talbros automotive components limited - …aceanalyser.com/analyst meet/105160_20070731.pdfsnapshot...

TRANSCRIPT

Talbros

Automotive Components Ltd. (TACL)

Analyst Meet

August 2007Mumbai

Gaskets Stamping & Rubber

Forging

Private & Confidential

Private & Confidential

Overview

Snapshot of the company

About the Company

Auto Component Industry and Peer Analysis

Future Outlook and Performance

Investor Information

Snapshot of the company

Financial Performance

Auto Component Industry and Peer Analysis

Future Outlook

Summary

Snapshot of Talbros

Automotive Components Limited (TACL)•

Background •

History•

Group Companies•

Plant Location & Products•

Market Position & Technical Collaboration•

Customers •

Promoters & Management•

Historical Financials

Snapshot of the company

Financial performance

Auto Component Industry and Peer Analysis

Future Outlook

Summary

Private & Confidential

Private & Confidential

Background

•

Talbros

Automotive Components Limited (TACL) is an auto ancillary promoted by the Talwar

Family (Talwar

Group). In addition to TACL the Talwar

Group consists of: •

Nippon Leakless

Talbros

(P) Ltd. (A joint venture with Nippon Leakless

Corporation of Japan & TACL)

•

QH Talbros

(A joint venture with Quinton Hazell

Automotive, UK & Talwar

family)•

T&T Motors a dealership for Mercedes Benz Passenger Vehicles

•

TACL is India's largest gasket manufacturer and is OE suppliers to almost all engine and vehicle manufacturers in India, including Trucks and Buses, Light Utility Vehicle, Passenger Cars, Tractors, Two Wheelers, industrial and Stationary Diesel Engines.

•

TACL is also the leader in the Indian aftermarket with the largest distribution network of over 80 exclusive outlets and 8,500 retailers.

•

Talbros

gaskets are exported to over 25 countries around the world.

•

TACL is certified under TS-16949 as well as ISO 14001.

•

TACL has received the Best Vendor Award from TATA Cummins Ltd twice, 2001 -

2002 and 2003-

2004. It has also received best vendor award for the years 2001-02 & 2002-03 from Eicher

Motors.

•

TACL is the single source supplier to TATA Cummins, Hyundai Motors, John Deere & Eicher

Motors.

Private & Confidential

Private & Confidential

History (1)

•

Incorporated on 8th September, 1956 in the name of Payen

Talbros

Private Limited by Talwar

Family in technical collaboration with Coopers Payen

Limited, UK and in financial collaboration with Engineering Components Limited, UK for manufacturing of automotive and industrial gaskets.

•

First Gasket manufacturing plant was set up in 1957 at Delhi which was later shifted to Faridabad

in the year 1967.

•

Converted into a public limited company in 1975 and the name of the company was changed to “Talbros

Automotive Components Ltd.,”

on 7th April, 1979. Maiden public issue in the year 1980.

•

In the year 1979, second manufacturing facility for gaskets was established in Chennai in order to cater to OEM’s requirement in southern India.

•

A backward integration plan was implemented during 1989 by setting up a plant at Sohna, near Gurgaon, Haryana

to manufacture ‘Beater’

(a raw material used in manufacturing of gaskets) for captive consumption.

Private & Confidential

Private & Confidential

History (2)

•

Third gaskets manufacturing plant at Pune

in Maharashtra

was added in the year 1995 primarily to cater to the needs of Tata

Motors, Bajaj

Tempo and other OEMs based in and around Pune.

•

In the year 2005, the company established a 40:60 JV with Nippon

Leakless

Corporation of Japan (NLK) for manufacturing of non-asbestos gaskets for Automobile Manufacturers. NLK is a major gasket supplier to Honda in various countries.

•

Recently, the company has set up a 8000 TPA hot forging plant for manufacturing hot forged auto components. Commercial production

started in January, 2007. Forging plant is backed by 2.5 MW captive power plant to ensure uninterrupted supply of power.

•

In another development the company has acquired two new business

–

Sheet Metal Components business of XO Stampings Ltd., (a Tier II

supplier to Maruti

& Tata

Motors) and IT Undertaking of XO Infotech

Ltd. These new acquisitions will provide significant tax benefits to the company, in addition to adding new product line.

Private & Confidential

Private & Confidential

Snapshot -

TACL

Particulars (In Rs million) CAGR 2007 2006 2005 2004 2003

Share Capital 113.8 106.5 57.5 16.4 16.4

Net Worth 60% 646.9 662.0 166.6 128.1 112.2

Gross Block 54% 1211.2 402.0 333.1 274.4 234.4

Net Sales 21% 1576.2 1423.4 1160.4 938.3 725.8

EBDIT 29% 171.9 140.0 127.3 79.8 62.0

Post Tax Profit 53% 80.2 56.0 46.7 20.1 14.8

Private & Confidential

Private & Confidential

Group Holdings

•

Investments & Assets•

40% Stake in Nippon Leakless

Talbros

(P) Ltd.In the year 2005, TACL joined hands with Nippon Leakless

Corporation of Japan (NLK) and established a 40:60 joint venture for manufacturing of

non-asbestos gaskets for Japanese Automobile Manufacturers & Multi Layer Steel Gaskets for Passenger Cars in India. NLK is a major gasket supplier to Honda world wide.

•

8% Stake in QH TalbrosTACL has 8% stake in QH Talbros

Limited, a JV with Quinton Hazell

Automotive Ltd., UK-

QH Talbros, an ISO 9001/QS 9000 certified company, is market leader in safety critical, 'Sealed for life and self lubricating' Ball Joints. For the year ended 31 March 2007 the company achieved Net Sales of Rs. 1576.6 million.

•

Long Term association with Technical Collaborators •

M/s Federal Mogul Sealing Systems Ltd. (UK).•

M/s Nippon Leakless

Corporation (Japan)•

Presswerk

Krefeld

Gmbh

(Germany)

Private & Confidential

Private & Confidential

Business LinesCore Business Lines

Gaskets Forging Stamping & Rubber

New Business Lines, which will drive major future Growth

Products Include:Gasket Kits, Cylinder Head gaskets, Manifold & Exhaust System Gaskets, Secondary gaskets, Gasket materials

Products Include:Forged and Machined Auto Components

Products Include:Sheet Metal Components like Suspension arms, Steering linkages, back plates Disc pads, Dust Covers & Rubber Bushes.

The Stamping business has been acquired by merger of XO Stamping Ltd. with the company.

Product Capacity (tpa) Product Capacity (tpa)

Hot Forged Products 8000 Beater Addition Joining 500

TACL have capacity to manufacture a variety of gaskets with varied shapes and sizes, hence installed capacity cannot be measured in uniform units and changes with the change in product mix.

Private & Confidential

Private & Confidential

Plant Locations

Gasket manufacturing plants. 14/1, Delhi Mathura

Road, Faridabad.

22-B, Sidco

Industrial Estate, Ambattur, Chennai

Plot No. 68, F-II Block, MIDC, Pimpri, Pune-411 018

Beater (Raw Material for Gasket) manufacturing plant

Village Atta, Tehsil Nuh, Distt. Gurgaon, Sohna

(Haryana)

Forging Plant Plot No. 39-46, Sector 6, Industrial Growth Centre, Bawal, Distt. Rewari

Stamping Plant 280-281, Udyog

Vihar, Phase VI, Near Khandsa

Village, Sector 37,Gurgaon-122 001

JV Company –

Nippon Leakless

Talbors

(P) Ltd 125 A, Sector 6 Industrial Growth Centre Bawal, Distt. Rewari

IT Division 28, Electronic City, Sector 18, Gurgaon.

Private & Confidential

Private & Confidential

Technical Collaboration

Nippon Leakless Corporation, Japan.www.nlk.co.jp

Federal Mogul Sealing Systems (Slough) Ltd. [UK]

www.federal-mogul.com

Presswerk Krefeld Gmbh,Germanywww.pwk-mf.de

Private & Confidential

Private & Confidential

Customers

Affinia, USA Elbe, Germany Piccinelli, Italy

Private & Confidential

Private & Confidential

Established Market Position•

Few Organized PlayersWithin the organised

sector, there are primarily four players in Gaskets, namely TACL, Banco

Products (India) Limited, Victor Gaskets Limited and Sankar

Sealings

Ltd. all of which (except Sankar

Sealing) have a presence both in the OEM and replacement segments. The unorganized sector, consisting of 25-30 players, is highly fragmented, and catering mainly to replacement demand.

•

Major Supplier of Gaskets to various OEMsTACL continues to be a major supplier of cylinder head gaskets to various OEM’s like Tata Cummins, Tata Motors, Bajaj Auto, Ashok Leyland, Maruti

Suzuki, Swaraj

Mazda, Hindustan Motors, and Eicher

Motors and Hyundai Motors India Ltd. 75% of the revenue is from OE segment.

•

OEM Relationships and Wide Distribution NetworkTACL’s

strong OEM relationships and wide distribution reach (with 8,500 dealers) have enabled it to maintain its market position with a share of 50% of the gasket industry.

•

Strong Technical PartnersCylinder head gaskets constitute a major portion of total sales of the company, a product, which requires relatively greater technology support. Because of the technical collaborations TACL is well equipped to handle any competition in this segment.

•

Order Book Position of Forged Products is more than Rs 450 millionTACL is witnessing good demand for its hot forged auto component

products as well. In the very first year of operation itself the order book position of forged

products is more than Rs. 450 million.

Private & Confidential

Private & Confidential

Management

Members –•Mr. Vidur Talwar (Promoter)•Mr. Navin Juneja (Finance) •Mr. K Sairam (Operations)

Mr. Sujat VoraPresident

Mr. Jayant VermaGM-Operations

Mr. K K DoraPresident

Steering Committee

Gasket Business Stamping & RubberForging Business

A Steering Committee comprising of Two professionals and one promoter has been formed to implement the decisions taken by the Board of Directors to run the business.

Private & Confidential

Private & Confidential

Steering Committee

Mr. Vidur

Talwar

MBA (Fin) from Drexel University, USA aged about 37 years has to

his credit setting up of XO Stampings Ltd. for sheet metal control arms for Maruti

Suzuki, Tata Motors and General Motors. He has also setup T & T Motors, dealer of Mercedes Benz.

Mr. Navin

Juneja

Aged about 49 years, is a Fellow Member of the Institute of chartered Accountants of India. He is associated with the group for last 18 years and has

played a key role in the growth of the group. He has excellent financial and negotiation skills.

Mr. K SairamB.E., PGDBM(MBA), 56 years, has worked in various organizations of repute such as Goetz India Ltd., Motherson

Sumi

Systems Ltd., Gulf Bitumen & Asphalt products Ltd. Dubai, Escorts Ltd (Yamaha Motor Cycle Division) before joining TACL in April 2001.

Private & Confidential

Private & Confidential

Key Management Personnel

•

Mr. R.P.Grover, Sr. Vice President-Finance:

Mr. R.P.Grover, B.Com.(Hons.), FCA, 49 years is the Chief Financial Officer of the company heading the

Finance and Accounts functions since 1997. Before joining the company he had worked for Tata Exports Ltd. and Usha

India Ltd.

•

Mr. Pankaj

Dhawan, Company Secretary :

Mr. Pankaj

Dhawan, 45 years is the Company Secretary and Assistant General Manager. He has been with the company since 1992. Prior to this he has worked as Asst. Company Secretary in Bindal

Agro Chem. Ltd., an Oswal

Group company.

•

Mr. Sudhir

Sabloke, Associate Vice President (Operations) :

Mr. Sudhir

Sabloke, PGD-Dies & Moulds, Dip. in Instrument Tech., 46 yrs. is heading the operations of the Faridabad Plant. He has worked for Escorts Ltd. and is backed by

24 year of experience.

•

Mr. D.B. Phatarphod, GM-Pune

Plant :

Mr. Phatarphod

a Diploma holder in Operation Management is backed by over 40 years of experience. He is the profit centre head of the Gasket Plant at Pune.

•

Mr. R.S. Balasubramanian, GM-Chennai Plant : Mr. Balasubramanian, B.E.(Mech. Engg.), 54 yrs is the profit centre head of Gasket Plant at Chennai having about 30 years experience. He has also worked for Sundram

Fasters Ltd.

Financial Performance

•

First quarter results•

Past performance•

Change in Shareholding pattern

Snapshot of the company

Financial Performance

Auto Component Industry and Peer Analysis

Future Outlook

Summary

Private & Confidential

Private & Confidential

First Quarter results -

June 30, 2007

Key Drivers during first quarter•

Sales growth continues. Sales up 30.4% over the corresponding quarter previous year

•

EBIDTA up by 61.2%•

Merger of XO Stamping ltd. and de-merger of IT business undertaking of XO InfoTech ltd. completed.

•

Construction activity for setting up a separate plant for rubber

components and expansion of stamping business capacities started.

•

Forging plant concluded orders in excess of Rs. 450 millions including orders of Rs. 250 millions for exports for which samples are being validated.

Private & Confidential

Private & Confidential

First Quarter results -

June 30, 2007

. (Rs. millions)

Particulars Qtr ending

June 30,2007 Qtr ending

June 30, 2006. Qtr ending

June 30, 2007 Qtr ending

June 30, 2006.

Net Sales 384.89 295.06 404.03 306.10

Other Income 6.95 3.80 7.46 3.08

Earning Before Interest & Depreciation (EBIDTA) 50.12 31.09 60.29 36.21

Interest & Financial Charges 17.85 4.25 17.89 4.27

Depreciation 16.26 7.50 16.56 7.74

Profit before Tax (PBT) 16.01 19.34 25.84 24.20

Provision for Taxation 1.40 5.97 3.63 7.58

Profit after Tax (PAT) 14.61 13.37 22.21 16.62

Paid up Equity Capital 113.79 106.52 113.79 106.52

Earning Per Share (EPS) (Rs.) 1.28 1.25 1.95 1.56

Financials for the Ist Quarter, April - June

Stand Alone Consolidated

Private & Confidential

Private & Confidential

Financials(In Rs million) Year End March 31 2002 2003 2004 2005 2006 2007

Equity Paid Up 0 16.4 16.4 16.4 57.5 106.5 113.8

Net worth 101.0 112.2 128.1 166.6 662.0 646.9

Gross Block 215.2 234.4 274.4 333.1 402.0 1,211.2

Net Sales 554.9 634.1 823.2 1,015.3 1,238.4 1,576.2

Other Income 10.1 18.4 16.9 16.1 21.9 30.5

EBIDTA 57.1 62.0 79.8 127.3 140.0 171.9

Depreciation 15.6 16.9 18.7 22.8 27.8 53.9

PAT 13.2 14.8 20.1 46.7 56.0 80.2

Book Value (in Rs.) 61.6 68.4 78.1 29.0 62.2 56.8

Market Capitalization 28.8 36.5 86.8 602.0 937.2 788.0

EPS (in Rs.) 8.1 8.8 12.0 8.0 6.74 7.1

EBIDTAM (%) 10.3 9.7 9.7 12.5 11.3 10.9

PATM (%) 2.4 2.3 2.4 4.6 4.5 5.1

ROCE (%) 17.2 17.0 19.2 26.3 18.2 13.5

RONW (%) 12.6 13.9 16.7 31.7 13.5 12.3

During the Financial Year 2005-06 the company raised Rs 475 million by fresh Issue of equity for setting up a forging plant. The Forging Plant has started commercial Production in January 2007.

Private & Confidential

Private & Confidential

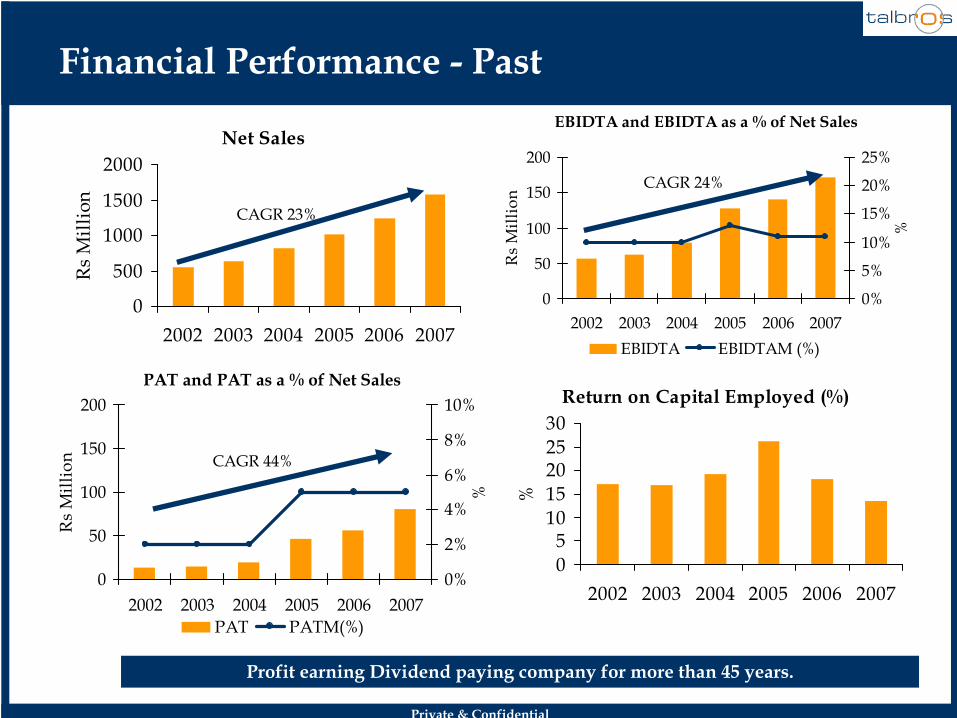

Net Sales

0

500

1000

1500

2000

2002 2003 2004 2005 2006 2007

Rs

Mill

ion

Financial Performance -

Past

CAGR 23%

EBIDTA and EBIDTA as a % of Net Sales

0

50

100

150

200

2002 2003 2004 2005 2006 2007

Rs

Mill

ion

0%

5%

10%

15%

20%

25%

%

EBIDTA EBIDTAM (%)

CAGR 24%

PAT and PAT as a % of Net Sales

0

50

100

150

200

2002 2003 2004 2005 2006 2007

Rs

Mill

ion

0%

2%

4%

6%

8%

10%

%

PAT PATM(%)

CAGR 44%

Return on Capital Employed (%)

05

1015202530

2002 2003 2004 2005 2006 2007

%

Profit earning Dividend paying company for more than 45 years.

Private & Confidential

Private & Confidential

Shareholding Pattern

As on 31st March 07 After the Merger After Conversion of Warrants

No. of Shares Held %

No. of Shares Held %

No. of Shares Held %

Promoters Holding

-

Individuals/ HUFs 2,559,421 24.03% 3,062,099 26.91% 3,062,099 24.34%

-

Bodies Corporate 241,509 2.27% 273,009 2.40% 1,473,009 11.71%

Sub-total 2,800,930 26.29% 3,335,108 29.31% 4,535,108 36.05%

Public Holding

a) Institutions

-

Mutual Funds/ UTI 123,304 1.16% 123,304 1.08% 123,304 0.98%

-

FIs/ Banks/Insurance Co. 968,173 9.09% 1,005,673 8.84% 1,005,673 7.99%

- FIIs 495,200 4.65% 495,200 4.35% 495,200 3.94%

b) Non-Institutions

-

Bodies Corporate 1,488,102 13.97% 1,580,550 13.89% 1,580,550 12.56%

-

Individuals 4,361,814 40.95% 4,406,896 38.73% 4,406,896 35.03%

- NRIs 382,666 3.59% 387,513 3.41% 387,513 3.08%

- Others 31,777 0.30% 45,386 0.40% 45,386 0.36%

Sub-total 7,851,036 73.71% 8,044,522 70.69% 8,044,522 63.95%

Grand Total 10,651,966 100.00% 11,379,630 100.00% 12,579,630 100.00%

Industry

•

About the Indian Auto Component Industry•

Industry Dynamics•

Growth in Auto Component Industry•

The Outsourcing Opportunity•

Competitor Analysis for TACL

Snapshot of the company

Financial performance

Auto Component Industry and Peer Analysis

Future Outlook and Performance

Summary

Private & Confidential

Private & Confidential

Auto Component Industry

•

The Indian auto component industry is extensive and highly fragmented.

•

Estimates by the Department of Heavy Industries, GOI, indicate there are over 400 large firms who are part of the organised

sector and cater largely to the Original Equipment Manufacturers (OEMs). Another 10,000 firms exist in the unorganized sector .

•

Around 4% of the companies operating in the auto component segment cater to 80% of the demand emanating from OEMs.

•

Auto component industry is highly dependent on the fortunes of automotive industry. Factors that drive the vehicle market also have an influence on the Auto

component market.

•

Secondary demand for auto component parts come from replacement market.

•

The Automobile Industry in the past years has shown impressive growth resulting in the demand for Passenger Cars, Commercial Vehicles and Motor Cycles.

•

The domestic auto component industry is also buoyant due to the interest shown by the global OEMs for sourcing their global requirements from India as well as increased demand from Domestic OE customers

Component Wise Share of Production

Others 34%

Engine Parts 23%

Equipments7%

Suspension &Braking Parts

12%

Drive Transmission & Steering Parts

16%

Electrical Parts7%

Private & Confidential

Private & Confidential

Industry Dynamics

•Performance of the auto sector•Performance of other user industries such as general engineering, Defence, Railways, Industrial

machinery and Machine tools•Easy availability of Finance•Investment & Growth in Infrastructure –

specifically in Transportation & Roads.•Large scale sourcing of components from Global Automotive MNCs.

•In-house designing, manufacturing and validating skills to match exacting global standards

•Manufacturing capabilities to consistently meet volumes demanded by major customers

•Smooth relationship with OEMs •Operational efficiency -

in raw-materials, scrap, manpower and financial aspects

•Zero-defect quality products, priced competitively •New product development capability -

to cater to emerging new markets

•Export focus -

maintaining product quality and price and sticking to delivery schedules.

•Access to contemporary technology by associating with a globally renowned technical partner.

•High bargaining power of OEMs •Recession in user industries, particularly auto •Rising cost of inputs -

like steel, other raw materials and power

•Need to continously

invest in order to meet the technology upgradation

required interms

of Safety, Comfort & Emissions.

•Economy trends in export markets coupled with stiff competition from other exporting nations

•Highly capital intensive; high working capital requirements with steel suppliers extending no credit while OEM customers demanding the same.

Demand Drivers

Critical Success factors Business Concerns

Private & Confidential

Private & Confidential

Growth in Auto Component Sector

•

The car components market in India is estimated to grow at a cumulative aggregate rate of 15% a year until 2012 as per AT Kearney.

•

Further, encouraging factor is that the industry is emerging from its dependence on the Indian car market and is gradually establishing it in global markets.

•

Exports of auto components from India have witnessed a CAGR of 20.3% over the last six years. Currently total exports are US$ 2 billion which is very insignificant compared to global component trade currently estimated at around US $1.2 trillion.

•

The total turnover of the Indian auto component industry is estimated at US$10 bn

in 2006. Indian automotive exports is expected to touch US$ 5.9 billion level by

2009 and US$ 40 billion by 2014 (ACMA).

•

Global OEMs are increasingly sourcing components from cheaper manufacturing destinations and Indian component manufacturers offer a great cost-quality proposition.

Economic Survey 2006-07 says:

The turnover of the auto component sector has grown from US$ 3.1

billion to US$ 10.0 billion between 1997-98 and 2005-06. In 2005-06, the sector's exports grew by 28 per cent to reach US$ 1.8 billion. The major destinations of export for this sector are US

and Europe, which belong to the category of high Accepted Quality Level (AQL).

Private & Confidential

Private & Confidential

The Outsourcing Opportunity

US Ancillary Manufacturers Indian Ancillary Manufacturers

Material & Capital Labor DepreciationOverheads & Others Profits

30%

32%

5%

28%

5%

50%

12.5%7.5%15%15%

20-30% Savings

Indian Ancillary Manufacturers Enjoy a 20-30% Cost Advantage over US Counterparts

The Indian auto component industry is one of the few sectors in the economy that has a distinct global competitive advantage in terms of cost and quality. The value in

sourcing auto components from India includes low labour

cost, raw material availability, technically skilled manpower and quality

assurance. An average cost reduction of nearly 25-30% has attracted several global automobile manufacturers to set base since 1991.

The global auto components industry is estimated at US$1.2 trillion

Estimated exports of Indian forging industry (15% of country's auto component exports for 2005-06) US$ 360 million. Projected exports of Forging industry by 2015 US$ 5 billion (15% of auto component exports).

Future Outlook

•

Future Plans•

Restructuring for Rapid growth•

Forthcoming Projects

Snapshot of the company

Financial Performance

Auto Component Industry and Peer Analysis

Future Outlook

Summary

Private & Confidential

Private & Confidential

Strengthening existing businesses

•

Growth Plans •

Setting up of machining facility at the forging plant. •

Setup a new Gasket Manufacturing Facility for OEMs in Uttrakhand•

Development of new generation gaskets with Technology Partnerships.•

Expanding Stamping Business from Rs.180 million during 2007 to over Rs.350 millions by 2010.

•

Facility for manufacturing of Rubber Products to be operational by April 2008.•

Plant in Lucknow

for supplying Sheet Metal components to Tata Motors

•

Benefits of forging Plant and expansion of the Stamping facility

will start accruing now. •

The commercial production in the Forging Plant started in January 2007. Current Order Book position is more than Rs. 450 millions.

•

The Stamping business, which was acquired in 2006 will also improve the performance of the company in the coming years

•

New facility for gaskets at Utrakhand

will be commissioned during 2008-09.

Forging & Stamping Businesses

Benefits

Private & Confidential

Private & Confidential

Future Plans

•

Increase Forging CapacityTACL is planning to invest in machining facility for its forgings, owing to very enthusiastic response from its customers.

•

Setup a Gasket Manufacturing Facility for OEM’s in UttrakhandTata Motors Ltd., Mahindra & Mahindra and Bajaj Auto Ltd., the two major customers of TACL are already setting up large vehicle manufacturing plants in Uttarakhand

due to the various benefits and incentives offered by Uttarakhnad

Government. TACL is also planning to setup its plant in the state; for supplying Gasket to these OEMs and to cater to the demand of replacement market; to exploit the various benefits and incentives being offered.

•

R&D in GasketsTACL is in the process of Developing gaskets for new generation commercial vehicles and passenger cars.

•

Expand Stamping BusinessTACL is also planning to expand the stamping business recently taken over by amalgamation of XO stampings Ltd.

•

Facility for Manufacturing of Rubber ProductsTACL is also planning to set up a separate facility for manufacturing of rubber products such as dust covers, bushes, rubber gaskets and a new generation Steel Elastometer

Gaskets.

•

Plant in Lucknow for Supplying Sheet Metal components to Tata MotorsTACL is in the process of setting up a new plant in Lucknow, Uttar Pradesh for exclusive supply of sheet metal components to Tata motors.

Private & Confidential

Private & Confidential

Restructuring for Rapid Growth

•

Change in management StructureThe management structure of the TACL has undergone a major revamp recently. The conscious decision to run the operations by the professionals has resulted in three fold rise in sales from FY 01 to FY 07.

•

JV with Nippon Leakless

Corporation of JapanA new joint venture company has been formed with a leading Japanese company –

Nippon Leakless

Corporation.

•

Stamping BusinessThe company has acquired the sheet metal business of XO Stampings Ltd. and IT business of XO Infotech

Ltd.

•

Forging BusinessIn order to diversify and to move to high margin products the company has started manufacturing of forged auto components.

Private & Confidential

Private & Confidential

Forthcoming Projects (1)

ProjectCost (in Rs million) Brief Description

Plant in Uttrakhand

110 The Uttaranchal Govt. offers a number of incentives to new industrial units in the state. Tata Motors Ltd. and Bajaj Auto Ltd., the two major customers are setting up large vehicle manufacturing plants in the state. Talbros

is also setting up gasket manufacturing plant in the state to cater to the OEMs. Moreover, the replacement market supplies from Uttarakhand

will be very cost competitive as there would not be any excise duty on product.

Expansion of Stamping Business

60 The company plans to expand the stamping business recently taken over by way of amalgamation of XO Stampings Ltd. which has been a tier two supplier to Maruti

and Tata Motors. Talbros

endeavor is to relocate the plant, modernize the facilities, widen its product range and quality and bring it to tier one status.

Rubber Plant 31 A separate facility to be set up at Faridabad for manufacturing automotive Dust Covers and Bushes. In addition to this the rubber plant will also be dedicated for manufacturing of rubber gaskets and Steel Elastomer

gaskets which is a new generation technology.

Private & Confidential

Private & Confidential

Forthcoming Projects (2)

ProjectCost (in Rs million) Brief Description

Forging Plant Expansion

70 The company, keeping in view the requirements of prospective customers, has decided to add facilities for machining of forged

components so as to provide finished components. Machining of components will facilitate higher value addition and consequently higher profitability.

Further investment in JV Company

30 The JV plant is being shifted to a newly constructed plant at Bawal, Haryana. The company has also acquired land at Hero Honda Vendor Park in Haridwar

and a new manufacturing facility will be established during the current year to cater to

the demands of Hero Honda.

Cap. Ex. at Faridabad & Pune

70 In order to adopt latest technologies to meet the requirements of new generation vehicles, the gasket manufacturing facilities at Faridabad and Pune

needs to be upgraded and expanded.

Real Estate Development

30 The real estate being part of IT Undertaking that is demerged with the company, is to be developed as it is a prime location and can fetch good rental.

Total Cost of Forthcoming Projects Rs 401 million

Private & Confidential

Private & Confidential

Product Mix -

2007

1,310 1,300

1,502

1,750

8

191 213361

506

1,180

814

407

0

500

1,000

1,500

2,000

2007 2008 2009 2010

Net Sales from various product lines (Rs. Millions)

Gasket Business Forgings Stampings & Rubber

Year ended 31st March

Private & Confidential

Private & Confidential

Summary

•

Market leader in Gasket manufacturing and forging plant already implemented (commercial production from Jan 07).

•

The company has entered into hot forged products business and has a healthy Order Book position of Rs. 450 million.

•

The company has long term international tie-ups giving access to latest technologies & processes in the gasket & forging business.

•

Stamping & Rubber products are being added to the company which will significantly contribute to top line as well as bottom line from

FY 09 onwards.

•

Actively looking for strategic partnership to boost exports•

TACL’s

JV with NLK is expected to boost its profitability further.•

Due to change in product mix, company expects margin expansion. •

Future Guidance:•

Expect CAGR of 27% in Sales upto

2010•

Expect CAGR of 35% in EBIDTA upto

2010

Private & Confidential

Private & Confidential

Snapshot -

TACL

Company DetailsChairman

: Mr. Naresh

TalwarAuditors : S.N. Dhawan

& Co.Bankers : ICICI Bank

State Bank of India.Registered Office

:14 / 1, Mathura Road Fairdabad

Haryanawww.talbros.com

Scrip DetailsMarket Capitalization

: Rs. 788 millionBook Value

: Rs. 56.84Equity Shares O/s1

: 11.4 million (as on 31/03/07)52 Week H/L

: Rs.80 / 44BSE Scrip Code

: 505160NSE Symbol

: TALBROAUTOReuters Code

: TALB.BO

1.

After allotment of shares due to merger of two companies

2. Figures for P/E, 52 Week H/L &Market Cap has been taken from the stocks listing details on BSE as on 6th

August 2007. Other figures as on 31st March 2007.

Shareholding as on March 31, 2007

Promoters, 36.05%

India Public and

Others, 35.39%

Pvt Corporate

Bodies, 12.56%

Institutions, 12.91%

NRIs, 3.08%

*After Conversions of warrants and Merger

*

Private & Confidential

Private & Confidential

Contact Information

Mr

Navin

JunejaGroup Chief Financial OfficerCorporate Office400, Udyog

Vihar, Phase IIIGURGAON 122016HARYANA, INDIA.Email: [email protected]: 0124-4002963

Private & Confidential

Private & Confidential

THANK YOU