tata jlr aquisition

TRANSCRIPT

TATA-JLR Acquisition:

Agenda

1 •Why Ford was selling JLR?•Why TATA Motors (TaMo) was interested in purchasing JLR?

2 •The deal and its financing.•Challenges that it faced.

3 •Post Merger scenario.•Cost of capital.

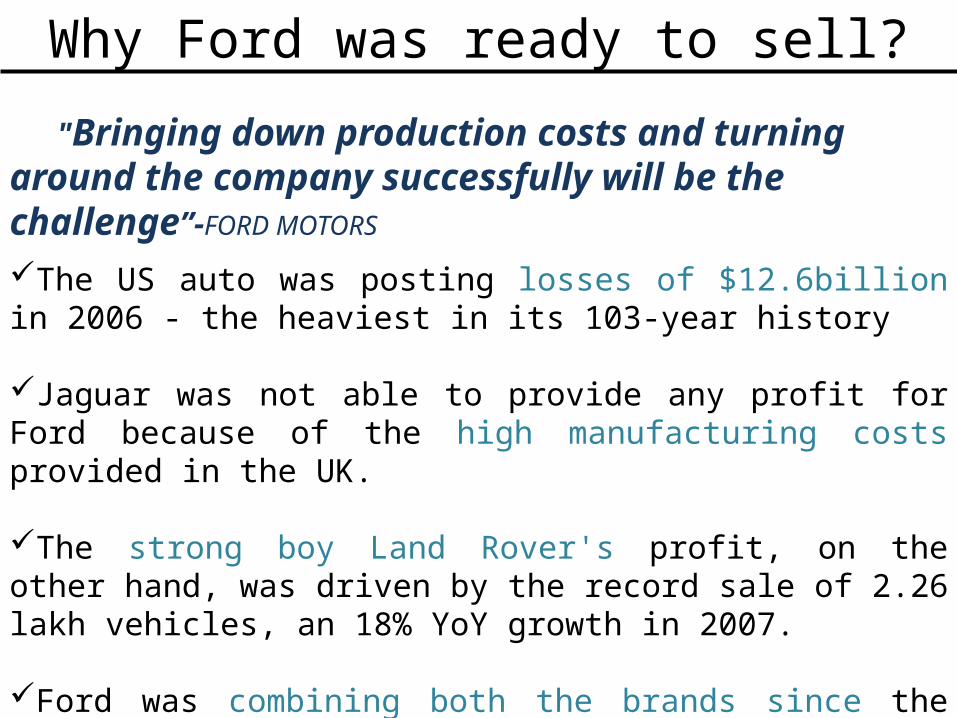

Why Ford was ready to sell?

The US auto was posting losses of $12.6billion in 2006 - the heaviest in its 103-year history

Jaguar was not able to provide any profit for Ford because of the high manufacturing costs provided in the UK.

The strong boy Land Rover's profit, on the other hand, was driven by the record sale of 2.26 lakh vehicles, an 18% YoY growth in 2007.

Ford was combining both the brands since the products and manufacturing of vehicles for Land Rover and Jaguar was so intertwined.

"Bringing down production costs and turning around the company successfully will be the challenge”-FORD MOTORS

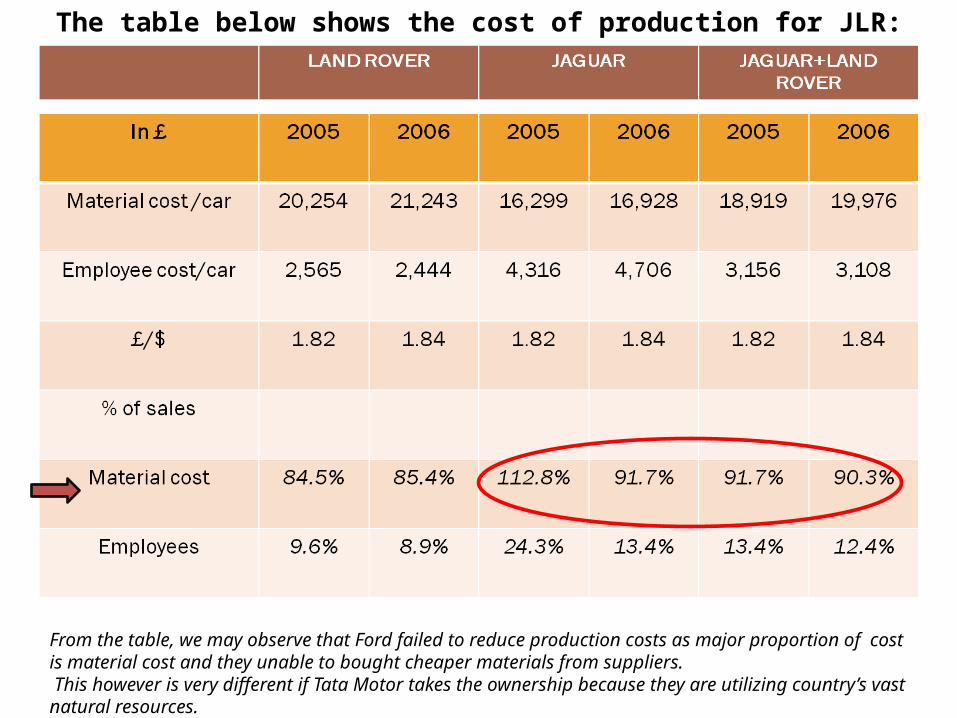

The table below shows the cost of production for JLR:

From the table, we may observe that Ford failed to reduce production costs as major proportion of cost is material cost and they unable to bought cheaper materials from suppliers. This however is very different if Tata Motor takes the ownership because they are utilizing country’s vast natural resources.

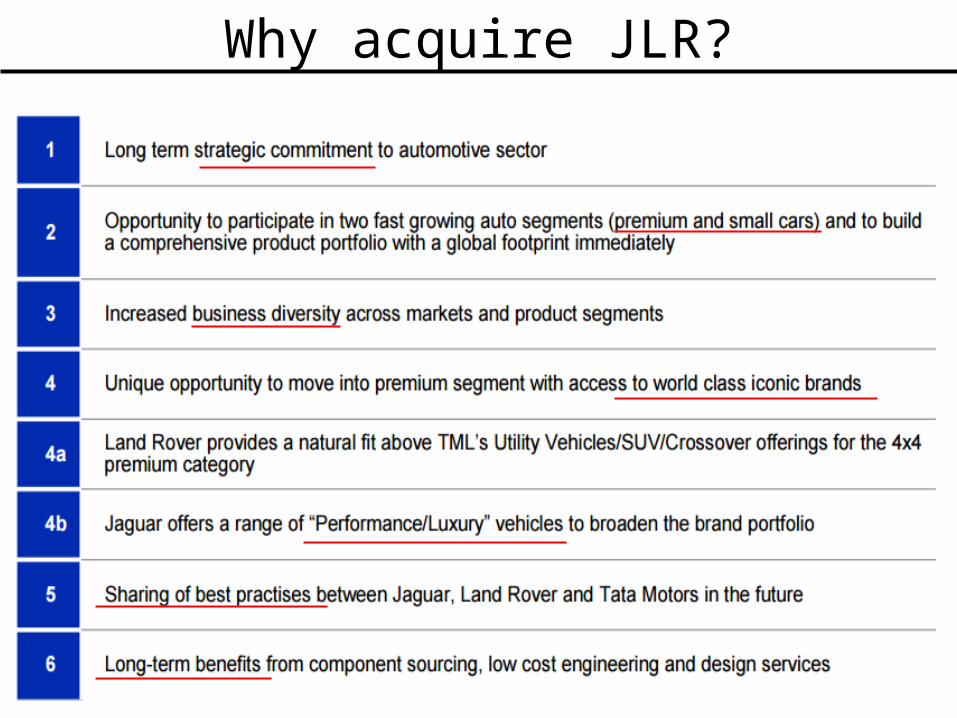

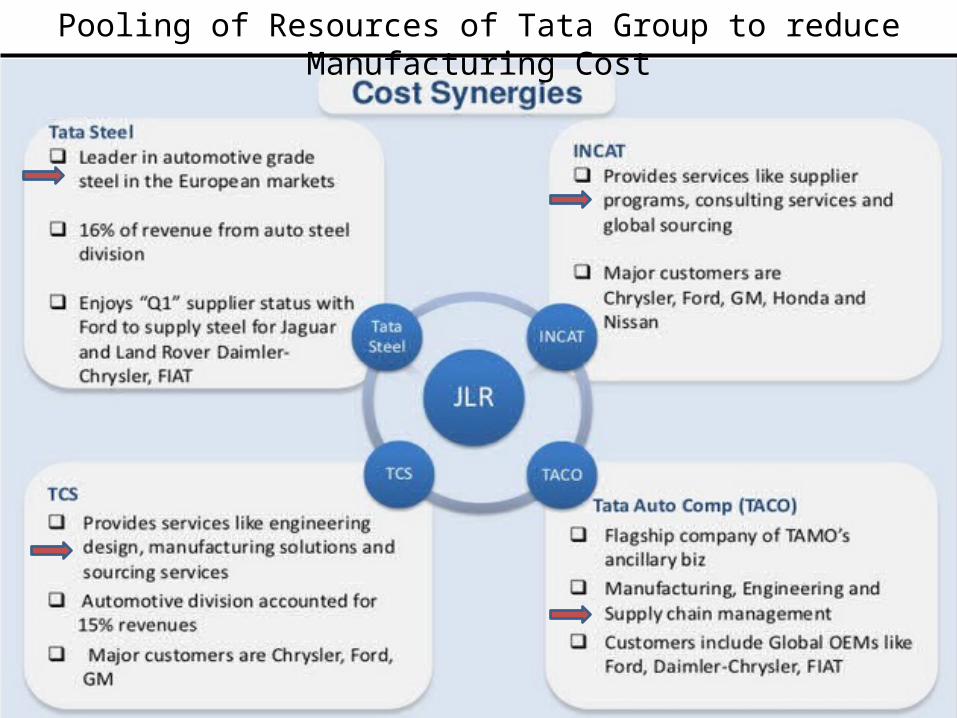

Why acquire JLR?

Pooling of Resources of Tata Group to reduce Manufacturing Cost

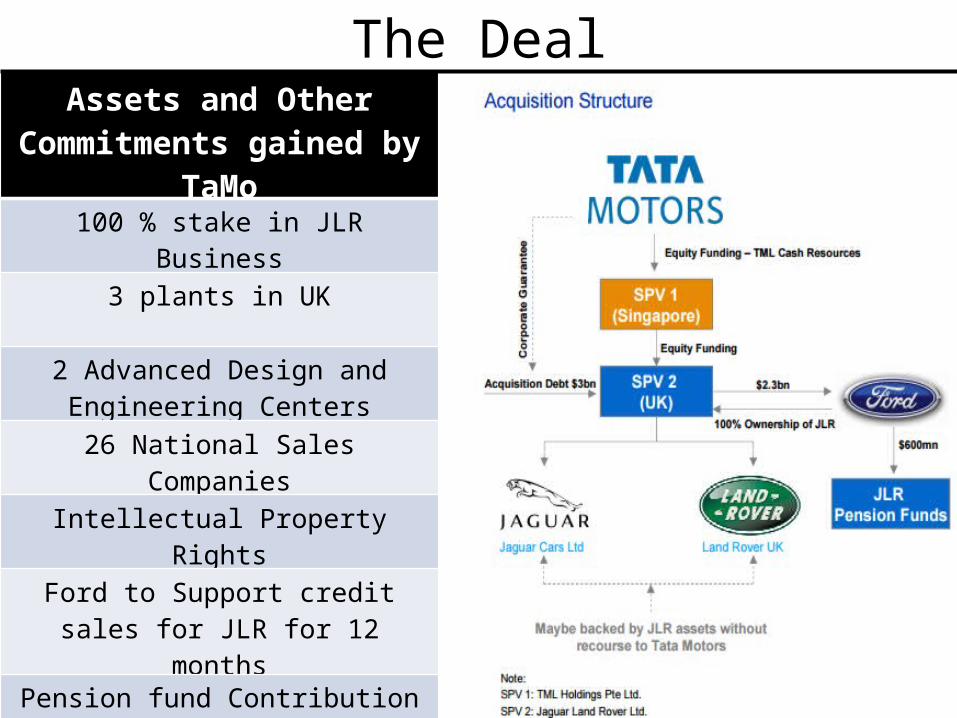

The DealAssets and Other

Commitments gained by TaMo

100 % stake in JLR Business

3 plants in UK

2 Advanced Design and Engineering Centers

26 National Sales Companies

Intellectual Property Rights

Ford to Support credit sales for JLR for 12 months

Pension fund Contribution $600 mn by Ford.

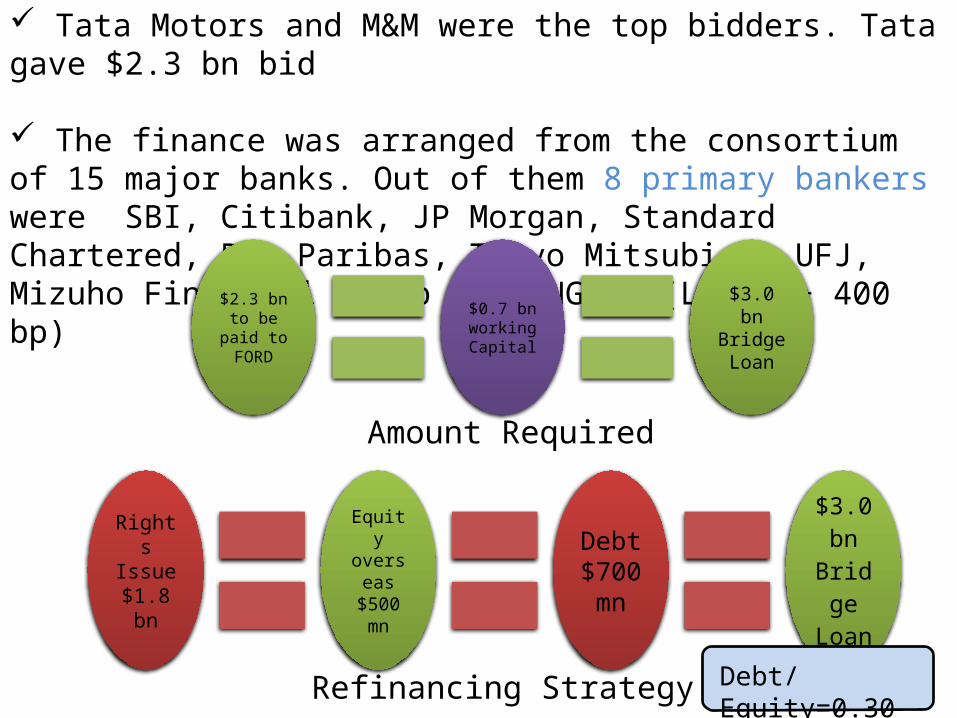

Tata Motors and M&M were the top bidders. Tata gave $2.3 bn bid

The finance was arranged from the consortium of 15 major banks. Out of them 8 primary bankers were SBI, Citibank, JP Morgan, Standard Chartered, BNP Paribas, Tokyo Mitsubishi UFJ, Mizuho Financial Group and ING. @ (LIBOR + 400 bp)

$2.3 bn to be

paid to FORD

$0.7 bn workin

g Capital

$3.0 bn

Bridge Loan

Rights Issue $1.8 bn

Equity overse

as $500 mn

Debt $700 mn

$3.0 bn

Bridge Loan

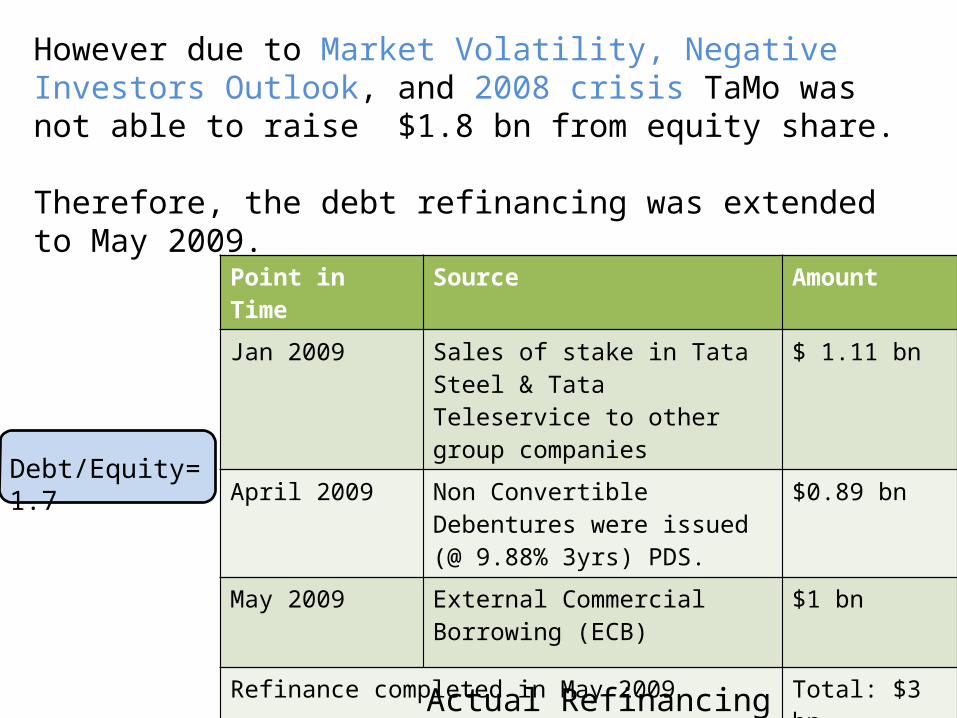

Refinancing Strategy

Amount Required

Debt/Equity=0.30

Point in Time Source Amount

Jan 2009 Sales of stake in Tata Steel & Tata Teleservice to other group companies

$ 1.11 bn

April 2009 Non Convertible Debentures were issued (@ 9.88% 3yrs) PDS.

$0.89 bn

May 2009 External Commercial Borrowing (ECB)

$1 bn

Refinance completed in May 2009 Total: $3 bn

Actual Refinancing

However due to Market Volatility, Negative Investors Outlook, and 2008 crisis TaMo was not able to raise $1.8 bn from equity share.

Therefore, the debt refinancing was extended to May 2009.

Debt/Equity= 1.7

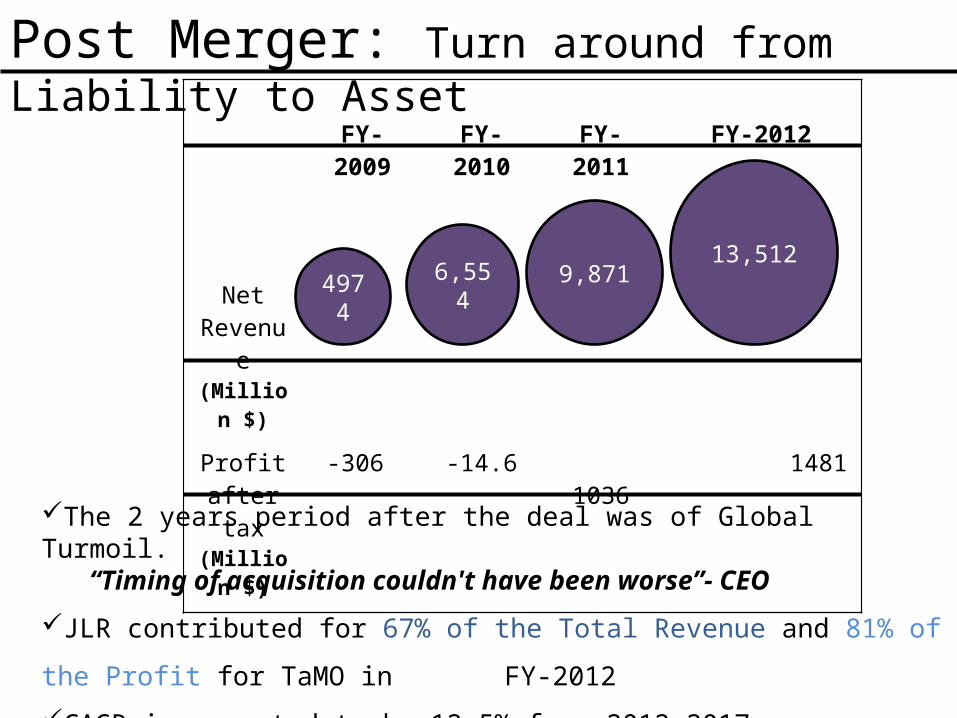

Post Merger: Turn around from Liability to Asset

FY-2009 FY-2010 FY-2011 FY-2012

Net Revenue(Million $)

Profit after tax

(Million $)

-306 -14.6 1036 1481

4974 6,554 9,87113,512

The 2 years period after the deal was of Global Turmoil.“Timing of acquisition couldn't have been worse”- CEO

JLR contributed for 67% of the Total Revenue and 81% of the Profit for TaMO in

FY-2012

CAGR is expected to be 12.5% from 2012-2017.

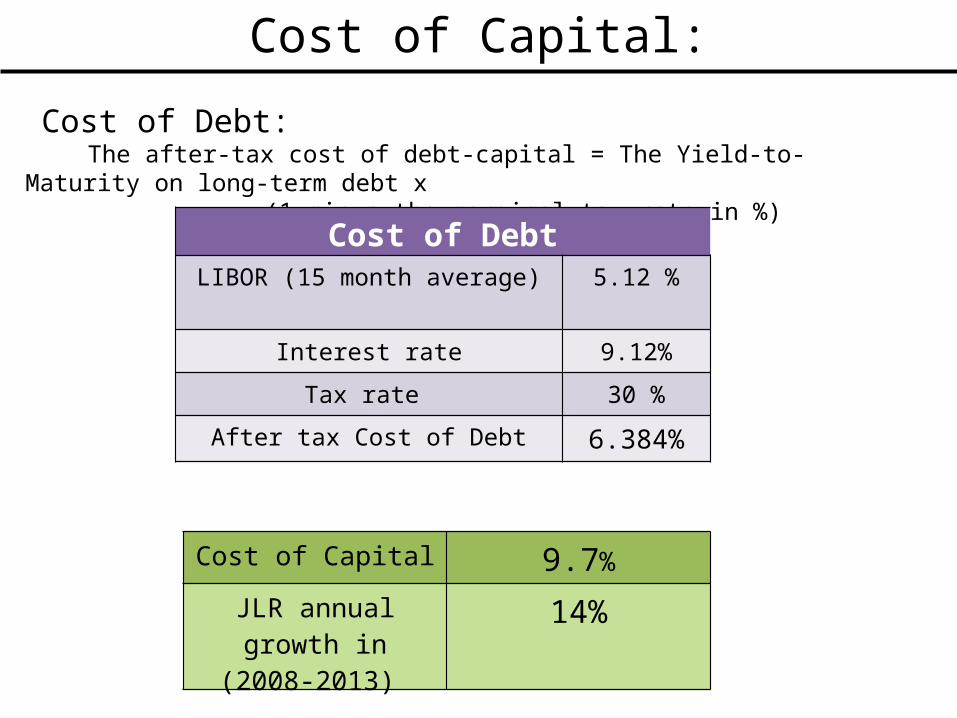

Cost of Capital:

Cost of Debt: The after-tax cost of debt-capital = The Yield-to-Maturity on long-term debt x

(1 minus the marginal tax rate in %)

Cost of DebtLIBOR (15 month average) 5.12 %

Interest rate 9.12%

Tax rate 30 %

After tax Cost of Debt 6.384%

Cost of Capital 9.7%

JLR annual growth in (2008-2013)

14%