tackle 25 - 2019

TRANSCRIPT

Tackle Trading - Tackle 252

Tackle 25

Dividends Fireworks

Poor Boy’s Covered Call

Dirty Sexy Money

Module 1: Meet the Covered Call

Module 2: Call Option Basics

Module 3: The Covered Call Playbook

Module 4: Trade Management › Bulls

Module 5: Trade Management › Sideways

Module 6: Trade Management › Bears

Module 7: Earnings & Collars

The Ultimate Power in the Universe

Rule of 72

Interests for Investors

Covered Calls Compounded

The Search for Better Risk-Adjusted Returns

How to Build a Better Mouse Trap

Covered Calls: Weekly vs. Monthly

Cash Flow Trickery: Part I

Cash Flow Trickery: Part II

3

4

5

6

7

10

13

16

19

21

23

27

28

28

29

31

36

40

42

44

SUMMARY

Tackle Trading - Tackle 253

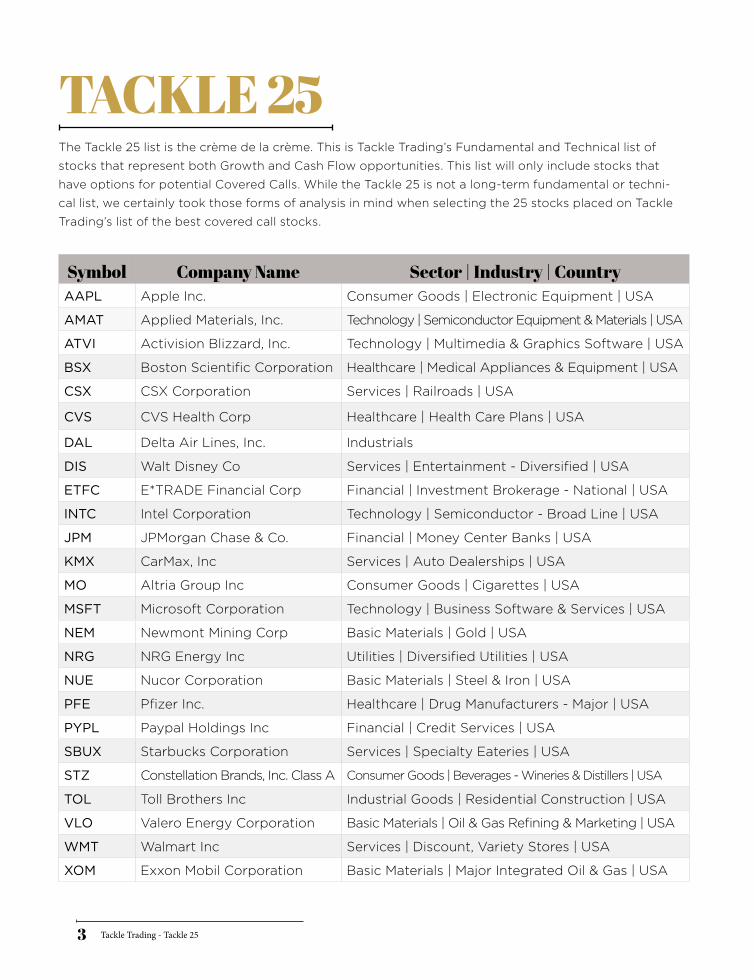

Symbol Company Name Sector | Industry | CountryAAPL Apple Inc. Consumer Goods | Electronic Equipment | USA

AMAT Applied Materials, Inc. Technology | Semiconductor Equipment & Materials | USA

ATVI Activision Blizzard, Inc. Technology | Multimedia & Graphics Software | USA

BSX Boston Scientific Corporation Healthcare | Medical Appliances & Equipment | USA

CSX CSX Corporation Services | Railroads | USA

CVS CVS Health Corp Healthcare | Health Care Plans | USA

DAL Delta Air Lines, Inc. Industrials

DIS Walt Disney Co Services | Entertainment - Diversified | USA

ETFC E*TRADE Financial Corp Financial | Investment Brokerage - National | USA

INTC Intel Corporation Technology | Semiconductor - Broad Line | USA

JPM JPMorgan Chase & Co. Financial | Money Center Banks | USA

KMX CarMax, Inc Services | Auto Dealerships | USA

MO Altria Group Inc Consumer Goods | Cigarettes | USA

MSFT Microsoft Corporation Technology | Business Software & Services | USA

NEM Newmont Mining Corp Basic Materials | Gold | USA

NRG NRG Energy Inc Utilities | Diversified Utilities | USA

NUE Nucor Corporation Basic Materials | Steel & Iron | USA

PFE Pfizer Inc. Healthcare | Drug Manufacturers - Major | USA

PYPL Paypal Holdings Inc Financial | Credit Services | USA

SBUX Starbucks Corporation Services | Specialty Eateries | USA

STZ Constellation Brands, Inc. Class A Consumer Goods | Beverages - Wineries & Distillers | USA

TOL Toll Brothers Inc Industrial Goods | Residential Construction | USA

VLO Valero Energy Corporation Basic Materials | Oil & Gas Refining & Marketing | USA

WMT Walmart Inc Services | Discount, Variety Stores | USA

XOM Exxon Mobil Corporation Basic Materials | Major Integrated Oil & Gas | USA

TACKLE 25The Tackle 25 list is the crème de la crème. This is Tackle Trading’s Fundamental and Technical list of

stocks that represent both Growth and Cash Flow opportunities. This list will only include stocks that

have options for potential Covered Calls. While the Tackle 25 is not a long-term fundamental or techni-

cal list, we certainly took those forms of analysis in mind when selecting the 25 stocks placed on Tackle

Trading’s list of the best covered call stocks.

Tackle Trading - Tackle 254

Symbol Company Name Sector | Industry | Country

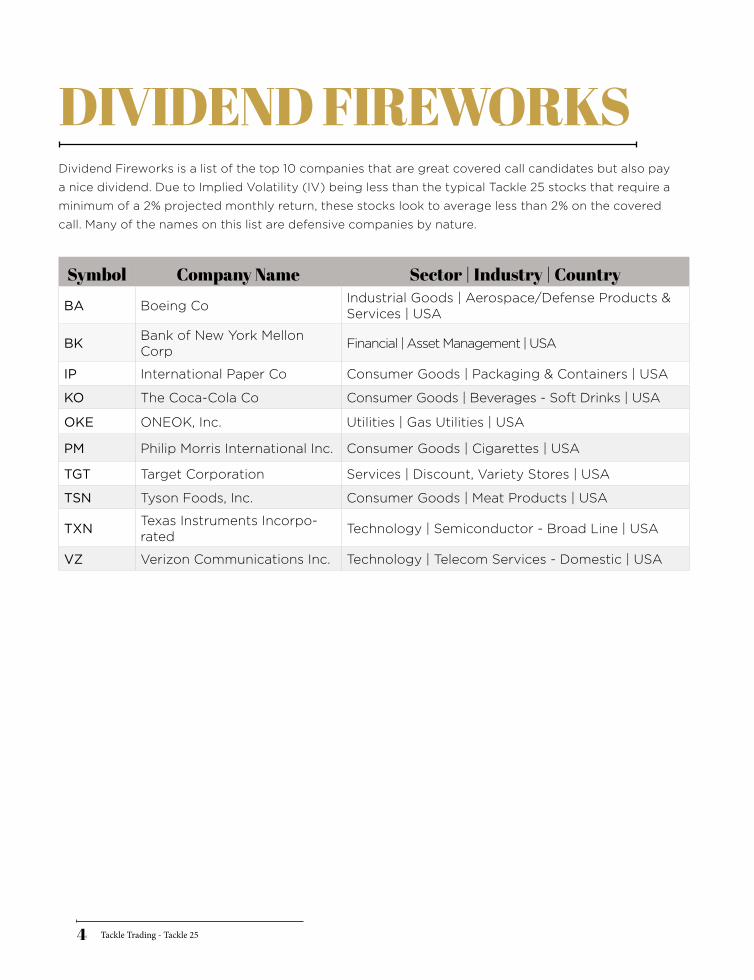

BA Boeing Co Industrial Goods | Aerospace/Defense Products & Services | USA

BK Bank of New York Mellon Corp Financial | Asset Management | USA

IP International Paper Co Consumer Goods | Packaging & Containers | USA

KO The Coca-Cola Co Consumer Goods | Beverages - Soft Drinks | USA

OKE ONEOK, Inc. Utilities | Gas Utilities | USA

PM Philip Morris International Inc. Consumer Goods | Cigarettes | USA

TGT Target Corporation Services | Discount, Variety Stores | USA

TSN Tyson Foods, Inc. Consumer Goods | Meat Products | USA

TXN Texas Instruments Incorpo-rated Technology | Semiconductor - Broad Line | USA

VZ Verizon Communications Inc. Technology | Telecom Services - Domestic | USA

DIVIDEND FIREWORKSDividend Fireworks is a list of the top 10 companies that are great covered call candidates but also pay

a nice dividend. Due to Implied Volatility (IV) being less than the typical Tackle 25 stocks that require a

minimum of a 2% projected monthly return, these stocks look to average less than 2% on the covered

call. Many of the names on this list are defensive companies by nature.

Tackle Trading - Tackle 255

Symbol Company Name Sector | Industry | CountryBABA Alibaba Group Holding Ltd Services | Specialty Retail, Other | China

BIIB Biogen Inc Healthcare | Biotechnology | USA

CRM salesforce.com, inc. Technology | Application Software | USA

GOOGL Alphabet Inc Class A Technology | Internet Information Providers | USA

LRCX Lam Research Corporation Technology | Semiconductor Equipment & Materi-als | USA

MA Mastercard Inc Financial | Credit Services | USA

NFLX Netflix, Inc. Services | CATV Systems | USA

NOC Northrop Grumman Corpo-ration

Industrial Goods | Aerospace/Defense - Major Di-versified | USA

NVDA NVIDIA Corporation Technology | Semiconductor - Specialized | USA

ULTA Ulta Beauty Inc Services | Specialty Retail, Other | USA

POOR BOY’S COVERED CALLThe Poor Boy’s Covered Call is a list of the top ten higher-priced stocks that are great for covered calls

but due to the cost of owning 100 shares can be better used in calendar spreads. The calendar spread

is an option spread established by simultaneously entering a long and short position on the same un-

derlying asset at the same strike price but with different delivery months

Tackle Trading - Tackle 256

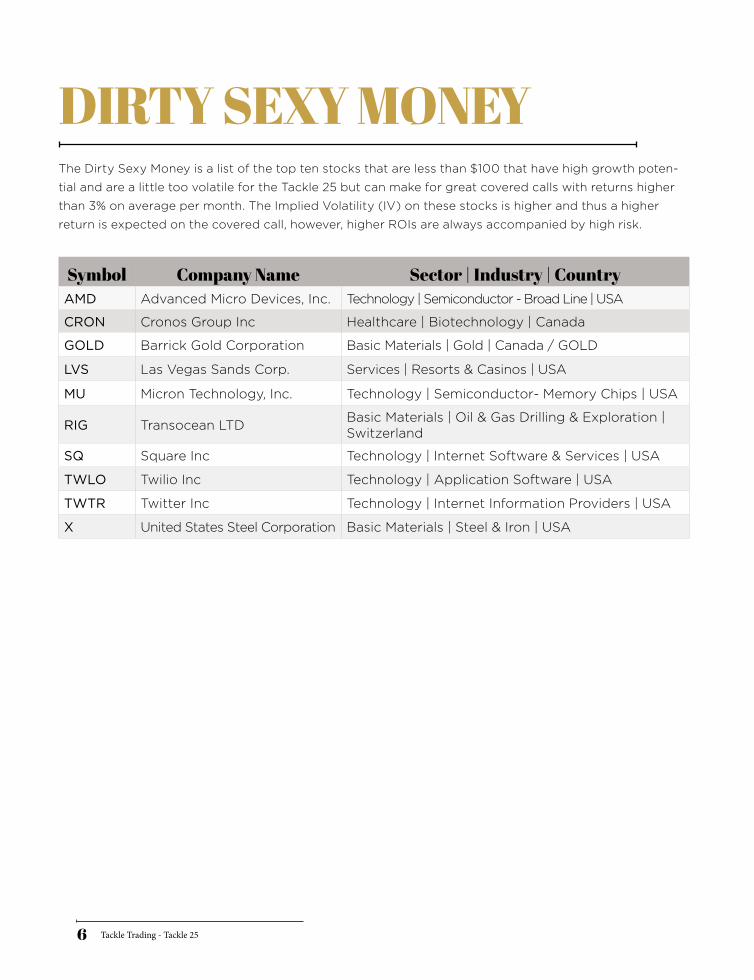

Symbol Company Name Sector | Industry | CountryAMD Advanced Micro Devices, Inc. Technology | Semiconductor - Broad Line | USA

CRON Cronos Group Inc Healthcare | Biotechnology | Canada

GOLD Barrick Gold Corporation Basic Materials | Gold | Canada / GOLD

LVS Las Vegas Sands Corp. Services | Resorts & Casinos | USA

MU Micron Technology, Inc. Technology | Semiconductor- Memory Chips | USA

RIG Transocean LTD Basic Materials | Oil & Gas Drilling & Exploration | Switzerland

SQ Square Inc Technology | Internet Software & Services | USA

TWLO Twilio Inc Technology | Application Software | USA

TWTR Twitter Inc Technology | Internet Information Providers | USA

X United States Steel Corporation Basic Materials | Steel & Iron | USA

DIRTY SEXY MONEYThe Dirty Sexy Money is a list of the top ten stocks that are less than $100 that have high growth poten-

tial and are a little too volatile for the Tackle 25 but can make for great covered calls with returns higher

than 3% on average per month. The Implied Volatility (IV) on these stocks is higher and thus a higher

return is expected on the covered call, however, higher ROIs are always accompanied by high risk.

Tackle Trading - Tackle 257

Meet the Covered Call

• How Stock Investors Profit

• How Real Estate Investors Profit

• How to generate Cash Flow with Covered Calls

Stock Investors (without options)

Stock investors have 2 ways to profit. 1st is price appreciation. This is the buy low, sell high mindset.

If you buy low and sell high you can capture profit through the gains on the stock. 2nd is through

dividend payments. Not all companies pay dividends, but some do, and it’s an extra payment to you

as a shareholder. Many investors look at the dividend as a key factor in the stocks they purchase.

There are 3 caveats, first, to buy low and then sell high for a profit, the stock does in fact has to go

up. Not all companies do rise over time. Even if you do all of your analysis, and make a strong entry,

there will be many times where the stock simply drops over time. Price appreciation is not as pre-

dictable or consistent as we might like as investors.

Dividends are nice and can be considered a bonus to your investment. To maximize profitability

on dividend paying companies, you will need to learn how to cash flow by selling calls and how to

protect downside risk with put options. Dividend payments aren’t enough on their own to make an

investment viable. It’s an incomplete system. That’s where the Covered Calls and Collars come in.

Real Estate Investors

When you buy a property to turn into a rental for income. How does an investor profit? Price appre-

ciation and rental income are the most common ways of doing so, for real estate investors.

Some years, price appreciation in Real Estate can provide fantastic returns. Other years, it doesn’t

beat the rate of inflation. The more predictable factor of the two, for real estate investors, is through

collecting rents from Tenants.

MODULE 1: MEET THE COVERED CALL/01

Tackle Trading - Tackle 258

How lucrative are the returns from rental income? Well, it depends on the circumstance and the

nature of the deal. You can do a simple calculation of the monthly Return on Investment with the

following formula:

Return / Investment = ROI % (Return on Investment)

In our example, the Real Estate investor received a $300 / month net cash flow. The cost to invest in the

property was $40,000 down payment. So, using this simple example, the formula would look like this:

$300 / $40,000 = 0.75% ROI % per month

For investors, this is called your Cash Flow Expectation (CFE). It’s important to measure to help you

identify the strength of any opportunity.

Break-Even Cost

Once you have calculated what your Investment cost and Cash Flow Expectation is, you can identify

how long it will take to pay off your initial investment with profits. In our Real Estate example, if you

make $300 per month, and you had a $40,000 down payment, it would take 133 months to pay off

your down payment with your profit. That’s over 11 years!

Break-Even Cost Formula:

Investment Cost / Cash Flow Expectation (monthly) = Total Months needed to Break-Even

$40,000 / $300 monthly = 133.33 months

Covered Calls Instead

Many Covered Call Investors prefer the strategy over Real Estate. Do they compete? No. You can

do both, and many investors do. But, you should evaluate the opportunities with some of the same

calculations and principles as you do in Real Estate Investing.

Tackle 25 candidates generally will produce 2-4% monthly Cash Flow Expectation (CFE). These

returns can vary from month to month, but the ROI % potential is usually going to be a little higher

when you look at the numbers.

Consider our example from Module 1:

AMD share cost is $19.90. If you buy 1000 shares, you spend $9950 down to control those shares.

This is based on your 50% requirement through standard margin rates. If you receive $100 per

contract when you sell a call option, and can sell 10 contracts against 1000 shares, then your total

premium received is $1000 per month.

$1000 premium / $9950 investment cost = 10% Return on Investment (ROI)

In this example with AMD, the break-even cost would be less than 1 year in time.

Tackle Trading - Tackle 259

Covered Call Philosophy

The Covered Call is the financial markets version of the real estate rental agreement. Whereas in a

rental agreement the Real Estate Investor will find a property to invest in and create monthly cash

flow through renting out the property. The Covered Call is similar in that an investor will find a differ-

ent asset class called a stock and create monthly cash flow through selling call options against the

stock that is owned.

The Covered Call has limited potential reward, positive cash flow expectation, higher downside risk

and these characteristics are very important for any investor to understand to trade Covered Calls

effectively. Throughout these modules, you will learn management techniques and mechanics to

help you build better Covered Calls and manage them wisely.

When you trade Covered Calls, you are simply giving up your rights to your stock in advance, and

by doing that, you receive a credit premium from the market. In other words, you promise to sell

your stock and you Get Paid by doing so.

Trade Management Basics

If you enter a Covered Call, and the stock price rises, you will build a profit on your stock, potentially

lose money on your short call, but you have the highest profit potential from a rise in the underlying

stock price. We’ll discuss more management techniques throughout these sessions, but, for a begin-

ner remember this: upward moving prices give you the potential to make the most net profit from

the strategy.

If the stock stays neutral, you will not gain on the stock through price appreciation, but you will gain

from the Cash Flow received when you sold the call and collected the premium. Sideways is a good

result for a Covered Call Investor, but it’s not as good as up in price.

If the stock drops in price, you will lose money on the stock, and reduce that risk from the call premi-

um that you received. You can lose money trading Covered Calls, particularly if the stocks you buy

drop in price. Managing downside risk is a critical skillset to develop. Modules 6 and 7 will help you

learn techniques to offset this downside risk, when prices drop on the stocks you buy.

Pre-Requisites to good Covered Call Trading

1. Options Trading Permission in your Brokerage Account

2. Enough Capital to buy 100 shares

3. Education to be able to implement and execute the system

Tackle Trading - Tackle 2510

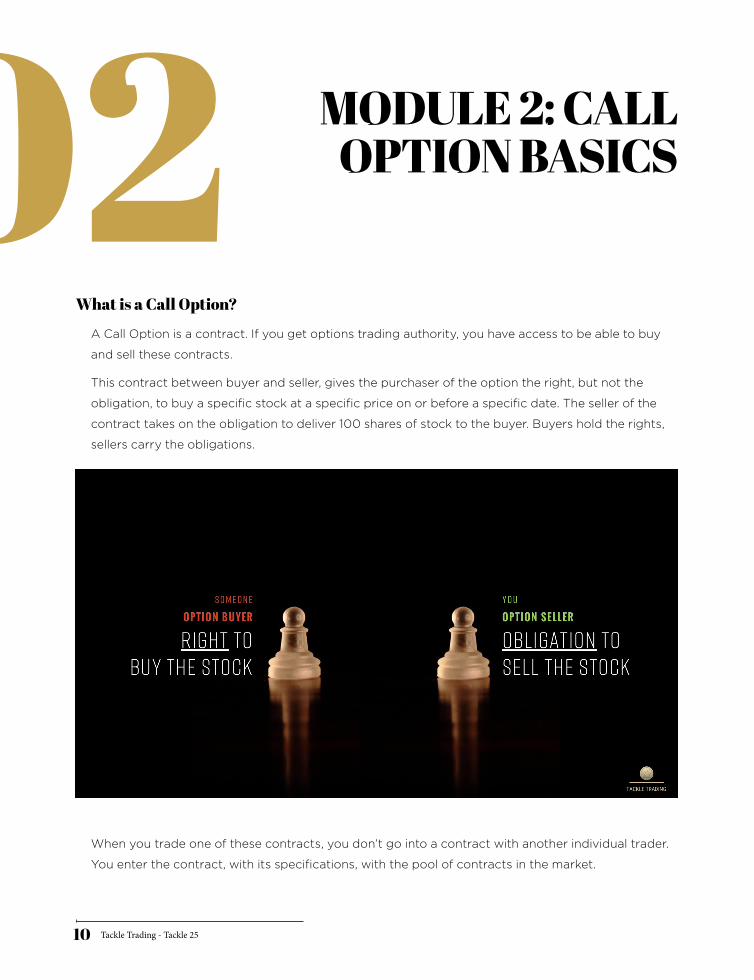

What is a Call Option?

A Call Option is a contract. If you get options trading authority, you have access to be able to buy

and sell these contracts.

This contract between buyer and seller, gives the purchaser of the option the right, but not the

obligation, to buy a specific stock at a specific price on or before a specific date. The seller of the

contract takes on the obligation to deliver 100 shares of stock to the buyer. Buyers hold the rights,

sellers carry the obligations.

When you trade one of these contracts, you don’t go into a contract with another individual trader.

You enter the contract, with its specifications, with the pool of contracts in the market.

MODULE 2: CALL OPTION BASICS/02

Tackle Trading - Tackle 2511

The Terms of the Deal

• Time: 30 Days

• Terms: 0.40 Delta per contract

When you build Covered Calls using the Tackle 25 system, you want to use the options that are

closest to 30 days in time until expiration. To determine your strike price, locate the delta per

contract in the option chain and find the strike closest to .40 delta per contract. Delta can range

between 0.01 to 1.00, so the 0.40 delta will be slightly Out of the Money (OTM) of the current

stock price when you enter the trade.

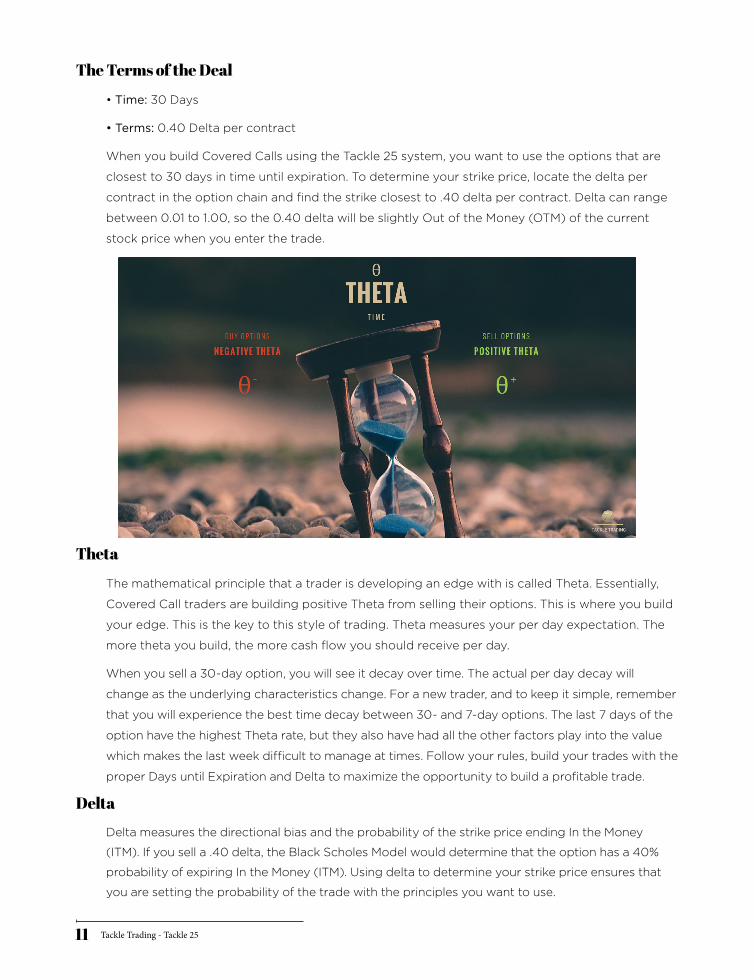

Theta

The mathematical principle that a trader is developing an edge with is called Theta. Essentially,

Covered Call traders are building positive Theta from selling their options. This is where you build

your edge. This is the key to this style of trading. Theta measures your per day expectation. The

more theta you build, the more cash flow you should receive per day.

When you sell a 30-day option, you will see it decay over time. The actual per day decay will

change as the underlying characteristics change. For a new trader, and to keep it simple, remember

that you will experience the best time decay between 30- and 7-day options. The last 7 days of the

option have the highest Theta rate, but they also have had all the other factors play into the value

which makes the last week difficult to manage at times. Follow your rules, build your trades with the

proper Days until Expiration and Delta to maximize the opportunity to build a profitable trade.

Delta

Delta measures the directional bias and the probability of the strike price ending In the Money

(ITM). If you sell a .40 delta, the Black Scholes Model would determine that the option has a 40%

probability of expiring In the Money (ITM). Using delta to determine your strike price ensures that

you are setting the probability of the trade with the principles you want to use.

Tackle Trading - Tackle 2512

Key Terms

• Strike: price at which the buyer has the right to purchase the underlying asset

• Expiration: the last day the contract owner can exercise their rights

• Underlying: The asset upon which the contract is based

• Premium: The cost (or value) of the contract

Covered Call traders sell the contract(s) and carry the obligation to deliver the underlying asset to

the market if the price moves above your strike and becomes an In-the-Money (ITM) option.

Option Pricing

The value of an option is built based on the Black Scholes Model. The basic variables that go into

determining the value of the option include the following:

Using the Black Scholes Model, the Delta, Gamma, Theta, Vega and Rho are all part of deter-

mining the end value of the option. Your job as a trader is to focus on the option value and

make decisions based on the money.

Option Premium is the amount of money that you receive in Cash Flow when you sell the option

in your Covered Call trade. Option premium is built by combining two concepts: Intrinsic and

Extrinsic value. Out of the Money (OTM) options are built entirely with Extrinsic Value. In the

Money (ITM) options have a combination of Intrinsic + Extrinsic value. Learning to calculate how

much of your underlying premium is split between Intrinsic vs. Extrinsic value is an important

skillset when you are managing Covered Calls. This will be discussed more in Module 4.

• Stock Price

• Strike Price

• Time until Expiration

• Volatility of the Underlying Asset

• Interest Rates

• Dividends

Tackle Trading - Tackle 2513

Covered Call Playbook

Building a Covered Call includes buying 100 shares of stock and selling 1 call option. You can sell 1 call

for every 100 shares that you won. The act of selling the call is what makes the position ‘Covered’.

When you trade one of these contracts, you don’t go into a contract with another individual trader.

You enter the contract, with its specifications, with the pool of contracts in the market.

Remember from Module 2, the rules are clear. Your Theta rule is to use an option closest to 30 days

until expiration. Your Delta rule is to use an option closest to 0.40 per contract. Follow these rules to

optimize your Covered Call system.

MODULE 3: THE COVERED

CALL PLAYBOOK/03

Tackle Trading - Tackle 2514

1. Cost Basis = Purchase Price – Call Premium

• $20 - $1 = $19

2. Max Risk = Cost Basis

• Max Risk = $19

3. Max Reward = Strike Price – Cost Basis

• $23 - $19 = $4

4. Downside Protection = Call Premium

• Downside Protection = $1

Formulas

Case Study

• XYZ Stock @ $20

• Sell $23 Call @ $1

Covered Call Benefits

When trading covered calls you gain some advantages as a trader. You receive downside protection

from the premium received from the call sale. When you receive this premium, this gives you a cal-

culable amount of downside protection. Overall, this produces a higher probability of profit, allows

you to generate Cash Flow as a trader and reduces the volatility of your overall equity curve.

Over time, if you continue to sell Calls against your equity position, you as the Covered Call trader,

can continue to reduce your cost basis over time. Given enough time, and assuming other variables

are stable, you can reduce your cost basis lower and eventually get to a Cost Basis of $0 per share.

Many Covered Call traders will target a 1 to 2-year time frame to reduce their cost basis to $0.

Tackle Trading - Tackle 2515

Probability of Profit (POP)

Every trading strategy has an inherent probability built into it. Covered Call traders have a higher

Probability of Profit (POP) over the traditional stock investor. This is due to the collection of the pre-

mium from the call sold. Traditional investing has a built in 50/50 POP. Covered Call traders using

the rules from the Tackle 25 system have an assumed 60/40 POP or 60% POP.

By increasing your overall POP in your trading system, you also should experience a smoother

equity curve over time. Simply put, Covered Call traders can build a better portfolio through these

higher probabilities, which lead to a more consistent return over time. It doesn’t mean more money

each month, but it means a more consistent portfolio if you do it right and the market operates as

it’s intended.

Position Size

The adage “don’t put all of your eggs in one basket” is appropriate in this part of the system. Every

trader has a limited amount of capital. How much will you spend per position as you build your port-

folio? Whatever the % is, it shouldn’t be too much relative to your overall portfolio. The maximum

and aggressive position size would be near 10% of your account per trade. The actual amount must

be determined by you the trader for your portfolio.

Journaling

It’s critical to journal each trade you take. Because a Covered Call involves buying shares and selling

calls, it’s best to separate the entries as individual trades. This is the best approach so that you can

keep an accurate journal for each entry, especially when you roll options and trade more than one

Covered Call on your underling asset over time.

Tackle Trading - Tackle 2516

When to Sell Calls

1. When your Market Bias is Neutral or Bullish

2. When a stock is at Resistance

3. When the Chart is Over-Extended

4. When we are not on Support

5. When indicators like Simple Moving Averages (SMA’s), Bollinger Bands or the Relative Strength

Index (RSI) confirm the entry point for a short call

Remember from Module 2, the rules are clear. Your Theta rule is to use an option closest to 30 days

until expiration. Your Delta rule is to use an option closest to 0.40 per contract. Follow these rules to

optimize your Covered Call system.

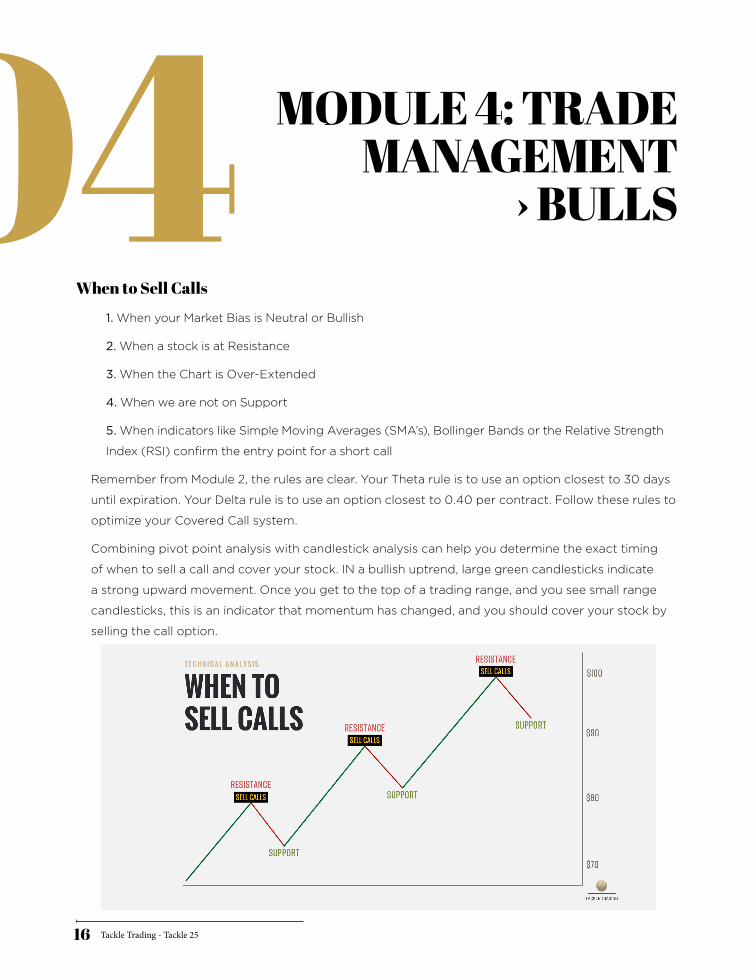

Combining pivot point analysis with candlestick analysis can help you determine the exact timing

of when to sell a call and cover your stock. IN a bullish uptrend, large green candlesticks indicate

a strong upward movement. Once you get to the top of a trading range, and you see small range

candlesticks, this is an indicator that momentum has changed, and you should cover your stock by

selling the call option.

MODULE 4: TRADE MANAGEMENT

› BULLS/04

Tackle Trading - Tackle 2517

Cash Flow Expectation (CFE)

When building Covered Calls, you should calculate this value.

Management Situations

If the call you sell is Out of the Money (OTM), over time, the premium will decay, and you will materi-

alize profit. Once you’ve made 70-80% of the extrinsic value you should buy the call back and roll it

into a new call.

If your original trade starts with a credit of $1.00 premium, then each penny of that credit rep-

resents a part of the total value of the option and trade that you’ve taken. Once the option starts

to drop in value, you will start to materialize the profit in the position. You don’t need to wait until

it’s worth 0.00 to do something with your trade. Using the rules from the Tackle 25 system you

should buy the option back once you’ve made 70-80% of the call premium. In this example, you

would materialize that profit when the option is worth 0.20 or 0.30 cents per contract because

you started it at 1.00 per contract. The value of the option dropping represents profit that you

have materialized from the call sold.

If the call you sell moves In the Money (ITM), you will need to make a management decision at some

point. Do you want to let the market take your stock? Then you can let it run in the money and do

nothing. Do you want to keep the stock and continue to sell calls? If so, you will need to buy the call

back and roll it into a new option.

In our example, if you let the market take your stock at $23 you capture the profit on the entire trade

and maximize your profit. There are times, when you are in this situation you should still buy the call

back and sell the stock manually. This mechanic is used to help avoid the assignment fee and reduce

your overall transaction costs.

(Call Premium / Purchase Price) * 100

• $1 Premium / $20 Per Shar Cost = 5% CFE

Formula

Tackle Trading - Tackle 2518

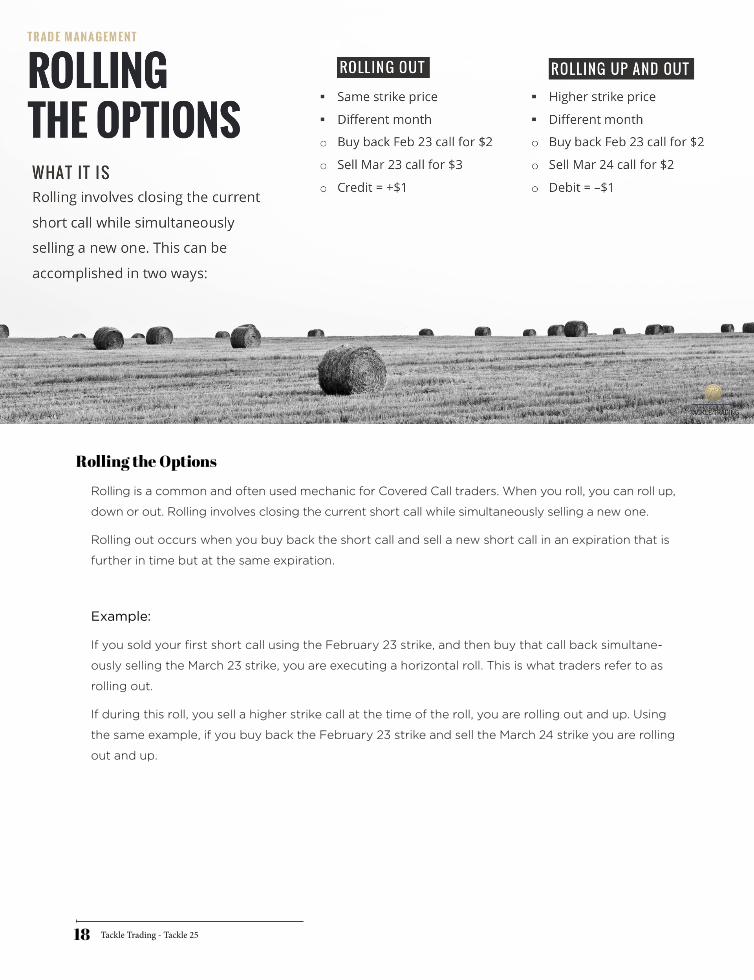

Rolling the Options

Rolling is a common and often used mechanic for Covered Call traders. When you roll, you can roll up,

down or out. Rolling involves closing the current short call while simultaneously selling a new one.

Rolling out occurs when you buy back the short call and sell a new short call in an expiration that is

further in time but at the same expiration.

Example:

If you sold your first short call using the February 23 strike, and then buy that call back simultane-

ously selling the March 23 strike, you are executing a horizontal roll. This is what traders refer to as

rolling out.

If during this roll, you sell a higher strike call at the time of the roll, you are rolling out and up. Using

the same example, if you buy back the February 23 strike and sell the March 24 strike you are rolling

out and up.

Tackle Trading - Tackle 2519

Trade Management: Sideways

When a stock is moving sideways, it will still have days where it moves up and days when it moves

down. At resistance, a trader tries to maximize their profitability when trading Covered Calls by

selling calls. At support, traders buy back their short calls to give them opportunities to gain on the

stock when it moves back up in price.

Near resistance, watch the daily candlesticks closely. Small range candlesticks, in conjunction with

the price being at resistance, gives the trader the cue to go ahead and sell call options to collect

premium. When the stock drops back towards support, watch the candlesticks closely. If they slow

in momentum near support and produce small range candlesticks, go ahead and buy the call back

to open up the profit potential on the call and capture the profit you’ve built in the call.

Management Situations

If the call option stays Out of the Money over time (OTM) the value of the premium will evaporate from

the passage of time and due to theta decay. Once you have materialized 70-80% of your net liquida-

tion in profit, you should buy your short call back and sell a new call. This is when you roll the option.

Traders who watch the extrinsic value of the option can better identify when they should buy the

short call back. Out of the Money (OTM) options are entirely made of extrinsic value. Every penny

in the price is extrinsic, when they are OTM. When that price drops over time, it gives you oppor-

tunities to buy the call back and capture your profit. A common mechanic is to watch the Extrinsic

Value relative to the underlying stock price.

MODULE 5: TRADE MANAGEMENT ›

SIDEWAYS/05

Call Premium / Stock Price = Extrinsic Value

Formula for OTM options:

Tackle Trading - Tackle 2520

Examples:

$20 Stock with 0.40 Call premium = 2% extrinsic value

$20 Stock with 0.30 Call premium = 1.5% extrinsic value

$20 stock with 0.20 Call premium = 1% extrinsic value

$20 stock with 0.10 Call Premium = 0.5% extrinsic value

Because the life cycle of an option will experience time decay at different points, watching the ex-

trinsic value will help you best identify when to buy back your short call and roll it into a new call op-

tion. Essentially, there isn’t much incentive to wait the last 5-10 days until expiration if you’ve already

built most of your profitability from the sale of the short call option. Watch these values to help you

identify when to buy these call options back.

If the sideways trend moves higher and breaks out, you have now moved into a bullish condition.

You should use your rules from Module 4 to manage these situations.

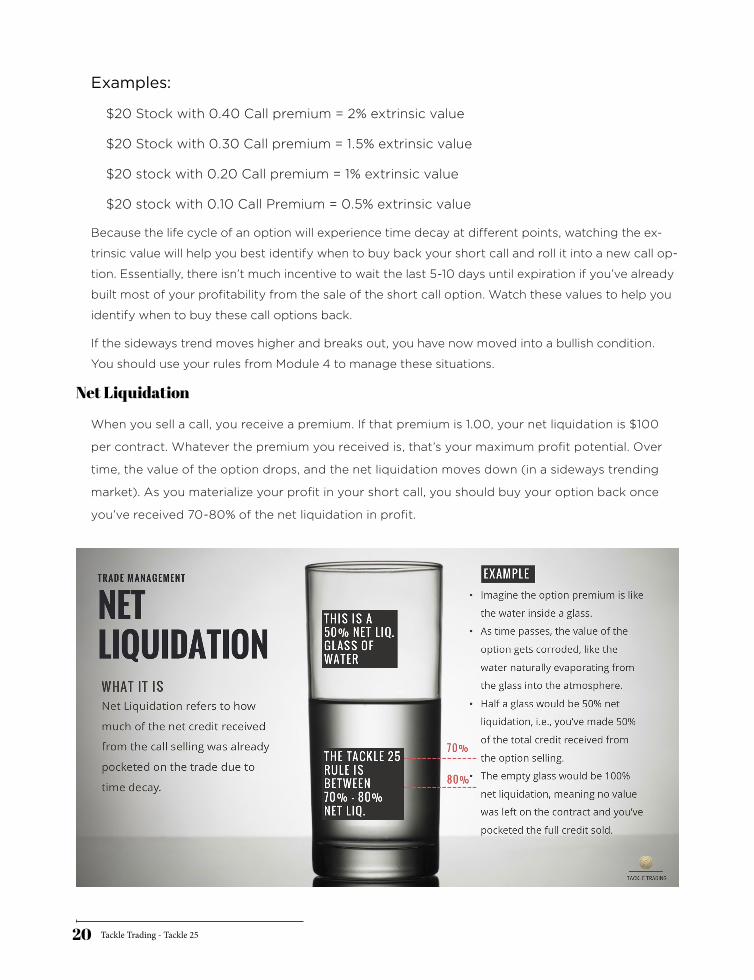

Net Liquidation

When you sell a call, you receive a premium. If that premium is 1.00, your net liquidation is $100

per contract. Whatever the premium you received is, that’s your maximum profit potential. Over

time, the value of the option drops, and the net liquidation moves down (in a sideways trending

market). As you materialize your profit in your short call, you should buy your option back once

you’ve received 70-80% of the net liquidation in profit.

Tackle Trading - Tackle 2521

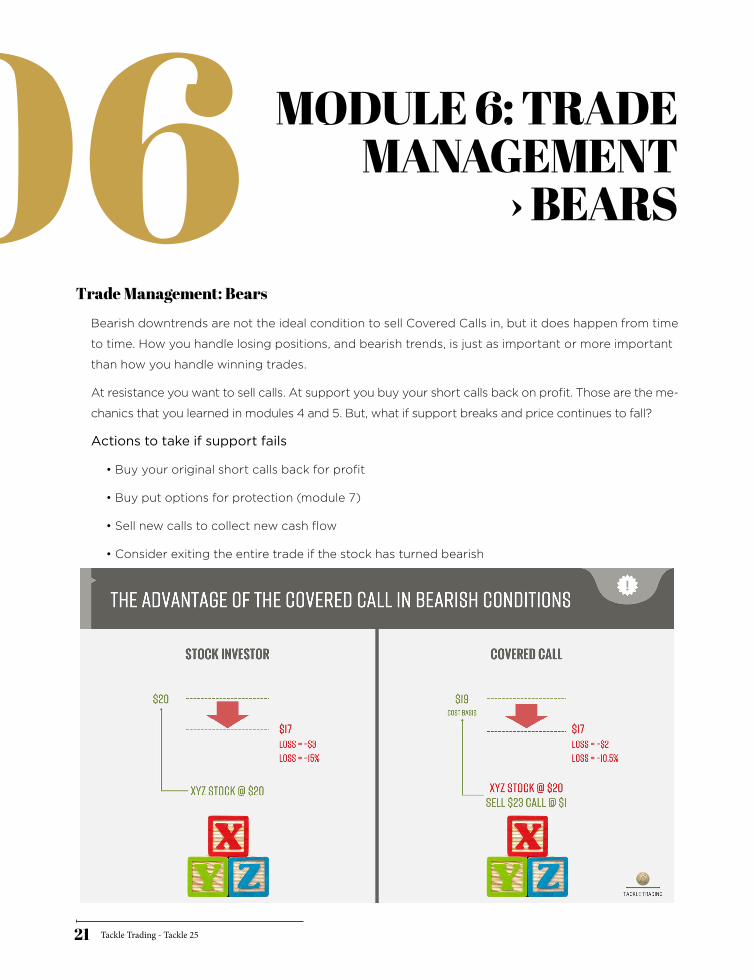

Trade Management: Bears

Bearish downtrends are not the ideal condition to sell Covered Calls in, but it does happen from time

to time. How you handle losing positions, and bearish trends, is just as important or more important

than how you handle winning trades.

At resistance you want to sell calls. At support you buy your short calls back on profit. Those are the me-

chanics that you learned in modules 4 and 5. But, what if support breaks and price continues to fall?

Actions to take if support fails

• Buy your original short calls back for profit

• Buy put options for protection (module 7)

• Sell new calls to collect new cash flow

• Consider exiting the entire trade if the stock has turned bearish

MODULE 6: TRADE MANAGEMENT

› BEARS/06

Tackle Trading - Tackle 2522

Case Study

If you buy the stock for $20 per share and the stock price falls to $17 per share, you will lose money

on the stock. Your loss will be at $3 per share in this circumstance.

Over time, if you buy back your short calls on profit and sell new call options for new premium, you

will have the opportunity to lower your cost basis. By selling call options as prices fall, you will re-

duce your cost basis over time, helping you offset your losses on the stock and reducing your

Consider our original case study. If you buy the stock at $20 per share and sell the $23 strike Febru-

ary call for $1. When the stock goes down, you will need to buy your $23 strike back and then sell a

new call option. That call would likely be in March, and at a lower strike price, like the $21 March Call.

This is defined as a Roll down and out.

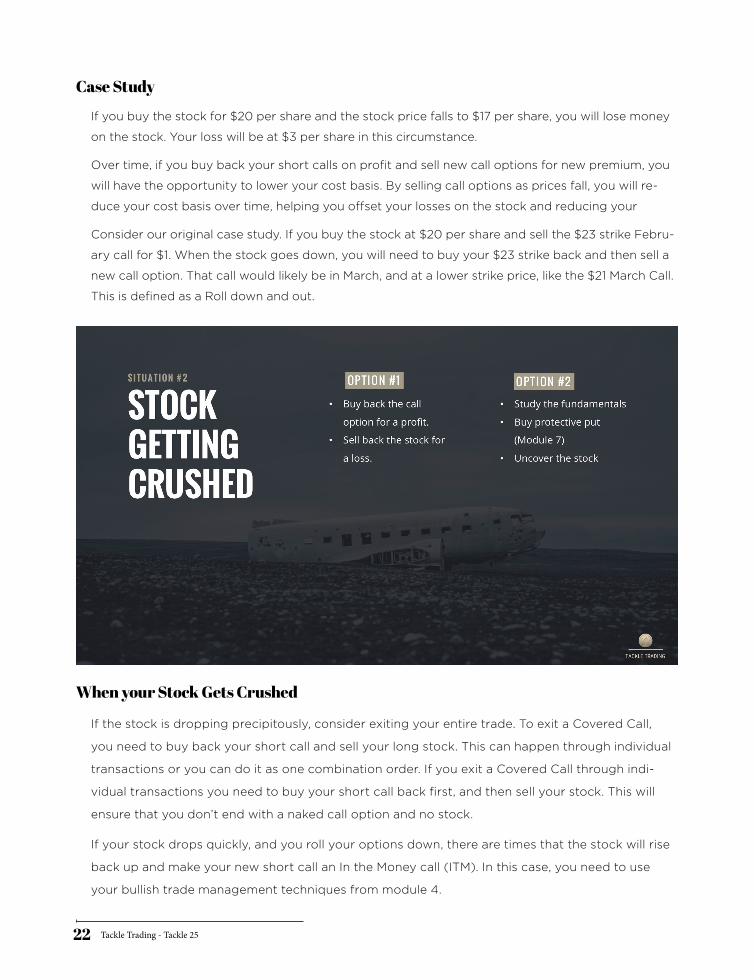

When your Stock Gets Crushed

If the stock is dropping precipitously, consider exiting your entire trade. To exit a Covered Call,

you need to buy back your short call and sell your long stock. This can happen through individual

transactions or you can do it as one combination order. If you exit a Covered Call through indi-

vidual transactions you need to buy your short call back first, and then sell your stock. This will

ensure that you don’t end with a naked call option and no stock.

If your stock drops quickly, and you roll your options down, there are times that the stock will rise

back up and make your new short call an In the Money call (ITM). In this case, you need to use

your bullish trade management techniques from module 4.

Tackle Trading - Tackle 2523

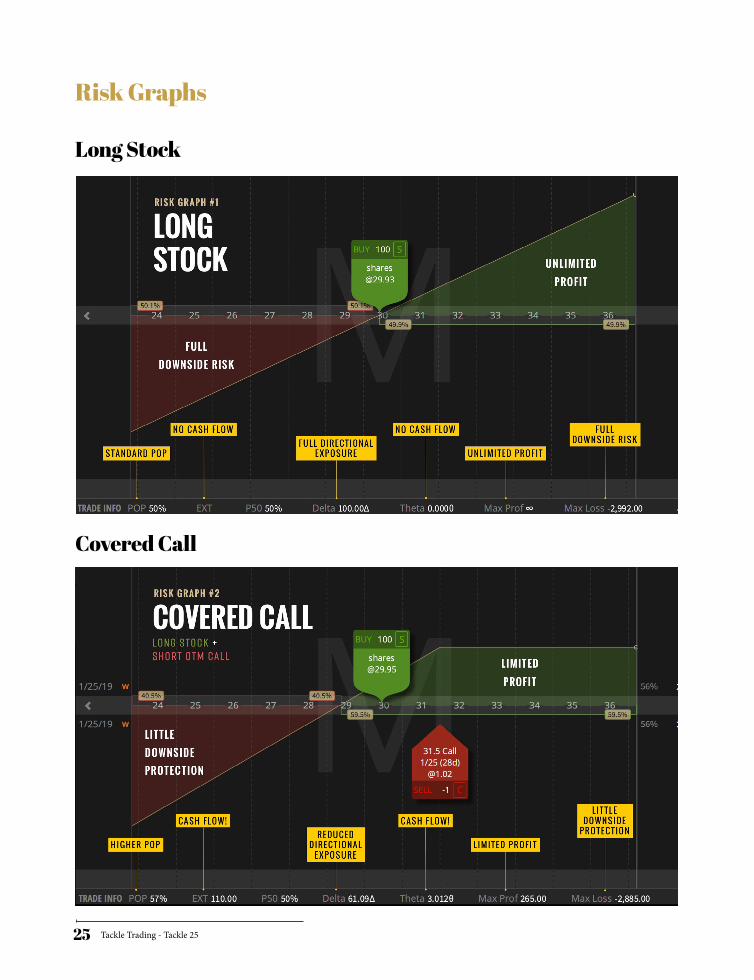

What is a Collar?

A Collar is a protective strategy that is implemented on a long stock position. Traders and investors

create a collar by purchasing an OTM put option while simultaneously selling an Out of the Money

(OTM) call option.

Key Elements

• Long Stock

• OTM Call Option

• OTM Put Option

• Adds downside protection

Characteristics of your Trade

When you start a trade with a long stock position, you have unlimited profit and full downside

risk. Your Probability of Profit is 50%. A long stock position has no cash flow elements, carries full

directional exposure but gives a trader unlimited profit potential while carrying full downside risk.

Adding a short call, turns the trade into a Covered Call. This limits your profit potential, improves

your Probability of Profit (POP) to near 60% and adds a cash flow element through the short call.

We call this a positive Theta position. But you still have higher downside risk in this position.

Adding a put option, and turning your trade into a collar, essentially reduces your downside risk

by adding a floor to your trade. When you do this, the intention is to reduce the risk. If the stock

is behaving as you planned, and staying bullish or neutral, you don’t need to add a collar. When

a trader adds a collar, you instantly reduce your Probability of Profit (POP)

MODULE 7: EARNINGS

& COLLARS/07

Tackle Trading - Tackle 2524

Collar Rules

Pre-Earnings Collar

• Theta Rule: Same expiration as your short call

• Delta Rule: 0.25 to 0.30 Delta per contract

There are essentially two situations where you should consider collaring your trade. First, you

should consider doing it before an earnings release to help you hedge your risk and avoid the

random risk of the earnings gap.

When you are before an earnings report, use the call premium you received to pay for your put

option. The Theta rule you will use is to use the same expiration as the call you have sold. In our

case study, if you are short the February call, you will buy a put in the same expiration of Febru-

ary. The Delta you will use is near 0.25 to 0.30 delta per contract.

Breaking of Support Collar

• Theta Rule: 2 months or more in time

• Delta Rule: .40

If a stock breaks support, you should consider adding a collar. You can do this manually, or you

can create an order before the break happens to protect risk on breakdowns. Using an ad-

vanced order to buy the put, and turn your trade into a collar, gives you a form of a ‘stop loss’ or

risk reduction order to help you control the downside risk.

Mechanics of adding the Collar on Support Breaks

• Identify the Weekly Support zone

• Subtract 1.5 of the Average True Range (ATR) below the support zone and trigger your

collar at this price

• Use a conditional or contingent order to buy this collar on the break of support

Tackle Trading - Tackle 2525

Risk Graphs

Long Stock

Covered Call

Tackle Trading - Tackle 2526

Long Stock

Tackle Trading - Tackle 2527

“This station is now the ultimate power in the universe. I suggest we use it.”

– Admiral Motti

Today we tackle a concept I’ve wanted to dig into

for a while now. It’s extremely powerful. And con-

trary to the late Admiral Motti ’s opinion, it’s not

the Death Star. Perhaps there is no more glowing

endorsement for the topic than that widely att rib-

uted to Albert Einstein, “The most powerful force

in the universe is compound interest.”

During my recent visit on the Trading Justi ce

Podcast my buddy Tim posed an interesti ng

questi on to Matt and me. The gist of it was, “If

you could go back what advice would you share

with your younger self now that you have all this

experience?” Matt and I shared similar thoughts in

regards to co pounding, re-allocati ng gains and

the like. Today I want to elaborate on my answer.

First, what is compound interest? Well, these days

any discussion surrounding interest usually re-

volves around how the Fed killed interest a long

ti me ago with its craft y plan to put the screws

to savers save the universe. Indeed, many of us

look back with fondness to the old days when you

could get 5% or so in the bank. But of course, inter-

est rates are making a comeback (if a 0.25% hike

even qualifi es as a comeback, that is).

Back to compounding. Let’s say interest rates do

eventually normalize to 3% and you have $100k in

the bank that you let sit for ten years. Check out

how the account will grow over time:

Take note, the first year your money grew by

$3,000 but by the last year it grew by $3,915.

That’s 30% more growth. You can thank the mag-

ic of compounding for the accelerati on. As Ben

Franklin once quipped, “The money that money

makes, makes money.” Remember, you didn’t add

any additi onal capital to your account. The sole

reason you made a 30% higher return during the

last year is because you had accumulated some

$30,477 in interest over the prior nine years that

was now earning interest itself. What a beautiful

thing!

Now, I know what you’re thinking. Well, that’s nice

and dandy Tyler but at this pace it will be five years

before Grandma Yellen takes rates anywhere close

to 3%. Tough to get excited about compounding

when rates are pinned near zero.

Well, friends, worry not. I’m just illustrati ng the

concept. We’re going to try to boost the rate of

return using a bit of magic from the double D’s.

I’m talking dividends and derivati ves. More on those in

a second. But fi rst, let’s take a look at the rule of 72.

Year 1: $103,000 / $3000 gainYear 2: $106,090 / $3090 gainYear 3: $109,273 / $3183 gainYear 4: $112,551 / $3278 gainYear 5: $115,927 / $3376 gainYear 6: $119,405 / $3478 gainYear 7: $122,987 / $3582 gainYear 8: $126,677 / $3690 gainYear 9: $130,477 / $3800 gainYear 10: $134,392 / $3915 gain

THE ULTIMATE POWER IN THE UNIVERSE

/01

Tackle Trading - Tackle 2528

One of the popular concepts that inevitably

weaves its way into a discussion on compound-

ing is the rule of 72. It’s a quick way to determine

how long it would take to double your original

principle. Let’s use the previous example where

we have $100K earning 1% per year. To estimate

how long it would take for the $100K to double

to $200K simply take 72 divided by the interest

rate of 1%.

Yep, that’s a whopping 72 years. Hate to break it to

you but you’ll probably be dead by then.

But, hey, your kids will enjoy it. Obviously we

need a higher rate of return to get any kind

of excitement out of this. Let’s say you throw

that $100K in the S&P 500 which conti nues to

produce its historical average of 10%. Well, then

you’ll double your money in 7.2 years. Woo-hoo!

The takeaway: earn a higher return and you’ll dou-

ble your principle faster. Captain Obvious, out.

Hopefully we all know that interest isn’t what

stock investors are gunning for. No, it’s price ap-

preciati on and dividends that deliver the good-

ies. And since dividends are virtually guaranteed

to be paid out for all but the most troubled com-

panies they can be thought of like interest.

If you want to compound the growth of your

money in stocks then don’t squander those divi-

dends. Re-invest them. That is, take the cash and

use it to buy more shares. Then, the next time a

dividend is paid you’ll receive even more. Rinse

and repeat.

Suppose instead of throwing your $100k in the

S&P 500 you purchased a basket of emerging

market stocks. They’re trading at lower valua-

ti ons (as of 2016) due to the commodity bear

market and boast a higher dividend yield. The iS-

hares MSCI Emerging Markets ETF (EEM) will do

the trick. The current dividend yield is just shy of

3%. That means every year you’ll receive around

$3,000 in cash for your investment in EEM.

Here’s another way to look at it. With EEM

trading at $33.25 your $100k would buy about

3,000 shares. The annual dividend payout is

approximately $1 per share. And with the $3,000

in dividends you can purchase another 90 shares

of stock every year (assuming the price remains

around $33.25).

Check out how the compounding will work over

five years:

RULE OF 72/02

INTEREST FOR INVESTORS

/03

Tackle Trading - Tackle 2529

While reinvesting dividends in EEM really starts

to shine a couple years out, just wait ti ll you run

the numbers with covered calls. Let’s say in ad-

diti on to buying the initi al 3000 shares of EEM

and reinvesti ng the $3000 in dividends, you

also sold monthly covered calls and reinvested

the call premiums. That is, take any profi ts from

your covered call selling venture to buy more

shares of EEM. Think of it. Every ti me you score

another 100 shares you can sell one more call

opti on. Let’s make a generous assumpti on and

say we could get about $30 per contract per

month. Since you’re starti ng with 3000 shares

you could sell 30 contracts which translates into

$900 premium per month. Annually that works

out to $10,800 or a 10.8% return on your $100k.

Now look at the compounding:

The further out in ti me we go, the bett er the compounding starts to look. It’s the same principle as

compounding interest, only we’re compounding dividends.

Now, to really supercharge the potenti al we turn to the second “D”, derivatives.

Year 1: $100,000 Principle or 3000 shares of EEM / $3000 paid in dividends.Year 2: $103,000 Principle or 3090 shares of EEM / $3090 paid in dividends.Year 3: $106,090 Principle or 3183 shares of EEM / $3183 paid in dividends.Year 4: $109,273 Principle or 3279 shares of EEM / $3279 paid in dividends.Year 5: $112,552 Principle or 3385 shares of EEM / $3385 paid in dividends.

COVERED CALLS COMPOUNDED

/04

Year 1

Year 2

$100,000 Principle or 3000 shares of EEM / $3000 paid in dividends, $10,800 received in selling 30 cov-

ered calls monthly (for $30 apiece). With the $13,800 received you could buy another 415 shares of EEM

$113,800 Principle or 3415 shares of EEM / $3415 paid in dividends, $12,240 received from selling 34 cov-

ered calls monthly (for $30 apiece). With the $15,565 received you could buy another 470 shares of EEM

Tackle Trading - Tackle 2530

Now that our heads are spinning with numbers

let’s pause to collect our wits. I want to make

sure the key takeaway wasn’t drowned in the

data. The fi rst year you received $3,000 in

dividends and $10,800 in premium from selling

covered calls, or $13,800 total. And remember

you started out owning 3,000 shares.

Because of reinvesting dividends and the call

premiums you were able to buy an additional

2,022 shares over the fi ve years. By the end you

were receiving $5,022 in annual dividends and

$23,022 in call premiums.

That’s accelerati on, baby! That’s compounding.

And the beauti ful thing? You didn’t add another

dime of your own capital. Think the numbers were

too rosy? Fine, cut the gains in half and it sti ll

looks impressive. Though, in my defense the divi-

dends are prett y dang reliable. They quietly flow

into your account come rain or shine. Whether

EEM rallies or falls the dividends keep on coming.

As for the call premiums, it’s a bit too opti misti c

to assume you’ll capture the gains every month.

If EEM rises too far you’ll have to buy back the

calls at a loss. But then again, you’d also have an

unrealized gain in the stock that wasn’t taken into

account in my above case study.

Compounding works in any situati on where

you’re reinvesti ng gains. The power of the dou-

ble D’s is they don’t rely as much on your abil-

ity to forecast a stock’s directi on. It’s really all

about cash fl ow along the way.

Sorry Admiral Motti . Albert was right. Compound-

ing could crush the Death Star any place, any time.

Year 3

Year 4

Year 5

$129,455 Principle or 3885 shares of EEM / $3885 paid in dividends, $13,680 received from selling 38 cov-

ered calls monthly (for $30 apiece). With the $17,538 received you could buy another 528 shares of EEM

$146,993 Principle or 4413 shares of EEM / $4413 paid in dividends, $15,840 received from selling 44 cov-

ered calls monthly (for $30 apiece). With the $20,253 received you could buy another 609 shares of EEM

$167,246 Principle or 5022 shares of EEM / $5022 paid in dividends, $18,000 received from selling

50 covered calls monthly (for $30 apiece). With the $23,022 received you could buy another 692

shares of EEM

Tackle Trading - Tackle 2531

Hang around the halls of the Street long enough

and you’ll be inundated with all sorts of jargon.

One of the most satisfying endeavors in life is to

travel from ignorance to understanding to mas-

tery of a subject. For dollar seeking drones like

us, that topic is trading and understanding the

language of fi nance.

The first time I read the Wall Street Journal I was

a babe in the woods. Sure, I could pronounce the

words, but I was oblivious to the meaning. Now,

I’m a well-oiled writi ng machine with a vocabu-

lary the size of Delaware.

Hyperbole much?

Why, yes, yes indeed.

There’s a particular phrase I suspect you have

come across in your journey, but have yet to

grasp its relevance fully. It’s known as risk-adjust-

ed returns. I wanted to take a deep dive into the

topic for selfi sh purposes. And what bett er way

to learn than to teach it to the masses?

Investors tend to focus on the market’s fi nal desti

nati on. In 2013 the S&P 500 was up 30%, in 2014

the S&P 500 was up 11%, year-to-date it’s up 3%,

so on and so forth. For attentive traders, however

it’s not just the fi nal desti nati on that matt ers but

also the path traveled to get there. Was it a windy

route punctuated by surprising twists and turns?

Or, was it a steady ascent with nary a setback?

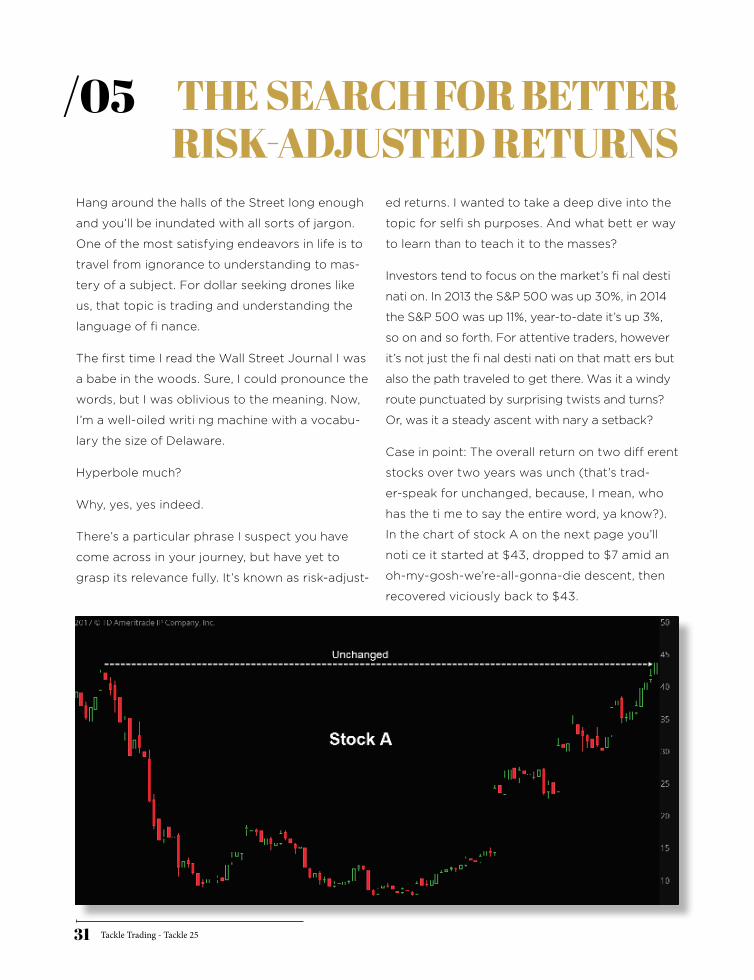

Case in point: The overall return on two diff erent

stocks over two years was unch (that’s trad-

er-speak for unchanged, because, I mean, who

has the ti me to say the entire word, ya know?).

In the chart of stock A on the next page you’ll

noti ce it started at $43, dropped to $7 amid an

oh-my-gosh-we’re-all-gonna-die descent, then

recovered viciously back to $43.

THE SEARCH FOR BETTERRISK-ADJUSTED RETURNS

/05

Tackle Trading - Tackle 2532

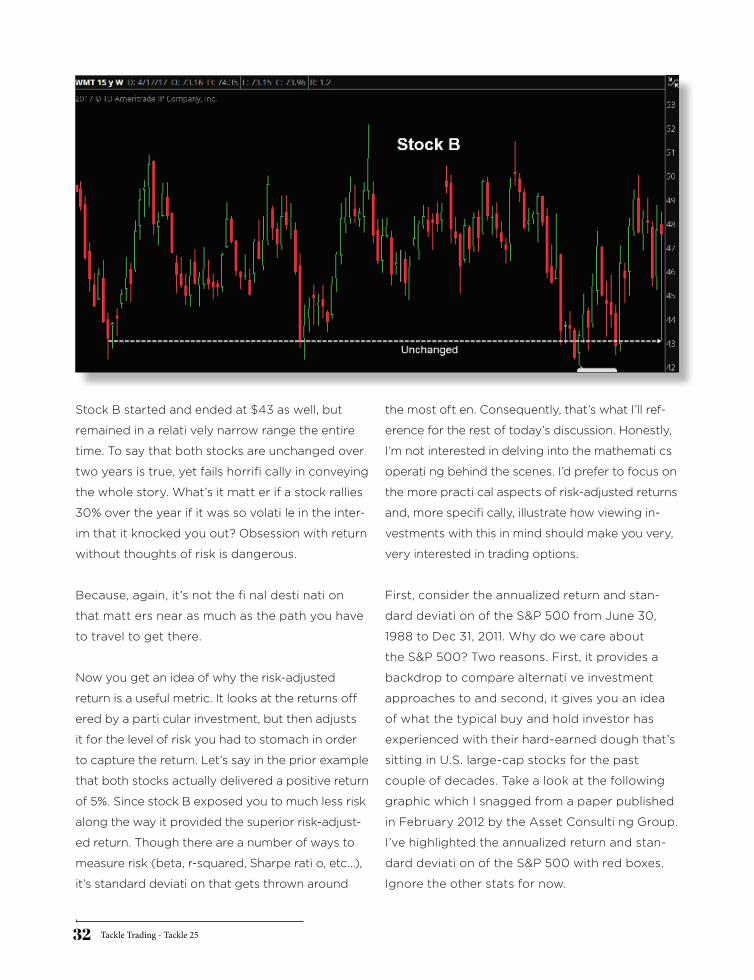

Stock B started and ended at $43 as well, but

remained in a relati vely narrow range the entire

time. To say that both stocks are unchanged over

two years is true, yet fails horrifi cally in conveying

the whole story. What’s it matt er if a stock rallies

30% over the year if it was so volati le in the inter-

im that it knocked you out? Obsession with return

without thoughts of risk is dangerous.

Because, again, it’s not the fi nal desti nati on

that matt ers near as much as the path you have

to travel to get there.

Now you get an idea of why the risk-adjusted

return is a useful metric. It looks at the returns off

ered by a parti cular investment, but then adjusts

it for the level of risk you had to stomach in order

to capture the return. Let’s say in the prior example

that both stocks actually delivered a positive return

of 5%. Since stock B exposed you to much less risk

along the way it provided the superior risk-adjust-

ed return. Though there are a number of ways to

measure risk (beta, r-squared, Sharpe rati o, etc…),

it’s standard deviati on that gets thrown around

the most oft en. Consequently, that’s what I’ll ref-

erence for the rest of today’s discussion. Honestly,

I’m not interested in delving into the mathemati cs

operati ng behind the scenes. I’d prefer to focus on

the more practi cal aspects of risk-adjusted returns

and, more specifi cally, illustrate how viewing in-

vestments with this in mind should make you very,

very interested in trading options.

First, consider the annualized return and stan-

dard deviati on of the S&P 500 from June 30,

1988 to Dec 31, 2011. Why do we care about

the S&P 500? Two reasons. First, it provides a

backdrop to compare alternati ve investment

approaches to and second, it gives you an idea

of what the typical buy and hold investor has

experienced with their hard-earned dough that’s

sitting in U.S. large-cap stocks for the past

couple of decades. Take a look at the following

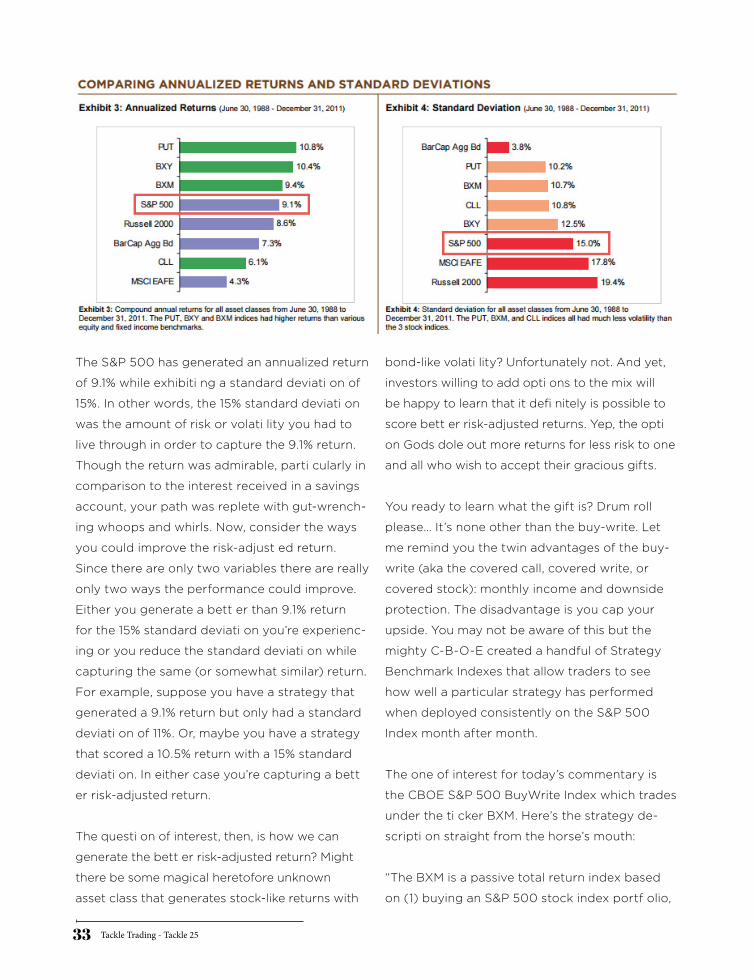

graphic which I snagged from a paper published

in February 2012 by the Asset Consulti ng Group.

I’ve highlighted the annualized return and stan-

dard deviati on of the S&P 500 with red boxes.

Ignore the other stats for now.

Tackle Trading - Tackle 2533

The S&P 500 has generated an annualized return

of 9.1% while exhibiti ng a standard deviati on of

15%. In other words, the 15% standard deviati on

was the amount of risk or volati lity you had to

live through in order to capture the 9.1% return.

Though the return was admirable, parti cularly in

comparison to the interest received in a savings

account, your path was replete with gut-wrench-

ing whoops and whirls. Now, consider the ways

you could improve the risk-adjust ed return.

Since there are only two variables there are really

only two ways the performance could improve.

Either you generate a bett er than 9.1% return

for the 15% standard deviati on you’re experienc-

ing or you reduce the standard deviati on while

capturing the same (or somewhat similar) return.

For example, suppose you have a strategy that

generated a 9.1% return but only had a standard

deviati on of 11%. Or, maybe you have a strategy

that scored a 10.5% return with a 15% standard

deviati on. In either case you’re capturing a bett

er risk-adjusted return.

The questi on of interest, then, is how we can

generate the bett er risk-adjusted return? Might

there be some magical heretofore unknown

asset class that generates stock-like returns with

bond-like volati lity? Unfortunately not. And yet,

investors willing to add opti ons to the mix will

be happy to learn that it defi nitely is possible to

score bett er risk-adjusted returns. Yep, the opti

on Gods dole out more returns for less risk to one

and all who wish to accept their gracious gifts.

You ready to learn what the gift is? Drum roll

please… It’s none other than the buy-write. Let

me remind you the twin advantages of the buy-

write (aka the covered call, covered write, or

covered stock): monthly income and downside

protection. The disadvantage is you cap your

upside. You may not be aware of this but the

mighty C-B-O-E created a handful of Strategy

Benchmark Indexes that allow traders to see

how well a particular strategy has performed

when deployed consistently on the S&P 500

Index month after month.

The one of interest for today’s commentary is

the CBOE S&P 500 BuyWrite Index which trades

under the ti cker BXM. Here’s the strategy de-

scripti on straight from the horse’s mouth:

“The BXM is a passive total return index based

on (1) buying an S&P 500 stock index portf olio,

Tackle Trading - Tackle 2534

and (2) “writing” (or selling) the near-term S&P

500 Index (SPXSM) “covered” call option, gener-

ally on the third Friday of each month. The SPX

call written will have about one month remaining

to expirati on, with an exercise price just above

the prevailing index level (i.e., slightly

out of the money). The SPX call is held unti l ex-

pirati on and cash sett led, at which ti me a new

one-month, near-the-money call is written.”

Let me break that down for you. The Index is buy-

ing the S&P 500 and selling one month slightly

out-of-the-money call opti ons. Then, riding to

expiration and letting the call option settle.

Rinse and repeat. How might you expect BXM has

stacked up versus simply buying and holding the

S&P 500? Your basic understanding of the cov-

ered call should give you some clues. For starters,

it should defi nitely outperform in sideways to

down markets since you’re capturing premium

that buy-and-holders aren’t. On the fl ipside the

BuyWrite Index will underperform in strong up

markets (you cap your upside, remember?). Ad-

diti onally, you probably experience less volati lity

since the premium received from the short call

helps buffer some of the downside each month.

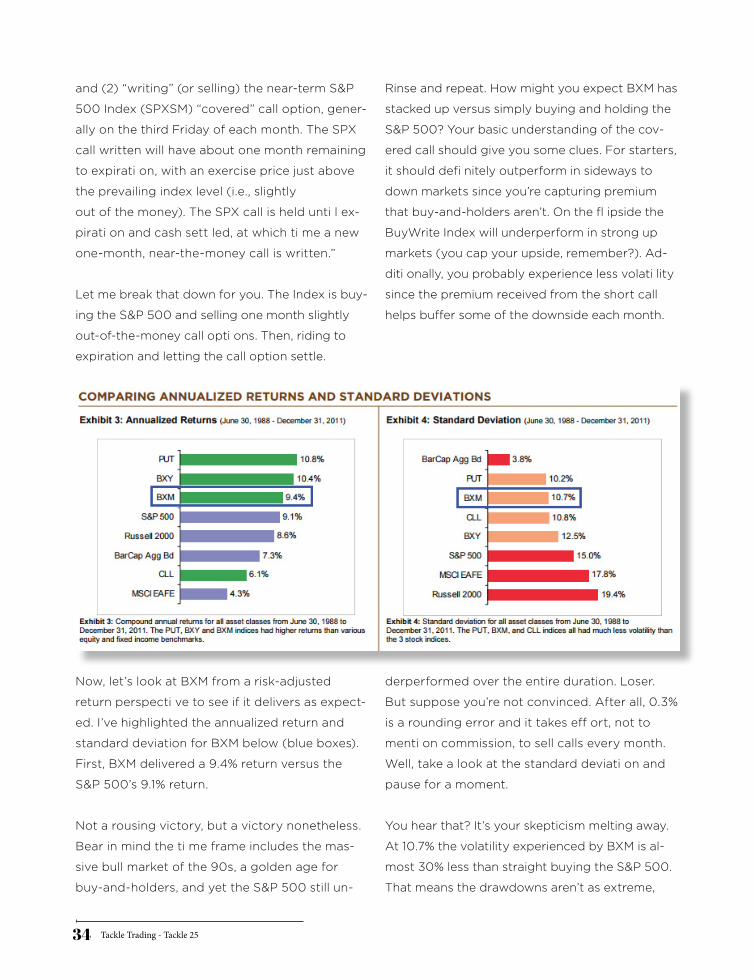

Now, let’s look at BXM from a risk-adjusted

return perspecti ve to see if it delivers as expect-

ed. I’ve highlighted the annualized return and

standard deviation for BXM below (blue boxes).

First, BXM delivered a 9.4% return versus the

S&P 500’s 9.1% return.

Not a rousing victory, but a victory nonetheless.

Bear in mind the ti me frame includes the mas-

sive bull market of the 90s, a golden age for

buy-and-holders, and yet the S&P 500 still un-

derperformed over the entire duration. Loser.

But suppose you’re not convinced. After all, 0.3%

is a rounding error and it takes eff ort, not to

menti on commission, to sell calls every month.

Well, take a look at the standard deviati on and

pause for a moment.

You hear that? It’s your skepticism melting away.

At 10.7% the volatility experienced by BXM is al-

most 30% less than straight buying the S&P 500.

That means the drawdowns aren’t as extreme,

Tackle Trading - Tackle 2535

nor are the short-term rallies in profit as vertical.

And that’s a good thing because you’re one of

those emoti onal humans. And nothing gets your

fear and greed going like massive swings in your

account value. BXM reduces account fluctuations,

which reduces your emotions, which increases the

likelihood that you’ll sti ck with the strategy and

not muck it up with your meddling paws.

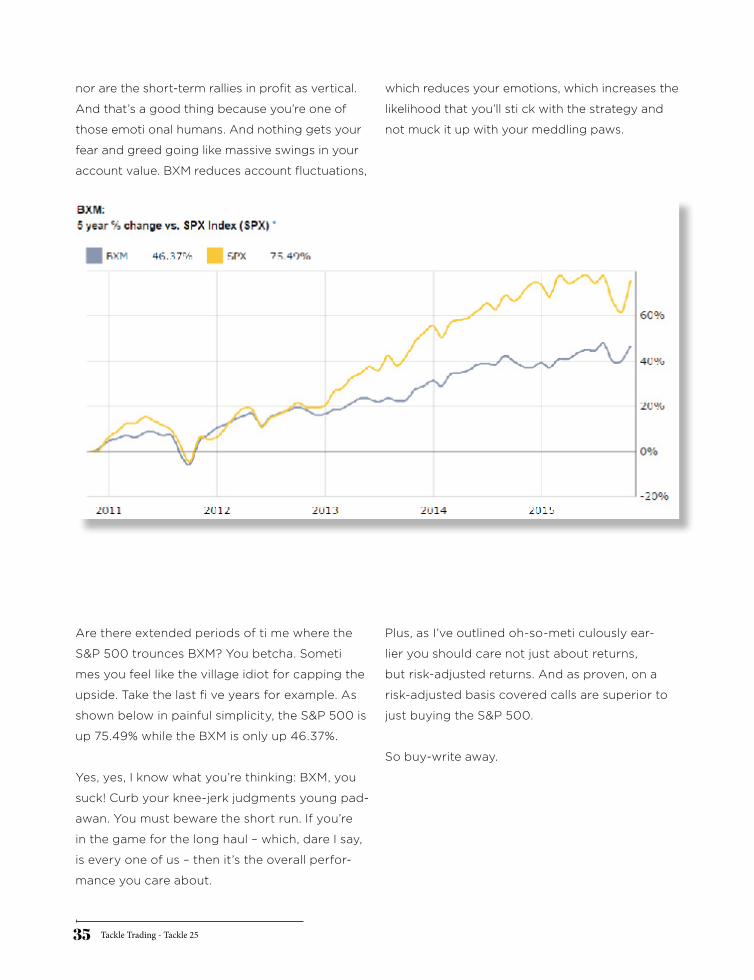

Are there extended periods of ti me where the

S&P 500 trounces BXM? You betcha. Someti

mes you feel like the village idiot for capping the

upside. Take the last fi ve years for example. As

shown below in painful simplicity, the S&P 500 is

up 75.49% while the BXM is only up 46.37%.

Yes, yes, I know what you’re thinking: BXM, you

suck! Curb your knee-jerk judgments young pad-

awan. You must beware the short run. If you’re

in the game for the long haul – which, dare I say,

is every one of us – then it’s the overall perfor-

mance you care about.

Plus, as I’ve outlined oh-so-meti culously ear-

lier you should care not just about returns,

but risk-adjusted returns. And as proven, on a

risk-adjusted basis covered calls are superior to

just buying the S&P 500.

So buy-write away.

Tackle Trading - Tackle 2536

The ti nker temptati on is oft en undeniable for

traders. It’s an itch to squeeze just a wee bit

more alpha out of your strategy that just never

goes away. No matt er your trading approach

the question of, “how can I make it better?” is

always circling that big old brain of yours.

The ultimate objecti ve is to craft a set of rules, a

master plan, which eff ecti vely maximizes gains

while minimizing losses in both turbulent and calm

seas. Even those who have long since optimized

their strategy still feel the tinkering itch beckoning.

Side Note: Alternate ti tles for this arti cle are

“Behold, Covered Call Perfecti on” and “The

Quest for Covered Call Perfection.” I just couldn’t

pass up the picture of the cute little mouse sec-

onds away from getting whacked. Don’t worry

though. All mice go to heaven.

Covered calls have commanded my attention

on and off over the past few months and I’ve

discovered a few tricks to improve the returns

delivered by the income generator.

And what better way to test my comprehension,

not to menti on signal to Karma that I’m a good little

soul willing to share my fi ndings with the masses,

than to divulge the details in all their glory to you?

Remember, the covered call (aka buy-write, cov-

ered write, synthetic short put) consists of buy-

ing 100 shares of stock and selling a call option

to score both income and downside protection.

If you own an ETF like the SPY and are selling

monthly covered calls then the only questi on

you really obsess over is strike price selection.

Selling lower strike calls aff ords more income,

more protection, but less potenti al profi t (you

quickly cut-off your upside in the stock). Selling

higher strike calls, say, 2% OTM, affords less in-

come, less protecti on, but more potenti al profit

since you can parti cipate in more upside in the

stock before having to part with your shares.

HOW TO BUILD ABETTER MOUSE TRAP

/06

Tackle Trading - Tackle 2537

Most traders selling calls on a monthly basis will

choose which approach appeals to them at the

outset and then conti nue to sell the same strike

price month after month. It’s systematic, consistent

and delivers the goodies as promised.

For example, suppose we purchased the Nas-

daq-100 ETF (QQQ) in April 2015 and had been

selling slightly OTM calls every month. As prom-

ised, the covered call has indeed delivered superior

risk-adjusted returns. At the time of this writing,

we’re up 3.8% while those who have simply bought

and held QQQ are down 3.5%.That right there is

what the high falut in traders like to call 730 basis

points of outperformance Alpha achieved!

But what if adopting a more adaptive approach

could yield better results? What if instead of

selling the same strike every month, we modified

the threshold depending on our directional bias?

When more bullish we could sell 2% OTM calls,

when neutral to bearish sell ATM calls.

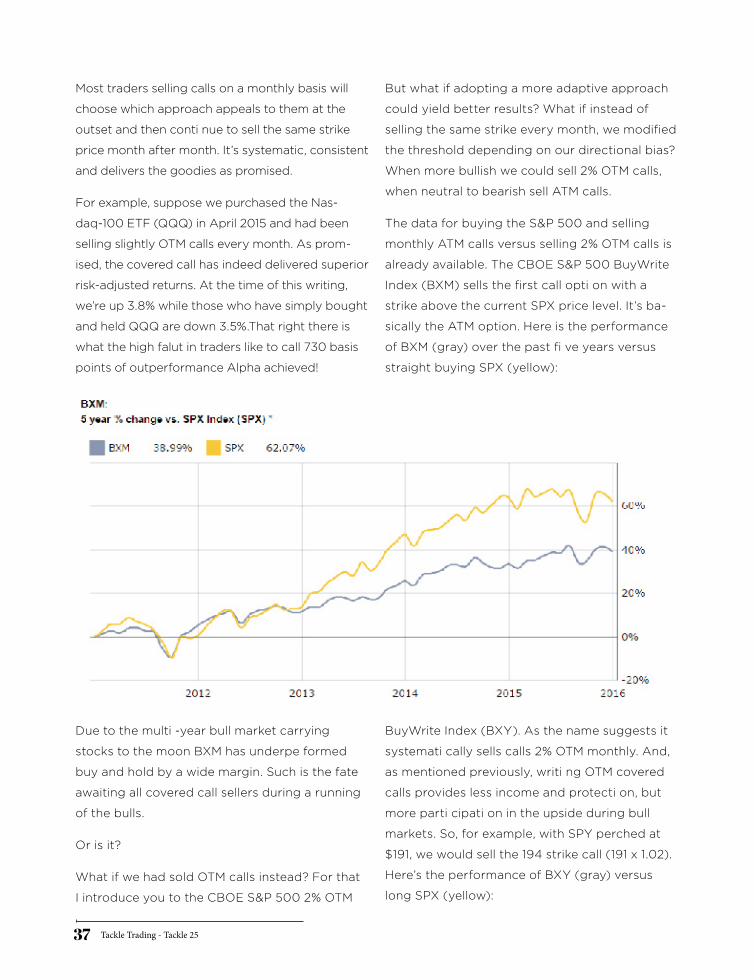

The data for buying the S&P 500 and selling

monthly ATM calls versus selling 2% OTM calls is

already available. The CBOE S&P 500 BuyWrite

Index (BXM) sells the first call opti on with a

strike above the current SPX price level. It’s ba-

sically the ATM option. Here is the performance

of BXM (gray) over the past fi ve years versus

straight buying SPX (yellow):

Due to the multi -year bull market carrying

stocks to the moon BXM has underpe formed

buy and hold by a wide margin. Such is the fate

awaiting all covered call sellers during a running

of the bulls.

Or is it?

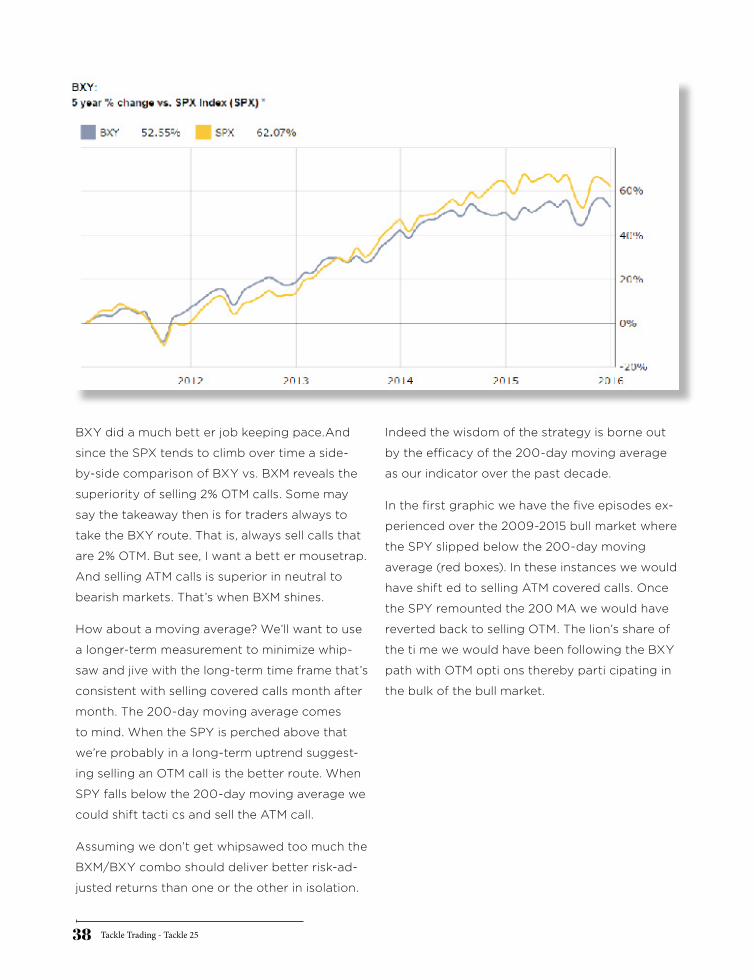

What if we had sold OTM calls instead? For that

I introduce you to the CBOE S&P 500 2% OTM

BuyWrite Index (BXY). As the name suggests it

systemati cally sells calls 2% OTM monthly. And,

as mentioned previously, writi ng OTM covered

calls provides less income and protecti on, but

more parti cipati on in the upside during bull

markets. So, for example, with SPY perched at

$191, we would sell the 194 strike call (191 x 1.02).

Here’s the performance of BXY (gray) versus

long SPX (yellow):

Tackle Trading - Tackle 2538

BXY did a much bett er job keeping pace.And

since the SPX tends to climb over time a side-

by-side comparison of BXY vs. BXM reveals the

superiority of selling 2% OTM calls. Some may

say the takeaway then is for traders always to

take the BXY route. That is, always sell calls that

are 2% OTM. But see, I want a bett er mousetrap.

And selling ATM calls is superior in neutral to

bearish markets. That’s when BXM shines.

How about a moving average? We’ll want to use

a longer-term measurement to minimize whip-

saw and jive with the long-term time frame that’s

consistent with selling covered calls month after

month. The 200-day moving average comes

to mind. When the SPY is perched above that

we’re probably in a long-term uptrend suggest-

ing selling an OTM call is the better route. When

SPY falls below the 200-day moving average we

could shift tacti cs and sell the ATM call.

Assuming we don’t get whipsawed too much the

BXM/BXY combo should deliver better risk-ad-

justed returns than one or the other in isolation.

Indeed the wisdom of the strategy is borne out

by the efficacy of the 200-day moving average

as our indicator over the past decade.

In the first graphic we have the five episodes ex-

perienced over the 2009-2015 bull market where

the SPY slipped below the 200-day moving

average (red boxes). In these instances we would

have shift ed to selling ATM covered calls. Once

the SPY remounted the 200 MA we would have

reverted back to selling OTM. The lion’s share of

the ti me we would have been following the BXY

path with OTM opti ons thereby parti cipating in

the bulk of the bull market.

Tackle Trading - Tackle 2539

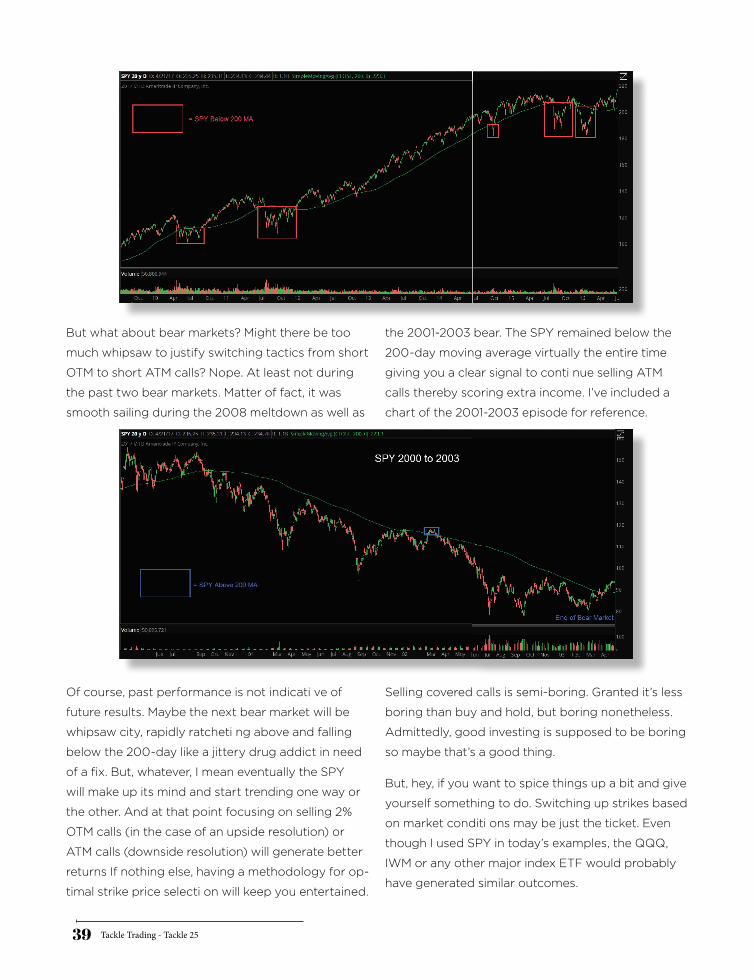

But what about bear markets? Might there be too

much whipsaw to justify switching tactics from short

OTM to short ATM calls? Nope. At least not during

the past two bear markets. Matter of fact, it was

smooth sailing during the 2008 meltdown as well as

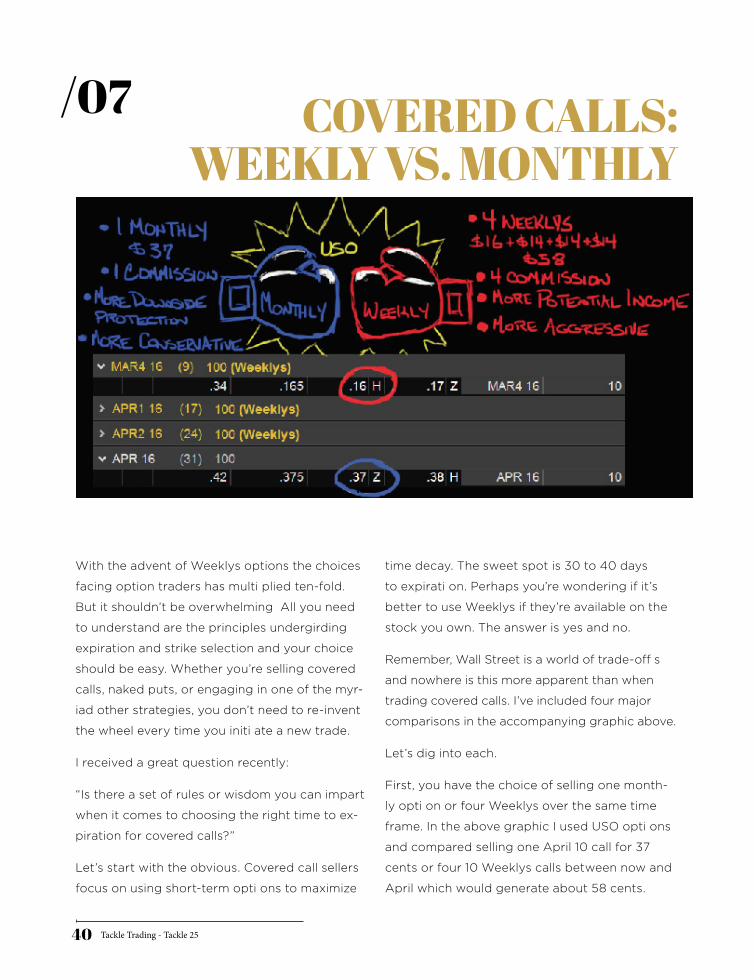

the 2001-2003 bear. The SPY remained below the

200-day moving average virtually the entire time

giving you a clear signal to conti nue selling ATM

calls thereby scoring extra income. I’ve included a

chart of the 2001-2003 episode for reference.

Of course, past performance is not indicati ve of

future results. Maybe the next bear market will be

whipsaw city, rapidly ratcheti ng above and falling

below the 200-day like a jittery drug addict in need

of a fix. But, whatever, I mean eventually the SPY

will make up its mind and start trending one way or

the other. And at that point focusing on selling 2%

OTM calls (in the case of an upside resolution) or

ATM calls (downside resolution) will generate better

returns If nothing else, having a methodology for op-

timal strike price selecti on will keep you entertained.

Selling covered calls is semi-boring. Granted it’s less

boring than buy and hold, but boring nonetheless.

Admittedly, good investing is supposed to be boring

so maybe that’s a good thing.

But, hey, if you want to spice things up a bit and give

yourself something to do. Switching up strikes based

on market conditi ons may be just the ticket. Even

though I used SPY in today’s examples, the QQQ,

IWM or any other major index ETF would probably

have generated similar outcomes.

Tackle Trading - Tackle 2540

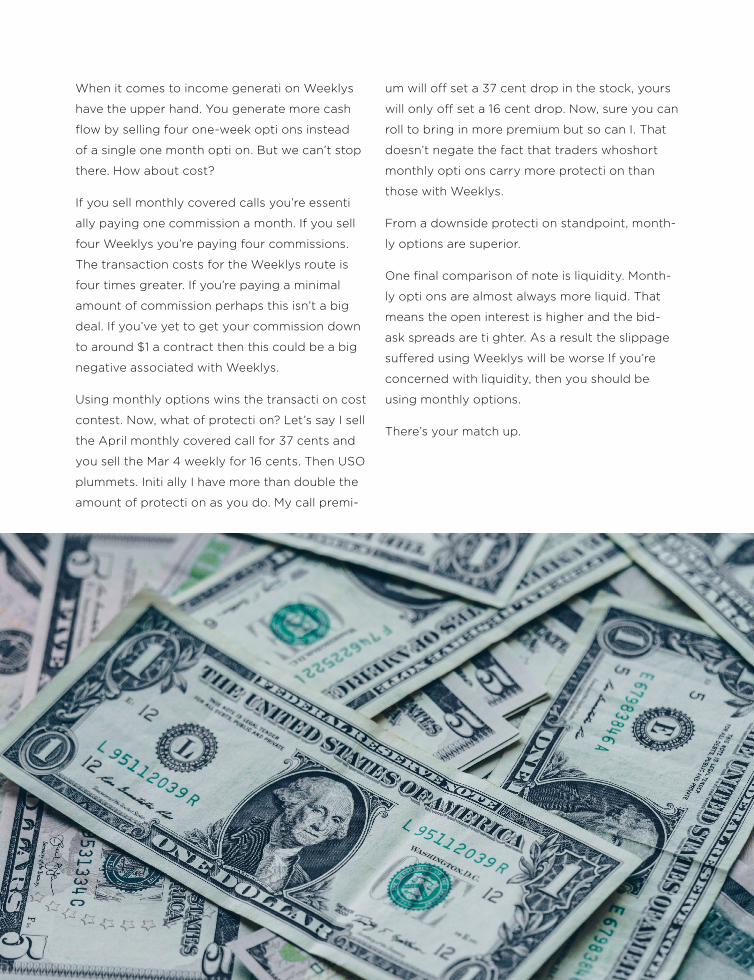

With the advent of Weeklys options the choices

facing option traders has multi plied ten-fold.

But it shouldn’t be overwhelming All you need

to understand are the principles undergirding

expiration and strike selection and your choice

should be easy. Whether you’re selling covered

calls, naked puts, or engaging in one of the myr-

iad other strategies, you don’t need to re-invent

the wheel every time you initi ate a new trade.

I received a great question recently:

“Is there a set of rules or wisdom you can impart

when it comes to choosing the right time to ex-

piration for covered calls?”

Let’s start with the obvious. Covered call sellers

focus on using short-term opti ons to maximize

time decay. The sweet spot is 30 to 40 days

to expirati on. Perhaps you’re wondering if it’s

better to use Weeklys if they’re available on the

stock you own. The answer is yes and no.

Remember, Wall Street is a world of trade-off s

and nowhere is this more apparent than when

trading covered calls. I’ve included four major

comparisons in the accompanying graphic above.

Let’s dig into each.

First, you have the choice of selling one month-

ly opti on or four Weeklys over the same time

frame. In the above graphic I used USO opti ons

and compared selling one April 10 call for 37

cents or four 10 Weeklys calls between now and

April which would generate about 58 cents.

COVERED CALLS:WEEKLY VS. MONTHLY

/07

Tackle Trading - Tackle 2541

When it comes to income generati on Weeklys

have the upper hand. You generate more cash

flow by selling four one-week opti ons instead

of a single one month opti on. But we can’t stop

there. How about cost?

If you sell monthly covered calls you’re essenti

ally paying one commission a month. If you sell

four Weeklys you’re paying four commissions.

The transaction costs for the Weeklys route is

four times greater. If you’re paying a minimal

amount of commission perhaps this isn’t a big

deal. If you’ve yet to get your commission down

to around $1 a contract then this could be a big

negative associated with Weeklys.

Using monthly options wins the transacti on cost

contest. Now, what of protecti on? Let’s say I sell

the April monthly covered call for 37 cents and

you sell the Mar 4 weekly for 16 cents. Then USO

plummets. Initi ally I have more than double the

amount of protecti on as you do. My call premi-

um will off set a 37 cent drop in the stock, yours

will only off set a 16 cent drop. Now, sure you can

roll to bring in more premium but so can I. That

doesn’t negate the fact that traders whoshort

monthly opti ons carry more protecti on than

those with Weeklys.

From a downside protecti on standpoint, month-

ly options are superior.

One final comparison of note is liquidity. Month-

ly opti ons are almost always more liquid. That

means the open interest is higher and the bid-

ask spreads are ti ghter. As a result the slippage

suffered using Weeklys will be worse If you’re

concerned with liquidity, then you should be

using monthly options.

There’s your match up.

Tackle Trading - Tackle 2542

/Part ICASH FLOW TRICKERY

When introducing the masses to the covered call

strategy we wisdom dispensers like to equate

real estate and rental income to stock ownership

and covered call selling. If you’ve yet to have the

pleasure to hear such a tale, then allow me.

In 2012 you bought a residential property for

$100k. All cash, because that’s how you roll. You’ve

heard for years that real estate can be a good

investment. It goes up in value, hedges against

inflation, and chicks dig real estate tycoons.

Fast forward to today. Five years have passed and

your home value is now, drum roll please … $100k.

So you complain to me, your buddy. Our conver-

sati on goes like so:

You: Curse you real estate gods! I’ve tied up

my hard earned dough for fi ve long years and

you’ve given me zippo for my troubles.

Me: Well, Tom (Dick, Harry, whatever your name

is) did you rent out your house along the way?”

You: Rent? What’s renting? Never heard of it.

I thought the only way you made money on a

house was if it went up in value.

Me: Well that’s one way but you also could have

rented your house out to someone in need of a

place to live. In doing so you could have brought

in I dunno, maybe $500 or $1,000 a month in

income. If you brought in even $500 per month

you would have scored $30K over the last five

years just in cash flow.

You: Wow, I’m dumb.

Me: Nope. Just ill-informed. There’s a diff erence.

And check this out. By scoring $30K along the

way you reduced your cost basis on the house to

$70K. Get it?

You: Got it.

Me: Imagine if you kept renti ng out the house

for the next 20 years. At some point you will

have captured $100K in income eff ecti vely

reducing your basis in the house to zero. Then

if the house blows up, technically you’re not out

any money at all.

Now to the stock market. Suppose instead of buy-

ing a house for $100K you bought shares of the

SPY in 2012. And pretend like the SPY has gone

sideways for the past fi ve years leaving you with

nothing to show for your big investment.

Guess what. If you came to me complaining my

response would be the same as that to the real

estate investor.

You: Curse you stock gods! Five years and noth-

ing to show for it.

Me: Well, did you rent out your stock along the

way?

You: Of what do you speak?

Me: You could have been renting out your stock

every month to score some income along the way.

Tackle Trading - Tackle 2543

You: No way!

Me: Way! It’s known as selling covered calls. Let’s

say you bought shares of the SPY at $100 apiece

in 2012. For $100K you could have purchased

1,000 shares. And every month you could have

sold ten call opti ons allowing you to capture,

let’s say, $1,000 per month ($100 per contract).

Over five years you would have generated accu-

mulated $60K in cash fl ow ($12k per year) from

selling covered calls. Think about the eff ect

that would have on your cost basis. Since you

brought in basically $60 per share, your basis

on the stock would have dropped to $40 from

the initi al $100. And if you conti nue to generate

income from covered calls for the next decade

there may even come a ti me where you reduced

your basis on the stock to zero.

So that’s the gist of the analogy. Now, here’s

where things diverge. When you rent out a

house you capture the rent no matter what the

house value does. Plus you’re not limiting how

much you can make in the house if it appreciates

in value. With covered calls it’s a bit different.

First off when you sell a call option you promise

to sell your stock at a set price. That limits your

upside in the stock right off the bat. In that sense

covered calls are more like a lease option in real

estate. Basically a lease opti on is when you allow

someone to rent your house with the opti on to

buy at a certain price for a set ti me frame. If my

house is $100K and I give you the right to buy it

at $105K for the next year, then I’m capping my

profi t potential on the house at $5K.

But it doesn’t stop there. If your stock falls you

have to keep selling lower strike calls. With XYZ

at $100 maybe I start out selling the 105 call.

But if the stock drops I’ll have to sell a 100 call,

then 95 call, then 90 call month to month if the

descent persists. Suppose aft er six months the

stock is down at $70 and I’m short the 75 call.

Sure, I may have brought in some income along

the way (say, $7) but I’m down $30 on the stock.

Feel free to get all excited about that $7, but

let’s be honest, your account value is sti ll down

substanti ally. So what’s the proper way to think

about your positi on here? Because of the short

75 call even if the stock were to magically recov-

er back to $100 tomorrow I wouldn’t parti cipate

in the bulk of the upside. Tricky, tricky.

You’ll find my answer in Cash Flow Trickery Part Two.

Tackle Trading - Tackle 2544

/Part IICASH FLOW TRICKERY

Previously we highlighted the poster child strate-

gy for cash fl ow kings – covered calls. Consider

the situation we left with last time:

“If your stock falls you have to keep selling lower

strike calls. With XYZ at $100 maybe I start out

selling the 105 call. But if the stock drops I’ll

have to sell a 100 call, then 95 call, then 90 call

month to month if the descent persists. Suppose

aft er six months the stock is down at $70 and

I’m short the 75 call. Sure, I may have brought

in some income along the way (say, $7) but

I’m down $30 on the stock. Feel free to get all

excited about that $7, but let’s be honest, you’re

account value is still down substantially.

So what’s the proper way to think about your

positi on here? Because of the short 75 call even

if the stock were to magically recover back to

$100 tomorrow I wouldn’t parti cipate in the bulk

of the upside. Tricky, tricky.”

In sum, we’re down $30 on the stock (an un-

realized loss) while having captured $7 along

the way in call premiums (a realized gain). The

fundamental problem is that we need the stock

to recover back towards $100 (our original pur-

chase price), and yet by virtue of our short 75

call option we are obligati ng ourselves to sell the

stock relati vely quickly if it were ever to recover.

Side note – our cost basis is really $93 for the

stock due to the $7 of premium received over

the past six months.

Consider your choices.

First, you could buy back the 75 call if the S70

stock were to rally past the $75 zone. Once

the short call has been closed you’re left with a

straight stock position allowing unfett ered parti

cipati on in any further rally. The drawback? You

no longer have any protecti on and you probably

just locked in a heft y sized loss on the 75 call.

Second, you could simply stop selling covered

calls altogether. Now that the stock is perched at

$70 (a substanti al 30% discount from its highs)

perhaps you’re willing to simply be long stock

at this point. At $70 it certainly has less down-

side risk than at $100. The drawback? What if

the stock languishes at $70 for months on end,

or worse, conti nues plumbing the depths? By

halting your covered call campaign you may be

leaving some serious dough on the table.

Third, stay the course. Remember, short calls

limit your profi t potential for a time. You’re not

limiting your profit potential on the stock forev-

er. Simply for the next month, or however long

you have ti ll expirati on. The beauty of selling

short-term covered calls (one month being the

preferred ti me slot) is that you can adjust the

strikes frequently as the stock undergoes price

shifts, subtle or otherwise.

For example, though we’re short a one month 75

call against our $70 stock it merely limitSs our

upside to $5 in the stock for one month. Aft er

Tackle Trading - Tackle 2545

that if the stock is hanging at $80, we could sell

the one month 85 call. If the stock keeps power-

ing higher and is sitti ng at $90 then, you guessed

it, we could sell the 95 call. Even if the stock ran

through my call strike month after month I’d sti ll

be capturing the lion’s share of the upside.

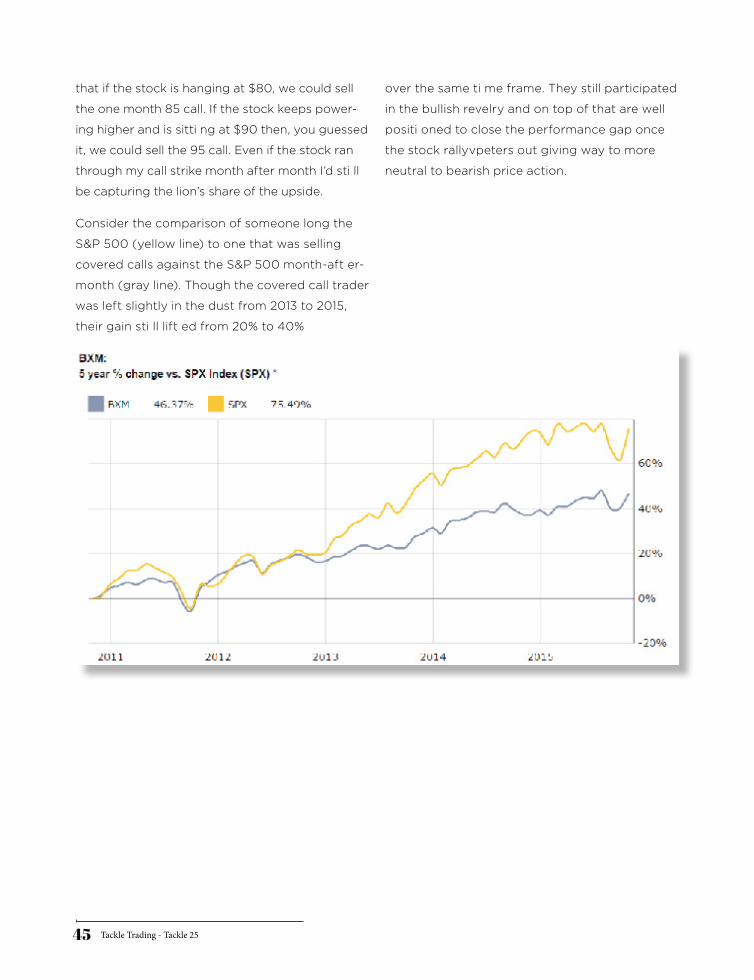

Consider the comparison of someone long the

S&P 500 (yellow line) to one that was selling

covered calls against the S&P 500 month-aft er-

month (gray line). Though the covered call trader

was left slightly in the dust from 2013 to 2015,

their gain sti ll lift ed from 20% to 40%

over the same ti me frame. They still participated

in the bullish revelry and on top of that are well

positi oned to close the performance gap once

the stock rallyvpeters out giving way to more

neutral to bearish price action.

Tackle Trading - Tackle 2546

www.tackletrading.com

IT IS A NO BRAINER, IF YOU ARE NOT ALREADY A TACKLE TRADING MEMBER, JOIN US FOR A 15-FREE TRIAL

SIGN UP NOW