taxation

TRANSCRIPT

Basic Principles and

Classification of Taxes

Basic Principles of Tax System

Classification of Taxes

Forms of Taxes

Some fees, charges and burdens collected by the Bureau of Customs

Examples of Direct Taxes

Examples of Indirect Taxes

Basic Principles of Tax System

1.Fiscal Adequacy

which means that sources of revenue be sufficient to meet the demands of public expenditures

2. Equality or Theoretical Justice

which means that the burden should be in proportion to the taxpayer’s ability to pay

3.Administrative Feasibility

which means that the tax laws should be capable of convenient, just effective and effective administration

Basic Principles of Tax System

Classification of Taxes

Forms of Taxes

Some fees, charges and burdens collected by the Bureau of Customs

Examples of Direct Taxes

Examples of Indirect Taxes

Classification of Taxes

AS TO SUBJECT MATTER

AS TO WHO BEARS THE BURDEN

AS TO DETERMINATION OF AMOUNT

Classification of Taxes

AS TO SUBJECT MATTER

1. Personal, or poll capitation tax

- is a tax of a fixed important on persons residing within a specific territory, whether citizens not , without regard to their priority, occupation or business in which they maybe engaged.

2. Property Tax

– is a tax imposed on property, whether real or proportional and proportion either to its value or in accordance with some reasonable method of appointment. Ex. Residence Tax

3. Excise Tax

- is a charge imposed upon the performance of an act, enjoyment of a privilage, or the engaging in a occupation, professions or bussiness

Ex. VAT

Classification of Taxes

AS TO WHO BEARS THE BURDEN

4. Direct Tax

- is a tax which is demanded from the person who also shoulders the burden of the tax : thus it is the tax for which the taxpayer is directly liable or which he cannot shift to another.

Ex. Income Tax

5. Indirect Tax

-refers to a tax imposed upon goods before they reached the consumer who ultimately pays for it not as tax but as part of purchased price.

Ex. VAT

Classification of Taxes

AS TO DETERMINATION OF AMOUNT

6. Specific Tax

- is a tax of a fixed amount imposed by the head or number,or by some standard of weight or measurement: it requires no

assessment other than listing or classification of the objects to be taxed.

Ex. Taxes on wines

7. Ad Valorem (According to Value)

-refers to tax of a fixed proportion of the value of the property with respect to which tax is assessed. Consequently, it requires the intervention of assessors or appraisers estimate the value of the property before amount due from taxpayer can be determine.

Ex. Taxes on cigarettes

Basic Principles of Tax System

Classification of Taxes

Forms of Taxes

Some fees, charges and burdens collected by the Bureau of Customs

Examples of Direct Taxes

Examples of Indirect Taxes

The Different Forms of

Taxes

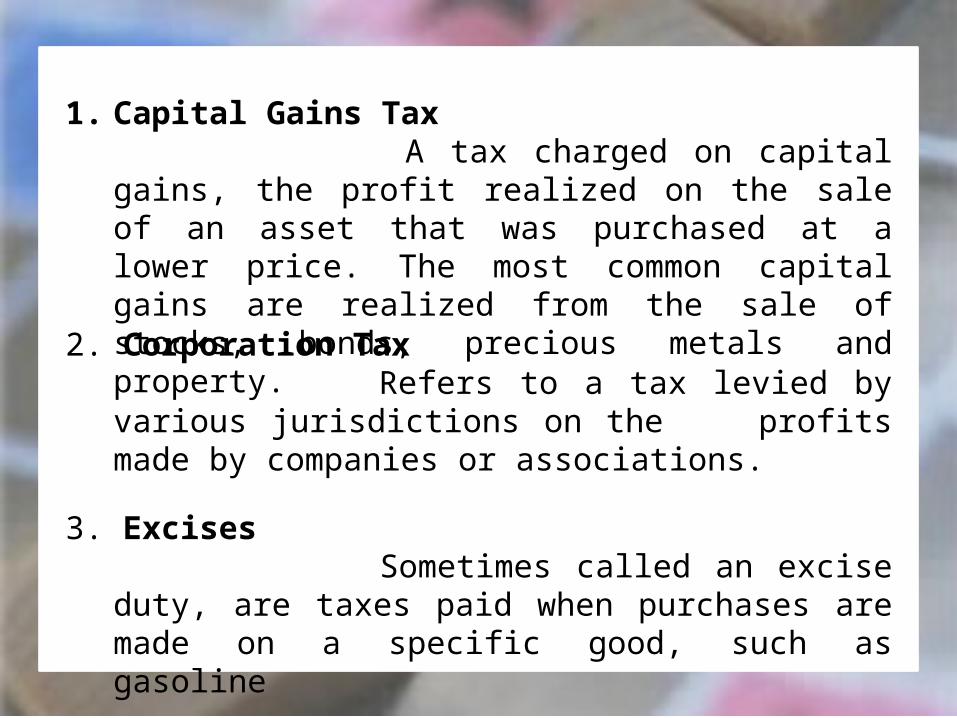

1. Capital Gains Tax A tax charged on capital gains, the profit realized on the

sale of an asset that was purchased at a lower price. The most common capital gains are realized from the sale of stocks, bonds, precious metals and property.

2. Corporation Tax Refers to a tax levied by various jurisdictions on the

profits made by companies or associations.

3. Excises Sometimes called an excise duty, are taxes paid when

purchases are made on a specific good, such as gasoline

4. Income Tax A tax levied on the financial income of persons,

corporations, or other legal entities.

5. Inheritance Tax Inheritance tax, estate tax and death duty are the names

given to various taxes which arise on the death of an individual.

6. Poll Tax A poll tax, head tax, or capitation is a tax of a uniform,

fixed amount per individual (as opposed to a percentage of income).

7. Property Tax Property tax, millage tax is an ad valorem tax that an

owner of real estate or other property pays on the value of the property being taxed.

8. Retirement Tax Some countries with social security systems, which

provide income to retired workers, fund those systems with specific dedicated taxes.

9. Sales Tax A state or locality imposed percentage tax at the

point of purchase for certain goods and services

10. Tariffs A tariff is a tax on foreign goods upon importation.

11. Toll A toll is a tax or fee charged to travel via a road, bridge,

tunnel or other route

12. Transfer Tax In a narrow legal sense, a transfer tax is essentially a

transaction fee (often relatively small in relation to the value of property) imposed on the transfer of title to property

13. Value Added Tax A tax on exchanges. It is levied on the value added that

results from each exchange

14. Wealth (net worth) Tax Because of the broad term “wealth”, property tax,

capital transfer taxes (inheritance tax, estate tax, gift tax), endowment tax and capital gains taxes are sometimes referred to as “wealth taxes”.

Basic Principles of Tax System

Classification of Taxes

Forms of Taxes

Some fees, charges and burdens collected by the Bureau of Customs

Examples of Direct Taxes

Examples of Indirect Taxes

DIRECT

Direct taxes are taxes that are imposed directly on the taxpayer. The burden of these taxes are not in general passed on to others. They are levied based on the ability-to-pay principle.

Personal Income TaxPersonal Income Tax (PIT) is a direct tax levied on income

of a person. A person means an individual, an ordinary partnership, a non-juristic body of person and an undivided estate. In general, a person liable to PIT has to compute his tax liability, file tax return and pay tax, if any, accordingly on a calendar year basis.

Corporate Income TaxAn assessment levied by a government on the profits of a

company. The rate of corporate income tax paid by a business varies between countries, although since corporations are legal entities distinct from their owners and operators, they are typically taxed as if they were people.

Transfer TaxesAny kind of tax that is levied on the transfer of official

documents or other property. Transfer tax is paid by the seller of the property.

Transfer taxes in the Philippines are of two kinds:

Gift TaxA federal tax applied to an individual giving anything

of value to another person. For something to be considered a gift, the receiving party cannot pay the giver full value for the gift, but may pay an amount less than its full value. It is the giver of the gift who is required to pay the gift tax. The receiver of the gift may pay the gift tax, or a percentage of it, on the giver's behalf in the event that the giver has exceeded his/her annual personal gift tax deduction limit.The following are generally excluded from gift tax:

1. Gifts to one's spouse.

2. Gifts to a political organization for use by the political organization.

3. Gifts that are valued at less than the annual gift tax exclusion for a given year.

4. Medical and educational expenses - payments made by a donor to a person or organization such as a college, doctor or hospital.

Estate Taxis a tax on the right of the deceased person to

transmit his/her estate to his/her lawful heirs and beneficiaries at the time of death and on certain transfers, which are made by law as equivalent to testamentary disposition. It is not a tax on property. It is a tax imposed on the privilege of transmitting property upon the death of the owner.

The Estate Tax is based on the laws in force at the time of death notwithstanding the postponement of the actual possession or enjoyment of the estate by the beneficiary.

Basic Principles of Tax System

Classification of Taxes

Forms of Taxes

Some fees, charges and burdens collected by the Bureau of Customs

Examples of Direct Taxes

Examples of Indirect Taxes

Indirect Tax

What Is Indirect Tax ???

is a tax collected by an intermediary such as a retail store from the person who bears the ultimate

economic burden of the tax such as the consumer. The intermediary later files a tax return and forwards the tax proceeds to government with the return. In this sense, the term indirect tax is contrasted with

a direct tax which is collected directly by government from the persons legal or natural on which it is

imposed.

A sales tax is a tax paid to a governing body for the sales of certain goods and services. Usually laws allow (or require) the seller to collect funds for the tax from the consumer at the point of purchase.Laws may allow sellers to itemize the tax separately from the price of the goods or services, or require it to be included in the price (tax-inclusive). The tax amount is usually calculated by applying a percentage rate to the taxable price of a sale.

Other types of sales taxes, or similar taxes, include:•Manufacturers' sales tax: a tax on sales of tangible personal property by manufacturers and producers•Wholesale sales tax: a tax on sales of wholesale of tangible personal property when in a form packaged and labeled ready for shipment or delivery to final users and consumers.•Retail sales tax: a tax on sales of retail of tangible personal property to final consumers and industrial users•Gross receipts taxes, levied on all sales of a business. This tax has been criticized for its "cascading" or "pyramiding" effect, in which an item is taxed more than once as it makes its way from production to final retail sale.Excise taxes, applied to a narrow range of products, such as gasoline or alcohol, usually imposed on the producer or wholesaler rather than the retail seller

•Use tax, imposed directly on the consumer of goods purchased without sales tax, generally items purchased from a vendor who is not under the jurisdiction of the taxing authority (e.g., a vendor in another state). Use taxes are commonly imposed by states with a sales tax, but are usually only enforced for large items such as automobiles and boats.[

•Securities turnover excise tax, a tax on the trade of securities.[]

•Value added taxes, in which tax is charged on all sales, thus avoiding the need for a system of resale certificates. Tax cascading is avoided by applying the tax only to the difference ("value added") between the price paid by the first purchaser and the price paid by each subsequent purchaser of the same item.]

•FairTax, a proposed federal sales tax, intended to replace the U.S. federal income tax.[

•Turnover tax, similar to a sales tax, but applied to intermediate and possibly capital goods as an indirect tax]

Most countries in the world have sales taxes or value-added taxes at all or sever

Basic Principles of Tax System

Classification of Taxes

Forms of Taxes

Some fees, charges and burdens collected by the Bureau of Customs

Examples of Direct Taxes

Examples of Indirect Taxes