tax and managerial effects of transfer pricing on … · tax and managerial e⁄ects of transfer...

TRANSCRIPT

DISCUSSION PAPER SERIES IN ECONOMICS AND MANAGEMENT

Tax and Managerial Effects of Transfer Pricing on Capital and Physical Products

Oliver Duerr, Thomas Rüffieux

Discussion Paper No. 17-19

GERMAN ECONOMIC ASSOCIATION OF BUSINESS ADMINISTRATION – GEABA

Tax and Managerial Effects of Transfer Pricing on

Capital and Physical Products∗

Oliver M. Duerr† Thomas Rüffi eux‡

March 27, 2017

- Preliminary and Incomplete Draft; please do not cite without author’s permission -

∗We thank Robert F. Goex and seminar participants at the University of Zurich for valuable comments

and suggestions.†Dr. Oliver M. Duerr, Esslingen University of Applied Sciences, Department of Management, Flandern-

strasse 101, D-73732 Esslingen, Germany, Tel.: +49 711 397 4312, eMail: [email protected]‡Thomas Rüffi eux, University of Zurich, Chair of Managerial Accounting, Seilergraben 53, CH-8001

Zurich, Switzerland, Tel.: +41 44 634 5967, eMail: thomas.rueffi [email protected].

1

Tax and Managerial Effects of Transfer Pricing on Capital and PhysicalProducts

Abstract We study the interrelation between product and capital transfer prices and

their effects on the optimal decision authority in multinational companies in an analytical

transfer pricing model. We find that in the case of centralized decisions both transfer prices

only serve as tax shifting devices and are independent of each other. In contrast, if operating

decisions are delegated to better informed subsidiaries, product and capital transfer prices

are interdependent and cannot be set independently. Because both transfer prices induce

negative coordination effects, either on the quantity or the capital invested, the interrelation

between the product and the capital transfer price is negative. We further show that, despite

this interrelation of transfer prices, the decentralized case can be an optimal structure of the

multinational company (MNC) due to the asymmetric information structure.

Keywords: Transfer Pricing, Multinationals, Capital Transfer Pricing

2

1 Introduction

The research on transfer pricing has a long tradition in management accounting. Start-

ing with Hirshleifer (1956), the research focus was on internal coordination. Despite other

extensions (e.g. asymmetric information (Wagenhofer (1994)), specific investments (Edlin

and Reichelstein (1995)) and strategic interactions (Goex (2000))), tax saving issues have

attracted a lot of attention during the last decade.1 The global transfer pricing report by

Ernst&Young (2013) for example shows that two-thirds of companies identify tax issues

(especially tax risk management) as their top priority in transfer pricing. In the manage-

ment accounting literature Baldenius et al. (2004) were among the first who analytically

analyze the integration of tax and managerial objectives in transfer pricing. Others ex-

tended the model with tax, and managerial objectives by adding specific investments (Duerr

and Goex (2013)), strategic interactions (Duerr and Goex (2011)) or intangibles (Johnson

(2006)). What has been largely ignored so far in the management accounting literature is

the analysis of transfer prices for physical products and for capital in an integrated analytical

model. This is notably astonishing because according to the global transfer pricing report

by Ernst&Young (2013) transfer pricing on capital is rated the second most important area

for MNCs.2

However, research on capital transfer prices is widely discussed in the public finance

literature. The studies on capital transfer prices in this literature stream mostly assume

centralized MNCs and focus on welfare effects and taxation issues, instead of optimal transfer

pricing issues.3

Our study thus contributes to the transfer pricing literature in management accounting

in the following ways. We integrate transfer pricing for physical goods and for capital in a

single model. As far as we know, our model is the first that integrates both transfer prices

in a single model setting. We compare centralized and decentralized decisions, the effects on

optimal transfer pricing and the interaction between physical and capital transfer prices.

We find the following results. First, we show that in the case of centralized investment

and quantity transfer decisions, the transfer prices for capital and for products can be set

1See Göx/Schiller (2007) for an extensive overview of analytical transfer pricing models.2See Ernst & Young (2013) survey where intra group financial arrangements and intangible property are

listed second and third on areas of transfer pricing controversy.3See e.g. Grubert (1998, 2003).

3

independently of each other. Further we find that the transfer prices only serve the tax

minimizing function. Second, we find in the case of decentralized investment and quantity

transfer decisions, that capital and product transfer prices are interdependent and cannot be

set independently of each other. Therefore a MNC has to be aware of the interdependencies

and has to take the mutual effects into account when setting the optimal transfer prices.

The model is based on a multinational corporation who uses a transfer price for inter-

nally supplied intermediate goods and a second transfer price for capital provided to its

subsidiaries. In addition to a standard analytical transfer pricing model we allow the opera-

tive subsidiaries to make capital investments under asymmetric demand information. In the

centralized case the MNC’s headquarter (HQ) takes all decisions, i.e. it determines transfer

prices, investments and quantity transferred. Our analysis reveals that in this setting, the

optimal capital and product transfer prices are set independently of each other. The transfer

prices have no coordinative function and solely serve the purpose of tax minimization. We

also find that optimal investments are larger in the presence of taxes than without taxes

because interest payments on the capital investments are tax deductible. A similar effect

results for the quantity that also increases (decreases) in the product transfer price for a

higher (lower) tax rate in the buyer’s country.

In the case of decentralized quantity and investment decisions, we find that transfer prices

have additional coordinative effects on quantities and investments. Because transfer prices

reflect the buyer’s marginal costs of the internally supplied product or capital, higher transfer

prices have direct negative effects on quantities and investments. The investments affect

marginal returns and costs and thus also have an indirect effect on the quantity decision.

Therefore, in the decentralized case, the optimal product and capital transfer prices are

interdependent of each other. In fact, we find that both transfer prices are negatively related

to each other. The intuition of this result is that the sequential decisions on investments

and quantities both have an impact on each other’s marginal returns and costs. A lower

quantity, induced by an increase in the product transfer price, leads to a decrease in marginal

investment returns and thus to a lower capital transfer price. Lower investments, induced by

an increase in the capital transfer price, in turn decrease marginal returns of the quantity and

thus lead to a lower product transfer price. However, we show that despite those negative

coordination effects the decentralization of investment and quantity decisions can be optimal

for a MNC. This result is due to the asymmetry of demand information between the HQ

and the subsidiaries and the resulting trade-off between the coordination and tax effect on

4

the one side and an information effect on the other side.

The remainder of the article is organized as follows. In Section 2, we present the basic

model. Section 3 characterizes the benchmark case where all decisions are taken centrally

by the headquarter. Section 4 discusses the decentralized planning case where the decisions

about the quantity and capital investments are delegated to the operative subsidiaries. In

section 5, a parametric example supports our findings. Section 6 concludes.

2 Model setup

We consider a MNC that consists of a HQ and three legally separate subsidiaries: a seller

(subsidiary S), a buyer (subsidiary B) and an internal financing company (subsidiary F ).

The subsidiaries are located in different tax jurisdictions with potentially different tax

rates.4 Subsidiary S produces an intermediate product that is supplied to subsidiary B

who processes it into a final product and sells it at a price p on the product market. For

means of simplicity, we assume one unit q of the intermediate product is transformed into

one unit of the final product. In exchange for each unit q of the intermediate product the

buyer pays the seller a product transfer price (PTP) t. Producing q units of the intermediate

product, the seller incurs production cost C(q, kS) that can be reduced by investing capital

kS in cost-saving activities. Accordingly, we assume the following additively separable cost

function C(q, kS) for the seller:

C(q, ks) := C1(q) + C2(kS) · q. (1)

The cost function consists of variable production costs C1(q) and a cost reduction effect

C2(kS) of the investment kS with the following properties:

∂C1(q)

∂q> 0,

∂2C1(q)

∂q2≥ 0, (2)

∂C2(kS)

∂kS< 0,

∂2C2(kS)

∂k2S≥ 0. (3)

4We assume no profit repatriations to the HQ, e.g. via dividend payments, which allows us to neglect

the tax rate of the headquarter.

5

Property (2) implies that the cost function is increasing and convex in the quantity q.

Condition (3) means that an investment kS reduces the cost of production for any given

quantity q at a decreasing marginal rate. The investment of capital kS results in utilization

cost of capital, denoted as IS(kS) which can be different from the pure amount of capital in-

vestment due to additional efforts to integrate new production equipment and organizational

changes. The utilization cost function has the following properties:

∂IS(kS)

∂kS> 0,

∂2IS(kS)

∂k2S≥ 0, (4)

implying that the utilization cost of capital is increasing in kS at an increasing marginal rate.

To keep the model focused on purposes of transfer pricing, we abstract from competi-

tion on the final product market and assume the subsidiary B to be a monopolist, facing

a decreasing price function in the quantity q. The demand on the product market is uncer-

tain and depends on the state of the world θ := (θ1, θ2), represented by two stochastically

independent random state variables θ̃1 and θ̃2.5

Alike the seller, the buyer can invest capital kB in marketing activities that increase rev-

enues. The revenue function R(q, θ, kB) is defined as:

R(q, θ, kB) := (R1(q, θ) +R2(kB)) · q. (5)

Its first part, R1,is the price function and depends on the quantity q and the realization of

the state of the world θ, whereas the second part, R2, represents the additional revenues

from marketing activities. The price function and the marketing revenue function have the

following properties:

∂R1(q, θ)

∂q< 0,

∂2R1(q, θ)

∂q2≤ 0, (6)

∂R2(kB)

∂kB> 0,

∂2R2(kB)

∂k2B≤ 0. (7)

The first property (6) states that the price function, R1, is decreasing and concave in the

quantity q. The second property (7) implies, that R2 is increasing in the amount of capital

invested kB but at a decreasing rate. As for the seller, the investment of capital kB implies

utilization cost IB(kB) that are convex in the amount of capital invested:

∂IB(kB)

∂kB> 0,

∂2IB(kB)

∂k2B≥ 0. (8)

5This setting is akine to Edlin and Reichelstein (1995).

6

The financial subsidiary’s scope of business is to provide capital to subsidiaries B and S

to fund their investments. Subsidiary F serves solely as an internal capital provider without

any decision-making authority. In exchange for capital kB and kS, subsidiaries B and S

have to pay the financing company an interest rate of r ∈ [r;_r] per unit of capital, referred

to as capital transfer price (CTP). The lower bound r represents the interest rate at which

subsidiary F can raise funds from the global capital market, the upper bound_r is the

maximum rate accepted by the tax authorities. Further we assume the lower bound of the

capital transfer price to be constant and independent of kB and kS.6 Likewise, we define an

acceptable range for the product transfer price t ∈ [t, t], such that t lies between marginal

production cost t = ∂C(q, kS)/∂q and the market price per unit of the final product t = p.

Due to the MNC’s possibility to raise funds from the global capital market, it faces few

restrictions for its financing subsidiary’s location. In order to benefit from tax savings, the

company has a vested reason to place subsidiary F in a country where the tax rate on

interest income is as low as possible. In contrast, the MNC might face more legal, political

and organizational restrictions for the location of its HQ. This finally makes a legally separate

and delocated financing subsidiary plausible and allows us to set the financing company’s

tax rate τF equal to zero. We define the effective tax rate for subsidiary S as τ ≥ 0 and the

one for subsidiary B as τ + δ ≥ 0, with δ ∈ [−τ ; 1− τ ].

The timeline of events and the information structure about the realization of the state

of the world θ is as follows:

[Please insert figure 1 about here]

The timeline starts with the HQ’s decision on the capital and the product transfer price,

r and t. At date t = 2, subsidiaries B and S observe the realization of the state variable θ̃1,

that gives them better, though not precise information about the product demand. Based on

that private information, they decide in t = 3 on the optimal amounts of capital investments

kB and kS. At date t = 4, subsidiary B observes the realization of θ̃2. Thus, subsidiary

B has full information about the product demand and decides at date t = 5 about the

optimal quantity ordered from subsidiary S. At the last stage, the transfer of q units of the

6We abstract from the case where the amount of capital raised influences the interest rate and assume the

group’s overall financing conditions on the global capital market to be independent of the concrete amount

of capital raised.

7

intermediate product takes place and the payments are settled. As it is usually the case in

product transfer pricing literature, we assume that communication of the realizations of the

state variables to the headquarter is limited such that the HQ cannot write any contract on

their realization.7 Therefore, the HQ can base its decisions solely on its expectation about

θ̃1 and θ̃2.

The three subsidiaries’after tax profits then unfold as:

ΠB(q, kB, θ) = (1− τ − δ) · ((R1(θ, q) +R2(kB)) · q − t · q − IB(kB)− r · kB) (9)

ΠS(q, kS) = (1− τ) · (t · q − C1(q)− C2(kS) · q − IS(kS)− r · kS) (10)

ΠF (kS, kB) = (r − r) · (kB + kS) (11)

The buyer’s after tax profit ΠB(q, kB, θ) consists of revenue R(q, θ, kB) minus the transfer

payment to the seller, minus the utilization cost of the invested capital and the interest paid

to subsidiary F . For means of simplicity we assume that interest payments are fully tax

deductible.8 Accordingly, the seller’s after tax profit, ΠS(q, kS), is calculated as the buyer’s

transfer payment minus the production cost, minus the utilization cost of the invested capital

kS and the interest paid to subsidiary F . Subsequently, the financing subsidiary’s profit

ΠF (kS, kB) consists of the difference between the interest r paid on funds raised on the

global capital market and the interest r gained from capital provided to subsidiaries B and

S.

The MNC’s after tax profit Π(q, kS, kB,θ) results as the sum of the three subsidiaries’

after tax profits:

Π(q, kS, kB, θ) = (1− τ − δ) · ((R1(θ, q) +R2(kB)) · q − t · q − IB(kB)− r · kB)

+(1− τ) · (t · q − C1(q)− C2(kS) · q − IS(kS)− r · kS)

+(r − r) · (kB + kS) (12)

In the following section we analyze the centralized planning case as a benchmark, where the

HQ takes the decisions about transfer prices, investments and the quantity transferred.

7The assumption that both managers observe the realization θ but outsiders do not is akine to Baldenius,

Reichelstein, Sahay (1999) and Edlin and Reichelstein (1996).8We do not consider so-called thin capitalization rules used in some countries that disallow firms to deduct

interest payments from taxable profit under certain circumstances.

8

3 Centralized planning (benchmark case)

As benchmark, we analyze a setting of centralized planning where the headquarter takes

all decisions, i.e. the HQ determines the quantity q transferred between B and S, the

subsidiaries capital investments kB and kS, the product transfer price t and the capital

transfer price r. The HQ, unlike the managers of subsidiaries B and S, cannot observe the

realizations of the state variables θ̃1 and θ̃2 and has to base its decisions on expectations

E[θ̃1] and E[θ̃2]. Therefore the group’s expected profit results as:

Eθ[Π(q, kS, kB, θ)] = (1− τ − δ) · (Eθ[R1(θ, q) · q] +R2(kB) · q − IB(kB))

+(1− τ) · (−C1(q)− C2(kS) · q − IS(kS))

+δ · t · q + (r · τ − r) · kS + (r · (τ + δ)− r) · kB (13)

Because the HQ takes all decisions based on the same information the decision process

can be modeled as a simultaneous optimization problem. Maximizing the group’s expected

profit to the capital and product transfer price yields the following optimality conditions:

∂Eθ[Π(q, kS, kB, θ)]

∂r= τ · kS + (τ + δ) · kB ≥ 0 (14)

∂Eθ[Π(q, kS, kB, θ)]

∂t= δ · q. (15)

Inspecting the above conditions (14) and (15) we derive our first proposition:

Proposition 1: In the centralized case, the optimal CTP and the optimal PTP are set

independently of each other. The optimal CTP is set at the upper bound of the admissible

interval, r = r, and the optimal PTP is set at the upper (lower) bound t = t ( t = t) for

a positive (negative) tax rate difference δ > 0 ( δ < 0). If the tax rate difference between

subsidiaries B and S is zero, δ = 0, the optimal PTP has no effect on the expected profit

and can be set arbitrarily between t and t.

Proof: Results directly from the FOC’s (14) and (15).

Condition (14) is positive for all levels of capital investments kB and kS and represents the

group’s tax benefit from shifting profits to the financing subsidiary that has the lowest tax

rate within the group. The similar argument holds for the product transfer price. Condition

9

(15) is positive or negative, depending on the tax rate difference δ between the subsidiaries

B and S. If the tax rate difference is δ > 0 (δ < 0), condition (15) is positive (negative) and

the optimal PTP is set at the highest (lowest) admissible level what results in optimal profit

shifting. Because all decisions are taken by the HQ there is no coordinative function for the

transfer prices. Therefore they can be set independently of each other and have only a tax

optimization function.

The optimality conditions for the HQmaximizing the group’s expected profit with respect

to the quantity q and the investment amounts kB and kS are as follows:

∂Eθ[Π(q, kS, kB, θ)]

∂q= (1− τ − δ) · (Eθ[R1(θ, q) + q · ∂R1(θ, q)

∂q] +R2(kB))

+(1− τ) · (−∂C1(q)∂q

− C2(kS)) + δ · t = 0 (16)

∂Eθ[Π(q, kS, kB, θ)]

∂kB= (1− τ − δ) · (∂R2(kB)

∂kB· q − ∂IB(kB)

∂kB) + (r · (τ + δ)− r) = 0 (17)

∂Eθ[Π(q, kS, kB, θ)]

∂kS= (1− τ) · (−∂C2(kS)

∂kS· q − ∂IS(kS)

∂kS) + (r · τ − r) = 0. (18)

Inspecting the conditions (16), (17), and (18) we state the following lemma 1:

Lemma 1: The optimal quantity increases (decreases) in the product transfer price if the

tax rate difference is positive (negative) and the optimal investments increase in the capital

transfer price. If we assume no tax rate difference, δ = 0, condition (16) reveals that

the optimal quantity transferred would equate expected marginal cost of production with

expected marginal revenues. This result is consistent with findings from traditional product

transfer pricing literature for the case of centralized decisions in absence of taxes.9 If indeed

subsidiary B and S exhibit different tax rates, δ 6= 0, then according to condition (16)

the optimal quantity increases (decreases) in the PTP if the tax rate difference is positive

(negative). This effect is due to the fact that the product transfer price is tax deductible for

the buying subsidiary. Therefore a positive tax rate difference δ > 0, acts like a tax subsidy

9Already Hirshleifer (1956) and Schmalenbach (1908/1909) show that in the absence of an external market

and specific investments, the optimal transfer price is set to the marginal cost of production.

10

and makes the transfer of a higher quantity favorable. The same logic applies to a negative

tax rate difference δ < 0.

Inspecting the two conditions (17) and (18) reveal that in absence of tax rate differences

between the operating subsidiaries B and S and the financing subsidiary F , that is τ =

0 and δ = 0, the optimal investment levels would equate the expected marginal returns

with expected marginal investment costs. In the case of a tax rate difference, the optimal

investment amounts increase in the capital transfer price r. Like for the product transfer

price, the effect is due to a tax saving effect. The capital transfer price paid to the financing

subsidiary is tax deductible for the investing subsidiaries and thus makes higher investments

more favorable because of the lower taxes that have to be paid. Since we assumed a tax rate

of zero for the financing subsidiary, this effect is always positive.

The key element for these two effects of the product and capital transfer price is that

all decisions are taken centrally. This means that the two transfer prices only have a tax

shifting function but are not vital to coordinate optimal decisions. In conclusion, since both

transfer prices are solely used for profit shifting and the investments and the quantity are

set by the HQ, the two transfer prices can be set independent of each other.

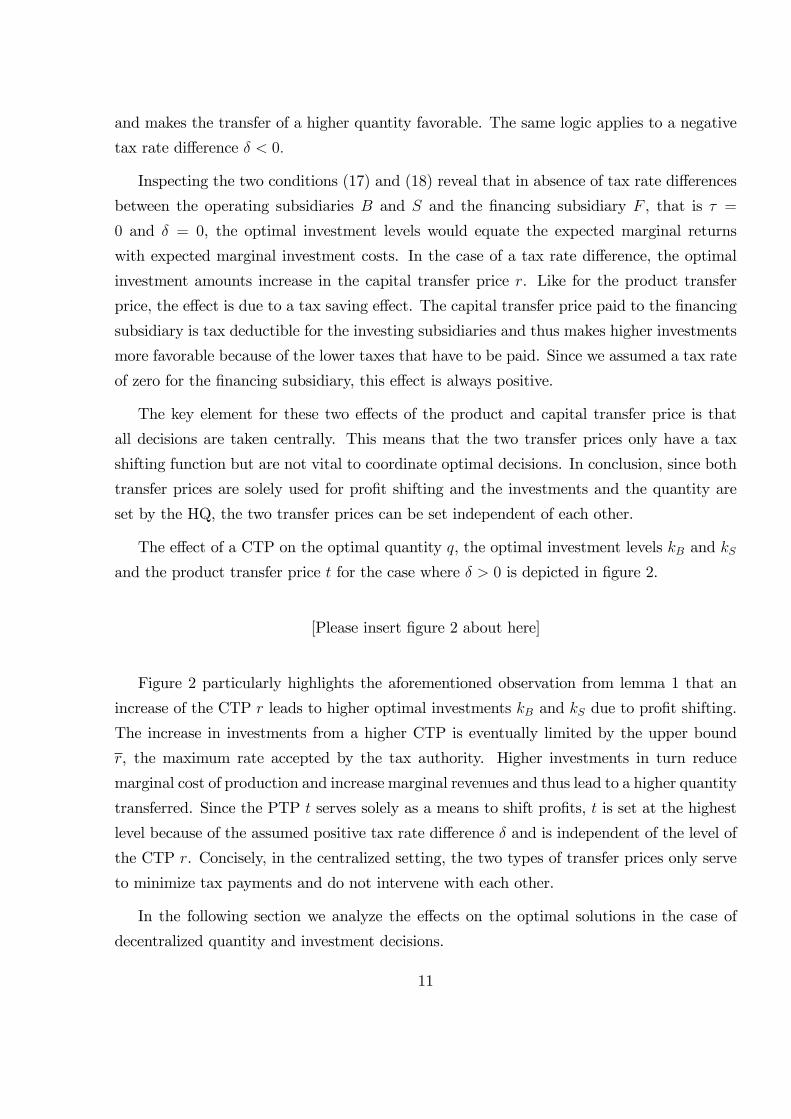

The effect of a CTP on the optimal quantity q, the optimal investment levels kB and kSand the product transfer price t for the case where δ > 0 is depicted in figure 2.

[Please insert figure 2 about here]

Figure 2 particularly highlights the aforementioned observation from lemma 1 that an

increase of the CTP r leads to higher optimal investments kB and kS due to profit shifting.

The increase in investments from a higher CTP is eventually limited by the upper bound

r, the maximum rate accepted by the tax authority. Higher investments in turn reduce

marginal cost of production and increase marginal revenues and thus lead to a higher quantity

transferred. Since the PTP t serves solely as a means to shift profits, t is set at the highest

level because of the assumed positive tax rate difference δ and is independent of the level of

the CTP r. Concisely, in the centralized setting, the two types of transfer prices only serve

to minimize tax payments and do not intervene with each other.

In the following section we analyze the effects on the optimal solutions in the case of

decentralized quantity and investment decisions.

11

4 Decentralized quantity and investment decisions

In the decentralized case, the HQ assigns the investment decisions to the subsidiaries B and

S and provides the buyer with the authority to set the quantity transferred. The motivation

to delegate these decisions is based on the assumption that the HQ cannot observe the

realization of the state variables θ̃1 and θ̃2. The subsidiaries indeed benefit from private

information and sequentially learn the realization of the state variables. In t = 2, both

subsidiaries observe the realization of the state variable θ̃1 before, in t = 3, they have to

decide about their respective capital investments. After the investment decision, subsidiary

B receives additional private information about the realization of the state variable θ̃2.

Observing θ1 and θ2, subsidiary B learns the true demand in the product market. Since

the subsidiaries of a MNC generally face multiple projects where in turn each project might

request a wide range of investment decisions it seems reasonable to assume that an elaborated

communication of all private information to the HQmight not be feasible or simply too costly.

In such a setting, the delegation of investment decisions from the headquarter to the better

informed subsidiaries may finally increase investment and process effi ciency.10

In order to solve the optimization problem for the sequential decision structure, we apply

backward induction. At the last stage subsidiary B maximizes its profit ΠB w.r.t. the

quantity q, yielding the optimality condition:

∂ΠB(q, kB, θ)

∂q= R1(q, θ) + q · ∂R1(q, θ)

∂q+R2(kB)− t = 0. (19)

Comparing condition (19) to the optimality condition in the centralized case (16) we observe

two differences from delegating the quantity decision to subsidiary B. First, condition (19)

is based on the realization of θ, respectively θ1 and θ2, instead of its expectation. Second,

the optimality condition (19) implies that the quantity decision now also depends on the

product transfer price t. We state these observations in the following lemma.

Lemma 2: In the case of decentralized quantity decision the optimal quantity q is decreasing

in the product transfer price t and increasing in the amount of invested capital kB.

We face the traditional coordination problem. The optimal quantity under decentralized

versus centralized planning is of equal amount if the product transfer price t is set to marginal

10The assumption of asymmetric information that arises from too costly or impossible communication of

all local information to the central management has already been mentioned in Kaplan & Atkinson (1998,

p. 291) as one major reason to decentralize decisions.

12

cost. If t exceeds marginal cost, the optimal quantity in the decentralized setting is lower

than in the centralized case. On the one hand, this effect stems from a higher t inducing

higher marginal costs for subsidiary B. On the other hand, unlike the HQ in the benchmark

case, subsidiary B does not internalize the group’s benefit from tax savings by shifting

profits to the lowest taxed subsidiary. Instead, subsidiary B bases its decision about the

quantity q only on its own profit and neglects the other subsidiaries’profits as well as the

overall benefit for the MNC. Consequently, subsidiary B’s decision on the optimal quantity

q◦(θ) := q(θ1, θ2, kB, t) depends solely on its marginal return, that in turn is a positive

function of the investment level kB, the product transfer price t as well as the realization of

the state variables θ̃1 and θ̃2.

Quite intuitively, in the prevailing model setting with asymmetric information and dele-

gated investment decisions, both subsidiaries set the investment amounts in order to optimize

their profits, given their information θ1 about the demand in the product market. In the

centralized case where the headquarter lacks this private information and bases its decisions

on expectations, the HQ is more likely to prescribe ineffi cient investment amounts. In that

respect, the delegation of the investment decisions to the subsidiaries may increase invest-

ment effi ciency but lead to divisional instead of overall profit maximization. The respective

optimality conditions of the subsidiaries w.r.t. the capital investments in the decentralized

case are as follows:

∂Eθ2[ΠB(q

◦(θ), kB, θ)

]∂kB

= Eθ2 [q◦(θ)] · ∂R2(kB)

∂kB− ∂IB(kB)

∂kB− r = 0, (20)

∂Eθ2[ΠS(q

◦(θ), kS)

]∂kS

= −Eθ2 [q◦(θ)] · ∂C2(kS)

∂kS− ∂IS(kS)

∂kS− r = 0. (21)

The optimal investment amounts k◦B := kB(Eθ2 [q

◦(θ)], r) and k

◦S := kS(Eθ2 [q

◦(θ)], r)

depend on the expected quantity and the capital transfer price. Both subsidiaries know

θ1 but at the time the investment decisions have to be reached the realization of θ̃2 is

still unknown. Therefore, subsidiaries B and S have to base their investment decisions on

expectations about the true demand. Considering the optimality conditions (20) and (21),

the capital transfer price r represents additional marginal investment costs to divisions B

and S. Thus a higher capital transfer price makes capital investments more costly and will in

turn reduce the subsidiaries investment incentives. We summarize this effect in the following

lemma 3.

13

Lemma 3: The optimal capital investments kB(Eθ2 [q◦(θ)], r) and kS(Eθ2 [q

◦(θ)], r) are de-

creasing in the capital transfer price r.

This is in contrast to the optimality conditions (17) and (18) in the centralized decision

case. In the benchmark the HQ prescribes the investment amounts and the group benefits

from a higher CTP due to profit shifting, respectively tax savings. In the decentralized

setting, the subsidiaries first care about their divisional profits and indeed neglect the group’s

tax benefits and the effects on the other subsidiaries’ profits when deciding about their

respective capital investments. Consequently, in the decentralized planning case, the effect

of r on the optimal investments is negative and is in the opposite direction compared to the

centralized setting.

In the final step of the optimization process, the HQ sets the capital transfer price r as well

as the product transfer price t to maximize the group’s expected profit Eθ[Π(q◦(θ), k

◦B, k

◦S, θ)].

To shorten notation we define Vθ(q◦, k

◦B, k

◦S) := Eθ[Π(q

◦(θ), k

◦B, k

◦S, θ)]. Maximizing the

group’s expected profit w.r.t. the capital and product transfer price, yields the following

optimality conditions:

∂Vθ(q◦, k

◦B, k

◦S)

∂r= Eθ[(τ + δ) · k◦B + τ · k◦S

+(1− τ) · (t− (∂C1(q

◦(θ))

∂q− C2(k

◦

S))) · ∂q∂kB

· ∂kB∂r

+(r − r) · ∂(k◦B + k

◦S)

∂r] = 0, (22)

∂Vθ(q◦, k

◦B, k

◦S)

∂t= Eθ[δ · q

◦(θ) + (1− τ) · (t− (

∂C1(q◦(θ))

∂q− C2(k

◦

S))) · ( ∂q∂kB

· ∂kB∂t

+∂q

∂t)

+(r − r) · ∂(k◦B + k

◦S)

∂t] = 0. (23)

Solving these FOC’s for r and t results in an optimal CTP r◦

:=r(Eθ[q◦(θ), k

◦B, k

◦S, θ])

and an optimal PTP t◦

:= t(Eθ[q◦(θ), k

◦B, k

◦S, θ]) being functions of the expectations about

the optimal quantity, the optimal investment amounts and the realization of the state of

the world. Inspecting the optimality conditions (22) and (23) we observe that the optimal

transfer prices are influenced by three distinct effects.

14

The optimal capital and product transfer prices r◦and t

◦balance a tax effect with two

negative coordination effects on the optimal quantity and the optimal capital investments.

The first term in the optimality conditions (22) and (23) represents the tax effect. This effect

is due to the transfer prices’serving as means to shift profits. With respect to the capital

transfer price, the profit is always shifted to the financing subsidiary and the tax effect is

unambiguously positive. For the product transfer price, the tax effect depends on the tax

rate difference δ between the subsidiaries B and S and can either be positive or negative.

The second term we refer to as quantity coordination effect. For the capital transfer price,

this effect is negative. Lemma 3 states that a higher capital transfer price reduces the

capital investment, ∂kB/∂r < 0, since the capital transfer price r represents additional

costs to the subsidiaries. Lemma 2 states that a higher capital investment increases the

quantity, ∂q/∂kB > 0. Therefore, the second term in condition (22) is strictly negative.

For the product transfer price, this effect is also negative as Lemma 2 states that a higher

product transfer price decreases the quantity, ∂q/∂t < 0. Finally, we observe a third effect

that we refer to as investment coordination effect. As aforementioned, with respect to the

capital transfer price, Lemma 3 states that a higher capital transfer price reduces investment

incentives. However, for the product transfer price we face an indirect effect on the optimal

capital investments that arises from the decision about the optimal quantity. Condition (19)

shows that a higher product transfer price decreases the optimal quantity and thus decreases

marginal investment returns what finally decreases optimal investments.

Comparing the optimality conditions in the decentralized setting (22) and (23) to the

conditions in the centralized case (14) and (15), the first term that is related to the direct tax

effect is similar. The two additional effects, the quantity and investment coordination effects,

result from delegating the quantity and investment decisions to the subsidiaries. While the

coordination of quantity and investment decisions is not necessary in the centralized setting,

a trade-off results in the decentralized case. The headquarter has to balance the positive tax

effect from higher transfer prices with the negative effects on the investment decisions and the

quantity decision. Because the subsidiaries B and S maximize their respective profits and

not the group’s profit, they face an increase in their marginal costs (intermediate product

and capital) but they do not internalize the tax benefits for the whole MNC from profit

shifting. Compared to the centralized setting, the two additional effects are thus weakly

negative and the resulting optimal product and capital transfer prices in the decentralized

setting are weakly lower than in the centralized case.

15

In addition, the optimality conditions (22) and (23) show that the CTP and PTP are no

longer independent of each other. We summarize this interrelation between the two transfer

prices in proposition 2.

Proposition 2: The optimal CTP and PTP negatively relate to each other, i.e. the optimal

CTP is decreasing in the optimal PTP and vice versa.

Proof: The second term of condition (22), we referred to as quantity coordination effect, is

negative in r and is scaled by the difference between t and the marginal cost. Therefore, a

higher product transfer price t intensifies the negative quantity coordination effect of r. The

proof for the PTP is similar. The third term in condition (23) represents the investment

coordination effect of the optimal product transfer price. This effect is negative in t and

is scaled by the difference between the capital transfer price and the interest paid on the

capital market. A higher capital transfer price r thus intensifies the negative investment

coordination effect of t.

The intuition for the interaction between the two transfer prices is straight forward. The

optimal capital transfer price internalizes the negative effect on the optimal investment kBthat results in a lower quantity. This effect is scaled by the difference between the product

transfer price and the marginal cost. If the product transfer price is equal to the marginal

cost, the quantity coordination effect is zero. A higher product transfer price results in a

higher quantity coordination effect that intensifies the negative effect on the capital transfer

price.

The intuition for the product transfer price is akin. The optimal product transfer price

internalizes the effect on the quantity and the resulting indirect effect on the capital invest-

ments kB and kS. This effect is scaled by the difference between the capital transfer price and

marginal cost of capital. If the capital transfer price is equal to the marginal cost of capital,

the investment effect is zero. A higher capital transfer price results in a higher investment

coordination effect that intensifies the negative effect on the product transfer price.

Figure 3 illustrates these effects of r on the optimal investment amounts, the optimal

quantity transferred and the PTP, again for the case δ > 0.

[Please insert figure 3 about here]

To sum up, in the case of decentralized quantity and investment decisions, implementing

a capital transfer price benefits the group from saving taxes via profit shifting, but leads

16

to lower investments, distorted managerial decisions, a negative effect on the PTP and its

respective tax savings.

5 A parametric example

In this section we provide a parametric example to illustrate the relations between the two

transfer prices, the impact of different tax rates and consequences of the decision to centralize

or decentralize.

For means of simplicity we assume the random state variable θ̃ to be a sum of θ̃1 and θ̃2,

where θ̃1 and θ̃2 are uncorrelated, uniformly distributed over an interval [−ξ, ξ] and exhibitan expected value of E[θ̃l] = 0 and a variance of V ar(θ̃l) = 1/12 · (ξ − (−ξ))2, for l ∈ {1, 2}.Further we assume quadratic utilization cost of capital Ii(ki) = γ · k2i , i ∈ {B, S}, where γis a scaling parameter. The revenue function for the buyer is specified as:

R(q, θ1, θ2, kB) = (R1(θ1, θ2, q) +R2(kB)) · q

= (a+ θ1 + θ2 − q + α · kB) · q (24)

and the seller’s cost of production is given by:

C(q, kS) = C1(q) + C2(kS) · q

= (c− α · kS) · q, (25)

where the scaling parameter α represents the investment effi ciency. The profit functions

of buyer B and seller S then unfold as:

ΠB(q, kB, θ1, θ2, t, r) = (1− τ − δ) · (R(q, θ1, θ2, kB)− t · q − IB(kB)− r · kB)

= (1− τ − δ) · ((a+ θ − q + α · kB − t) · q − γ · k2B − r · kB),(26)

ΠS(q, kS, t, r) = (1− τ) · (t · q − C(q, kS)− IS(kS)− r · kS)

= (1− τ) · ((t− c+ α · ks) · q − γ · k2S − r · kS). (27)

The profit function of the financial subsidiary F remains as in the general model and the

MNC’s profit function is simply the sum of the three subsidiaries profit functions.

17

5.1 The centralized case

In the centralized setting, the HQ sets the following optimal quantity q∗ according to condi-

tion (16) as:

q∗ =1

2· (a+ α · k∗B +

δ · t∗ + (1− τ) · (α · k∗S − c)(1− τ − δ) ). (28)

The parametric representation of the optimal quantity q∗supports lemma 1. The optimal

quantity increases (decreases) in the product transfer price if the tax rate difference δ is

positive (negative). Because the HQ takes its decisions based on the expectation about the

state variable θ̃, the quantity decision is not affected by the realization of θ. Further, from

equation (??) we observe that the decision about the optimal quantity depends also on the

capital investments. Plugging the parametric functions into the optimality conditions (17)

and (18), yields the following conditions on the optimal capital investments:11

∂Eθ[Π(q∗, kB, kS, θ)]

∂kB= (1− τ − δ) · (α · q∗ − 2 · γ · k∗B) + (τ + δ) · r∗ − r = 0, (29)

∂Eθ[Π(q∗, kB, kS, θ)]

∂kS= (1− τ) · (α · q∗ − 2 · γ · k∗S) + τ · r∗ − r = 0. (30)

Inspecting the above conditions (29) and (30), we find that the optimal capital invest-

ments increase in the capital transfer price r∗ what supports lemma 1. As mentioned above,

this effect results from a higher capital transfer price shifting taxes to the lowest taxed

subsidiary F . This finally makes higher investments more attractive for the MNC.

In this setting, the HQ also takes the decisions about the optimal transfer prices. The

resulting optimality conditions are identical to the benchmark case (see (14) and (15)).

These two conditions, (14) and (15), accede proposition 1. The two transfer prices can

be set independently of each other. The optimal capital transfer price is set at the upper

bound of the admissible interval r and the optimal product transfer at the upper or lower

level of the admissible interval, depending on the tax rate difference δ.

11One could solve these equations for the optimal investment amounts being aware that q∗ is in turn a

function of kB and kS . We forego this step due to the more intuitive representation of the interdependences

out of the FOC.

18

5.2 The decentralized case

In the decentralized setting the optimal quantity is denoted by q◦. The subsidiary B chooses

the optimal quantity according to the optimality condition (19). Using the parameterization

we derive the following optimal quantity:

q◦(θ) =

1

2· (a+ α · k◦B − t

◦+ θ1 + θ1). (31)

Comparing the optimal quantity q◦to the one in the centralized case (28), we find that

the optimal quantity q◦does not depend on the tax rates. Because subsidiary B does not

internalize the group’s tax benefits of profit shifting, the tax rate differences are not relevant

for the subsidiary‘s quantity decision. Further, as stated in lemma 2, the optimal quantity

q◦ decreases in the product transfer price t◦since a higher PTP represents higher costs to

the buyer. As a consequence of subsidiary B’s private information about the final demand,

the realization of the state variable θ directly affects the buyer’s decision about the optimal

quantity q◦(θ). Finally, the optimal quantity increases in subsidiary B’s capital investment

kB because it increases the product’s marginal revenues.

Applying the parametric specifications to the optimality conditions (20) and (21) yields:

∂Eθ2[ΠB(q

◦(θ), kB, θ)

]∂kB

= α · Eθ2 [q◦(θ)]− 2 · γ · k◦B − r

◦= 0, (32)

∂Eθ2[ΠS(q

◦(θ), kS)

]∂kS

= −α · Eθ2 [q◦(θ)]− 2 · γ · k◦S − r

◦= 0. (33)

Solving the optimality conditions yields the following optimal investment amounts:

k◦

B = k◦

S =α · (a− t◦ + θ1)− 2 · r◦

4 · γ − α2 . (34)

While in the centralized setting the optimal investments depend on the tax rates, they

do not rely on tax issues in the decentralized case. In that respect, the parametric example

shows that the subsidiaries do not internalize the opportunity to shift profits. In the decen-

tralized case, the capital transfer price represents additional cost to subsidiaries B and S

and leads to a decrease in the optimal investment amounts. Because the subsidiaries observe

the realization of θ̃1 their decision about the respective investments is directly affected by

19

θ1. Another difference to the centralized case is the dependence of the decentralized capital

investment decisions on the product transfer price. Compared to the centralized case, where

the PTP has no effect on the optimal quantity, in the decentralized setting, the product

transfer price influences the subsidiaries’s capital investment decisions through the expec-

tation about the optimal quantity. Finally, the decisions about the optimal transfer prices

remain to the HQ. Solving the respective conditions (22) and (23) and taking the parametric

specifications into account, we get the following optimality conditions w.r.t. the capital and

product transfer price:

∂Vθ(q◦, k

◦B, k

◦S)

∂r= (2 · τ + δ) · α · (a− t

◦)− 2 · r◦

4 · γ − α2

+(1− τ) · Eθ[(t−(c− α · α · (a− t

◦)− 2 · r◦

4 · γ − α2

))· ∂q

◦

∂kB· ∂k

◦B

∂r

]− 4

4 · γ − α2 · (r◦ − r) = 0, (35)

∂Vθ(q◦, k

◦B, k

◦S)

∂t= δ · (2 · γ · (a− t◦)− r◦

4 · γ − α2 )

+(1− τ) · Eθ[(t−(c− α · α · (a− t

◦)− 2 · r◦

4 · γ − α2

))·(∂q

◦

∂kB· ∂k

◦B

∂t+∂q

◦

∂t

)]− 2 · α

4 · γ − α2 · (r◦ − r) = 0. (36)

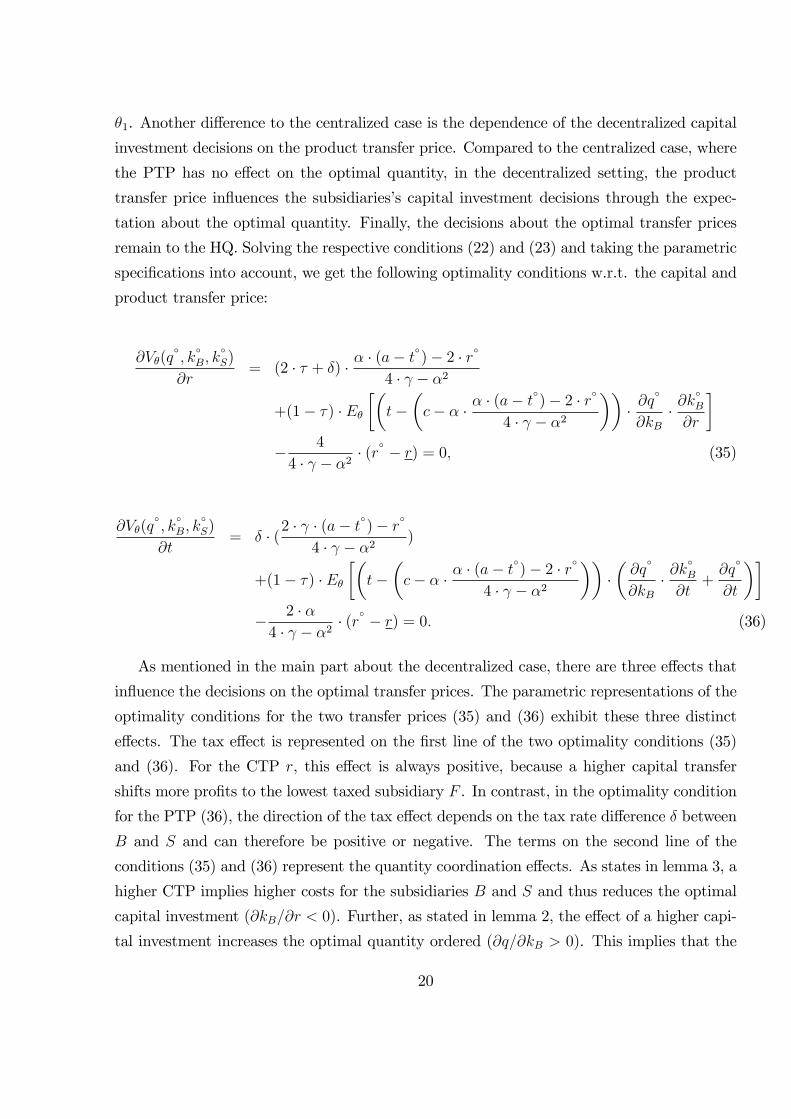

As mentioned in the main part about the decentralized case, there are three effects that

influence the decisions on the optimal transfer prices. The parametric representations of the

optimality conditions for the two transfer prices (35) and (36) exhibit these three distinct

effects. The tax effect is represented on the first line of the two optimality conditions (35)

and (36). For the CTP r, this effect is always positive, because a higher capital transfer

shifts more profits to the lowest taxed subsidiary F . In contrast, in the optimality condition

for the PTP (36), the direction of the tax effect depends on the tax rate difference δ between

B and S and can therefore be positive or negative. The terms on the second line of the

conditions (35) and (36) represent the quantity coordination effects. As states in lemma 3, a

higher CTP implies higher costs for the subsidiaries B and S and thus reduces the optimal

capital investment (∂kB/∂r < 0). Further, as stated in lemma 2, the effect of a higher capi-

tal investment increases the optimal quantity ordered (∂q/∂kB > 0). This implies that the

20

quantity coordination effect for the optimal CTP is unambiguously negative - as long as the

PTP exceeds marginal cost of production. If the PTP is identical to marginal production

cost, the effect becomes zero as in the standard transfer pricing model. Considering lemma

2 and lemma 3 and the fact, that ∂q/∂t < 0, the argumentation for the product transfer

price is similar. Finally, the third line in the conditions (35) and (36) represent the invest-

ment coordination effect. This effect is always negative because the investment amount is

decreasing in both transfer prices.

5.3 Some comparative statics

In order to analyze the effects of a variation in the tax rate difference and the uncertainty

about the state of the world, we conduct a numerical example with the following specifica-

tions:

τ = 0.2, δ ∈ [−0.15, 0.15], θ1 ∈ [−10, 10], θ2 ∈ [−10, 10], t = 70, r = 0.25, r = 0,

a = 100, c = 50, α = 0.05, γ = 0.05.

Solving the optimality conditions for the decision variables derived in the sections 5.2

and 5.3 for the centralized and decentralized case, we get the following results:

[Please insert table 1 about here]

First, we analyze the results for the centralized case. According to proposition 1 the two

transfer prices just have a tax saving function and are set at the bounds of the admissible

intervals. Because the financing subsidiary has a tax rate of zero, the capital transfer price

is set at the upper bound. The optimal product transfer price depends on the tax rate

difference δ between the subsidiaries and is set at the lower bound that is equal to marginal

cost for δ < 0 and at the upper bound for δ > 0. Both transfer prices are independent of

each other and only react to tax rate differences.

The optimal quantity increases in the product transfer price when the tax rate difference

becomes positive. This effect is stated in lemma 1 and is due to tax shifting opportunities

once the PTP is above marginal cost. Because the CTP does not vary in the centralized

case with δ, the increase in the investments comes from the higher quantity that increases

21

marginal returns of the investments. Finally, the expected profit is decreasing in the tax rate

difference because the tax rate for subsidiary B is increasing what reduces after-tax profits.

Second, we analyze the results for the decentralized case. For a higher (less negative)

tax rate difference δ, higher investments become more favorable for the MNC because of tax

shifting opportunities. Higher investments are thus stimulated by a lower CTP. Because the

PTP is already set at marginal cost it can be decreased only marginally to the lower marginal

cost that are induced by higher investments. Increasing the tax rate difference further to

positive levels has two effects. First, the PTP increases due to the tax saving effect of profit

shifting between subsidiariesB and S. Second, the CTP further decreases as the coordination

effects become more negative in the higher PTP. These negatively interacting effects between

the transfer prices is described in proposition 2. The effects on the optimal quantity and the

optimal investments are stated in lemmas 2 and 3. The optimal quantity is decreasing in the

PTP as it represents additional cost to the buyer. This in turn decreases marginal returns

of the investments and leads to reduced optimal investment levels. Finally, the expected

profit is decreasing in higher tax rates like in the centralized case. What is different is

that the profit for a negative or zero tax rate difference is higher in the decentralized case

than with centralized decisions. This effect appears because of the information asymmetry

between the HQ and the subsidiaries. The HQ can base the quantity and the investment

decision only on expected information whereas the subsidiaries have partial information at

the date of the investment decision and full information at the date of the quantity decision.

Therefore, the numerical example shows that despite of negative coordination effects in

the decentralized setting, the decentralization of decisions can be beneficial in the case of

asymmetric information between the HQ and the subsidiaries.

We summarize the effects of the tax rate differences δ < 0, δ = 0 and δ > 0 on the

optimal transfer prices in the following table 2:

[Please insert table 2 about here]

A graphical representation of the dependence of the HQ’s decisions about the transfer

prices on the tax rate difference δ and ultimately of the interaction between those three

effects is depicted in figure 4.

[Please insert figure 4 about here]

22

The figure on the left hand side shows the positive interdependence between the tax rate

difference δ and the product transfer price. The higher the tax rate difference between the

subsidiaries B and S, the higher the profit shifting opportunity and thus the higher the PTP.

The PTP is however increasing in δ at a decreasing marginal rate due to the amplifying

negative quantity and investment coordination effects. In case of a tax rate difference of

δ ≤ 0, the PTP is set to marginal cost of production because the tax effect and the quantity

and investment coordination effect are all three negative. Since the PTP and CTP interact

negatively, the effect for the capital transfer price is in the opposite direction. While the

tax effect of the CTP is positive for all tax rate differences, the investment coordination

effect is negative for all δ and the quantity coordination effect on r is zero for δ ≤ 0 and

negative for positive tax rate differences. However, the positive tax effect decreases in δ

due to a higher tax rate difference increasing the PTP that in turn reduces the buyer’s

capital investment and the quantity ordered. Hence, the increasing negative investment

and quantity coordination effects push the CTP further down. If we assume an upper

border r for the acceptable range of the CTP we would get a cap at the accepted upper

range of r, preventing the capital transfer price to be set above that threshold when the

tax rate difference becomes low. The values for the capital and product transfer prices in

table 1 also support proposition 2 and show the negative mutual interdependence between

the two transfer prices. Recall, for a tax rate difference δ > 0, the group benefits from

a higher product transfer price due to the opportunity to shift profits from subsidiary B

to subsidiary S. As mentioned in lemma 2, this however reduces the quantity ordered

by subsidiary B (increases the negative quantity coordination effect) because a higher PTP

means higher cost to the buyer that in turn decreases the quantity ordered. A lower quantity

ordered in fact decreases also the marginal investment returns of subsidiary B (increases the

negative investment coordination effect) and we face decreasing optimal investments out

of the amplification through the two negative effects. As a consequence of lower capital

investments, the positive tax effect decreases and the quantity coordination effect gets even

more negative that in turn leads to a lower CTP. For a tax rate difference of δ ≤ 0, the

optimal PTP is always set to marginal cost of production since subsidiary B faces a lower

tax rate than subsidiary S, inducing the MNC to keep the buyer’s profits within division

B. Further, as mentioned above, increasing the capital transfer price means, for all tax

rate differences, higher investment cost to the subsidiaries B and S and thus lower optimal

capital investments (higher negative investment coordination effect). That in turn reduces

23

the optimal quantity because lower investments reduce buyer B’s marginal returns from

investments and this ultimately reduces the group’s tax savings (decrease in the positive

tax effect). Overall, the group’s benefit out of profit shifting decreases such that a higher

CTP finally leads to a lower product transfer price. We depict that interaction between the

capital and the product transfer prices for the decentralized case in the following figure.

[Please insert figure 5 about here]

Figure 5 pinpoints the negative relation between the two transfer prices, i.e. that the

increase of one transfer price decreases the other transfer price. An intersection sets in,

where the aforementioned effects of a higher CTP offset the effects resulting from a lower

PTP and vice versa.

Finally the question arises if the decentralized case can be beneficial to the MNC. The

results of our numerical example, presented in table 1, have already shown that decentral-

izing the quantity and the investment decision can be beneficial for the MNC. Because the

decentralization decision ultimately depends on the uncertainty about the true state of the

world θ, respectively the benefit of private information of the subsidiaries B and S, we finally

depict the expected decentralized profits for the group depending on the uncertainty about

the state variable θ̃, respectively θ̃1 and θ̃2, and compare it to the expected centralized profit.

Figure 6 illustrates the change in expected group profits due to changes in the variance of

the state variables for the tax rate differences δ = −0.15, δ = 0 and δ = 0.15.

[Please insert figure 6 about here]

In Figure 6, the solid lines represent the expected decentralized profits, whereby in each

of the three figures the lower solid lines represent the case where there is no uncertainty

about the state variable θ̃2 and the upper solid lines represent the case for a variance of

θ̃2 of V ar(θ̃2) = 100/312. The dashed lines represent the expected centralized profits that

are independent of the uncertainty about the state variable θ. As we would expect, the

benefit of decentralization increases in the uncertainty about the state of the world θ. This

is graphically represented by the positive slope of the solid lines and is the effect of the

12The Variance of a uniformly distributed random variable θ̃2 betweeen [−10, 10], is: V ar(θ̃2) = 1/12 ·(10− (−10))2 = 100/3.

24

subsidiaries private information about the realization of the state variable θ̃1. in addition,

the upward shift of the solid lines is the additional benefit of the two subsidiaries B and

S private information about the realization of the second state variable θ̃2. This parallel

upward shift is a consequence of the scaling of the variance of θ̃2 by (1 − τ − δ) > 0, so an

increase in V ar(θ̃2) just amplifies the results for the expected decentralized profits to the

upside. As table 1 has indicated, the decision to decentralize also depends on the tax rate

difference δ. For a tax rate difference of δ ≤ 0, the quantity coordination effect is zero and the

investment coordination effect is negative. Lower capital investments in turn decrease the

tax effect, since less profits are shifted to the lowest taxed subsidiary, the capital provider

F . In result, for a tax rate difference of δ ≤ 0, the benefit of better private information

might dominate the positive tax effect that results from shifting profits to subsidiary F .

However, with an increasing tax rate difference, the positive tax effect and the negative

investment coordination effect both get stronger. Further, for a tax rate difference of δ > 0

the group faces also the negative quantity coordination effect that decreases the benefits from

decentralization even more. Thus, these three effects might finally dominate the benefits of

private information leaving the MNC better off by keeping all decisions within the HQ.

6 Conclusion

With the raise of multinational companies and their possibilities to raise capital on the global

market and to place subsidiaries in different locations, international coordination, financing

opportunities and tax issues have become important. The public finance literature addresses

this issues mainly in research about capital transfers and its tax implications while the

managerial transfer pricing literature mainly addresses transfer pricing on physical products

and managerial issues. We try to fill the gap in research about interrelations between product

and capital transfer prices.

In the benchmark setting, where the MNC’s headquarter takes all decisions, we show

that the optimal capital and product transfer price are set independently of each other.

This result is in concurrence with the transfer pricing literature on physical products that

states that in this case the transfer price serves solely to save taxes and has no coordinative

function. Further, we show that optimal investments in the centralized setting with taxes

are larger than without taxes. This is due to the fact that interest payments on the capital

25

invested are tax deductible. We also find that the quantity ordered increases (decreases) in

the product transfer price for a negative (positive) tax rate difference between the supplying

and producing subsidiary.

In the decentralized planning case, where quantity and investment decisions are delegated

to the operative subsidiaries of the multinational corporation, we find that transfer prices

do not just affect tax savings but entail additional coordinative effects on quantities and

investments. We show that those additional quantity and investment coordination effects

directly lead to lower quantities and investments, since the transfer prices represent marginal

costs to the buyer. Because the amount of capital invested ultimately affect marginal returns

and costs, we perceive an additional indirect effect on the quantity decision. In that respect,

we show that the two transfer prices are negatively related to each other. The intuition

for their negative interrelation is indeed found in the sequential decisions on investments

and quantities that have a negative impact on each other’s cost and returns. The key

findings is thus that the two transfer prices can no longer be set independent of each other

and the headquarter has to consider these interrelations while taking its decisions on the

optimal transfer prices. The amplitude of the three effects essentially depends on the tax

rate difference between the operative subsidiaries.

26

REFERENCES

Baldenius, T., Reichelstein, S., and Sahay, S. (1999). Negotiated versus cost-based transfer

pricing. Review of Accounting Studies, 4, 67—91.

Baldenius, T., Melumad, N., and Reichelstein, S. (2004). Integrating managerial and tax

objectives in transfer pricing. The Accounting Review, 79, 591-615.

Duerr, O.M. and Goex, R.F. (2011). Strategic incentives for keeping one set of books

in international transfer pricing. Journal of Economics & Management Strategy, 20,

269-298.

Duerr, O.M. and Goex, R.F. (2013). Specific investment and negotiated transfer pricing in

an international transfer pricing model. Schmalenbach Business Review, 65, 27-50.

Edlin, A.S. and Reichelstein, S. (1995). Specific investment under negotiated transfer

pricing: An effi ciency result. The Accounting Review, 70, 275-291.

Ernst & Young (2013): Navigating the choppy waters of international tax —2013 Global

Transfer Pricing Survey, http://www.ey.com/Publication/vwLUAssets/EY-2013_Global_

Transfer_Pricing_Survey/$FILE/EY-2013-GTP-Survey.pdf.

Goex, R.F. (2000): Strategic transfer pricing, Absorption Costing, and Observability. Man-

agement Accounting Research, 11, 327-348.

Goex, R.F. and Schiller, U. (2007). An economic perspective on transfer pricing. C.S.Chapman,

A.G. Hopwood, and M.D. Shields, ed., Handbook of Management Accounting Research

(Vol.2). Oxford: Elsevier, 673-693.

Grubert, H. (1998). Taxes and the division of foreign operating income among royalties,

interest, dividends and retained earnings. Journal of Public Economics, 68, 269-290.

Grubert, H. (2003). Intangible income, intercompany transactions income shifting, and the

choice of location. National Tax Journal, 56, 211-242.

Hirshleifer, J. (1956). On the economics of transfer pricing. Journal of Business, 29, 172-

184.

27

Johnson, N.B. (2006). Divisional performance measurement and transfer pricing for intan-

gible assets. Review of Accounting Studies, 11, 339-365.

Kaplan, R., and Atkinson, A.A. (1998). Advanced management accounting (3rd ed.).

Englewood Cliffs: Prentice-Hall.

Schmalenbach, E. (1908/1909). Über Verrechnungspreise. Zeitschrift für handelswirtschaftliche

Forschung, 3, 165—185.

Wagenhofer, A. (1994). Transfer pricing under asymmetric information —An evaluation of

alternative methods. European Accounting Review, 1, 71-104.

28

29

30

31

32

33

34