tax update 2016. key changes and trends - deloitte us | … · · 2018-02-27tax code, it was not...

TRANSCRIPT

Tax update 2016Key changes and trendsDecember 2015

Introduction

In today’s unstable global economy, tax policy has become one of the key instruments for regulating economic processes and creating a favorable environment for investment and business development. Russia is currently improving its tax legislation in line with global taxation trends, making changes aimed at improving the country’s investment climate.

The adjustments in Russia’s tax code are being made with an eye toward balancing the interests of the state with those of taxpayers. Since the tax burden on businesses engaged in priority sectors has been reduced, the tax burden on super incomes of businesses and individuals has gone up. Additionally, while extending benefits aiming atimproving the attractiveness of Russia as an investment destination, the government has simultaneously expanded the range of information subject to disclosure to the tax authorities, with the goal of preventing profit shifting and tax evasion. While some of the changes to Russian tax law will be introduced only in upcoming years, others will come into effect already in 2016.

In this review, we highlight the most significant changes to Russian tax legislation that entered into force on 1 January 2016 – both those stipulated under recently adopted laws and those introduced before 2015, but coming into effect in 2016. We also take a look at developments in OECD taxation polices and initiatives undertaken by Russian lawmakers to bring local legislation more in line with global standards.

Additionally, we include a section on current trends in Russian taxation legislation. Even though the changes we examine in this section did not enter into force on 1 January 2016, we believe they will come into effect in the short-to-medium term, and are therefore relevant for tax planning purposes.

Contents

Profit tax

Participation exemption rule

Simplification of the procedure for selling financial instruments

Amendments to the participation exemption rule

New tax incentives

Other amendments to the profit tax

Environmental duty

Consolidated taxpayers

Excise duties

Mineral Extraction Tax

Extension of the powers of the Russian Ministry of Finance

VAT

Personal Income Tax

Taxation of income derived from sale of real estate

Extension of tax amnesty

Taxation of income derived from alienation of shares

Proceeds from liquidation

New rules for the application of DTTs

Other amendments to PIT

Changes enacted on 1 January 2016

BEPS

Controlled foreign companies

Focus on Asia

Introduction

Contacts

Subscribe to Deloitte periodicals

Links

Super income tax for the oil industry

Liabilities for non-settlement of mandatory social contributions

VAT on e-services

Measures to support exports

Changes to transfer pricing rules

Limitations to interest deductions in intracompany loans

Improvements to the exchange of tax information

Improving the investment climate

Control over unincorporated foreign entities

Key trends in Russian taxation

Changes enacted on 1 January 2016

Participation exemption rule2016 is the first tax period when the participation exemption rule can be applied. According to the rule, income derived from the sale or other redemption of shares and participation interest in the charter capital of Russian companies purchased on or after 1 January 2011 will be exempt from taxation, subject to certain terms and conditions 1.

Reduction of the ownership term for applying participation exemption rules to bonds and investment units in high-tech companiesParticipation exemption can be applied to income derived from the sale or other disposal of bonds and investment units of Russian hi-tech companies if these securities have been held for more than 12 months 2.

Application of arm’s-length principles in transactions with securities and derivatives not regarded as controlled for transfer pricing purposesAs of 1 January 2016, the liability to confirm the application of arm’s-length pricing principles in sales of securities and derivatives will be limited to transactions that are regarded as controlled according to transfer pricing rules.

This change is aimed at simplifying the taxation of income derived from the sale of securities and derivatives by bona fide taxpayers 3.

Profit tax

Profit tax and MET incentivesA special tax regime has been established for residents of the Free Port of Vladivostok. According to the regime, the profit tax rate for residents of the Free Port should not exceed 5% during the first five years and could be reduced up to 12% for the following five years 4.

Similar benefits are provided to taxpayers registered within the Special Economic Zone in the Magadan region. The profit tax rate for qualified taxpayers could be reduced up to 13.5% subject to certain conditions. Qualified taxpayers should maintain separate accounting for income and expenses attributable to activities carried out within the Special Economic Zone. Qualified taxpayers will also be able to apply the specific 40% discount to standard MET rates for mineral resources extracted from the land plots within the Special Economic Zones 5.

Starting from 2016, corporate taxpayers providing childcare services will be able to apply a reduced profit tax rate of 0%, provided the income from childcare services constitutes at least 90% of the total income recognized for profit tax purposes 6.

Enacting the participation exemption rules is likely to spur a number of M&A transactions and intragroup restructurings previously delayed due to unfavorable tax implications

Tax update 2016 Key changes and trends4

Changes enacted on 1 January 2016

Profit tax

Other changes to business tax• For debt obligations that are regarded as controlled transactions for transfer

pricing purposes and executed in rubles, the safe harbor for interest rates has been narrowed. Starting 1 January 2016, it is set from 75% to 125% of the key rate of the Central Bank of Russia 7.

• Temporary rules for interest limitations under thin capitalization rules are extended until 31 December 2016 due to continuing currency fluctuations. Specific rules (disregarding FOREX charges for debt-to-equity ratio calculation) are applicable to borrowings attracted before 1 October 2014 if the terms and conditions of these borrowings remain unchanged 8.

• The value of property recognized as a fixed asset for profit tax purposes is increased from RUB 40,000 to RUB 100,000; as a result, property that has been put into operation on or after 1 January 2016 will be regarded as depreciable only if its value exceeds RUB 100,000; otherwise its cost should be written-off immediately upon putting it into operation 9.

• The government has introduced developments in taxation for FOREX differences arising from revaluation of precious metals booked by the banks at depersonalized metal accounts. Since there was wording ambiguity in the Tax Code, it was not clear, whether or not such FOREX differences should be accrued for Profits tax purposes. This resulted in disputes between taxpayers and tax authorities 10.

• According to amended rules for taxation of transactions with clearing participation certificates the following items should be excluded from Profits tax: (1) profit of the clearing organization derived from issuance of clearing participation certificates; (2) assets derived from redemption of clearing participation certificates; (3) expenses associated with transfer of assets into the assets pool; and (4) expenses of the clearing organization arising at redemption stage. Service fees of clearing organizations related to issuance and circulation of clearing participation certificates are deductible for profits tax purposes 11.

Tax update 2016 Key changes and trends5

Changes enacted on 1 January 2016

In particular, the new measures specify the following:• CT agreements registered by tax authorities through 2014 – 2015

are deemed unregistered. Affected CTs should be notified of this on or before 1 March 2016;

• Registration of new CT agreements and amendments to existing CT agreements extending them is suspended until 1 January 2018;

• The minimum length of a CT agreement is increased from two tax periods to five tax periods.

Consolidated taxpayers (hereinafter – CT)The introduction of the CT concept has resulted in a reduction of tax income at hands of regional tax authorities, since it encourages the utilization of tax losses and shifting revenues to low tax regions

Positive and negative impact on regional budgetsTotal impact Russia-wide (in RUB billion)

Increase of tax income (number of regions)

Decrease of tax income (number of regions)–150 –100 –50 0 50 100

Total

Decrease of income

Increase of income

Results and perspectiveThe government has undertaken a number of measures to suspend both the registration of new CTs and extension of existing CTs12. The introduction of the CT concept has resulted in a reduction of tax income for regional tax authorities since it encourages the utilization of tax losses and the shifting of revenues to low tax regions13.

Tax update 2016 Key changes and trends6

Changes enacted on 1 January 2016

Environmental duty

A new duty for producers and importersProducers and importers are now required to pay an environmental duty on goods that must be disposed of at the end of their commercial life. Alternatively, producers and importers can dispose of the waste on their own, but such disposal requires a license. However, the procedure for obtaining such a license has not yet been clarified 14.

The environmental duty will not apply to goods produced for export or not intended for use in Russia.

As of today, most of the documents governing the payment of the environmental duty have been approved by the Russian government, with the notable exceptions of the calculation form and environmental duty rates.

2016 will be the first reporting year for the environmental duty; it must be paid on or before 15 April 2017. We believe that the amount of the environmental duty may turn out to be quite significant, and may seriously affect the cost of produced goods and business profitability.

Producers and importers are now required to pay an environmental duty

Tax update 2016 Key changes and trends7

Changes enacted on 1 January 2016

Personal Income Tax (hereinafter – PIT)

Extension of the voluntary disclosure period for foreign-held assetsThe period for individuals to voluntarily declare their assets and accounts held in foreign banks has been extended until 30 June 2016 15.

Taxation of income derived from sale of real estateThe conditions for exempting income derived from the sale of real estate from taxation have been amended. The changes include:

• Full PIT exemption for real estate that has been held for over five years 16;• In a limited number of cases, the PIT exemption can be applied after three years

of ownership;• The amount of income derived from the sale of real estate should be compared

against the cadastral value multiplied by the reducing coefficient of 0.7. Should the actual income amount be below the calculated value, the difference should be regarded as the individual’s taxable income.

Taxation of income derived from alienation of sharesStarting this year, the income from sale of stocks and shares in the charter capital of an LLC owned by a taxpayer for more than five years (acquired in 2011 or earlier) are exempt from taxation. Similar to Profits tax, participation exemption could be applied to income derived from sale or other disposal of bonds and investment units of Russian hi-tech companies, if these securities have been held for more than 12 months 17.

Additionally, the rules for calculation of PIT in case of sale, reduction of the nominal value or redemption of the shares in the charter capital of an LLC as well as the distribution of liquidation proceeds upon liquidation of an LLC have been specified as follows:

• In indicated cases, expenses related to the acquisition of property or proprietary rights may be deducted from the PIT base 18;

• The deductible expenses related to the acquisition of the shares in the charter capital of an LLC must be listed;

• The requirements for applying of a PIT deduction associated with the sale of shares in the charter capital of an LLC have been prescribed.

Everything you need to know aboutvoluntary disclosures

LT in focus Все, что нужно знать о добровольном декларировании имущества и вкладов Вниманию физических лиц

Ниже мы приводим краткое описание возможностей, которые предоставляет закон «О добровольном декларировании»1.

Закон «О добровольном декларировании» дает физическим лицам возможность указать в специальной декларации активы и счета (вклады) в зарубежных банках и воспользоваться рядом гарантий и льгот, предусмотренных для декларанта, номинальных владельцев и ряда иных лиц.

В отношении специальной декларации не предусмотрены какие-либо процедуры проверки или обработки предоставленных данных. Хранение деклараций производится централизованно, а в отношении предоставленных сведений устанавливается режим налоговой тайны, без каких-либо исключений.

Если у вас есть контролируемые иностранные компании, информация о которых должна быть раскрыта налоговым органам, вы можете воспользоваться гарантиями освобождения от уголовной ответственности за нарушения в сфере налогового и таможенного законодательства, от административной ответственности в части осуществления предпринимательской деятельности без регистрации/лицензий, а также от ответственности за совершение налоговых правонарушений. В случае полной или частичной неуплаты налога его взыскание в отношении операций с указанными в декларации активами не производится.

1 Здесь и далее — Законопроект № 754388-6 «О добровольном декларировании физическими лицами

активов и счетов (вкладов) в банках и о внесении изменений в отдельные законодательные акты Российской Федерации», направленный 23 мая 2015 года в Совет Федерации РФ.

Департамент консультирования по налогообложению и праву 02 июня 2015 года

В нашем выпуске от 30 марта мы писали о том, что на официальном сайте Государственной Думы РФ опубликован текст законопроекта «О добровольном декларировании физическими лицами имущества и счетов (вкладов) в банках». В пятницу 22 мая данный законопроект был принят Государственной Думой РФ в третьем чтении. Следующими шагами станут рассмотрение законопроекта Советом Федерации РФ и его подписание Президентом РФ.

В настоящем выпуске мы постараемся ответить на вопросы о том, для кого предусмотрено добровольное декларирование, какие гарантии и льготы предоставляет данный закон, как должен работать механизм предоставления гарантий и какие шаги уже сейчас необходимо предпринять тем лицам, которые хотят воспользоваться данной возможностью.

RU ENG

Tax update 2016 Key changes and trends8

Changes enacted on 1 January 2016

PIT benefits applicable in case of the liquidation of a foreign company/structureIndividuals are granted the right to liquidate their foreign companies/structures and distribute liquidation proceeds without tax consequences. The PIT exemption should apply to foreign companies/structures liquidated before 1 January 2017. In order to apply the PIT exemption, along with the tax return, the taxpayer should submit an application supported with documents confirming the book value of the received assets as of the termination date of the relevant foreign company/structure 19.

Should the received assets be further resold, the individual will be entitled to reduce his PIT base by their book value, provided that the amount of such a deduction does not exceed the market value of these assets.

The above provisions should not apply to monetary funds transferred to shareholders / participants upon the liquidation of a foreign company/structure.

New rules for applying the provisions of Double Tax Treaties (hereinafter – DTTs)The rules for applying the provisions of DTTs by individuals have been changed as of 1 January 2016. The period for submitting documents supporting the application of a foreign tax credit has now been extended to up to three years after the end of the tax period in which the relevant income taxed in a foreign country has been derived. The right to apply a foreign tax credit must be supported by either a certificate issued by foreign tax authorities confirming the amount of income received and foreign tax paid on it, or a copy of the foreign tax return along with payment documents confirming payment of the tax in the relevant foreign state, or a certificate issued by a foreign tax agent confirming that the relevant tax was duly withheld in this foreign state 20.

Additionally, the list of documents confirming the individual’s right for a partial or full PIT exemption in Russia has been expanded. A foreign passport is now one of the documents accepted.

PIT

Tax update 2016 Key changes and trends9

Changes enacted on 1 January 2016

PIT

Other amendments to PIT• Starting from 1 January 2016, tax agents are obliged to submit quarterly reports

on amounts of withheld PIT using the 6-NDFL form. Quarterly reports should be submitted by 30 April, 30 July and 30 October after the respective first three quarters, and the annual report should be submitted by 1 April of the year following the reporting year. Additionally, the period for submitting the 2-NDFL form with under-withheld PIT has been changed; the form is now due by 1 March of the year following the reporting year 21.

• The rules for calculating PIT on income derived from transactions with clearing participation certificates and settlement of mutual claims due to failure to execute the reverse leg have been specified 22.

• It was finally clarified that the PIT exemption on interest income can be applied only in respect of deposits opened with Russian banks 23. The amendments also specify the procedure for taxation of the interest income in case of fluctuations in the key rate of the Central Bank of Russia.

• New rules were introduced for calculating PIT on transactions with securities and derivatives booked on depersonalized investment accounts. In particular, it clarifies calculation of the tax base, utilization of losses, calculation and settlement of PIT 24.

• It is now clearly stated that reimbursement of litigation costs based on the relevant court decision can be exempt from taxation 25.

• Social PIT deduction for medical treatment and education can be obtained by submitting of the relevant application to the tax agents 26. Tax agents should suspend withholding of PIT from an individual’s income starting from the month when the application was submitted. As of 1 January 2016, the threshold for standard PIT deductions has also been increased up to RUB 350,000.

• New rules are introduced for defining the date of receiving deemed income from beneficial loans (i.e. with an interest rate lower than the established limits) and acquisition of securities at a price below the market price as well as income arising upon the offset of mutual claims, write-off of bad debts and reimbursement of business trip expenses. Particularly, the date of receiving deemed income from a beneficial loan is considered to be the last day of each month during the period for which the loan is granted, regardless of whether or not the interests have actually been paid by the borrower 27.

• FOREX dealers should now act as tax agents with regard to transactions carried out based on agreements concluded with individuals.

• The revised Russian Tax Code specifies the cases when the broker (discretionary manager) or the managing company of a mutual fund should act as a tax agent with regard to the transactions related to the investment units of the mutual fund.

Tax update 2016 Key changes and trends10

Changes enacted on 1 January 2016

New types and rates A new type of goods subject to excise was introduced as of 1 January 2016 – medium distillate. Medium distillates are petroleum products that are created in the distillation process and fall between light distillates, such as LNG and gasoline, and heavy distillates, such as fuel oil. New legislation specifies the list of transactions involving medium distillates that are acknowledged as taxable, as well as how to calculate the tax base for these transactions. Additionally, the procedure for issuing registration certificates for organizations carrying out transactions with medium distillates has been clarified.

Excise rates for 2016 and 2017 have also been specified. The following duty rates will apply:

• For alcohol products with a.b.v. up to 9% and over 9%, the rates are same as in 2014 and 2015;

• For wines with protected geographic status or place of origin, the excise duty rate in 2016 will be RUB 5 per liter, and for sparkling wines, RUB 13 per liter;

• The excise duty rates for other wines and sparkling wines will be RUB 9 liter and 26 per liter, respectively;

• The excise duty rate for Class-5 gasoline will beRUB 7,530 per 1 ton, an increase of RUB 2,000 per ton;

• For gasoline not classified as Class-5, the increase will be more significant: the excise duty will be increased by RUB 3,200 to RUB 10,500 per ton;

• Excise duty rates for beer, cigarettes, vehicles of more than 90 horsepower also will be increased;

• Excise duty rate for straight run gasoline and motor oil will be reduced.

Some changes have also been introduced to the procedure for applying tax deductions to calculated excise duties.

VAT Excise duties

Changes to the declarative VAT refundThe threshold for applying the declarative VAT refund is reduced from RUB 10 billion to RUB 7 billion of the total amount of taxes paid during the three years preceding the year in which the relevant application is filed 28.

Temporary VAT reduction for rail transport Long-distance rail transport services for passengers and luggage should be subject to a reduced VAT of 10% for the period starting 1 January 2016 and lasting until 31 December 2017 29.

Tax exemption for import of equipmentThe Russian government has adopted resolutions that expand the list of imported technological equipment, including components and spare parts, that are exempt from import VAT 30. The exemption applies to the following types of equipment:

• Specific gas-turbine power generators;• Electric generators;• Heat-treating equipment;• Other equipment.

The government has also approved a new unified list of imported medical goods that are exempt from import VAT 31. This list replaces all earlier ones.

Tax update 2016 Key changes and trends11

Changes enacted on 1 January 2016

Mineral Extraction Tax (MET)

Specification of the procedure for calculating of loss limits for METThe new amendments have been passed that more precisely specify types of extracted minerals in accordance with the Federal Law “On precious metals and stones” and clarify the conditions of applying 0% MET rates to technical loss limits. These changes are long-awaited by MET payers, since the number of disputes arising from uncertainty in the calculation of the MET base has dramatically increased in recent years. The determination of the final product subject to MET is extremely important as it defines the stage of weighing extracted goods (whether it is performed at the ore stage or at the semi-finished extraction stageor at the final stage of pure precious metal). This determination affects the applicability of 0% MET to technical loss limits arising at the various stages of extraction of semi-finished and pure precious metals. The Federal Agency on Subsoil Usage has taken up the issue, but the number of court disputes has not decreased. We believe that these changes will help decrease the number of disputes and minimize the risk of additional MET charges 32.

Extension of the Ministry of Finance powers

Unified management system for tax and non-tax payment In accordance with the Decree of the President dated 15 January 2016 the Ministry of Finance is set as a management body for the Federal Tax Service,the Federal Customs Service, the Federal Service for Regulation of Alcohol Turnover, the Federal Service for Financial and Budgetary Supervision and the Federal Treasury. Previously Earlier the Federal Tax Service and the Federal Service for Regulation of Alcohol Turnover were reporting directly to the Russian Government. The aforementioned changes are performed in line with the intention to implement the Unified management system for tax and non-tax payment 33.

Control over unincorporated foreign entities

Extension of information disclosureDespite the abundance of unincorporated entities in global practice, until now, their activities have been regulated neither by DTTs, nor by domestic Russian legislation. The elimination of these gaps in regulation is long overdue, and a newly adopted law introduces the concept of unincorporated foreign entities, which includes funds, partnerships, associations, trusts and other forms of collective investment and (or) discretionary management. The law also determines the amount of information about unincorporated foreign legal entity clients subject to disclosure for the purposes of identifying their beneficiaries 34.

Tax update 2016 Key changes and trends12

Key trends in Russian taxation

BEPS

Key developmentsIn line with the OECD’s Base Erosion and Profit Shifting Plan, we expect Russia to introduce the following measures:

• Further harmonization of taxation rules in line with the OECD Guidelines and BEPS initiative;

• Extension of automatic exchange of information on financial transactions with foreign jurisdictions for taxation purposes;

• Changes in taxation of intercompany loans;• Improvements in taxation of controlled foreign corporations;• Improvement of direct and indirect taxation of e-commerce.

Even though Russia is not an OECD member, the BEPS plan is referred to by the Russian government in its strategic goals for the development of tax legislation during 2016 – 2018

Tax update 2016 Key changes and trends13

Changes to transfer pricing rules

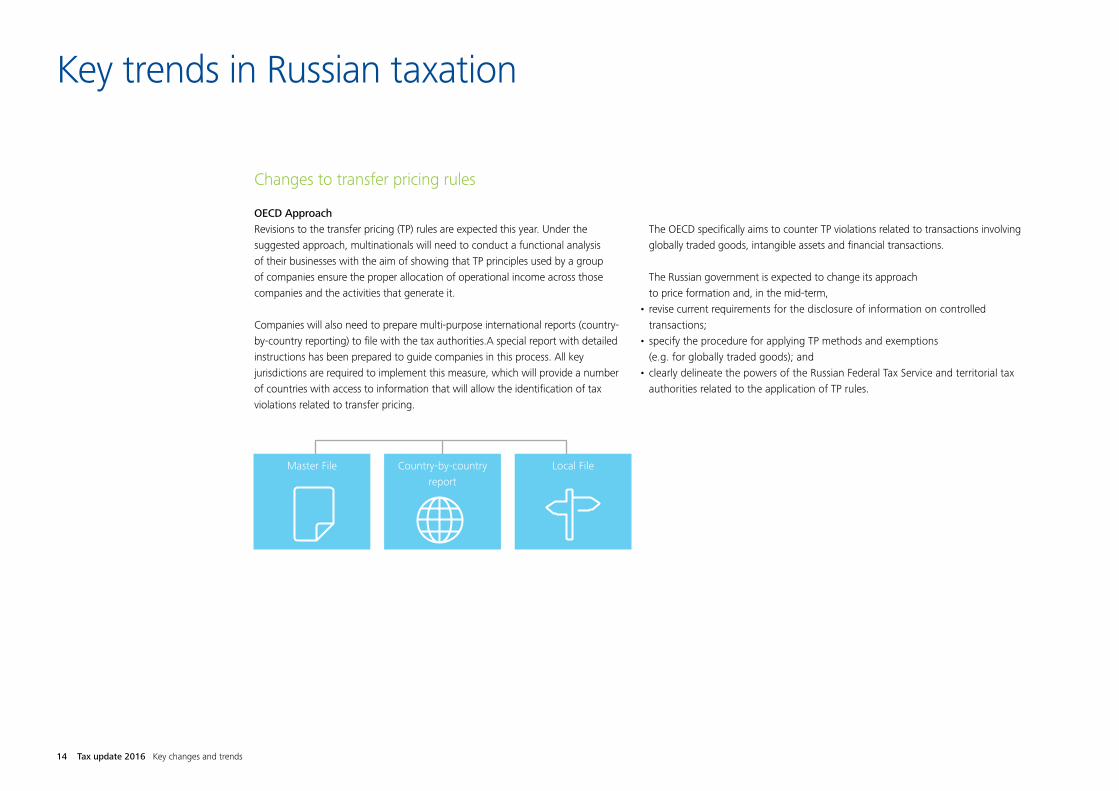

OECD ApproachRevisions to the transfer pricing (TP) rules are expected this year. Under the suggested approach, multinationals will need to conduct a functional analysis of their businesses with the aim of showing that TP principles used by a group of companies ensure the proper allocation of operational income across those companies and the activities that generate it.

Companies will also need to prepare multi-purpose international reports (country-by-country reporting) to file with the tax authorities.A special report with detailed instructions has been prepared to guide companies in this process. All key jurisdictions are required to implement this measure, which will provide a number of countries with access to information that will allow the identification of tax violations related to transfer pricing.

The OECD specifically aims to counter TP violations related to transactions involving globally traded goods, intangible assets and financial transactions.

The Russian government is expected to change its approach to price formation and, in the mid-term,

• revise current requirements for the disclosure of information on controlled transactions;

• specify the procedure for applying TP methods and exemptions (e.g. for globally traded goods); and

• clearly delineate the powers of the Russian Federal Tax Service and territorial tax authorities related to the application of TP rules.

Master File Local FileCountry-by-country report

Key trends in Russian taxation

Tax update 2016 Key changes and trends14

Transfer pricing in RussiaIn 2015, the business community, acting through the Chamber of Commerce and Industry, presented its suggestions for improving TP rules, some of which have been formalized in a draft law prepared by the Russian Ministry of Finance. Key changes suggested by the Ministry of Finance include the following:

Revision of the requirements for TP documentationTaxpayers will no longer be obligated to prepare TP documents for transactions with counterparties that do not exceed 5% of the total amount of transactions with the same counterparty for a single year and also do not exceed RUB 10 million.

TP tax audits• TP audits can be conducted based on information from a territorial tax authority

regarding potential non-correspondence of the prices in controlled transactions to market prices;

• Territorial tax agents may be engaged in TP audits.

Median value of the market range• The median value of the market range concept will be introduced.• Tax authorities will calculate median values during tax audits in those cases where the

price / profitability ratio of a control transaction goes outside the market range and the taxpayer fails to adjust the tax base. When adjusting the tax base, the taxpayer is entitled to set minimum and maximum price range values.

Change of the threshold for acknowledging transactions as controlled• The threshold for intra-Russian transactions is increased from RUB 2 billion to RUB 3

billion;• The threshold for transactions with foreign affiliated entities is set at RUB 60 million;• The total threshold for income must be indexed on or before 31 December of the

current year using the deflator coefficient set for the next calendar year.

The key amendments to TP rules can be attributed to the state’s transition from exercising formal control of all intra-group transactions to exercising control over only the most significant transactions – ones that may potentially cause significant losses to the state budget and the budgets of the constituent entities. In the mid-term, taxpayers are expected to improve the transparency of transactions and disclose more information related to transactions acknowledged as controlled.

Changes to transfer pricing rules

Key trends in Russian taxation

Tax update 2016 Key changes and trends15

Innovations in thin capitalizationAs part of the BEPS plan, the OECD has developed a number of initiatives aimed at limiting interest deductions. These initiatives are widespread in the domestic legislation of member countries, and are codified particularly in

• thin capitalization rules, • requirements towards the purposive nature of lending

and its correlation with income from its purposive use,• limitations on the recovery of interest on loans provided

for the payment of dividends.

The new OECD guidelines are primarily related to controlling interest-to-EBITDA ratios and the limitation of deductions. However, a number of exceptions have been proposed with an eye to balancing fiscal and business interests. For example, establishing a threshold materiality for the limits to become applicable, as well as the possibility of estimating interest-to-EBITDA ratios at the group level. These changesshould markedly decrease the relative ratio and amount of interest subject to limitation, as the data of intragroup borrowers will be aligned with that of creditors. The possibility of carrying forward non-deductible interest or unused quotas for interest deduction has also been proposed.

The Russian government is participating in the working group for the development of the OECD approach towards corporate lending, and any decision on amending domestic regulations in relation to such lending has been postponed until after the adoption of the resulting OECD guidelines. For this reason, we do not expect significant changes in the short term.

The Russian thin capitalization rules are extremely similar to the proposed changes regarding the determination of threshold interest expenses. Therefore, we believe that the proposed developments are more likely to provide Russian taxpayers with greater room for tax optimization (accounting for aggregated group figures, carrying forward non-deductible interest expenses and unused quotas for interest deduction), than create additional limitations.

In the short term, it is worth noting a draft law that changes the concept of controlled debt 35. The draft law is generally aimed at harmonizing thin capitalization rules with the terms and principles of transfer pricing.

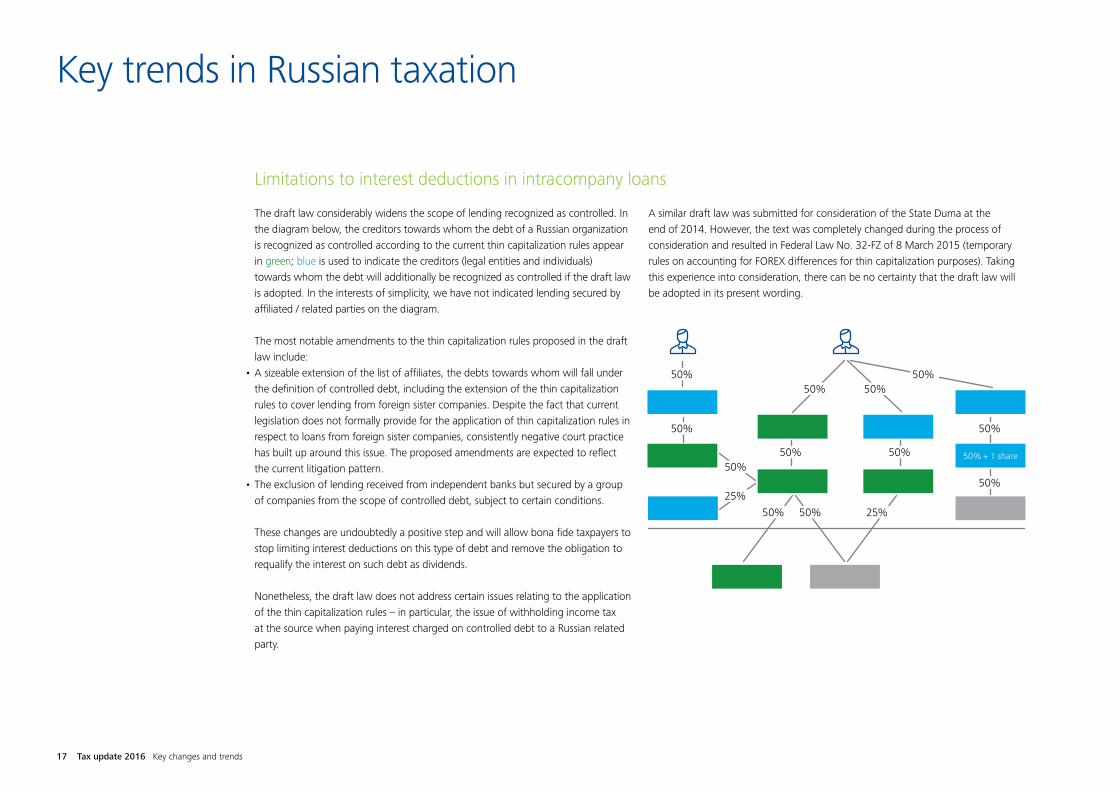

Limitations to interest deductions in intracompany loans

Debt towards a foreign affiliated party with an ownership share exceeding 20%

Debt towards a foreign related party:• With an ownership share in the Russian borrower exceeding 25%• With successive direct participation of each previous entity in each

following organization exceeding 50%

Debt towards a Russian parent / sister / subsidiary affiliated with the abovementioned foreign affiliated party

Debt towards a related party of a foreign related party

Debt secured by any of abovementioned affiliated partiesDebt secured by any of abovementioned related parties with the exception of debt towards independent banks (apart from back-to-back loans)

Key trends in Russian taxation

Tax update 2016 Key changes and trends16

The draft law considerably widens the scope of lending recognized as controlled. In the diagram below, the creditors towards whom the debt of a Russian organization is recognized as controlled according to the current thin capitalization rules appear in green; blue is used to indicate the creditors (legal entities and individuals) towards whom the debt will additionally be recognized as controlled if the draft law is adopted. In the interests of simplicity, we have not indicated lending secured by affiliated / related parties on the diagram.

The most notable amendments to the thin capitalization rules proposed in the draft law include:

• A sizeable extension of the list of affiliates, the debts towards whom will fall under the definition of controlled debt, including the extension of the thin capitalization rules to cover lending from foreign sister companies. Despite the fact that current legislation does not formally provide for the application of thin capitalization rules in respect to loans from foreign sister companies, consistently negative court practice has built up around this issue. The proposed amendments are expected to reflect the current litigation pattern.

• The exclusion of lending received from independent banks but secured by a group of companies from the scope of controlled debt, subject to certain conditions.

These changes are undoubtedly a positive step and will allow bona fide taxpayers to stop limiting interest deductions on this type of debt and remove the obligation to requalify the interest on such debt as dividends.

Nonetheless, the draft law does not address certain issues relating to the application of the thin capitalization rules – in particular, the issue of withholding income tax at the source when paying interest charged on controlled debt to a Russian related party.

A similar draft law was submitted for consideration of the State Duma at the end of 2014. However, the text was completely changed during the process of consideration and resulted in Federal Law No. 32-FZ of 8 March 2015 (temporary rules on accounting for FOREX differences for thin capitalization purposes). Taking this experience into consideration, there can be no certainty that the draft law will be adopted in its present wording.

50% + 1 share

50%50% 50%

50%

50%

50%

50%50%

50% 50% 25%

50%

50%

25%

Limitations to interest deductions in intracompany loans

Key trends in Russian taxation

Tax update 2016 Key changes and trends17

Controlled foreign companies

Eliminating gaps and ambiguitiesPlans call for the introduction of amendments to tax legislation in 2016 regarding the profits of controlled foreign companies (CFCs) and the income of foreign companies. The most significant changes may include:• Improvement of the rules for calculation of profits (losses) of CFCs• Improvement of the rules for calculation of ownership shares in CFCs• Improvement of the rules for recognizing entities or individuals as beneficiaries• Extension of the tax-free liquidation of CFCs until 1 January 2018

As part of the CFC strategy, the Federal Tax Service has developed a draft “List of States and Territories not Exchanging Tax Information with Russia” 36. The draft covers both typical offshore countries (such as the British Virgin Islands, the Seychelles, Belize, the Bahamas among others), and countries which entered the DTTs with Russia (e.g.: Austria, Great Britain, Switzerland among others).

Improvements to the exchange of financial information

Preparations for the automatic exchange of tax informationThe Russian Government reports the planned entry of Russia to agreements on tax information exchange. Following the ratification of the Convention on Mutual Assistance in Tax Matters and the Model Intergovernmental Agreement on Exchange of Information in Tax Matters for information exchange with offshore and low-tax jurisdictions, plans call for Russian legislation to be amended to introduce the automatic exchange of tax information about financial operations with foreign jurisdictions. This should allow for the planned accession to the multilateral agreement on the automatic exchange of financial information in 2018 as envisaged by the Unified Reporting Standard for financial operations developed by the OECD for taxation purposes, and the beginning of the exchange of such information.

Separately, plans call for the improvement of taxpayers’ access to information about Russian counterparties. To this end, a proposal has been made to extend the list of information not considered as tax secret. However, only the disclosure of information about taxpayer companies and information that is already published in corporate financial reporting is being considered. While rendering corporate financial reporting submitted to the tax authorities no longer a tax secret, the Government is also planning to exempt taxpayers from resubmitting such financial reporting to the statistical authorities. If these initiatives are put into effect, they will simplify the collection of information about bad faith counterparties and lower the number of disputes about the exercise of due diligence during counterparty selection.

Key trends in Russian taxation

Tax update 2016 Key changes and trends18

Extension of the DTT network Recently, a number of DTTs have been signed with Asian states that could positively impact investment strategies of Russian legal entities and individuals. In November 2015, Russia and Singapore signed a Protocol to amend the DTT between them. In December 2015, the Russian Government approved a draft DTT between the Russian Federation and Hong Kong. Double tax treaties enter into force after they are signed by the parties, ratified, and diplomatic notes are exchanged. In January 2016, the Russian Government has ratified the new DTT with China.

Focus on Asia

The new and amended DTTs open up new possibilities for both Russian and Asian investors. Together with the well-developed infrastructure and banking systems of Asian nations, and in light of the sanctions currently in place against Russia, these agreements should help Asian countries compete with popular European jurisdictions for Russian business

Key trends in Russian taxation

Tax update 2016 Key changes and trends19

Encouraging investment

New tax incentives The Russian Government has proposed a draft law offering 10% Profits tax rates for newly established Russian industrial enterprises (“green fields”). These incentives are planned to be applied upon claim procedure and selection similar to one applied for regional investment projects 37.

In addition, the Russian government proposes introducing a number of preferences for investors executing special investment contracts. Specifically, this will involve limitation of tax rates for regional and local taxes, as well as on the Profits tax rate at its level as per investment contracts until 2025 with an eye to stable tax burden for such investors. In addition to these guarantees, the draft law proposes opportunity to accelerate depreciation (with multiplying coefficient of 2) of fixed assets fitting in depreciation groups 1-7 and utilized for execution of a special investment contract.

These initiatives could be introduced already in 2016 and may be applied retrospectively, which would improve the position of investors.

Key trends in Russian taxation

Tax update 2016 Key changes and trends20

Cancelation of the requirements concerning bank guaranteesBecause of the substantial increase in the cost of bank guarantees, a proposal has been made to exempt large taxpayers from provision of bank guarantees required in order to apply excise duty exemptions. To define a large taxpayer, the same criteria noted in the Russian Tax Code in relation to VAT payers selling goods for export should apply 38.

Measures to support exporters

Changes to the procedure for justification of 0% VAT rate and claiming VAT on advances for recovery Plans also call for changing the procedure for recovering input VAT on operations subject to a 0% VAT. The recovery of VAT on goods (work, services and property rights) used during operations subject to a 0% VAT will take place according to the standard procedure outlined in relation to goods (work, services and property rights) subject to VAT at 10% and 18% rates. This will simplify the procedure for offsetting input VAT considerably and reduce the number of tax disputes 39.

Another positive change may affect all taxpayers using advances to pay for goods. A proposal has been made that the tax base for goods shipped (work or services performed) in advance upon receipt of a partial payment be determined as the remaining part of the value of the shipped goods (work or services performed) not settled by the purchaser before the shipment date. If the draft law is adopted, it will enter into force on 1 July 2016, but no earlier than one month from the day of its official publication and no earlier than the first day of the following VAT period 40.

Changes to the procedure of confirmation of taxpayers’ rights to 0% VAT will speed up the process of recovery of VAT from tax autohrities and positively impact cash flows

Key trends in Russian taxation

Tax update 2016 Key changes and trends21

VAT on electronic services

Harmonizing approachA draft law submitted to the Russian government for consideration would require foreign businesses supplying electronic services (e-services) to private customers in Russia to register for VAT purposes in Russia and charge VAT of 18%, and would abolish the VAT exemption for software licensing. The draft law was published on the government’s website on 28 December 2015 and has passed through the State Duma Committee on Budget and Taxation and is now awaiting discussion in the Duma. If the draft law is adopted, the changes would apply as from 1 January 2017.The draft law has similarities to the EU rules on the supply of electronic services by non-EU providers, as well as to recent rules introduced in Korea and South Africa and proposed rules in Australia and New Zealand; its approach also has been endorsed by the OECD under the base erosion and profit shifting (BEPS) project.The draft legislation contains a definition of e-services and lists e-services that potentially would fall within the scope of Russian VAT; makes changes to the place of supply rules; and introduces registration and other compliance obligations on foreign businesses where such services are provided to private customers. The draft law also seeks to abolish the current VAT exemption for the licensing of software and databases and would introduce an income tax preference that would allow Russian information technology (IT) companies to reduce their income tax base by up to 80% 41.

Key trends in Russian taxation

Tax update 2016 Key changes and trends22

Super income tax for the oil industry

Additional tax burdenThe Russian Ministry of Finance announced an initiative to introduce a new tax for enterprises in the oil sector – the Super income tax. It is expected that the tax rate will be set at 70%, and that the tax base will consist of estimated income (based on prices, rather than actual income) with deductions available for operational costs during extraction, capital expenditures, estimated expenses on transport, mineral extraction tax and duties. However, the Ministry proposes limiting deductible expenses to no more than USD 20 per barrel. According to the Ministry’s proposals, the Super income tax will apply after the internal rate of return reaches 6%. A corresponding draft law on the introduction of the Super income tax has not yet been officially published. Please note that an alternative draft law proposing the introduction of a special taxation regime based providing for calculation of Profits tax based on profits from sales of extracted oil is currently under consideration in the Russian State Duma.

Key trends in Russian taxation

Liability for non-settlement of mandatory social contributions

Potential introduction of criminal liabilityA draft law has been introduced in the State Duma that would introduce criminal liability for large-scale (from RUB 600,000) and extra large-scale (from RUB 3 million) non-settlements of mandatory social insurance contributions 42.

Tax update 2016 Key changes and trends23

Links

Tax update 2016 Key changes and trends24

Federal Law No. 395-FZ of 28 December 2010

Federal Law dated 29 December 2015 #396-FZ

Federal Law No. 420-FZ of 28 December 2013

Federal Law No. 214-FZ of 13 July 2015

Federal Law No. 321-FZ of 23 November 2015

Federal Law No. 110-FZ of 2 May 2015

Federal Law No. 32-FZ of 8 March 2015

Federal Law dated 29 December 2015 #386-FZ

Federal Law No. 150-FZ of 8 June 2015

Federal Law No. 328-FZ of 28 November 2015

Federal Law No. 326-FZ of 28 November 2015

Federal Law No. 325-FZ of 28 November 2015

Key areas for development of tax legislation during 2016 – 2018

Federal Law No. 458-FZ of 29 December 2014

Federal Law No. 401 of 29 December 2015

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

Federal Law No. 382-FZ of 29 November 2014

Federal Law No. 396 of 29 December 2015

Federal Law No. 146-FZ of 8 June 2015

Federal Law No. 150-FZ of 8 June 2015

Federal Law No. 146-FZ of 8 June 2015

Federal Law No. 113-FZ of 2 May 2015

Federal Law No. 326-FZ of 28 November 2015

Federal Law No. 320-FZ of 23 November 2015

Federal Law No. 327-FZ of 28 November 2015

Federal Law No. 320-FZ of 23 November 2015

Federal Law No. 85-FZ of 6 April 2015

Federal Law No. 113-FZ of 2 May 2015

Federal Law No. 397 of 29 December 2015

Federal Law No. 386 of 29 December 2015

Russian Government Resolution No. 126 of 14 February 2015; No. 617 of 24 June 2015; No. 716 of 17 July 2015; No. 931 of 3 September 2015

Links

Tax update 2016 Key changes and trends25

Russian Government Resolution No. 1042 of 30 September 2015

Federal Law No. 319-FZ of 23 November 2015

The Decree of the President dated 15 January 2016

Federal Law dated 30 December 2015 #424-FZ

Draft law No. 724609-6 “On the Introduction of Amendments to Article 269, Part Two of the Russian Tax Code” adopted at its third reading on 29 January 2016

Draft List of States and Territories Not Exchanging Tax Information with the Russian Federation

Draft law No. 801288-6 “On the Introduction of Amendments to the Russian Tax Code”

Key areas for development of tax legislation during 2016 – 2018

Draft law No. 730216-6 “On the Introduction of Amendments to Articles 165 and 172 of the Russian Tax Code”

Draft law No. 02/04/08-15/00038680 prepared by the Russian Ministry of Finance

Draft Federal Law #962487-6

Draft law No. 927133-6

31

32

33

34

35

36

37

38

39

40

41

42

Subscribe to Deloitte periodicals

Stay up to date with tax news by subscribing to our publications Tax Smart – our mobile app, on which you can find news, surveys, opinions of Deloitte specialists on key Russian and international tax issues, and reviews of the most important court decisions. This app also contains a calendar of Deloitte events and the contact details of our industry group leaders. TaxSmart makes it easier to keep up-to-date with events in the world of taxation.

We also hold live and webcast client events dedicated to key taxation news. Subscribe to our newsletter to receive invitations to these events.

Legislative Tracking – a daily review of legislative changes.Legislative Tracking in Focus – weekly reviews each of which is dedicated to key events in the world of taxation and law.R&D News – reviews of changes in regional and federal law relating to state support for investment activities in Russia.

Tax update 2016 Key changes and trends26

Contacts

BU Leaders

Corporate Tax

Grigory Pavlotsky

Managing partner

Indirect Tax

Oleg Berezin

Partner

Government Relations

Gennady Kamyshnikov

Partner

Business Process Solutions (BPS)

Pavel Balashov

Partner

Technology & Processes

in Tax and Accounting (TPTA)

Kazbek Dzalaev

Director

Global Financial Services

Industry (FSI)

Vladimir Elizarov

Partner

International Tax

Elena Solovyova

Partner

Global Employer Services (GES)

Tatiana Kiseliova

Partner

Private Client Services

Svetlana Meyer

Partner

Legal Services

Raisa Alexakhina

Partner

Transfer pricing (TP)

Dmitry Kulakov

Partner

R&D and Government

Incentives

Vasily Markov

Director

Tax update 2016 Key changes and trends27

Contacts

Tax & Legal Industry Leaders

Travel, Hospitality & Leisure

Artem Vasyutin

Partner

Automotive

Tatiana Kofanova

Director

Banking & Securities,Insurance

Alexander Sinitsyn

Director

Technology, Media

& Telecommunications

Vladimir Yumashev

Director

Industrial Products, Metals

and processing

Yulia Orlova

Partner

Consumer products, Food,

Beverages & Agriculture

Oxana Zhupina

Director

Real Estate

Yulia Krylova

Director

Retail, wholesale & distribution

Artem Vasyutin

Partner

Health Care & Life Sciences

Oleg Berezin

Partner

Energy & Resources

Andrey Panin

Partner

Tax update 2016 Key changes and trends28

deloitte.ruAbout Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a more detailed description of DTTL and its member firms. Please see www.deloitte.ru/en/about for a detailed description of the legal structure of Deloitte CIS.

Deloitte provides audit, tax, consulting, and financial advisory services to public and private clients spanning multiple industries. With a globally connected network of member firms in more than 150 countries and territories, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address their most complex business challenges. Deloitte’s more than 225,000 professionals are committed to becoming the standard of excellence.

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte Network”) is, by means of this communication, rendering professional advice or services. No entity in the Deloitte network shall be responsible for any loss whatsoever sustained by any person who relies on this communication. © 2016 Deloitte & Touche Regional Consulting Services Limited. All rights reserved.