table of contents - home | food and agriculture centre...

TRANSCRIPT

© Confederation of Indian Industry (CII), 2012

All rights reserved. No part of this document may be reproduced, stored, adapted, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, or translated in any language or performed or communicated to the public in any manner whatsoever, or any cinematographic film or sound recording made therefrom without the prior written permission of the copyright holders.

The information presented in this publication has been compiled from various published and electronically available primary and secondary sources. CII makes every effort to ensure the accuracy of information presented in this document. However, neither CII nor any of its office bearers or analysts or employees can be held responsible for any financial consequences arising out of the use of information provided herein.

Published by Confederation of Indian Industry (CII)The Mantosh Sondhi Centre, 23, Institutional Area,Lodi Road, New Delhi – 110003 (India)

3 Feasibility Report for Setting-up Integrated Cold Chain for Banana in Tamil Nadu

Table of Contents

1. Introduction 5

2. Banana Production: Global, India, TN State 8

3. Banana Trade: Global, India, TN State 25

4. SWOT Analysis for TN Banana Business 42

5. Banana Cold Chain in Tamil Nadu: An Overview 46

5.1 Present Chain 46

5.2 Ideal Chain and Temperature Control Intervention 49

5.3 Gap Analysis for Banana Cold Chain Intervention 52

6. Project Report for Setting Up of an Integrated Cold Chain for 53 Banana in Tamil Nadu

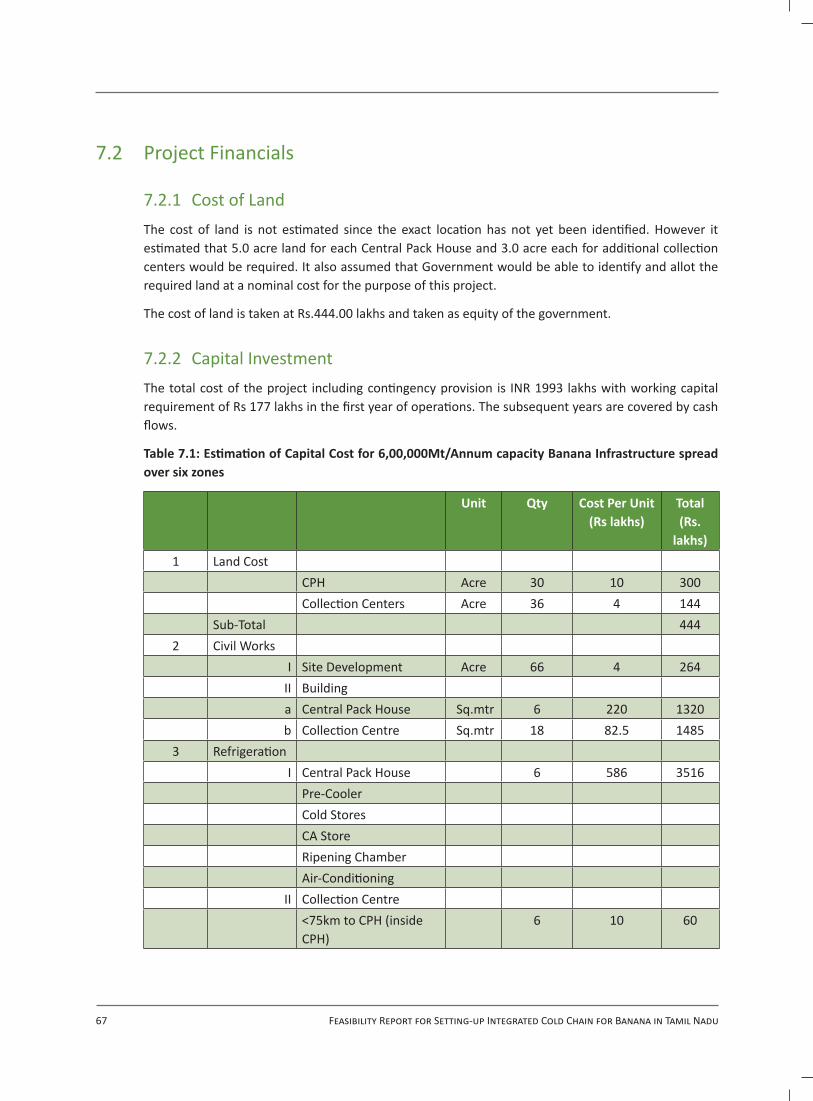

7. Project Cost and Financial Analysis 66

8. Governement Interventions Required 74

9. Recommendations 76

Annexures1. Project Cost for One Module of 1,00,000 Mt/Annum 77

2. Means of Finance for One Module of 1,00,000 Mt/Annum 77

3. Projected Balance Sheet for the First Ten Years 78

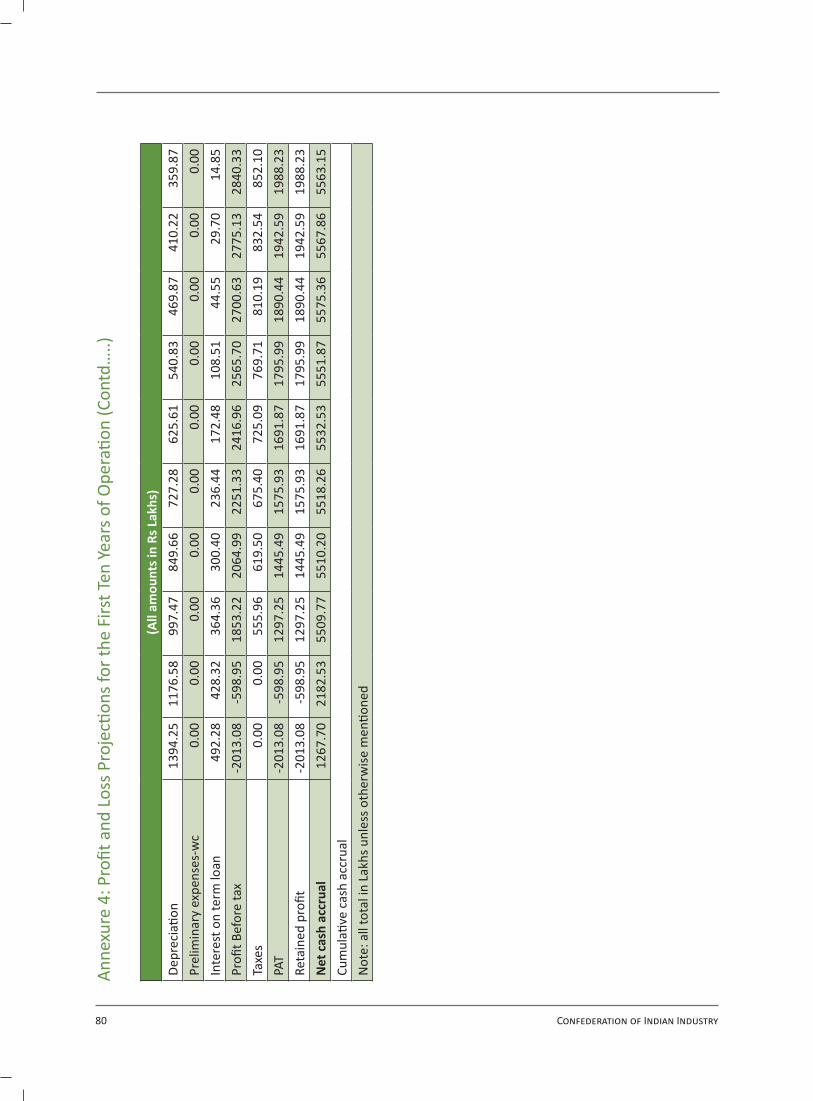

4. Profit and Loss Projections for the First Ten Years of Operation 79

5. Projected Cash Flow Statement for the First Ten Years of Operation 81

6. Discounted Cash Flow for the First Ten Years of Operation and NPV 82

7. Break Even Analysis 82

8. Return on Investment Analysis 83

5 Feasibility Report for Setting-up Integrated Cold Chain for Banana in Tamil Nadu

1. Introduction

Banana is the common name for the fruit produced by herbaceous plants of genus: Musa. It was native to South East Asia, over a period these have been domesticated worldwide and today they are grown in 130 countries world wide, more than any other fruit crop. Bananas are the fourth most widely consumed food for humans after rice, wheat, and corn.

The global production of banana is around 93,716 thousand tons of which India contributed 28% in the year 2009. Besides India, other major banana producing countries are Philippines, China, Brazil, Ecuador, Indonesia, Tanzania, Mexico, Thailand and Costa Rica.

During last five years, production of banana in India and China has substantially increased where as the traditional major producing countries like Ecuador, Costa Rica, have shown stagnation and marginal decline in the production.

In India, South and West zones are major banana producing belts comprising of Tamil Nadu, Maharashtra, Karnataka and Gujarat. Tamil Nadu accounts for 25% of India’s Banana production. The productivity level of banana varies depending on varieties. In Tamil Nadu, areas around Theni, Tirichurapally, Coimabattore are the major producing districts contributing to most of the state’s production.

It was proposed to develop an Integrated Chain for Banana in Tamil Nadu in the Cold Chain Summit 2009, a CII cold chain initiative as part of “ Making Cold Chain Development a reality in India: Infrastructure for Value Creation in Horticulture” and accordingly engaged M/s Ahara Technology Group for carrying out a feasibility study.

1.1. Study Objective and Scope of Work The broad objective of the study is to ascertain techno – economic feasibility of setting up of an Integrated Cold Chain for Banana in the state of Tamil Nadu.

1.2. Scope of the Worka) To assess the quantities of Banana produced annually and to provide data (variety wise and area

wise) covering Tamil Nadu state

6 Confederation of Indian Industry

b) To study prevailing value chain for the banana in the state of Tamil Nadu

c) To study the existing marketing arrangements, processing facilities and their performance from post harvest stage to product stage and assess value addition at each stage

d) To assess deficiencies in backward integration, harvesting, post harvest handling and banana packing and processing infrastructure

e) To Bench mark, against relevant countries and states, in terms of productivity, wastage and price realization.

f) To suggest required measures to improve backward integration to ensure quality during harvesting and post harvest handling and required processing infrastructure for better value addition, marketability, reducing post harvest losses and meeting the export requirements by an appropriate Banana Processing Infrastructure including the following

Identifying key collection centers��

Mapping locations and suggesting where ripening and storage facilities can be set up��

Forward linkage to mandis, wholesalers and food processing units��

Cost of setting of chain��

Funding details through various Government schemes��

Economic feasibility��

1.3. Approach and MethodologyA multidisciplinary team of in house and external consultants of Ahara Technology Group have carried out the study. The requirements of the information were listed down and sources were identified. The information collected was counter verified with those of checklists developed for this purpose.

The list of organizations contacted is:

Department of Horticulture, Govt. of Tamil Nadu.��

District offices of Department of Horticulture in Madurai, Tiruchy.��

National Research centre for Banana��

National Horticulture Board��

APEDA��

MFPI��

Tissue culture labs supplying banana platelets.��

Farmers growing banana plantlets.��

Banana farmers association in Theni.��

7 Feasibility Report for Setting-up Integrated Cold Chain for Banana in Tamil Nadu

Traders of Banana.��

Exporters of banana.��

Owners of Pack houses.��

Suppliers of equipment.��

A few focused group discussions were also held with the farmers growing banana.

The information thus collected was analyzed and forms the basis of recommendations in this report. For fixed cost estimates, quotation were invited from the leading suppliers of Pack house and refrigeration equipment suppliers and for operating expenses, the information from the pack houses currently operational was obtained.

The list of organizations outside country could not be contacted due to time and budgetary constraints.

1.4. Structure of the Study and ReportThe techno economic feasibility report deals with different aspects related to Banana and establishment of Integrated Chain in the state of Tamil Nadu.

The report comprises of 9 chapters, which deal with different aspects of report.

Chapter 1: is the introduction,

Chapter 2: deals with production of banana in the World, India and Tamil Nadu.

Chapter 3: deals with trade of Banana in World, in India and in Tamil Nadu. India’s export of fresh banana, constraints in export of banana and potential target market for Indian banana exports.

Chapter 4: deals with SWOT Analysis with separate sections for Varieties, Pre harvest practices, Post harvest practices and practices that need to be followed for producing export quality banana.

Chapter 5: comprises of Banana cold chain scenario in Tamil Nadu, with details of Present Chain, Ideal Chain and Gap analysis.

Chapter 6: contains Project concept and configuration along with Technical aspects.

Chapter 7: deals with project cost and financial analysis.

Chapter 8: Government Interventions required

Chapter 9: Recommendations from the study

8 Confederation of Indian Industry

2 Banana Production: Global, India, TN State

2.1. Banana BasicsBanana is the common name for herbaceous plants of the genus Musa and for the fruit they produce. Bananas come in a variety of sizes and colors when ripe, including yellow, purple, and red (See Fig-2.1). In popular culture and commerce, “banana” usually refers to soft, sweet “dessert” bananas. By contrast, Musa cultivars with firmer, starchier fruit are called plantains. Many varieties of bananas are perennial.

Fig 2.1: Different colour and shapes of Bananas

The banana plant is one of the largest herbaceous flowering plant. Plants are normally tall and fairly sturdy and are often mistaken for trees, but their main or upright stem is actually a pseudo stem that grows 6 to 7.6 meters (20 to 24.9 ft) tall, growing from a corm. Each pseudo stem can produce a single bunch of bananas. After fruiting, the pseudo stem dies, but offshoots may develop from the base of the plant.

Leaves are spirally arranged and may grow 2.7 meters (8.9 ft) long and 60 cm (2.0 ft) wide. They are easily torn by the wind, resulting in the familiar frond look.

9 Feasibility Report for Setting-up Integrated Cold Chain for Banana in Tamil Nadu

Each pseudo stem normally produces a single inflorescence, also known as the banana heart. Banana fruit develop from the banana heart, in a large hanging cluster, made up of tiers (called hands) with up to 20 fruit to a tier. The hanging cluster is known as a bunch, comprising 3–20 tiers, or commercially as a “banana stem”, and can weigh from 30–50 kilograms (66–110 lb). In common usage, bunch applies to part of a tier containing 3-10 adjacent fruits.

Individual banana fruits (commonly known as a banana or ‘finger’), weigh on an average 125 grams (0.28 lb), of which approximately 75% is water and 25% dry matter. There is a protective outer layer (a peel or skin) with numerous long, thin strings (the phloem bundles), which run lengthwise between the skin and the edible inner portion. The inner part of the common yellow dessert variety splits easily lengthwise into three sections that correspond to the inner portions of the three carpels.

Banana fruit is of very high nutritional value (Table 2.1) and supplies daily requirement of many vitamins to an extent of 1to20% of an average individual. Further it is highly palatable across the globe.

Table 2.1: Nutritional Value of Banana

Banana : Nutritional value per 100 g of raw edible partsEnergy 371 kJ (89 kcal)Carbohydrates 22.84 gSugars 12.23 gDietary fiber 2.6 gFat 0.33 gProtein 1.09 gVitamin A equiv. 3 μgThiamine (Vit. B1) 0.031 mgRiboflavin (Vit. B2) 0.073 mgNiacin (Vit. B3) 0.665 mgPantothenic acid (B5) 0.334 mgVitamin B6 0.367 mgFolate (Vit. B9) 20 μgVitamin C 8.7 mgCalcium 5 mgIron 0.26 mgMagnesium 27 mgPhosphorus 22 mgPotassium 358 mgZinc 0.15 mgOne banana is 100–150 g. Source: USDA Nutrient database

10 Confederation of Indian Industry

2.2. Commercial Banana VarietiesIndia is endowed with diverse agro climatic conditions, which have encouraged the development and sustenance of large number of varieties catering to local needs. More than 20 varieties are commercially grown in different parts of India. However, ‘Cavendish clones’ dominate the production and forms the main stay of Indian banana industry, owing to its high yield, wide market acceptability, short crop duration and high economic returns per unit area. The important Cavendish clones are Basrai (Dwarf Cavendish), Robusta, Harichal, Grand Naine, Shrimanthi, Bhusaval and Pedda Pachha Arati. Cavendish group of banana has larger area and production and contribution is more than 50% to the production. But it is not available in the coastal region due to high susceptibility to Sigatoka leaf spot disease. Some of the important varieties are as follows:

2.2.1. Grand Naine It is most accepted international variety. It is a tall statured plant and a heavy yielder with long cylindrical bunch. On an average it produces a bunch weighing 25 kg and may go up to 32-35 kg, with 8-10 hands with 200-220 fruits/bunch. The length of the fruit is 15-21 cm and girth is 12-13 cm.

2.2.2. RobustaIt is normal statured with black brown blotches on the stem, bunches weigh around 20 kg having 8-10 hands/bunch. The length of the fruit is 15-20 cm and girth is 12 cm with thick fruit skin

2.2.3. Dwarf CavendishThe plant stature is dwarf. Dark black brown blotches appear all along the stem. Bunches are large with compactly arranged 8-10 hands weighing about 20kg. Length of fruit is 13-14 cm and girth 8-10 cm. Skin is thick and the fruit tapers gradually towards the tip. It is not fit for export.

2.2.4. Red BananaThe plant is tall and robust statured. The colour of the fruit, pseudo tem, petiole and midrib is purplish red. The bunch weight is 20-25 kg with 6-7 hands and 80 fruits/bunch. The length of the fruit is 16-18 cm.

2.2.5. NendranThere is considerable diversity in plant stature. Bunch has 5-6 hands weighing about 6-12 kg. Fruits have a distinct neck with thick green skin turning buff yellow on ripening. Fruits remain starchy even on ripening.

2.3. Global ProductionBanana and Plantain is the 4th important food crop in terms of gross value. It is produced in 130 countries in tropical and sub-tropical regions of the world of mostly developing economies. Globally,

11 Feasibility Report for Setting-up Integrated Cold Chain for Banana in Tamil Nadu

banana and plantain are cultivated 4.879 million hectares with a total production of 93.7 million tones.

Bananas, due to the special climatic conditions required, are mainly produced in developing countries. About 98% of world productions are grown in these countries. Developed countries are the usual destination for export of bananas. The crop is grown by millions of small-scale farmers in Africa, South Asia and Northern Latin America for household consumption and or /local markets. Most of this production achieved with few or no external inputs.

In most of the banana and plantain growing countries, it is grown perennially with single or two cultivars dominating the whole economy. Due to the tropical nature, these countries are receiving plenty of rains with good soil; the perennial system of cultivation is followed in large areas. Due to the non- availability of labour, mechanization is commonly adapted with aerial spraying for plant protection measures.

In the banana republic countries, Cavendish group of bananas are grown commercially for export to USA and UK markets. In South American countries like Brazil etc., Pome group of fruits are the most important type grown commercially in large areas. In the Western African countries, Plantain is the most preferred variety grown for local and export trade. In the eastern African countries, high land AAA bananas are commonly grown with Cavendish and cooking bananas.

In the South East Asian countries, like India, polyclonal system of cultivation is adopted for local and export market. In this region, Philippines, Indonesia and Malaysia are the major banana growing countries while Australia, Cavendish banana are grown in a larger extent.

Production of banana is concentrated in few countries and not equitably and widely spread. The ten major banana producing countries accounted for more than 3/4th of total banana production in 2010. A significant change from 2002 to present times is the substantial production increase in Philippines pushing Ecuador to fourth position from 2nd position. Thus the concentration of banana production has increased over time although different regional distribution has changed.

The top 20 banana producing countries is mentioned in Table 2.2.

Table 2.2: Top 20 countries in Banana Production in World (2010) (Source: FAO Stat)

Rank Area Production (Int $1000)

Production (MT)

1 India 8386971 297800002 China 2773754 98488953 Philippines 2306897 91013404 Ecuador 2233632 79310605 Brazil 1960937 69627906 Indonesia 1620806 57550707 United Republic of Tanzania 823686 29247008 Guatemala 714658 26375709 Mexico 592371 2103360

12 Confederation of Indian Industry

The table 2.3 given below shows the 10 major banana producing countries in the world and percentage share in world production.

Table 2.3: International Status: Production & share (2010) of top ten producers

Rank Area Production (Int $1000)

Production (MT)

10 Colombia 572933 203434011 Burundi 538664 191266012 Costa Rica 493963 180394013 Thailand 446357 158490014 Viet Nam 417208 148140015 Egypt 289784 102895016 Cameroon 267605 95020017 Papua New Guinea 266141 105000018 Bangladesh 230445 81825419 Kenya 222930 79157020 Dominican Republic 207011 735045

Sr No. Country Production Share (%)1 India 2,97,80,000.00 32.062 China P Rp 98,48,895.00 10.603 Philippines 91,01,340.00 9.804 Ecuador 79,31,060.00 8.545 Brazil 69,62,790.00 7.506 Indonesia 57,55,070.00 6.207 Guatemala 26,37,570.00 2.848 Mexico 21,03,360.00 2.269 Colombia 20,34,340.00 2.1910 Burundi 19,12,660.00 2.06 Page Total 7,80,67,085.00

The factors such as the system of cultivation and the varieties grown, affects the biotic stresses influencing the production and productivity in the different regions of world. In ‘banana republics’ and South American countries, due to the monoculture system of Cavendish group of varieties cultivation undertaken, leaf spot disease is highly prevalent requiring 25-30 rounds of aerial spraying of fungicides. But in Asian and South East Asian countries, many biotic stresses like Fusarium wilt, weevil, nematodes and viruses are the main factors affecting the production. In the African countries,

13 Feasibility Report for Setting-up Integrated Cold Chain for Banana in Tamil Nadu

the Moko disease is becoming more serious concern in the production of high land and plantain and cooking bananas which form the main staple food in the region.

Internationally, the research activities in different regions of the world are undertaken by well established institutions and these are further well coordinated and facilitated by the International Network for the Improvement of Banana and Plantain (INIBAP) located in France. With in Asia, the Banana and Plantain Network (BAPNET) located in Philippines is undertaking the coordination of the banana research activities carried out by the National Agricultural Research System (NARS) of Asia and South East Asian countries.

Some of the important features of international Banana production scenario are:

Grown in more than 130 countries worldwide.��

Banana production is taken up in back yard cultivation, small farm cultivation and large automated ��

farm corporate cultivation.

Top 4 countries i.e. India, China, Philippines, and Ecuador account for 60% of world’s ��

production.

Top 10 countries account for more than 80% of world’ production.��

The productivity in 2009 varied substantially amongst countries varying from 5.4Mt/ha in Burundi ��

to 54.3 Mt/ha in Indonesia.

The countries with large, mechanized system of cultivation normally are able to achieve better ��

productivity.

Per capita production varies substantially amongst different countries as well as exportable ��

surpluses.

2.4. Production in India

2.4.1. Banana Importance in Indian AgricultureIndian economy is still largely dependent on agriculture and Industrial system based on the raw material produced by rural production systems. Banana is 10th in importance in terms of value of production in the year 2009 and the value is put at US$ 3.736 billions as per the FAO estimate. If live stock based products are not considered, then it is 8th most important commodity for Indian agriculture. But in terms of investments made by private capital, it is negligible in comparison to Paddy/Rice, Wheat, Sugarcane, Cotton and potatoes. Probably, the vegetables are the only other agricultural commodity which has not attracted the required investments especially in post harvest processing systems.

14 Confederation of Indian Industry

From table 2.4 below Banana comes in top 10 products monetary value wise.

Table 2.4: Importance of Banana in Indian Agriculture Based on 2010 production (Source: FAO)

2.4.2. Growth pattern of Banana in IndiaIndia with its rich bio–diversity of banana and plantain is the largest producer and consumer with estimated production of 29.78 million tones annually. Within the country, banana ranks first in production and third in area, after Mango and Citrus group, among the fruit crops. It occupies about 13% area among the fruit crops and constitutes 31% of the production of all fruit crops. There has been a spectacular increase in production of bananas during the last 20 years due to

Increased acreage:�� Area under cultivation of banana has increased from 2 lakh hectares to 6.2 lakh hectares by 2002 and estimated to be around 7 lakh hectares in 2008-09

Improved productivity:�� The productivity has also increased from 9.0 tones/ha to 33.5 tones/ha, with some states reporting the productivity up to 53 tones/ha

R&D: �� concerted efforts in banana research and development.

Rank Commodity Production (MT)1 Rice, paddy 1439630002 Wheat 808000003 Potatoes 365773004 Bananas 297800005 Onions, dry 151180006 Mangoes, Mangosteens, Guavas 150267007 Maize 140600008 Millet 132900009 Tomatoes 1243320010 Eggplants (aubergines) 1056300011 Chick peas 748000012 Cabbages and other brassicas 728140013 Sorghum 670000014 Cauliflowers and broccoli 656900015 Oranges 596640016 Groundnuts, with shell 564000017 Papayas 419600018 Hen eggs, in shell 337810019 Peas, green 302940020 Lemons and limes 262920021 Chicken meat 219300022 Apples 177720023 Buffalo meat 148943024 Pineapples 138680025 Barley 1350000

15 Feasibility Report for Setting-up Integrated Cold Chain for Banana in Tamil Nadu

Table 2.5: Area, Production and Productivity of Banana in India

Year Area (In 000’’Ha)

% Of Total Frt.Area

Production (In 000’’ Mt)

% Of Total Frt.Production

Productivity (In Mt/Ha)

1991- 92 383.9 13.4 7790.0 27.2 20.32001- 02 466.2 11.6 14209.9 33.0 30.52002 -03 475.3 12.5 13304.4 29.4 28.02003 -04 498.6 10.7 13856.6 30.4 27.82004 -05 589.6 11.9 16744.5 34.0 28.42005 -06 569.5 10.7 18887.8 34.1 33.22006 -07 604.0 10.9 20998.0 35.3 34.82007- 08 658.0 11.2 23823.0 36.3 36.22008- 09 709.0 11.6 26217.0 38.3 37.02009-10 770.4 - 26469.5 - 34.4

Banana primacy in overall horticulture production by quantity is growing and has increased from 27.2% in 19991-92 to 33% in 2001-02 and now reached 38.3% in 2008-9. The importance of banana amongst horticulture produce is only going to increase because of its advantages such as universal acceptance, less seasonality compared to other fruits and vegetables, availability of well developed technologies for storage/transport internationally and better returns to farmers.

2.4.3. Distribution Pattern of Banana in India

2.4.3.1. Among States:

Availability of wide genetic diversity, varying production systems and its suitability to wide range of agro climatic conditions are the reasons for wide range adaptability of Banana in India. It is grown as homestead garden as well as on commercial plantation. Commercial production system is well irrigated, while subsistence cultivation is under rain fed farming. It is mainly grown along the riverside but drip based cultivation among non river irrigations have also been increasing and most of Grand Naine variety is coming up in these areas.

Major growing states are Tamil Nadu, Maharashtra, Gujarat, Andhra Pradesh and Karnataka. These account for 68.67% of India’s production in the year 2008-09. Other states have limited area and production. The state wise details of production and percent share in total is given in Table 2.6.

Table 2-6: Production of Banana in India State wise in 2010-11 (Source: APEDA AgriExchange)

Sr No. State Production (000 Tonnes)

Share (%)

1 Tamil Nadu 8,253.00 27.71

2 Maharashtra 4,303.00 14.45

3 Gujarat 3,978.02 13.36

16 Confederation of Indian Industry

Sr No. State Production (000 Tonnes)

Share (%)

4 Andhra Pradesh 2,774.76 9.32

5 Karnataka 2,281.58 7.66

6 Madhya Pradesh 1,719.58 5.77

7 Bihar 1,517.11 5.09

8 Uttar Pradesh 1,346.05 4.52

9 West Bengal 1,010.15 3.39

10 Assam 723.57 2.43

Page Total 27,906.82

Among the states, the area and production of Banana is largest in Tamil Nadu, while the productivity is highest for Maharashtra state followed by Gujarat state. Maharashtra excels in productivity owing to monoculture of high – yielding Cavendish clones, coupled with adoption of improved technologies, i.e. micro irrigation, fertigation and use of tissue cultured plants besides targeted management. Strategically, adoption of improved technologies in other states has potential to improve productivity. The area and productivity of banana in the year 2008-09 is given at Table 2.7.

Table 2.7: State wise area and productivity of Banana in 2009-10 (Source: NHB)

S.No. State Area ('000'HA.)

Production ('000'MT.)

Percentage Of Total

Production

Productivity

1 Maharastra 85.000 5,200.000 19.645 61.176

2 Tamil Nadu 113.680 4,980.860 18.817 43.815

3 Gujarat 61.920 3,779.810 14.280 61.043

4 Andhra Pradesh 80.600 2,819.600 10.652 34.983

5 Karnataka 104.400 2,132.300 8.056 20.424

6 Madhya Pradesh 33.000 1,459.800 5.515 44.236

7 Bihar 31.500 1,435.300 5.422 45.565

8 Uttar Pradesh 30.430 1,138.580 4.301 37.416

9 West Bengal 40.978 982.228 3.711 23.970

10 Assam 53.390 805.240 3.042 15.082

Total 770.421 26,469.540 100.000 34.357

17 Feasibility Report for Setting-up Integrated Cold Chain for Banana in Tamil Nadu

2.4.3.2. Banana production and Varieties:

The variety wise distribution of banana in the country is shown at figure 2.1 and 2.2.

Fig 2.1: Variety wise area distribution

2.2 Variety wise production distribution

As can be seen, Cavendish variety account for 49% of area and 69% of production in the country followed by Poovan which account for 18% area and 17% production. Among the varieties which have presence at 4% are Pome, Nendran, Rasthali, Bluggoe. There are many other local and non local varieties contributing to about 17% production and 18% area.

18 Confederation of Indian Industry

Variety wise yield varies substantially. The average yields of different varieties are shown at table 2.8 Grand naine, Shrimanti also an equivalent variety show maximum yields per ha. There are reports of even 105 mt/ha that have been achieved by farmers especially in some parts of Andhra Pradesh and Tamilnadu.

Table 2.8 : Variety-wise average yield of banana (tonnes/ha.)

Varieties Average yield (tones/ha.)Basrai, Rasthali 40-50Shrimanti 70Grand Naine 65Ardhapuri , Meanyham 55Hirsal, Safed Velchi, Red banana, Lal Velchi 45Poovan 40-50Monthan 30-40Dwarf Cavendish , Robusta Champa & Chini desi 50-60Nendran 30-35

2.5. Production of Banana in Tamil Nadu

2.5.1. Geography and agro-climateTamil Nadu covers an area of 130,058 square kilometres (50,216 sq mi), and is the eleventh largest state in India. The bordering states are Kerala to the west, Karnataka to the northwest and Andhra Pradesh to the north. To the east are the Bay of Bengal and the union territory of Puducherry. The southernmost tip of the Indian Peninsula is located in Tamil Nadu.

The western, southern and the north-western parts are hilly and rich in vegetation. Tamil Nadu is the only state in India which has both the Western Ghats and the Eastern Ghats and they both meet at the Nilgiri hills. The Western Ghats dominate the entire western border with Kerala, effectively blocking much of the rain bearing clouds of the South West Monsoon from entering the state. The eastern parts are fertile coastal plains and the northern parts are a mix of hills and plains. The central and the south central regions are arid plains and receive less rainfall than the other regions.

Tamil Nadu has a coastline of about 910 kilometres (600 mi) which is the country’s third longest coastline. Tamil Nadu’s coastline bore the brunt of the 2004 Indian Ocean Tsunami when it hit India, which caused 7,793 direct deaths in the state. Tamil Nadu falls mostly in a region of low seismic hazard with the exception of the western border areas that lie in a low to moderate hazard zone; as per the 2002 Bureau of Indian Standards (BIS) map, Tamil Nadu falls in Zones II & III. Historically, parts of this region have experienced seismic activity in the M5.0 range.

Tamil Nadu state comprises 31 districts (including Chennai) as shown in Figure 2.3

19 Feasibility Report for Setting-up Integrated Cold Chain for Banana in Tamil Nadu

Figure 2.3: Tamil Nadu map with districts

Tamil Nadu is heavily dependent on monsoon rains, and thereby is prone to droughts when the monsoons fail. The climate of the state ranges from dry sub-humid to semi-arid. The state has three distinct periods of rainfall:

advancing monsoon period, South West monsoon from June to September, with strong southwest ��

winds;

North East monsoon from October to December, with dominant northeast winds;��

dry season from January to May.��

The normal annual rainfall of the state is about 945 mm (37.2 in) of which 48% is through the North East monsoon, and 32% through the South West monsoon. Since the state is entirely dependent on rains for recharging its water resources, monsoon failures lead to acute water scarcity and severe drought.

Tamil Nadu is classified into seven agro-climatic zones: north-east, north-west, west, southern, high rainfall, high altitude hilly, and Cauvery Delta (the most fertile agricultural zone). The maximum and minimum temperatures range from 43˚C and 13.1˚C in the plains and 32.3˚C and 3.0˚C in hills.

Mango and Banana are the leading fruit crops in Tamil Nadu accounting for over 84% of the area under fruit and over 87% of the total fruit production.

20 Confederation of Indian Industry

The main fruits and their production areas in Tamilnadu are as follows:

Fruit Main Production AreasBanana Thiruchirapalli, Thoothukudi, Thirunelveli, Pudukottai, ThanjavurMango Krishnagiri, Vellore, Dindigul, Theni, Dharmapuri, MaduraiSapota Thirunelveli, Erode, KarurGrapes Theni, CoimbatoreGuava Madurai, Dindigul, Vellore, VirudhunagarAonla Thirunelveli, Sivagangai, Thoothukudi, Coimbatore, Dindigul, Erode

2.5.2. Promotional Bodies in TNHorticulture development is planned, organised and supervised by Horticulture department. A separate mission approach, as part of national policy is being implemented in Tamilnadu also as State Horticulture Mission.

The National horticulture Mission is following cluster approach for development of horticulture sector. The plan for 2009-10 under Mission approach is as follows:

Table 2.9 Cluster and crop matrix in Tamil Nadu (2009-10)

S.No Cluster Districts Crops1 Cluster I Krishnagiri, Dharmapuri and Pudukottai Aonla

Dharmpuri, Krishnagir and Vellore Banana & Mango FloricultureDharmpuri and Vellore Spices (Chilli and Turmeric),

Medicinal & Aromatic Plants.2 Cluster 2 Salem, Tiruchirapalli and Villipuram Aonla

Salem, Tangore, Tiruchirapalli and Villipuram BananaPerambalur, Pudukottai, Salem, Tirukirapalli and Villipuram

Mango

Cudalore, Perambalur, Pudukottai, Tangore and Villipuram

Cashew and cocoa

Salem Floriculture, spicesPerambelukr, Pudukotai, Salem and Villipuram Medicinal & aromatic plants

3 Cluster 3 Kanyakumari, Tirunalveli Aonla, Banana , Mango , Medicinal & Aromatic plants.

Shivagangai Cashew and ChilliKanyakumari, RamaldhapuramTirunalveli Cashew, cocoa, Floriculutre,

spices.4 Cluster 4 Oimbatore, Dindigul, Madurai, and Theni Aonla, Banana, Mango

Coimbatore, Dindigul and Erode Spice (Chilli and Turmeric)Coimbatore, Dindigul, Erode and The Nilgiris FloricultureDindigul and Madurai Medicinal & Aromatic plantsDistricts=20 Crops=10

21 Feasibility Report for Setting-up Integrated Cold Chain for Banana in Tamil Nadu

As can be seen from the cluster crop matrix, Banana is an important component in all the four clusters.

2.5.3. District-wise ProductionDistrict wise banana production in the sate of Tamilnadu in the year 2009 is shown at Table 2.10. Banana is grown in all 31 districts of Tamilnadu.

Table 2.10: District wise Area, production and productivity of Banana in the state of Tamilnadu

S.No District

AREA, PRODUCTION AND PRODUCTIVITY OF HORTICULTURE CROPSArea: Ha., Prod.: Tonnes & Proty : Tonnes /Ha

2012-13Area Prodn Productivity

1 Ariyalur 369 24934 66.112 Coimbatore 12353 751016 60.803 Cuddalore 5427 245893 45.314 Dharmapuri 1804 95956 53.195 Dindigul 6105 246205 40.336 Erode 13841 935056 67.567 Kancheepuram 348 18392 52.858 Kanyakumari 7747 409749 52.899 karur 6682 352646 52.7810 Krishnagiri 2836 150000 52.8911 Madurai 3376 201493 59.6812 Nagapattinam 728 38517 52.9113 Namakkal 3408 180253 52.8914 Perambalur 247 25722 104.1315 Pudukottai 4557 248686 54.5716 Ramanathapuram 484 25589 52.8717 Salem 4573 241892 52.8918 Sivagangai 926 48979 52.8919 Thanjavur 5265 275572 52.3420 Theni 6105 629209 266.8621 The Nilgiris 1155 61106 55.2922 Thiruvallur 1688 89293 52.8923 Thiruvannamalai 3965 348553 87.9124 Thiruvarur 506 26788 52.9425 Thoothukudi 12408 723983 58.3526 Tirupur 4963 293728 59.1827 Thiruchirapalli 10665 463101 43.4228 Thirunelveli 11992 448389 37.3929 Vellore 8716 288176 33.0630 Villupuram 1698 89827 52.9031 Virudhunagar 1087 57508 52.90 TOTAL 146024 8036211 54.90

22 Confederation of Indian Industry

2.5.4. Disrict-Wise AcreageCultivated area distribution amongst districts in 2009 is shown at Figure 2.4. As can be seen top 10 district account for 66% area while remaining 21 districts account for only 34% area.

Fig 2.4: Banana cultivation area distribution amongst Districts in 2012-13

2.5.5. Disrict-Wise QuantityDistribution of Quantity of banana produced amongst districts follows area pattern excepting Theni district. Theni accounts for 8.1% production even though it accounts for only 4% area. Pl see fig 2.5.

The

ka

Dindigul, 4.1

eni, 4.18%

O

rur, 4.58%

8%

Others, 34%

Kany5

Erode, 9.4

akumari, 5.31%

48%,

Thiru8.2

Vellore, 5.97

Thoothukudi8.50%

Coim8.4

nelveli, 21%

Thiruchirapa7.30%

7%

i,

batore, 46%,

alli,

23 Feasibility Report for Setting-up Integrated Cold Chain for Banana in Tamil Nadu

Fig 2.5: Banana Production distribution amongst Districts in 2012-13

The reason is mainly the productivity levels. Amongst top 10 banana producing districts, the productivity varies from high of 89.3 Mt/ha in Theni to only 27.8 Mt/ha in Vellore district. Only four out of top 10 banana producing districts have higher productivity than state average of 46.5 mt/ha. The details are depicted in fig 2.6.

Fig 2.6 : Productivity of Districts in 2012-13

Th

Tir

K

iruvannamalai4%

upur, 4%,

anyakumari, 5

Karur, 4%,,

Others, 33%

T%

%,

Ero

Thirunelveli, 6%

ode, 12%

Co

T

Thiruchir6%%

imbatore, 9%,

Thoothuku9%

Theni, 8%

rapalli, %

udi,

24 Confederation of Indian Industry

2.5.6. Variety DistributionThe varietal distribution with in Tamilnadu based on experience of the field people is as follows:

S.No. Variety Approximate share1 Grand Naine 30-35%2 Puvan 15-20%3 Rasthali 7-8%4 Karpuravalli 7-8%5 Nendran 4-5%6 Virupakhi/Malapalam 4-5%7 Neypoovan 2-3%8 Others 15-20%

The distribution of varieties by area/region is Grand Naine variety in Theni, Rasthali and Poovan in Tuticorin, Poovan; Rasthali, Neypoovan, Nendran in Tiruchi area; Karpooravalli in Tanjavur; Robusta varieties in Krishnagiri and Dharmapuri areas.

2.5.7. Planting MaterialThere is no shortage of planting material. About 20 tissue culture plants are supplying planting material to the farmers. Some of them like Jain, Growmore and SPIC tissue culture labs are very large and sophisticated and can meet the requirements of farmers in large numbers. It is the experience of the department that the number of tissue culture labs are increasing as the demand is increasing and there is no shortage of supply.

2.5.8. Industry view on varietyThe general opinion of administrators and scientists is that the multiplicity of varieties are going to be existing in Tamilnadu for very long time in view of the following factors:

Familiarity with cultivation practices and ready availability of planting material.��

Farmers are happy with the returns they are getting��

Traders insist that variety like Grand Naine is not suitable for religious functions, marriages, temples ��

etc. One reason could be the cost per unit and better handling characteristics.

Ready demand for the varieties being grown��

Even from bio diversity reasons, it may be necessary to maintain at least 3-4 main varieties so as to ensure germ plasma is retained at field level.

Farmers follow a mix of both traditional and modern practices in cultivation of Banana.

The production of banana in Tamil Nadu alone is almost equal to Ecuador and higher than Indonesia.

There is adequate production for introduction of any modern systems to optimize the returns in Tamil Nadu.

25 Feasibility Report for Setting-up Integrated Cold Chain for Banana in Tamil Nadu

3. Banana Trade

3.1. Basics of Trading

3.1.1. HarvestingBanana fruit trading life starts from the time it is cut from mother plant. Thus the start of post harvest life is also start of trading life of a banana. This ends when the fruit is consumed/sold for consumption. Since supply of water, photosynthesis and nutrients is cut off after separation of the fruit from the plant, fruit enters ‘perishable phase’. Banana is highly perishable and has got short shelf life being a climacteric fruit.

Post harvest storage life and quality of banana depends on two factors:

Stage of maturity at which it is harvested��

Post harvest handling system��

3.1.2. MaturityThe stage of maturity is of prime importance in banana trade. Minor modifications are made in harvesting in relation to maturity depending on the market and time it takes to reach market.

Several parameters are used for determining the maturity of banana fruits. These are either based on external appearance or chemical constituents. These are not universally applicable and differ depending on varieties and even strains and locations. Some of these indices are

Age after emergence of flower.��

Angularity of the fingers��

Diameter and length of fruit��

Heat units��

26 Confederation of Indian Industry

An indicative maturity at harvesting stage vis-à-vis market and consumption time from the time of harvest is indicated at table 3.1 below:

Table 3.1: Maturity stage of harvest and markets

S.No. Market and Consumption time from harvest Maturity stage at the time of harvesting

1 Domestic market and consumption with in 7 days Fully matured bunches i.e. 90-95%2 Regional markets and consumption with in 15

days 85 to 90% maturity with fairly defined angles

3 Long distance transportation and export 75% maturity and fruit with well defined angles.

3.1.3. Stages of Banana In trade, banana’s post harvest life/trading life is divided into seven stages as indicated table 3.2.

Table 3.2: Banana Colour Stage ChartStage 1 Dark Green, Stage at which fruit should be shipped from fields

Stage 2 Light Green, as ripening begins either through natural process or through application of Ethylene

Stage 3 More Green than Yellow, starches turning to sugar, as the fruit start producing it’s own ethylene. Sale in Summer and hot weather recommended at this stage

Stage 4 More Yellow than Green, continuing the ripening process, ideal for retail display. Sale in Winters periods can start at this stage.

Stage 5 Yellow with Green tips, ideal for purchase by customers and to finish ripening at home

Stage 6 All Yellow firm fruit, with good flavour, ready for eating, especially those who want their fruit firm

Stage 7 Yellow with spots, perfect flavour and softness for eating

27 Feasibility Report for Setting-up Integrated Cold Chain for Banana in Tamil Nadu

3.1.4. Grades and Criteria According to Codex and Agmark standards banana is classified into following classes:

Table 3.3: Showing grade designation of banana as per AGMARK standards

Grade designation Grade requirements Grade tolerancesExtra class Bananas shall be of superior quality. They

must be characteristic of the variety and/or commercial type. The fingers must be free of defects, with the exception of very slight superficial defects, provided these do not affect the general appearance of the produce, quality, the keeping quality and presentation in the package.

5% by number or weight of bananas not satisfying the requirements of the class

Class I Bananas shall be of good quality. They must be characteristic of the variety and/or commercial type.

The following slight defects of the fingers, however, may be allowed, provided these do not affect the general appearance of the produce, quality, the keeping quality and presentation in the package.

- slight defects in shape and colour;

- slight defects due to rubbing and other superficial defects not exceeding 2 sq.cm. of the total surface area

10% by number or weight of bananas not satisfying the requirements of the class

Class II The defects must not affect the flesh of the fruit.

This includes bananas which do not qualify for inclusion in the higher classes, but satisfy the minimum requirements.

The following defects may be there, provided the bananas retain their essential characteristics as regards the quality, the keeping quality and presentation.

- defects in shape and colour provided the product remains the normal characteristics of bananas;

- skin defects due to scrapping, scabs, rubbing, blemishes or other causes not exceeding 4 sq.cm. of the total surface area; The defects must not affect the flesh of the fruit

10% by number or weight of bananas not satisfying the requirements of the class, nor the minimum requirements. With the exception of produce affected by rotting, major imperfections or any other deterioration rendering it unfit for human consumption

28 Confederation of Indian Industry

3.1.5. Size of Banana Size of banana is an important aspect in the trade. Size of banana varies depending on the variety.

According to codex standard, normally applicable to Cavendish groups

For the purposes of sizing bananas, the length of the fingers is determined along the outside curve ��

from the blossom end to the base of the pedicel where the edible pulp ends and the diameter is defined as the thickness of a transverse section between the lateral faces. The reference fruit for measurement of the length and grade is:

for hands, the median finger on the outer row of the hand,��

for clusters, the finger next to the cut section of the hand, on the outer row of the cluster.��

The minimum length should not be less than 14.0 cm and the minimum grade not less than ��

2.7 cm.

For all classes, a tolerance limit of 10% by number or weight of bananas not satisfying the sizing ��

characteristics, up to a limit of 1 cm for the minimum length of 14 cm is allowed.

3.2. World TradeBanana is the fourth most important staple crop in the world. It is critical for food security in many tropical countries. Globally, it ranks first in terms of volume and second after citrus in terms of value. It is consumed in almost all the countries of the world even though production is skewed and few countries account for bulk of the world’s production. Cavendish variety of banana is a crucial source of export income for many small countries. Since the 1900s, banana has played a central role in the economies of a number of countries especially in Central and Latin America. For at least 15 Latin American and Caribbean producer countries, several million people depend on the banana trade for their livelihood. About 20% of the 70 million tones of bananas produced each year enter world trade. Ironically, Brazil and India, the two biggest banana producing countries hardly have any significant share in the international banana trade.

Banana and plantain consumptions were maximum in African countries with 40-45kg/year/ individual as against 10.5 kg/year in India. Banana and plantain are the main staple food in East and West African countries. Most of the plantains grown in West Africa is exported to France and European markets. Thus banana and plantain cultivation forms the food security of the millions of people and also sustenance of the small and marginal farmers in African and Asian countries.

Out of the total world production of Banana of 90.7 million tons in 2009, only 14.6 million tons i.e. 16.1% of the banana was traded across countries. The world buyers of banana purchased a total volume of 13.92 million tones valued at US $ 9.888 billion in 2008. The industrialized countries are the major markets for banana and import about 80-85% of the banana, traded worldwide, with USA being the major buyer of banana with total import of 2.53 million tones or about 19.3% of total imports. In terms of value, Belgium is top importer of Bananas valued at 1.946 Billion Dollars even though quantity wise it is only 11.52% of total imports. The Latin American countries dominate the US market for banana. Other major importing countries of banana are Belgium, Japan, United Kingdom and Russia. Among Asian countries Japan and Russian Federation are the major importers. In parts of Europe and Middle East the banana market is growing, as increasing consumption trend is noted during the last few years.

29 Feasibility Report for Setting-up Integrated Cold Chain for Banana in Tamil Nadu

The world trade and top ten importing countries are mentioned in table 3.4.

Table 3.4: Top 20 importers of Banana in the World in 2010

Rank Area Quantity (tonnes) Value (1000 $) Unit value ($/tonne)1 United States of America 4114891 1974545 4802 Belgium 1351242 1532190 11343 Germany 1233712 873434 7084 Japan 1109068 842900 7605 United Kingdom 979397 732720 7486 Russian Federation 1068179 703536 6597 Italy 658391 494719 7518 France 549809 414634 7549 Iran (Islamic Republic of) 661390 392402 59310 Canada 495939 353877 71411 China 665230 246819 37112 Republic of Korea 337910 210269 62213 Poland 245476 198150 80714 Sweden 183496 178738 97415 Saudi Arabia 307420 176394 57416 Netherlands 222327 161689 72717 Austria 126151 127936 101418 Ukraine 151899 116162 76519 Argentina 351094 114365 32620 Czech Republic 161505 106319 658

The imports of Banana in the last three years both in Quantity and Value is shown at table 3.5. Banana imports seem to have stagnated around 13 to 14 million tons but in value terms there is an increase of 10% per annum. Year 2008 appears to be particularly high in value terms but part of it could be explained by weak US$ value in relation to other currencies.

Table 3.5: Trend in World Banana Imports Year 2006 2007 2008

Qty in Mts Value US$ 000’s

Qty in Mts Value US$ 000’s

Qty in Mts Value US$ 000’s

Total Imports 1,41,52,853 76,17,798 1,44,63,059 84,55,114 1,31,19,969 98,88,476Source: UNCOMTRADE

The top exporting countries are Ecuador, Belgium, Columbia, Costa Rica, USA, Germany, Guatemala, Philippines, and Dominican Republic. Out of these, Belgium, Germany, USA are re-exporters of Banana as they are not producing countries, excepting USA.

World exports of bananas also show a high level of concentration, with developing countries accounting for the bulk of exports. Although a number of African and Caribbean producers such as Cote d’lvoire, Cameroon and Martinique – have come to rely on banana exports, the largest exporters are the Latin American countries. The largest banana exporters’ bow includes Ecuador (18% of world trade), Costa Rica (12%), Colombia (12%), Honduras (11%), Philippines (11%) and Panama (9%). These six countries account for 73% of the world banana trade. Most of this trade is controlled by just a handful of firms for example,

30 Confederation of Indian Industry

United Brands (also Known as Chiquita) and Del Monte control nearly 40% of world banana trade. The Asian countries have a meager share of approximately 0.04%, with Philippines having the biggest share. The details of the world banana export and top ten exporting countries are given in Figure 3.1

Figure 3.1: Top exporters of Banana in World in 2010

The USA and European Union are the major consumers with consumption being on rise in USA. However, in European Union very little increase is noticed during the decade. Other parts of Europe and Middle East have growing market for Banana. World export of banana has shown increase during the last decade, which was largely contributed by Latin America and Caribbean.

Banana Imports 2011, Source: UNCOMTRADE

Country Trade Value NetWeight (kg) Trade Quantity

Afghanistan $3,335,876 27,692,268 27,692,268

Albania $12,933,916 17,395,939 17,395,939

Algeria $188,732,034 245,285,019 245,285,019

Argentina $143,695,584 394,881,395 394,881,395

Armenia $15,441,397 11,025,713 11,025,713

Aruba $1,933,781 2,839,365 2,839,365

Australia $700,591 243,068 243,068

Austria $133,088,577 127,007,757 127,007,757

Azerbaijan $23,556,353 23,089,947 23,089,947

Bahamas $5,213,129 1,014,136 1,014,136

Bahrain $12,464,909 15,651,092 15,651,092

31 Feasibility Report for Setting-up Integrated Cold Chain for Banana in Tamil Nadu

Country Trade Value NetWeight (kg) Trade Quantity

Barbados $1,494,115 3,573,825 3,573,825

Belarus $29,420,500 40,073,760 40,073,760

Belgium $1,623,210,791 1,403,156,926 1,403,156,926

Bermuda $513,323 647,664 647,664

Bhutan $78,891 438,247 438,247

Bolivia (Plurinational State of) $1,690 353 353

Bosnia Herzegovina $21,504,598 38,033,632 38,033,632

Botswana $5,043,775 6,618,626 6,618,626

Brazil $35,824 5,488 5,488

Bulgaria $42,412,338 49,652,546 49,652,546

Burkina Faso $89,901 2,920,000 2,920,000

Canada $388,632,959 506,659,506 506,659,506

Cape Verde $140 35 35

Chile $54,856,221 380,691,736 380,691,736

China $401,728,003 818,674,659 818,674,659

China, Hong Kong SAR $42,504,887 88,295,882 88,295,882

China, Macao SAR $1,520,273 2,538,752 2,538,752

Colombia $4,049,278 45,249,233 45,249,233

Costa Rica $12,807,378 24,804,352 24,804,352

Côte d'Ivoire $120 18 18

Croatia $38,691,586 48,650,751 48,650,751

Cyprus $6,476,759 4,964,629 4,964,629

Czech Rep. $126,457,959 148,934,990 148,934,990

Denmark $83,685,819 81,280,045 81,280,045

Dominican Rep. $781 985 985

Ecuador $8,721 19,327 19,327

Egypt $13,792,149 17,401,676 17,401,676

El Salvador $12,668,307 107,023,094 107,023,094

Estonia $11,481,833 11,490,020 11,490,020

Ethiopia $808 788 788

Finland $90,354,233 74,320,918 74,320,918

France $458,676,489 582,221,600 582,221,600

French Polynesia $5,047 761 761

Gambia $1,712 1,800 1,800

32 Confederation of Indian Industry

Country Trade Value NetWeight (kg) Trade Quantity

Germany $987,104,925 1,295,136,950 1,295,136,950

Ghana $9,752 20,737 20,737

Greece $121,151,157 139,584,220 139,584,220

Greenland $97,829 43,545 43,545

Guatemala $508,824 5,327,288 5,327,288

Guyana $86 10 10

Hungary $56,492,000 61,272,100 61,272,100

Iceland $6,266,130 5,889,856 5,889,856

India $625 820 820

Indonesia $849,998 1,631,045 1,631,045

Iran $409,672,474 615,879,444 615,879,444

Ireland $68,216,698 87,521,892 87,521,892

Israel $51,000 10,571 10,571

Italy $550,939,321 668,061,079 668,061,079

Japan $905,705,379 1,064,745,781 1,064,745,781

Jordan $35,688,213 48,263,193 48,263,193

Kazakhstan $27,504,675 44,832,040 44,832,040

Kyrgyzstan $7,410,480 11,528,372 11,528,372

Latvia $22,244,581 24,069,840 24,069,840

Lebanon $74,878 185,062 185,062

Lithuania $27,825,147 33,162,129 33,162,129

Luxembourg $8,802,115 4,963,688 4,963,688

Malawi $3,018 1,941 1,941

Malaysia $837,481 2,084,125 2,084,125

Maldives $565,647 990,508 990,508

Malta $7,395,959 5,845,418 5,845,418

Mauritania $307,612 2,542,649 2,542,649

Mauritius $39 5 5

Mexico $223,188 114,932 114,932

Montenegro $4,434,103 7,460,407 7,460,407

Mozambique $55,000 591,396 591,396

Namibia $4,441,315 4,576,808 4,576,808

Nepal $508,168 16,722,410 16,722,410

Netherlands $244,056,958 308,799,189 308,799,189

33 Feasibility Report for Setting-up Integrated Cold Chain for Banana in Tamil Nadu

Country Trade Value NetWeight (kg) Trade Quantity

New Caledonia $12,903 1,725 1,725

New Zealand $62,039,978 86,798,914 86,798,914

Nicaragua $291,068 6,713,620 6,713,620

Niger $261,187 3,699,871 3,699,871

Nigeria $2,247,053 1,096,051 1,096,051

Norway $90,274,243 78,221,439 78,221,439

Oman $6,325,649 13,740,002 13,740,002

Pakistan $277 251 251

Panama $23,168 7,792 7,792

Paraguay $78,022 388,301 388,301

Poland $181,395,698 231,053,549 231,053,549

Portugal $106,468,087 144,904,629 144,904,629

Qatar $16,476,845 24,779,358 N/A

Rep. of Korea $245,521,571 352,670,762 352,670,762

Rep. of Moldova $8,446,555 12,192,613 12,192,613

Romania $44,577,352 54,249,485 54,249,485

Russian Federation $950,432,729 1,307,599,929 1,307,599,929

Rwanda $174,368 1,916,068 1,916,068

Saint Kitts and Nevis $15,377 35,052 35,052

Senegal $7,586,888 14,318,126 14,318,126

Serbia $39,273,375 52,435,092 52,435,092

Singapore $19,753,519 41,584,668 41,584,668

Slovakia $53,089,572 54,810,881 54,810,881

Slovenia $47,187,564 67,476,361 67,476,361

South Africa $12,559,283 52,266,519 52,266,519

Spain $152,547,571 212,202,881 212,202,881

Sri Lanka $20,492 55,268 55,268

Sweden $168,865,796 174,734,903 174,734,903

Switzerland $107,769,497 79,394,798 79,394,798

TFYR of Macedonia $12,523,748 19,086,918 19,086,918

Thailand $2,345,888 10,568,330 10,568,330

Tunisia $11,865,960 41,338,077 41,338,077

Turkey $110,436,179 234,632,778 234,632,778

34 Confederation of Indian Industry

Country Trade Value NetWeight (kg) Trade Quantity

Turks and Caicos Isds $791,948 1,067,452 1,067,452

Uganda $425 172 172

Ukraine $152,617,460 247,824,961 247,824,961

United Kingdom $836,574,079 1,073,126,090 1,073,126,090

United Rep. of Tanzania $57 81 81

USA $2,326,686,875 4,397,475,105 4,397,475,105

Vanuatu $118 31 31

Zambia $174,678 377,641 377,641

3.3. Banana Trade in India

3.3.1. Export MarketIndia while being the largest producer of Banana at about 28% of world production does not account as one of the Banana trading nations of the world. The total exports of Banana from India are about 0.03 million tons out of the total world exports of 14.58 million tons. i.e. 0.2% of World trade.

Indian exports of banana in the last three years are shown at table 3.6.

Table 3.6: Indian Exports of Banana in 2011-12

Sr No. Country Qty Value

1 U Arab Emts 1,51,33,609.00 37,94,20,734.00

2 Saudi Arab 50,13,961.00 12,46,03,406.00

3 Iran 41,26,123.00 9,50,94,209.00

4 Kuwait 31,95,585.00 7,17,65,328.00

5 Baharain Is 24,36,678.00 5,83,61,689.00

6 Nepal 97,65,991.00 5,14,38,613.00

7 Qatar 20,53,138.00 4,93,40,210.00

8 Oman 22,28,150.00 4,85,05,499.00

9 Maldives 9,12,546.00 1,77,98,040.00

10 Korea Rp 1,47,000.00 46,64,546.00

Total 4,50,12,781.00 90,09,92,274.00

Source: NHB

35 Feasibility Report for Setting-up Integrated Cold Chain for Banana in Tamil Nadu

The share of Banana in fresh fruit exports has declined in 2011-12, perhaps because of low pricing in the International Markets (table 3.7). The banana share was only 1.93% by quantity and 2.09% by value in 2009-10 but has gone up to 8.38% by quantity and 3.99% by value in the year 2011-12.

Table 3.7 : Share of Banana in fresh fruit exports from India

Description 2009-2010 2010-2011 2011-2012Qty in Mts Value Rs

LakhsQty in Mts Value Rs

LakhsQty in Mts Value Rs

LakhsAll Fresh fruits 2,60,678 52,278 2,54,900 49,598 2,56,767 73,583Bananas 5,049 1,093 34,711 8,119 21,525 2,939Banana % 1.93 2.09 13.62 16.37 8.38 3.99

There is good export market for banana particularly to the countries/places like U.A.E., Dubai, Sharjah and Abu Dhabi, Sultanate of Oman, Kuwait, Saudi Arabia, Qatar, Bahrain and other gulf countries; also Singapore, Nepal, Sri Lanka, Malaysia and so on.

3.3.2. Domestic TradeMost of the trade of Banana is domestic in nature as 99.8% of banana produced in the country is consumed locally. Banana has wide acceptance across the regions and religions in India.

Banana trade is highly unorganized and mostly undertaken by traders who do not invest in any infrastructure.

The data of arrivals recorded in important markets across India in the year 2009 is shown at table 3.8.

Table 3.8: All India market arrivals of fresh Banana in 2009 (Source: Ag Market)

S.NO Center Name ARRIVALS1 ABOHAR 8902 AGRA 11,8903 AHMEDABAD 13,7084 AMRITSAR 12,4755 BANGALORE 82,2186 BARAUT 2,7637 BHOPAL 12,7358 BHUBANESHWAR 14,0239 CHANDIGARH 16,42410 CHENNAI 1,26,36111 DEHRADUN 4,22712 DELHI 1,58,02413 GANGATOK 90914 GUWAHATI 10,164

36 Confederation of Indian Industry

S.NO Center Name ARRIVALS15 HYDERABAD 44,20216 JAIPUR 32,84717 JAMMU 23,23718 KANPUR 34,65219 KOLKATA 48,56020 LUCKNOW 15,90021 MUMBAI 1,77,08822 NAGPUR 17,17023 NASIK 10,72724 PATNA 21,07525 PUNE 13,14026 RAIPUR 9,87527 RANCHI 12,21028 SHIMLA 2,03029 SRINAGAR 28,06530 SURAT 13,11531 TRIVENDRUM 5,807 Total 9,76,511

In the year 2009, total arrivals in all 31 markets are less than 1 million Mt, as compared to total banana production in the country at 26.17 million tonnes. It shows that about 95% of the produce is getting traded either in unregulated markets or in unorganized sector.

Within the 31 markets, Mumbai, Delhi, Chennai and Bangalore are the 4 markets showing maximum arrivals and accounting for more than 60% of total arrivals.

Intra year arrival distribution is shown at Table 3.9. Variation among the months exists, with lowest in the month of April at 58,089 Mts and highest in the month of September at 1,07,712 Mts. The ratio of highest to lowest is almost 1:2. But in most of the months there is no significant variation and shows that uniform demand exists.

Monthly prices at whole sale level and retail level recorded can be seen at Table 3.9. the price data indicates that on an average the whole sale prices recorded are at about 63% of the retail prices. Maximum prices recorded are in Chennai market. Prices are related to the variety and quality and as the data recorded are with out break up of variety and quality, no analysis can be made from the data.

There is a need to improve the arrivals of banana produced to regulated markets and in order to achieve these regulated markets need to be strengthened with suitable infrastructure.

37 Feasibility Report for Setting-up Integrated Cold Chain for Banana in Tamil Nadu

Table 3.9: Table showing Month wise arrivals at all 31 markets in the year 2009

MONTH Total Arrivals in all Centres

in MT

Max Arrival in any

centre in MT

Max Av Whole

sale price in any

centre Rs/MT

Max Av Retail price in any

centre in Rs/MT

Average Whole

sale price of all

centres Rs/MT

Average retail price in all

centres Rs/MT

Average arrival Per

Centre

January 78616 15218 2178 2739 869 1399 2536February 76611 15580 2239 2896 910 1456 2471March 86198 16777 2204 2939 958 1507 2781April 58098 9670 1938 3295 989 1587 1874May 73414 16485 2074 3333 1033 1706 2368June 81853 18527 2435 3335 1014 1579 2640July 94374 19500 2957 3874 1107 1729 3044August 91170 19100 2204 3621 1123 1788 2941September 107712 17535 2283 3567 1181 1902 3475October 87929 14340 2226 3608 1151 1857 2836November 71745 14100 2237 3555 1097 1779 2314December 68791 9594 2195 3506 1112 1753 2219TOTAL 976511

Source: AGNET

The main markets and their collection and supply blocks in India are shown at Table 3.10. Thus in each of the important states like Tamil Nadu, Maharashtra, Andhra Pradesh, Madhya Pradesh, Karnataka, only 3 to 4 main markets are prevalent even though the production is more wide spread.

3.10: Main Markets and feeding blocks for Banana in India

States Market BlocksMaharashtra Jalgaon Chopda, Yaval, Raver, Edalbad, Bhusawal, Jamner, Pachora,

Bhadgaon, Chalisgaon, Parola, Amainer, BoradiDhule Shirpur, Sindhkheda, Sakri, Nardana, Boradi, SangviBuldhana Malkapur, Khamgaon, Mehekar, Chikhli

Tamil Nadu Thiruchirapalli Turaiyur, Thottiyam, Musiri, Manachanallur, Lalgudi, SrirangamCoimbatore Muttuppalaiyam, Avinashi, Tiruppur, Palladam, Udumallaip

pettai, Pollachi, ValparaiTheni Periyakulam, Andipatti, Uttammapalayam, Bodimayakkanur,

Kamban, Megamali, Vadugapatti

38 Confederation of Indian Industry

States Market BlocksMadhya Pradesh

Khandwa Harsud, Pandhana, Nepanagar, BurhanpurDhar Badnawar, Sardarpur, Gandhqwani, Manaawr, Kukshi,

DharmapuriBadwani Thikri, Rajpur, Newali, Pansemal, Sendwa

Andhra Pradesh Guntur Tangeda, Dachepalle, Piduguralla, Sattenapalie, Vinkoda, Ponnuru, Bapatia, Narasaraopet, Purti, Prattipadu, Pallapatla.

Vijayanagaram Parvatipuram, Bobblli, Gajapatinagaram, Chipurupalla, SalurPrakasham Erragondapalem, Markapur, Giddalur, Tarlupadu, Podile, Darsai,

Baulipali, ChundiGujarat Surat Mangrol, Umarwada, Mandvi, Vyara, Valod, Mahuva, Palsana,

Kamrej, Olpad, Nizer, Vadoli, UnalAnand Sojitra, Sarsa, Sunav, Undel, Lunej, Ras, Kantha, Morai, Vadtal,

Bochasan, Dhuwaean, Khambhat, Rohoni, WadgamKarnataka Uttar Kannad Maliyal, Mundgod, Yellapur, Sirsi, Siddapur, Bhatkal, Ankol

Udupi Kundapura, Kokkaroni, Karkal, Goligudelej, Chittur, Harmanu, Kokkaroni, Shivapura, Kodlamale, Yermal

In most of the places the trade follows the pattern as shown in Fig 3.3. The channel mainly consists of farmer, village level/Block level accumulator, Whole sale seller, Local resellers, Consumer. Some times, there could be more than one accumulator at block level and a semi wholesale distributor between reseller and whole sale seller. The channel is characterized by negligible or nil infrastructure, no value addition other than facilitation services and unscientific handling/logistics. The mark up is usually actual costs of handling, loss of produce in quantity/quality and profit margin. Since, the chain partner is able to pass on the loss of produce in quantity and quality at each level to next higher level or pass down to next lower level, all the burden of inefficiencies are carried by either farmers or consumers.

There are very few exceptions to this and these are in Bharuch in Gujarat, Jalgaon in Maharashtra, Theni in Tamil Nadu and few other places where export or retail revolution led infrastructure is created and available. The amount of Banana passing through such infrastructure will be less than 1% in quantity and 2% in value.

Fig 3.3: Banana Trade Channel

39 Feasibility Report for Setting-up Integrated Cold Chain for Banana in Tamil Nadu

3.3.3. Domestic Consumption:Average banana consumption as per NSS survey is shown in Figure 3.4. As can be seen the banana consumption varied at 2-3 nos per capita in Rural areas and 4-5 Nos per capita in Urban areas.

Fig 3.4: Per Capita Banana Consumption in 30 Days

Source: NSS Survey

Assuming that the consumption numbers are still holding well, the total market for banana in urban areas for population of 35 Crores at 50 nos per year is 1750 Crore numbers and in Rural areas for a population of 65 Crores at 27 Nos per year is 1755 Crore numbers. The demand is almost equal in both areas in terms of numbers. It may vary in terms of quantity to some extent and value to a large extent because of the unit sizes and unit values will be higher in urban areas.

Table 3.11: Per capita Consumer Expenditure on Fruits and Food in 30 days

Year URBAN RURALFruits Exp in

Rs in 30 Days

Total Food Exp in Rs in 30 days

Fruits & Nuts as %

of Total Exp

Food Exp as % of Total

Exp

Fruits Exp in

Rs in 30 Days

Total Food Exp in Rs in 30 days

Fruits & Nuts as % of

Total Exp

Food Exp as % of Total

Exp1987-88 6.27 139.73 2.51 55.91 2.57 100.82 1.63 63.771993-94 12.2 250.3 2.63 53.91 4.90 177.80 1.71 62.151999-00 20.68 410.84 2.42 48.06 8.36 288.80 1.72 59.402004-05 23.65 447.41 2.14 40.50 10.42 307.60 1.80 53.11

40 Confederation of Indian Industry

Year URBAN RURALFruits Exp in

Rs in 30 Days

Total Food Exp in Rs in 30 days

Fruits & Nuts as %

of Total Exp

Food Exp as % of Total

Exp

Fruits Exp in

Rs in 30 Days

Total Food Exp in Rs in 30 days

Fruits & Nuts as % of

Total Exp

Food Exp as % of Total

Exp2005-06 25.52 467.82 2.18 39.96 11.75 333.15 1.88 53.342006-07 28.00 517.25 2.13 39.41 12.47 363.42 1.79 52.282007-08 31.02 582.43 2.11 39.58 13.56 404.33 1.76 52.35

Source: NSS surveys

The trend in per capita consumer expenditures as per National Sample Surveys is shown at Table 3.11. While the share of expenditure on food is falling continuously both in rural areas and urban areas, the expenditure on fruits is increasing with in the food expenditure and maintaining its share in overall expenditure. This shows that the Banana market will increase at the same rate of growth in incomes and GDP in future.

With consumers becoming more demanding in terms of presentation, quality, the market for ��

banana in India will be a growing market requiring matching infrastructure to process and distribute with in the country.

3.4. Banana Trade in Tamil NaduBanana trade in Tamil Nadu is similar to all India situation in all aspects, be it trade channels, arrivals at markets, availability of the processing facilities etc.

The banana produced in Tamil Nadu is consumed substantially in the local areas and limited quantities get transported to other states such as Kerala, Karnataka and to a small extent to Andhra Pradesh. Mostly the production in southern districts of Tamil Nadu goes to Kerala; production from North western districts goes to Karnataka state.

The arrivals in markets are very less compared to the actual production. For example the arrivals reported in Theni market are as follows:

Table 3.10 Arrival Particulars of Banana in Theni Market (Source: Web site of TNAMB)

S.No. Particulars Quantity1 Production 70880 Mt2 Unit of measurement in market One Bunch3 Averege price per unit Rs 604 Arrivals

4.1 Max Arrivals per day 404.2 Min Arrival per day 04.2 Average per day 204.4 Arrivals in 2002-03 60,0004.5 Arrivals in 2003-04 500004.6 Arrivals in 2004-05 45000

41 Feasibility Report for Setting-up Integrated Cold Chain for Banana in Tamil Nadu

Similarly the banana growers associations (12 in Tamil Nadu) have formed a federation to link the banana production to the export market. The farmer associations are planning to brand the produce as TAN MANGO / TAN BANANA and market the same in the domestic and international markets (on the lines of Mahagrape and Mahabanana in Maharashtra)

According to the discussions with Banana traders in Koyambedu fruit market in Chennai, the Koyambedu market receives on an average 40 to 60 truckloads of banana fruit per day. This can go as high as 150-160 truckloads during festival seasons like Vijayadashmi and Pongal at worst 20-30 truck loads even in the lean/dry periods. Each truckload contains 450 to 500 bunches. The arrivals are from a specific region in specific months. For example more arrivals in September are seen from Cuddalore region, in October from Vellore region, in January from Tiruchi. The unloading and loading charges are at Rs.750 per truck.

Processing infrastructure available in Tamil Nadu is negligible. Only notable infrastructure available is Farm fresh unit in Theni district. There are also some multi produce pack houses in Tamil Nadu. Unlike in other states, setting up small ripening chambers at producing centers has not picked up in Tamil Nadu, in spite of having largest production in the country. In the banana processing sector, only 3-4% of the total production is processed. The banana processed products mainly consists of banana chips which is produced to a tune of over one lakh tons a year. Majority of the chips are produced from Nendran banana, however, Robusta and Monthan banana fruits are also being processed as chips to some extent. There are no units producing other banana products popular in the market such as banana puree and powder.

The main issues regarding lack of exports from the state are:

Lack of market intelligence��

Information of production estimates is required at a block and district level variety wise at a quarterly level.

Lack of a transparent price discovery mechanism��

The price discovery is very arbitrary and Electronic or mannual Auction markets exist at present.

Lack of adequate post harvest infrastructure��

There is inadequate post harvest infrastructure, especially pack houses, cold stores, refrigerated vans and market infrastructure

42 Confederation of Indian Industry

4 SWOT Analysis for TN Banana Business

Strength, weaknesses, opportunities and threats analysis is undertaken to understand the situation in Tamil Nadu so as to arrive at the required infrastructure and systems to develop the sector. In order to have more detailed analysis the banana sector SWOT analysis is undertaken at the following aspects:

Policy frame work��

Varieties��

Pre harvest practices��

Post harvest practices��

Infrastructure and ��

marketing aspects��

4.1. Strengths1. Well established Institutional network in Tamil Nadu: Presence of leading institutions like Tamil

Nadu agricultural University (TNAU), Tamil Nadu Horticulture Department, Tamil Nadu State Horticulture Mission and National Research Centre for Banana and other Institutions.

2. Central and State Government policies facilitating growth of the sector such as Micro Irrigation subsidies, Subsidies for Tissue culture seedlings, Crop Loans and other agriculture credit, regulated market yards etc. (TANFLORA, AEZs).

3. Tamil Nadu has one of the largest numbers of varieties being produced in the country. India being one of the centre of diversity and one of the hot spot for the wild Musa species and gives wide choices for farmers to grow.

4. Adequate supply of quality plantlets and seedlings both from Government and private sources

5. Favorable Agro climatic conditions to grow different varieties of banana.

6. Enthusiastic and progressive farmers and farming community well versed in farming techniques and receptive to the newer ideas and cultivation practices, improved or newer varieties.

43 Feasibility Report for Setting-up Integrated Cold Chain for Banana in Tamil Nadu

7. Adequate local and domestic demand for all varieties

8. Growing awareness of bananas’ nutritional and medicinal values have encouraged the export of non-traditional banana varieties other than Cavendish banana.

9. The intensive cultivation practices with higher productivity and availability in different regions could be strength for the export of bananas through out the year from different regions of cultivation.

10. In India, since polyclonal system is followed, in a growing system which varies under different climatic conditions, banana and plantain production can be made free from sudden out break of diseases and viruses and also break down of resistant which have been observed in the monoclonal system of planting of Cavendish group of banana.

11. Availability of wild relatives of Musa is the latest strength for banana conservation activities.

12. High genetic diversity can provide an opportunity for selection of superior clones from the population.

13. Banana can be grown in any season and the fruits will be available throughout the year providing an opportunity for export of banana to the foreign markets throughout the year.

4.2. Weaknesses1. Too many varieties leading to spread of resources, difficulties in introducing modern systems.

2. Cavendish variety being the most accepted variety internationally, no immediate acceptance for other varieties in Export markets.

3. There is a lack of awareness on Hi-tech cultivation of Banana and quality consciousness among growers

4. Lack of Adherance to phyto-sanitary standards hinders acceptance in foreign markets.

5. The presence of small land holdings hampers adoption of best practices and certifications under Global Gap, pesticide residue testing, organic certification etc.

6. Lack of price discovery mechanism often leads to wide fluctuation in market prices.

7. There is low focus on post harvest management and inadequate facilities like cold storage, pre-cooling and waxing centers, processing units etc.

8. The marketing channels are not well developed and lot of produce gets lost in post harvest handling.

9. India being the largest producer of banana in the world, and the average productivity is less as compared to the states which have recorded the maximum productivity of 60-70 tons per / hectare. This is due to growing of low-yielding local cultivars and non-adoption of improved production and protection technologies.

10. Regional problems and consumer preferences leading to low productivity.

44 Confederation of Indian Industry

11. Non availability of high yielding cultivars other than Cavendish group with resistance to wilt is one of the major constraints of production. In addition, biotic stresses like wilt and leaf spot diseases, nematode and viruses for the major threats in reducing the productivity and also sustainability.

12. No concerted efforts have been made to evolve improved varieties which are resistance to these biotic stresses so that the productivity can be improved with minimum cost.

13. The land holdings being small, the farmers could not adopt better post harvest handling methods so that these losses could be minimized.

14. Lack of infrastructure facilities like cold storage, reefer van facility for transportation and better marketing facilities required to minimize the losses.

15. Not having well developed banana marketing, resulting in farmers not getting remunerative prices during the glut seasons. The farmers are forced to sell at throw away prices due to its perishable nature and not having infrastructure to balance the peaks and lows of supply with peaks and lows of demand.

16. Development of value addition is one of the weak areas which need further strengthening and commercial exploitation.

17. Commodity specific markets are not available which is one of the weaknesses in the marketing links.

4.3. Opportunities1. Growing per capita incomes and changing production patterns of other main food crops like rice,

wheat is an opportunity to increase the production significantly

2. Changing consumer patterns by the upcoming retail chain stores is creating a premium segment that is willing to pay extra for quality, both physical and chemical.

3. Development of disease resistant varieties:

4. The field gene bank which could be further exploited in the breeding program.

5. Large tracts of dry lands / rain fed areas / waste lands can be utilized for promotion of horticulture.

6. Scope for removal of production constraints due to the varying production systems and cultivation of bananas from coastal region to hill region.

7. Availability of ethnic Indian population in many countries with ready market for non Cavendish varieties and ability of Tamil Nadu to produce different varieties of banana due to poly clonal cultivation.

8. Availability of business opportunity to create a niche market for a variety having huge differentiation to Cavendish variety in colour, size, taste and properties such as red Banana internationally similar to New Zealand efforts for Kiwi fruit.

9. Large potential to set up processing industries, specially that give value to the whole fruit and plantation like waste and discarded fruit based flour product.

45 Feasibility Report for Setting-up Integrated Cold Chain for Banana in Tamil Nadu

10. Strategic location to tap export opportunities to the Far East.

11. Well poised to capture the increasing demand in developed countries for Green foods/Organic foods as traditional low use of pesticides, fertilizers and traditional and non chemical methods of disease control and use of organic fertigation.

12. Exploiting the contract farming legal frame work to avoid uncertainties of market price besides getting right quality inputs.

13. After the WTO regime and opening up of the banana trade, there are enhanced opportunities for export of banana to UK and US markets due to cheap production cost and availability of organic bananas.

4.4. Threats1. High post harvest losses, estimated to be 20-30%. The resulting monetary loss is borne by the

farmers who are at bottom of pyramid.

2. Valuable genetic resources in the form of wild Musa species and other related species are being lost due to the de-forestation, Jhum cultivation and urbanization in the centre of diversity viz., North Eastern region.