tail risk hedging - canadian investment revie · tail risk hedging should be an integral part of...

TRANSCRIPT

August 2012

Tail Risk Hedging2012 Risk Management Conference

This document is provided for informational purposes only and is not intended to be an offer or solicitation, or the basis for any contract to purchase or sell any security or other instrument, or for AllianceBernstein to enter into or arrange any type of transaction as a consequence of any information contained herein. AllianceBernstein and its business units do not provide tax, legal or accounting advice and you should consult your professional advisors with respect to such matters. This presentation is not intended for public use or distribution. Neither this presentation nor any of its contents may be used for any other purpose without the express consent of AllianceBernstein.

This presentation is being provided to you upon request as a financially sophisticated investor.

Please Read the Following Disclosure

Simulated Performance: HYPOTHETICAL OR SIMULATED PERFORMANCE RESULTS HAVE CERTAIN INHERENT LIMITATIONS. The data presented herein is solely for illustrative purposes which may include among other things back testing, simulated results and scenario analyses. The information is based upon certain factors, assumptions and historical information that AllianceBernstein may in its discretion have considered appropriate, however, AllianceBernstein provides no assurance or guarantee that actual trades or trade structures will be the same as shown, or that this product will operate or would have operated in the past in a manner consistent with these assumptions. In the event any of the assumptions used do not prove to be true, results are likely to vary materially from the examples shown herein. Additionally, the results may not reflect material economic and market factors, such as liquidity constraints, transaction costs and other expenses which could reduce potential return. All levels are indicative and there is no representation that any transaction can or could have been effected at such level.

Fees: Investment management fees and incentive fees associated this this service may be higher than those charged by traditional funds and can offset trading profits. The incentive allocation made to the investment manager may create an incentive for the investment manager, to make investments that are riskier or more speculative than if the there was no incentive fee.

Investment and Trading Risks: The AllianceBernstein Tail Risk Hedging Strategy may engage in speculative investment practices, including the use of leverage, short sales and derivatives, that may increase the risk of investment loss.

Strategy-Specific Risks: In addition to the risks discussed above, the strategy is subject to the following investment and trading risks, risks associated with investment techniques such as limited diversification, margin transactions, short sales and leverage through derivative instruments, including options, futures and forward contracts, and swaps; and risks associated with investments in undervalued securities, in fixed income securities, in commodities futures, and in non-US securities and currencies, including those of emerging markets countries.

1

Tail Hedging: Mitigate Draw Downs, Higher Risk Premium, Lower Volatility

Tail risk frequency and severity are often underestimated using traditional methods

Managing tail risk and avoiding large losses is critical to long term wealth creation

Exp

ecte

d R

etur

n

long term wealth creation

Traditional methods of hedging tail risk are expensive and may have limited effectiveness

Innovative tail risk hedging techniques may help:

Lower overall portfolio risk and mitigate tail risk

Protect portfolios against increased tail correlations (diversification failure)

Tail risk hedging should be an integral part of asset allocation

2

RiskPortfolio+Tail HedgingOriginal Portfolio

Risk

allocation

August, 2012For illustrative purposes onlyThere can be no assurances objectives will be achieved.

What Is a Tail Hedge?

Technical Definition: A Tail Hedge strategy is designed to buffer a portfolio during a 3-standard deviation market event

Practical Definition: A Tail Hedge Strategy is like an umbrella…you want to own one before it rains

3

Traditional Portfolios Are Not Diversified By Risk

12-Month 99%VaR of a 60/40 Portfolio = 23.6%January 1988–December 2011

Equity96.8%

Source of VaR

Equity60%

Fixed Income

40%

Common Diversified Portfolio

4

Curve 0.8%Swap Spreads 0.0%Spread Credit and EMG 1.7%Spread Securitized 0.4%

Analysis for the period January 1988-December 2011

The Challenge:60% of the Allocation = 96.8% of the Risk

10%

…..60/40 Portfolio Drawdown vs SPX Drawdowns

Correlation: 88%

(40)%

(30)%

(20)%

(10)%

0%

(60)%

(50)%

71 73 75 77 79 81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 11

SPX Drawdown 60% SPX 40% Agg Drawdown

5

60/40 portfolio is 60% SPX/40% Barclays US AGG Index from 1976. Prior to1976, it is 60% SPX/40%US10yr Note

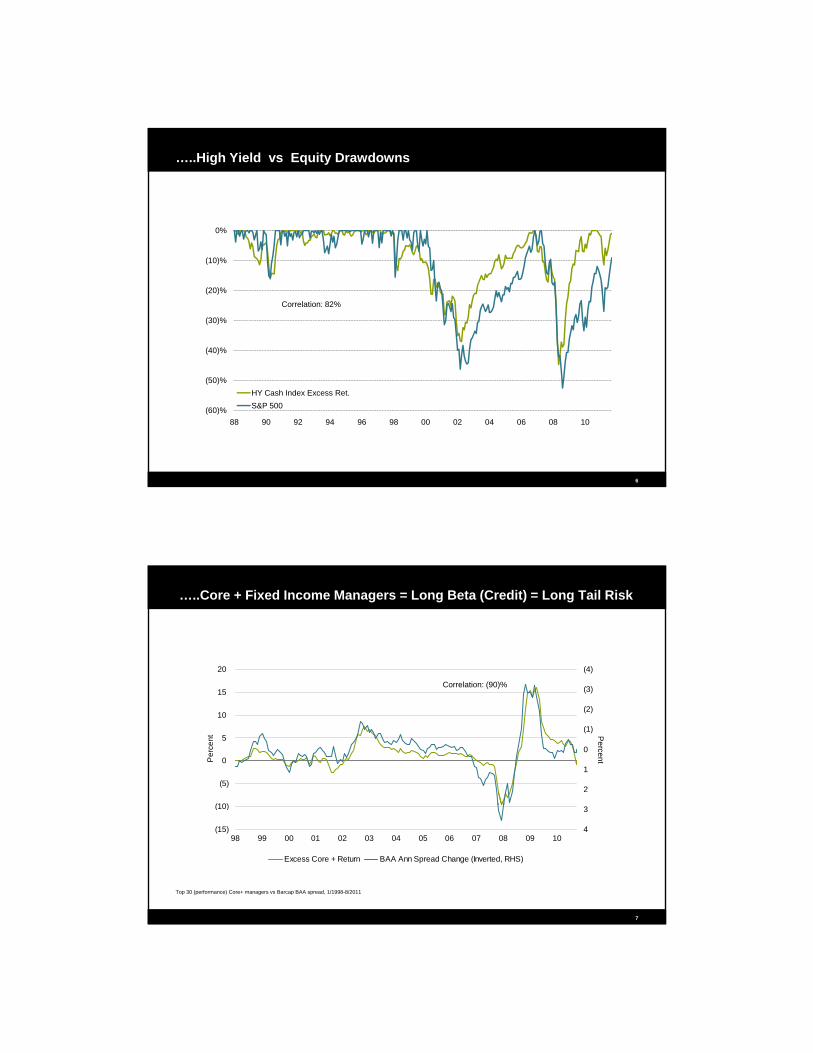

…..High Yield vs Equity Drawdowns

0%

(40)%

(30)%

(20)%

(10)%

Correlation: 82%

6

(60)%

(50)%

88 90 92 94 96 98 00 02 04 06 08 10

HY Cash Index Excess Ret.S&P 500

…..Core + Fixed Income Managers = Long Beta (Credit) = Long Tail Risk

20 (4)

Correlation: (90)%

(10)

(5)

0

5

10

15

Per

cent

(3)

(2)

(1)

0

1

2

Percent

Correlation: (90)%

7

Top 30 (performance) Core+ managers vs Barcap BAA spread, 1/1998-8/2011

(15)

(10)

98 99 00 01 02 03 04 05 06 07 08 09 10

3

4

Excess Core + Return BAA Ann Spread Change (Inverted, RHS)

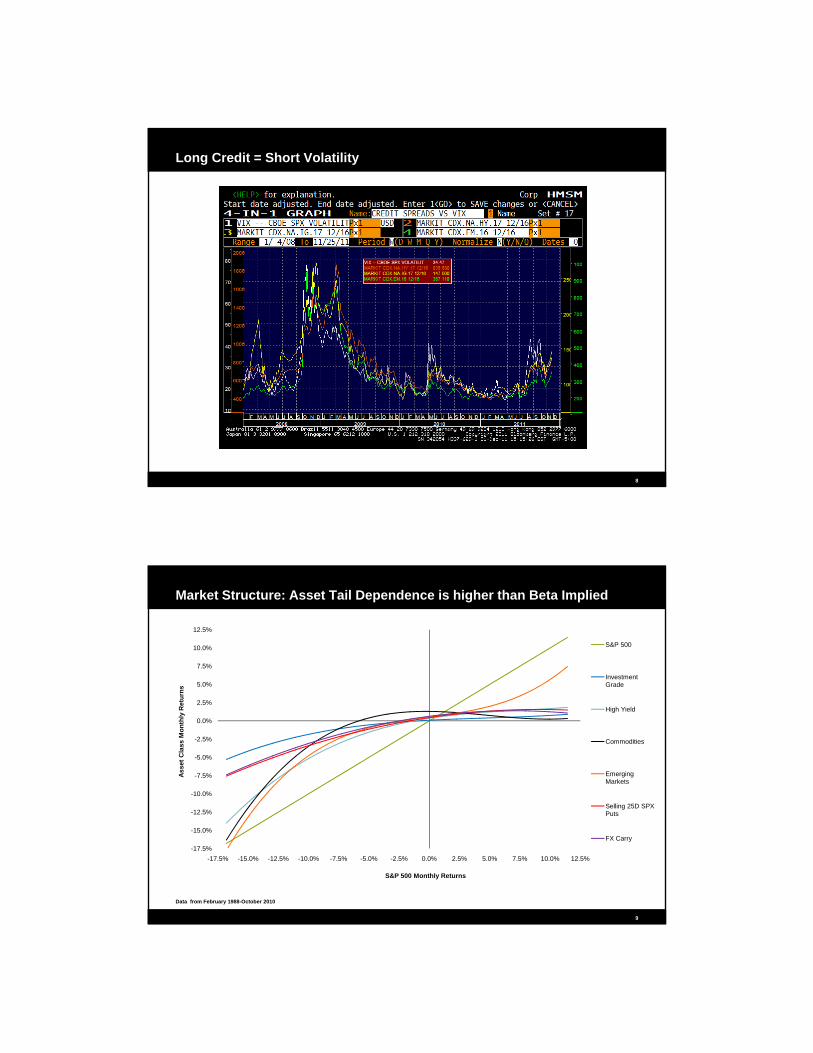

Long Credit = Short Volatility

8

5 0%

7.5%

10.0%

12.5%

S&P 500

Investment Grade

Market Structure: Asset Tail Dependence is higher than Beta Implied

-10.0%

-7.5%

-5.0%

-2.5%

0.0%

2.5%

5.0%

Asse

t Cla

ss M

onth

ly R

etur

ns

Grade

High Yield

Commodities

Emerging Markets

Selling 25D SPX

9

-17.5%

-15.0%

-12.5%

-17.5% -15.0% -12.5% -10.0% -7.5% -5.0% -2.5% 0.0% 2.5% 5.0% 7.5% 10.0% 12.5%

S&P 500 Monthly Returns

Selling 25D SPX Puts

FX Carry

Data from February 1988-October 2010

Statistics vs Reality: Tail Events Occur More Frequently Than Expected

Actual Tails Are “Fatter” Than Implied by a Normal Distribution

2.0%

on

0.5%

1.0%

1.5%

Cum

ulat

ive

Dis

tribu

tion

Func

tio

“In a normal distribution, a negative tail event should have occurred on about 28 days since 1928. In reality, extreme losses occurred about seven times as often, on 198 days”

Alli B t i Whit P

10

10January 1992–December 2011There can be no assurances fund objectives will be achieved*Copies of “Taking The Sting Out of the Tail: Hedging Against Extreme Events” are available upon requestSource: Bloomberg and AllianceBernstein

0.0%(4.5) (4.0) (3.5) (3.0) (2.5) (2.0)

Standard DeviationUS 10Yr S&P 500 BRL VIX US IG Normal

AllianceBernstein White Paper -Taking The Sting Out of the Tail: Hedging Against Extreme Events: October 2011*

Hedge Fund vs. SPX Monthly Returns

Hedge Fund Return Profiles: Short Volatility, Liquidity and/or Correlation

11

Hedge Fund Universe–HFRX Global Hedge Fund data from 01/98–10/10. Distressed/Restruc.–HFRI Distresssed/Restructuring Index data from 12/94–10/10. Convertible Arb–DJCS Convertible Arbitrage index data from 12/94–10/10. Event Driven–HFRI Event Driven (Total) index data from 12/94–10/10. Equity Hedge–HFRX Equity Hedge Index data from 01/98–10/10. Macro–HFRX Macro Index from 01/96–10/10. Managed Futures–DJCS Managed Futures Index from 12/94–10/10. Selling 25D Puts in S&P–data from 01/96–10/10.

VIX Distribution = Attractive Tail Hedge Profile, But Too Costly

12%

14%

Vix Daily Return Distribution

%

2%

4%

6%

8%

10%

Prob

abili

ty

12

-2%

0%-30% -23% -17% -11% -5% 1% 7% 13% 20% 26% 32% 38% 44% 50% 57% 63%

Daily Return

Data: 1/1997- 12/2010

Traditional Methods of Hedging are Expensive and May Have Marginal Impact

3m Delta 25 Put/Call Strike Moneyness 3mo Cost Annual Cost

Annual Breakeven

S&P 500 Put 1185 ‐7.21% 198bps 792bps ‐15.13%

VIX Call 37.5 39.93% 578bps 2312bps 63.05%Receiver On US 10yr Rates 1.9 27bps 70bps 280bps ‐49bps

CDX IG Payer 160 42bps 27.5bps 110bps 67bps

Brazilian Real Put 2.03 8.80% 161bps 644bps ‐15.24%

13

*Annual breakeven is the movement required (in % or in bps) in the underlying in order for the hedge to breakeven.

As of January 3, 2012

Tail Hedging Process

Seek to be long volatility (and liquidity/correlation)

Long Volatility

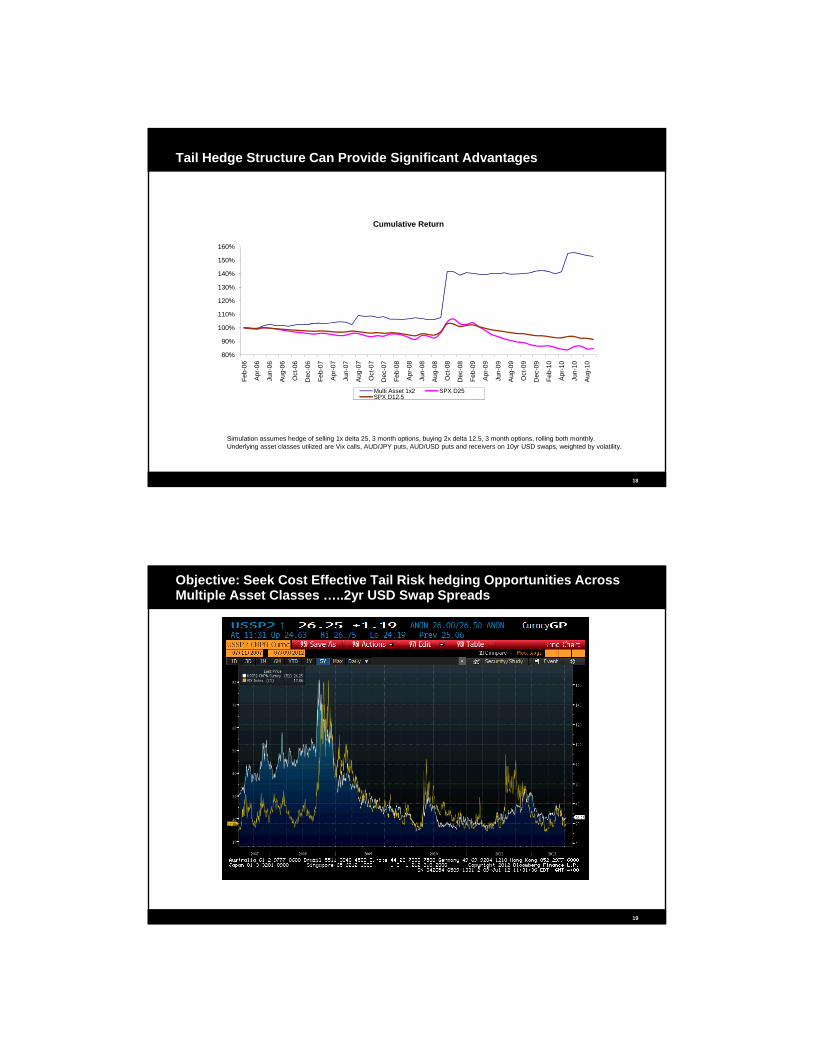

Objective: seek cost-effective tail-risk hedging opportunities across multiple asset classes

Identify the most efficient tail hedges (cost vspayout)

Diversify hedges across asset classes and structures, including indirect or non-traditional hedges that provide long volatility exposure

Interest rates / yield curve

Currencies

C dit

Long Volatility Exposure

Identify Most Efficient Tail

HedgesActively Manage

Tail Hedge Portfolio

14

Credit

Equity

Actively manage the strategy

Diversify Across Asset

Classes

As of July, 2012There can be no assurances fund objectives will be achieved.

Volatility Correlated Across Asset Classes

15

Diverse Range of Hedging Choices

Equities

VolatilityThe market has evolved to allow investors to implement strategies based on market volatility

h ti th VIX i d

Option strategies in global equity markets are just one way to hedge tail risk

Volatility

Rates

Sovereign Relative value opportunities in sovereign credit risk can offer attractive cost-efficient tail hedging

Duration and exposure to ‘risk-free’ assets may serve investors well in periods of market stress. Yield curve strategies (ie curve flatteners) may also help

such as options on the VIX index

16

CurrencyAs one of the most liquid markets in the world, currency strategies can provide effective and efficient tail hedge strategies including ‘anti-carry’ trades

As of August, 2012There can be no assurances fund objectives will be achieved.

CreditCredit and credit derivatives can offer compelling payout profiles in tail hedging. Credit strategies can span CDS to default protection on credit tranches

Objective: Seek Cost Effective Tail Risk hedging Opportunities Across Multiple Asset Classes

40 00%

50.00%

Seeks to provide large payoff in the tail (>3 Std), while minimizing hedge costs in calm/rising markets.

10 00%

0.00%

10.00%

20.00%

30.00%

40.00%

-8.40 -7.80 -7.20 -6.60 -6.00 -5.40 -4.80 -4.20 -3.60 -3.00 -2.40 -1.80 -1.20 -0.60 0.00

0.60

1X2

Pay

Off

At Expiration

Before Expiration

17

-20.00%

-10.00%

Underlying Asset Return

Strike X2 Strike X1

Simulation assumes hedge of selling 1x delta 25, 3 month options, buying 2x delta 12.5, 3 month options, rolling both monthly. Underlying asset classes assumed are Vix calls, AUD/JPY puts, AUD/USD puts and receivers on 10yr USD swaps, weighted by volatility.

Tail Hedge Structure Can Provide Significant Advantages

160%

Cumulative Return

80%

90%

100%

110%

120%

130%

140%

150%

160%06 06 06 06 06 06 07 07 07 07 07 07 08 08 08 08 08 08 09 09 09 09 09 09 10 10 10 10

18

Feb-

0

Apr-

0

Jun-

0

Aug-

0

Oct

-0

Dec

-0

Feb-

0

Apr-

0

Jun-

0

Aug-

0

Oct

-0

Dec

-0

Feb-

0

Apr-

0

Jun-

0

Aug-

0

Oct

-0

Dec

-0

Feb-

0

Apr-

0

Jun-

0

Aug-

0

Oct

-0

Dec

-0

Feb-

1

Apr-

1

Jun-

1

Aug-

1

Multi Asset 1x2 SPX D25SPX D12.5

Simulation assumes hedge of selling 1x delta 25, 3 month options, buying 2x delta 12.5, 3 month options, rolling both monthly. Underlying asset classes utilized are Vix calls, AUD/JPY puts, AUD/USD puts and receivers on 10yr USD swaps, weighted by volatility.

Objective: Seek Cost Effective Tail Risk hedging Opportunities Across Multiple Asset Classes …..2yr USD Swap Spreads

19

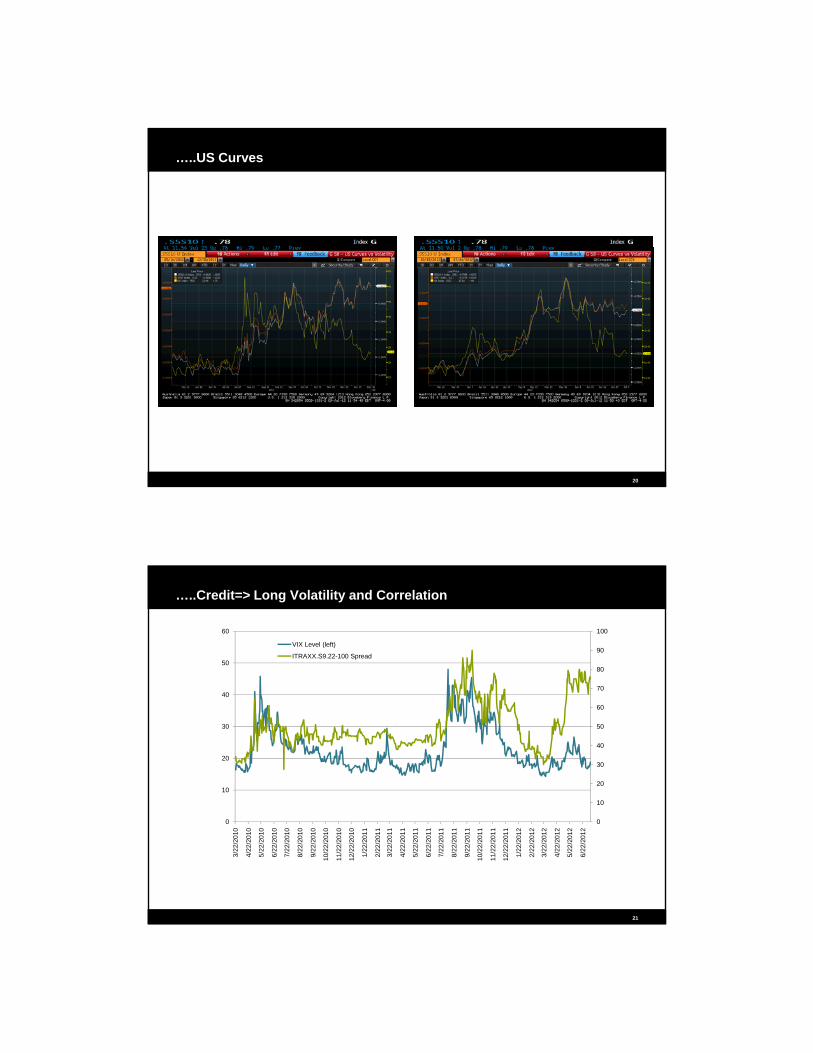

…..US Curves

20

…..Credit=> Long Volatility and Correlation

80

90

100

50

60

VIX Level (left)

ITRAXX.S9.22-100 Spread

10

20

30

40

50

60

70

10

20

30

40

21

0

10

0

3/22

/201

0

4/22

/201

0

5/22

/201

0

6/22

/201

0

7/22

/201

0

8/22

/201

0

9/22

/201

0

10/2

2/20

10

11/2

2/20

10

12/2

2/20

10

1/22

/201

1

2/22

/201

1

3/22

/201

1

4/22

/201

1

5/22

/201

1

6/22

/201

1

7/22

/201

1

8/22

/201

1

9/22

/201

1

10/2

2/20

11

11/2

2/20

11

12/2

2/20

11

1/22

/201

2

2/22

/201

2

3/22

/201

2

4/22

/201

2

5/22

/201

2

6/22

/201

2

…..Brazil, Mexico CDS

22

…..FX =>Short AUD, Long CAD (inverted)

23

Implementation and Challenges

Implementation

InternalResources/expertiseResources/expertise

FundLimited track recordsRange of strategies

Challenges

Basis RiskBasis Risk

Counterparty Risk

24

Summary

Mitigating large drawdowns is critical to investment success

Asset class based allocation/diversification is not sufficient

Innovative tail risk hedging strategies can provide downside protection at reasonable cost

Tail risk hedging should become an integral part of the asset allocation decision

25

Appendix

Presentation Disclosure

This presentation is for informational purposes only and is not intended to be an offer or solicitation, or the basis for any contract to purchase or sell any security or other instrument, or for AllianceBernstein to enter into or arrange any type of transaction as a consequence of any information contained herein. AllianceBernstein and its business units do not provide tax, legal or accounting advice and you should consult your professional advisors with p , g g y y prespect to such matters. This presentation is not intended for public use or distribution. Neither this presentation nor any of its contents may be used for any other purpose without the express consent of AllianceBernstein.

AllianceBernstein utilizes research and data from proprietary, public and private sources. Third party sources include Barclays Capital, Bloomberg, Bridgewater Associates, eVestment, HFRX, JP Morgan Securities, RiskMetrics.

26