tax planning guide

DESCRIPTION

Tax Planning guideTRANSCRIPT

www.PersonalFN.com

2

Preface

All of us engage in some economic activity and work hard to make a living. But as you start

doing so you tend to attract the attention of the Income Tax Department, as they too are doing

their task of taxing your income, as you earn. And thus as we work hard to make a living, it

becomes imperative for us to work a little more harder and smarter to save our taxes (the legal

way) too, so that it can help us make our dreams come true - A dream of buying a better car,

bigger house etc.

But, remember in the quest of attaining the same, if you keep your tax planning exercise

pending till the eleventh hour, then it would be merely a “tax saving” exercise leading to sub-

optimal gains.

The last union budget which was expected to be stricter on austerity, turned out to be a

populous one. Instead of expenditure cuts, the government emphasised on raising revenues.

Due to this, there were fewer new tax benefits provided to taxpayers. So this requires you to be

even more particular about tax planning.

This guide on Tax Planning has been written with the purpose of helping you plan your taxes

smartly. If one incorporates the financial planning aspects such as your age, income, ability to

take risk and financial goals to tax planning exercise, then one can wisely complement tax

planning to investment planning as well.

Also, realisation will dawn on you that there’s more to tax planning than the mere Rs 1 lakh

limit under Section 80C, of the Income Tax Act, 1961. There are many other provisions that can

provide you tax benefits. A simple thing like taking a loan for buying a house can make you

eligible to get tax benefits.

So, read on and wish you all VERY HAPPY TAX PLANNING!!

Team Personal FN

www.PersonalFN.com

3

Disclaimer

Quantum Information Services Private Limited (PersonalFN) is enrolled as AMFI Registered Mutual Fund Advisor (ARMFA) under

AMFI Registration No. ARN- 1022 and adheres to AMFI Guidelines and Norms for Intermediaries (AGNI), and all its employees

engaged in distribution of Mutual Fund products have passed the prescribed AMFI certification examination. This is a

generalized Service, provided on an "As Is" basis by PersonalFN. PersonalFN and its affiliates disclaim any warranty of any kind,

imputed by the laws of any jurisdiction whether in or outside India, whether express or implied, as to any matter whatsoever

relating to the Service, including without limitation the implied warranties of merchantability, fitness for a particular purpose.

PersonalFN will and its subsidiaries / affiliates / sponsors / trustee or their officers, employees, personnel, directors will not be

responsible for any direct/indirect loss or liability incurred to the user or any other person as a consequence of his or any other

person on his behalf taking any investment decisions based on the above recommendation. This is not a specific advisory

service to meet the requirements of a specific client. Use of the Service is at any persons, including a Client's, own risk. The

investments discussed or recommended under this service may not be suitable for all investors. Investors must make their own

investment decisions based on their specific investment objectives and financial position and using such independent advisors

as they believe necessary. Information herein is believed to be reliable but PersonalFN does not warrant its completeness or

accuracy. The Service should not be construed to be an advertisement for solicitation for buying or selling of any securities. All

intellectual property rights emerging from this guide are and shall remain with PersonalFN. This guide is for user’s personal use

and the user shall not resell, copy, or redistribute this guide, or use it for any commercial purpose. Please read the Terms of Use

on the website www.personalfn.com.

An Invitation to Join 'Money Simplified' Course PersonalFN and Franklin Templeton Mutual Fund presents 'Money Simplified Your Guide to Money & Mutual Funds' course. An investor education initiative that would act as a one-stop resource for all your investment related needs... ...and ultimately guide you in planning your finances, so that all your life's goals can be achieved. Click Here to Sign Up Now... It's Absolutely Free!

www.PersonalFN.com

4

Index

Section I: Introduction

Tax Saving Vs. Tax Planning 05

Section II: Mistakes which you have been doing while saving tax 06

Section III: Your small steps (to “Tax Planning”) can take you leaps

Steps to “tax planning” 09

Parameters for prudent tax planning 12

Section IV: Optimal tax planning with section 80C 17

Tax planning with market-linked instruments 18

Tax planning the assured return way 23

Section V: Thinking beyond section 80C 30

Section VI: Your home loan and tax planning 38

Section VII: House Property and taxes 43

Section VIII: Save tax on your hard earned salary 47

Section IX: Conclusion 52

www.PersonalFN.com

5

I - Introduction

“All men make mistakes, but only wise men learn from their mistakes.”- Sir Winston Churchill.

The above proverb is very much relevant to our daily lives - be it handling finances or even in

any other facets of life.

Moreover the famous author John C. Maxwell has also quoted “A man must be big enough to

admit his mistakes, smart enough to profit from them, and strong enough to correct them.” But

again this is conveniently forgotten by most, which often leads to failure to learn from

mistakes, the arrogance to admit it and which thus leads you to repeat the same mistakes

again.

While undertaking your tax planning exercise too, you tend to repeat the same mistake of

waiting till the eleventh hour and are arrogant enough to admit it.

As the financial year draws to a close, we all start feeling the heat and realise that yes, now we

have to invest in order to save tax. But have you ever wondered whether it is the prudent way

for tax planning?

Remember, waiting till the eleventh hour to undertake your tax planning exercise will often

drive it towards mere “tax saving” rather than “tax planning”; which in our opinion is a sub-

optimal way to undertake a tax planning exercise.

Unlike “tax saving” which is generally done through investments in tax saving

instruments/products, under “tax planning” we take into consideration one’s larger financial

plan after accounting for one’s age, financial goals, ability to take risk and investment horizon

(including nearness to financial goals). And by adapting to such a method of “tax planning”, you

not only ensure long-term wealth creation but also protection of capital.

Hence, please remember to commence your “tax planning” exercise well in advance by

complementing it with your overall investment planning exercise.

www.PersonalFN.com

6

II - Mistakes which you have been doing while saving tax

We recognise the fact that many of you are too busy throughout the year, in your economic

activities intended to make a living. But if you show the same dedication in your tax planning

exercise, the same will enable you to save more and fulfil all your dreams in life. Our experience

reveals following 4 mistakes which individuals do while saving taxes.

1. Doing your tax planning at the last moment:

The root of all mistakes in tax planning lies in waiting till the last minute to save taxes, which

eventually leads to mere tax saving, rather than tax planning. And this in return is a sub-optimal

way of saving taxes, caused by the sheer attitude of delay. Your last moment hurry, will often

lead you to forgetting or ignoring the facets of financial planning such as your age, income,

ability to take risk and financial goals (explained further in this guide) thus guiding you to not

complement your tax planning exercise with investment planning.

Remember waiting till the eleventh hour, is just going to lead you to a path of sub-optimal tax planning

exercise, which would destroy the essence of holistic tax planning.

2. Unnecessarily Buying Endowment and Unit Linked Insurance Plans:

At the end of the financial year, many of you might have attended telephone calls of insurance

agents pestering you to buy an investment cum insurance plan – typically market linked i.e.

Unit Linked Insurance Plans (ULIPs) or some kind of Endowment plans. And many of you

realising the need to save your taxes, even entertain these calls and eventually tear a cheque

for buying one. But do you ever wonder whether you have done the right thing?

www.PersonalFN.com

7

The answer in our opinion is a sheer “No”. And that’s because of the ignorance and / or

arrogance (of not admitting your mistakes) which you have, while doing your tax saving

investments.

Remember when you think of insuring yourself, it should purely mean protecting your life against any

contingent events; and thus given that you should be ideally buying only pure term life insurance plans,

which gives due importance to your human life value. It is noteworthy that ULIPs are investment-cum-

insurance plans where for the premium paid, the insurance cover offered under these plans is far less

(usually 10 times of your annual premium) when compared to pure term life insurance plans; where for a

lesser premium amount you get a greater life cover – which precisely what a life insurance plan is

intended for.

3. Ignoring power of compounding through tax saving mutual funds:

Many of you despite the fact that age, income, ability to take risk along with financial goals

support you to take risk, you absolutely rule out the concept of power of compounding to your

portfolio. It is noteworthy that if you want to meet and / or elevate your standard of living

going forward, you need to beat the rate of inflation. And thus, role of equity as an asset class

cannot be ignored in one’s tax saving portfolio too. While some do consider the tax saving

mutual funds in their tax saving portfolio the ideal composition (depending on your age, income

ability to take risk and financial goals) is not maintained, which leads the tax saving portfolio to

give sub-optimal returns.

It is noteworthy that being risk averse is well appreciated by us. But if your age, income, ability to take

risk and financial goals, permit you to take equity exposure one should not ignore the same.

www.PersonalFN.com

8

4. Not optimizing all options for tax saving:

For many tax planning starts as well as ends with Section 80C - which enunciates investment

instruments for tax saving. But investing only in these investment instruments would not lead

to optimal reduction of your tax liability.

To bring to your notice our Income Tax Act, 1961 also considers humane side of our life and also gives

deduction for contributions you make on such developments. So, in case if you pay your medical

insurance premium, incur expenditure on the medical treatment of a “dependant” handicapped, donate

to specified funds for specified causes, contribute in monetary form to political parties or electoral trusts,

take a loan for pursuing higher education or if you are an individual suffering from “specified” diseases,

then all this too can help you effectively plan your tax obligations, thus optimally reducing your tax

liability. Moreover, taking into account the urge to buy your dream home by taking a loan, the Act also

extends tax saving benefits to you.

www.PersonalFN.com

9

III - Your small steps can take you forward by leaps

There is an old Chinese proverb which says, “It is better to take many small steps in the right

direction than to make a great leap forward only to stumble backward.” which in our opinion

applies even to your “tax planning” exercise.

Remember, it is vital for you to step-by-step ascertain where you stand, in terms of your Gross

Total Income and Net Taxable Income, so that you effectively undertake your tax planning

exercise which in turn would deliver you the objective of long-term wealth creation along with

capital protection.

In the past if you have taken your tax planning decisions at the last moment, never mind. But,

please learn from them and don’t repeat the same mistakes again. Adopt the prudent steps

while doing your tax planning.

Steps to “tax planning”:

Step 1: Compute the Gross Total Income

The process of tax planning begins with computation of your Gross Total Income (GTI). This step

enables you to ascertain the total income earned by you during a financial year, from various

under-mentioned sources of income, and helps you to judge where you stand.

Income from salary

Income from house property

Profits and gains from business & profession

Capital gains (short term and long term) and

Income from other sources.

Hence, GTI is the total income earned by one before availing any deductions under the Income

Tax Act, 1961. And it is vital to know the same, in order for you to undertake your tax planning

effectively, so that you can plan within the sources of income (by using the relevant provisions

www.PersonalFN.com

10

of the Income Tax Act applicable to the aforementioned sources of income), as well as by

availing deductions to GTI.

Now, one may ask – “how do I undertake this activity if I’m a novice?”

Well, the answer is pretty simple! You can either get it done at your company (many

organisation do offer this facility), ask your CA / tax consultant to do it, or use the convenience

of the new and updated tax portals that have emerged in more recent times. But, along with all

this please do not forget to do your self-study to carry out effective tax planning exercise. One

must note that it is vital to know at least those provisions of the Income Tax Act, which directly

have an impact on your finances.

Step 2: Compute the Net Taxable Income

After having done with computation of GTI by using the relevant provisions of the Income Tax

Act for each source of income, the next step is to compute your Net Taxable Income (NTI).

Under NTI from the GTI, the various deductions allowed under the Income Tax Act, should be

accounted for (i.e. subtracted from your GTI), which would thus reduce your taxable income.

These deductions enable you to enjoy reduction in tax liability, as it covers Sections under the

Income Tax Act for:

Investing in tax saving instruments (your most loved and sought after Section 80C, along

with the recently introduced RGESS - Rajiv Gandhi Equity Savings Scheme)

Donations

Expenditure on handicapped dependent

Premium payment for your medical insurance

Interest paid on loan taken for higher education

Rent paid for residential accommodation

Expenditure incurred on a specified diseases suffered by you

Remember, if you use the respective provisions effectively to do tax planning, it will enable you

to achieve the long-term objective of wealth creation.

www.PersonalFN.com

11

Step 3: Calculate the tax payable

After having effectively saved tax in the prudent way mentioned above, the next step is to

compute your tax liability based on the present income tax slabs, and thereafter file your tax

returns.

The income tax rates for Individuals and HUFs for FY 2013-14 are as follows:

Net Taxable Income (in Rs) Rate

Upto Rs 2,00,000 (for general tax payers – male and female)

Nil Upto Rs 2,50,000 (for senior citizens) Upto Rs 5,00,000 (for very senior citizens aged 80 and above)

Rs 2,00,001 to Rs 5,00,000 # 10%

Rs 5,00,001 to Rs 10,00,000 20%

Above Rs 10,00,000 30% A Tax Credit or Special Rebate of Rs 2,000 is allowed for individuals whose Taxable

Income is below Rs 5 lakhs

Source: Finance Act 2013, Personal FN Research)

# For senior citizens (aged above 60 but below 80), with NTI falling between Rs 2,50,001 to Rs

5,00,000 will be taxable @ 10%. For very senior citizens (individuals who have completed 80

years of age), the base exemption limit is extended upto first Rs 5 lakh of their income.

Moreover you would also have to pay an education cess @ 3% on your computed tax liability.

Also note that an additional surcharge @ 10% would be levied if your total income in the

financial year exceeds Rs 1 crore. The levy of this one time surcharge was announced in the

Union Budget in order to generate more tax revenue by increasing the tax liability of the rich.

This one-time surcharge, which is applicable only for the assessment year 2014-2015, will be in

addition to the education cess of 3% that is paid on total income-tax.

While the union Budget 2013 introduced a New Section 87A (which allows a Tax Credit or

Special Rebate of Rs 2,000 to individuals whose NTI is below Rs 5 lakhs), the rebate will be

limited to the extent of your tax liability or Rs 2,000 whichever is less.

So if your tax liability is say Rs 1,500, you will get a tax credit of only Rs 1,500 under section 87A

and no tax will be payable.

www.PersonalFN.com

12

Now let us see how you can compute your income tax liability:

Say if your net taxable income after availing for all deductions available is Rs 12 Lac in the

current financial year, then your tax liability will be computed as under:

Computation of Tax Liability (2013-14)

Taxable Income (in Rs) 12,00,000

Upto 2,00,000 Nil -

Rs 2,00,001 to Rs 500,000 10% 30,000

Rs 500,001 to Rs 10,00,000 20% 1,00,000

Rs 10,00,001 & above 30% 60,000

Tax payable (in Rs) 1,90,000

Education Cess 3% 5,700

Total Tax (in Rs) 1,95,700

(Source: Personal FN Research)

Parameters for “prudent tax planning”:

A Prudent exercise of tax planning also extends to appropriate investment planning, which also

takes into account your ideal asset allocation by considering the under-mentioned factors.

Hence after you have utilised the tax provisions within each head / source of income for

effective reduction in GTI, you must also consider the following parameters as these will enable

you to optimally reduce your tax liability.

Age

Your age and the tenure of your investment play a vital role in your asset allocation. The

younger you are more risk you can take and vice-a-versa. Hence, for prudent tax planning

too, if you are young, you should allocate more towards market-linked tax saving

instruments such as Equity Linked Saving Schemes (ELSS), Unit Linked Insurance Plans

(ULIPs) and National Pension System (NPS), as at a young age the willingness to take risk is

high. One may also consider taking a home loan at a younger age, as the number of years

of repayment is more along with your willingness to take risk being high.

www.PersonalFN.com

13

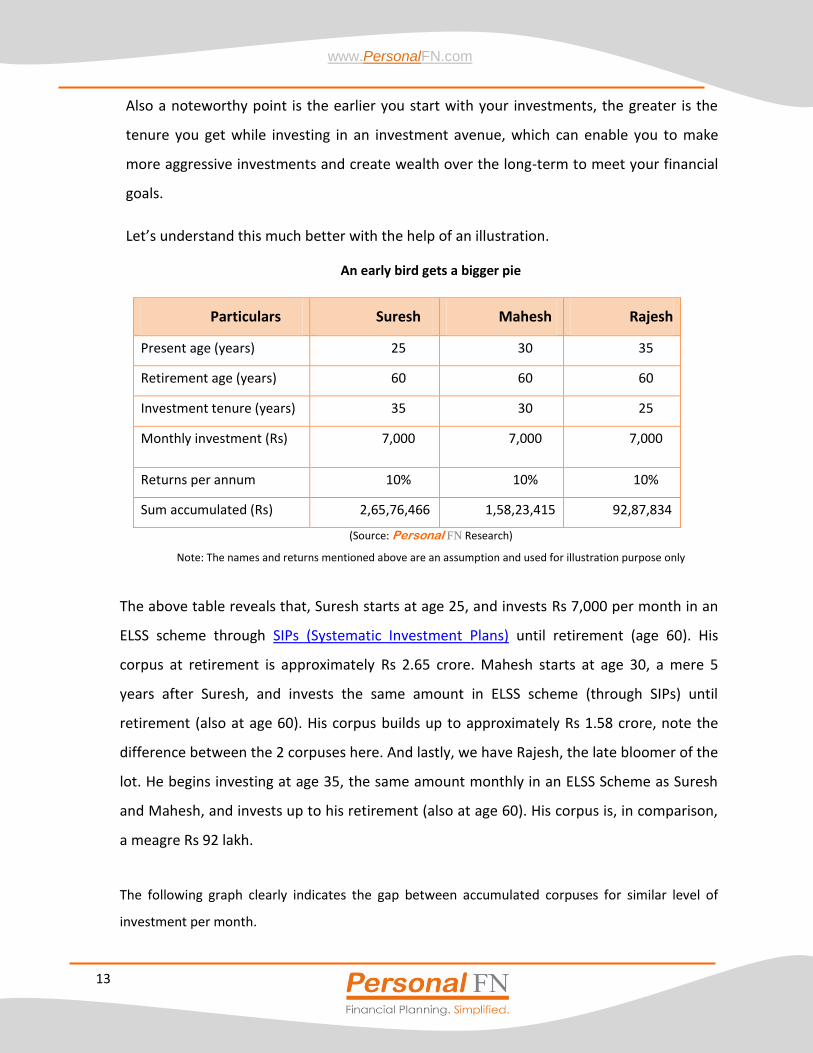

Also a noteworthy point is the earlier you start with your investments, the greater is the

tenure you get while investing in an investment avenue, which can enable you to make

more aggressive investments and create wealth over the long-term to meet your financial

goals.

Let’s understand this much better with the help of an illustration.

An early bird gets a bigger pie

Particulars Suresh Mahesh Rajesh

Present age (years) 25 30 35

Retirement age (years) 60 60 60

Investment tenure (years) 35 30 25

Monthly investment (Rs) 7,000 7,000 7,000

Returns per annum 10% 10% 10%

Sum accumulated (Rs) 2,65,76,466 1,58,23,415 92,87,834

(Source: Personal FN Research)

Note: The names and returns mentioned above are an assumption and used for illustration purpose only

The above table reveals that, Suresh starts at age 25, and invests Rs 7,000 per month in an

ELSS scheme through SIPs (Systematic Investment Plans) until retirement (age 60). His

corpus at retirement is approximately Rs 2.65 crore. Mahesh starts at age 30, a mere 5

years after Suresh, and invests the same amount in ELSS scheme (through SIPs) until

retirement (also at age 60). His corpus builds up to approximately Rs 1.58 crore, note the

difference between the 2 corpuses here. And lastly, we have Rajesh, the late bloomer of the

lot. He begins investing at age 35, the same amount monthly in an ELSS Scheme as Suresh

and Mahesh, and invests up to his retirement (also at age 60). His corpus is, in comparison,

a meagre Rs 92 lakh.

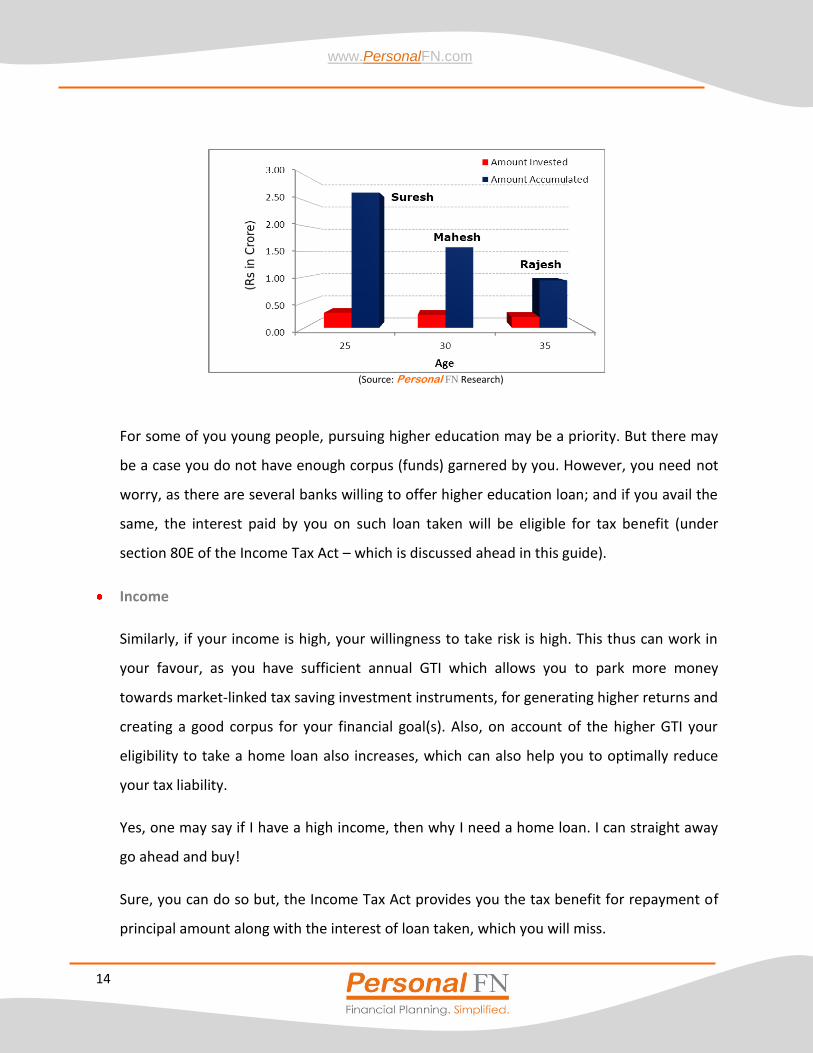

The following graph clearly indicates the gap between accumulated corpuses for similar level of

investment per month.

www.PersonalFN.com

14

(Source: Personal FN Research)

For some of you young people, pursuing higher education may be a priority. But there may

be a case you do not have enough corpus (funds) garnered by you. However, you need not

worry, as there are several banks willing to offer higher education loan; and if you avail the

same, the interest paid by you on such loan taken will be eligible for tax benefit (under

section 80E of the Income Tax Act – which is discussed ahead in this guide).

Income

Similarly, if your income is high, your willingness to take risk is high. This thus can work in

your favour, as you have sufficient annual GTI which allows you to park more money

towards market-linked tax saving investment instruments, for generating higher returns and

creating a good corpus for your financial goal(s). Also, on account of the higher GTI your

eligibility to take a home loan also increases, which can also help you to optimally reduce

your tax liability.

Yes, one may say if I have a high income, then why I need a home loan. I can straight away

go ahead and buy!

Sure, you can do so but, the Income Tax Act provides you the tax benefit for repayment of

principal amount along with the interest of loan taken, which you will miss.

www.PersonalFN.com

15

Also given that you are financially strong, you can also consider donating some of your

money towards a noble cause, as doing so will make you eligible for a tax benefit (under

section 80G of the Income Tax Act – which is discussed ahead in this guide).

Similarly, if your income is not high enough (i.e. it is low), and you do not want to put your

money to risk; you can invest in tax saving instruments which provide you assured returns.

These instruments can be Public Provident Fund (PPF), National Savings Certificates (NSCs),

5 Yr Bank Fixed Deposits, 5 Yr Post Office Time Deposits and Senior Citizen Savings Scheme

(provided you are a senior citizen).

Financial goals

The financial goals which one sets in life, also influences the tax planning exercise. So, say

for example your goal is retiring from work 5 years from now, then your tax saving

investment portfolio will be also less skewed towards market-linked tax saving instruments,

as you are quite near to your goal and your regular income will stop.

Likewise if you are many years away from the financial goal, you should ideally allocate

maximum allocation to market linked tax saving instruments and less towards those tax

saving instruments which provide you low assured returns.

Risk Appetite

Your willingness to take risk which is a function of your age, income, expenses, nearness to

goal, will be an important determinant while doing your tax planning exercise. So, if your

willingness to take risk is high (aggressive), you can skew your tax saving investment

portfolio more towards the market-linked instruments. Similarly, if your willingness to take

risk is relatively low (conservative), your tax saving investment portfolio can be skewed

towards instruments which offer you assured returns, and if you are a moderate risk taker

you can take a mix of 60:40 into market-linked tax saving instruments and assured return

tax saving instruments respectively.

www.PersonalFN.com

16

Yes, we reckon the fact that “prudent tax planning” exercise can be time consuming and

complex. But please note the fact that it’s an annual activity which every tax payer has to

go through – and if you start early and plan properly, the task becomes easier.

Remember, delay will only ensure that you invest at the last moment but not in line with

the parameters discussed above. If you are hard pressed for time, consider hiring a

competent tax consultant along with an investment advisor.

www.PersonalFN.com

17

IV - Optimal tax planning with section 80C

Section 80C of the Income Tax Act enables you to effectively invest in tax saving instruments, in

order to optimally reduce your tax liability; and this is seen as one of the most sought after

sections when it comes to tax planning. It offers a host of popular investment instruments

mentioned below which qualify you for a deduction from your Gross Total Income (GTI):

Life Insurance Premium

Public Provident Fund (PPF)

Employees’ Provident Fund (EPF)

National Saving Certificate (NSC) , including accrued interest

5-Year fixed deposits with banks and Post Office

Senior Citizens Savings Scheme (SCSS)

National Pension System (NPS)

Unit-Linked Insurance Plans (ULIPs)

Equity Linked Savings Schemes (ELSS)

Tuition fees paid for children’s education (maximum 2 children)

Principal repayment on Housing Loan

Hence, if you invest in any or all of the aforementioned instruments; you would qualify for

deduction under this section subject to the maximum of Rs 1,00,000 p.a. But we think rather

than just merely investing in any of the above tax saving instruments, you can also use these tax

saving instruments for prudent tax planning by recognising your age, income, financial goals

and risk appetite.

Now you may ask “how”?

Well, it’s simple! In the aforementioned list you can classify the tax saving instruments into

those offering variable returns (i.e. market-linked instruments) and those offering fixed returns

(i.e. assured return instruments). By doing so you would be able to ascertain which suits you

www.PersonalFN.com

18

best (taking into account the factors mentioned above) and would extend your tax planning

exercise to investment planning too.

Let’s discuss in detail the classification into market-linked tax saving instruments and assured

return tax saving instruments.

Tax Planning with market-linked instrument:

If you are young, income is high, and therefore willingness to take risk is high along with your

financial goals being far away, then this category would be suitable for you. Under this category

you can invest in the capital markets, giving you variable returns. Following tax saving

instruments are available for investment.

1. Equity Linked Savings Schemes (ELSS):

These are mutual fund schemes, which are 100% diversified equity funds providing tax saving

benefits. And these are popularly known as Tax Saving Mutual Funds. A distinguishing feature

about them is that they are subject to a compulsory lock-in period of three years, but the

minimum application amount in most of them is as little as Rs 500, with no upper limit. You can

either make lump sum investments or investments through the Systematic Investment Plan

(SIP).

It is noteworthy that, in the long-term if you intend to create wealth by hedging the inflation

risk, then this tax saving instrument can give you luring returns.

Yes, you may say – “but there is risk involved”. Well, no doubt about that, but in order to even

out the shocks of volatility in the equity markets you can adopt the SIP route of investing here

which will provide you the advantage of “compounding” along with “rupee-cost averaging”.

www.PersonalFN.com

19

SIPs provide cushion against market volatility

(Source: ACE MF, Personal FN Research)

Get wealthy Sip by Sip

(Source:ACE MF, Personal FN Research)

While SIPs in ELSS can help you tackle volatility and may help you gradually create wealth in the

long run, a noteworthy point in SIP investing in ELSS is that your every SIP installment (which

can be monthly, quarterly or half yearly) should complete the minimum lock-in period of 3

years.

Deduction: The maximum tax benefit which you can enjoy under section 80C is Rs 1,00,000 p.a.

Moreover, if you make any long term gains at the time of exit, any time after the end of the

lock-in period; then you would not have to pay any Long Term Capital Gains Tax (LTCG) too.

www.PersonalFN.com

20

2. Unit-Linked Insurance Plans (ULIPs):

These are typically insurance-cum-investment plans which enable you to invest in equity and /

or debt instruments depending on what suits you as per your age, income, risk profile and

financial goals. All you simply need to do is, select the allocation option as provided by the

insurance company offering such a plan. Generally they are classified as “aggressive” (which

invests in equity), “moderate or balanced” (which invests in debt as well as equity) and

“conservative” (which invests purely in debt instruments).

Hence apart from the insurance cover (which is 10 times your annual premium) offered under

these plans, the returns which you would get would be completely market-linked as your

premium amount (after accounting for allocation and other charges) is invested in equity and

debt securities.

And in order for you to track such plans the NAV is declared on a regular basis. These policies

have a minimum 5 year lock-in period, and also have a minimum premium paying term of 5

years. The overall term of the policy would vary from product to product.

In case of any eventuality the beneficiaries would be paid the sum assured or fund value,

whichever is higher.

But a noteworthy point is, while some well selected ULIPs may add value to your portfolio in the

long-term; your insurance and investment needs should be dealt separately, thus enabling you

to have the optimum insurance coverage and the right investment instruments for long-term

wealth creation.

Deduction: The premium which you pay for your ULIP would be eligible for tax benefit, subject

to the maximum eligible amount of Rs 1,00,000 p.a. as available under Section 80C. Moreover,

a positive point is that at maturity the amount which you or your beneficiary would receive is

tax free (exempt) as per the provisions of Section 10(10D) of the Income Tax Act.

www.PersonalFN.com

21

3. National Pension System (NPS):

National Pension System which was earlier available only for Government employees was later

on May 1, 2009 also introduced for people in the unorganised (private) sector, as need for

deeper participation in the pension contribution (through this product) was felt.

For NPS, if you (eligibility age: from 18 years to 60 years) belong to the unorganised sector (i.e.

private sector); the contributions done by you towards the scheme would be voluntary, and

you can invest in any of the two under-mentioned accounts:

Tier-I Account:

In this account your minimum investment amount is Rs 500 per contribution and Rs 6,000

per year, and you are required to make minimum 4 contributions per year. Under this

account, premature withdrawals upto a maximum of 20% of the total investment is not

permitted before attainment of 60 years, however the balance 80% of the pension wealth

has to be utilised by you to buy a life annuity.

Tier-II Account:

For opening this account you will have to make a minimum contribution of Rs 1,000 per

annum. The minimum number of contributions is 4, subject to a minimum contribution of

Rs 250. However, if you open an account in the last quarter of the financial year, you will

have to contribute only once in that financial year. You will be required to maintain a

minimum balance of Rs 2,000 at the end of the financial year. In case you don’t maintain

the minimum balance in this account and do not comply with the number of contributions

in a year, a penalty of Rs 100 will be levied. Moreover, in order to have Tier-II account, you

first need to have a Tier-I account. Tier-II account is a voluntary account and withdrawals

will be permitted under this account, without any limits.

www.PersonalFN.com

22

Even if you hold both the above accounts under NPS, only the Tier-I account will be eligible for

tax benefits.

While investing money in NPS, you have two investment choices i.e. “Active” or “Auto” choice.

Under the “Active” choice asset class, your money will be invested in various asset classes viz. E

(Equity), C (Credit risk bearing fixed income instruments other than Government Securities) and

G (Central Government and State Government bonds); where you will have an option to decide

your asset allocation into these asset classes. In case of Auto Choice, your money will be

invested in the aforesaid asset classes in accordance with predetermined asset allocation.

But remember, the return on your investment is not guaranteed as it is market-linked. At your

age of 60 years, you can exit the scheme; but you are required to invest a minimum 40% of the

fund value to purchase a life annuity. And the remaining 60% of the money can be withdrawn in

lump sum or in a phased manner upto your age of 70 years.

In our opinion this product is not very appealing for creating a substantial corpus to meet your

retirement need. Rather, if you chalk-out a prudent financial plan with the help of a financial

planner, and invest wisely as per the plan laid out (which would mostly recommend you equity

allocation at younger age, and then as your age progresses balance the asset allocation

between equity and debt instruments), then the corpus which you would be able to create will

be substantial enough to meet your retirements needs. Also the money withdrawn under this

scheme, even at the age of 60 is taxable.

Deduction: Those who are salaried employees may claim deduction under section 80C upto Rs

1 lac for their own contributions towards NPS account. In addition to this, they are entitled to

claim deductions under section 80 CCD if there is any contribution made by their employer but

only upto 10% of their salary (for this purpose salary construes as Basic Salary plus Dearness

Allowance). It is noteworthy that the deduction under section 80CCD can be claimed over and

above the permissible deductions under section 80C.

So if an Individual contributes alone from his income towards NPS, it will be considered within

the limits of 1 Lakh p.a. under sec 80C.

www.PersonalFN.com

23

It is only if the Employer contributes to employee for NPS – sec 80 CCD is applicable.

So to avail this extra tax exemption limit, the employees need to convince their employers to

start contributing to NPS.

However, those who are self-employed can avail deduction under section 80CCD upto 10% of

their gross total income (which is comprised of income computed under different heads before

reducing it by all other deductions available under section 80). In addition to deductions under

section 80CCD, self-employed people are also entitled to deductions under section 80C for

other instruments eligible therein.

Tax Planning the “assured return” way:

Unlike the case presented above (i.e. tax planning with market-linked instruments), if your age,

income, risk profile and financial goals do not permit you to invest in market-linked instruments

(for your tax planning) along with the fact that your risk taking ability is low; then you should

plan investing in tax saving instruments which offer you assured returns. Under these

instruments there is zero risk of erosion to your capital. Following are the tax saving

instruments available under this category:

1. Non-Unit Linked Life Insurance Plans:

Life Insurance plans can be broadly classified as “pure term life insurance plans” and

“investment-cum-life insurance plans”.

Pure term life insurance plans are authentic in nature, as they cater to the need of only

protection and not investment. Hence such plans offer a high life insurance coverage at low

premiums. Generally the term insurance plans offer a policy term of 10, 15, 20, 25 or 30 years.

Investment-cum-life insurance plans on the other hand, as the name suggest offer you an

investment option along with insurance option. But here your insurance coverage is far lesser,

than the one provided under pure term insurance plans. So, you pay a high premium which gets

www.PersonalFN.com

24

invested, but insurance coverage on the other hand is meagre. Such insurance plans can be

offered in various forms such as ULIPs (as discussed above), endowment plans, money back

plan, pension plans etc.

We think that while you are considering your insurance needs, you should ideally look at only

pure term life insurance plans, thus keeping your insurance needs separate from investment

needs.

Deduction: Over here too the premium which you pay for your such non-ULIP life insurance

plans would be eligible for tax benefit, subject to the maximum eligible amount of Rs 1,00,000

p.a. as available under Section 80C. Moreover, a positive point is that at maturity the amount

which you or your beneficiary would receive is exempt (tax free) as per the provisions of

Section 10(10D) of the Income Tax Act.

2. Public Provident Fund (PPF):

The PPF scheme is a statutory scheme of the Central Government of India.

In order to invest in PPF, you are required to open a PPF account (which is irrespective of your

age) at your nearest post office or public sector (nationalized) bank providing this facility. You

can open the account in your name, and also in the name of your wife as well as children. If you

do not wish to open a separate account in the name of your wife as well as children, you can

nominate them; but joint application is not permissible.

The account so opened will have an expiry term of 15 years from the end of the year in which

the initial investment (subscription) to the account is made. You can invest in the account

ranging from a minimum of Rs 500 to a maximum of Rs 100,000 in a financial year in order to

enjoy the tax saving benefit under Section 80C, and the amount to the credit of your account

will be entitled to a tax-free interest at 8.8% p.a. Your each deposit in the PPF account should at

least be Rs 500, and one has the convenience of depositing in either lump sum or in

installments not exceeding 12 such installments. However, a noteworthy point is that it is not

necessary to deposit every month and the amount too can be any amount subject to the

minimum (Rs 500) and maximum (Rs 1,00,000) amount.

www.PersonalFN.com

25

The interest to the account will be calculated on the lowest balance to the credit of the account

between the close of the 5th day and the end of the month, and will be credited to account on

31st of March, each year.

As regards withdrawal from the account is concerned; it is permitted any time after the expiry

of 5 years from the end of the year in which initial investment (subscription) to the account is

made. However, your withdrawal will be restricted to 50% of the amount which stood to the

credit of your account in the immediate 4th year immediately preceding the year of withdrawal

or at the end of the preceding year, whichever is lower. And in case if your term of 15 year is

over, you can withdraw the entire amount together with the interest accrued till the last day of

the month, preceding the month in which application for withdrawal is made.

After your term of 15 years is over if you wish to renew your account, you can do so for a

period of another 5 years at the rate of interest prevailing then, without having the compulsion

of putting any further deposits in case of extension. The withdrawal in case of extended

accounts is permissible once in every financial year. But the total withdrawal should not exceed

60% of the balance accumulated to the account at the commencement of the extension period

(of 5 years).

It is noteworthy that if you are risk averse, then this product is best in its class for tax planning.

Moreover, it also offers you an appealing tax-free return of around 8% p.a. (compounded

annually).

Deduction: The contributions which you make to the accounts mentioned above, would be

eligible for tax benefit but subject to the maximum eligible amount of Rs 1,00,000 p.a. as

available under Section 80C.

3. National Savings Certificate (NSC):

The NSC is also a scheme floated by the Government of India, and one can invest in the same

through your nearest post offices, as the scheme is available only with the India Post. The

certificates can be made in your own name, jointly by two adults, or even by a minor (through

the guardian), and has a tenure of 5 years or 10 years.

www.PersonalFN.com

26

The minimum amount which you can invest is Rs 100, with no maximum limit to the same. NSC

maturing in 5 years offers interest @ 8.5% p.a. compounded half-yearly whereas NSC maturing

in 10 years offers interest @ 8.8% p.a. compounded half-yearly, thus giving you an effective

interest rate of 8.68% p.a. and 8.99% p.a. The interest income accrues annually and is

reinvested further in the scheme till maturity (i.e. 5 or 10 years) or until the date of premature

withdrawals.

Premature withdrawals are permitted only in specific circumstances such as death of the

holder.

Deduction: Your investment in NSC is eligible for a deduction of upto Rs 1,00,000 p.a. under

Section 80C. Furthermore, the accrued interest which is deemed to be reinvested qualifies for

deduction under Section 80C. However, the interest income is chargeable to tax in the year in

which it accrues. But in case if you have no other income apart from interest income, then in

order to avoid Tax Deduction at Source (TDS), you can submit a declaration in Form 15-H (for

general) or Form 15-G (for senior citizens) as applicable.

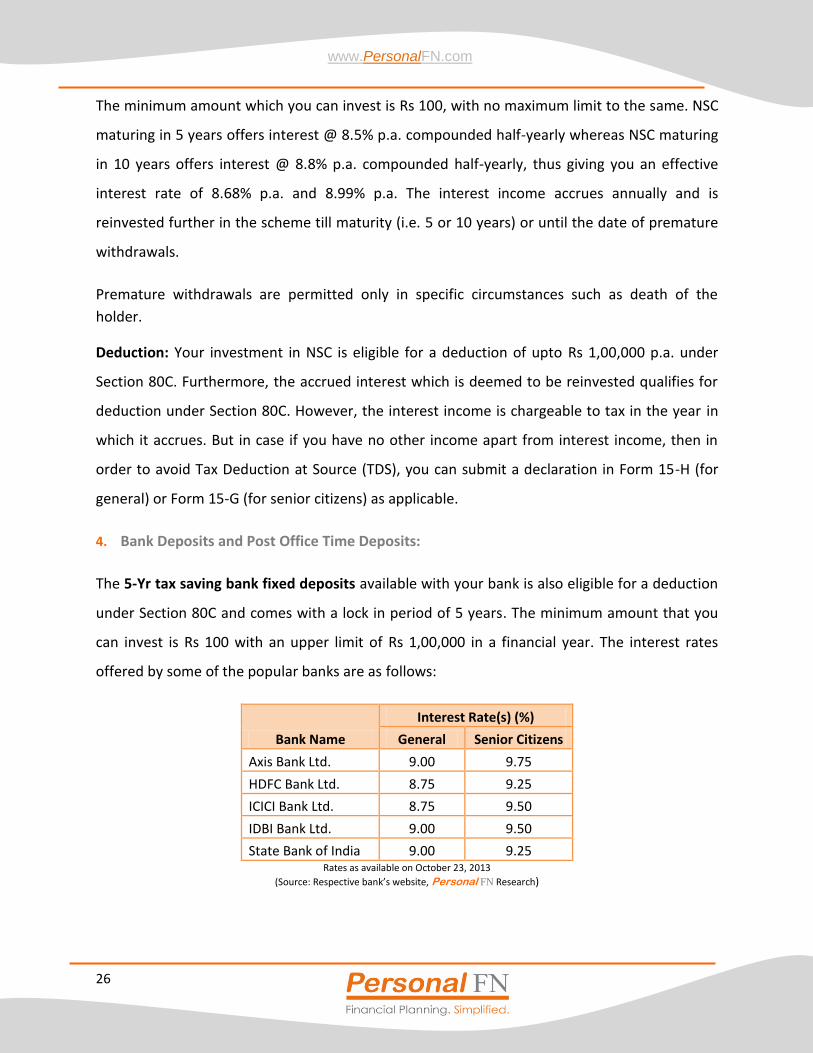

4. Bank Deposits and Post Office Time Deposits:

The 5-Yr tax saving bank fixed deposits available with your bank is also eligible for a deduction

under Section 80C and comes with a lock in period of 5 years. The minimum amount that you

can invest is Rs 100 with an upper limit of Rs 1,00,000 in a financial year. The interest rates

offered by some of the popular banks are as follows:

Bank Name

Interest Rate(s) (%)

General Senior Citizens

Axis Bank Ltd. 9.00 9.75

HDFC Bank Ltd. 8.75 9.25

ICICI Bank Ltd. 8.75 9.50

IDBI Bank Ltd. 9.00 9.50

State Bank of India 9.00 9.25 Rates as available on October 23, 2013

(Source: Respective bank’s website, Personal FN Research)

www.PersonalFN.com

27

However, the interest earned here would be subject to tax deduction at source, making it

detrimental for your tax planning, but again you can submit a declaration in Form 15-H (for

general) or Form 15-G (for senior citizens) as applicable for not deducting tax at source.

Similarly 5 Yr Post Office Time Deposits (POTDs) also offer you a tax benefit under Section 80C.

The account can be opened by you either in single name or jointly or even by a minor (through

a guardian) who has attained the age of 10.

The minimum investment amount is Rs 200, and there isn’t any upper limit. However, the

investment amount over Rs 1,00,000 will not be eligible for any tax benefit.

A 5-Yr POTD earns a return of 8.4% p.a. (compounded quarterly), but paid annually. Hence, say

if you deposit an amount of Rs 10,000, the interest income which you will fetch would

approximately be Rs 867 p.a. As regards premature withdrawals are concerned, they are

permitted only after 1 year from the date of deposit and interest on such deposits shall be

calculated at the rate, which shall be 1% less than the rate specified for a period of 5-Year

deposit.

Deduction: Your investment in both these schemes are eligible for a deduction of upto Rs

1,00,000 p.a. under Section 80C. But as mentioned above, the interest earned on your

investments will be subject to tax deduction at source. However, in case if you have no other

income apart from interest income, then in order to avoid Tax Deduction at Source (TDS), you

can submit a declaration in Form 15-H (for general) or Form 15-G (for senior citizens) as

applicable.

5. Senior Citizens Savings Scheme (SCSS):

Well, the SCSS is an effort made by the Government of India for the empowerment and

financial security of senior citizens. So, in case if you are over 60 years old, you are eligible to

invest in this scheme. Moreover, if you have attained 55 years of age and have retired under a

voluntary retirement scheme; then too you are eligible to enjoy the benefits of this scheme.

www.PersonalFN.com

28

In order to avail the benefits of this scheme, you are required to open a SCSS account (either in

a single name, or jointly along with your spouse) at your nearest post office or any nationalised

bank. You can do a onetime deposit under this scheme subject to the minimum investment

amount of Rs 1,000 and a maximum of Rs 15,00,000. The maturity period provided for this

scheme is 5 years offering a rate of interest of 9.20% p.a. payable on a quarterly basis (i.e. on

March 31, June 30, September 30 and December 31) every year from the date of deposit.

Premature withdrawals are permitted only after one year from the date of opening the

account. If you withdraw between 1 and 2 years, 1.5% of the initial amount invested will be

deducted. And in case if you withdraw after 2 years, 1.0% of the balance amount is deducted.

Deduction: Your investments upto Rs 1,00,000 in SCSS are entitled for a deduction under

Section 80C. However, the interest earned by you would be subject to tax deduction at source.

But in case if you have no other income apart from interest income, then in order to avoid Tax

Deduction at Source (TDS), you can submit a declaration in Form 15-H (for general) or Form 15-

G (for senior citizens) as applicable.

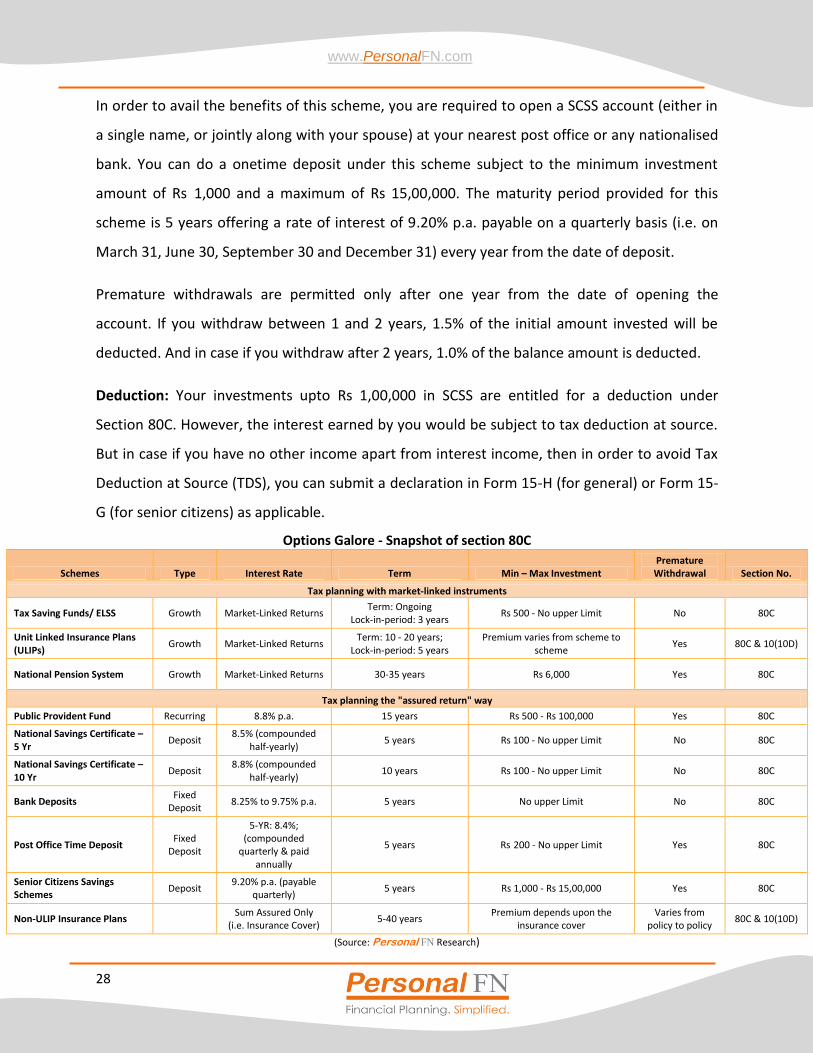

Options Galore - Snapshot of section 80C

Schemes Type Interest Rate Term Min – Max Investment Premature Withdrawal Section No.

Tax planning with market-linked instruments

Tax Saving Funds/ ELSS Growth Market-Linked Returns Term: Ongoing

Lock-in-period: 3 years Rs 500 - No upper Limit No 80C

Unit Linked Insurance Plans (ULIPs)

Growth Market-Linked Returns Term: 10 - 20 years;

Lock-in-period: 5 years Premium varies from scheme to

scheme Yes 80C & 10(10D)

National Pension System Growth Market-Linked Returns 30-35 years Rs 6,000 Yes 80C

Tax planning the "assured return" way

Public Provident Fund Recurring 8.8% p.a. 15 years Rs 500 - Rs 100,000 Yes 80C

National Savings Certificate – 5 Yr

Deposit 8.5% (compounded

half-yearly) 5 years Rs 100 - No upper Limit No 80C

National Savings Certificate – 10 Yr

Deposit 8.8% (compounded

half-yearly) 10 years Rs 100 - No upper Limit No 80C

Bank Deposits Fixed

Deposit 8.25% to 9.75% p.a. 5 years No upper Limit No 80C

Post Office Time Deposit Fixed

Deposit

5-YR: 8.4%; (compounded

quarterly & paid annually

5 years Rs 200 - No upper Limit Yes 80C

Senior Citizens Savings Schemes

Deposit 9.20% p.a. (payable

quarterly) 5 years Rs 1,000 - Rs 15,00,000 Yes 80C

Non-ULIP Insurance Plans Sum Assured Only

(i.e. Insurance Cover) 5-40 years

Premium depends upon the insurance cover

Varies from policy to policy

80C & 10(10D)

(Source: Personal FN Research)

www.PersonalFN.com

29

6. Tuition fees paid for children’s education (maximum 2 children):

The tuition fees that you pay to any university, college, school or other educational institution

situated within India for your children’s education is also eligible for deduction under section

80C. However the fees paid towards any coaching center or private tuition may not be eligible.

Also you need to note that this deduction is available only to Individual Assesse and not for

HUF, and is limited to Rs. 1,00,000 and a maximum 2 children. If someone has four children,

then husband and wife both can enjoy a separate limit of two children each, so they can

separately claim deduction (upto Rs 1,00,000) for 2 children each, subject to the amount they

have actually paid.

7. Principal repayment on Housing Loan:

You always wanted to have your dream home and now you have been able to get it with the

help of housing loan from a bank or a financial institution. But after you have got your home

through this loan, you have the obligation to repay the principal amount of the loan on time.

The “repayment of principal amount”, makes you eligible to claim a deduction upto a sum of Rs

1,00,000 under section 80C; and that benefit is available with you immaterial of the fact

whether you stay in the same property (Self Occupied Property - SOP), or have let it out on rent

(Let Out Property LOP). You can also claim tax benefit on the interest you pay on your housing

loan, but under a separate section (Section 24 which is covered in detail at the later stage in the

guide)

In case you have taken a second home loan for another property, then the principal amount

repaid (up to Rs 1 lakh) for the home loan taken only on your self-occupied property qualifies

for deduction under Section 80C. However you cannot claim deduction for the principal

repayment made against the home loan on the other property.

www.PersonalFN.com

30

V - Thinking beyond Section 80C

Well, most people think that tax planning ends with Section 80C; but please note that there’s

more to tax planning than just investment instruments specified under Section 80C. Our Income

Tax Act, 1961 also considers the humane side of our life and also gives deduction for such

expenditure. So, in case if you pay your medical insurance premium, incur expenditure on the

medical treatment of a “dependant” handicapped, donate to specified funds for specified

causes, contribute in monetary form to political parties or electoral trusts, take a loan for

pursuing higher education or if you are an individual suffering from “specified” diseases, then

all this too can help you effectively plan your tax obligations, thus optimally reducing your tax

liability.

So, let’s understand how each of the above expenses for a cause or an investment, can help you

in effective tax planning. Herein below is the list of some major ones.

1. Premium paid for medical insurance (Section 80D):

The premium paid by you on medical insurance policy (commonly referred to as a mediclaim

policy) to cover your spouse and you, dependent children and parents against any unexpected

medical expenses, qualifies for a deduction under Section 80D.

The maximum amount allowed annually as a deduction (from your GTI) is Rs 15,000, in case if

you pay for yourself, spouse and dependent children. And if you are a senior citizen, the

maximum deduction gets extended to Rs 20,000.

Further, if you pay medical insurance premium for your parents (irrespective of whether they

are dependent on you or not), you can claim an additional deduction of upto Rs 20,000 in case

parents are senior citizens or Rs 15,000 in other cases under this section. So, for example, if you

pay a premium of Rs 15,000 for yourself and Rs 17,000 for your parents, you will be eligible for

a total deduction of Rs 30,000 only, assuming your parents are not senior citizens.

However, while paying the premium you need to ensure that the payment is made in any mode

other than cash.

www.PersonalFN.com

31

2. Maintenance including medical treatment of a handicapped dependent (Section 80DD):

If you have incurred any expenditure in the form medical treatment (including nursing), training

and rehabilitation for a handicapped “dependent” suffering from disability, then the

expenditure so incurred by you qualifies for deduction under Section 80DD of the Income Tax

Act. Similarly, if you have deposited a sum of money under any scheme framed in this behalf by

LIC (Life Insurance Corporation of India) or any other insurer or administrator or a specified

company (approved by the Board), for maintenance of the “dependent” being a person with

disability; also qualifies for a deduction under Section 80DD.

The quantum of deduction here depends upon the severity of the disability suffered by the

“dependent”. Hence, if the “dependent” is suffering from 40% of any disability [Specified under

section 2(i) of the Person with Disability (Equal Opportunities, Protection of Rights and Full

Participation) Act, 1955], then you would be entitle to a deduction of a fixed sum of Rs 50,000

p.a. from your GTI irrespective of the expenditure incurred or amount deposited. Similarly, if

the “dependent” is suffering from severe disability (i.e. 80% of any disability), then you claim a

higher deduction of fixed sum of Rs 100,000, from your GTI irrespective of the expenditure

incurred or amount deposited.

It is noteworthy that over here the term “dependent” being a person with disability means your

spouse, children, parents, brothers and sisters.

Moreover, in order to claim the deduction you need to submit a medical certificate issued by a

medical authority along with your return of income. Also if you are claiming a deduction in your

tax returns for such an expenditure incurred or amount deposited, your “dependent” cannot

claim a deduction under Section 80U in case he’s (handicapped dependent) filing his tax returns

separately.

www.PersonalFN.com

32

3. Expenditure incurred on your medical treatment (Section 80DDB):

If you have incurred expenditure on your medical treatment or for your “dependents”, then too

the expenditure so incurred, makes you eligible for deduction under Section 80DDB of the

Income Tax Act.

The deduction from your GTI, which you are entitled to, is Rs 40,000 or the amount actually

paid, whichever is lower. And if you are a senior citizen, then you are eligible for a deduction of

Rs 60,000 or the amount actually paid, whichever is lower.

It is noteworthy that over here the term “dependent” means your wholly or mainly dependent

spouse, children, parents, brothers and sisters. Also, in order to claim a deduction under this

section, you are required to submit a medical certificate from a doctor (neurologist, oncologist,

urologist, haematologist, immunologist, or any other specialist) working in a Government

hospital.

4. Repayment of loan taken for pursuing higher education (Section 80E):

While pursuing a personal goal of enrolling for “higher education” in order to be competitive

enough to meet your financial goals; the Income Tax Act offers you deduction (from your GTI),

when you take a loan to fulfil such dreams.

Sure, you can also take an education loan for your wife’s or children’s education or for any

person (minor) for whom you are the legal guardian. But that makes you eligible for deduction

under Section 80E of the Income Tax Act, to the extent of the interest paid on such a loan

taken.

The deduction is available for a maximum of 8 years or till the interest is paid, whichever is

earlier. So, to simplify it further, the deduction is available from the year in which you start

paying the interest on the loan, and the seven immediately succeeding financial years or until

the interest is paid in full, whichever is earlier.

www.PersonalFN.com

33

It is noteworthy that, here the term “higher education” means full-time studies for any

graduate or post-graduate course in engineering (including technology / architecture) ,

medicine, management or for post-graduate courses in applied science or pure science

including mathematics and statistics. But from the Finance Act of 2011 its scope is extended to

cover all fields of studies (including vocational studies) pursued after passing the Senior

Secondary Examination or its equivalent from any school, board or university recognised by the

Central or the State Government or local authority or any other authority authorised by the

Central or the State Government or local authority to do so. However, no deduction is available

for part-time courses

5. Donations to certain funds and charitable institutions (Section 80G):

As mentioned earlier that our Income Tax Act considers the humane side of our life, and so if on

humanitarian grounds you donate to certain specified funds, charitable institutions, approved

educational institutions etc, the donation amount qualifies for deduction under this section.

The deductions allowed can be 50% or 100% of the donation, subject to the stated limits as

provided under this section. For example, donations to “National Defence Fund” set up by the

Central Government are allowed 100% deduction, while for “Prime Minister Drought Relief

Fund” are allowed at 50%. If you make donations to any of the host of notified funds and / or

charitable institutions, you are eligible for deduction under Section 80G.

Funds / Charitable Institutions Amount Deductible

National Defence Fund 100%

Prime Minister’s National Relief Fund 100%

Prime Minister’s Armenia Earthquake Relief Fund 100%

Africa (Public Contributions – India) Fund 100%

National Foundation for Communal Harmony 100%

Any approved university or educational institution 100%

Maharashtra Chief Minister’s Relief Fund and Chief Minister’s Earthquake Relief Fund 100%

Any fund set up by Gujarat State Government for providing relief to earthquake victims 100%

National Children’s Fund 100%

Jawaharlal Nehru Memorial Fund 50%

Prime Minister’s Drought Relief Fund 50%

Indira Gandhi Memorial Trust 50%

Rajiv Gandhi Foundation 50% Note: There are also other funds and charitable institutions that are eligible for deduction under Section 80G.

(Source: Personal FN Research)

www.PersonalFN.com

34

While there are 3.3 million registered NGOs and scores of causes, selecting a genuine charity is

a challenge. HelpYourNGO has set up an initiative which can help you make an informed

donation decision. The organisation promotes philanthropy through transparency, by providing

easy access to financials of over 240 NGOs and allows comparison of data and ratios across

multiple parameters.

Visit www.HelpYourNGO.com to Evaluate and then Donate to the right cause.

In order to claim deduction under this section, you are required to attach a proof of payment

along with your return of income.

6. Rent paid in respect to property occupied for residential use (Section 80GG):

If you are a self-employed or a salaried individual who is not in receipt of any House Rent

Allowance (HRA), and is paying a rent for an accommodation (irrespective of whether furnished

or unfurnished) occupied for residential use, then you can claim a deduction under this section.

But as a pre-condition for availing deduction under this section,

- You must pay rent for the house you live in, and should not get HRA for even a part of

the year

- You should not own and occupy any other house anywhere

- You or your spouse or your minor child or Hindu Undivided Family (if you are part of

one) must not own any residential accommodation in the city you reside or work in.

And the deduction which will be available to you under this section is the least of:

25% of your total income or,

Rs 2,000 per month or,

Rent paid in excess of 10% of your total income

To claim deduction under section 80GG, you need to file a declaration in Form No. 10BA

www.PersonalFN.com

35

7. Contributions made to any political parties or electoral trust (Section 80GGC):

Say, if you have some nepotism for any political party or electoral trust as you appreciate the

work done by them; and therefore decide to make a monetary contribution to the party or

electoral trust, then the amount so contributed would be eligible for a deduction under this

section.

8. Specified disability(s) (Section 80U):

As said earlier, that our Income Tax Act, 1961 considers the humane side of life; so if you as an

individual resident in India is suffering from any specified disability i.e. you suffering 40% or

more than 40% of any of the below specified diseases, then you would be eligible for deduction

under this section.

Specified disabilities:

Blindness

Low vision

Leprosy-cured

Hearing impairment

Locomotor disability

Mental retardation

Mental illness

The deduction available under this section is flat (i.e. fixed) Rs 50,000, immaterial of the

expenditure incurred. But if the disability is severe in nature (i.e. 80% or above), then one is

entitled to flat (i.e. fixed) deduction of Rs 1,00,000.

However in order to avail of the deduction, you need to be an individual resident in India during

the financial year for which you are claiming the deduction. Also you need to file the copy of

certificates issued by the medical authority, at the time of filing returns.

www.PersonalFN.com

36

9. Rajiv Gandhi Equity Savings Scheme (RGESS):

The Finance Act 2012 introduced a new section 80CCG on ‘Deduction in respect of investment

made under an equity savings scheme’ to give 50% tax break to new investors who can invest

up to Rs. 50,000 and whose gross total annual income is less than or equal to Rs. 10 lakhs. Later

in the union budget 2013-14, the limit was increased to Rs 12 lakh. Since the scheme was

introduced for novice investors only i.e. for those who are entering the market for the first

time, the benefit u/s 80CCG was to be claimed only in the first year. However, in the budget

2013-14, it was extended to first-three successive years.

The objective of the scheme is to encourage flow of savings in the financial instruments and

improve the depth of the domestic capital market. In order to device safety measures for new

investors investing in direct equity through the RGESS, the stocks of Maharatna, Navaratna and

Miniratna, besides the top 100 stocks (BSE 100 or CNX 100) listed on the stock exchanges are

considered under RGESS. The argument for proposing investments only from the large caps and

PSU domain is, not only to provide security but also to ensure liquidity.

The first time investors can take benefit of RGESS, by investing in eligible stocks, RGESS eligible

close-ended Mutual Fund schemes and RGESS eligible Exchange Traded Funds. To make it

convenient to identify the eligible stocks and mutual funds, the stock exchanges shall furnish

list of RGESS eligible stocks / ETFs / MF schemes on their website. Further, the list shall also be

forwarded to the depositories at monthly intervals and whenever there is any change in the

said list. For this purpose, mutual fund houses shall communicate the list of RGESS eligible MF

schemes / ETFs to the stock exchanges.

The money invested under RGESS is subject to an overall lock-in period of 3 years, though one

can sell / pledge / hypothecate their securities after the expiry of the mandatory lock-in period

of 1 year, but he cannot withdraw the money before 3 years. i.e. Investors may be allowed to

churn their portfolio after completion of fixed lock in period of 1 year, but his account will be

converted into an ordinary demat account only on completion of 3 years.

www.PersonalFN.com

37

Options Galore - Snapshot of deduction under other 80s

Section Quick Description of Deduction Limit

80D Premium paid for medical insurance

Maximum upto Rs 15,000 or Rs 20,000 in case of senior citizen. Additional deduction of upto Rs 20,000

is available on premium paid for parents. The maximum amount of exemption that can be availed

by an individual is Rs 40,000

80DD Maintenance including medical treatment of a

handicapped dependent who is a person with disability

Rs 50,000, irrespective of the amount incurred or deposited. However in case of disability of more than

80% a higher deduction of flat Rs 1,00,000 shall be allowed.

80DDB Expenditure incurred in respect of medical treatment Actual incurred, with a ceiling of up to Rs 40,000 or Rs

60,000 in case of senior citizen, whichever is lower

80E Repayment of loan taken for pursuing higher education Maximum deduction for interest paid for a maximum

of 8 years or till such interest is paid, whichever is earlier

80G Donations to certain funds and charitable institutions Maximum deductions allowed can be 50% or 100% of the donation, subject to the stated limits as provided

under this section

80GG Rent paid in respect of property occupied for residential

use

Maximum deduction allowed is least of the following: Rs 2,000 per month; 25% of total income; Excess of

rent paid over 10% of total income

80GGC Contribution made to any political parties or electoral

trust Amount donated to political party is fully exempt

80U Person suffering from specified disability(s) Rs 50,000, irrespective of the amount incurred or

deposited. However in case of disability of more than 80% a higher deduction of flat Rs 100,000 is allowed.

80CCG Rajiv Gandhi Equity Savings Scheme (RGESS) Maximum deduction allowed is 50% of investment upto Rs 50,000, only for first time investors having total income of less than or equal to Rs 12 Lakhs.

(Source: Personal FN Research)

www.PersonalFN.com

38

VI - Your home loan and tax planning

While all of us have a dream of buying a dream home or constructing or reconstructing or

repairing our homes, it’s also important to consider the tax angle when we decide to do any of

these activities. For some of us, the amount of wealth we have created allows buying or

constructing or reconstructing or repairing or renewing homes from our own funds - i.e.

without opting for a “home loan”; but again doing so precludes you to avail of the tax benefit,

which are attached if one takes a home loan for such activities.

But again just to reiterate please don’t rule out the financial planning aspect of number of years

left with you for repayment of your home loan.

Yes, our Income Tax Act, 1961 too considers our desire to buy or construct or reconstruct or

repair or renew our dream home and gets a little benevolent, if one avails of a loan to fulfill

these desires for one’s dream home. The Act encourages you to buy, to do the aforementioned

activities (for your home) with a loan, as it provides you with tax benefits (that come along with

it). Both, “repayment of principal amount” and “payment of interest” are eligible for tax

benefit.

As we know that the “repayment of principal amount”, makes you eligible to claim a deduction

upto a sum of Rs 1,00,000 under section 80C; and that benefit is available with you immaterial

of the fact whether you stay in the same property (Self Occupied Property - SOP), or have let it

out on rent (Let Out Property LOP).

As far as the payment of interest amount (for the loan amount availed) is concerned, it’s

available for deduction under section 24(b). So, if you buy or acquire a house and decide to stay

in the same (SOP) then the maximum sum of Rs 1,50,000 p.a. can be availed by you as a

deduction for interest. However, if you have let out the property on rent (LOP), then the actual

interest payable is eligible for deduction, thus not being subject to any maximum limit. This

applies even in the case where you have two home loans for two different properties, where

one is self-occupied and the other is let out on rent.

www.PersonalFN.com

39

Similarly, if you have taken a loan for the purpose of reconstructing, repairing or renewing the

property, the amount of deduction under section 24(b) which you’ll be eligible for will be

restricted to Rs 30,000, irrespective whether you want to stay in it or let it out on rent.

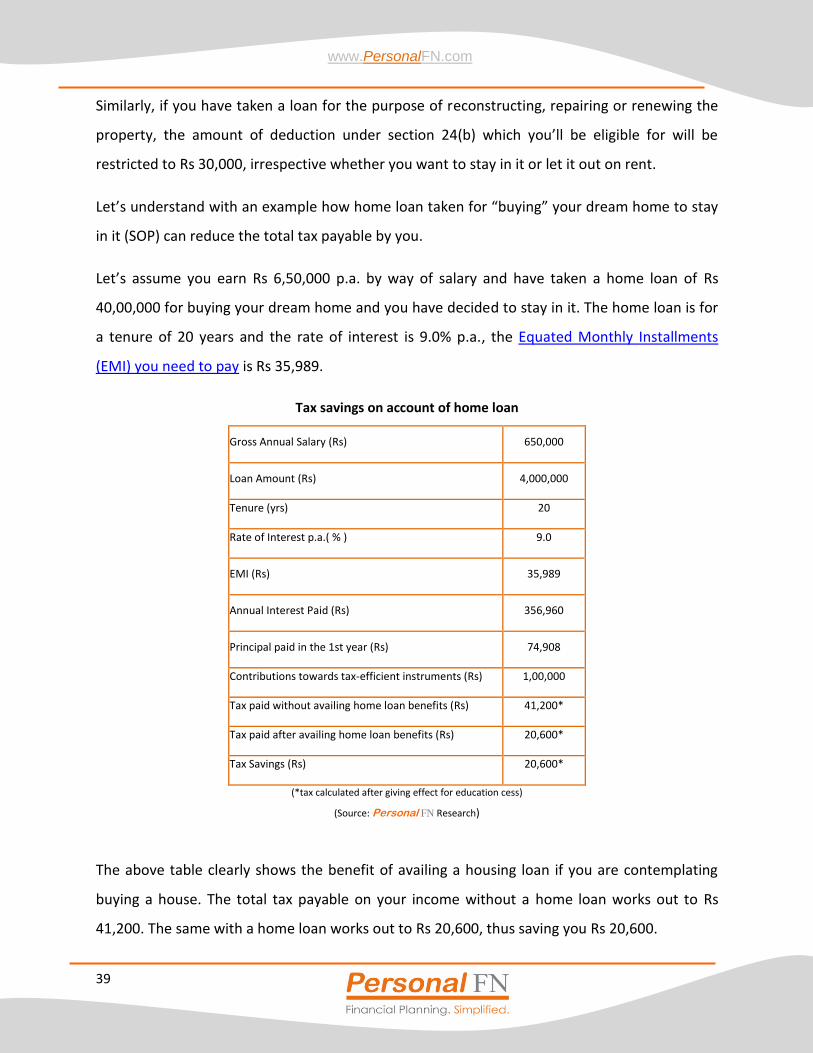

Let’s understand with an example how home loan taken for “buying” your dream home to stay

in it (SOP) can reduce the total tax payable by you.

Let’s assume you earn Rs 6,50,000 p.a. by way of salary and have taken a home loan of Rs

40,00,000 for buying your dream home and you have decided to stay in it. The home loan is for

a tenure of 20 years and the rate of interest is 9.0% p.a., the Equated Monthly Installments

(EMI) you need to pay is Rs 35,989.

Tax savings on account of home loan

Gross Annual Salary (Rs) 650,000

Loan Amount (Rs) 4,000,000

Tenure (yrs) 20

Rate of Interest p.a.( % ) 9.0

EMI (Rs) 35,989

Annual Interest Paid (Rs) 356,960

Principal paid in the 1st year (Rs) 74,908

Contributions towards tax-efficient instruments (Rs) 1,00,000

Tax paid without availing home loan benefits (Rs) 41,200*

Tax paid after availing home loan benefits (Rs) 20,600*

Tax Savings (Rs) 20,600*

(*tax calculated after giving effect for education cess)

(Source: Personal FN Research)

The above table clearly shows the benefit of availing a housing loan if you are contemplating

buying a house. The total tax payable on your income without a home loan works out to Rs

41,200. The same with a home loan works out to Rs 20,600, thus saving you Rs 20,600.

www.PersonalFN.com

40

Maximise your tax benefits

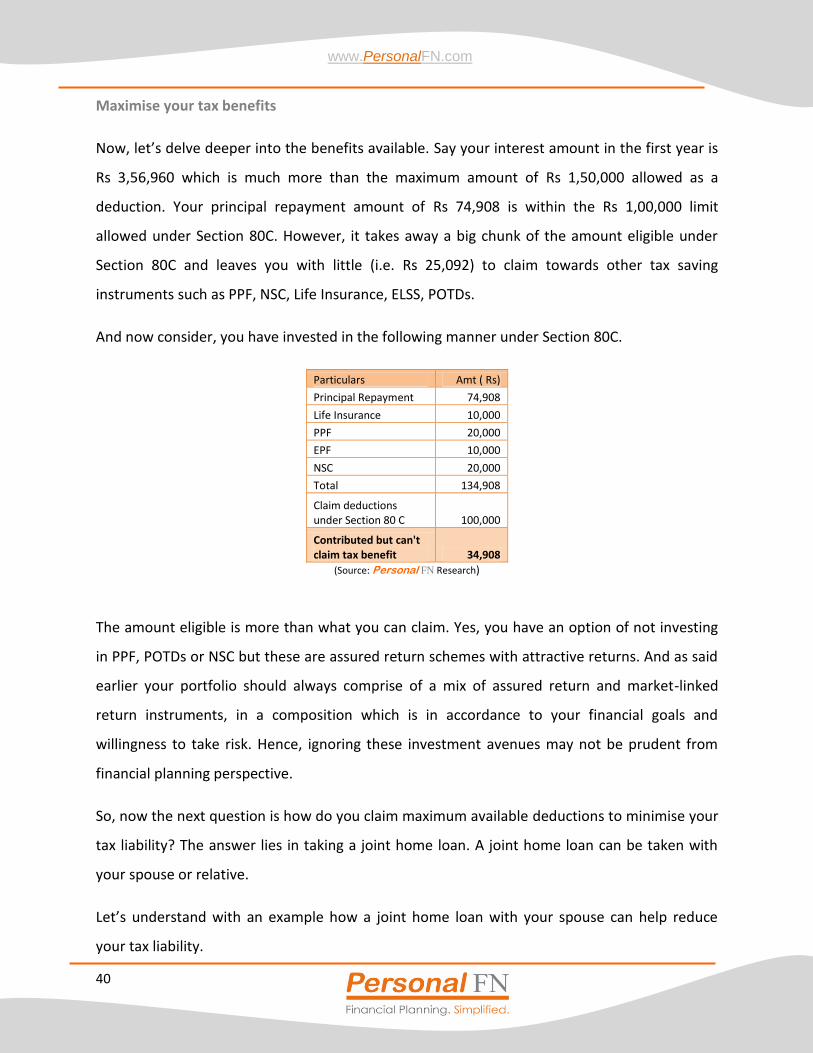

Now, let’s delve deeper into the benefits available. Say your interest amount in the first year is

Rs 3,56,960 which is much more than the maximum amount of Rs 1,50,000 allowed as a

deduction. Your principal repayment amount of Rs 74,908 is within the Rs 1,00,000 limit

allowed under Section 80C. However, it takes away a big chunk of the amount eligible under

Section 80C and leaves you with little (i.e. Rs 25,092) to claim towards other tax saving

instruments such as PPF, NSC, Life Insurance, ELSS, POTDs.

And now consider, you have invested in the following manner under Section 80C.

Particulars Amt ( Rs)

Principal Repayment 74,908

Life Insurance 10,000

PPF 20,000

EPF 10,000

NSC 20,000

Total 134,908

Claim deductions under Section 80 C 100,000

Contributed but can't claim tax benefit 34,908

(Source: Personal FN Research)

The amount eligible is more than what you can claim. Yes, you have an option of not investing

in PPF, POTDs or NSC but these are assured return schemes with attractive returns. And as said

earlier your portfolio should always comprise of a mix of assured return and market-linked

return instruments, in a composition which is in accordance to your financial goals and

willingness to take risk. Hence, ignoring these investment avenues may not be prudent from

financial planning perspective.

So, now the next question is how do you claim maximum available deductions to minimise your

tax liability? The answer lies in taking a joint home loan. A joint home loan can be taken with

your spouse or relative.

Let’s understand with an example how a joint home loan with your spouse can help reduce

your tax liability.

www.PersonalFN.com

41

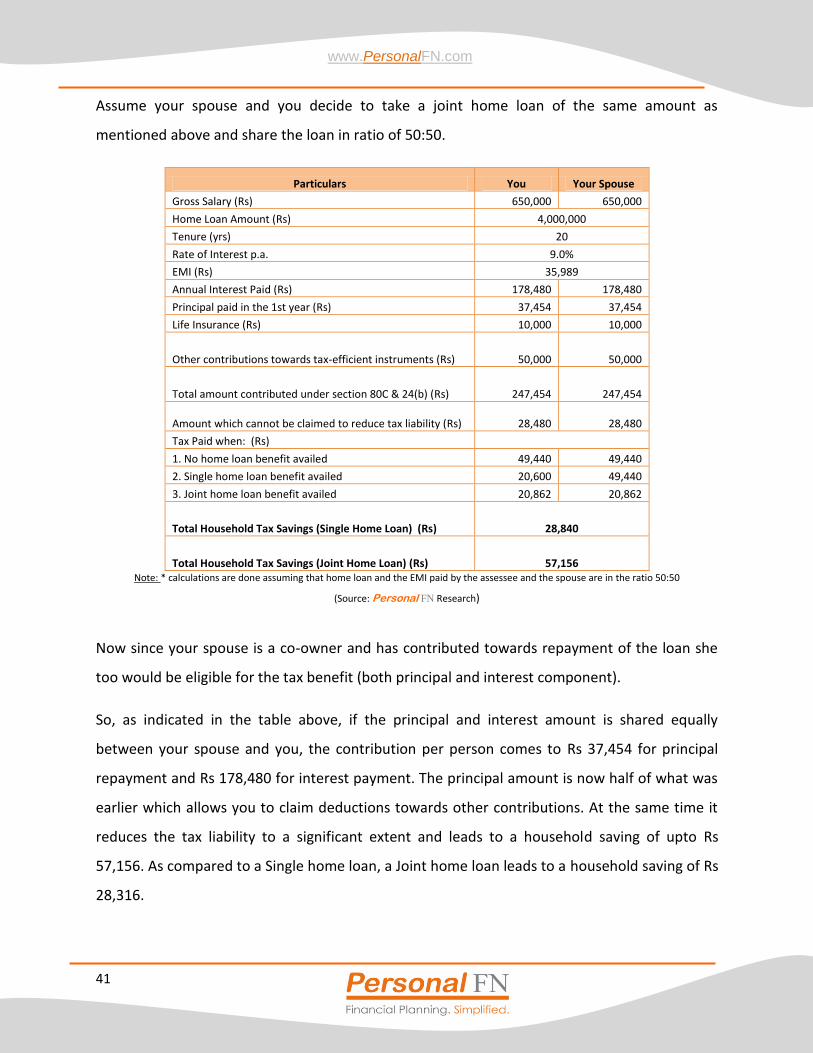

Assume your spouse and you decide to take a joint home loan of the same amount as

mentioned above and share the loan in ratio of 50:50.

Particulars You Your Spouse

Gross Salary (Rs) 650,000 650,000

Home Loan Amount (Rs) 4,000,000

Tenure (yrs) 20

Rate of Interest p.a. 9.0%

EMI (Rs) 35,989

Annual Interest Paid (Rs) 178,480 178,480

Principal paid in the 1st year (Rs) 37,454 37,454

Life Insurance (Rs) 10,000 10,000

Other contributions towards tax-efficient instruments (Rs) 50,000 50,000

Total amount contributed under section 80C & 24(b) (Rs) 247,454 247,454

Amount which cannot be claimed to reduce tax liability (Rs) 28,480 28,480

Tax Paid when: (Rs)

1. No home loan benefit availed 49,440 49,440

2. Single home loan benefit availed 20,600 49,440

3. Joint home loan benefit availed 20,862 20,862

Total Household Tax Savings (Single Home Loan) (Rs) 28,840

Total Household Tax Savings (Joint Home Loan) (Rs) 57,156 Note: * calculations are done assuming that home loan and the EMI paid by the assessee and the spouse are in the ratio 50:50

(Source: Personal FN Research)

Now since your spouse is a co-owner and has contributed towards repayment of the loan she

too would be eligible for the tax benefit (both principal and interest component).

So, as indicated in the table above, if the principal and interest amount is shared equally

between your spouse and you, the contribution per person comes to Rs 37,454 for principal

repayment and Rs 178,480 for interest payment. The principal amount is now half of what was

earlier which allows you to claim deductions towards other contributions. At the same time it

reduces the tax liability to a significant extent and leads to a household saving of upto Rs

57,156. As compared to a Single home loan, a Joint home loan leads to a household saving of Rs

28,316.

www.PersonalFN.com

42

From the tax planning point of view, it is vital to ensure that the higher earning member pays

higher portion of the home loan EMI. This is because the tax benefit accrues in proportion to

your contribution towards loan repayment.

So, remember if you plan to buy a house, it makes sense to include your spouse as a co-owner;

especially if your spouse’s income is taxable. This will result in higher tax saving in addition to

boosting your loan eligibility.

Additional benefit to first-time home buyers (Under Section 80EE)

In the union budget 2013-14, the finance minister introduced a new benefit for first time home

buyers looking for affordable houses. So individuals who have borrowed between April 01,

2013 and March 31, 2013 are entitled to get extra benefit in tax breaks. Besides, standard

deduction of upto Rs 1,50,000, such borrowers are now allowed to claim an additional

deduction of upto Rs 1,00,000 (U/S 80EE) for the interest payable on loan of less than Rs

25,00,000. Although this is a one-time benefit and it can be claimed over two Financial Years

(FYs) in piecemeal manner; i.e. one may claim benefit spreading it over FY 2013-14 and FY

2014-15.

Who is eligible?

Only individual assessees can claim the benefit and that too only if they do not own any

residential property before buying the one for which the tax benefits would be claimed.

Other conditions to avail benefit under section 80EE

- The assessee should be a first time home buyer, he does not own any other house on

the date of sanction and this house should be used for self-occupancy

- The value of residential house shouldn’t exceed Rs 40, 00,000

- Loan amount sanctioned shouldn’t exceed Rs 25,00,000 and is sanctioned in the FY

2013-14

- The loan must be obtained from a bank or a public listed company which has a main

objective for providing long term housing finance.

www.PersonalFN.com

43

VII - House Property and taxes

After showing benevolent side by providing you with the tax benefit, for availing a home loan

(to buy or construct or reconstruct or repair or renew), the Income Tax Act then eyes the

*house property owned by you for taxing the same. And this applies especially when you have

an income from let out property, or in case where you have more than one property which

aren’t let out on rent, but which are vacant (known as Deemed to be Let Out Property – DLOP).

*Owning a farm house, which forms a part of your agriculture income, is not brought under the tax net.

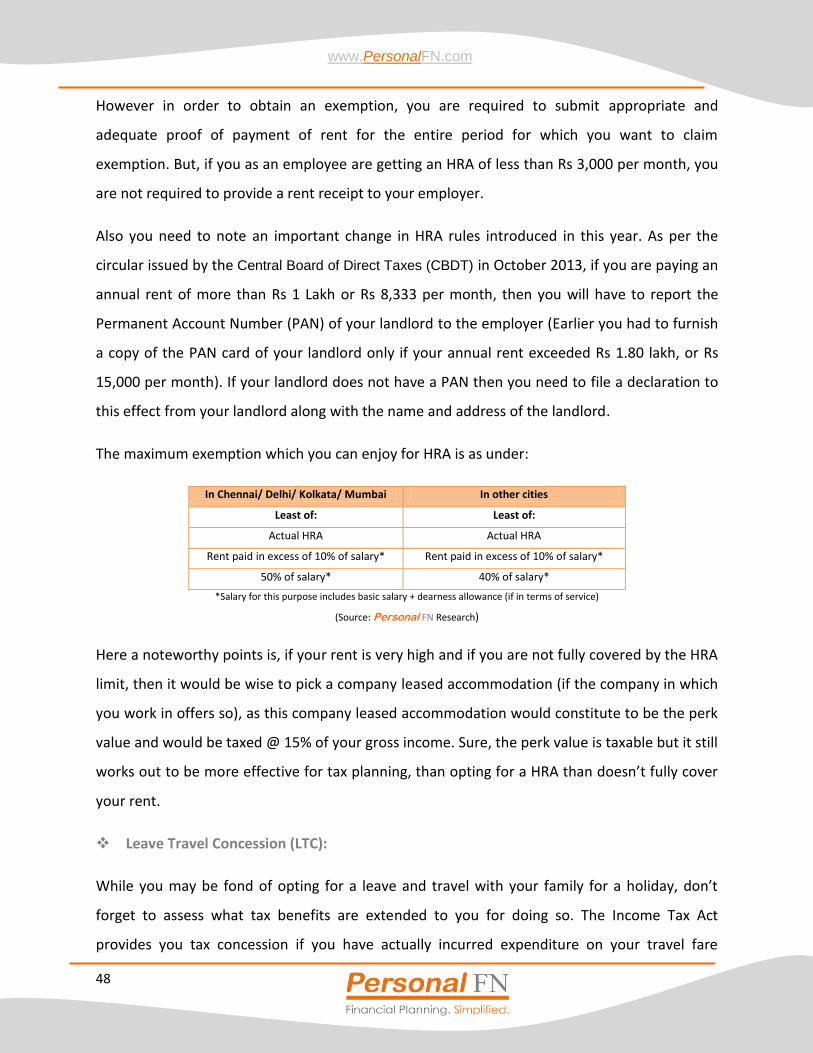

Now you may ask – “How can the income tax authority tax me, if I have not let out my property

on rent”?