tanf regulation: fiscal provisions u funding options u moe requirements u financial principles u...

TRANSCRIPT

TANF Regulation: Fiscal Provisions Funding Options MOE Requirements Financial Principles Definition of Expenditure Admin Costs Penalties / Annual Report Use of Funds Expenditure Report

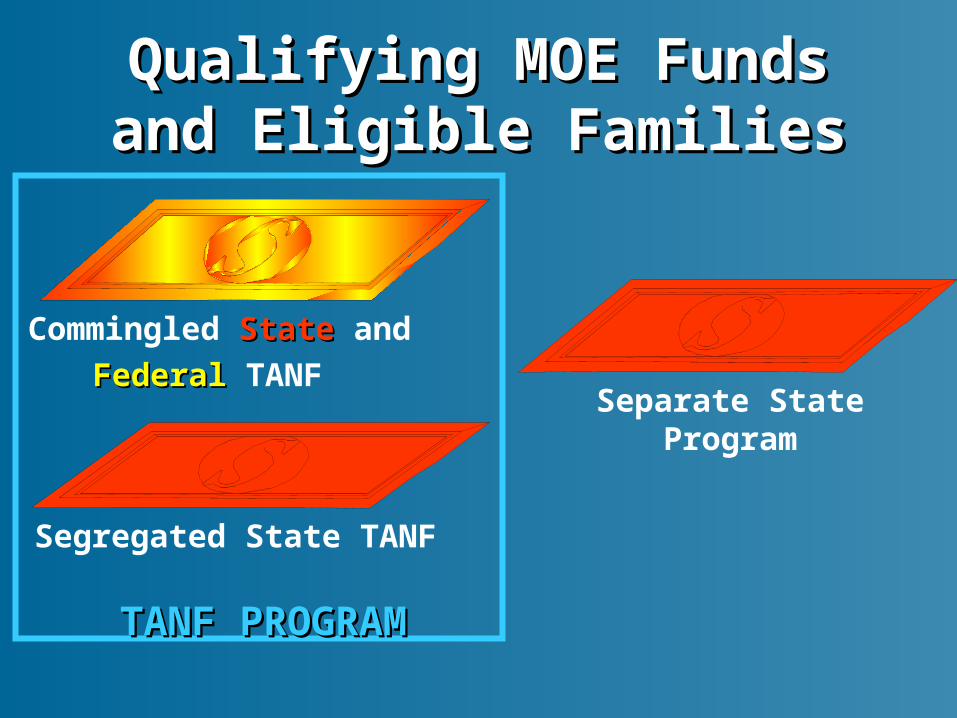

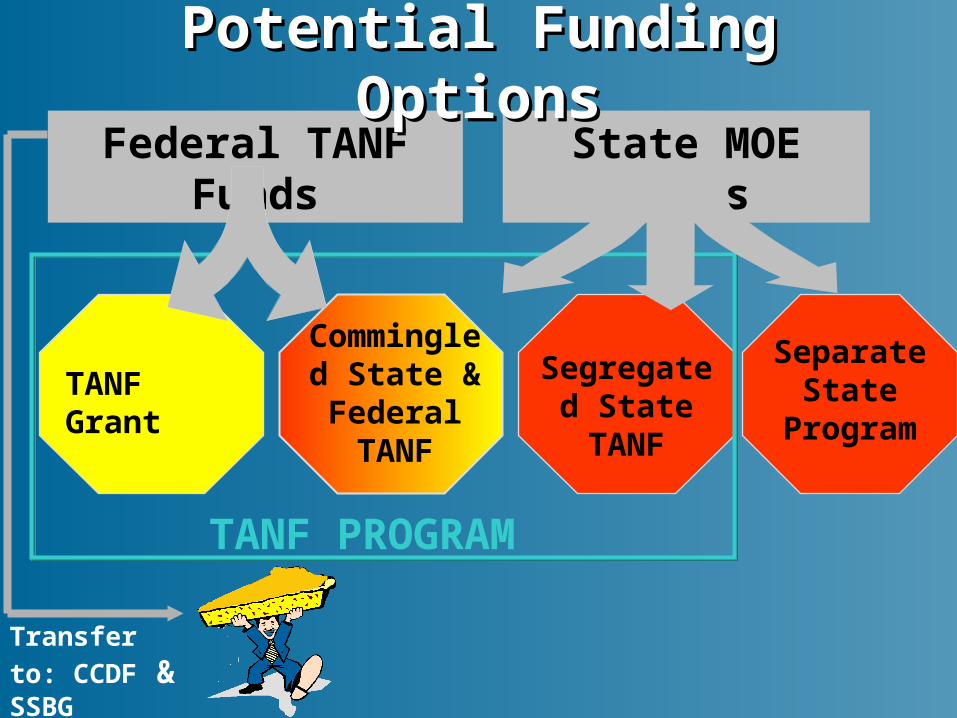

Federal TANF Funds State MOE Funds

TANF Grant

Commingled State & Federal TANF

Segregated State TANF

Separate State

Program

TANF PROGRAM

Potential Funding OptionsPotential Funding Options

Transfer to:

CCDF & SSBG

Each FY a State participates in TANF

80% of what spent in FY 1994, or 75% if meet work participation rates

If Tribe (or consortium) is awarded TFAG, then MOE amount is reduced by same percentage as the reduction in the State’s SFAG

Basic MOE RequirementsBasic MOE Requirements

TANF PROGRAMTANF PROGRAM

Commingled StateState and FederalFederal TANF

Segregated State TANF

Separate State Program

Qualifying MOE Funds and Qualifying MOE Funds and Eligible FamiliesEligible Families

MOE Funds Must Be Spent on MOE Funds Must Be Spent on Eligible FamiliesEligible Families

Families must meet:

1) Family composition requirement– child 1/w parent or other adult relative, or

– pregnant woman

2) Financial eligibility criteria established by State

– per appropriate income and resources (when applicable) standards

– contained in TANF plan

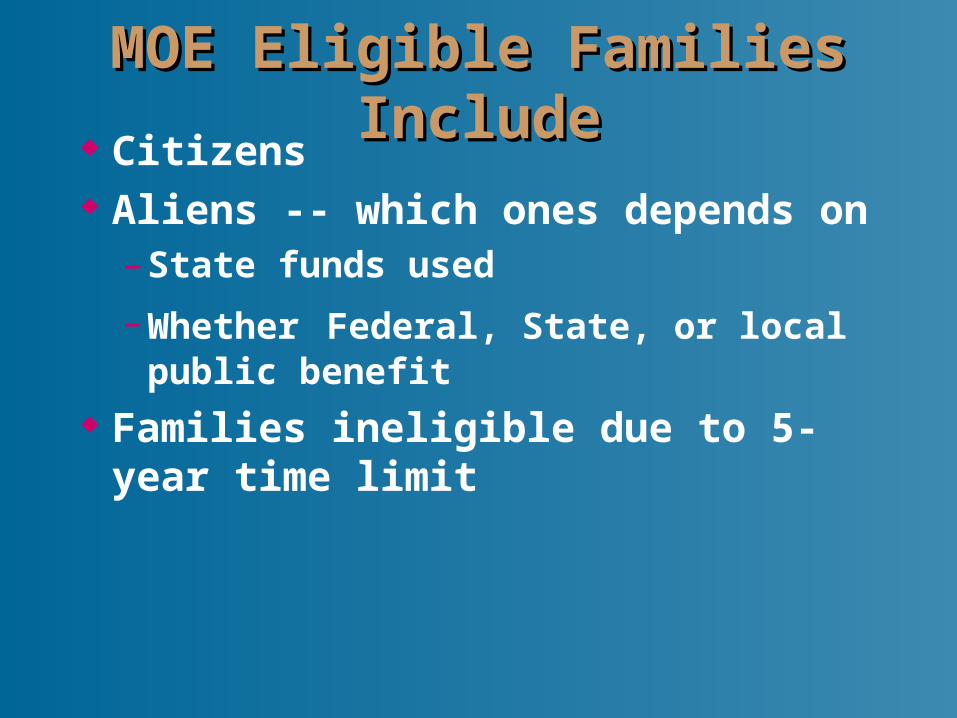

MOE Eligible Families IncludeMOE Eligible Families Include Citizens Aliens -- which ones depends on

– State funds used

– Whether Federal, State, or local public benefit

Families ineligible due to 5-year time limit

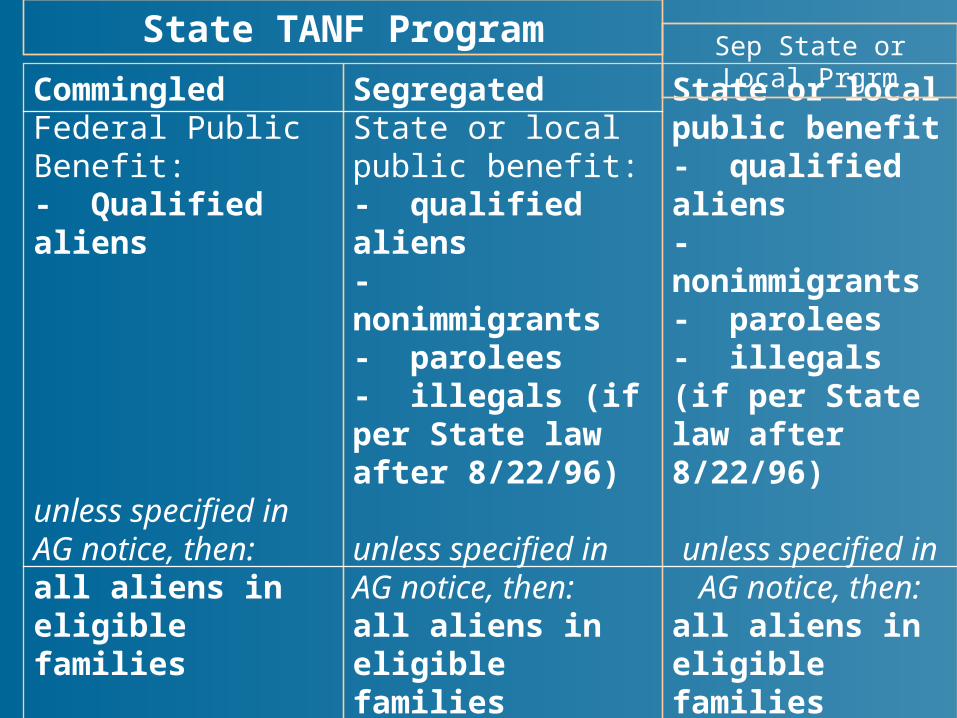

CommingledFederal Public Benefit:- Qualified aliens

unless specified in AG notice, then:all aliens in eligible families

SegregatedState or local public benefit:- qualified aliens- nonimmigrants - parolees- illegals (if per State law after 8/22/96)

unless specified in AG notice, then:all aliens in eligible familiesNon State or local public benefit:- all aliens

State or local public benefit- qualified aliens- nonimmigrants- parolees- illegals (if per State law after 8/22/96)

unless specified in AG notice,

then:all aliens in eligible familiesNon State or local public benefit:- all aliens

State TANF Program Sep State or Local Prgrm

Funds Must Be Used in Ways Funds Must Be Used in Ways That “Qualify”That “Qualify”

Cash Assistance– Including any part of State’s share of child

support collection sent to the family & disregarded

Child care assistance

Under all programs: TANF (commingled, segregated) & separate

Educational activities if

– Provided to increase self-sufficiency, job training, & work; and

– The service is not available to other residents without cost and without regard to their income (e.g., generally excludes public education)

Funds Must Be Used in Ways Funds Must Be Used in Ways That “Qualify” (cont.)That “Qualify” (cont.)

Any other benefits or services that are reasonably calculated to accomplish a purpose of the TANF program

Benefits/services that exclusively fall under 404(a)(2) do not qualify

Funds Must Be Used in Ways Funds Must Be Used in Ways That “Qualify” (cont.)That “Qualify” (cont.)

Administrative costs in connection with the above activities

– Up to 15% of countable expenditures

– Except costs for information technology & computerization for tracking and monitoring

Funds Must Be Used in Ways Funds Must Be Used in Ways That “Qualify” (cont.)That “Qualify” (cont.)

TANF Regulation: Fiscal Provisions Funding Options MOE Requirements Financial Principles Definition of Expenditure Admin Costs Penalties / Annual Report Use of Funds Expenditure Report

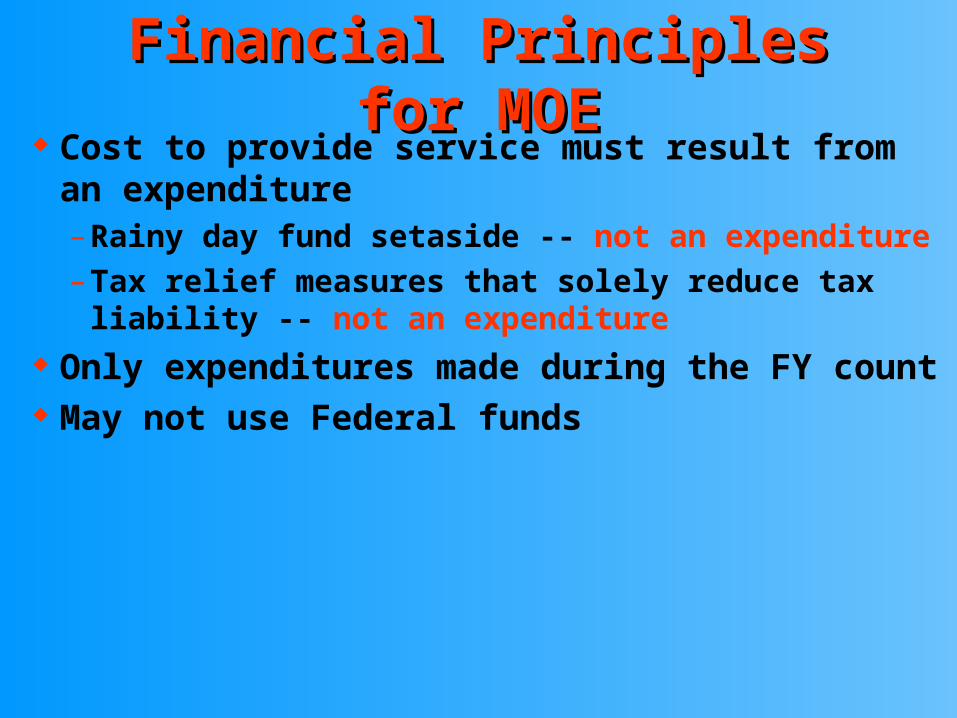

Financial Principles for MOEFinancial Principles for MOE Cost to provide service must result from an

expenditure– Rainy day fund setaside -- not an expenditure– Tax relief measures that solely reduce tax liability --

not an expenditure Only expenditures made during the FY count May not use Federal funds

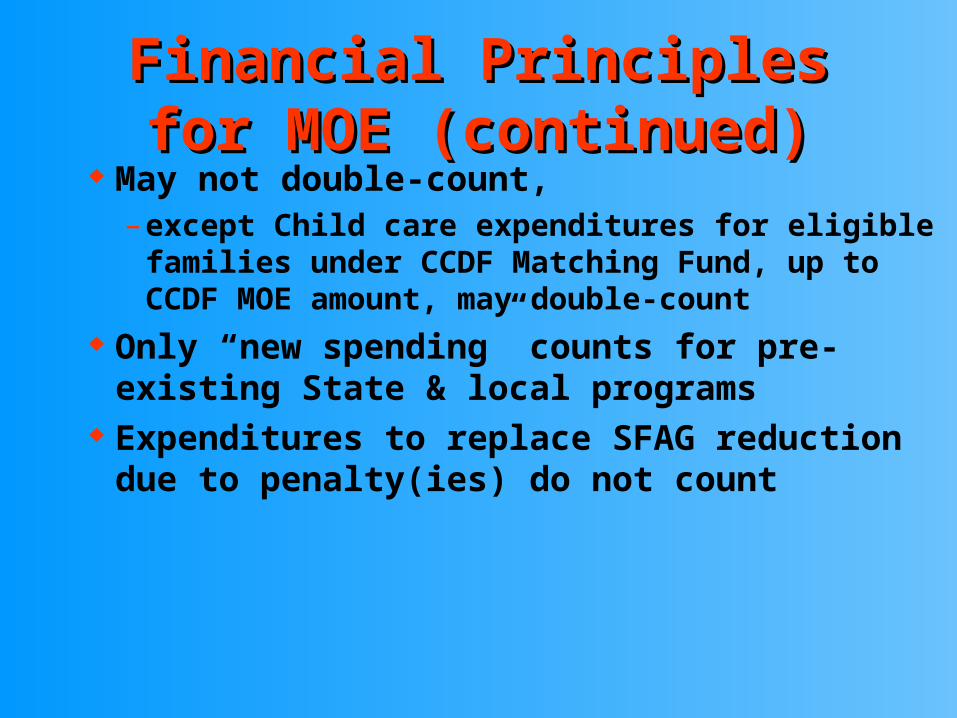

May not double-count, – except Child care expenditures for eligible families

under CCDF Matching Fund, up to CCDF MOE amount, may double-count

Only “new spending” counts for pre-existing State & local programs

Expenditures to replace SFAG reduction due to penalty(ies) do not count

Financial Principles for MOE Financial Principles for MOE (continued)(continued)

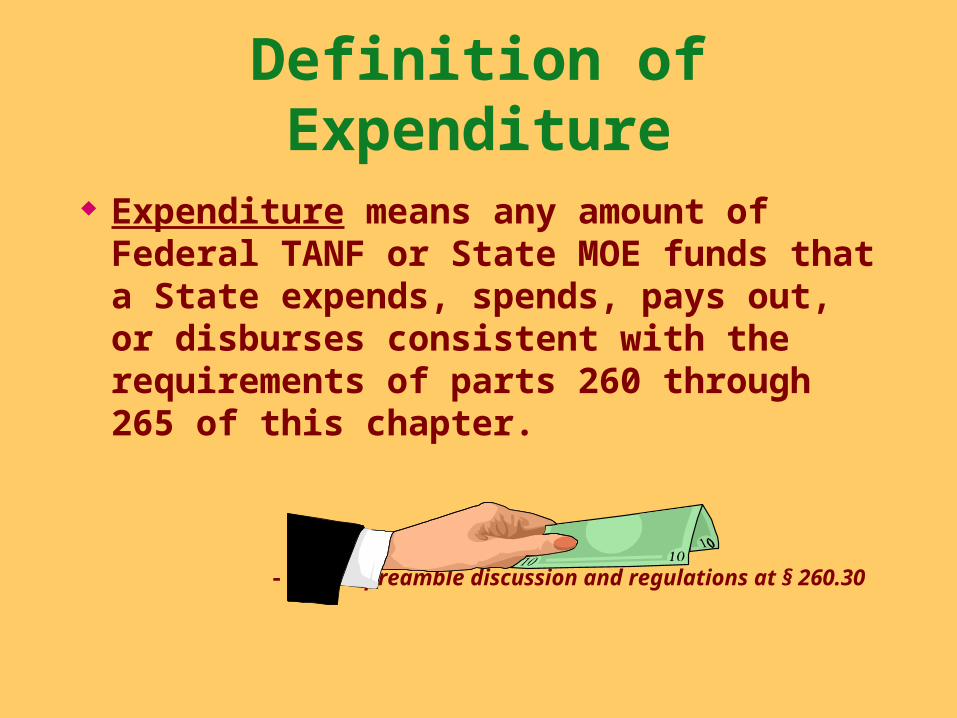

Definition of Expenditure

Expenditure means any amount of Federal TANF or State MOE funds that a State expends, spends, pays out, or disburses consistent with the requirements of parts 260 through 265 of this chapter.

- - See preamble discussion and regulations at § 260.30

What the Term "Refundable" Does Not Mean::

Not simply a tax refund check to a taxpayer

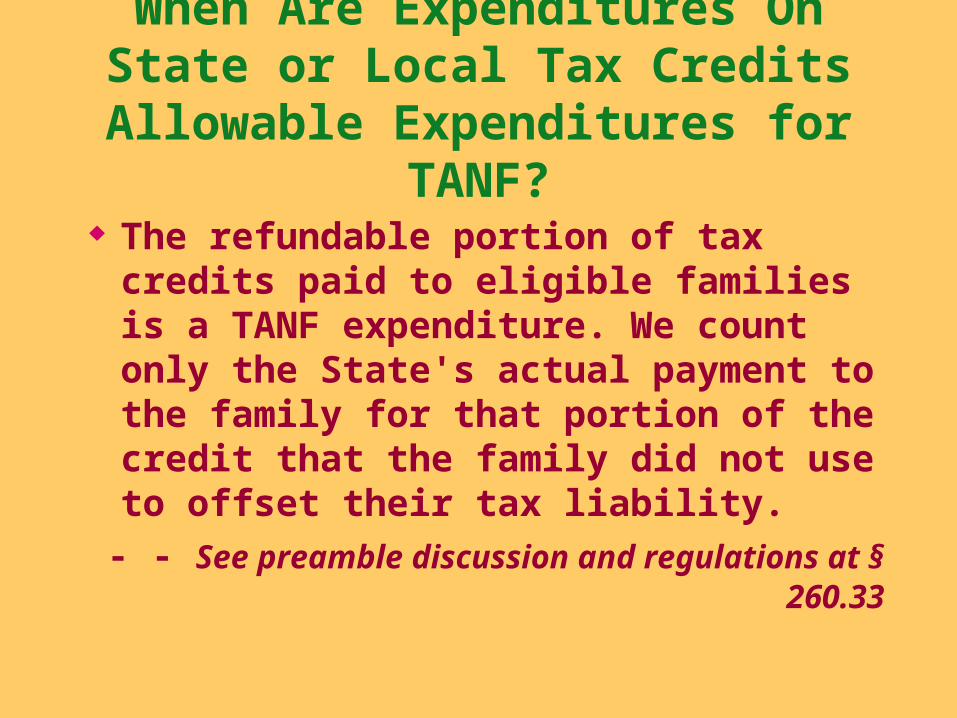

When Are Expenditures On State or Local Tax Credits Allowable

Expenditures for TANF?

The refundable portion of tax credits paid to eligible families is a TANF expenditure. We count only the State's actual payment to the family for that portion of the credit that the family did not use to offset their tax liability.

- - See preamble discussion and regulations at § 260.33

TAX CREDIT CALCULATION TAX CREDIT CALCULATION EXAMPLEEXAMPLE

Earned income tax credit (EITC): $200

Tax liability: - $ 75

If actually paid to the family,

the refundable portion of EITC

could be as much as: $125

Administrative Costs(Statutory Provisions)

15% limit on Fed. and State administrative expenditures

Excludes costs for information technology and computerization for tracking and monitoring TANF requirements

Administrative Costs

- - costs necessary for the proper administration of the TANF program or separate State programs.

--general administration, eligibility determination, and coordination of these programs, including indirect (or overhead) costs.

- - See §263.0(b) of preamble and reg

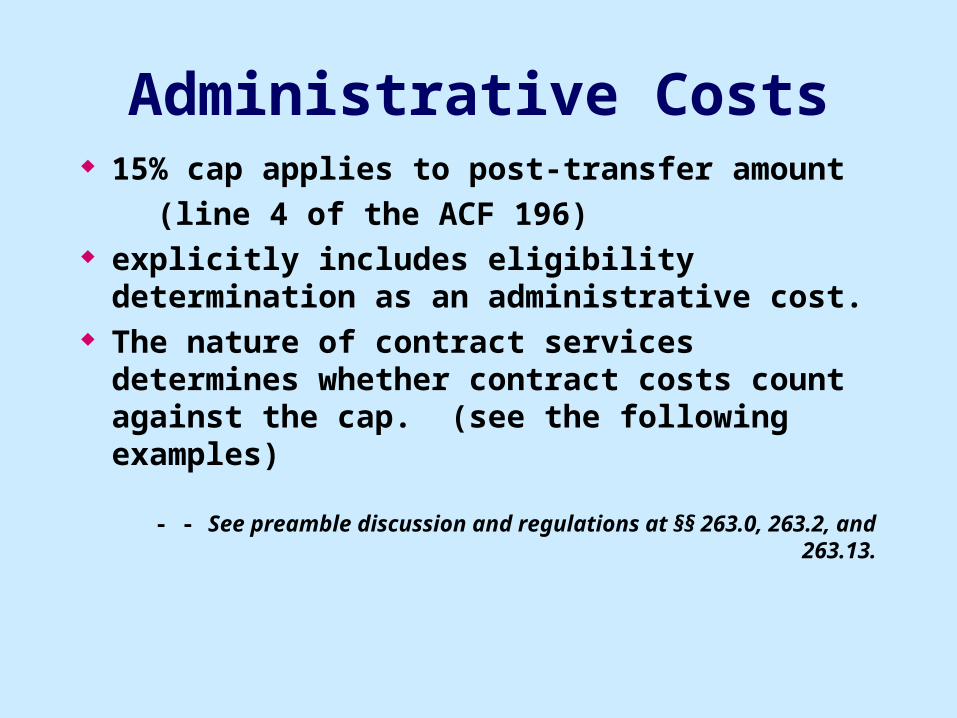

Administrative Costs 15% cap applies to post-transfer amount

(line 4 of the ACF 196) explicitly includes eligibility determination as an

administrative cost. The nature of contract services determines

whether contract costs count against the cap. (see the following examples)

- - See preamble discussion and regulations at §§ 263.0, 263.2, and 263.13.

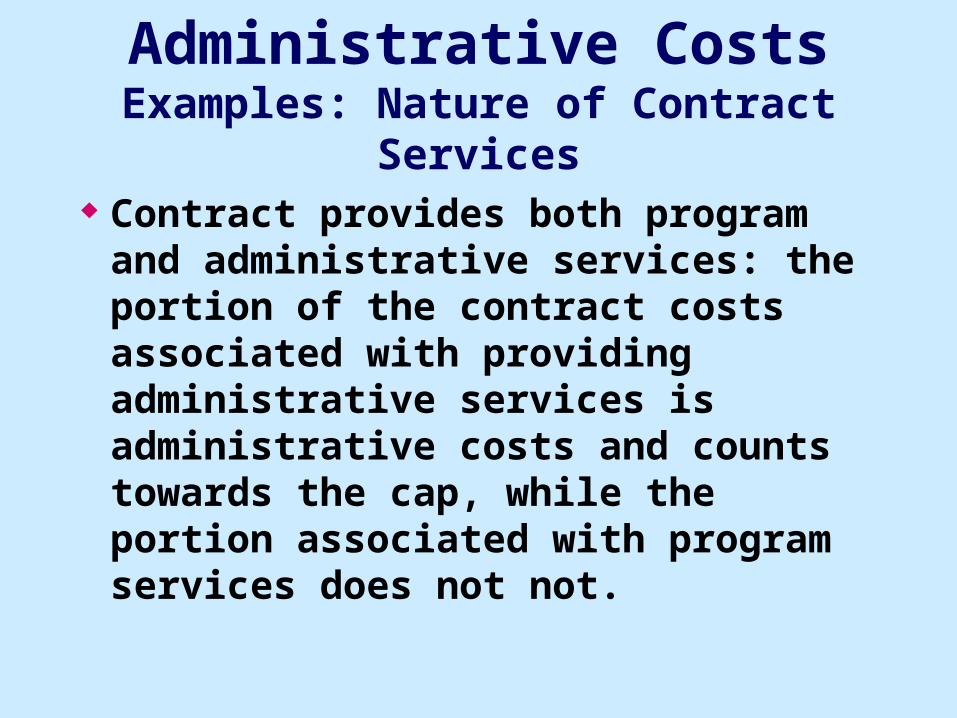

Administrative CostsExamples: Nature of Contract Services

Contract provides program services only: the entire cost of the contract is program costs.

Contract provides only administrative services to the State: the entire cost of the contract counts towards the 15% cap.

Administrative CostsExamples: Nature of Contract Services

Contract provides both program and administrative services: the portion of the contract costs associated with providing administrative services is administrative costs and counts towards the cap, while the portion associated with program services does not not.

TANF Regulation: Fiscal Provisions Funding Options MOE Requirements Financial Principles Definition of Expenditure Admin Costs Penalties / Annual Report Use of Funds Expenditure Report

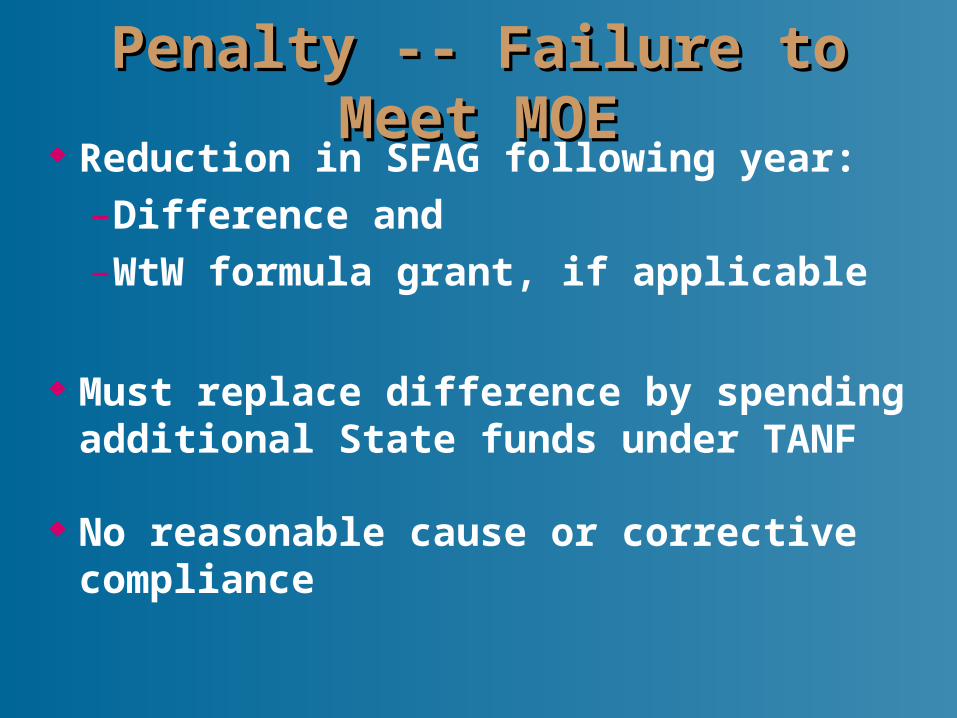

Penalty -- Failure to Meet MOEPenalty -- Failure to Meet MOE Reduction in SFAG following year:

– Difference and

– WtW formula grant, if applicable

Must replace difference by spending additional State funds under TANF

No reasonable cause or corrective compliance

Annual ReportAnnual Report

With 4th quarter data report or as a separate report

Report on all programs for which State claims MOE expenditures

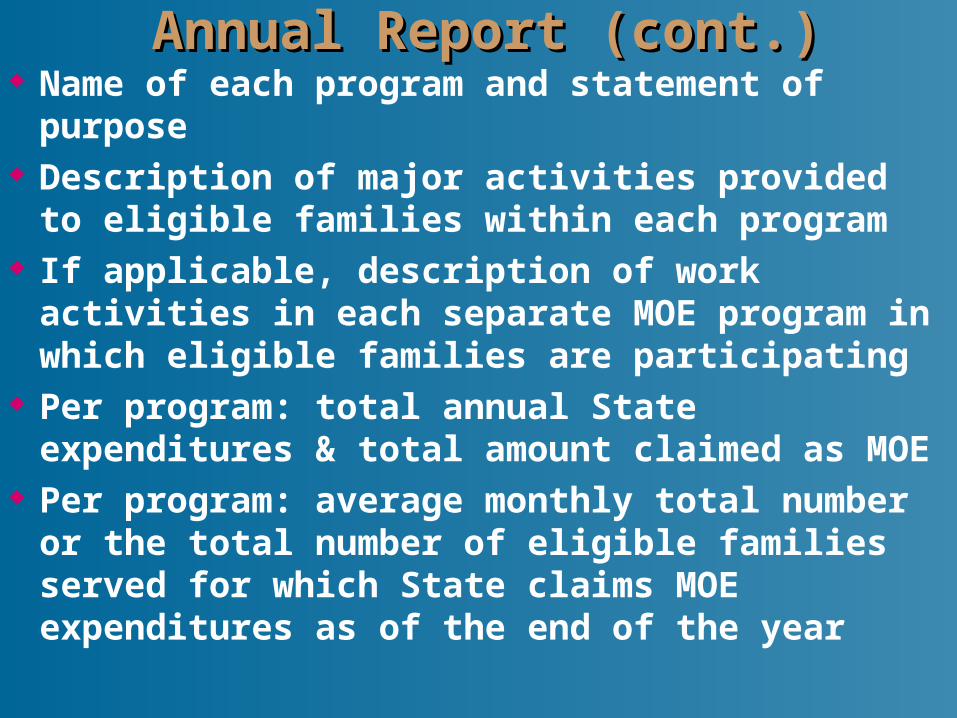

Annual Report (cont.)Annual Report (cont.) Name of each program and statement of purpose Description of major activities provided to

eligible families within each program If applicable, description of work activities in

each separate MOE program in which eligible families are participating

Per program: total annual State expenditures & total amount claimed as MOE

Per program: average monthly total number or the total number of eligible families served for which State claims MOE expenditures as of the end of the year

Eligibility criteria of families served under each program/activity

State whether program/activity had been previously authorized & allowable as of 8/21/96 under prior law

If not previously authorized & allowable, give FY 95 expenditures

Certification that all families for which State claims MOE expenditures met State’s criteria for “eligible families”

Annual Report (cont.)Annual Report (cont.)

Use of Federal TANF FundsUse of Federal TANF Funds

Use Federal TANF FundsUse Federal TANF Funds In any manner reasonably calculated to

accomplish a purpose of TANF -- 404(a)(1)– provide assistance to needy families

– end dependence of needy parents by promoting job preparation, work, and marriage

– reduce & prevent out-of-wedlock pregnancies, and

– encourage formation & maintenance of 2-parent families

Use Federal TANF Funds (cont.)Use Federal TANF Funds (cont.) In any manner authorized under old

programs, as of 9/30/95 or 8/21/96 -- 404(a)(2)– covers activities not permissible under 404(a)

(1)

– allowable, if activities authorized via former approved IV-A or IV-F plan

– 408 provisions n/a -- e.g., 408(a)(1)

– per financial criteria in former approved plan

Use Federal TANF Funds (cont.)Use Federal TANF Funds (cont.) To transfer up to 30% per year to CCDBG

&/or SSBG (up to 10% for FY’s 97-00; 4.25% eff. FY 2001) -- 404(d)

To reserve amount for subsequent years -- 404(e)– must be expended to provide “assistance” under

TANF

– may not transfer reserved funds to CCDBG or SSBG

ConsiderationsConsiderations 15% admin. cap unless excepted

Prohibitions in 408 of Act & 115(a)(1) of PRWORA & limitations in 404 (e.g., reserve funds) apply even if an activity seems otherwise consistent with a purpose of TANF

OMB Circular A-87 & 45 CFR Part 92 apply to TANF

Considerations (cont.)Considerations (cont.) May use Federal TANF funds to match other grant

programs only if authorized by law -- funds so used subject to TANF requirements

Use program income for allowable TANF activities Do not use TANF funds for construction or

purchase of facilities or buildings Use reasonable interpretations of statutory language

for any provisions not addressed in the final rule

MisuseMisuse Violations of: sections 404, 408 & other

provisions of the Act; section 115(a)(1) of PRWORA

Violations of provisions of Part 92 or OMB Circular A-87

Examples:– Administrative expenditures in excess of cap

– In appropriate transfers including transfers to CCDBG or SSBG in excess of caps

1. Families that receive federally-funded “assistance” or any MOE-funded “assistance” or “non-assistance” must also meet the family composition requirement (have a child living with a parent or other adult-caretaker relative, or be a pregnant woman.

2. This column and the next one do not apply if Federal funds have been commingled with State MOE funds.

Potential Services to FamiliesPotential Services to Families

TANF Regulation: Fiscal Provisions Funding Options MOE Requirements Financial Principles Definition of Expenditure Admin Costs Penalties / Annual Report Use of Funds Expenditure Report

Federal TANF Funds State MOE Funds

TANF Grant

Commingled State & Federal TANF

Segregated State TANF

Separate State

Program

TANF PROGRAM

Transfer to:

CCDF & SSBG

Potential Funding OptionsPotential Funding Options

ACF-196

ACF-196 Line Items

AVAILABLE FEDERAL FUNDSAVAILABLE FEDERAL FUNDS 1. Awarded 2. Transferred To CCDF

Discretionary 3. Transferred To SSBG 4. Adjusted SFAG

$$

EXPENDITURE CATEGORIES

5. EXPENDITURES ON ASSISTANCE

a. BASIC ASSISTANCE b. CHILD CARE c. OTHER SUPPORTIVE SERVICES d. ASSISTANCE AUTHORIZED

SOLELY UNDER PRIOR LAW

ACF-196 Line Items

Top Portion of ACF-196

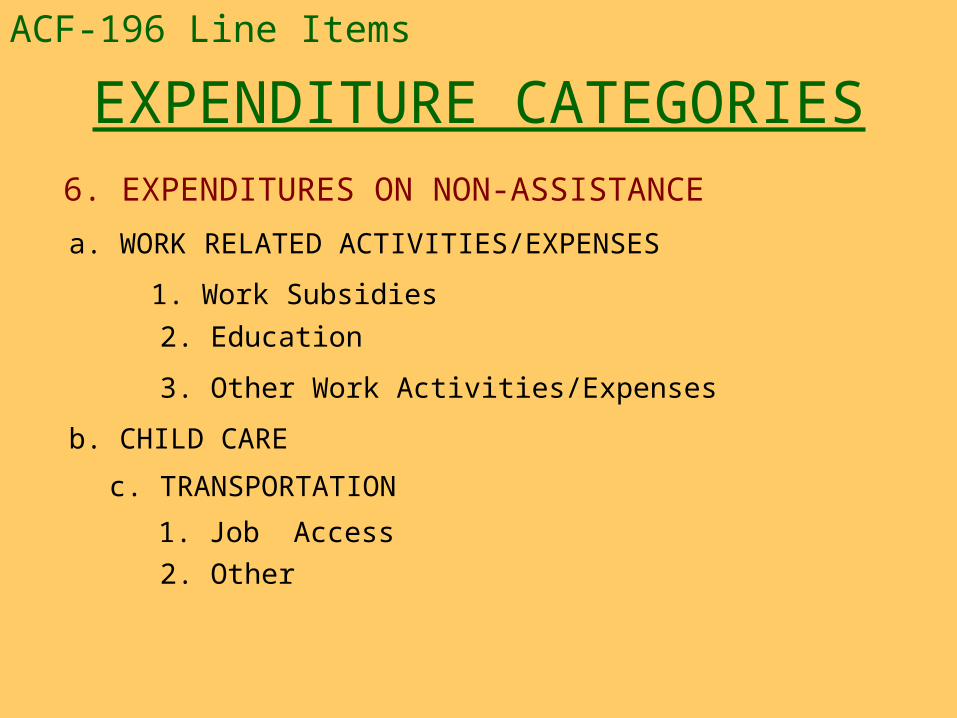

EXPENDITURE CATEGORIES 6. EXPENDITURES ON NON-ASSISTANCE

a. WORK RELATED ACTIVITIES/EXPENSES

1. Work Subsidies

2. Education

3. Other Work Activities/Expenses b. CHILD CARE

c. TRANSPORTATION

1. Job Access

2. Other

ACF-196 Line Items

EXPENDITURE CATEGORIES 6. EXPENDITURES ON NON-ASSISTANCE (continued)

d. Individual Development Accounts e. Refundable Earned Income Tax Credits f. Other Refundable Tax Credits g. Diversion Payments h. Prevention Of Out-of-wedlock

Pregnancies i. 2-parent Family Formation And

Maintenance j. Administration k. Systems l. Other

ACF-196 Line Items

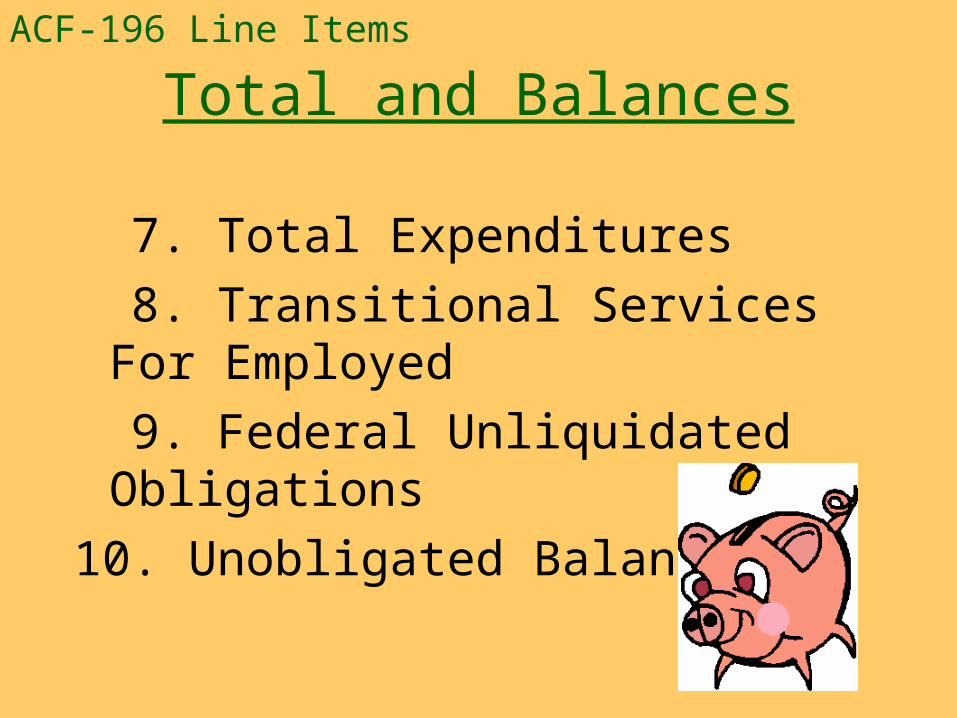

Total and Balances

7. Total Expenditures 8. Transitional Services For

Employed 9. Federal Unliquidated

Obligations10. Unobligated Balance

ACF-196 Line Items

Middle of ACF-196Column: A B C D

State Replacement Funds &

Quarterly Estimate

11. State Replacement Funds

12. Estimate for Next Quarter Ended

ACF-196 Line Items

Bottom of ACF-196

Questions?Questions?