tax clearance for foreign employees - home - iras · tax clearance for foreign employees . 2 ©...

TRANSCRIPT

1 1 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

Twitter.com/IRAS_SG Facebook.com/irassg www.iras.gov.sg

Tax Clearance for Foreign Employees

2 2 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

• What is Tax Clearance

• When to seek Tax Clearance

• When is Tax Clearance not required

• Tax Clearance Calculator

• What you need to do for Tax Clearance

• Why e-File tax clearance

• Demo on e-Tax Clearance

• Points to note when filing Tax Clearance

3 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

Foreign employee gives notice of resignation

Employer withholds all monies due and notifies IRAS by filing Form IR21

IRAS issues Tax Bill to employee and Clearance Directive to employer

Employer remits monies withheld to IRAS and employee pays any remaining tax before departure

4 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

• At least 1 month before the foreign employee:

• ceases employment in Singapore; or

• is posted overseas; or

• leaves Singapore for any period exceeding three months.

• If insufficient notice is given by the foreign employee, you need to submit the Form IR21:

• once you are aware of the employee’s intention to leave; or

• within 10 days from his cessation of employment, whichever is earlier.

File IR21 on time to avoid late-submission fines of up to $1,000

5 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

• Singapore citizens;

• Singapore Permanent Residents who are not leaving Singapore permanently (this administrative concession does not apply to overseas postings);

• Non-citizens who:

- are transferred to another company in Singapore within the group due to merger, takeover or restructuring;

- are away from Singapore for training or business purposes (excluding overseas postings) for three to six months.

Use the Tax Clearance Calculator to help you decide whether Tax Clearance is required

6 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

7 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

8 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

9 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

Issue Tax Bill to employee

& Clearance Directive to

employer

IRAS process Tax Clearance

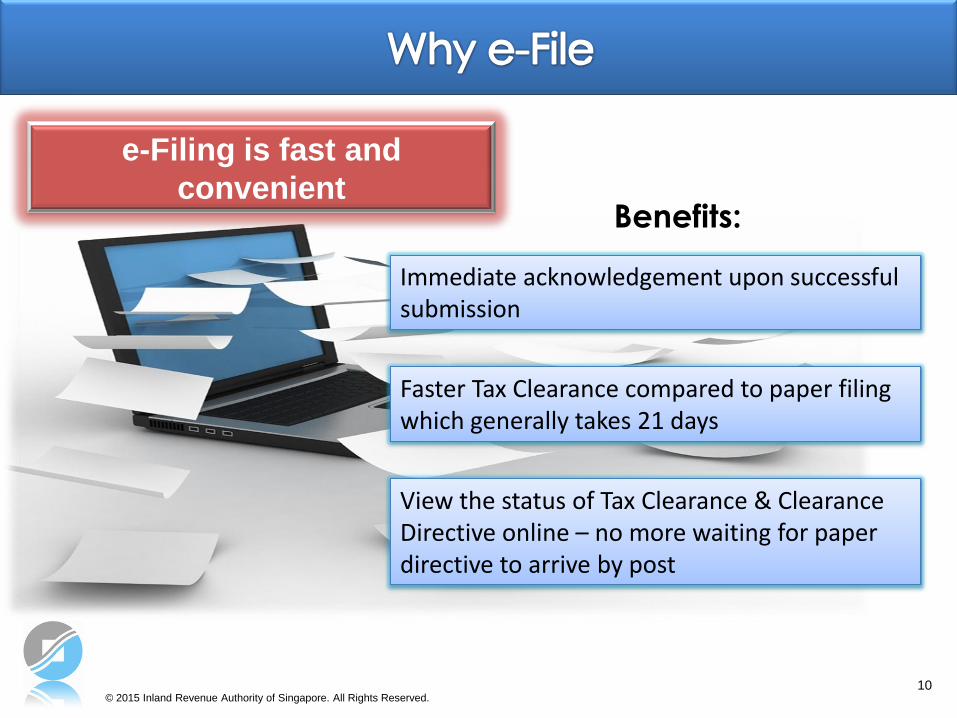

10 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

Benefits:

e-Filing is fast and

convenient

Immediate acknowledgement upon successful submission

Faster Tax Clearance compared to paper filing which generally takes 21 days

View the status of Tax Clearance & Clearance Directive online – no more waiting for paper directive to arrive by post

11 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

12 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

13 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

14 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

15 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

16 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

17 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

18 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

19 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

20 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

21 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

22 22 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

23 23 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

24 24 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

25 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

26 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

27 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

28 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

29 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

30 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

1) Date of Cessation Date of cessation is the last day of service with employer. It does not refer to EP/WP cancellation date.

2) Resignation Date Date of resignation (if available) should be filled in, in order for IRAS to ascertain whether employer has fulfilled its obligations.

3) Monies Withheld

Employer should withhold ALL monies that is due to the employee from the point the employer is notified of his intention to cease employment. Monies withheld may not be just the last month’s salary.

4) Income Details Employer should report employee's income separately for each calendar year.

5) Tax Borne by Employer Paying taxes from the withheld salary is not considered as tax borne by employer. Only select “Yes, fully borne” if the employer is bearing the tax for the employee.

31 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

6) Total income in each year is $20,000 or less

“Total income in each year is $20,000 or less” refers to the yearly income of the employee and not solely the cessation year’s income. Enter ‘No’ if you have paid your employee more than $20,000 in any calendar year.

7) Particulars of the Employee’s Spouse and Children

Employer should fill in the particulars of the employee’s spouse and children in the Form IR21 so that the relevant dependant reliefs can be included in the tax assessment. This will help in reducing the employee’s tax.

8) Amendment to Form IR21 If there are amendments to be made to Form IR21, please submit an Additional/Amended Form IR21 as appropriate.

9) Submission of IR8A for Employees who have Sought Tax Clearance

Employer need not submit IR8A for employees who have sought tax clearance. However, if the payroll system is unable to exclude employees who have sought tax clearance, employer can include and submit the salary data of these employees to IRAS. IRAS will not tax the same income again if the employee has already been assessed to tax.

10) File Form IR21 early Employer are advised to file Form IR21 early to allow sufficient time for tax clearance processing and avoid late-submission fine.

32 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

Access from: https://www.iras.gov.sg/IRASHome/Businesses/Employers/Tax-Clearance-for-Foreign---SPR-Employees--IR21-/

33 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

Access from: https://www.iras.gov.sg/irashome/e-Services/Businesses/Employers/

34 34 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

Enquiries:

Email: [email protected]

Helpline: 1800-356 8300

35 35 © 2015 Inland Revenue Authority of Singapore. All Rights Reserved.

The information presented in the slides aims to provide a better general understanding of Employers’ Tax Clearance Obligations and is not intended to comprehensively address all possible tax issues that may arise. This information is correct as at 010915(DDMMYY). While every effort has been made to ensure that this information is consistent with existing law and practice, should there be any changes, IRAS reserves the right to vary our position accordingly.

Thank You