tahoe resources bmo global metals & mining conference presentation

TRANSCRIPT

New Leader in Precious Metals

Corporate PresentationJanuary 2016

New Leader in Precious Metals

New Leader in Precious Metals

Safe Harbour DisclaimerCautionary Language on Forward‐Looking InformationThis presentation contains “forward‐looking information” within the meaning of applicable Canadian securities legislation, and “forward‐looking statements” within the meaning of the United States Private Securities Litigation Reform Act of 1995 (collectively referred to as “forward‐looking statements”). All statements, other than statements of historical fact, are forward‐looking statements. The words "believe", "expect", "anticipate", "contemplate", "target", "plan", "intend", "continue", "budget", "estimate", "may", "will", "schedule" and similar expressions or statements identify forward‐looking statements. Forward‐looking statements in this presentation include, but are not limited to, statements and/or information related to: (i) the Company’s 2016 goals, (ii) 2016 outlook related to gold and silver mineral reserves and mineral resources, production, total cash cost per ounce, all‐in sustaining cost per ounce, capital expenditures, corporate general and administration expenses and exploration expenses, (iii) estimated production over the life of the Escobal and La Arena mines, (iv) estimates of royalties and taxes paid in Guatemala and Peru (v) the timing of the anticipated commencement of commercial production at Shahuindo; and (vi) the advancement of exploration projects, including the Sulfide Project at La Arena and the El Alizar Oxide Project adjacent to La Arena (vi) estimated mill and leach pad recoveries, smelter payables and doré and silver concentrate details over the first ten years of mine life. Forward‐looking statements are based on management’s reasonable assumptions, estimates, expectations, analyses and opinions, which are based on management’s experience and perception of trends, current conditions and expected developments, and other factors that management believes are relevant and reasonable in the circumstances, but which may prove to be incorrect. Assumptions have been made regarding, among other things: the Company’s ability to implement operational improvements at the Escobal and La Arena mines; the Company’s ability to carry on exploration and development activities, including construction; the timely receipt of required approvals; the price of silver, gold and other metals; prices for key mining supplies, including labor costs and consumables, remaining consistent with the Company’s current expectations; production meeting expectations and being consistent with estimates; plant, equipment and processes operating as anticipated; there being no material variations in the current tax and regulatory environment; the Company’s ability to operate in a safe, efficient and effective manner; the exchange rates among the Canadian dollar, Guatemalan quetzal, Peruvian nuevo sol and the United States dollar remaining consistent with current levels; and the Company’s ability to obtain financing as and when required and on reasonable terms. Readers are cautioned that the foregoing list is not exhaustive of all factors and assumptions which may have been used. Tahoe’s actual results, programs and financial position could differ materially from those anticipated in such forward‐looking statements as a result of numerous factors, risks and uncertainties, many of which are beyond the Company’s control. These include, but are not necessarily limited to, the Company’s dependence on the Escobal and La Arena mines; the fluctuation of the price of silver, gold and other metals; changes in national and local government legislation, taxation and controls or regulations; social unrest, and political or economic instability in Guatemala and/or Peru; the availability of additional funding as and when required; the speculative nature of mineral exploration and development; the timing and ability to maintain and, where necessary, obtain necessary permits and licenses; the uncertainty in the estimation of mineral resources and mineral reserves; the uncertainty in geologic, hydrological, metallurgical and geotechnical studies and opinions; infrastructure risks, including access to water and power; the impact of inflation; changes in the administration of governmental regulation, policies and practices; environmental risks and hazards; insurance and uninsured risks; land title risks; risks associated with illegal mining activities by unauthorized individuals on the Company’s mining or exploration properties; risks associated with competition; risks associated with currency fluctuations; contractor, labor and employment risks; dependence on key management personnel and executives; the timing and possible outcome of pending or threatened litigation; the risk of unanticipated litigation; risks associated with the repatriation of earnings; risks associated with negative operating cash flow; risks associated with the Company’s hedging policies; risks associated with dilution; and risks associated with effecting service of process and enforcing judgments. For a further discussion of risks relevant to the Company, see the Company’s Annual Information Form available on SEDAR under the heading “Description of Our Business – Risk Factors”. There is no assurance that forward‐looking statements will prove to be accurate. Actual results, performance or achievement could differ materially from those expressed in, or implied by, these forward‐looking statements and, accordingly, no assurance can be given that any of the events anticipated by the forward‐looking statements will transpire or occur, or if any of them do so, what benefits may be derived there from. Accordingly, readers should not place undue reliance on this information. Tahoe does not undertake to update publicly or revise any forward‐looking statements, except as, and to the extent required by, applicable securities laws. For more information about the risks and challenges of Tahoe’s business, investors should review Tahoe’s current Annual Information Form available at www.sedar.com. All prices in U.S. Dollars unless otherwise stated.

Revised February 2016

2

New Leader in Precious Metals

2015 Tahoe Highlights

3

Record production of 20.4 moz silver at Escobal; completed 4500 tpdexpansion on‐time and on‐budget

Record 230,436 ounces gold at La Arena (Tahoe 174,025 oz) Completed Rio Alto merger in Q2 Shahuindo‐Increased reserves from 1 moz to 1.9 moz—Poured first gold and

commissioning commenced in Q4 Repaid $50 million in debt Returned $49.7 million in shareholder dividends Established $150 million revolving credit facility

New Leader in Precious Metals

Tahoe – New Leader in Precious Metals

4

Large-Scale, low-cost production 450,000 oz gold & 20M oz silver per year (700,000 – 750,000 oz gold equivalent) Gold equivalent cash costs <$700/oz, AISC <$900/oz

Large portfolio of growth assets • Growing gold production in Peru and Canada• Attractive exploration targets in all regions

Industry-Leading free cash flow Peer leading free cash flow yield of 5.4% over 2016-2018

Strong balance sheet >$150m of cash, zero net debt

Returning capital to shareholders Strong free cash flow supporting monthly dividend of $0.02 per share per month ($0.24/share/yr.)

New Leader in Precious Metals

Transaction Highlights

5

A premier Americas focused precious metals producer Diversified operating platform with three low‐cost precious metal operations across Guatemala, Peru and Canada Anchored by the Escobal mine, one of the largest and highest grade silver mines globally

Significant low‐cost production and low‐risk growth

All operations generate free cash flow in the current commodity price environment Significant built‐in growth driven by Shahuindo expansion to 36,000 tpd rate and the advancement of a number of growth

initiatives in Timmins, including the ramp up of the 144 Gap deposit Growth in Peru and Canada targeted to increase gold production to >500,000 ounces in 2018

Exciting exploration potential Over 3.4 mozs of M&I gold and 6.0 mozs of inferred gold across eight exploration projects in Peru and Ontario Strong near‐mine potential to add additional gold resources Large unexplored land package across all regions

Superior financial performance and strong balance sheet Zero net debt, modest capital requirements and strong free cash flow generation provide industry‐leading financial strength

and flexibility Tahoe plans to continue monthly dividend policy of $0.02 per share

1. See Tahoe press release dated January 14, 2016; 2. See Lake Shore press release dated January 8, 2016; 3. Using Gold price of $1,175/oz and Silver price of $15.00/oz

2016E Combined Guidance1,2 Gold Silver Gold Equivalent3

Production 370 - 430kozs 18 - 21mozs 600-700kozs

Cash Costs $675 - $725/oz $7.50 - $8.50/oz $640 - $700/oz

All-in Sustaining Costs $950 - $1,000/oz $10.00 - $11.00/oz $885 - $950/oz

New Leader in Precious Metals

Transaction Summary

6

ProposedTransaction

• Business combination with Lake Shore via Plan of Arrangement• Implied equity value of approximately C$945 million1

• Pro forma ownership: 74% Tahoe / 26% Lake Shore1

Consideration

• 0.1467 of a Tahoe common share per Lake Shore common share, representing total consideration of CAD$1.71 per common share1

• 14.8% premium over the closing price of Lake Shore on February 5th and a 28.6% premium to the closing price of Lake Shore on February 4th

• 25.7% premium based on each company’s 20‐day volume weighted average price (“VWAP”)2 to February 5, and 30.4% to February 4

Conditions• Lake Shore shareholder vote (66 2/3% of shareholder votes cast)• Tahoe shareholder vote (majority of shareholder votes cast)• Customary regulatory and court approvals

AnticipatedTiming

• Mailing of meeting materials by early March• Shareholder meetings by early April• Closing expected in April

Other Terms

• Customary non‐solicitation covenants, subject to normal fiduciary outs• Right to match in favor of Tahoe• Break fee of CAD$37.8 million payable to Tahoe; break fee of CAD$20.0 million payable to Lake Shore• Officers and directors of Lake Shore and Tahoe intend to enter into voting support agreements, pursuant to

which they will vote their common shares held in favor of the Transaction• Alan Moon to join Tahoe Board of Directors and Tony Makuch to join Tahoe as President of Canadian

Operations

• 1. At market closing on February 5, 2016. Equity value and pro forma ownership on a fully diluted in the money basis assuming the conversion of in the money convertible debentures• 2. VWAP based on TSX trading only

New Leader in Precious Metals

Diversified Operating Platform in the Americas

7

Note: M&I resources reported inclusive of mineral reserves; See endnotes 1,2,3

La Arena Oxides Shahuindo Oxides2016E Prod. 200-250koz AuCash Costs US$700-$750/ozReserves Au 0.9Moz @ 0.36g/t 1.9Mozs @ 0.53g/tM&I Res. Au 1.2Moz @ 0.32g/t 2.3Mozs @ 0.50g/t

La Arena SulfidesReserves Au 0.6Moz @ 0.31g/tReserves Cu 0.6Blbs @ 0.43%M&I Res. Au 2.1Moz @ 0.24g/tM&I Res. Cu 2.0Blbs @ 0.33%

Shahuindo SulfidesInf. Res. Au 2.0Moz @ 0.71g/tInf. Res. Ag 59Moz @ 21g/t

Timmins West Bell Creek

2016E Prod. 170-180koz Au

Cash Costs <$650/oz

Reserves Au 0.5Moz @ 4.30g/t 0.3Moz @ 4.57g/t

M&I Res. Au 0.7Moz @ 4.76g/t 0.7Moz @ 4.36g/t

Escobal2016E Prod. 18-21Moz Ag

Cash Costs $7.50-$8.50/oz

Reserves Ag 310Moz @ 332g/t

M&I Res. Ag 389Moz @ 332g/t

Other Lake Shore AssetsResources M&I (Moz) Inferred (Moz)

144 Gap Zone 0.3 @ 5.41g/t 0.3 @ 5.19g/tWhitney 0.7 @ 6.85g/t 0.2 @ 5.34g/t

Gold River 0.1 @ 5.29g/t 1.0 @ 6.06g/tJuby 1.1 @ 1.28g/t 2.9 @ 0.94g/tVogel 0.1 @ 1.75g/t 0.2 @ 3.60g/t

Marlhill 0.1 @ 4.52g/t -Fenn-Gib 1.3 @ 0.99g/t 0.8 @ 0.95g/t

Total 3.7 @ 2.77g/t 5.4 @ 2.41g/t

New Leader in Precious Metals

Benefits for LSG shareholders

Premium bid provides immediate value to shareholders

Stronger balance sheet unlocks value from growth opportunities sooner, without dilution or financial risk

Participation in industry-leading dividend

LSG, Tahoe Business Combination AgreementUnlocking Immediate Value

Accelerating Future Value Creation

8

New Leader in Precious Metals

LSG: Quality Operations Driving Financial Strength

0

500

1000

1500

2000

2012 2013 2014 2015

966766

592 580

1,813

1,139872 870

Cash Operating Costs(1)

(1) Non‐GAAP Measure (see Slide 28); (2) All‐in sustaining cost

US$/oz

Low Unit Costs

Solid Production & Sales

0

40,000

80,000

120,000

160,000

200,000

2012 2013 2014 2015

83,800135,600

183,300 183,300Ounces

Gold SalesStrong Growth in Cash

0

50

100

2012 2013 2014 2015

6134

62

100$M

Cash and Bullion

Reduced Debt Levels

0

20

40

60

80

13‐Feb 13‐Dec 2014 2015

6852

70

$M Senior Secured Debt

9

New Leader in Precious Metals

LSG: Three‐Year Outlook

Production 170,000 to 180,000 oz per year

Cash operating costs better than US$650/oz

AISC below US$950/oz

Strong free cash flow (at current prices)

Improved balance sheet

Advance growth opportunities

Significant exploration upside

10

New Leader in Precious Metals

BELL CREEK MINE

BELL CREEK COMPLEX – MILL

Large-scale underground mining complex – two deposits (Timmins Deposit & Thunder Creek Deposit)

2,770 tpd at 4.4 gpt in 2015 509.7k oz reserves (3.7M tonnes at 4.3 gpt) Dec. 2014 M&I resources 695.0 oz (4.5M tonnes at 4.8 gpt(1),

Inferred resources 206.0k oz (1.6M tonnes at 5.0 gpt) at Dec. 2014

Exploration drift from Thunder Creek to 144 Gap

TIMMINS WEST MINE

Underground ramp mining operations 810 tpd at 4.4 gpt in 2015 263.6k oz reserves (1.8M tonnes at 4.6 gpt) Dec. 2014 M&I resources 687.0k oz(4.9M tonnes at 4.4 gpt)(1),

Inferred resources 685.0k oz (4.4M tonnes at 4.8 gpt) Dec. 2014

Significant resource potential at depth

Conventional gold mill circuit, involving crushing and grinding, gravity and leaching, followed by CIL and CIP processes for gold recovery• Recoveries of 96.6% in 2015 (consistently above

95%)

Processed 1,307,200 tonnes (3,580 tpd) at 4.4 gpt in 2015, 4,270 tpd in Dec. 2015

0

50,000

100,000

150,000

2012 2013 2014 2015

64,000

110,000142,200 139,000

Ounces Timmins West Production

0

500,000

1,000,000

1,500,000

2012 2013 2014 2015

719,300952,700

1,245,900 1,307,200

Tonnes Processed

010,00020,00030,00040,00050,000

2012 2013 2014 2015

22,50027,500

43,300 39,700

Ounces Bell Creek Production

LSG: Portfolio of Well‐Built, Low‐Cost AssetsWell Built Infrastructure Supports Low Cost Growth

(1) M&I resources inclusive of reserves

11

New Leader in Precious Metals

LSG: Growth Opportunities Near Existing Infrastructure

First resource released; Development, test stoping to follow

> 1.0M oz inferred resources; Drilling of GR Extension in 2016

144 Gap Zone

Gold River

Whitney

Bell Creek Mill capable of >4000 tpd and expandable to 5500 tpd

BC Deep Completing study for deepening of shaft to access deep resources

Resource confirmation/expansion using open-pit model in 2016

144 SW/N/S Continuing drilling along 144 Trend – focus on 144 South in 2016

12

New Leader in Precious Metals

Timmins West ComplexPotential for Multiple Gold Deposits

13

144 Gap DepositIndicated: 1,734,000 tonnes @ 5.41 gpt (301.7k oz)Inferred: 1,914,000 tonnes @ 5.19 gpt (319.2k oz)

New Leader in Precious Metals

144 Gap Deposit Encouraging New Drill Results

14

1. The 144 Gap resource was estimated using the Inverse Distance to the power 2 (ID2) interpolation method with capping of gold assays evaluated by zone and ranging between 70 and 120 gpt, and anassumed long‐term gold price of US$1,100 per ounce with an average exchange rate of $0.90 $US/$CAD. The cut‐off grade for the base case is 2.6 gpt.

New Leader in Precious Metals

144 Gap DepositEncouraging New Drill Results

15

Confirms existing resultsIntersections in defined resource (but not included in resource estimate)

49.92gpt/22.7m

31.27gpt/18.5m

10.56gpt/7.8m

5.41gpt/36.0m

Highlights potential to expand resource Intersections outside defined resource

6.43gpt/12.5m

5.97gpt/18.8m

8.09gpt/9.9m

New Leader in Precious Metals

Gold RiverNew Exploration Program in 2016

986,000 tonnes @ 9.81 gpt for 310,900 ozs (between 400 and 800 metres)

1,700 m

800 m

Gold River Trend – East Two highly prospective deposits

within 4 kms of Timmins West mine shaft – East and West deposits

Resource contains high-grade core consisting of 310,900 oz at 9.81 gpt

Drilling to date focused on shallow targets in East Deposit

2016 drilling largely focused on Gold River Extension

3D View –Conceptual

16

New Leader in Precious Metals

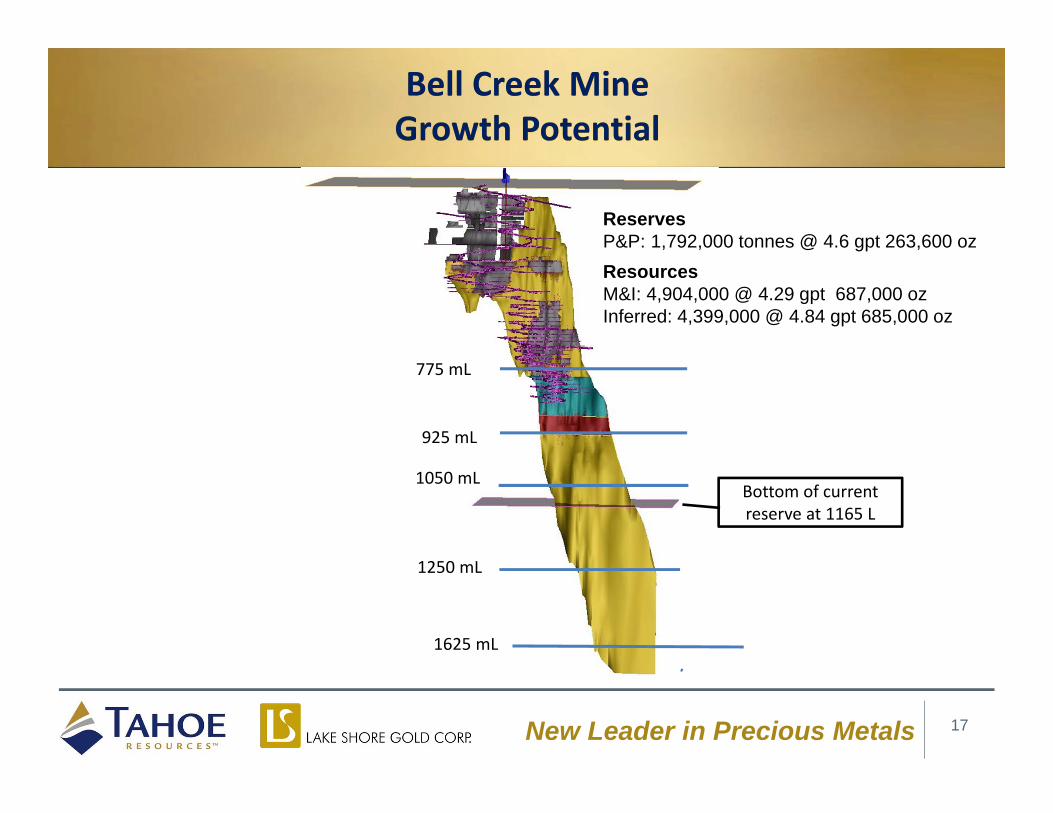

775 mL

925 mL

1250 mL

1050 mL

1625 mL

Reserves P&P: 1,792,000 tonnes @ 4.6 gpt 263,600 oz ResourcesM&I: 4,904,000 @ 4.29 gpt 687,000 ozInferred: 4,399,000 @ 4.84 gpt 685,000 oz

Bottom of current reserve at 1165 L

Bell Creek Mine Growth Potential

17

New Leader in Precious Metals

Bell Creek Mine: Growth Potential

Conceptual shaft extension and

development plan

775 mL

925 mL

1250 mL

1050 mL

1625 mL

Bottom of current reserve at 1165 L

Reserves P&P: 1,792,000 tonnes @ 4.6 gpt 263,600 oz ResourcesM&I: 4,904,000 @ 4.29 gpt 687,000 ozInferred: 4,399,000 @ 4.84 gpt 685,000 oz

18

New Leader in Precious Metals

Temex TransactionWhitney Project: In‐Market Acquisition

Whitney Project JV – Resources(1)(2)

Tonnes Grade* Ounces

Measured 966,000 7.02 218,100

Indicated 2,253,000 6.77 490,500

Total M&I 3,219,000 6.85 708,600

Inferred 995,000 5.34 170,700

* Grams per tonne, at 3.0 gptcut-off

(1) Lake Shore Gold has not verified themineral resources disclosed in the technicalreport for the Whitney Project. To the bestof Lake Shore Gold’s knowledge,information, and belief, there is no newmaterial scientific or technical informationthat would make the disclosure of themineral resources inaccurate ormisleading.

(2) 60% Interest

19

New Leader in Precious Metals

Whitney Project: Open-Pit Potential

20

New Leader in Precious Metals

Timmins West Mine - Canada

21

New Leader in Precious Metals

Bell Creek Complex - Canada

22

New Leader in Precious Metals

Escobal Mine - Guatemala

23

New Leader in Precious Metals

La Arena Mine - Peru

24

New Leader in Precious Metals

Shahuindo Mine - Peru

25

New Leader in Precious Metals

Guatemala Exploration

26

Sept 2015

New Leader in Precious Metals

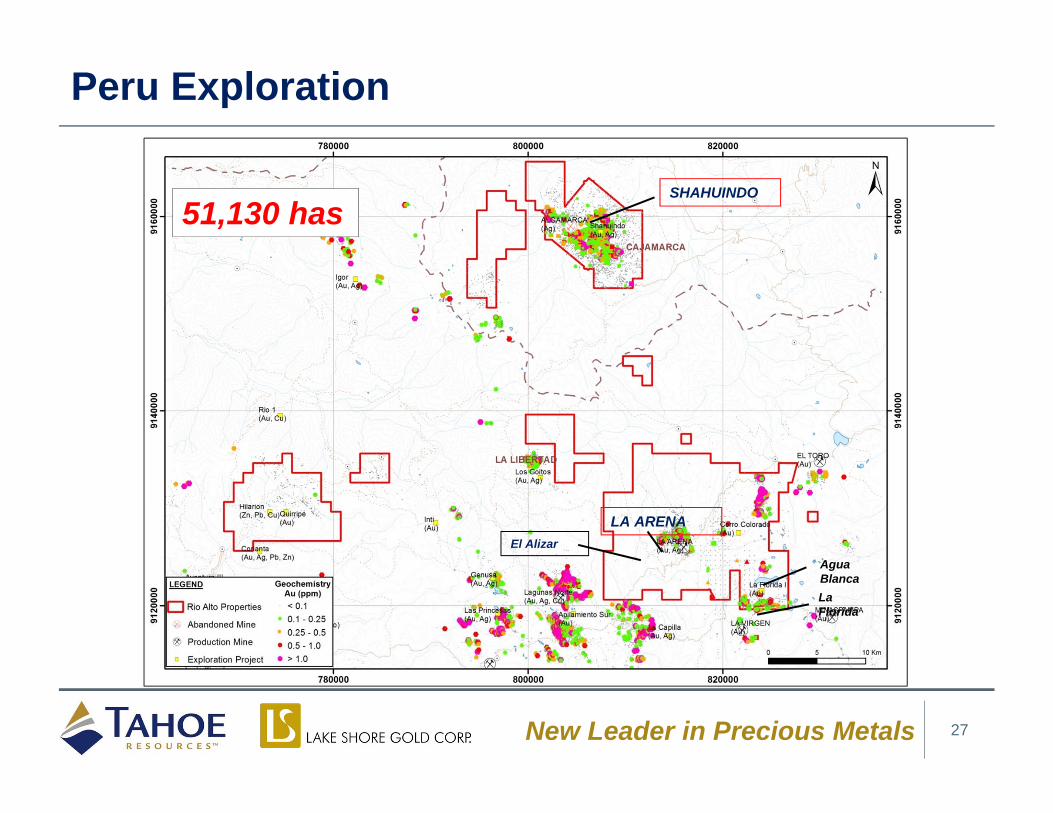

Peru Exploration

27

SHAHUINDO

LA ARENAEl Alizar

La Florida

Agua Blanca

51,130 has

New Leader in Precious Metals

Upside Potential Across All Regions

28

EXPLORATION UPSIDEEl Alizar• Look for potential to

extend La Arena oxide144 Trend• Drilling of SW, North and

South ZonesGold River• >1mozs high-grade U/G

resource near Timmins West mine

Fenn-GibRegional Exploration

IN DEVELOPMENT

La Arena Sulfide• Scoping in 2016 and

Feasibility in 2017

Bell Creek Shaft• Deepen shaft to 1,225m

Whitney• High-grade U/G resource • 5km from Bell Creek mill

PRODUCTION

Escobal• 20mozs Ag / yr

La Arena Oxide• 170kozs Au / yr

Shahuindo Phase 1• 75kozs Au / yr

Timmins/Bell Creek• 175kozs Au / yr

NEAR-TERM EXPANSION

144 Gap• Commencing production

in H2 2016• Implement long-range

development plans

Bell Creek Mill• Expansion to 5500 tpd

for ~$30M by 2017

Shahuindo Phase 2• 36ktpd expansion in

2018 (170 kozs / yr)

New Leader in Precious Metals

Growing Low-Cost Production, Strong Margins

29

Source: Available analyst estimates Note: EBITDA as per Bloomberg consensus estimates

20.4 20.3 20.3

$7.57 $7.10 $7.06

2016E 2017E 2018E

Silv

er P

rodu

ctio

n (M

ozs)

Ag Production - THO Cash Cost (US$/oz Ag)

Stable Prodution

254 283 300

175 175 176

429 458 476

$621 $622 $628

2016E 2017E 2018E

Gol

d Pr

oduc

tion

(koz

s)

Au - THO Au - LSG PF Cash Cost (US$/oz)

StrongGrowth

Potential

0%10%20%30%40%50%60%70%80%90%

100%

2016E 2017E 2018E 2019E 2020E

Tahoe LakeShore

New Leader in Precious Metals

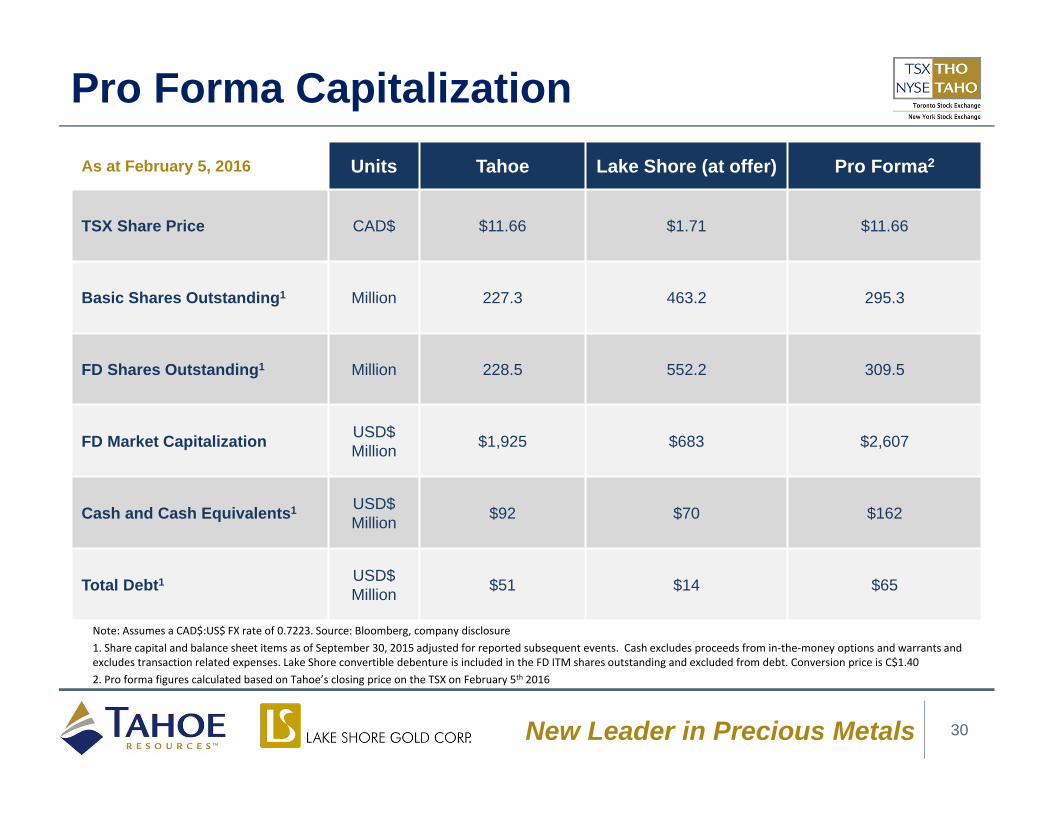

Pro Forma Capitalization

30

Note: Assumes a CAD$:US$ FX rate of 0.7223. Source: Bloomberg, company disclosure1. Share capital and balance sheet items as of September 30, 2015 adjusted for reported subsequent events. Cash excludes proceeds from in‐the‐money options and warrants and excludes transaction related expenses. Lake Shore convertible debenture is included in the FD ITM shares outstanding and excluded from debt. Conversion price is C$1.402. Pro forma figures calculated based on Tahoe’s closing price on the TSX on February 5th 2016

As at February 5, 2016 Units Tahoe Lake Shore (at offer) Pro Forma2

TSX Share Price CAD$ $11.66 $1.71 $11.66

Basic Shares Outstanding1 Million 227.3 463.2 295.3

FD Shares Outstanding1 Million 228.5 552.2 309.5

FD Market Capitalization USD$Million $1,925 $683 $2,607

Cash and Cash Equivalents1 USD$Million $92 $70 $162

Total Debt1 USD$Million $51 $14 $65

New Leader in Precious Metals

Delivering Long-Term Shareholder Value

31

Focused on Growing Free Cash Flow Per Share

MonthlyDividend

Organic Growth

OperationsFocus

Responsible Management

High Margin, Low Cost Operations

Strong Balance

Sheet

Geographic Diversity

New Leader in Precious Metals 32

Endnotes & AppendicesTahoe Resources Investor Relations [email protected]

775.448.5807