tata motors

TRANSCRIPT

LeadingThe

Future

Sep. - Oct., 2003

1

Statements in this presentation describing the Company’s objectives, projections, estimates, expectations may be “forward looking statements” within the meaning of applicable securities laws and regulations. Actual results could differ materially from those expressed or implied. Important factors that could make a difference to the Company’s operations include, among others, economic conditions affecting demand / supply and price conditions in the domestic and overseas markets in which the Company operates, changes in Government regulations, tax laws and other statutes and incidental factors

2

Presentation Outline

x Introduction to Tata Group & Tata Motors

x Growth Strategy

x De-risking The Business

x The Way Forward

3

Tata Group – Leading Business Group in India

x Among the prominent industrial houses of India, with a pioneering track record of more than 125 years

x Over 80 companies with dominant presence in a wide range of businesses such as Materials, Chemicals, Energy, Engineering, Communications & Information Systems, Services and Consumer Goods

x Turnover : Rs 542 bn (US$ 11.2 bn) in FY03 (equivalent to 2.4% of India’s GDP at current prices)

x Net Profit : Rs 39 bn (US$ 805 mn) in FY03

x Strong Brand Equity

x Good Business Ethics

4

Tata Motors – India’s Largest Automotive Companyx India’s first and only fully integrated Automobile manufacturer, with a

significant presence in Commercial and Passenger vehicle markets

x Commenced operations in 1945

x Indigenous technology development for all its products

x FY03 Financial Overview

- Highest ever Net Revenues (unconsolidated) of Rs 91 bn (US$ 1.9 bn)

- PAT (unconsolidated) of Rs 3 bn (US$ 63 mn)

- Operating EVA positive - Operating ROIC of 13.6%

- Dividend of 40%

- Asset base of Rs 41.6 bn (US$ 877 mn)

5

Milestones

1954

19861990

19911994

1945Incorporated as a Public Ltd. Company with a factory at

Jamshedpur for manufacturing locomotives

Daimler-Benz collaboration for CVs

Produced one millionth vehicle

Entered the Car market with Sierra & Estate

Tata Sumo (UV) launched

1997100,000th Sumo rolled out

1998Two millionth vehicle rolled out.

Indica launched

2002100,000th Indica rolled out

Indica V2 launched

1967 Engineering Research Centre set up at Pune

2003

200,000th Indica sold, 500,000th PV rolled outIndica platform achieves break-even

Indigo launchedAgreement with MG Rover for Indica exports

Produced first in-house LCV Tata 407

1969Technical agreement with Benz expired

2001

Three millionth vehicle rolled out

6

Wide Product RangeTrucks (2MT– 40 MT GVW) Buses (12 -60 seater) Passenger Vehicles

7

Maintaining Leadership In Domestic Market

82,564

107,438

88,865104,414

0

20,000

40,000

60,000

80,000

100,000

120,000

CVs PVs

FY02 FY03

+30% +17%Growth

Market share in FY03

x CVs: 56%

x PVs: 15%

April-August, 2003

CVs: Volumes +39% Market share: 58% (+410 bps) PVs: Volumes +45% Market share: 16% (+220 bps)

8

Financial Snapshot

Last 2 yearsRevenue CAGR of 16% & PBT swing of Rs 10 bn

Net Revenue and EBITDA MarginRs bn

6875

91

6.1%

9.9%

12.5%

0

20

40

60

80

100

FY01 FY02 FY030

5

10

15

Net Revenue EBITDA Margin

%PBT and PAT

Rs bn

(5.0)

(1.1)

5.1

(5.0)

(0.5)

3.0

(8)

(4)

0

4

8

FY01 FY02 FY03

PBT PAT

9

Financial Performance – 1Q FY04

x Net Revenues of Rs 25 bn (up 43% YoY)

x EBITDA margin of 13.3% - highest in last 21 quarters

x Pre-tax Cash Profit of Rs 2.9 bn (up 125% YoY)

x PBT of Rs 1.6 bn against Rs 0.4 bn in 1Q FY03

x PAT of Rs 1 bn - highest since April 1998

10

5042

52 50

63

40

88

148

218

120

0

50

100

150

200

250

Apr-02 Jul-02 Oct-02 Jan-03 Apr-03 Jul-030

20

40

60

80

100

Tata Motors Mcap (RHS) Total Auto Index Tata Motors BSE Sensex

Rs bnIndex

Stock Price Performance

+118%8840Tata Motors Market Cap (Rs bn)

+118%275126Tata Motors Stock Price (Rs)

+48%148100Auto Index (April 1, 2002=100)

+20%4,2173,500BSE Sensex

% changeSep 19, 2003Apr 1, 2002

11

Presentation Outline

x Introduction to Tata Group & Tata Motors

x Growth Strategy

x De-risking The Business

x The Way Forward

12

Strategy Ladder - Turnaround

Further BE point reduction

Platform strategy

Customer-centric activities

Positive PBT in Car Project

Aggressive Cost reduction Re-engineered processesMarket share gainsOrganisational

transformation

Turnaround (FY01-03)Improving Internal Efficiencies

13

Strategy Ladder – Growth Phase

Profitable Growth (FY04-06)Leveraging Strengths

Revenue growth through

- Consolidation in domestic market

- Significant presence in international markets

New business activities

ROIC improvement

New Generation Products

Capitalise on prod. dev. skills and costs globally

Turnaround (FY01-03)Improving Internal Efficiencies

Further BE point reduction

Platform strategy

Customer-centric activities

Positive PBT in Car Project

Aggressive Cost reduction Re-engineered processesMarket share gainsOrganisational

transformation

14

Economic Recovery

Auto sector to benefit from increased Industrial and Consumer demand

Indian Economy

Economic Growthx Industrial recovery x Improvements in Capital

Equipment industryxNormal monsoon

InfrastructurexStrong construction activityxRoad Projects

Fiscal InitiativesxBenign interest ratesxRationalisation of Excise duties

15

India Commercial Vehicle Market

FY03 Market size : 192,000 units

Tata Motors’ Market share: 56%

LCV Bus10%

HCV trucks20%

MCV trucks24%

LCV Truck18%

MHCV Bus10%

Pickups12%

ICV trucks6%

(80%)

(65%)

(28%)(63%)

(37%)(17%)

(51%)

Tata Motors – Leading the CV market

No. of foreign players: 2

Market share: 0.3%

16

Source: NHAI

Road Development Programme

Year-wise completion schedule of NHDP

Planned length – 14,000 km

Between 1997 - 2002, Highway length in China increased by around 15,000 km and

CV volumes nearly doubled from 1.2 mn to 2.1mn …

….. Indicative of likely future directions in Indian market

2005-0752%

200312%

200421%

Completed15% 0

100

200

300

400

500

600

700

800

900

1000

0 0.5 1 1.5 2

Tru

ck p

enet

rati

on

MH

CV

/ m

pop

ulat

ion

Germany

FranceUK

Spain

Portugal

Turkey

Australia

IndiaIndonesia

South AfricaChina

BrazilArgentina

Russia

12

3

4

Stage

Road DensityPaved Highway (km) / Area (km2)

Dramatic impact on volumes in initial

stage of road development

0

100

200

300

400

500

600

700

800

900

1000

0 0.5 1 1.5 2

Tru

ck p

enet

rati

on

MH

CV

/ m

pop

ulat

ion

Germany

FranceUK

Spain

Portugal

Turkey

Australia

IndiaIndonesia

South AfricaChina

BrazilArgentina

Russia

12

3

4

Stage

Road DensityPaved Highway (km) / Area (km2)

Dramatic impact on volumes in initial

stage of road development

17

Emerging Trends In CV Demand

MHCVs

LCVs

HCVs gaining strength due to lower cost of operationGrowth in Pickups indicating desegregation of load at the lower end

0

40000

80000

120000

160000

FY97 FY98 FY99 FY00 FY01 FY02 FY03

HCV trucks MCV trucks MHCV Buses

020000400006000080000

100000

FY97 FY98 FY99 FY00 FY01 FY02 FY03

Pickups LCV Trucks Buses

18

Tonnage Addition – More Than A Cyclical Recovery

Factors behind the recoveryEconomic Recovery Lower Interest rates Market Share gains from Railways Replacement & Upgradation of VehiclesInfrastructure Projects

Despite lower GDP growth, the tonnage addition in FY03 nearly equalled

the addition in last peak (FY97)

0.7

0.50.6

0.8

1.4

0.70.8

1.0

1.3

0.7

1.2

1.0

1.3%

5.1%

7.8%

4.8%

6.5%

4.3%5.6%

4.0%

-

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

FY92 FY93 FY94 FY95 FY96 FY97 FY98 FY99 FY00 FY01 FY02 FY030%

3%

6%

9%

Tonnage Addition (mn MT) GDP Growth

Transporters’ ROE continues to be healthy

19

Upside Potential In Bus Demand

China Bus market India Bus market

(‘000)

410 488631

247276

344

71

5844

0

200

400

600

800

1000

1200

2000 2001 2002

Mini Light Medium/Large

701,000Total 822,000 1,046,000(‘000)

12 1418

20

1725

0

10

20

30

40

FY01 FY02 FY03

Light Medium

37,000Total 31,000 38,000

With a geographic & population profile similar to China, India bus market is under-penetrated

20

Tata Motors – Initiatives & Achievements

x MHCV & LCV segment– Superior range of EX series of

M&HCVs and 709LPT launched

x Pick-up Segment – 207DI pickup launched in Aug’02– Gained market share in high

growth segmentx Fully Built Vehicles

– Increased thrust on fully built vehicles & solutions– Wide range of buses, tippers & other applications– FBV volumes doubled

21

Tata Motors – Capturing The Upswing

x Focus on hi-performance Total CV solutions

– Truck of the Future to match global standards

– Higher GVW, power to weight ratio

x Range of Fully Built Buses– Contract manufacturing route

for body building

x Non-vehicular business– Customer Financing– Spares, Recon, AMC

22

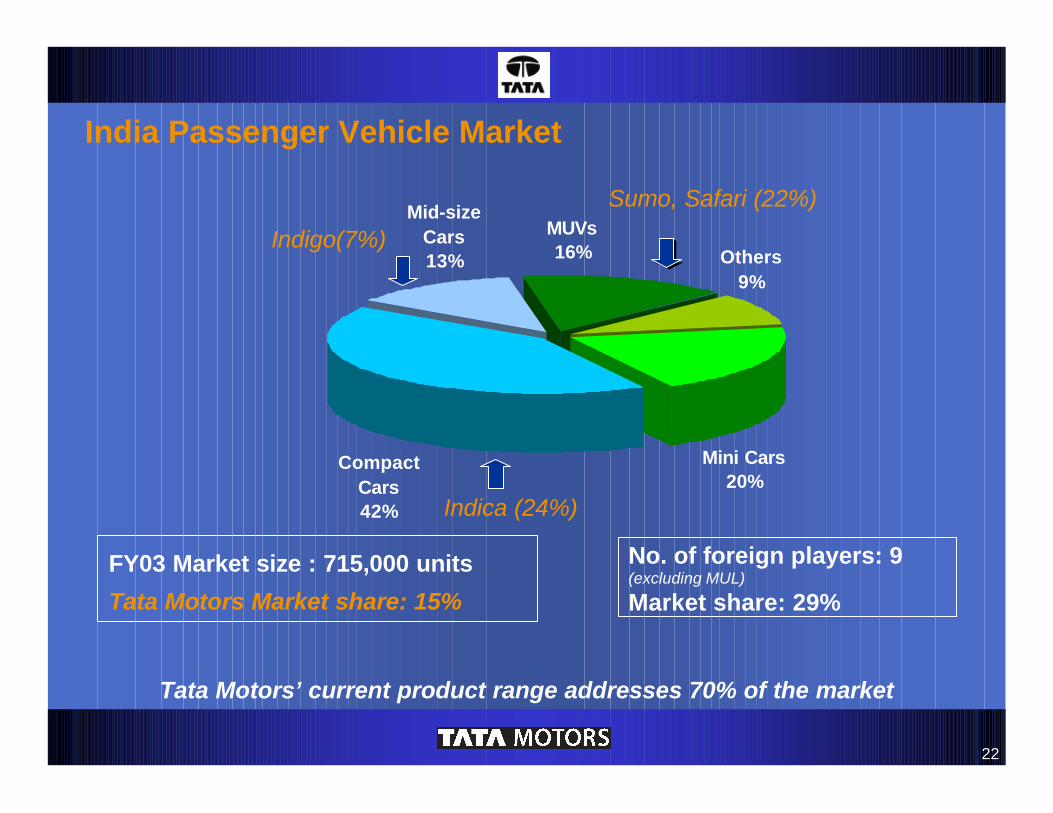

Mini Cars20%

Compact Cars42%

MUVs16% Others

9%

Mid-size Cars13%

Indica (24%)

Indigo(7%)

Sumo, Safari (22%)

Tata Motors’ current product range addresses 70% of the market

India Passenger Vehicle Market

No. of foreign players: 9(excluding MUL)

Market share: 29%

FY03 Market size : 715,000 units

Tata Motors Market share: 15%

23

x Demographics

x Infrastructure

x Economic Factors

x Competitive Intensity

x Technology

x Regulations

Growth Drivers

India Passenger Vehicle Market Potential

PV Market potential

647

1,187

2002 2008E

CAGR 11%

‘000 units

24

Growth Drivers

China PV market

612717

1,121

0

200

400

600

800

1000

1200

1400

2000 2001 2002

‘000 units

x Release of pent-up demand in 2002– Price cuts by OEMs– Easing of Regulations– Low cost finance– Finance availability

+56%

India PV market

?

x Similar conditions in India– Excise duty reduction– Low cost finance– Finance availability– New product launches

‘000 units

624 606647

0

200

400

600

800

1000

2000 2001 2002 2003E

FY04 YTD growth 25%

25

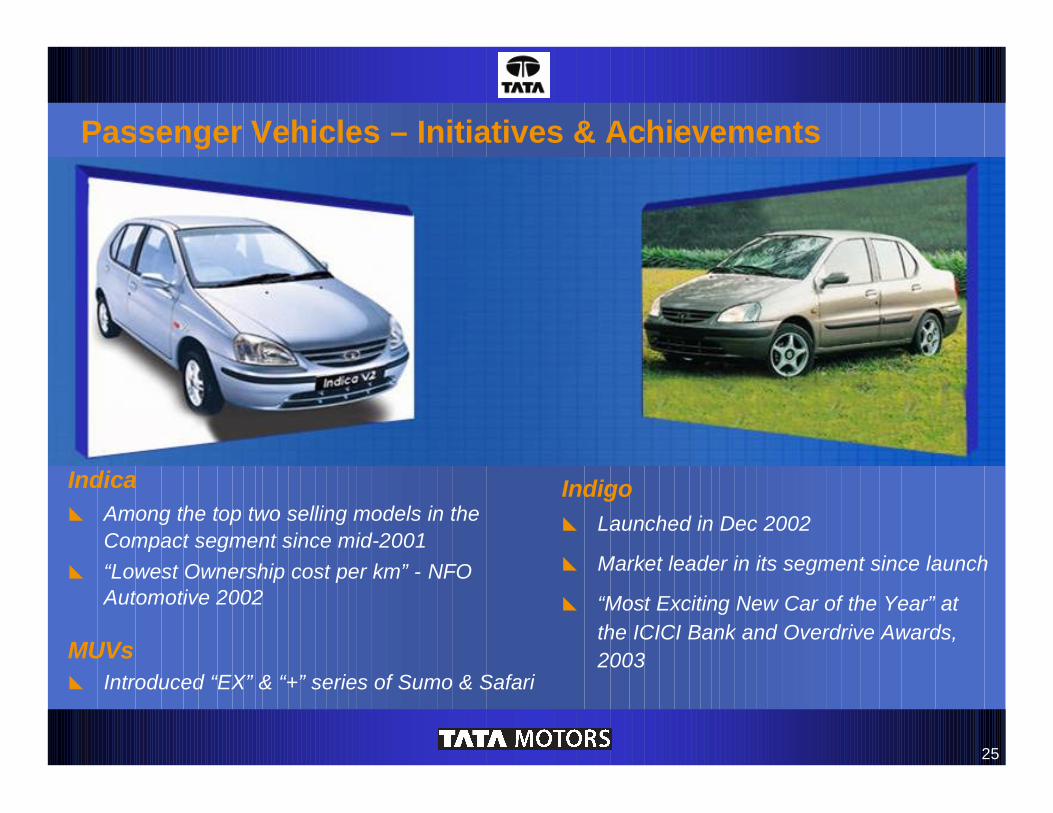

Indicax Among the top two selling models in the

Compact segment since mid-2001x “Lowest Ownership cost per km” - NFO

Automotive 2002

Indigox Launched in Dec 2002

x Market leader in its segment since launch

x “Most Exciting New Car of the Year” at the ICICI Bank and Overdrive Awards, 2003MUVs

x Introduced “EX” & “+” series of Sumo & Safari

Passenger Vehicles – Initiatives & Achievements

26

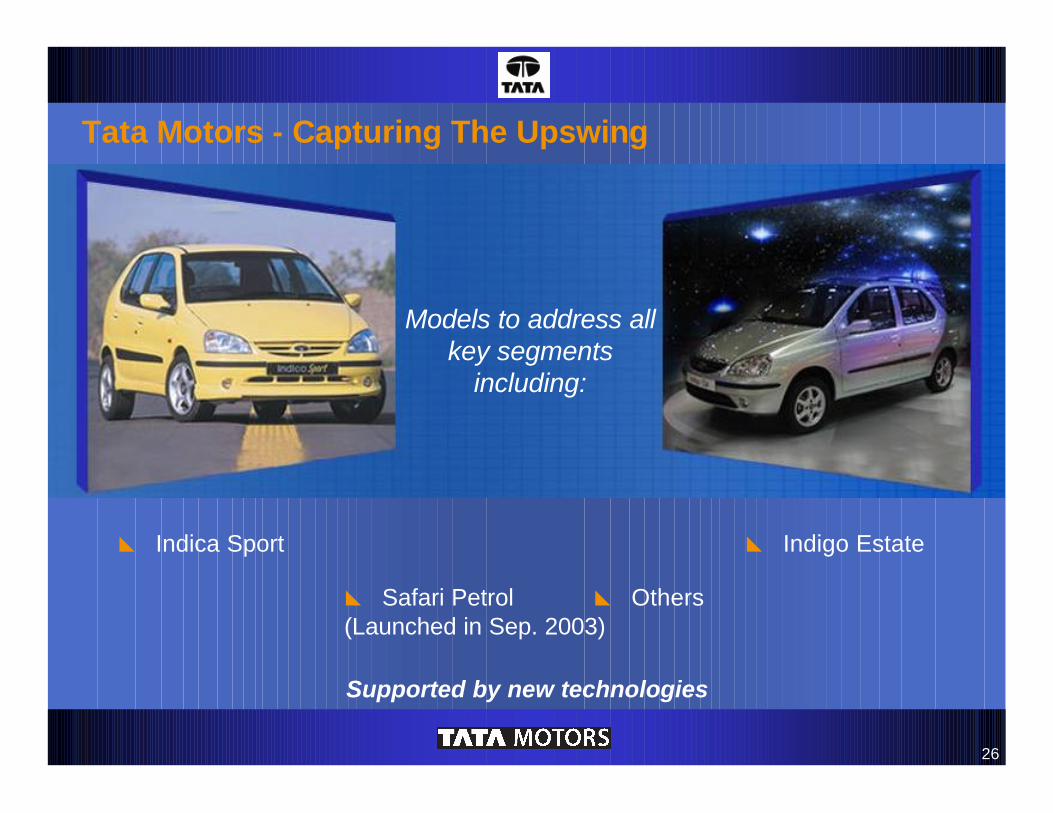

Models to address all key segments

including:

x Indica Sport x Indigo Estate

x Safari Petrol (Launched in Sep. 2003)

x Others

Supported by new technologies

Tata Motors - Capturing The Upswing

27

Presentation Outline

x Introduction To Tata Group & Tata Motors

x Growth Strategy

x De-risking The Business

x The Way Forward

28

Going Globalx Near term strategy

– Strengthen presence in traditional and niche markets• Exports volumes up 71% in first five months of FY04

– Establish regional alliances for marketing

Focussed markets identified for growth

– Re-launched CVs in Colombo and 5 other cities in Sri Lanka

Reflected in the agreement with MG Rover Group – Intend to export 100,000+ Indica to EU over 5 years

• Shipments to begin in 3Q FY04

– Distribution of Safari & Pick-ups in EU

x Long term strategy– Develop ”Truck of the future”– Leverage technical capabilities for product development

Significantly expand presence in the global market

29

Non-Cyclical Revenue Stream

x Exports

x Spares

x Vehicle Financing

x Reconditioned Vehicles / Aggregates

x Marine & Industrial Engines

Plan to increase it to around 20% of Net Revenue in next 2-3 years

13% of Net Revenue

Revenue from Non-cyclical Business in FY03

30

Rs bn

Cost Reduction

Cost Reduction ElementsFY01 – FY03

Total Cost Reduction

Var. Conv. 10%

Raw Mat.65%

Interest25%

Total Cost reduction of Rs 9.5 bn in last three years

3.3

2.8

9.53.3

0

1

2

3

4

5

6

7

8

9

10

FY01 FY02 FY03 Total

31

36%31%

45%

45%43%

54%

0

10

20

30

40

50

60

FY01 FY02 FY03

BEP as % of capacityCapacity utilisation

CVs

62%

48%

95%

29% 44%

54%

0

20

40

60

80

100

FY01 FY02 FY03

BEP as % of capacityCapacity utilisation

Cars% %

Lower Break-even Points

32

Reduction In Balance Sheet Size72 68 63 48

ROCE (pre-tax) 3.7% 2.7% -1.1% 5.4% 17.4%

42Rs bn

40 40 38 35 33

12 12

78

9

141210

14 8 2

0

(4)

11

-10

0

10

20

30

40

50

60

70

FY99 FY00 FY01 FY02 FY03

Net Fixed Assets Investments Net Working Capital

Deferred Revenue Expenses Deferred Tax Assets (Net)

Avg. Asset Turnover 0.8 1.0 1.0 1.4 2.0

33

Tighter Fiscal Discipline

Days of sale

Inventory

Receivables (non-HP)

Days of sale

Net Working Capital

Negative Working Capitalfor the first time in the Company’s history

112

77

33

7

0(15)

-20

0

20

40

60

80

100

120

FY98 FY99 FY00 FY01 FY02 FY03

74

57

29 28 2518

0

20

40

60

80

100

FY98 FY99 FY00 FY01 FY02 FY03

48 4741

5041

39

0

20

40

60

FY98 FY99 FY00 FY01 FY02 FY03

34

Stronger Cash Flows & Debt Reduction

67

11

0

2

4

6

8

10

12

FY01 FY02 FY03

1523

30

0.56

0.94

1.27

0

5

10

15

20

25

30

35

FY01 FY02 FY030

0.2

0.4

0.6

0.8

1

1.2

1.4

Debt D/E (adj.) - RHS

Rs bn

Free Cash Flow Debt & D/E

Rs bn

35

Presentation Outline

x Introduction to Tata Group & Tata Motors

x Growth Strategy

x De-risking the business

x The Way Forward

36

Leveraging Our Strengths

Backed by TATA Brand

Global scales in CVs

Advantage Tata Motors

Distribution network & service reach

Integrated & cost competitive mfg.

facilities

Partnerships for components/ aggregates

Excellent R&D capabilities

Low cost product development

capability

37

The Way Forward

x Domestic demand drivers in place – Capture advantage of CV uptrend and growth in PVs

x Expand presence in global markets

x Reduce interest cost

x Explore further opportunities for cost reduction

x Disciplined capex programme

x Better working capital management

38

Tata MotorsCombining capabilities and cost advantage to emerge as a

world class automotive company

Leading the future ……Leading the future ……

39

Thank YouThank You

Visit us at www.tatamotors.com