofincome by portfolio investment entities

337 216Cost of revenue account property338 217Research or development339 217Some definitions340 217Charitable or other public benefit gifts by company341 218New heading and new section DB 51B inserted

Adjustments for leases that becomefinance leases

DB 51B Adjustments for leases that become finance 218leases

342 218Portfolio investment entities: zero-rated portfolioinvestors and allocated losses

343 219Accident compensation payment for attendant careDF 4 219Payments for social rehabilitation

344 219When FIF loss arises345 220Acquiring film rights346 220Film production expenditure347 221New section DS 2B inserted

DS 2B 221Expenditure when film or film right intended fordisposal

348 221Maori authorities: donations349 222Cost350 222Discounted selling price351 223Valuing closing stock consistently352 223Discounted selling price for low-turnover traders353 223Valuing closing stock consistently for low-turnover

traders

15

Taxation (Business Taxation and RemedialMatters) Act 2007 2007 No 109

354 223Reduction: bloodstock not previously used for breedingin New Zealand

355 224Valuation of excepted financial arrangements356 224Special rate or provisional rate357 224Meaning of adjusted tax value358 224Meaning of annual rate359 225Allocation of income and deductions by portfolio tax

rate entity360 225Expenditure incurred in acquiring film rights in feature

films361 225Expenditure incurred in acquiring film rights in films

other than feature films362 226Film production expenditure for New Zealand films363 226Film production expenditure for films other than New

Zealand films364 226What spreading methods do365 226What is included when spreading methods used366 227New sections EW 15B to EW 15I inserted

EW 15B Applying IFRSs to financial arrangements 227EW 15C Preparing and reporting methods 228EW 15D IFRS financial reporting method 228EW 15E Determination alternatives 229EW 15F Expected value method 231EW 15G Modified fair value method 232EW 15H Mandatory use of some determinations 232EW 15I Mandatory use of yield to maturity method for 233

some arrangements367 234Yield to maturity method or alternative368 235Straight-line method369 235Market valuation method370 235Choice among first 3 spreading methods371 235Determination method or alternative372 236Financial reporting method373 236Default method374 236Failure to use method for financial reporting purposes375 236Consistency of use of spreading method376 237New section EW 25B inserted

EW 25B Consistency of use of IFRS method 237377 237Change of spreading method378 238When calculation of base price adjustment required379 238Base price adjustment formula380 238New section EW 46B inserted

EW 46B Consideration when party changes from fair 238value method

16

Taxation (Business Taxation and RemedialMatters) Act 20072007 No 109

381 239Meaning of controlled foreign company382 239Options and similar rights in certain cases383 239Associates and 10% threshold384 239Taxable distribution from non-complying trust385 239Exemption for ASX-listed Australian companies386 240Exemption for Australian unit trusts with 25% turnover

EX 32 240Exemption for Australian unit trusts with ade-quate turnover or distributions

387 243Venture capital company emigrating to grey list country:10-year exemption

388 243Grey list company owning New Zealand venture capitalcompany: 10-year exemption

389 244New section EX 37B insertedEX 37B Share in grey list company acquired under 244

venture investment agreement390 245Exemption for employee share purchase scheme of grey

list company391 245Terminating exemption for grey list company with

numerous New Zealand shareholders392 245Limits on choice of calculation methods393 246Comparative value method394 247Fair dividend rate method: usual method395 248Fair dividend rate method for funds that value investors’

units396 249Cost method397 250Codes: comparative value method, deemed rate of return

method, fair dividend rate method, and cost method398 250Limits on changes of method399 251Consequences of changes in method400 251FIF rules first applying to interest on or after 1 April

2007401 252Measurement of cost402 252Policyholder income formula403 253New sections EY 43B and EY 43C inserted

EY 43B Policyholder income formula: FDR 253adjustment

EY 43C Policyholder income formula: PILF 254adjustment

404 256Terminating exemption for grey list FIF investing inAustralasian listed equities

405 257New section EZ 32B insertedEZ 32B Transitional rule for IFRS reporting 257

406 258Consecutive or successive finance leases

17

Taxation (Business Taxation and RemedialMatters) Act 2007 2007 No 109

FA 11 258Adjustments for leases that become financeleases

FA 11B Adjustments for certain operating leases 259407 261Attribution rule for income from personal services408 261Arrangements involving family support credits409 262Fully imputed distributions410 262Scheme of subpart411 263Section HL 3 replaced

HL 3 263Eligibility requirements for entities412 265Effect of failure to meet eligibility requirements for

entities413 265New sections HL 5B and HL 5C inserted

HL 5B 265Meaning of investor and portfolio investor classHL 5C 267Income interest requirement

414 267Investor membership requirement415 268Investor return adjustment requirement: portfolio tax rate

entity416 269Imputation credit distribution requirement: portfolio

listed company417 269Investor interest size requirement418 270Further eligibility requirements relating to investments419 270Election to become portfolio investment entity and

cancellation of election420 270Unlisted company choosing to become portfolio listed

company421 270Becoming portfolio investment entity422 271Tax consequences from transition423 271Treatment of income from interest when entitlement

conditional or lacking424 272Portfolio entity tax liability and tax credits of portfolio

tax rate entity for period425 272Payments of tax by portfolio tax rate entity making no

election426 272Payments of tax by portfolio tax rate entity choosing to

make payments when investor leaves427 273Optional payments of tax by portfolio tax rate entities428 273Portfolio investor allocated income and portfolio investor

allocated loss429 274Treatment of portfolio investor allocated loss for zero-

rated portfolio investors and investors with portfolioinvestor exit period

430 274Credits received by portfolio tax rate entity or portfolioinvestor proxy

431 275Portfolio investor proxies

18

Taxation (Business Taxation and RemedialMatters) Act 20072007 No 109

432 275Common ownership: group of companies433 276Remaining refundable credits: PAYE, RWT, and certain

other items434 276Remaining refundable credits: family scheme income435 276Use of tax credits436 276Heading: subpart LB437 277Tax credits for family scheme income438 277Tax credits for caregivers

LB 6 277Tax credits for RSCT

LB 7 278Tax credits related to personal service rehabilita-tion payments: providers

LB 8 279Tax credits related to personal service rehabilita-tion payments: payers

439 280Tax credits for housekeeping440 280Tax credits for charitable and other public benefit gifts441 280Tax credits for imputation credits442 281New section LE 7B

LE 7B 281Credit of RSCT for imputation credit443 281Application of imputation ratio444 281Application of combined imputation and FDP ratio445 282Tax credits for FDP credits446 282Application of FDP ratio447 282Application of combined imputation and FDP ratio448 282New subpart LH inserted

Subpart LH—Tax credits for expenditure onresearch and development

LH 1 282Who this subpart applies toLH 2 283Tax credits relating to expenditure on research

and developmentLH 3 285RequirementsLH 4 286Calculation of amount of creditLH 5 287Adjustments to eligible expenditureLH 6 288Research and development activities outside

New ZealandLH 7 290Research and development activities and related

termsLH 8 291Orders in CouncilLH 9 291Internal software development: generalLH 10 292Internal software development: no associated

internal software developerLH 11 293Internal software development: associated inter-

nal software developer with same income year

19

Taxation (Business Taxation and RemedialMatters) Act 2007 2007 No 109

LH 12 294Internal software development: associated inter-nal software developer with different incomeyear

LH 13 295Internal software development: limitLH 14 296Treatment of depreciation loss for certain depre-

ciable propertyLH 15 297Listed research providersLH 16 299Industry research co-operativesLH 17 300Some definitions

449 301New section LO 2BLO 2B 301Credit of RSCT for Maori authority credit

450 302Tax credits for supplementary dividends451 302Application of benchmark dividend rules and imputation

credit ratio452 302Relationship with exempt income rules453 302What this subpart does454 303Avoidance arrangements455 303Some definitions for family scheme456 304Adjustments for calculation of family scheme income457 304New section MB 6

MB 6 304Treatment of distributions from retirementsavings schemes

458 305What this subpart does459 306Third requirement: residence460 306When person does not qualify461 306When spouse or partner entitled under family scheme462 306Continuing requirements463 307Credits for person aged 18464 307Principal caregiver465 307Heading: subpart MD466 307Family assistance credit467 308Calculating net contributions to credits468 309Calculation of family support469 309Entitlement to in-work payment470 309First requirement: person’s age471 310Second requirement: principal care472 310Third requirement: residence473 310Fourth requirement: person not receiving benefit474 310Fifth requirement: full-time earner475 310Calculation of in-work payment476 311Calculation of family credit abatement477 311Person receiving protected family support478 311New section MD 16

MD 16 311Calculation of parental tax credit abatement

20

Taxation (Business Taxation and RemedialMatters) Act 20072007 No 109

479 312Heading: subpart ME480 312Family tax credit481 312Meaning of employment for this subpart482 312New section ME 3

ME 3 312Meaning of net family scheme income483 313Application for payment of tax credit by instalment484 313When person not entitled to payment by instalment485 314Calculating amount of interim family assistance credit486 314Requirements for calculating instalment of tax credit487 314Recovery of overpaid tax credit488 314Overpayment of tax credit489 314Orders in Council490 315New subpart ML inserted

Subpart ML—Tax credits for redundancypayments

ML 1 315What this subpart doesML 2 316Tax credit for redundancy paymentsML 3 316Payment by Commissioner

491 316Entitlement to child tax credit492 317Calculation of maximum permitted ratios493 317Australian companies with imputation credit accounts494 317ICA payment of tax495 317New sections OB 7B and OB 7C

OB 7B 317ICA payment of qualifying company electiontax

OB 7C 318ICA expenditure on research and development496 318ICA attribution for personal services497 318Table O1: imputation credits498 318ICA on-market cancellation499 319Further income tax when company stops being ICA

company500 319Statutory producer boards attaching imputation credits to

cash distributions501 319Statutory producer boards’ notional distributions that are

dividends502 320Co-operative companies attaching imputation credits to

cash distributions503 320Co-operative companies’ notional distributions that are

dividends504 320FDP credits and imputation credits attached to dividends505 320General rules for companies with CTR accounts506 320CTR credits and imputation credits attached to dividends507 321Branch equivalent tax accounts of companies

21

Taxation (Business Taxation and RemedialMatters) Act 2007 2007 No 109

508 321BETA payment of income tax509 321BETA unused amount of debit balance510 321MACA payment of tax511 321New section OK 4B

OK 4B 321MACA expenditure on research anddevelopment

512 322Table O17: Maori authority credits513 322When credits and debits arise only in consolidated impu-

tation group accounts514 322Consolidated ICA payment of tax515 322New section OP 11B

OP 11B Consolidated ICA expenditure on research and 322development

516 323Table O19: imputation credits of consolidated imputationgroups

517 323CTR accounts of consolidated groups518 323When credits and debits arise only in branch equivalent

tax group accounts519 323Consolidated BETA payment of income tax520 324New sections OZ 7 to OZ 17 added

OZ 7 324Memorandum accounts in transitional periodOZ 8 324Attaching imputation credits and FDP credits:

maximum permitted ratioOZ 9 325Benchmark dividends: ratio changeOZ 10 326Modifying ratios for imputation credits and FDP

creditsOZ 11 326Tax credits for imputation credits and FDP

creditsOZ 12 328Tax credits for non-resident investorsOZ 13 329Fully credited dividends: modifying actual ratioOZ 14 329Dividends from qualifying companiesOZ 15 330Attaching imputation credits and notional distri-

butions: modifying amountsOZ 16 331BETA reductionsOZ 17 331CTRA reductions

521 331What this Part does522 332New section RA 6B

RA 6B 332Withholding and payment obligations for retire-ment scheme contributions

523 332When obligations not met524 332Payment dates for interim and other tax payments525 333Amalgamation of companies526 333New section RA 24

22

Taxation (Business Taxation and RemedialMatters) Act 20072007 No 109

RA 24 333Application of other provisions for purposes ofRSCT rules

527 333Estimation method528 333GST ratio method529 334Provisional tax payable in instalments530 335Calculating amount of instalment under standard and

estimation methods531 335Who may use GST ratio?532 335When GST ratio must not be used533 335Changing calculation method534 336Disposal of assets535 336Paying provisional tax in transitional years536 336Consequences of a change in balance date537 337Registering for GST or cancelling registration538 337What this subpart does539 337PAYE income payments540 337Private use of motor vehicle: when schedular value not

used541 337Private use of motor vehicle: when schedular value used542 338Resident passive income543 338When amount of tax treated as FDP credit544 338New section RF 16 inserted

RF 16 338Relationship with RSCT rules545 339New subpart RH inserted

Subpart RH—Withholding tax on retirementscheme contributions

RH 1 339RSCT rules and their applicationRH 2 340Retirement scheme contributionsRH 3 341Retirement savings schemesRH 4 342Retirement scheme contributors

Calculating amounts of tax

RH 5 342Calculating amounts of tax for retirementscheme contribution

RH 6 342Calculating amounts of tax on failure towithhold

546 343Using refund to satisfy tax liability547 343Standard method: 2008–09 and 2009–10 income years548 343GST ratio method: 2008–09 and 2009–10 income years549 344Calculating amounts under standard method: 2008–09

and 2009–10 income years550 344Definitions551 355Company and company’s associate: 1988 version

provisions

23

Taxation (Business Taxation and RemedialMatters) Act 2007 2007 No 109s 1

552 355Partnerships: partnership and associate of partner553 355Some definitions554 355Schedule 1—Basic tax rates: income tax, ESCT, RWT,

and attributed fringe benefits555 356Schedule 2—Basic tax rates for PAYE income payments556 357Schedule 4—Rates of tax for schedular payments557 357Schedule 14—Depreciable intangible property558 357New schedule 21559 357Schedule 32—Recipients of charitable or other public

benefit gifts560 357Schedule 49—Enactments amended561 358Schedule 50—Amendments to Tax Administration Act

1994562 358Consequential amendments to Income Tax Act 2007

Schedule 1 359Amendments to subpart KD of the

Income Tax Act 2004

Schedule 2 362Amendments to other Acts and Regulations

Schedule 3 364New schedule 21 inserted in Income Tax Act 2007

The Parliament of New Zealand enacts as follows:

1 TitleThis Act is the Taxation (Business Taxation and RemedialMatters) Act 2007.

2 Commencement(1) This Act comes into force on the date on which it receives the

Royal assent, except as provided in this section.

(2) Section 284 is treated as coming into force on 1 April 1995.

(3) Sections 286 and 287 are treated as coming into force on1 April 1997.

(4) Sections 241(1) and (3) and 269(1) are treated as coming intoforce on 1 April 1999.

(5) Sections 281 and 282(3) are treated as coming into force on1 April 2001.

24

Taxation (Business Taxation and RemedialMatters) Act 2007 s 22007 No 109

(6) Section 273(2), (4), and (5) are treated as coming into force on24 October 2001.

(7) Section 285 is treated as coming into force on 1 April 2002.

(8) Section 269(3) is treated as coming into force on 1 April 2003.

(9) Section 133(1) is treated as coming into force on 4 June 2004.

(10) Section 288(3) is treated as coming into force on 16 Nov-ember 2004.

(11) Sections 6, 7, 8, 9, 10, 13, 18, 19, 22, 23, 24, 25, 35, 39, 40, 41,54, 55, 56, 76, 77, 79, 102, 128, 154, 165, 167, 182(25), (28),(33), and (55), 185(2), 230(1) and (2), and 272(1) are treatedas coming into force on 1 April 2005.

(12) Section 129(1) is treated as coming into force on 1 July 2005.

(13) Sections 176 and 177 are treated as coming into force on1 April 2006.

(14) Sections 130, 182(44), and 185(1) are treated as coming intoforce on 1 December 2006.

(15) Sections 4, 16, 26, 27, 31, 32, 38, 43, 44, 45, 46, 47, 49, 58,59, 60, 61, 62, 63, 64, 65, 66, 67, 68, 69, 70, 71, 72, 73, 74, 80,81, 82, 83, 84, 85, 87, 88, 89, 90, 91, 92, 94, 95, 96, 97, 100,104, 131, 132, 135(2), 136, 138, 140, 153, 178, 179(1) and(3), 181, 182(5), (6), (7), (8), (9), (10), (11), (12), (13), (14),(15), (16), (18), (19), (20), (22), (24), (27), (29), (30), (43),(45), (46), (47), (48)(a) and (b), (49), (50), (51), (52), (53),(54), and (56), 184, 189(2) and (5), 192, 193(1), 194(1), 202,210, 224(1) and (4), 227(1), 228(1) and (3), 231(1), 252(2),262(1), 295, 299, 300, 302, 304, and 305 are treated as cominginto force on 1 April 2007.

(16) Sections 156(1) and (2), 256, 258, 273(1) and (3), and 274 aretreated as coming into force on 17 May 2007.

(17) Sections 50, 51, 52, 78, 101, and 182(17), (26), and (59) aretreated as coming into force on 20 June 2007.

(18) Sections 5, 12, 28, 29, 30, 34, 75, 98, 99, 103, 105, 106, 107,108, 109, 110, 111, 112, 113, 114, 115, 116, 117, 118, 119,120, 121, 122, 123, 124, 125, 126, 127, 134, 135(1), 139, 141,142, 143, 144, 145, 146, 147, 148, 149, 150, 151, 152, 157,158, 159, 160, 161, 162, 163, 164(2), 166(2), 168, 169, 170,171, 172, 173, 174, 175, 179(2), 180, 182(2), (4), (23), (31),(35), (36), (37), (38), (39), (40), (41), and (42), 186, 190, 195,196(1), (2), and (4), 207(2), (5), (6), (8), and (9), 208(1), 236,

25

Taxation (Business Taxation and RemedialMatters) Act 2007 2007 No 109s 2

237, 238, 239, 240, 245, 246, 247, 248, 249, and 279(1) aretreated as coming into force on 1 October 2007.

(19) Section 275 is treated as coming into force on 30 November2007.

(20) Sections 191, 193(2) and (3), 194(2) and (3), 196(3) and (5),201, 203(2), 204(1), 205, 206(2) and (3), 207(1), (3), (4), (7),and (10), 208(2), 211, 212, 213, 214, 215, 216, 217, 218, 219,222, 223, 224(2), (3), and (5), 227(2), 228(2), 231(2) to (4),241(2), 242, 243, 244, 250(1) to (3), 251, 252(1), (3), and (4),253, 254, 255, 257, 259, 260, 261, 262(2), 263, 264, 265, 266,267, 269(2) and (4), 272(2), 278, 279(2), 290, 294, 307 to 318,321 to 328, 330 to 342, 344 to 437, 438(1), 439 to 538, 540 to549, 550(2) to (41) and (43) to (68), 551 to 553, 554(1) and(2), and 555 to 562 come into force on 1 April 2008.

(21) Sections 14, 15, 21, 36, 37, 137, 182(32), 183, 197(1) to (3),198, 303, 319, 320, 329, 343, 438(2), 539, 550(42), and554(3) come into force on 1 July 2008.

(22) Sections 220(1), 293, 297, and 298 come into force on theearlier of the following:(a) a date to be fixed by the Governor-General by Order in

Council:(b) 1 April 2009.

(23) Section 229 comes into force on the earlier of the following:(a) a date to be fixed by the Governor-General by Order in

Council:(b) 1 April 2010.

Part 1Amendments to Income Tax Act 2004

3 Income Tax Act 2004Sections 4 to 186 amend the Income Tax Act 2004.

4 Withholding liabilities(1) After section BE 1(5), the following is inserted:

‘‘Retirement scheme contributions

‘‘(5B)A person who makes a retirement scheme contribution to aretirement savings scheme must pay retirement scheme con-tribution withholding tax under the RSCWT rules.’’

26

Taxation (Business Taxation and RemedialMatters) Act 2007 Part 1 s 52007 No 109

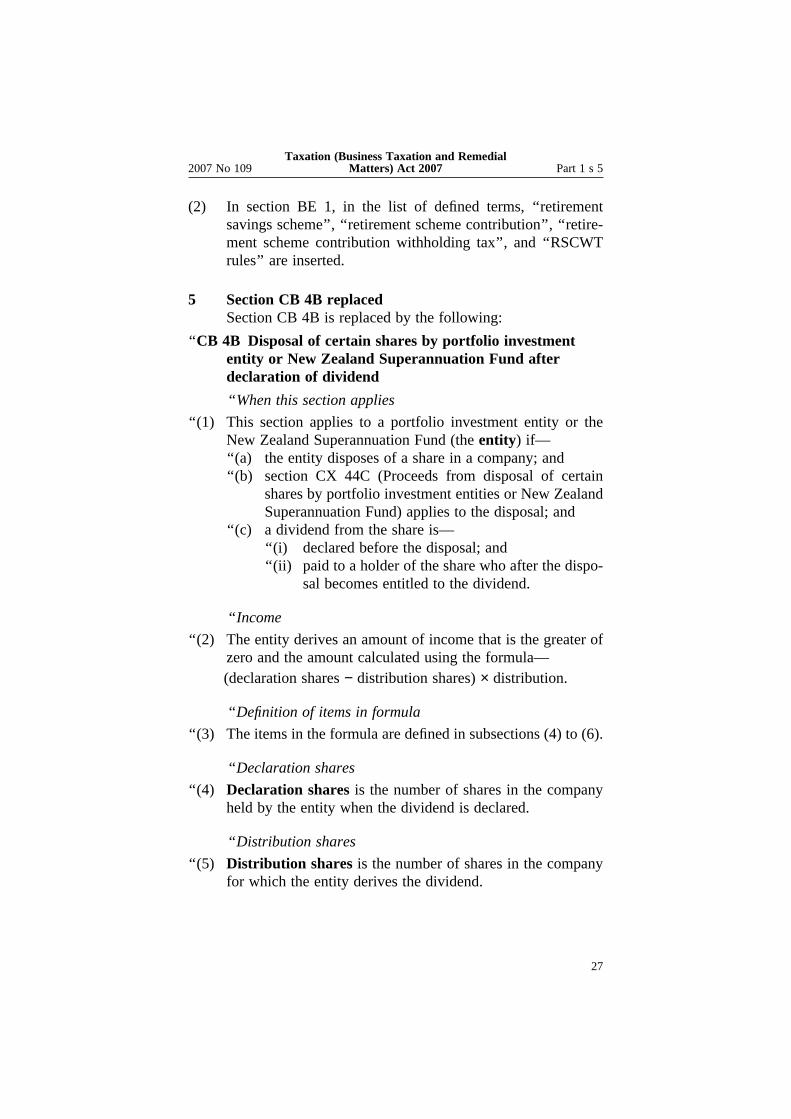

(2) In section BE 1, in the list of defined terms, ‘‘retirementsavings scheme’’, ‘‘retirement scheme contribution’’, ‘‘retire-ment scheme contribution withholding tax’’, and ‘‘RSCWTrules’’ are inserted.

5 Section CB 4B replacedSection CB 4B is replaced by the following:

‘‘CB 4B Disposal of certain shares by portfolio investmententity or New Zealand Superannuation Fund afterdeclaration of dividend

‘‘When this section applies

‘‘(1) This section applies to a portfolio investment entity or theNew Zealand Superannuation Fund (the entity) if—‘‘(a) the entity disposes of a share in a company; and‘‘(b) section CX 44C (Proceeds from disposal of certain

shares by portfolio investment entities or New ZealandSuperannuation Fund) applies to the disposal; and

‘‘(c) a dividend from the share is—‘‘(i) declared before the disposal; and‘‘(ii) paid to a holder of the share who after the dispo-

sal becomes entitled to the dividend.

‘‘Income

‘‘(2) The entity derives an amount of income that is the greater ofzero and the amount calculated using the formula—(declaration shares − distribution shares) × distribution.

‘‘Definition of items in formula

‘‘(3) The items in the formula are defined in subsections (4) to (6).

‘‘Declaration shares

‘‘(4) Declaration shares is the number of shares in the companyheld by the entity when the dividend is declared.

‘‘Distribution shares

‘‘(5) Distribution shares is the number of shares in the companyfor which the entity derives the dividend.

27

Taxation (Business Taxation and RemedialMatters) Act 2007 2007 No 109Part 1 s 5

‘‘Distribution

‘‘(6) Distribution is the amount for a share of—‘‘(a) the dividend that is not fully imputed as that term is

defined in section NG 2(3) (Application of NRWTrules), if the share is issued by a company that has animputation credit account; or

‘‘(b) the dividend, if paragraph (a) does not apply.

‘‘Defined in this Act: amount, company, dividend, imputation credit account,income, portfolio investment entity, share’’.

6 New section CB 5A inserted(1) Before section CB 5, the following is inserted:

‘‘CB 5A Land partially sold or sold with other landSections CB 5 to CB 21 apply to amounts derived from thedisposal of land if the land—‘‘(a) is part of the land to which the relevant section applies:‘‘(b) is the whole of the land to which the relevant section

applies:‘‘(c) is disposed of together with other land.

‘‘Defined in this Act: amount, dispose, land’’.

(2) Subsection (1) applies for the 2005–06 and later income years.

7 Disposal: amount from major development or divisionand not already in income

(1) Section CB 11(2) is replaced by the following:

‘‘Exclusions

‘‘(2) Subsection (1) is overridden by the exclusions for residentialland in section CB 15, for business premises in section CB 18,for farm land in section CB 19, and for investment land insection CB 21.’’

(2) Subsection (1) applies for—(a) a disposal of land occurring on or after the date on

which this Act receives the Royal assent:(b) a person and a disposal of land occurring before the date

on which this Act receives the Royal assent, if theperson—(i) is the person disposing of the land; and(ii) takes a tax position relating to the disposal in a

return for the income year of the disposal; and

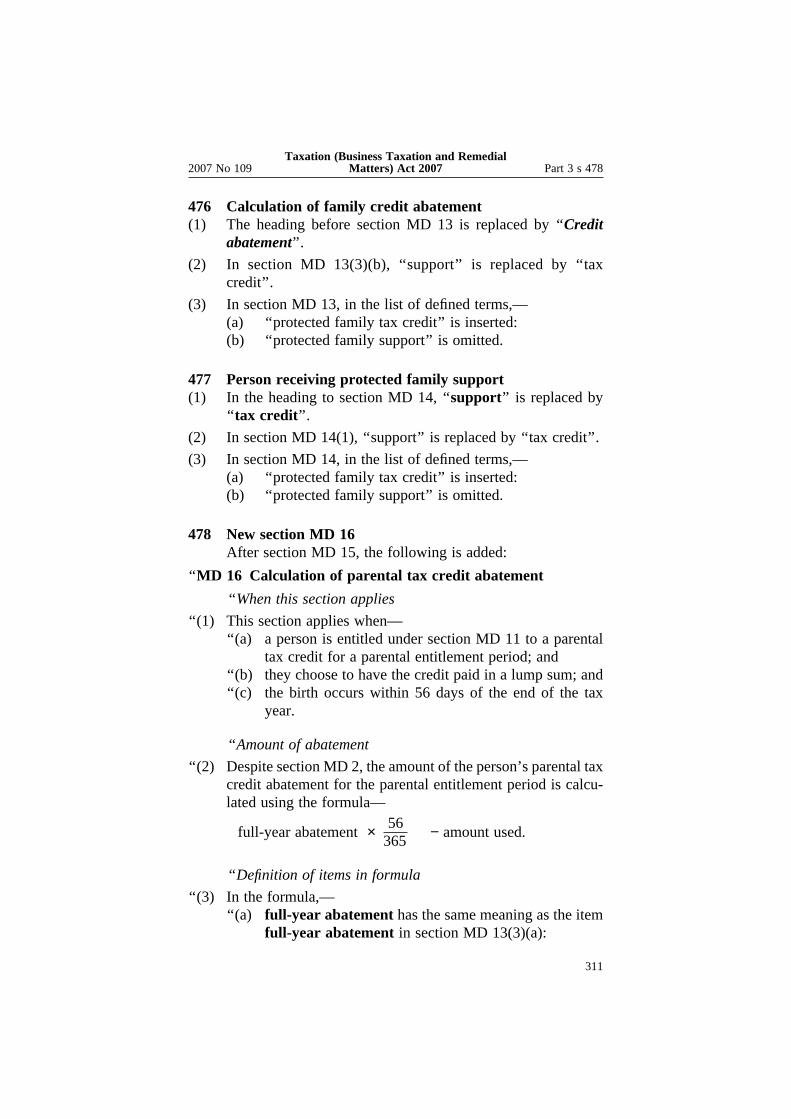

28

Taxation (Business Taxation and RemedialMatters) Act 2007 Part 1 s 102007 No 109

(iii) in taking the tax position, relies on the law thatwould apply if subsection (1) applied for the dis-posal; and

(iv) provides the return to the Commissioner by thedue date for the return.

8 Residential exclusion from sections CB 10 and CB 11In section CB 15(1), in the words before paragraph (a),‘‘Section CB 10 does’’ is replaced by ‘‘Sections CB 10 and CB11 do’’.

9 Business exclusion from section CB 10(1) In the heading to section CB 18, ‘‘section CB 10’’ is replaced

by ‘‘sections CB 10 and CB 11’’.

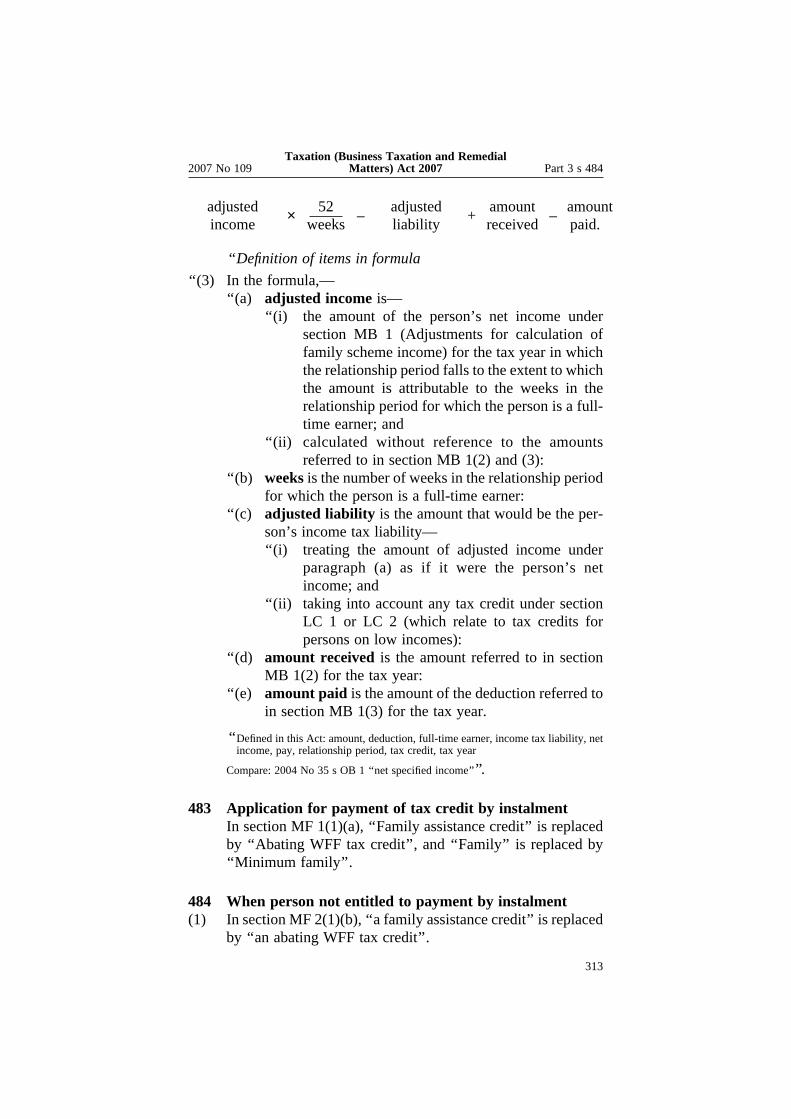

(2) In section CB 18, in the words before paragraph (a), ‘‘SectionCB 10 does’’ is replaced by ‘‘Sections CB 10 and CB 11 do’’.

(3) Subsection (2) applies for—(a) a disposal of land occurring on or after the date on

which this Act receives the Royal assent:(b) a person and a disposal of land occurring before the date

on which this Act receives the Royal assent, if theperson—(i) is the person disposing of the land; and(ii) takes a tax position relating to the disposal in a

return for the income year of the disposal; and(iii) in taking the tax position, relies on the law that

would apply if subsection (2) applied for the dis-posal; and

(iv) provides the return to the Commissioner by thedue date for the return.

10 Investment exclusion from section CB 10(1) In the heading to section CB 21, ‘‘section CB 10’’ is replaced

by ‘‘sections CB 10 and CB 11’’.

(2) In section CB 21, in the words before paragraph (a), ‘‘SectionCB 10 does’’ is replaced by ‘‘Sections CB 10 and CB 11 do’’.

(3) Subsection (2) applies for—(a) a disposal of land occurring on or after the date on

which this Act receives the Royal assent:

29

Taxation (Business Taxation and RemedialMatters) Act 2007 2007 No 109Part 1 s 10

(b) a person and a disposal of land occurring before the dateon which this Act receives the Royal assent, if theperson—(i) is the person disposing of the land; and(ii) takes a tax position relating to the disposal in a

return for the income year of the disposal; and(iii) in taking the tax position, relies on the law that

would apply if subsection (2) applied for the dis-posal; and

(iv) provides the return to the Commissioner by thedue date for the return.

11 Foreign investment fund incomeSection CD 26(b) is replaced by the following:

‘‘(b) the person calculates their FIF income or loss in relationto the interest and the period in which the amount ispaid under—‘‘(i) the comparative value method:‘‘(ii) the deemed rate of return method:‘‘(iii) the cost method:‘‘(iv) the fair dividend rate method; and

‘‘(c) if the calculation referred to in paragraph (b) is underthe fair dividend rate method,—‘‘(i) the FIF is not a grey list company:‘‘(ii) the person does not hold a direct income interest

of 10% or more in the FIF at the beginning of theincome year of the period.’’

12 Determination of amount of credit in certain casesIn section CD 32(26)(b), ‘‘dividend:’’ is replaced by ‘‘divi-dend (section MZ 18 (Fully credited: modifying the actualratio) modifies this paragraph):’’.

13 When does a person have attributed repatriation from aCFC?

(1) In section CD 34(1)(b), ‘‘EX 16’’ is replaced by ‘‘EX 17’’.

(2) Subsection (1) applies for the 2005–06 and later income years.

14 New heading and section CE 12 insertedAfter section CE 11, the following is added:

30

Taxation (Business Taxation and RemedialMatters) Act 2007 Part 1 s 162007 No 109

‘‘Tax credits‘‘CE 12 Tax credits under section LD 1B added to provider’s

income

‘‘When this section applies

‘‘(1) This section applies when a person is allowed under sectionLD 1B (Tax deductions from certain accident compensationpayments: credit allowed to provider) a credit against theperson’s income tax liability in an income year.

‘‘Income

‘‘(2) An amount equal to the credit is income of the person in theincome year, if the amount is not income under any otherprovision.

‘‘Defined in this Act: income, income year, payment’’.

15 Benefits, pensions, compensation, and governmentgrants

(1) In section CF 1(2), in the definition of accident compensa-tion payment (paragraph (f)), ‘‘of that Act’’ is replaced by ‘‘ofthat Act:’’, and the following is added:

‘‘(g) a personal service rehabilitation payment for a claimantunder the Injury Prevention, Rehabilitation, and Com-pensation Act 2001.’’

(2) In section CF 1, in the list of defined terms, ‘‘personal servicerehabilitation payment’’ is inserted.

16 When FIF income arises(1) In section CQ 5(1),—

(a) in paragraph (d), in the words before subparagraph (i),‘‘any time during the income year’’ is replaced by ‘‘anytime in the year’’:

(b) in paragraph (db), in the words before subparagraph (i),‘‘, at any time in the year,’’ is inserted after ‘‘the personholds’’:

(c) in paragraph (f), ‘‘, EX 48 (Top-up FIF income: deemedrate of return method), or EX 49 (Top-up FIF income: 1April 1993 uplift interests)’’ is inserted after ‘‘income orloss)’’.

(2) After section CQ 5(1), the following is inserted:

31

Taxation (Business Taxation and RemedialMatters) Act 2007 2007 No 109Part 1 s 16

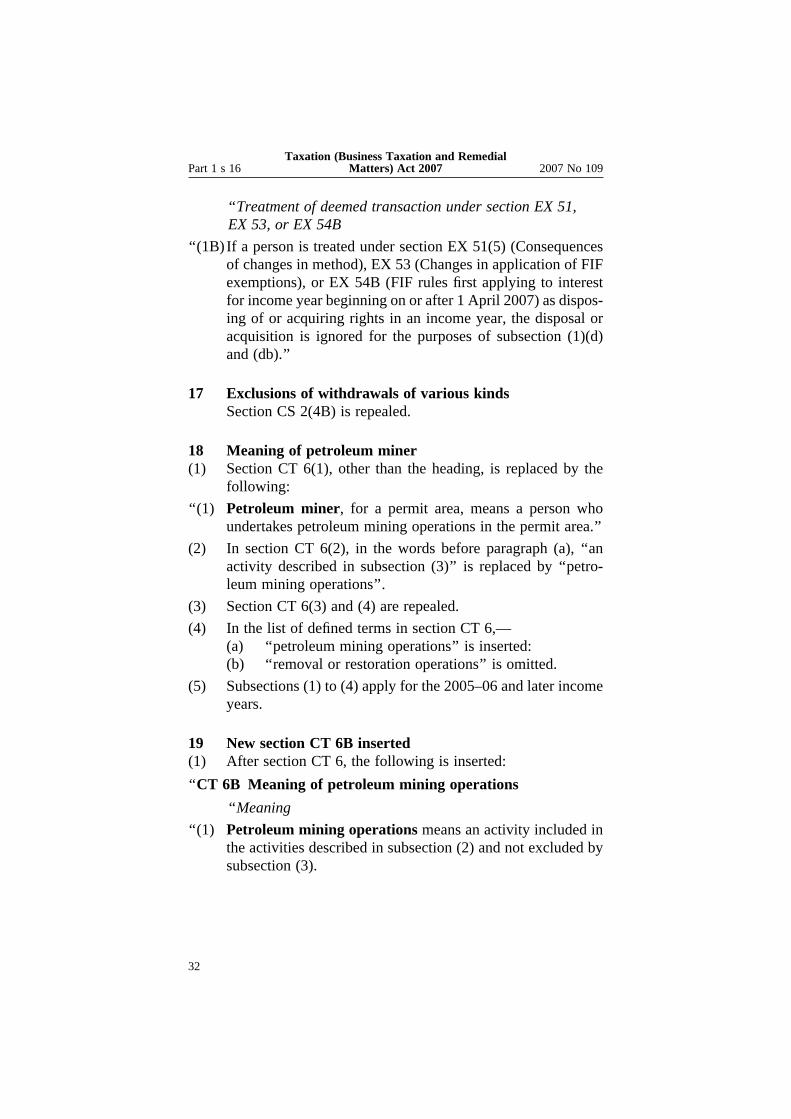

‘‘Treatment of deemed transaction under section EX 51,EX 53, or EX 54B

‘‘(1B) If a person is treated under section EX 51(5) (Consequencesof changes in method), EX 53 (Changes in application of FIFexemptions), or EX 54B (FIF rules first applying to interestfor income year beginning on or after 1 April 2007) as dispos-ing of or acquiring rights in an income year, the disposal oracquisition is ignored for the purposes of subsection (1)(d)and (db).’’

17 Exclusions of withdrawals of various kindsSection CS 2(4B) is repealed.

18 Meaning of petroleum miner(1) Section CT 6(1), other than the heading, is replaced by the

following:

‘‘(1) Petroleum miner, for a permit area, means a person whoundertakes petroleum mining operations in the permit area.’’

(2) In section CT 6(2), in the words before paragraph (a), ‘‘anactivity described in subsection (3)’’ is replaced by ‘‘petro-leum mining operations’’.

(3) Section CT 6(3) and (4) are repealed.

(4) In the list of defined terms in section CT 6,—(a) ‘‘petroleum mining operations’’ is inserted:(b) ‘‘removal or restoration operations’’ is omitted.

(5) Subsections (1) to (4) apply for the 2005–06 and later incomeyears.

19 New section CT 6B inserted(1) After section CT 6, the following is inserted:

‘‘CT 6B Meaning of petroleum mining operations

‘‘Meaning

‘‘(1) Petroleum mining operations means an activity included inthe activities described in subsection (2) and not excluded bysubsection (3).

32

Taxation (Business Taxation and RemedialMatters) Act 2007 Part 1 s 202007 No 109

‘‘Activities: inclusions

‘‘(2) The activities are those carried out in connection with—‘‘(a) prospecting or exploring for petroleum:‘‘(b) developing a permit area for producing petroleum:‘‘(c) producing petroleum:‘‘(d) processing, storing, or transmitting petroleum before its

dispatch to a buyer, consumer, processor, refinery, oruser:

‘‘(e) removal or restoration operations.

‘‘Activities: exclusions

‘‘(3) The activities do not include further treatment to which all thefollowing apply:‘‘(a) it occurs after the well stream has been separated and

stabilised into crude oil, condensate, or natural gas; and‘‘(b) it is done—

‘‘(i) by liquefaction or compression; or‘‘(ii) for the extraction of constituent products; or‘‘(iii) for the production of derivative products; and

‘‘(c) it is not treatment at the production facilities.

‘‘Defined in this Act: permit area, petroleum, petroleum mining operations,removal or restoration operations’’.

(2) Subsection (1) applies for the 2005–06 and later income years.

20 Proceeds of share disposal by qualified foreign equityinvestor

(1) In section CW 11B(4), in the definition of foreign exemptentity,—(a) paragraph (c) is replaced by the following:

‘‘(c) under the laws of the territory, or of the part of theterritory, is not subject to a tax on income other than asa body that handles income of the members; and’’:

(b) in paragraph (f)(iii), ‘‘taxation laws’’ is replaced by‘‘laws’’ in both places that it occurs:

(c) in paragraph (f)(iii), ‘‘subparagraph (ii)’’ is replaced by‘‘subparagraph (ii); and’’ and the following is added:

‘‘(g) does not have a holder of a direct or indirect interest inthe capital of the legal entity who—‘‘(i) is a resident of New Zealand; and

33

Taxation (Business Taxation and RemedialMatters) Act 2007 2007 No 109Part 1 s 20

‘‘(ii) holds a total direct or indirect interest of 10% ormore in the capital of the legal entity, whentreated as holding the interests of any person whois associated with the holder under section OD8(1)’’.

(2) In section CW 11B(4), in the definition of foreign exemptpartnership,—(a) paragraph (c) is replaced by the following:

‘‘(c) under the laws of the territory, or of the part of theterritory, is not subject to a tax on income other than asa body that handles income of the partners; and’’:

(b) in paragraph (h)(ii), ‘‘taxation laws’’ is replaced by‘‘laws’’ in both places that it occurs:

(c) in paragraph (h)(ii), ‘‘subparagraph (i)’’ is replaced by‘‘subparagraph (i); and’’ and the following is added:

‘‘(i) does not have a holder of a direct or indirect interest inthe capital of the unincorporated body who—‘‘(i) is a resident of New Zealand; and‘‘(ii) holds a total direct or indirect interest of 10% or

more in the capital of the unincorporated body,when treated as holding the interests of any per-son who is associated with the holder undersection OD 8(1)’’.

(3) In section CW 11B(4), in the definition of foreign exemptperson,—(a) paragraph (d) is replaced by the following:

‘‘(d) under the laws of the territory, or of the part of theterritory, derives the proceeds from a disposal of sharesor options that are held by the person; and’’:

(b) in paragraph (e)(ii), ‘‘taxation laws’’ is replaced by‘‘laws’’ in both places that it occurs:

(c) in paragraph (e)(ii), ‘‘subparagraph (i)’’ is replaced by‘‘subparagraph (i); and’’ and the following is added:

‘‘(f) does not have a holder of a direct or indirect interest inthe person who—‘‘(i) is a resident of New Zealand; and‘‘(ii) holds a total direct or indirect interest of 10% or

more in the capital of the person, when treated asholding the interests of any person who is associ-ated with the holder under section OD 8(1)’’.

34

Taxation (Business Taxation and RemedialMatters) Act 2007 Part 1 s 232007 No 109

(4) Section CW 11B(5)(a) and (b) are replaced by the following:

‘‘(a) under a double tax agreement between New Zealandand the territory that is in force under the terms of thedouble tax agreement, if—‘‘(i) there is such a double tax agreement; and‘‘(ii) the double tax agreement provides for the resi-

dency of the person:‘‘(b) under the laws of the territory, if paragraph (a) does not

apply.’’

21 New section CW 28B insertedAfter section CW 28, the following is inserted:

‘‘CW 28B Payment of certain accident compensationpaymentsThe amount paid to a person (the claimant) for an incomeyear as a personal service rehabilitation payment for the per-son under the Injury Prevention, Rehabilitation, and Compen-sation Act 2001 is exempt income of the claimant if—‘‘(a) the claimant pays an amount to another person for pro-

viding a key aspect of social rehabilitation referred to inthe definition of personal service rehabilitation paymentin section OB 1; and

‘‘(b) the amount paid by the claimant for a key aspect ofsocial rehabilitation for the income year is equal to ormore than the amount of personal service rehabilitationpayments, after any deduction of tax under this Act,paid to the claimant for the year.

‘‘Defined in this Act: exempt income, income year, payment, personal servicerehabilitation payment’’.

22 Local authoritiesSection CW 32(4)(c)(i) is replaced by the following:

‘‘(i) a council-controlled organisation, other than acouncil-controlled organisation operating a hos-pital as a charitable activity on behalf of the localauthority:’’.

23 Charities: non-business incomeSection CW 34(3), other than the heading, is replaced by thefollowing:

35

Taxation (Business Taxation and RemedialMatters) Act 2007 2007 No 109Part 1 s 23

‘‘(3) This section does not apply to income derived by—‘‘(a) a council-controlled organisation, other than a council-

controlled organisation operating a hospital as a charita-ble activity:

‘‘(b) a local authority from a council-controlled organisation,other than from a council-controlled organisation oper-ating a hospital as a charitable activity on behalf of thelocal authority.’’

24 Charities: business incomeSection CW 35(2), other than the heading, is replaced by thefollowing:

‘‘(2) This section does not apply to income derived by—‘‘(a) a council-controlled organisation, other than a council-

controlled organisation operating a hospital as a charita-ble activity:

‘‘(b) a local authority from a council-controlled organisation,other than from a council-controlled organisation oper-ating a hospital as a charitable activity on behalf of thelocal authority.’’

25 New heading and sections CW 49C and CW 49Dinserted

(1) After section CW 49B, the following is inserted:

‘‘Income of, and distributions by, certaininternational funds

‘‘CW 49C Income of certain international fundsAn amount of income derived by a person is exempt income ifthe person is—‘‘(a) the trustee of the Niue International Trust Fund:‘‘(b) the trustee of the Tokelau International Trust Fund.

‘‘Defined in this Act: amount, exempt income, income, Niue International TrustFund, Tokelau International Trust Fund, trustee

‘‘CW 49D Distributions by certain international fundsAn amount of income derived by a person is exempt income ifthe income is a distribution by—‘‘(a) the trustee of the Niue International Trust Fund:

36

Taxation (Business Taxation and RemedialMatters) Act 2007 Part 1 s 272007 No 109

‘‘(b) the trustee of the Tokelau International Trust Fund.

‘‘Defined in this Act: amount, distribution, exempt income, income, Niue Interna-tional Trust Fund, Tokelau International Trust Fund, trustee’’.

(2) Subsection (1) applies for the 2005–06 and later income years.

26 Heading above section CX 42 replacedThe heading above section CX 42 is replaced by ‘‘Contribu-tions to superannuation scheme or retirement savingsscheme’’.

27 New section CX 42B insertedAfter section CX 42, the following is inserted:

‘‘CX 42B Contributions to retirement savings scheme

‘‘Excluded income

‘‘(1) A retirement scheme contribution is excluded income of—‘‘(a) the person for whose benefit the retirement scheme

contribution is provided, to the extent to which theretirement scheme contribution is—‘‘(i) money:‘‘(ii) an amount of imputation credit or Maori autho-

rity credit that is used to meet the liability of theretirement scheme contributor for retirementscheme contribution withholding tax on theretirement scheme contribution:

‘‘(b) the retirement savings scheme.

‘‘Exclusion

‘‘(2) Subsection (1)(a) does not apply if the person for whosebenefit the retirement scheme contribution is provided—‘‘(a) supplies to the retirement scheme contributor, or to the

retirement savings scheme, a retirement scheme with-holding rate that is less than the retirement schemeprescribed rate for the person:

‘‘(b) includes the retirement scheme contribution in a returnof income for the income year in which the retirementscheme contribution is provided:

37

Taxation (Business Taxation and RemedialMatters) Act 2007 2007 No 109Part 1 s 27

‘‘(c) is a non-resident and the retirement scheme contribu-tion is non-resident withholding income.

‘‘Defined in this Act: excluded income, income year, non-resident, non-residentwithholding income, retirement savings scheme, retirement scheme contribution,retirement scheme contributor, retirement scheme prescribed rate, retirementscheme withholding rate, return of income ’’.

28 Proceeds from disposal of certain shares by portfolioinvestment entities or New Zealand SuperannuationFund

(1) In section CX 44C(1), in the words before paragraph (a),‘‘portfolio investment entity’’ is replaced by ‘‘portfolio invest-ment entity or by a life insurer, in relation to that part of thelife insurer that is a portfolio investment-linked life fund,’’.

(2) Section CX 44C(1)(a)(i) is replaced by the following:

‘‘(i) resident in Australia and not treated as being resi-dent in a country other than Australia in an agree-ment between Australia and another country thatwould be a double tax agreement if the agreementwere negotiated between New Zealand and theother country; and’’.

(3) In section CX 44C(1)(b), ‘‘share.’’ is replaced by ‘‘share; and’’and the following is added:

‘‘(c) the entity disposing of the share is not assured, under anarrangement entered with another person when theshare is acquired, of having a gain on the disposal.’’

(4) In section CX 44C, in the list of defined terms, ‘‘portfolioinvestment-linked life fund’’ is inserted.

29 Portfolio investor allocated income and distributions ofincome by portfolio investment entities

(1) Section CX 44D(1) is replaced by the following:

‘‘Portfolio investor allocated income

‘‘(1) Portfolio investor allocated income derived under section CP1 (Portfolio investor allocated income) in a portfolio calcula-tion period in an income year by an investor in a portfolio taxrate entity is excluded income of the investor if—‘‘(a) the prescribed investor rate for the investor and the

portfolio calculation period is more than zero; and

38

Taxation (Business Taxation and RemedialMatters) Act 2007 Part 1 s 312007 No 109

‘‘(b) the prescribed investor rate for the investor and theportfolio calculation period is not more than the portfo-lio investor rate for the investor and the portfolio calcu-lation period when the entity calculates in relation to theportfolio investor allocated income—‘‘(i) the portfolio entity tax liability of the entity; or‘‘(ii) the amount of a payment under section HL 23B

(Optional payments of tax by portfolio tax rateentities) that the entity intends to be a final pay-ment of the portfolio entity tax liability of theentity in relation to the portfolio investor allo-cated income; and

‘‘(c) for a portfolio tax rate entity making payments of taxunder section HL 21 (Payments of tax by portfolio taxrate entity making no election), the portfolio investorallocated income is not allocated to a portfolio alloca-tion period that includes part of a portfolio investor exitperiod for the investor.’’

(2) In section CX 44D(2), ‘‘distribution by’’ is replaced by ‘‘dis-tribution or dividend of’’.

(3) In section CX 44D(3), in the words before paragraph (a),‘‘distribution by’’ is replaced by ‘‘distribution or dividend of’’.

(4) Section CX 44D(3)(a)(i) is replaced by the following:

‘‘(i) is a natural person or a trustee; and’’.

30 Cost of revenue account property(1) Section DB 17(3)(a) is replaced by the following:

‘‘(a) the person is a portfolio investment entity or a lifeinsurer in relation to that part of the life insurer that is aportfolio investment-linked life fund; and’’.

(2) In section DB 17, in the list of defined terms, ‘‘portfolioinvestment-linked life fund’’ is inserted.

31 Research or development(1) In section DB 26(2), ‘‘paragraph 5.1 or 5.2 of the reporting

standard’’ is replaced by ‘‘paragraph 68(a) of the reportingstandard, applying, for the purposes of that paragraph,paragraphs 54 to 67 of the reporting standard’’.

(2) Section DB 26(3) is repealed.

39

Taxation (Business Taxation and RemedialMatters) Act 2007 2007 No 109Part 1 s 31

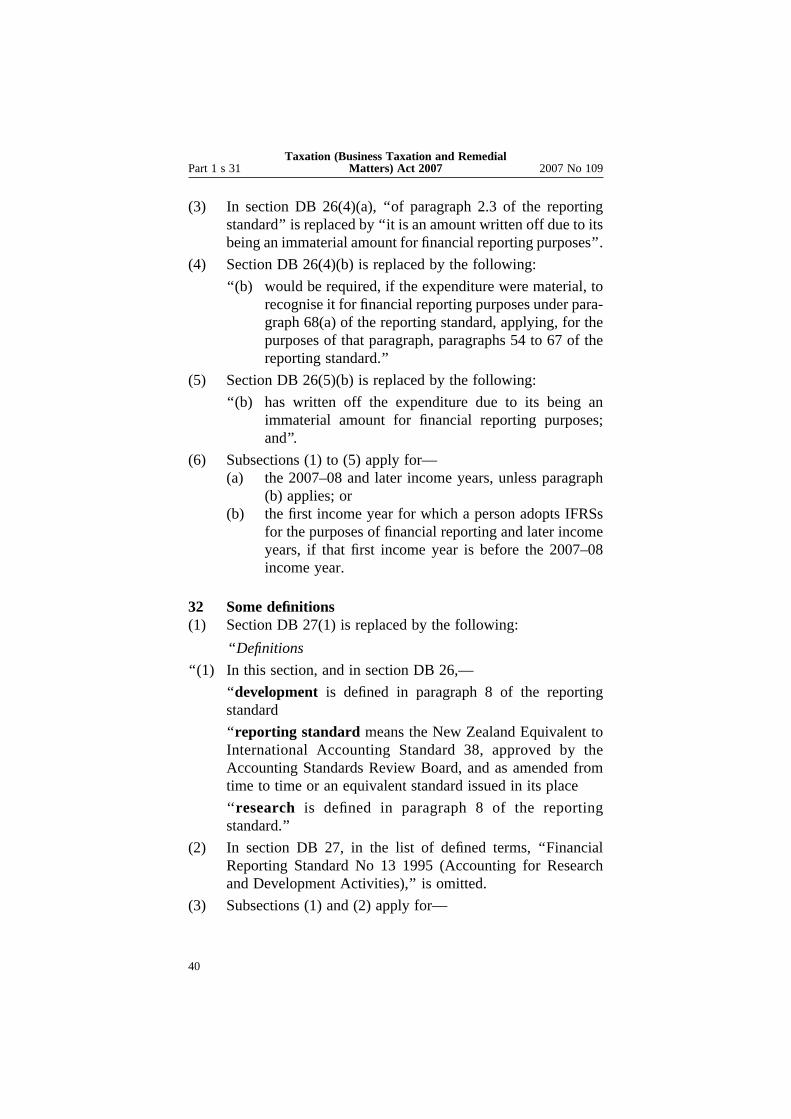

(3) In section DB 26(4)(a), ‘‘of paragraph 2.3 of the reportingstandard’’ is replaced by ‘‘it is an amount written off due to itsbeing an immaterial amount for financial reporting purposes’’.

(4) Section DB 26(4)(b) is replaced by the following:

‘‘(b) would be required, if the expenditure were material, torecognise it for financial reporting purposes under para-graph 68(a) of the reporting standard, applying, for thepurposes of that paragraph, paragraphs 54 to 67 of thereporting standard.’’

(5) Section DB 26(5)(b) is replaced by the following:

‘‘(b) has written off the expenditure due to its being animmaterial amount for financial reporting purposes;and’’.

(6) Subsections (1) to (5) apply for—(a) the 2007–08 and later income years, unless paragraph

(b) applies; or(b) the first income year for which a person adopts IFRSs

for the purposes of financial reporting and later incomeyears, if that first income year is before the 2007–08income year.

32 Some definitions(1) Section DB 27(1) is replaced by the following:

‘‘Definitions

‘‘(1) In this section, and in section DB 26,—

‘‘development is defined in paragraph 8 of the reportingstandard

‘‘reporting standard means the New Zealand Equivalent toInternational Accounting Standard 38, approved by theAccounting Standards Review Board, and as amended fromtime to time or an equivalent standard issued in its place

‘‘research is defined in paragraph 8 of the reportingstandard.’’

(2) In section DB 27, in the list of defined terms, ‘‘FinancialReporting Standard No 13 1995 (Accounting for Researchand Development Activities),’’ is omitted.

(3) Subsections (1) and (2) apply for—

40

Taxation (Business Taxation and RemedialMatters) Act 2007 Part 1 s 352007 No 109

(a) the 2007–08 and later income years, unless paragraph(b) applies; or

(b) the first income year for which a person adopts IFRSsfor the purposes of financial reporting and later incomeyears, if that first income year is before the 2007–08income year.

33 Gifts of money by companyIn section DB 32(3), ‘‘5% of’’ is omitted.

34 Certain investors have deduction for portfolio investorallocated lossSection DB 43B(2)(a) is replaced by the following:

‘‘(a) the portfolio tax rate entity makes payments of taxunder section HL 21 (Payments of tax by portfolio taxrate entity making no election) and the investor’sincome year includes the end of the portfolio tax rateentity’s income year:’’.

35 Sale of business: transferred employment incomeobligations

(1) In section DC 9(2)(a), ‘‘any part’’ is replaced by ‘‘the provi-sion made by the seller for a part’’.

(2) In section DC 9(2)(b), ‘‘of the provision’’ is inserted after ‘‘theamount’’.

(3) Section DC 9(3), other than the heading, is replaced by thefollowing:

‘‘(3) If the seller and the buyer are associated persons at the time ofthe sale,—‘‘(a) the buyer is allowed a deduction for the provision made

by the seller for the amount of employment income ifthe seller would have been allowed a deduction for theamount if the business, or the part of the business, hadnot been sold; and

‘‘(b) section EA 4(5) (Deferred payment of employmentincome) applies.

41

Taxation (Business Taxation and RemedialMatters) Act 2007 2007 No 109Part 1 s 35

‘‘Deduction: Buyer’s payment exceeding provision

‘‘(3B)The buyer is allowed a deduction for any part of the amount ofemployment income that the buyer pays and that exceeds theprovision made by the seller for that amount.’’

(4) In section DC 9(4)(b), ‘‘subsection (3) overrides’’ is replacedby ‘‘subsections (3) and (3B) override’’.

(5) Subsections (1) to (4) apply for the 2005–06 and later incomeyears.

36 Heading to subpart DFIn the heading to subpart DF, ‘‘grants’’ is replaced by ‘‘grantsand compensation’’.

37 New section DF 4 addedAfter section DF 3, the following is added:

‘‘DF 4 Payment by claimant receiving personal servicerehabilitation payment

‘‘When this section applies

‘‘(1) This section applies when a person (the claimant) is paid apersonal service rehabilitation payment for the claimant underthe Injury Prevention, Rehabilitation, and Compensation Act2001 for an income year, and the amount of the payment isassessable income.

‘‘Deduction

‘‘(2) The claimant is allowed a deduction for the income year of theamount given by subsection (3).

‘‘Formula

‘‘(3) The amount of the deduction allowed under subsection (2) iscalculated using the following formula:

amount paid1 − tax rate.

‘‘Definition of items in formula

‘‘(4) In the formula,—‘‘(a) amount paid is the amount paid by the claimant for an

income year for a key aspect of social rehabilitation

42

Taxation (Business Taxation and RemedialMatters) Act 2007 Part 1 s 392007 No 109

referred to in the definition of personal service rehabili-tation payment in section OB 1, to the extent to whichthe amount is less than the amount of personal servicerehabilitation payments, after any deduction of taxunder this Act, paid to the claimant for the income year:

‘‘(b) tax rate is the rate at which tax is deducted under thisAct from personal service rehabilitation payments forthe income year.

‘‘Link with subpart DA

‘‘(5) This section supplements the general permission and over-rides the capital limitation and private limitation for theamount described in subsection (2). The other general limita-tions still apply.

‘‘Defined in this Act: assessable income, capital limitation, general limitation,general permission, income year, payment, personal service rehabilitation pay-ment, private limitation’’.

38 When FIF loss arises(1) In section DN 6(1),—

(a) in paragraph (d), in the words before subparagraph (i),‘‘any time during the income year’’ is replaced by ‘‘anytime in the year’’:

(b) in paragraph (db), in the words before subparagraph (i),‘‘, at any time in the year,’’ is inserted after ‘‘the personholds’’.

(2) After section DN 6(1), the following is inserted:

‘‘Treatment of deemed transaction under section EX 51,EX 53, or EX 54B

‘‘(1B) If a person is treated under section EX 51(5) (Consequencesof changes in method), EX 53 (Changes in application of FIFexemptions), or EX 54B (FIF rules first applying to interestfor income year beginning on or after 1 April 2007) as dispos-ing of or acquiring rights in an income year, the disposal oracquisition is ignored for the purposes of subsection (1)(d)and (db).’’

39 Acquiring film rights(1) In section DS 1(2)(c), ‘‘expenditure.’’ is replaced by ‘‘expen-

diture; or’’ and the following is added:

43

Taxation (Business Taxation and RemedialMatters) Act 2007 2007 No 109Part 1 s 39

‘‘(d) section DS 2B applies to the expenditure.’’

(2) In section DS 1(4), ‘‘except under section DS 2B’’ is insertedafter ‘‘under any other provision of this Act’’.

40 Film production expenditure(1) Section DS 2(3) and (4) are replaced by the following:

‘‘Exclusion

‘‘(3) This section does not apply to film production expenditureif—‘‘(a) the film is produced mainly for broadcast in New

Zealand by a person who operates a television station, atelevision network, or a cable television system:

‘‘(b) the film is intended to be shown as an advertisement:‘‘(c) section DS 2B applies to the film production

expenditure.

‘‘Timing of deduction

‘‘(4) The deduction is allocated under—‘‘(a) section EJ 7 (Film production expenditure for New

Zealand films having no large budget screen productiongrant) or EJ 8 (Film production expenditure for otherfilms having no large budget screen production grant) ifthe film is not one for which a large budget screenproduction grant is made; or

‘‘(b) section EJ 4 (Expenditure incurred in acquiring filmrights in feature films) or EJ 5 (Expenditure incurred inacquiring film rights in films other than feature films) ifthe film is one for which a large budget screen produc-tion grant is made.’’

(2) In section DS 2(5), ‘‘except under section DS 2B’’ is insertedafter ‘‘under any other provision of this Act’’.

(3) Subsection (1) applies for the 2005–06 and later income years.

41 New section DS 2B inserted(1) After section DS 2, the following is inserted:

44

Taxation (Business Taxation and RemedialMatters) Act 2007 Part 1 s 432007 No 109

‘‘DS 2B Expenditure in acquiring film, or film right, intendedfor disposal

‘‘Deduction

‘‘(1) A person is allowed a deduction for film production expendi-ture or expenditure incurred in acquiring a film right if, whenthe person incurs the expenditure, the person intends to dis-pose of the film or film right.

‘‘Timing of deduction

‘‘(2) The deduction is allocated under section EA 2 (Other revenueaccount property).

‘‘Link with subpart DA

‘‘(3) This section overrides the capital limitation. The general per-mission must still be satisfied and the other general limitationsstill apply.