tax implications of acquisition financing - … implications of ... a acquisitions, financing &...

TRANSCRIPT

TAX IMPLICATIONS OF ACQUISITION FINANCING

Post-Acquisition Debt Consolidation and

Interest Deduction Limitations in Germany in Comparison to the United States and France

A thesis submitted to the Bucerius/WHU Master of Law and Business Program in partial fulfillment of the requirements for the award of the Master of Law and Business (“MLB”) Degree

Dominik Pavlik July 22, 2011

14.227 words (excluding footnotes)

Supervisor 1: Florian Lechner Supervisor 2: Prof. Dr. Deborah Schanz

I

TABLE OF CONTENTS

LIST OF ABBREVIATIONS ............................................................................ III

LIST OF DIAGRAMS ...................................................................................... IV A ACQUISITIONS, FINANCING & TAXATION – AN INTRODUCTION .............. 1 I Relationship Between Acquisitions and Taxation – Empirical Evidence .... 1 II The Acquisition ................................................................................................ 3 III Financing an Acquisition ............................................................................... 4

1 Cash Financing .............................................................................................. 5 2 Equity Financing ............................................................................................. 7

IV Scope of the Following Chapters .................................................................. 8 B GERMANY ...................................................................................................... 10 I Debt Consolidation ......................................................................................... 10

1 Mergers ........................................................................................................ 10 2 Tax Consolidation ........................................................................................ 12 3 Debt Push-Down .......................................................................................... 12

II The Interest Barrier ....................................................................................... 14 1 Business Tax Reform 2008 .......................................................................... 15 2 Background .................................................................................................. 15 3 The New Interest Barrier .............................................................................. 17

a Group Independence ............................................................................................ 19 b Escape Clause ..................................................................................................... 20

4 Impact on Acquisition Financing .................................................................. 20 5 Efficient Structuring in Light of the Interest Barrier ....................................... 21

a Realization of Hidden Reserves ........................................................................... 23 b Variable Interest Expenses and Debt-to-Equity Swap ......................................... 24 c Accounting Measures ........................................................................................... 25

C UNITED STATES ............................................................................................. 26 I Debt Consolidation ......................................................................................... 26

1 Mergers ........................................................................................................ 26 2 Tax Consolidation ........................................................................................ 27 3 Debt Push-Down .......................................................................................... 28

II Earnings-Stripping Rules ............................................................................. 29 1 Background .................................................................................................. 30 2 Application .................................................................................................... 31 3 Impact on Acquisition Financing .................................................................. 35 4 Efficient Structuring in Light of the Earnings-Stripping Rules ....................... 36

a Debt-to-Equity and Adjusted Taxable Income Optimization ................................. 36 b Debt Push-Down .................................................................................................. 37

D FRANCE .......................................................................................................... 38 I Debt Consolidation ......................................................................................... 38

1 Mergers ........................................................................................................ 38 2 Tax consolidation ......................................................................................... 40 3 Debt push-down ........................................................................................... 41

II

II Thin Capitalization Rule ................................................................................ 41 1 Background .................................................................................................. 43 2 Application .................................................................................................... 44 3 Impact on Acquisition Financing .................................................................. 47 4 Efficient Structuring in Light of the Thin Capitalization Rule ........................ 48

E CONCLUSION ................................................................................................. 50

Bibliography ................................................................................................. 53

III

LIST OF ABBREVIATIONS AG Aktiengesellschaft (Germany)

CGI Code Général des Impôts (France)

CIT Corporate Income Tax

DTT Double Tax Treaty

EBITDA Earnings Before Interest, Taxes, Depreciation and Amortization

EC European Community

EEA European Economic Area

EStG Einkommensteuergesetz (Germany)

EU European Union

GewStG Gewerbesteuergesetz (Germany)

GmbH Gesellschaft mit beschränkter Haftung (Germany)

HGB Handelsgesetzbuch (Germany)

IFRS International Financial Reporting Standards

IRC Internal Revenue Code

IRS Internal Revenue Service

KStG Körperschaftsteuergesetz (Germany)

PIT Personal Income Tax

Sec. Section

SEC Securities and Exchange Commission

TT Trade Tax

UmwStG Umwandlungssteuergesetz (Germany)

U.S. United States

U.S.-GAAP United States Generally Accepted Accounting Principles

WHT Withholding Tax

IV

LIST OF DIAGRAMS Diagram 1: Acquisition Scenario p. 8

Diagram 2: Interest Barrier Applicability Test p. 22

Diagram 3: Earnings-Stripping Rule Applicability Test p. 32

Diagram 4: Thin Capitalization Rule Applicability Test p. 44

Diagram 5: Back-to-Back Arrangements and Secured

Third Party Loans p. 45

1

A ACQUISITIONS, FINANCING & TAXATION – AN INTRODUCTION

I Relationship Between Acquisitions and Taxation – Empirical

Evidence

Tax optimization plays an important role for organizations. Hence, it also plays

an important role in relation to M&A transactions.1 Furthermore, empirical

studies point to to the importance of considering taxes when planning M&A

transactions.2 On one hand, taxes can be beneficial in a tax environment,

allowing tax savings and thereby a decrease in the acquisition price. On the

other hand, where no such benefit is provided by the relevant legislation,

taxes increase the total cost of the transaction, limiting the potential economic

advantage, and may even jeopardize the actual transaction.

For the acquirer, the most important tax consideration in relation to

acquisitions is the possibility of deductible expenses – deduction of the

acquisition price and the financing costs.3 The target, on the other hand, aims

to compensate its tax burden by increasing the sales price. As a result, taxes

may create challenges and even hinder the deal from going though. This is

particularly the case in acquisition scenarios where the tax burden of the

seller and the potential for tax savings of the acquirer are not in equilibrium.4

In such cases, the motivation of the acquirer to compensate the seller’s tax

burden by paying a higher price is likely to be limited, unless the acquisition is

based on other more valuable intentions.

Most of the empirical studies conducted in this area focus on the U.S.

market.5 All of the studies concentrate on three aspects of the relationship

between taxes and acquisitions: First, the relationship and effect of taxes on

1 See Schreiber & Ruf, p. 435. 2 See Desai & Hines; Becker & Fuest 3 See Schreiber and Ruf, p. 437. 4 See Schreiber and Ruf, p. 438. 5 See Schreiber and Ruf, p. 435.

2

the acquisition price; second, whether taxes hinder economically useful

acquisitions or may be a reason for acquisitions to take place; and third, the

aim to prove the existence of a relationship between tax planning activities

and acquisitions. 6

One important finding regarding the effect of tax on the acquisition price was

that the acquirer, in most cases, is not able to compensate its tax burden by a

lower price, whereas the seller can.7 An additional study in this area of

research proves that sellers will increase the acquisition price if they face an

increasing tax burden by having to pay capital gains tax.8 Thereby this study

supports the findings of the previous one on the effect and relationship

between tax and price.9

Empirical studies have proven that the existence of taxes deter economically

useful mergers and acquisitions. Ayers, Lefanowicz and Robinson performed

one of the most convincing studies in this area in 2007.10 Their analysis

focused on the number of taxable M&A transactions in times of low and high

taxation on capital gains. The results showed a decrease in the number of

M&A transactions in times of high capital gains taxes.11 In combination with

previously performed studies12 there is convincing evidence “that taxes inhibit

economically useful transactions”13.

Studies concentrating on tax planning activities in relation to acquisitions

found that the likelihood of debt financing increases if the acquirer faces a

higher tax rate since the tax savings grow.14 Other researchers who extended

the study by analyzing 167 acquisitions found that the lower an acquirer’s

possible tax deduction rate, the lower the level of debt financing.15 Further

6 See Schreiber & Ruf, p. 438. 7 See Henning, Shaw & Stock (2000). 8 See Schreiber & Ruf, p. 440. 9 See Ayers, Lefanowicz & Robinson (2004). 10 See Schreiber & Ruf, p. 447. 11 See Ayers, Lefanowicz & Robinson (2007). 12 See Scheider & Ruf, pp. 444 ff. 13 Schreiber & Ruf, p. 447 (autor’s translation). 14 See Erickson (1998). 15 See Dhaliwal, Newberry & Weaver (2005).

3

studies came to the conclusion that acquisitions are not limited to tax efficient

structuring. In addition, acquisitions provide long-term tax savings if they are

used as a means of tax planning.16

II The Acquisition

The acquisition of a company can take place in two ways: by means of an

asset or a share deal. In an asset deal, the acquirer receives the title to the

targeted assets after consideration has been given. Where a transaction is

performed as a share deal, instead of title to the assets the acquirer receives

the target’s shares after consideration has been given.

From a tax perspective, an asset deal is generally advantageous for the

acquirer because of the possibility of an accounting step-up. The higher tax

basis allows an increase in the depreciation and amortization expenses which

can be used as a deduction measure to lower the tax base and thereby the

future tax burden. Consequently, in cases where the target has many

undervalued assets in its balance sheet, an asset deal may be the right form

of acquisition.

On the other hand, the asset deal has two disadvantages for the acquirer.

First, transfer taxes may be applicable to all or specific types of transferred

assets. To limit the additional costs resulting from transfer tax, the acquirer

should analyze to which assets transfer tax is applicable and whether a share

deal may be more favorable, taking future tax savings due to a potential step-

up into account. Another possibility is to negotiate with the seller who pays the

applicable transfer taxes. Second, tax credits resulting from the target’s past

net operating losses may not be carried forward. Accordingly, in cases of

targets with high tax credits, an acquisition by means of a share deal may be

preferable to the acquirer.

From the seller’s perspective, these tax credits are the main advantage of an

asset deal as “such tax considerations remain with the holders of the target

16 See Schreiber & Ruf, p. 444.

4

firm’s stock”17. In other words, if the target continues operating after the asset

sale, the tax credits can still be used.

The tax disadvantage of an asset deal for the seller is the taxation on gains

arising from the sale. Thus, the lower the book values in comparison to the

current market values, the higher the taxable gains of the target. This may

create conflicts between the acquirer and the target as the acquirer may favor

an asset deal in cases which allow a high post-acquisition step-up, while the

target is likely to prefer a share deal in such cases. Furthermore, if the target’s

shareholders intend to liquidate the business after the transaction, depending

on the legal form of the entity, they might even be subject to double taxation.

The sales gain will be taxed on the level of the business, and the

shareholders’ capital gain will be taxed.

Besides the form of the acquisition, the acquirer and the target have to agree

on all the other structural aspects of the transaction. These include their goals

and future plans, the amount of risk they are willing to take, the price they are

willing to pay / to accept, the exact stake in the company they are willing to

acquire / to give up, and whether or not approval will be needed to go forward

with the transaction. When each of the parties has found a clear position on

all of these aspects, including the form, the parties must reach consent to

finally structure the acquisition. Doing so, an in-depth evaluation of each

aspect – taking into account the overall transaction – is of great importance as

“decisions made in one area affect other aspects of the overall deal

structure”18. This includes additional costs due to a higher tax burden resulting

from the chosen acquisition structure.

III Financing an Acquisition

The first and most important decision in relation to the financing of the

acquisition is to choose the right type of currency for the payment of the

17 DePamphilis, p. 464. 18 DePamphilis, p. 444.

5

acquisition price.19 The two basic currencies available are either the acquirer’s

stock or cash. A third option is to use a combination of the two.20 Other

instruments which can be used to finance an acquisition are convertible debt,

real property, rights to intellectual property, royalties, earn-outs and

contingency payments.

When choosing the currency, four characteristics have to be taken into

account.21 First, in relation to the necessity of taking additional debts in order

to use cash, the acquirer’s capital structure, debt capacity and cost of capital

have to be analyzed. Second, how will the ownership structure be affected? In

the case of cash, the acquirer will control the target, while a payment in

shares will change the overall ownership structures and may limit the

acquirer’s and its shareholders’ level of control.22 Third, “who will bear the risk

of the enterprise going forward”23? When cash is used, it will be the acquirer

that bears all the risks, whereas in the case of shares being used, the risk will

be split between acquirer and target.24 The fourth aspect is the tax liabilities in

relation to the chosen form of financing.

1 Cash Financing

If cash is used to finance the acquisition, the necessary amount can be

obtained by several methods. The most liquid form of cash is retained

earnings. Debt is another relatively liquid form of cash, whereas the level of its

liquidity and the acquirer’s access to debt depends on its cost of capital. If the

cost of capital is too high, debt financing might not be an option. Additionally,

using debt to gain the necessary level of cash increases the risk of bankruptcy

for the acquirer.25 Another possibility and frequently used method of

increasing the level of cash is the sale of “either the acquirer’s existing assets

19 See Thompson, p. 17. 20 See Thompson, p. 17. 21 See Thompson, p. 18. 22 See Thompson, p. 20. 23 See Thompson, p. 18. 24 See Thompson, p. 20. 25 See Thompson, p. 18.

6

or some of the target’s assets that won’t produce synergies with the

acquirer”26.

In terms of taxation, the use of cash may be the preferred form of payment for

the acquirer. Since the interest payments are deemed to be expenses, they

are tax deductible. However, as most jurisdictions limit the level of interest

that can be deducted from an entity’s taxable income, the benefits are limited.

In other words, the tax benefit is lost as soon as the optimum leverage level of

the organization is reached.27

From the seller’s point of view, being paid in cash is unfavorable in terms of

tax, as the capital gains of the target’s shareholders are subject to immediate

taxation.28 It has to be borne in mind that the tax base and tax rate on the

capital gains are exempt due to certain criteria such as the holding period of

the shares or a tax-free level of capital gains.29 In many cases, this may limit

the tax disadvantages of a cash transaction for the shareholders of the target

company.

As the previous illustration shows, the taxation of a cash transaction may

create differing interests between the acquirer and the target. A common

reaction by the seller in cash transactions is to require a higher purchase price

in order to compensate for the tax disadvantage.30

Cash “is the most commonly used means of acquiring shares or assets”31.

Besides the potential tax advantages for the acquirer, another reason for this

is the simplicity of collecting the necessary cash in comparison to the issuing

of sufficient shares to undertake the acquisition. Depending on the regulatory

environment and the shareholder structure, the “process can take months

longer than a similar deal in which the currency is cash”32.

26 See Thompson, p. 17. 27 See Thompson, pp. 18 and 71. 28 See DePamphilis, p. 451. 29 See Thompson, pp. 70 – 71. 30 See Thompson, p. 71. 31 DePamphilis, p. 451. 32 Thompson, p. 18.

7

2 Equity Financing

Issuing sufficient shares requires a series of preconditions. In cases where

there is no or too little authorized capital, a shareholder meeting needs to be

held in order to obtain the shareholders’ approval on the share increase.

Moreover, the shareholders have to withdraw their pre-emption rights in

regard to the new shares, which are given to shareholders in most

jurisdictions. In addition to the shareholder resolution, jurisdictions may

impose specific disclosure rules for the issue of new stock (e.g. SEC

disclosure rules in the U.S.).33

Issuing new shares also creates a variety of costs for the acquirer. The most

obvious and - to some extent controllable – expenses are the organizational

costs, e.g. costs incurred by the shareholder meeting, and the transaction

costs. The more dangerous costs, in the case of publicly traded acquirers,

stem from the risk of the share price decreasing due to the share increase.

Empirical studies show that the price of existing shares decreased in many

cases where companies issued new shares. This may be a result of the

investors’ “belief that the newly issued shares will result in a long-term dilution

in earnings per share”34 or due to the market interpreting the acquisition by

shares as the management signaling a current overvaluation of the shares35.

In some jurisdictions like the U.S. and Germany, reorganizations are treated

favorably in terms of taxation. In order to benefit from those tax advantages,

certain preconditions have to be met by the reorganization. A share

transaction, for example, qualifies as a reorganization in many cases. Thus

the share transaction is likely to be treated favorably in terms of taxation.36

An acquisition using shares is much more favorable for the seller than using

cash from a tax perspective. In many cases, a potential cpaital gain by the

target occurring through a share purchase is not considered to be income for

33 See Thompson, p. 18. 34 DePamphilis, p. 451. 35 See Thompson, p. 18. 36 See Thompson, p. 19.

8

tax purposes. Hence, there is no tax liability for the seller until it realizes a

capital gain on the sale.37

IV Scope of the Following Chapters

The analysis made in the following chapters on Germany, the U.S., and

France is based on the acquisition scenario outlined below:

Diagram 1: Acquisition Scenario

The acquirer in the given scenario is a holding company with no income other

than dividends. This is a typical case for acquisition vehicles.38 Since the

acquirer only has limited taxable income, as dividends received by corporate

shareholders are partially tax exempt – in Germany and France 95% of

dividend income is tax exempt. In the U.S. between 70% and 100% of

dividend is tax exempt depending on a corporate shareholder’s interest in the

37 See Thompson, p. 71. 38 See Gröger, p. 352.

9

distributing company. The taxable income of the acquirer is not sufficient for

the deduction of interest expenses incurred by the acquisition financing.

Hence, to have sufficient taxable income to offset against the interest

expenses arising, the first step after the acquisition is to perform a debt

consolidation.

In acquisition scenarios, the limited deductibility of interest expenses incurred

via the acquisition financing, which may be due to limited income on the level

of the acquirer, as mentioned above, requires the performance of post-

acquisition debt consolidation measures to create a tax shield against the

interest expenses. These tax shields aim to concentrate the taxable income

and the acquisition expenses on one level in order to reduce one by the

other.39 In other words, the objective is to use the interest expenses to reduce

the tax base and thereby decrease the tax burden. Three possible

mechanisms that can be used to consolidate the debt on the level of the

target or another entity of of any given group are a merger, tax consolidation

or a debt push-down. These will be analyzed in respect of each country in the

following chapters.

Following this analysis, the countries’ regulations in regard to a limitation of

the potential deductibility of interest expenses – the interest barrier

(Zinsschranke) in Germany, the earnings-stripping rule in the U.S., and the

thin capitalization rule (règles de sous-capitalisation) in France – are

examined.

The tax implications of these regulations for acquisition financing, i.e. external

or internal financing or a combination of the two, will be examined.

Furthermore, optimization measures to counteract these regulations will be

introduced. For the case of Germany, which is the main focus of this thesis,

several accounting mechanisms, which allow the acquirer to decrease

negative tax effects due to the interest barrier, will be discussed.

39 See Gröger, p. 360.

10

B GERMANY

I Debt Consolidation

The following description of a merger, tax consolidation and debt-push-down

transaction as a means of debt consolidation illustrates the necessity of an in-

depth evaluation of the overall situation. Due to each method’s advantages

and disadvantages, which may have a greater or lesser effect on the

individual group situation, the appropriate method has to be chosen on a

case-by-case basis. Particularly, an evaluation has to demonstrate whether

the individual tax advantages of one method outweighs its disadvantages,

taking into account the same analysis of the other available methods for the

given case.

1 Mergers

In the case of a merger, the acquirer has two options – to perform an

upstream or a downstream merger.

Upstream merger means the target (one level below the acquirer in the

organization’s chart) is merged into the acquirer. According to sec. 11(1) and

(2) KStG, the merger can take place at book value.40 In other words, hidden

reserves will not be realized (no step-up). The performance of the upstream

merger without the realization of hidden reserves requires an application to,

and acceptance by, the tax authorities. Usually, the acceptance of the

application is unproblematic. The only requirements by the tax authorities are

that the merged target will remain a tax resident of Germany and no

compensation is given.41

The advantage of this scenario is that as no capital gains arise and no taxes

are triggered. On the other hand, if the acquisition took place shortly before

and in the form of an asset deal, the value of any hidden reserves is likely to 40 See Gröger, p. 360. 41 See Gröger, p. 360.

11

be relatively low. Even though there will be no taxation on capital gains, a

potential merger gain may be taxed at a rate of 5% of CIT and TT according

to sec. 8b(3) KStG. In most mergers, the accrual of a merger loss is more

likely than a merger gain. So, no taxes will be levied in most cases.42 The

downside of the merger loss, on the other hand, is that it does not offer any

tax advantage as provided by sec. 12(2) sentence 1 UmwStG. The loss

cannot be used in order to reduce the taxable income of a given entity.

Another tax disadvantage of the merger may exist when the target has

valuable tax credits or accounts carried forward. These are canceled in the

case of the merger as defined by sec. 12(3) in conjunction with sec. 4(2)

sentence 2 UmwStG.43 Bearing this in mind, as those losses were already

canceled due to the acquisition – except EBITDA carry forwards – the

potential disadvantage is limited.

A downstream merger is the exact opposite - the acquirer merges into the

target. Before any downstream merger, the merging entities have to ensure

that corporate law does not prohibit the merger. Especially in post-acquisition

mergers, as is the case in this analysis, conformity with corporate law is an

important issue. That is because the high debt of the acquisition financing on

the level of the acquirer may reduce the target’s equity level considerably.

Primarily in cases of limited liability corporations (GmbH) and stock

corporations (AG) this is an important principle which may be violated through

the performance of a downstream merger.44

In terms of taxation, a downstream merger is treated in the same way as an

upstream merger. Generally, there is no tax advantage or disadvantage. One

exception may apply to any post-acquisition merger. As the acquirer’s

accounts carried forward were not canceled by the acquisition, their loss due

to a downstream merger may be more significant in comparison to a loss of

the target’s accounts carried forward in the upstream merger.

42 See Gröger, p. 361. 43 See Gröger, p. 362. 44 See Gröger, p. 363.

12

2 Tax Consolidation

Tax consolidation (Organschaft) means that the profits and expenses of all

consolidated companies (Organgesellschaften) which participate in the tax

group are consolidated and taxed on the level of the dominant enterprise

(Organträger). Besides the financial integration of the target, it is necessary to

conclude a profit and loss transfer agreement with a minimum duration of five

years for the purposes of tax consolidation.45 In addition, the dominant

enterprise needs to own the majority voting rights of each consolidated

company since the beginning of the consolidated company’s fiscal year.46

This is unlikely in the year of the acquisition. To overcome the potential tax

disadvantage in the year of the acquisition, the acquirer can apply to the tax

authorities for a change of the target’s fiscal year as provided by sec. 7(4)

sentence 3 KStG. Where this is done, it is later necessary to bring forward the

end the target’s fiscal year (Rückumstellung) before the end of the acquirer’s

fiscal year in order to offset the target’s profits against the acquirer’s interest

expenses. This backward adjustment can be performed under the same

conditions as the previous change of the fiscal year through an application to

the tax office. Usually, the tax office does not challenge such applications.47

These modifications of the target’s fiscal year enable the target to benefit from

the tax consolidation as soon as the acquisition is performed.

While, in cases of merger, tax credits and accounts carried forward are

canceled, they are frozen and therefore cannot be used for the duration of the

tax consolidation.48

3 Debt Push-Down

A debt push-down is performed through a payment by the target to the

acquirer. The cash generated by the acquirer through these inflows will be

used to repay or reduce the loan it has taken out to finance the acquisition.

Hence, no more interest expenses arise on the level of the acquirer. 45 See Gröger, p. 364. 46 See Gröger, p. 365. 47 See Gröger, p. 365. 48 See Gröger, p. 365.

13

The payment by the target to the acquirer can either be made by means of

external or internal financing. If the target has sufficient cash from retained

earnings, these can be used. Alternatively, the target can take out a bank loan

to pay the acquirer.

The mechanisms available to the parties to effect the payment are a refund of

contributions (Einlagenrückgewähr), a payout of dividends (Ausschüttung) or

the redemption of an investor’s stake (Anteilsrückkauf). A further option is the

use of an assumption of debt (Schuldenübernahme). This option is not

beneficial for consolidating the debt since the acquirer would still be paying

the interest on the loan. In other words, as the interest expenses would still

arise on the level of the acquirer, these cannot be deducted from the target’s

earnings. The assumption of debt may only be advantageous and a tax

beneficial debt-consolidation measure in combination with tax consolidation or

a waiver of the contribution claim. In order to waive the contribution claim, the

target needs suficient capital to secure the refund of debt.49 Where this is not

the case, the assumption of debt should not be considered an alternative.

Anyway, as the formation of a tax group would be necessary, which already is

a beneficial debt-consolidation method on its own, an assumption of debt is

no true alternative.

When evaluating the tax advantages and disadvantages of the debt push-

down, an analysis in relation to each of the available debt-push-down

mechanisms needs to be performed. Furthermore, the risk of taxes being

levied on capital gains needs to be taken into account. If the level of taxable

capital gains – usually this should not be the case shortly after the acquisition

– is high, the payout of dividends may be a more appropriate solution as

dividends are 95% tax-exempt.50 Another aspect which should be considered,

even though it might not be an issue shortly after an acquisition, is the target’s

accounts carried forward. In the case of a change in the ownership structure,

they are canceled accordingly.

49 See Gröger, p. 367. 50 See Gröger, p. 368.

14

If the group owns more operating businesses in Germany besides the target,

the other businesses could be included in the debt push-down. In such a

situation, the acquirer can sell the target’s shares to those businesses in the

group and offset these inflows against the outstanding loan. Obviously such a

scenario is only beneficial in the case of businesses with sufficient income

that the interest expenses can be offset against.

II The Interest Barrier

In general, interest expenses related to the financing of the acquisition are tax

deductible according to sec. 4(4) EStG.51 Besides this general regulation, the

level of deductible interest expenses may be limited due to the interest barrier,

discussed in section III of this chapter. A further limitation on the level of

deductible interest expenses is applicable in relation to trade tax. Unlike in the

case of CIT and PIT, for which 100% of interest expenses can be deducted,

only 75% of interest expenses exceeding the exemption level of €100,000 are

deductible for TT purposes, according to sec. 8 (1)(a) GewStG.52

After the implementation of the 2008 business tax reform, which is briefly

introduced in the next subsection, the interest barrier, governed by sec. 4h

EStG in conjunction with sec. 8 KStG, limits the interest deductibility granted

by sec. 4(4) EStG.53 By introducing the interest barrier, the government aimed

to control and limit the level of any financing activity by undertakings of all

legal forms.54 Therefore the interest barrier limits the level of interest payment

on any form of financing which may be deducted from an undertaking’s

income as an expense. In consequence, there is a limit to the benefit of a tax

advantage due to a decrease in the tax base resulting from the deductibility of

interest expenses. In other words, the level of tax advantages due to financing

activities is restricted to a certain level, as illustrated in detail by subsection 3.

51 See Gröger, p. 344. 52 See Gröger, p. 346. 53 Gröner, p. 344 (author’s translation). 54 See Schult, p. 37.

15

Another aspect intended by the government was to improve interest

deductibility for mid-sized companies, while increasing the tax advantage to

large multinationals. Unfortunately, as research already proves, while the

effect on multinationals is rather limited, the interest barrier is highly

disadvantageous for mid-sized companies.55

1 Business Tax Reform 2008

As part of the coalition agreement made between the CDU, CSU and SPD on

11 November 2005, the parties agreed to reform the German business tax

system by 2008.56 The coalition agreed that the reform had to cover all legal

forms, i.e. both corporations and partnerships.57 The coalition intended to

achieve five goals by means of the reform. Its first and primary goal was to

create a business tax system which was more attractive and capable of

competing on the international level while at the same time being appropriate

for the needs of the EU, and to abolish future conflicts with the European

Court of Justice.58 An additional benefit for undertakings was intended to be

easier tax planning.59 In a last point, the reform also had to guarantee the

“sustainable security of the German tax base”60.

The reform came into force on 1 January 2008 and included numerous

changes to many aspects of business taxation. One of these was the

introduction of the interest barrier. Overall, the governing coalition intends to

make Germany more attractive for undertakings and thereby eliminate tax

evasion.61

2 Background

The first limitation of external financing was implemented by the German tax

office in 1987 and was applicable solely to debt financing by foreign

55 See Prinz (2008). 56 See CDU, CSU & SPD, p. 69. 57 See CDU, CSU & SPD, p. 69. 58 See CDU, CSU & SPD, p. 69. 59 See CDU, CSU & SPD, p. 69. 60 CDU, CSU & SPD, p. 69 (author’s translation). 61 See Schult, p. 36.

16

shareholders. This regulation, as did many of the following regulations

implemented until 2002, aimed to limit the corporation’s possibility to transfer

profits to its shareholders abroad in the form of interest payments and

amortizations, without triggering WHT liability.

This regulation was ruled to be invalid by the Federal Finance Court on 05

February 1992.62 In a first reaction to the judgment, the tax office annuled the

regulation and passed the responsibility of implementing a new regulation to

the legislative authority.

The legislative authority did so and implemented a new regulation in 1994 as

part of the Location Protection Act (Standortsicherungsgesetz). The act was

the first government legislation which limited the deductibility of interest

expenses in Germany. It is important to know that the limitation only applied to

interest payments on loans provided directly or indirectly by shareholders who

had an interest of more than 25% in the undertaking and were not subject to

German CIT.63 In particular, similarly to the previous regulation by the tax

office, the legislative body “intended to limit interest payments of national

undertakings to foreign shareholders” by introducing this limitation.64 In order

to achieve its aim, the legislature limited the deductible amount of interest

expenses to a specific ratio between equity and debt – the so-called “safe

haven”. The equity/debt ratio for holding companies was 1:9 (holding

privilege), 1:0.5 for loans with a variable interest rate and 1:3 for loans with a

fixed interest rate.65 In 2001, those ratios were further reduced to 1:3 for

holdings; 1:1.5 on fixed interest and the “safe haven” on variable interest was

abolished.66 All interest expenses on debt trapped by the regulation

exceeding the ratio – the safe haven – were not deductible.

In 2002, the European Court of Justice found the legislation to violate the

freedom of establishment. Hence, the regulation only applied to foreigners of

third countries and was not applicable to interest payments to EU and EEA

62 See Köhler, Vogel & Adolf, p. 655. 63 See Köhler, Vogel & Adolf, pp. 655-656. 64 Köhler, Vogel & Adolf, p. 655 (author’s translation). 65 See Köhler, Vogel & Adolf, p. 656. 66 See Köhler, Vogel & Adolf, p. 656.

17

members anymore.67 Furthermore, a tax exemption of €250,000 was

implemented in 2004 which was applicable to all shareholders.68

In terms of M&A transactions, a high level of uncertainty existed in relation to

the previously described regulations. In consequence, finding the appropriate

structure and performing effective tax planning for the transaction were

challenging and created a high level of uncertainty.

3 The New Interest Barrier

Unlike the previous regulations that were implemented to limit an

undertaking’s level of external financing, the newly introduced interest barrier

applies to undertakings of any legal form and any form of financing. In order to

stimulate a more intense use of retained earnings or other internally available

cash, the interest barrier limits the level of deductible net-interest payments to

30% of the EBITDA.69 Interest expenses exceeding the deductible level can

be brought forward for an unlimited period. Whereas this results in an

increased level of interest expenses in future years, profits will not be affected

by the carry forward.70 Hence, an interest carry forward can only be exercised

in the case of a future decrease in the ratio of net-interest expenses to the

EBITDA. Furthermore, the ‘real’ value of the interest carry forward is limited

since it is canceled in certain restructuring scenarios and in cases of

significant changes in the ownership structure.71

On the other hand, when the EBITDA exceeds the interest expenses, the

EBITDA can be carried forward (EBITDA-Vortrag) and increases the level of

net-interest deductibility.72 The EBITDA carry forward is limited to five years.

Interest expenses include all payments on financing activities. These include

interest payments based on “fixed and variable interests, typical silent

67 See Köhler, Vogel & Adolf; p. 656. 68 See Köhler, Vogel & Adolf; p. 657. 69 See Gröger, pp. 344-345 and Schult, p. 37. 70 See Gröger, p. 344. 71 See Reiche & Kroschewski, p. 1331. 72 See Gröger, pp. 344-345.

18

partners, participation rights and share of profits such as commission”73.

Besides these expenses, tax authorities even deem several other non-interest

expenses which are directly related to the financing activity to be interest

expenses. An example of these are fees charged by a creditor in relation to a

loan.74

In order to support small and medium-sized businesses, the interest barrier

was introduced with an exemption for interest expenses up to a specific

amount. At its introduction in 2008, interest expenses of up to €1 million were

exempted from the interest barrier and fully deductible. In 2009, the

exemption was increased to €3 million by the Citizens’ Relief Act

(Bürgerentlastungsgesetz) – initially meant for a limited time period.75 The

time limitation was abolished in 2010 through the Growth Acceleration Act

(Wachstumsbeschleunigungsgesetz).76

Regarding the exemption level, it is of crucial importance to know that the

exemption is not a general tax-free amount. In other words, the exemption of

€3 million only applies to cases where the undertaking’s total interest

expenses do no exceed the exemption level. As soon as this level is reached

(e.g. interest expenses exceeding € 2,9999,999.99) the total amount is

subject to the interest barrier.

From this point on, undertakings whose interest expenses exceed the

exemption level slightly and which are unsure whether these expenses

exceed 30% of their EBITDA should try to reduce their interest expenses

below the €3 million threshold in order to create a tax benefit by avoiding the

application of the interest barrier. In a corporate group scenario, as the

interest barrier applies to each autonomous business, the allocation of interest

expenses throughout the group may provide a solution to the non-applicability

of the interest barrier. Potential ways which help to structure the financing in

such a way as to avoid tax disadvantages due to the interest barrier are

introduced in section 5.

73 Gröger, p.345 (author’s translation). 74 See Gröger, p. 345. 75 See Gröger, p.345. 76 See Köhler, Vogel & Adolf, p. 658.

19

Two other options provided by legislation which may result in the non-

applicability of the interest barrier are group independence (Konzern-

unabhängigkeit) according to sec. 4h(2) sentence 1(b) and sec. 4h(3)

sentences 5 and 6 EStG and the escape clause provided in sec. 4h(2)

sentence 1(c) EStG.

a Group Independence

The group independence exemption applies to “undertakings which are not or

only proportionally part of a group”.77 In relation to the interest barrier, the

definition of a group is extended. According to German regulations, an

undertaking is considered part of a group if it can be consolidated with other

undertakings by means of the IFRS, the US-GAAP or according to any other

accounting legislation of an EU member state.78 Alternatively, in cases where

the financial and business policies of a group can be controled by, or are

equal to those, of another undertaking, the prerequisites for being considered

part of a group are satisfied.79

Besides the necessity to satisfy the previously mentioned prerequisites, a

business entity may not provide so-called “harmful shareholder financing”

(schädliche Gesellschafterfremdfinanzierung).80 Harmful shareholder

financing occurs when more than 10% of the total net-interest expenses are

paid to shareholders whose interest in the company exceeds 25%. This

includes interest on loans provided by any related party to those

shareholders, or a third party which is capable of having recourse

(steuerlicher Rückgriff)81 to the shareholder or also a related party to it.82

Consequently, any undertaking which has a diverse ownership structure, has

no subsidiaries, and where less than 10% of interest expenses are a result of

harmful shareholder financing, is implicitly considered to be independent and 77 Reiche & Kroschewski, p. 1332. 78 See Reiche & Korschewski, p. 1332 and Gröger, p. 346. 79 See Reiche & Korschewski, p. 1332. 80 See Sinewe & Witzel, p. 317 and Schult, p. 42. 81 See Sinewe & Witzel, p. 319. 82 See Sinewe & Witzel, p. 318.

20

free of a group. In connection with this exemption, it is crucial to note that the

ownership structure and financing situation of the previous fiscal year are the

determining factors.83 Therefore, a target previously independent of the group

which satisfyies the requirements of this exemption according to its status in

the prior fiscal year can be exempted from the interest barrier in the fiscal year

of the acquisition.

b Escape Clause

Undertakings which are members of a group and are therefore not able to use

the group independence exemption can use the escape clause to be

exempted from the interest barrier. This exemption takes effect in cases

where the equity capital ratio84 of a group’s undertaking does not surpass the

group’s equity capital ratio by more than 1%.85

In order to be exempted due to the applicability of the escape clause, also the

requirements in regard to harmful shareholder financing described in the

previous paragraphs have to be fulfiled [sec. 4(2) sentence 1(c) EStG]. In

relation to the harmful financing of groups, it is important to know that “internal

group financing is harmless in relation to the interest barrier and the harmful

shareholder financing”86.

4 Impact on Acquisition Financing

Since the implementation of the interest barrier, the annual level of the

interest expenses’ deductibility – for those cases in which the exemption level

of €3 million is reached – is limited to 30% of the EBITDA of a given year.

Where the debt is consolidated by means of a merger, the EBITDA of the

combined undertakings is of relevance; in the case of tax consolidation, it is

the EBITDAs of all consolidated companies and the dominant company.

When debt-push-down measures are used, the EBITDA of the undertaking to

83 See Sinewe & Witzel, p. 317. 84 The relationship of equity to the balance-sheet total. 85 See Reiche & Korschewski, p. 1332; Gröger, p. 346 and Sinewe & Witzel, p. 320. 86 Sinewe & Witzel, p. 321 (author’s translation).

21

which the debt has moved – and therefore where the interest expenses

appear – is the significant figure.

All excess interest expenses have to be carried forward until either the

interest expenses of a future year decrease or the EBITDA becomes high

enough to allow the deductibility of the current interest and the interest

expenses carried forward. Other than would have been the case for the

previous regulations, since the introduction of the interest barrier, the form of

acquisition financing – external (e.g. bank loan) or internal (e.g. debt provided

by the foreign parent company) – does not play a role in relation to the

deduction limitation. In other words, whereas the previous regulation only

applied to specific types of financings by foreign shareholders, the choice of

acquisition financing became subordinated in terms of interest deduction

because the interest barrier applies to all financing activities.

Nevertheless, in the case of internal financing, two conditions have to be

considered. First, the acquirer has to ensure that the underlying conditions

meet arm’s length requirements. Where this is not the case and arm’s length

is exceeded, interest payments are only considered interest expenses up to

the arm’s length level. Expenses above this level are considered constructive

dividends and are not tax deductible. Second, if the application of the escape

clause may be an option, it should be ensured that the undertaking using the

escape clause – acquirer, target or the combined entity after a merger – does

not provide any harmful shareholder financing.

5 Efficient Structuring in Light of the Interest Barrier

In order to allow the acquirer to perform appropriate tax-planning activities

and reduce the potential tax disadvantages due to the applicability of the

interest barrier, the first step is to examine the individual likelihood of its

applicability.

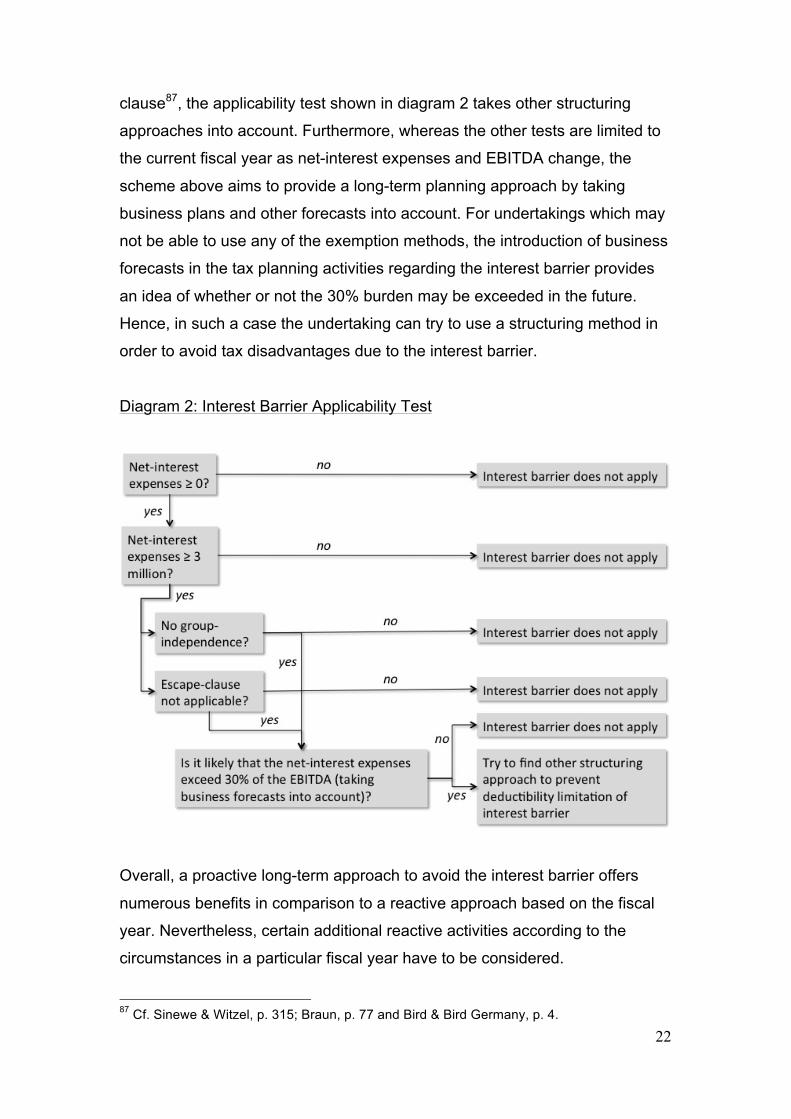

In comparison to other interest barrier applicability tests that solely consider

the applicability of the exemption level, group independence or escape

22

clause87, the applicability test shown in diagram 2 takes other structuring

approaches into account. Furthermore, whereas the other tests are limited to

the current fiscal year as net-interest expenses and EBITDA change, the

scheme above aims to provide a long-term planning approach by taking

business plans and other forecasts into account. For undertakings which may

not be able to use any of the exemption methods, the introduction of business

forecasts in the tax planning activities regarding the interest barrier provides

an idea of whether or not the 30% burden may be exceeded in the future.

Hence, in such a case the undertaking can try to use a structuring method in

order to avoid tax disadvantages due to the interest barrier.

Diagram 2: Interest Barrier Applicability Test

Overall, a proactive long-term approach to avoid the interest barrier offers

numerous benefits in comparison to a reactive approach based on the fiscal

year. Nevertheless, certain additional reactive activities according to the

circumstances in a particular fiscal year have to be considered.

87 Cf. Sinewe & Witzel, p. 315; Braun, p. 77 and Bird & Bird Germany, p. 4.

23

A previously formed tax group may already be beneficial and decrease the

likelihood of negative tax effects due to the interest barrier.

Under this arrangement, all entities participating in the consolidation are

treated as one undertaking [sec. 15(3) KStG] for tax purposes.88 As a result,

the EBITDA of the tax consolidation refers to that of all consolidated

companies and the dominant enterprise, and all interest expenses are

consolidated on the level of the dominant enterprise. Hence, the consolidated

companies with high net-interest expenses benefit from the high EBITDA

contributed by others, while those companies with high profits and low

expenses benefit from the deductibility of the others’ expenses.

The same also applies for a merger. The positive effect may be especially

advantageous where more businesses than only the acquirer and target are

consolidated or merged.

Another, but similar, option in the case of a group is available for cases where

debt push-down is used as the measure of debt allocation: The interest

expense is distributed in such a way that the individual taxable unit’s interest

expenses remain below the exemption level of three million euros. Such a

scenario may already be created before the acquisition takes place by using

more than one acquisition vehicle89. Bearing in mind if the acquisition vehicles

are mere holding companies, the advantage is limited because a minimum

amount of taxable income is involved.

Besides these structuring opportunities going hand in hand with the debt

consolidation, German law provides for further accounting-related

opportunities to improve the deductibility of interest expenses.

a Realization of Hidden Reserves

One restructuring option to increase the level of deductible interest expenses

is the increase in the tax EBITDA through the realization of hidden reserves.

In the case of a target acquired in an asset deal, this alternative may not be

88 See Gröger, p. 364 89 See Reiche & Korschewski, pp. 1333-1334.

24

available after the acquisition. Nonetheless, hidden reserves of the acquirer or

other group undertakings may be available; it may be possible to realize them.

Those undertakings could ultimately be used for a debt push-down.90

Before beginning to realize available hidden reserves, an in-depth analysis of

the potential benefit in terms of the interest barrier is as important as for any

other structuring activity. In relation to the realization of hidden reserves, the

evaluation should explicitly concentrate on the potential tax payments on

capital gains created by the realization of hidden reserves. If they exist, they

have to fall below the realized tax advantages in comparison to the interest

barrier. Otherwise the realization of hidden reserves is not advantageous.

b Variable Interest Expenses and Debt-to-Equity Swap

Two other options, in most cases likely to be exclusively available to internal

financing, are the payment of variable interest91 and a debt-to-equity swap.

Agreeing on the payment of variable interest in relation to any given fiscal

year’s EBITDA allows the acquirer to ensure that its interest expenses on the

acquisition financing will be fully deductible and not exceed the 30%

threshold. Obviously, when more than the one loan is taken out, the interest

barrier can become an issue due to the other loans. To avoid or limit this risk,

the interest on all other loans and an EBITDA forecast should be taken into

account when the variable interest rate is negotiated.

A second option is to use a hybrid loan in a similar manner. For the hybrid

loan to be advantageous in terms of the interest barrier, the creditor and

acquirer have to conclude an agreement including the possibility of a shadow

interest carry forward (Schattenzinsvortrag). Such an agreement may be

formulated as follows: “In the case of a low cash-flow and limited deductibility

of interest, no interest will be paid and carried forward until cash-flow has

increased again”92.

90 See Liekenbrock, p. 312. 91 See Liekenbrock, p. 287. 92 Liekenbrock, p. 288 (author’s translation).

25

For any agreement on the payment of variable interest between related

parties, attention must be given to the possibility that the interest rate exceeds

arm’s length terms. In such a case, the interest expenses in excess of arm’s

length are not deductible.

In the case of a debt-equity swap, any possible risks of the interest barrier are

canceled. As the former creditor becomes a shareholder and receives

dividends which are not triggered by the interest barrier, no more interest

payments are made.

c Accounting Measures

A corporate group could try to improve its equity capital ratio by means of

accounting. To achieve such an improvement, the change to IFRS accounting

is advantageous. IFRS offers such an advantage due to the possibilities of

performing time-value accounting on certain assets, the allocation of goodwill

to so-called cash-generating units and the right to elect the type of valuation

(Bewertungswahlrecht).93 In terms of the interest barrier, the improvement

measures have to focus on the individual business’s balance sheet rather

than the group balance sheet to allow the employment of the escape clause.

A second available accounting measure is limited only to very few and

specific acquisitions provided by sec. 255(3) sentence 2 HGB. According to

the section, interest expenses which can definitely be assigned to the

production process can be treated as production costs.94 As this rule is also

applicable in terms of tax accounting, a tax advantage is created in relation to

the interest barrier.

Even though the application of this measure cannot be applied to most

acquisitions, in some cases – such as that of a previous subcontractor

involved in the production process – the use of this option allows the acquirer

to account for the interest expenses of the acquisition financing as production

expenses. Hence, the interest barrier is not applicable and the interest

expenses, being considered production costs, are fully deductible.

93 See Liekenbrock, p. 314. 94 See Liekenbrock, p. 313.

26

C UNITED STATES

I Debt Consolidation

Any debt-consolidation method performed has to consider potential threats by

the step transaction doctrine, often applied to post-acquisition reorganizations

by courts. According to U.S. tax law, reorganizations have to be borne by a

general business purpose and on economic grounds.95 Reorganizations

performed solely for tax optimization reasons can therefore be challenged by

the courts and may result in unpredicted negative tax consequences. To avoid

such tax disadvantages, it is crucial to take reasonable and justifiable

business purposes and economic grounds into account when determining

restructuring measures in relation to post-acquisition debt consolidation.

1 Mergers

Sec. 355 of the IRC is applicable to tax-free mergers in the U.S. In order to

perform a tax-free merger as defined by Sec. 355 IRC, six requirements have

to be fulfiled. These include “a five-year business history”96, a minimum 80%

interest by one shareholder, and the continuity of the business after the

merger, such as a business purpose being the reason for the merger.

In relation to a post-acquisition merger as a means of debt consolidation,

where the business history requirement or any other requirement cannot be

met, a tax-free merger according to sec. 355 IRC is not an option. In such

cases, a merger can be performed at book value or as a statutory merger

under sec. 368(a)(1)(A) IRC. For the statutory merger to be tax neutral

several statutory and non-statutory (case law) requirements such as the step

transaction doctrine and the continuity of the business after the merger need

to be fulfilled.

95 See Taxand, p. 367. 96 Chip, p. 1.

27

When the merger is performed at book value, it may be advantageous for tax

purposes to perform an upstream merger as hidden reserves on the level of

the target may already be realized during the acquisition. This is especially

true if the acquisition was performed by means of an asset deal. However,

according to sec. 338 IRC, under certain conditions a share deal may also be

treated as an asset deal for income tax purposes.97 Where this is possible,

the acquirer should elect this option in order to limit capital gains arising from

a post-acquisition merger.

2 Tax Consolidation

The single requirement for forming a tax group in the U.S. is a direct interest

of 80% by the dominant company in one of the consolidated companies. If

more than the acquirer (e.g. dominant company) and the target (e.g.

consolidated company) are joining the tax group, it is sufficient if any

consolidated company other than the dominant company holds an interest of

at least 80% in one of the other consolidated companies.98

When those requirements are satisfied, a tax group can be formed by means

of a consolidation election under sec. 1501 IRC.

Alternatively, the tax consolidation can either be performed by “checking the

box” or through the establishment of a partnership for tax purposes.

By using the “checking the box” option, each consolidated company becomes

a division of one single undertaking – the tax group.99 Since this conversion is

considered to be a liquidation for tax purposes, it may trigger built-in gains. If

the assets causing the gain are kept in the U.S. business for less than ten

years, those gains are subject to taxation.100

Where the tax group is formed by means of a partnership for tax purposes, no

new entity will be established, and assets will not be moved. The shifting of

assets may give rise to taxable gains. To establish the partnership, it is

sufficient that all participating businesses conclude a profit and loss pooling

97 See Taxand, p. 361. 98 See Deloitte (Highlights U.S.), p. 3. 99 See Chip, p. 2. 100 See Chip, p. 2.

28

agreement. This agreement has to contain wording such as the following:

“Neither party may sell business assets without the other’s consent, each

party indemnifies the other for business-associated liabilities, each party

agrees to ’true up’ disproportionate losses, businesses are to be carried on

under a single trade name, new assets are acquired in the name of the joint

venture and the businesses are accounted for as a joint venture”101.

3 Debt Push-Down

In terms of taxation, the distribution of dividends may be an attractive option

for performing a debt push-down. This is especially the case where a member

of the same group holds an interest of 100% in the distributing business. In

this case, dividend income is 100% tax exempt.102

Since the maximum possible level of dividend distributions may not be

sufficient to push down all debt incurred by the acquisition from the acquirer to

the target, additional measures such as a distribution of the target’s assets

may be necessary. In relation to such a transaction with other affiliated

companies, it is crucial to take potential tax consequences created by the

realization of capital gains into account.

A third method frequently used in the U.S. as a means of debt push-down is

to combine the acquirer and the target in a newly established holding

company.103 For tax purposes, such a transaction – which is somewhat similar

to a merger – can be performed as a share deal to minimize tax implications

due to the realization of hidden reserves.

Additionally, a carry forward is not lost proportionally in the case of such

restructuring. This is a significant advantage in comparison to Germany.

101 Chip, p. 2. 102 See Deloitte (Highlights U.S.), p. 1. 103 See Chip, p. 2.

29

II Earnings-Stripping Rules

As in Germany, interest expenses incurred due to acquisition financing can

generally be offset against taxable income. Besides this general principle,

certain exceptions exist under which the level of deductibility is limited. The

most important exceptions are the question whether financing is classified as

debt or equity in accordance with the principles of economic import [sec. 385

IRC], IRS standards and judicial principles.104 Classification as debt is the first

necessary prerequisite for allowing any interest deduction. Mainly in cases of

shareholder loans not granted at arm’s length [sec. 482 IRC] or debt secured

by a related guarantor – who may be considered the primary borrower by the

tax authorities – interest payments are treated as dividends and are therefore

not deductible.105

Another limitation applies when discounted securities are the financing

instrument used. If a foreigner holds a security instrument, where the issuer

did not pay the original issue discount, the discount is not deductible.

Likewise, the deduction can be limited or disallowed, “if the debt instrument is

treated as an applicable high yield discount obligation”106.

When the acquisition is financed or the financing is secured by a related party,

the interest deductibility may also be limited under the earnings-stripping rule.

The earnings-stripping rule governed by sec. 163(j) IRC, limits the

deductibility of interest payments by U.S. corporate enterprises when the

financing is conducted by a related party abroad, underlying a back-to-back

arrangement, or is provided by a third party where the agreement includes a

disqualifying guarantee and no WHT is levied on the interest payments. If the

interest payment is not taxed or taxed at a rate below 30%107 in the U.S., the

deduction of the interest expenses is limited. In the case of a WHT rate below

30%, the interest deduction is limited in accordance with the level of WHT

levied (e.g. 10%) and the statutory rate of 30%. A more detailed analysis in 104 See KPMG (U.S.), p. 7 and Bohn, pp. 153-154. 105 See KPMG (U.S.), p.7. 106 KPMG (U.S.), p. 9. 107 30% being the total level of withholding tax levied in the U.S.

30

relation to the application of the earnings-stripping rule is provided in

subsection 2.

If a corporation’s financing includes disqualified interest expenses108 – in

cases with excess interest expenses – the deductibility of the expenses may

be limited. The limitation only occurs when the debt-to-equity safe harbor of

1.5:1 and the cash-flow safe harbor, being 50% of the adjusted taxable

income109, are exceeded.110

Once the interest expenses of one fiscal year exceed both safe harbors, not

all interest expenses will be deductible. Non-deductible interest expenses can

be carried forward for an unlimited time.111 In addition, if the interest expenses

are below 50% of the adjusted taxable income, the excess portion of this 50%

– the excess limitation – can be carried forward. This can be carried forward

for a maximum of “three years and added to the 50% of the adjusted taxable

income to increase the threshold”112 of the following years.

1 Background

The earnings-stripping rule was primarily introduced by means of the

Omnibus Budget Reconciliation Act in 1989. With its introduction, the U.S.

government intended to generate equal taxation for all U.S. businesses, by

limiting the tax structuring opportunities of U.S. businesses with foreign

undertakings. While they were able to create tax advantages by shifting profits

abroad, purely domestic businesses had a tax disadvantage.

In addition, by implementing the earnings-stripping rule, the U.S. government

was able to limit a further decrease in its tax revenue.113

Initially, the regulation only applied to direct financing activities by a related

party and back-to-back transactions. In 1993, as part of the Revenue 108 Interest expenses on financing activities falling under the earnings-stripping rule (see PWC (2004), p. 1). 109 Adjusted taxable income = taxable income + net interest expense+ net operating loss deduction + depreciation, amortization, depletion. (See BDI & KPMG, p. 23). 110 See PWC (2004), pp. 1-2 and BDI & KPMG, p. 20. 111 See Deloitte (U.S.), p. 11. 112 PWC (2004), p. 2. 113 See BDI & KPMG, p. 20.

31

Reconciliation Act, the application was extended to third party debt with

recourse authority.

In the early 2000s two proposals, the “Thomas Bill” 114 of 11 July 2002 and the

“Bush Proposal” 115 as part of the 2004 budget, were introduced aiming to

modify the earnings-stripping rule.

Both proposals suggested a reduction of the adjusted taxable income safe

harbor from 50% to 35%, a limitation on disallowed interest carried forward to

a maximum of 5 years, and the elimination of the excess limitation carry

forward.116 While the Thomas Bill proposed the elimination of the debt-to-

equity safe harbor, the Bush Proposal intended to replace the 1.5:1 ratio with

a debt-to-asset test.117 Furthermore, in cases where “the U.S. group is more

heavy levied than the rest of the group”118,the Thomas Bill aimed to disallow

disqualified interest of such groups, while the Bush Proposal suggested

disallowing the interest either completely or only partially. This was to apply to

U.S.-based and foreign-based multinational groups. Neither of the two

proposals has been enacted and come into force to date.

2 Application

The earnings-stripping rule only applies to U.S. businesses which are

considered members of a group. To be deemed a member of a group, an

interest of at least 80% must be held directly or indirectly by another corporate

entity.119 Especially when a corporate parent holds a significant interest in two

or more U.S. businesses, those businesses are considered members of a

group.120

For partnerships, the earnings-stripping rule is not applicable – at least on the

level of the partnership. In the case of a corporate partner, the earnings-

stripping rule may apply proportionally to its interest in the partnership –

114 Named after the representative William Thomas, who chaired the House Ways and Means Committee. 115 Named after the U.S. president at that time, whose administration advanced the proposal. 116 See PWC (2004), p. 3. 117 See PWC (2004), p. 3. 118 PWC (2004), p. 3. 119 See Ernst & Young LLP, p. 43. 120 See BDI & KPMG, p. 25.

32

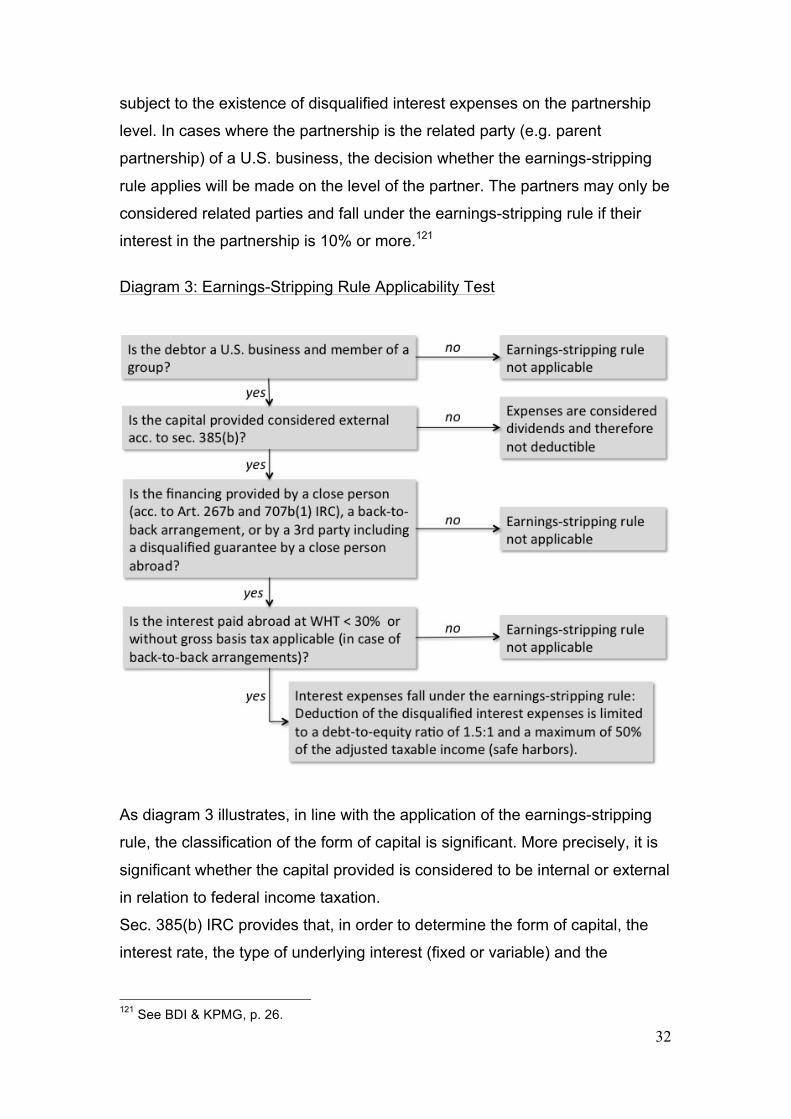

subject to the existence of disqualified interest expenses on the partnership

level. In cases where the partnership is the related party (e.g. parent

partnership) of a U.S. business, the decision whether the earnings-stripping

rule applies will be made on the level of the partner. The partners may only be

considered related parties and fall under the earnings-stripping rule if their

interest in the partnership is 10% or more.121

Diagram 3: Earnings-Stripping Rule Applicability Test

As diagram 3 illustrates, in line with the application of the earnings-stripping

rule, the classification of the form of capital is significant. More precisely, it is

significant whether the capital provided is considered to be internal or external

in relation to federal income taxation.

Sec. 385(b) IRC provides that, in order to determine the form of capital, the

interest rate, the type of underlying interest (fixed or variable) and the

121 See BDI & KPMG, p. 26.

33

creditor’s ranking in comparison to other creditors are of vital importance.122

Financing activities providing an inappropriate interest rate – in comparison to

the market rate - demand the payment of variable interest rates, or in the case

of a subordinated creditor’s ranking, the financing is deemed to be internal.123

Internal capital is treated as an equity investment for tax purposes. Hence,

interest payments are considered as dividend payments and not deductible.124

On the one hand, when the interest rate is appropriate and fixed, and the

creditor’s ranking equals those of similar creditors, the capital is categorized

as external. This makes the deductibility of interest expenses generally

possible, whereas the level of deductibility may be limited. In addition to the

requirements set out in the IRC, a great deal of case law handed down by

U.S. federal courts exists in connection with the classification of financing.

According to these decisions, “the overall intention of the parties, the terms

and conditions of the loan, the history of the actual dealings of the parties

(e.g. payment history), and the hypothetical ability of the borrower to obtain

similar financing from an unrelated party”125 are criteria which should be taken

into account.

Where the financing has been classified as external, the next step is to

analyze whether the creditor belongs to one of the three groups / financing

parties to which the earnings-stripping rules apply. As previously mentioned,

these three groups include related parties abroad which do not pay or pay a

U.S. WHT below 30% on the interest, back-to-back arrangements and third

party debt (e.g. bank loan) which is secured by a disqualified guarantee and

on which interest payments no WHT is levied.

Whether a creditor is considered a related person has to be analyzed by

applying the criteria provided by sec. 267b and sec. 707b(1) IRC.126

According to these provisions, the creditor has to satisfy one of the following

three criteria: natural persons holding an interest of above 50%, “corporate

122 See BDI & KPMG, p. 20. 123 See BDI & KPMG, p. 20 and Ernst & Young LLP, p. 46. 124 See KPMG (U.S.), p.7. 125 Ernst & Young LLP, p. 46. 126 See BDI & KPMG, p. 21.

34

enterprises of the same affiliated group having a parent-subsidiary

relationship or being corporate sisters holding an interest of above 50% on

each level”127, or partnerships having an interest of above 50% in the

corporate entity or vice-versa.128 For both cases, the interest can either be

owned directly or by adding the interest of family members of others. In

general terms, a creditor not dealing at arm’s length is considered to be a

related person.129

Back-to-back arrangements involve the use of an unrelated party – such as a

bank – as an intermediary between the related person abroad and the U.S.

corporate entity. Instead of granting a loan to the corporate entity, the related

party grants a loan to the bank on condition that the loan is passed on to the

corporate entity by the bank. In consequence, even though the corporate

entity pays interest to the bank, the interest payment is deemed to be an

indirect payment of interest from the corporate entity to its related party as the

bank pays interest to the related party. The deduction of such indirect interest

payments is also limited by the earnings-stripping rule.130

The third category of financing affected by the earnings-stripping rule is third

party loans that satisfy certain requirements. These requirements are the

guarantee of repayment by a related person and that no WHT is levied on the

interest payment. According to IRS standards and the evolution of the

legislative process in the U.S., the guarantee requirements are not solely

limited to disqualified guarantees. In principle, any form of credit support by a

foreign related party can fulfill the requirement.131 The WHT prerequisite is

only based on the guarantor. Thus, even when the financing bank is based

and located in the U.S. and therefore subject to U.S. taxation, the earnings-

stripping rule applies if the guarantor is not subject to U.S. WHT.132 In other

words, if WHT were not levied or WHT were imposed below 30% in the

127 BDI & KPMG, p. 21 (author’s translation). 128 See BDI & KPMG, p. 21. 129 See Ernst & Young LLP, p. 44. 130 See BDI & KPMG, p. 21. 131 See BDI & KPMG, p. 22. 132 See BDI & KPMG, p. 22.

35

hypothetical case of a direct interest payment to the guarantor, the earnings-

stripping rule would be applicable.

3 Impact on Acquisition Financing

The illustrations in the previous section show under which conditions the

deductibility of interest might be limited. As the introduction to this section

described, certain forms of financing such as discounted securities and

financing subject to underlying conditions that lead to its classification as

internal capital are not tax deductible in general. Hence, such forms of

financing should be avoided when choosing the appropriate financing method.

Furthermore, other forms of financing provided or secured by related persons

may be disadvantageous due to the possible applicability of the earnings-

stripping rule.

The earnings-stripping rule can be compared to the German legislation prior

to the introduction of the interest barrier in 2008. Moreover, the previous

German regulations and today’s environment in the U.S. are more

advantageous in terms of deducting interest expenses incurred due to

acquisition financing. Overall, this advantage is based on the fact that the

earnings-stripping rule is applicable only to a specifically defined set of

financing methods including those provided by a foreign related party whose

WHT rate is below 30%, back-to-back arrangements, and third party financing

secured by those related parties. Considering the earnings-stripping rule and

its underlying applicability requirements, an acquirer, given its costs of capital

allows it to use external (e.g. bank) financing, may have little difficulty in

choosing a form of financing that does not trigger the earnings-stripping rule.