tax investment reimbursement proofs 2016-17 tax... · driver salary child education allowance . 3...

TRANSCRIPT

1

FAQ’s

Tax Investment

&

Reimbursement Proofs

2016-17

2

Contents

INVESTMENT CLAIMS

HRA Exemption

Housing Loan

Section 80C – LIC, PPF, ULIP, Mutual Fund etc.

Section 80D – Medical Insurance

Section 80DD – Handicapped Dependents

Section 80E – Higher Education Loan

Section 80U – Disability

Section 80G – Donations

Previous Employment Declaration

General REIMBURSEMENT CLAIMS

Medical Reimbursement

Telephone Reimbursement

Leave Travel Reimbursement ( LTA)

Vehicle Reimbursement

Driver Salary

Child Education Allowance

3

HRA Exemption

Q1) Is format for rent receipt available in the ESS Portal? Ans. Yes, it is available in the ESS Portal. You can take print of it & get it filled up by landlord. Rent receipt should contain the address of the landlord and the property (Refer tax guidelines in ESS Portal for documents required). Q2) How can I submit the rent receipts for January, February and March? Ans. You can submit the rent receipts till December along with a declaration for future months. Q3) Can I claim rent paid for my family who are staying in a different location? Ans. Yes can be claimed provided your base location is the claiming location & rent is paid by you. However, you are required to claim only one rent payment in a month (base or current location) & rent receipt should be in your name. Q4) Can I submit photocopy of the rent receipts as proof? Ans. Photocopy of the rent receipts are not acceptable. You need to submit the original rent receipts. Q5) I am staying in hostel/PG. Can I submit hostel bill towards HRA exemption? Ans. Yes. You can submit the original hostel rent receipts to avail HRA exemption. Please note that only the amount paid towards the stay will be considered. Amount paid towards food and other services will not be considered. Q6) I have not declared against rent till now. However I am staying in the rented accommodation. Can I submit the original rent receipts? Ans. You can submit the original rent receipts and avail HRA exemption. HRA exemption will be given only if the amount is allocated against HRA in your CTC structure. Q7) Is there any format available to provide the declaration from the landlord in case of non-availability of PAN? Ans. Yes. Format is available in the ESS portal as a combination of Rent receipt format. Q8) What if I don’t provide the declaration from my landlord, will I still get HRA exemption? Ans. If the rent paid by you exceed Rs 8,333/ per month then it is mandatory to provide the landlord’s PAN & if no PAN then the self-declaration from the landlord is a must, without the declaration you will not get HRA exemption.

4

Housing Loan

Q1) What are the documents I need to submit in order to avail the tax benefits for housing loan? Ans. You need to submit Loan certificate issued by the financial institution with break-up of both interest and principal repayment for the current financial year (April 2016 to March 2017). Bank statement will not be construed as a proof for providing exemption. Q2) I have availed housing loan jointly (two or more names in the certificate). Am I required to submit any additional documents? Ans. Yes. It is mandatory to submit the Joint loan declaration form duly filled up. Sample format is available in ESS portal. In case of non-submission, % of exemption will be derived based on the number of Joint holders printed in the certificate. Q3) I will be taking possession/construction of flat/house in the next financial year. I am not able to enter the date details to avail housing loan benefits, Why? Ans. You can avail the tax benefits only after taking possession/construction of the flat/house by submitting the House completion certificate. Q4) In tax declaration page what date should I enter against Possession Date? Ans. Possession date is the date on which you have taken possession of the house from the builder after completion of construction. Q5) I will be submitting the online soft copy of the housing loan repayment statement. Is it valid? Ans. No, online statement is not accepted. However, online repayment certificate with the bifurcation of Interest & Principal is accepted as a valid proof. Q6) Can I claim exemption on the HRA as well as the interest paid on housing loans at the same time? Ans. Yes, subject to following conditions. HRA & Self Occupied exemption cannot be claimed simultaneously. However, in the case of deemed let-out property, annual rent value to be taken as market rent value of the location of property. Only deduction is on account of interest on housing loan, which is restricted to a maximum of Rs 200,000/-. (If the loan is taken before 1st April 1999, the maximum amount allowed is 30,000/- or else 200,000/-).

5

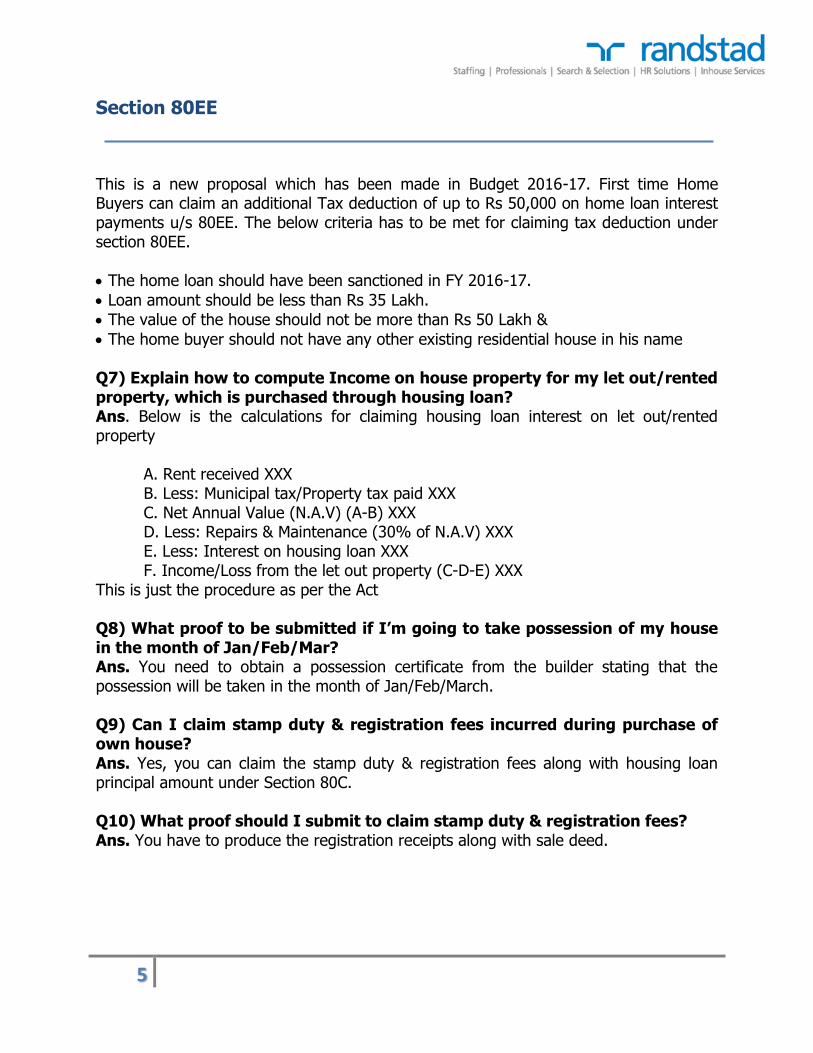

Section 80EE

This is a new proposal which has been made in Budget 2016-17. First time Home Buyers can claim an additional Tax deduction of up to Rs 50,000 on home loan interest payments u/s 80EE. The below criteria has to be met for claiming tax deduction under section 80EE.

The home loan should have been sanctioned in FY 2016-17.

Loan amount should be less than Rs 35 Lakh.

The value of the house should not be more than Rs 50 Lakh &

The home buyer should not have any other existing residential house in his name Q7) Explain how to compute Income on house property for my let out/rented property, which is purchased through housing loan? Ans. Below is the calculations for claiming housing loan interest on let out/rented property

A. Rent received XXX B. Less: Municipal tax/Property tax paid XXX C. Net Annual Value (N.A.V) (A-B) XXX D. Less: Repairs & Maintenance (30% of N.A.V) XXX E. Less: Interest on housing loan XXX F. Income/Loss from the let out property (C-D-E) XXX

This is just the procedure as per the Act Q8) What proof to be submitted if I’m going to take possession of my house in the month of Jan/Feb/Mar? Ans. You need to obtain a possession certificate from the builder stating that the possession will be taken in the month of Jan/Feb/March. Q9) Can I claim stamp duty & registration fees incurred during purchase of own house? Ans. Yes, you can claim the stamp duty & registration fees along with housing loan principal amount under Section 80C. Q10) What proof should I submit to claim stamp duty & registration fees? Ans. You have to produce the registration receipts along with sale deed.

6

Section 80 C Benefits

Q1) Can I claim the benefit of life insurance premium, which falls due in February/March? Ans. Yes, the benefit for premium payable from 16th February 2016 to 31st March 2016 will be given provided you declare it in 80C Projections and produce a copy of the last year receipt. Q2) Can I claim the Life insurance premium paid for my parents/sister/brother u/s 80C? Ans. No, Insurance premium paid for self/spouse/children alone are eligible for deduction u/s 80C. If spouse is claiming the tax benefit, then it is not eligible for deduction u/s 80C. Q3) Will the late fee paid on premium eligible for tax deduction? Ans. No, it is not eligible for tax deduction. Q4) What are the documents that need to be submitted against the life insurance premium paid? Ans. You can submit photocopy of current year FY 2016-17 life insurance premium receipt (online receipt is also accepted) or annual statement issued by your insurer with all the necessary details. Q5) I have recently taken the insurance and I am yet receive the First Premium Receipt. Can I submit copy of the proposal deposit receipt? Ans. Copy of the proposal deposit receipt is not adequate. You need to submit the copy of the first premium receipt to consider as a proof. Q6) Can you brief out on tax benefits available on investment under National Savings Certificate (NSC)? Ans. Subscription in the name of SELF to NSC issued by postal department is eligible for tax benefit u/s 80C. Q7) Can I declare NSC accrued interest u/s 80C for tax benefits? Ans. Yes, NSC accrued interest will be considered for tax benefit u/s 80C. However, note that such amount will also be taken as other income in your tax computation. Q8) Is the amount invested in mutual funds eligible for deduction u/s 80C? Ans. All mutual funds investments are NOT eligible for tax benefits. Only investments in equity-linked saving schemes (ELSS) and pension plans get deduction u/s 80C within the overall limit of Rupee 1.5 lakh a year.

7

Q9) I am yet to receive the account statement from the Mutual Fund. Can I submit the acknowledgement receipt issued by the Mutual Fund as a proof? Ans. Acknowledgement receipt issued by the Mutual Fund is not adequate. It is mandatory to submit the statement issued by the respective Mutual Fund Company to consider as a proof. Q10) I am investing Systematic Investment Plan (SIP) on a monthly/quarterly basis. How can I submit the proof for the remaining periods of this Financial Year (FY 2016-17)? Ans. Yes, the benefit for premium payable from 21st February 2016 to 31st March 2016 will be given provided you declare it in 80C Projections and produce a copy of the last year receipt. Q11) What are the documents that need to be submitted against Public Provident Fund (PPF)? Ans. You can submit current year investment receipt along with the photocopy of passbook covering page, which displays your name and account no, and transactions for this financial year 2016-17. Investments made in the name spouse/children will also be considered. Q12) Can I claim the tax benefit for the PPF invested in the name of my family members under section 80C? Ans. Yes, it is restricted to your spouse and children only. However, declaration to the effect from the Spouse / Children is required mentioning that they will not claim the benefit. Q13) I have Post office Recurring Deposits can I claim tax exemption u/s 80C? Ans. Post office Recurring Deposit is not considered for tax exemption as per Income tax act. Q14) What are the documents that need to be submitted against Pension Plan Premium paid u/s 80C? Ans. You can submit photocopy of current year FY 2016-17 insurance premium receipt or annual statement issued by your insurer. Q15) Where to declare PF deducted through pay slip in tax declaration page to avail tax exemption? Ans. PF deducted through pay slip will be automatically considered for exemption u/s 80C. You need not have to declare it or provide any supporting for the same separately.

8

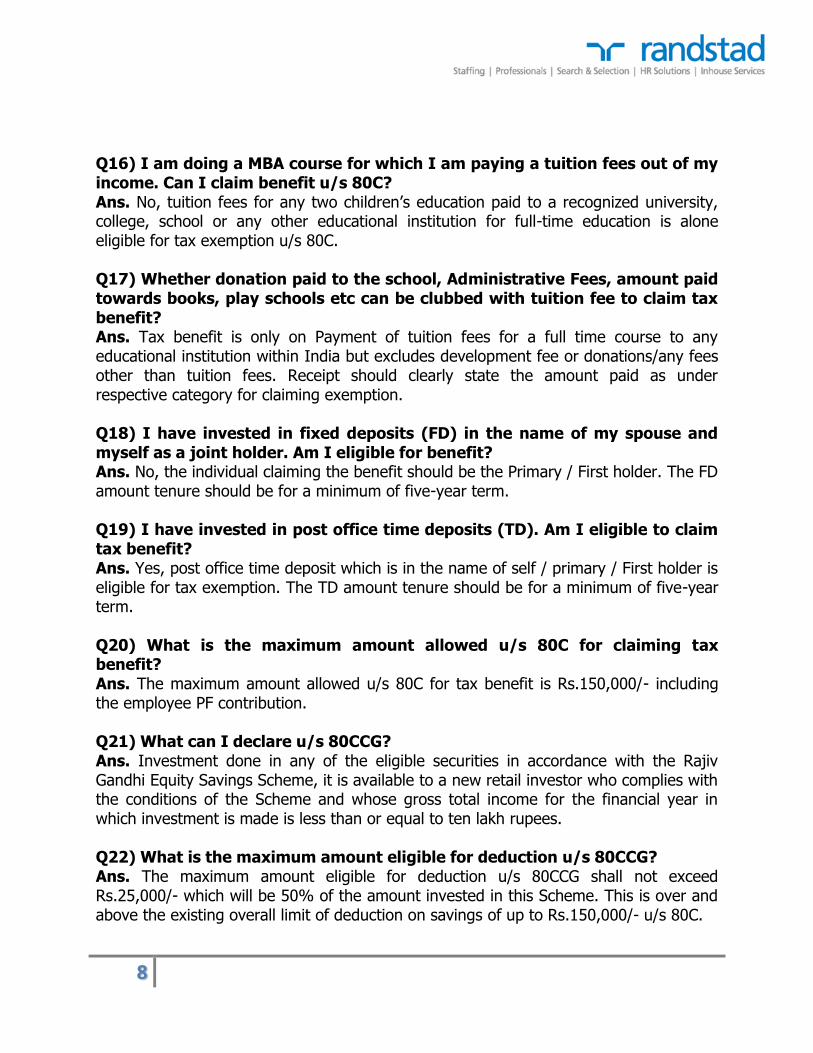

Q16) I am doing a MBA course for which I am paying a tuition fees out of my income. Can I claim benefit u/s 80C? Ans. No, tuition fees for any two children’s education paid to a recognized university, college, school or any other educational institution for full-time education is alone eligible for tax exemption u/s 80C. Q17) Whether donation paid to the school, Administrative Fees, amount paid towards books, play schools etc can be clubbed with tuition fee to claim tax benefit? Ans. Tax benefit is only on Payment of tuition fees for a full time course to any educational institution within India but excludes development fee or donations/any fees other than tuition fees. Receipt should clearly state the amount paid as under respective category for claiming exemption. Q18) I have invested in fixed deposits (FD) in the name of my spouse and myself as a joint holder. Am I eligible for benefit? Ans. No, the individual claiming the benefit should be the Primary / First holder. The FD amount tenure should be for a minimum of five-year term. Q19) I have invested in post office time deposits (TD). Am I eligible to claim tax benefit? Ans. Yes, post office time deposit which is in the name of self / primary / First holder is eligible for tax exemption. The TD amount tenure should be for a minimum of five-year term. Q20) What is the maximum amount allowed u/s 80C for claiming tax benefit? Ans. The maximum amount allowed u/s 80C for tax benefit is Rs.150,000/- including the employee PF contribution. Q21) What can I declare u/s 80CCG? Ans. Investment done in any of the eligible securities in accordance with the Rajiv Gandhi Equity Savings Scheme, it is available to a new retail investor who complies with the conditions of the Scheme and whose gross total income for the financial year in which investment is made is less than or equal to ten lakh rupees. Q22) What is the maximum amount eligible for deduction u/s 80CCG? Ans. The maximum amount eligible for deduction u/s 80CCG shall not exceed Rs.25,000/- which will be 50% of the amount invested in this Scheme. This is over and above the existing overall limit of deduction on savings of up to Rs.150,000/- u/s 80C.

9

Section 80D – Medical Insurance / Mediclaim

Q1) What are the documents that need to be submitted as a proof against Medical Insurance? Ans. You can submit copy of the premium receipt issued by the insurer. Note that only the actual premium paid by any mode other than cash will be considered and service tax will not be considered for tax benefit. The premium amount paid on self/parents/spouse/children can be claimed deduction u/s 80D. Q2) What is the maximum amount allowed u/s 80D for claiming tax benefit? Ans. The maximum amount allowed u/s 80D for tax benefit is for self, spouse & children Rs.15,000/ & additional for parents Rs.15,000/- & in case of senior citizens it is Rs.20,000/.

Section 80DD – Handicapped Dependant

Q1) Can I claim for my handicapped Father/Mother/ Brother/Sister u/s 80DD, who is my dependent? Ans. Yes. You can claim by submitting Form 10 IA certificate issued by a government recognized doctor. Q2) Can I claim for my handicapped Niece/Nephew u/s 80DD, who is my dependent? Ans. No. As per IT rules they cannot be treated as your dependent for claiming the tax benefits. Q3) What are the relevant documents I need to submit for claiming 80DD tax benefits? Ans. Certificate (Form 10 IA) from a government recognized doctor regarding the percentage of disability of the dependent and a declaration from the employee stating the relationship of the disabled & amount spent towards the maintenance should be submitted as proof for 80DD. Q4) What is the maximum amount I can claim under section 80DD? Ans. If the percentage of disability is 40% and above then you are eligible to claim Rs.75,000/-, if the percentage of disability is 80% and above then you can claim up to 1,25,000/-.

10

Section 80E – Education Loan

Q1) What is the maximum amount of interest on education loan u/s 80E? Ans. Interest payment without any limit on education loan will qualify for exemption u/s 80E. You need to enter the interest amount you would be paying for the financial year 2016-17. The bank certificate giving the breakup of interest and principal repayment along with the self-declaration form should be submitted as proof. Q2) I am repaying the education loan taken for my younger brother. Can I claim tax benefits u/s 80E? Ans. No, repayment of education loan in the name of self/spouse/children/legal guardian alone qualifies for exemption. Loan taken for your brother does not qualify for exemption.

Section 80U – Self Physical Disability

Q1) What are the documents I need to submit in order to avail the tax benefits u/s 80U? Ans. Certificate (Form 10 IA) from a government recognized doctor regarding the percentage of disability should be submitted as proof for 80U. Q2) What is the maximum amount I can claim under section 80U? Ans. If the percentage of disability is 40% and above then you are eligible to claim Rs.75,000/-, if the percentage of disability is 80% and above then you can claim up to 1,25,000/-.

Form 12C – Previous Employment

Q1) What do you mean by previous employer salary? Why should I declare my previous employer salary details? Ans. Previous employer salary means gross salary earned during the tenure from 1st April 2016 to your last working day in your previous organization. Previous employer income is required to arrive at proper tax computation by considering the total salary earned as well as the total tax paid for the entire financial year. (FY- 1st Apr 2016 to 31st Mar 2017) Q2) What are the documents that need to be submitted towards tax proof towards previous employment? Ans. You need to submit copy of the Form 16 or attested tax computation sheet issued by your previous employer along with Form – 12B (Form 12B is a declaration given by

11

employee to present employer about his previous salary details incase he is not able to submit copy the form 16). Q3) My previous employer has not yet issued the Form 16. Can I submit any other alternative documents? Ans. If Form 16 is not available, then you can submit attested tax computation sheet and full & final settlement issued by your previous employer along with the Form 12B. Q4) What are the details will be considered from the form 16 / tax computation sheet about previous employment? Ans. We will be considering only salary after section 10, profession tax, provident fund and income tax deducted from the documents. The following details need to be provided in Form 12B in the front page:

Total Salary; Salary after Section 10; Profession Tax; PF Contribution; Income Tax Deducted (TDS)

Note that proofs submitted with the Previous employer need not be submitted again Q5) Will tax be deducted if I declare the amount earned from the previous employer. Ans. Tax Liability will be calculated after clubbing the income of the previous employer with the income of the current company after reducing the tax deducted from previous employer, if any. Q6) I have not declared my previous employer income; will there be any impact of the Tax? Ans. Yes. There will be tax implications when both the income will be clubbed at the time of filing your annual return (ITR). You should declare the previous employer income in your tax declaration page & provide the necessary proofs.

Other General Questions on Proof submission

Q1) Should I submit the original copy of all the supporting documents for as a proofs? Ans. No, Reimbursement bills (Including rent receipt ) should be provided in original, rest for all other investments supporting document’s photocopy can be provided.

Q2) What happens if I don’t provide the investment supporting proofs for tax before the cutoff date? Ans. Tax will be calculated without considering the investment declared by you and respective tax will be deducted in February and March.

Q3) How should I submit the supporting documents for investment proofs?

12

Ans. The investment proofs should be submitted to the Tax Team Chennai. (Address – Ms.Preethi Karunakaran, Randstad India Pvt Ltd , 'RANDSTAD HOUSE', 3rd Floor, Old No.5 & 5A,new No.9, Pycrofts Garden Road, Chennai 600 006.)

Q4) I am at onsite. Can I submit the documents once I am back to India? Ans. No, you need to submit the tax proof within the specified timelines. You can request your family Member/Friends/Colleagues to submit the tax proofs on your behalf. Alternatively you can courier the tax proof to tax team within the specified timelines.

Q5) I am at home due to health reasons. Can I submit the tax proof once I have joined back the office (i.e. after the cut-off date)? Ans. No, you need to submit the tax proof within the specified timelines. You can request your family Member/Friends/Colleagues to submit the tax proofs on your behalf. Alternatively you can courier the tax proof to tax team within the specified timelines.

Q6) What will happen if I resign from the company, whom should I handover the proofs? Ans. In case, you are resigning from the services of the company, you should submit the proofs directly to the Full and Final settlement department before the last working day. (Address – Mr Vijaya Sandeep, Randstad India Pvt Ltd , 'RANDSTAD HOUSE', 3rd Floor, Old No.5 & 5A,new No.9, Pycrofts Garden Road, Chennai 600 006.)

Q7) Which year investment proofs can I claim for tax benefit? Ans. The investment proofs done during the respective income tax financial year April’15 to March’16 can be claimed the tax benefit.

Q8) I am paying annually premium against my house & car insurance, can I claim the same for tax benefit? Ans. No, house & car insurance is not covered for deduction u/s 80C.

13

Medical Reimbursement

Q1) What is the maximum exemption limit to claim medical reimbursement?

Ans. Maximum limit is Rs.15000/-p.a or to the extent of reimbursement provided in salary whichever is lower.

Q2) What are the bills that can be claimed under medical reimbursement?

Ans. Medical expenditure incurred during the normal course can be claimed but will not include Medical insurance premium, expenses towards cosmetics, baby care & non-medical expenses.

Q3) Can I submit medical bills in my spouse name?

Ans. Yes. You can submit medical bills in the name of your family members. Declaration of the dependent which is available in ESS portal needs to be submitted for claiming the same.

Q4) Can mediclaim insurance premium be claimed under medical reimbursement?

Ans. No, the mediclaim insurance premium can be claimed only under sec 80D. Any submission of Mediclaim under medical reimbursement will be rejected & will not be considered for exemption.

14

Telephone Reimbursement

Q1) What is the maximum exemption limit to claim telephone reimbursement?

Ans. Telephone Reimbursement is exempted the extent of amount provided in your CTC Structure or bills approved value whichever is lower.

Q2) Can I submit telephone exemption in the name of my family member?

Ans. No. Telephone exemption is not eligible family members. Bills should be name of the employee only.

Q3) Can I claim telephone reimbursement for more than one number?

Ans. Yes, you can claim for maximum of two numbers. It can be either landline, mobile or Broadband.

Q4) Can I claim the DTH expenses for exemption under Telephone reimbursement?

Ans. No. DTH expenses are not eligible to be claimed as exemption.

Q5) How can I submit a proof for prepaid mobile recharge?

Ans. You may submit the recharge statement in case of Online transactions or you need to submit the recharge voucher with the retailer details clearly mentioning your name & recharged number for claiming exemption.

Q6) What are the documents to be submitted for telephone reimbursement?

Ans. Original bills of Landline, Mobile or Broadband connection in your name can be accepted as proofs.

15

Leave Traval Reimbursement ( LTA)

Q1) What is the amount that can be claimed for LTA?

Ans. LTA is a benefit provided by the employer. Maximum amount of exemption is the LTA as mentioned in your CTC. However, exemption is provided only the extent of bills provided or amount in CTC whichever is lower.

Q2) When an employee can claim LTA?

Ans. An employee can claim LTA for 2 years in a block of 4 block years as non-taxable & remaining 2 claims will be taxable.

Q3) What is a block year in LTA?

Ans. Income tax rules define block year for claiming LTA. Current block is 2014-2017.

Q4) How a year is defined by IT rules for claiming LTA?

Ans. For the purpose of LTA, Income tax act clearly mentions it as calendar year viz., 1st Jan to 31st Dec of the respective year.

Q5) How many trips an employee is eligible to claim for claiming LTA?

Ans. The employee can claim LTA for only one trip in a year. One cannot claim multiple trips in a year to claim LTA.

Q6) If an employee does one trip, but visits multiple places, is he eligible to claim LTA?

Ans. Income tax rule indicates that LTA can be claimed for the shortest distance between the starting point and farthest point. In between, if there are more places to visit, you can do that & the exemption will be limited to the extent of 1st AC train fare on the shortest distance for the farthest point.

Q7) Who is eligible to travel along with employee to get LTA benefit?

Ans. The employee can take his spouse, kids and dependent parents, dependent brother or sister as part of travel to claim LTA benefit.

16

Q8) How many kids are eligible to travel to get LTA benefit?

Ans. The exemption will not be available to more than 2 surviving children of an individual born after 01.10.1998. This restriction shall not apply in respect of children born before 01.10.1998 and also in case of multiple births after one child. It may be noted that section 2 (15B) of the Act defines a child as includes a step child and an adopted child of the individual.

Q9) Can I claim LTA by travelling abroad trip?

Ans. LTA can be claimed for travel taken within India. You cannot claim foreign trip expenses for LTA benefit.

Q10) What expenses can be claimed under LTA Benefit?

Ans. LTA can be claimed only for ticket cost from starting point to the destination point and vice versa. One cannot claim food expenses, lodging expenses and other miscellaneous expenses under LTA claim.

Q11) What mode of travel is eligible for claiming LTA?

Air - Economy Air fare of national carrier by shortest route to the place of destination (In case the travel is by private carrier, restriction will be limited to the extent of air fare of National carrier whichever is less)

Rail - 1st class AC by shortest route to the place of destination. Other modes - 1st class AC or the amount spent

whichever is less will be exempt

Q12) If an employee travel at the end of the year and returns from a trip which falls beyond 31st Dec, how does it work?

Ans. In such case, employee needs to consider starting date as a basis and claim for that calendar year. No exemption of such claim is possible in the current year.

Q13) Do I need to submit a single bill for our trip or multiple bills would be accepted for LTA?

Ans. LTA benefit is given for a trip. Means, one family is travelling. Ideally, there would be one bill. However, there are cases where multiple bills would be received for a single trip (for airfare bills, where a family member agreed to join later and the booking was made later, but travel date is same of the remaining members). In such case, if the dates are same bills can be accepted for exemption.

17

Vehicle Reimbursement

Q1) What is the exemption limit for Vehicle Reimbursement? Ans. Where vehicle is owned by the employee, used partly for official and partly for personal and running charges are borne by employer, exemption can be claimed based on nature of vehicle:

If cubic capacity of the car is below 1.6 liters i.e. 1600CC, expenses for use of the

car are considered at the rate of Rs. 1,800/- p.m.

If cubic capacity of the car is above 1.6 liters i.e. 1600CC, expenses for use of the

car are considered at the rate of Rs. 2,400/- p.m Q2) What are the documents to be provided to claim exemption?

Undertaking that the employee owns the said vehicle RC book copy to verify capacity of the vehicle along with fuel / Repairs &

maintenance / Insurance bills Q3) Can I claim exemption if RC book is in my spouse or family member name? Ans. Your spouse or family member should provide a declaration that you are using the vehicle for official purpose in order to provide exemption. Q4) Will exemption be provided in case RC book is not available? Ans. If RC book copy is not provided, vehicle will be deemed to be under <1600 CC category but you need to provide a self-declaration that RC book is missing & you are using the vehicle for official purpose.

18

Driver’s Salary

Q1) Can I claim the salary paid to my driver for tax exemption? Ans. Yes. You can claim the exemption but will be restricted to the extent of Rs, 900/- p.m. Q2) What are the relevant documents to claim exemption? Ans. Driver's salary voucher (one per quarter) in prescribed format to be submitted as proof. (Sample format is available in ESS portal).

Child Education Allowance

Q1) What is the maximum amount of Child education allowance u/s 10? Ans. Fixed education allowance received from employer is exempted from tax to the extent of Rs. 100 per month for maximum of 2 children

Q2) What are the relevant documents I need to submit for claiming child education allowance tax benefits? Ans. Duly filled in Declaration form should be submitted as proof (Sample format is available in ESS portal). Q3) Where should I mention about the children details to claim exemption? Ans. You need to declare the number of children in the Reimbursement page available in ESS portal. Q4) If the child education allowance not provided in my CTC will I get the tax benefit? Ans. No, this exemption will be based on you CTC structure.

HAPPY LEARNING