tax reform for michigan robert j. kleine state treasurer community college business officials...

TRANSCRIPT

Tax Reform For Michigan

Robert J. Kleine

State Treasurer

Community College Business Officials Association

November 2, 2006

2

Economic and Revenue Forecasting Division, Michigan Department of Treasury

Michigan Still Dependent on Autos

7.88

1.02 0.82 0.55 0.78 0.92 0.96

Autos andParts

Mfg. exc.Autos &

Parts

Finance +Insurance

Nat,resources,

mining

Tourist-oriented

Knowledge-based

All Other

Location Quotient in Michigan(Percentage of Michigan Employment over Percentage U.S.)

Source: George Fulton, University of Michigan, except finance + Insurance calculated by Deptof Treasury.

3

Economic and Revenue Forecasting Division, Michigan Department of Treasury

Michigan Employment by Sector

-289.9

66.3

-77.3

9.1

-8.0-48.3

-217.9

Total Ed &HealthServ.

TradeTrans &

Util.

Fin. Act. Gov. Prof Serv. Mfg.

Tho

usan

ds o

f Jo

bs

Employment Change From 2000 to 2005

Source: Bureau of Labor Statistics.

Note: Detail does not add to total because not all sectors of employment are presented.

4

Economic and Revenue Forecasting Division, Michigan Department of Treasury

Michigan Manufacturing Employment

500

600

700

800

900

1,000

1990 1992 1994 1996 1998 2000 2002 2004 2006

Mon

thly

Em

ploy

men

t (1

000s

)

Source: Bureau of Labor Statistics.

Sep 2006643,600

Jan 1992775,900

Jul 1999908,200

5

Economic and Revenue Forecasting Division, Michigan Department of Treasury

Big 3 Losing Market Share

12.913.9

15.114.8 15.115.215.617.0 17.417.216.8 16.616.916.9

02468

101214161820

1992 1995 1998 2001 2004

Mil

lion

s of

Uni

ts

40%

45%

50%

55%

60%

65%

70%

75%

U.S. Light Vehicle Sales Big 3 Share

Source: Automotive News.

6

Economic and Revenue Forecasting Division, Michigan Department of Treasury

Big Three Still Produce in Michigan

Pct Point1995 2005 Diff

GM 31.0% 28.5% -2.5%

Ford 22.4% 26.7% 4.4%

Chrysler 40.8% 42.8% 2.0%

MI Big 3 % of U.S. 29.7% 30.8% 1.1%

Michigan Big 3 Production as a Percent of Total U.S. Production

7

Economic and Revenue Forecasting Division, Michigan Department of Treasury

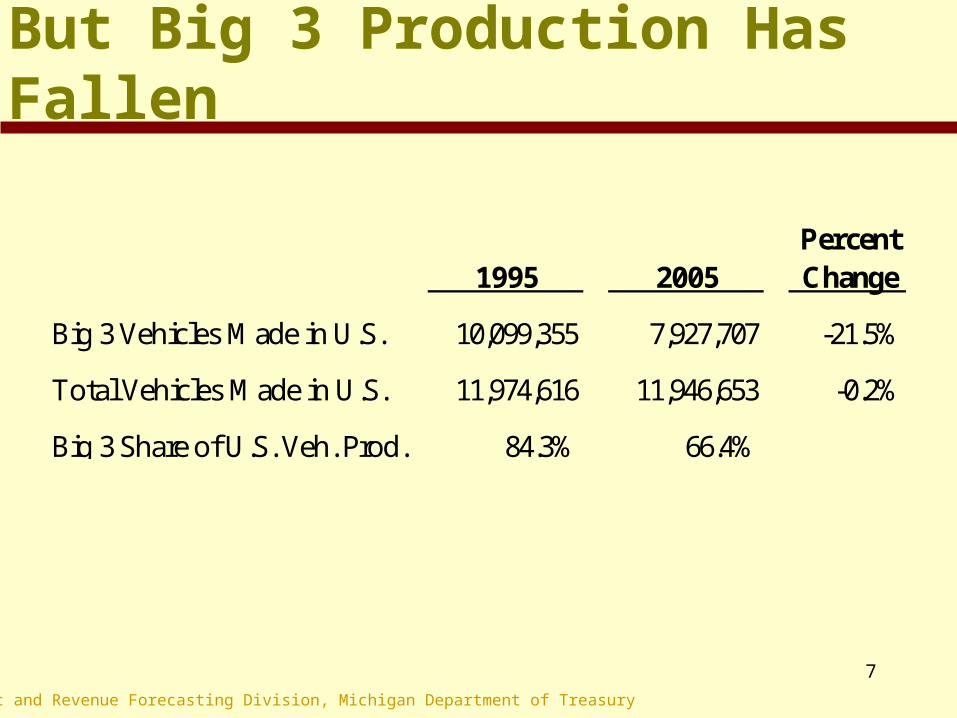

But Big 3 Production Has Fallen

Percent1995 2005 Change

Big 3 Vehicles Made in U.S. 10,099,355 7,927,707 -21.5%

Total Vehicles Made in U.S. 11,974,616 11,946,653 -0.2%

Big 3 Share of U.S. Veh. Prod. 84.3% 66.4%

8

Economic and Revenue Forecasting Division, Michigan Department of Treasury

999

732760

550

650

750

850

950

1,050

1990 1992 1993 1995 1996 1998 1999 2001 2002 2004 2005

12 M

onth

Mov

ing

Ave

rage

Big 3 Light Vehicle Sales

Source: Wards Automotive.

Sales Have Fallen Nearly 24 Percent Since Mid 2000

9

Economic and Revenue Forecasting Division, Michigan Department of Treasury

Slow Michigan Employment Due to Autos

-1.5%-1.0%-0.5%0.0%0.5%1.0%1.5%2.0%2.5%

Michigan annualemploymentgrowth rate,1990-2000

U.S. annualemploymentgrowth rate,1990-2000

Michigan annualemploymentgrowth rate,2000-2005

U.S. annualemploymentgrowth rate,2000-2005

hypotheticalMichigan

growth, 2000-2005, withbetter auto

industryperformance

Source: Michigan Economic Competitiveness and Public Policy, Upjohn Institute 2006.

10

Economic and Revenue Forecasting Division, Michigan Department of Treasury

Michigan Private Sector Employment% of

Michigan Employment

Number of Jobs 8/03 to 8/06

Increasing Sectors

Education & Health 15.3% 30,500

Professional & Business Services 15.9% 20,600

Leisure & Hospitality 10.9% 12,500

Other Private Super Sectors 19.6% 6,500

Total 61.7% 70,100

Decreasing Sectors

Manufacturing 18.3% -70,800

Wholesale/Retail Trade 18.2% -28,400

Other Private Super Sectors 1.8% -2,900

Total 38.3% -102,100Government lost 18,800 jobs from 8/03 to 8/06 and is 15.4% of total wage & salary employment.

11

Economic and Revenue Forecasting Division, Michigan Department of Treasury

-25.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Jan-9

9

Apr-9

9

Jul-9

9

Oct-9

9

Jan-0

0

Apr-0

0

Jul-0

0

Oct-0

0

Jan-0

1

Apr-0

1

Jul-0

1

Oct-0

1

Jan-0

2

Apr-0

2

Jul-0

2

Oct-0

2

Jan-0

3

Apr-0

3

Jul-0

3

Oct-0

3

Jan-0

4

Apr-0

4

Jul-0

4

Oct-0

4

Jan-0

5

Apr-0

5

Jul-0

5

Oct-0

5

Jan-0

6

Apr-0

6

Jul-0

6

Veh

icle

Pro

duct

ion

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

Wit

hhol

ding

Gro

wth

6 Month Vehicle Production 6 Month Withholding

Withholding Still Correlated with Michigan Auto Production

Through September 2006

12

Economic and Revenue Forecasting Division, Michigan Department of Treasury

Michigan Income Growth Trails U.S.

80

100

120

140

160

180

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

US Michigan

U.S. and Michigan Personal Income Growth1995 = 100

Source: U.S Bureau of Economic Analysis.

13

Economic and Revenue Forecasting Division, Michigan Department of Treasury

Problems with Current System

• High personal property tax burden discourages investment in Michigan

• SBT has been made more complicated through the years

• SBT’s bad reputation may be discouraging investment in Michigan

14

Economic and Revenue Forecasting Division, Michigan Department of Treasury

Advantages of SBT

• Stability• Rate or base has never been increased• Familiarity (30 years of experience)• Low rate lessens interference with economic

decisions and does not penalize efficient companies – the tax is about 0.6 percent of private GSP

• Taxes all economic factors equally

15

Economic and Revenue Forecasting Division, Michigan Department of Treasury

SBT Falling as Share of GSP

0.0%

0.5%

1.0%

1.5%

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

SBT as Percent of Private Gross State Product

16

Economic and Revenue Forecasting Division, Michigan Department of Treasury

COST Study Puts Michigan BusinessTaxes Below National Average

4.3% 4.8%

Michigan U.S. Average

Source: Council on State Taxation. Bureau of Economic Analysis.

FY 2005 State and Local Business Taxes as a Percent of Gross State Product

17

Economic and Revenue Forecasting Division, Michigan Department of Treasury

Michigan Business Burden Compares Well with Neighbors

StateBusiness Tax as %

of GSP Rank

Wyoming 9.6% 1

Illinois 5.3% 19

Minnesota 4.9% 23

Ohio 4.7% 27

Indiana 4.5% 30

Wisconsin 4.4% 33

MichiganDE, NC, VA

4.3%3.7%

3648

Source: Council on State Taxation.

18

Economic and Revenue Forecasting Division, Michigan Department of Treasury

Upjohn Study Finds Michigan Taxes Below U.S. Average

-5.0%

-12.0%

-19.0%

S & L Taxes Per Dollar PersonalIncome

S & L Business Taxes Per Dollar ofPrivate GSP

S & L Business Taxes onInvestment in New Business Facility

Source: Michigan Economic Competitiveness and Public Policy, Upjohn Institute 2006.

19

Economic and Revenue Forecasting Division, Michigan Department of Treasury

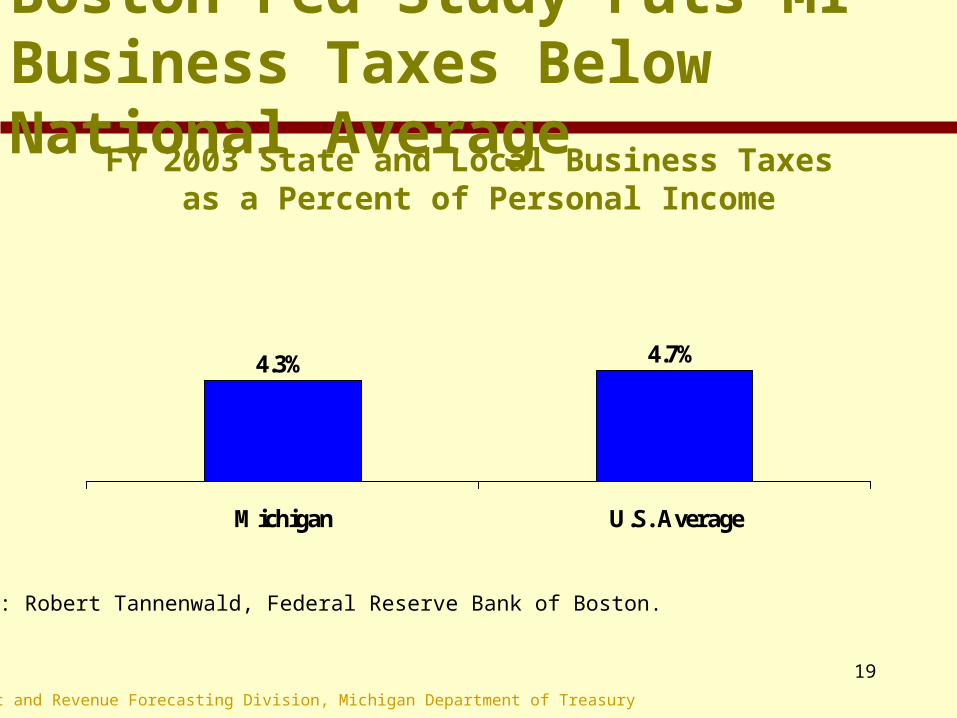

Boston Fed Study Puts MI Business Taxes Below National Average

4.3% 4.7%

Michigan U.S. Average

Source: Robert Tannenwald, Federal Reserve Bank of Boston.

FY 2003 State and Local Business Taxes as a Percent of Personal Income

20

Economic and Revenue Forecasting Division, Michigan Department of Treasury

Governor’s Criteria for Reform

• Broaden tax base and lower tax rate

• Do not raise taxes on individuals

• Fully replace revenues to protect healthcare, education, and public safety

• Simplify business taxes

• Some consideration of ability to pay

21

Economic and Revenue Forecasting Division, Michigan Department of Treasury

Other Criteria for High Quality Business Tax System

• Stable revenue source

• Low compliance costs

• Competitive tax rates with other states

22

Economic and Revenue Forecasting Division, Michigan Department of Treasury

Alternative Business Taxes

• Subtractive VAT

• Gross receipts

• Licensing Fee

• Franchise

• Income

• Business-to-business services

• Other: Texas reforms, factor tax, MJIA

23

Economic and Revenue Forecasting Division, Michigan Department of Treasury

Michigan Jobs and Investment Act

• Broader tax base and lower rate– Eliminate excess compensation reduction– Eliminate gross receipts reduction– Lower rate by more than 1/3 to 1.2%

• 35% refundable manufacturing personal property tax credit• 35% R&D personal property tax credit• Change to 100% sales factor• Increased profits weighting• Raise insurance tax to national median (2% of premiums)• Overall plan revenue neutral

In 2005, the Governor Proposed the Michigan Jobs and Investment Act

24

Economic and Revenue Forecasting Division, Michigan Department of Treasury

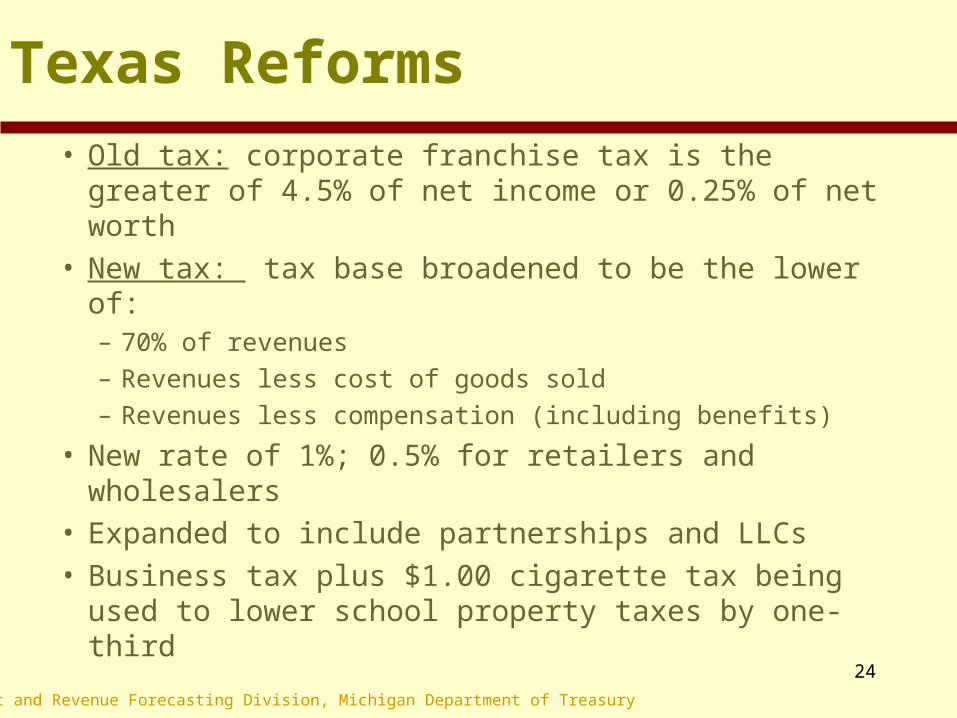

Texas Reforms

• Old tax: corporate franchise tax is the greater of 4.5% of net income or 0.25% of net worth

• New tax: tax base broadened to be the lower of:– 70% of revenues

– Revenues less cost of goods sold

– Revenues less compensation (including benefits)

• New rate of 1%; 0.5% for retailers and wholesalers• Expanded to include partnerships and LLCs• Business tax plus $1.00 cigarette tax being used to

lower school property taxes by one-third

25

Economic and Revenue Forecasting Division, Michigan Department of Treasury

Ohio Reforms

• Old tax: corporate franchise tax is the greater of 4 mills on net worth or 8.5% of income in excess of $50,000

• New tax: Commercial Activities Tax– Tax base is gross receipts of a business or individual

sourced to Ohio

– Tax rate is 0.26 percent (5 year phase-in)

• Tangible personal property tax eliminated• Personal income tax reduced

– Top bracket reduced from 7.5% to 5.95%

– Taxpayers with income under $10,000 exempt

26

Economic and Revenue Forecasting Division, Michigan Department of Treasury

MI Chamber of Commerce Proposal (1)

• Combination income and gross receipts• Business income tax rate 3.05%• “License tax” paid on gross receipts

– 0.48% general rate– 0.24% on wholesale/retail– Paid on excess above $350k in gross receipts– $150 minimum tax on businesses with at least 1

employee– $2 million cap on license tax

• 50% personal property tax credit

27

Economic and Revenue Forecasting Division, Michigan Department of Treasury

MI Chamber of Commerce Proposal (2)

• Combination income and gross receipts• Business income tax rate 1.5%• “License tax” paid on gross receipts

– 0.24% general rate– 0.18% on wholesale/retail– Paid on excess above $350k in gross receipts– $150 minimum tax on businesses with at least 1

employee– $2 million cap on license tax

• No personal property tax credit

28

Economic and Revenue Forecasting Division, Michigan Department of Treasury

GR Chamber of Commerce Proposal

• Tax on MI business activity– MI sales or service revenues, less cost of tangible personal

property purchased for resale, manufacturing, leasing, or cost of funds for financial institutions

• Also replaces personal property tax• Rate not to exceed 0.75%• If tax exceeds estimates, credit in following year (e.g.

Oregon)• Flat fee of $150 for business with at least 1 employee

29

Economic and Revenue Forecasting Division, Michigan Department of Treasury

Detroit Chamber Proposal

• Annual business license “fee” based on sales

• Fee based on sales level.

• Fee ranges from $1,000 to $1,000,000.

• Effective rate varies from about 0.2 percent to 0.5 percent

• Maximum tax set at $1,000,000

30

Economic and Revenue Forecasting Division, Michigan Department of Treasury

Factor Tax Proposal

• Tax Base can include– a measure of gross receipts or sales– compensation – assets or property– Business income times 10

• Low tax rate (below 0.2 percent)

• Broad base provides stability

• Inclusion of business income makes tax more sensitive to profitability

31

Economic and Revenue Forecasting Division, Michigan Department of Treasury

Replacement Tax Issues

• Winners and losers

• How much revenue should be replaced

• Minimum tax?

• Ability to pay

• Personal property tax relief

• Filing threshold

• Capital and human investment incentives

32

Economic and Revenue Forecasting Division, Michigan Department of Treasury

SBT Provides One Quarter of GF-GP Revenue

May 06 Consensus EstimateAdjusted for Proposed Budget

FY 2007 GF-GP Revenues Total $9.2 billion

33

Economic and Revenue Forecasting Division, Michigan Department of Treasury

$8,697 $8,533$8,844

$9,503 $9,788

$8,990$8,427

$7,959 $8,042 $8,309 $8,282 $8,435

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007May 2006 Estimates

Note: Totals exclude transfers and savings from adjusting statutory revenue sharing payments to local governments.

$ in Millions

Nominal General Fund Net Revenue in 2007 Less Than in 1996

34

Economic and Revenue Forecasting Division, Michigan Department of Treasury

Inflation Adjusted GF-GP RevenueDown 28 Percent Since FY 1999

Totals Exclude Transfers and are adjusted to 2007 dollars using U.S. CPI-U.

$6.0

$7.0

$8.0

$9.0

$10.0

$11.0

$12.0

$13.0

1999 2000 2001 2002 2003 2004 2005 2006 2007

Bil

lion

s of

200

7 $

$11.8 billion

$8.4 billion

35

Economic and Revenue Forecasting Division, Michigan Department of Treasury

Replacement Tax Issues

• Winners and losers

• How much revenue should be replaced

• Minimum tax?

• Ability to pay

• Personal property tax relief

• Filing threshold

• Capital and human investment incentives

36

Economic and Revenue Forecasting Division, Michigan Department of Treasury

Comparison: Michigan SBT vs. CIT

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001

Mil

lion

s CIT revenues at 7.2% rate

SBT Revenue at 1.9% Rate

Michigan SBT vs. Business Income Tax

SBT Revenues Paid by Corporations

37

Economic and Revenue Forecasting Division, Michigan Department of Treasury

Replacement Tax Issues

• Winners and losers

• How much revenue should be replaced

• Minimum tax?

• Ability to pay

• Personal property tax relief

• Filing threshold

• Capital and human investment incentives

38

Economic and Revenue Forecasting Division, Michigan Department of Treasury

Options for Personal Property Tax Relief

• Tax credits – if too large could result in classification change from real to personal

• Exemption from 24 school mills (6 state and 18 local school) delivers nearly 50 percent relief

• Exempt new property

• Differential credits based on new or existing

• Mandatory PA 198 for new

• Any change to personal property tax must take into account effects on local government