survey of key data - raiffeisen banka · pdf filesurvey of key data raiffeisen banka a.d. 2007...

TRANSCRIPT

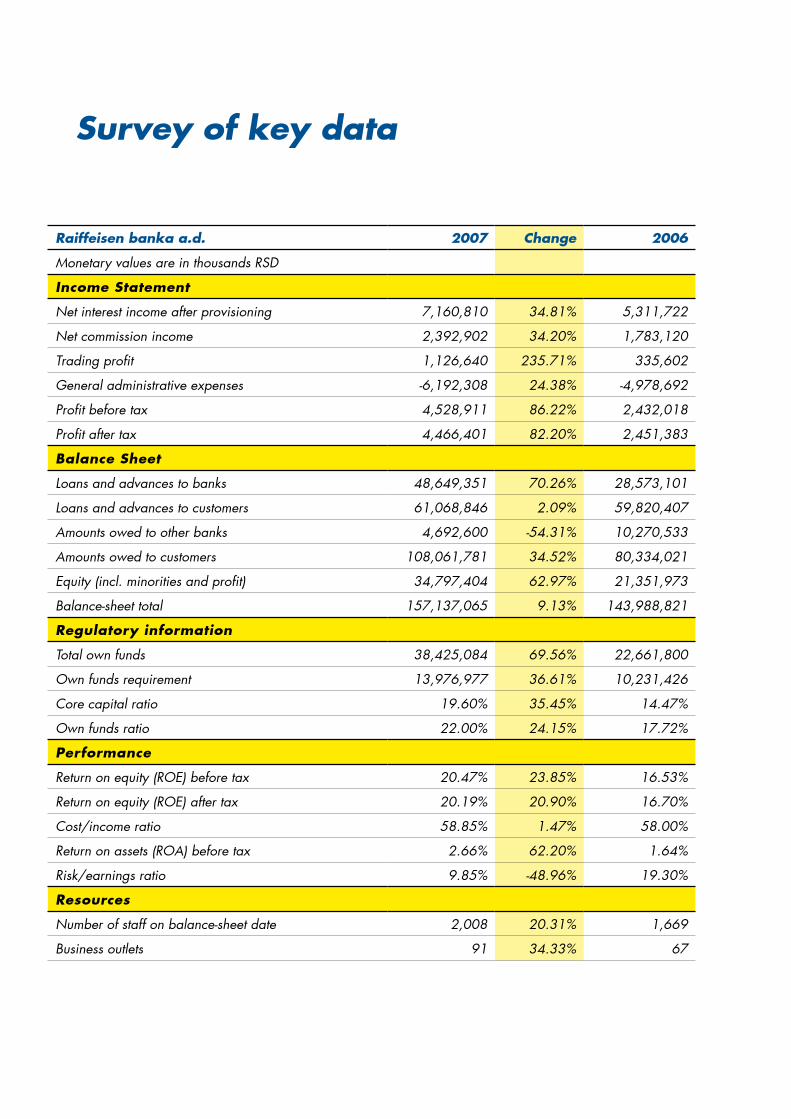

Survey of key data

Raiffeisen banka a.d. 2007 Change 2006

Monetary values are in thousands RSD

Income Statement

Net interest income after provisioning 7,160,810 34.81% 5,311,722

Net commission income 2,392,902 34.20% 1,783,120

Trading profit 1,126,640 235.71% 335,602

General administrative expenses -6,192,308 24.38% -4,978,692

Profit before tax 4,528,911 86.22% 2,432,018

Profit after tax 4,466,401 82.20% 2,451,383

Balance Sheet

Loans and advances to banks 48,649,351 70.26% 28,573,101

Loans and advances to customers 61,068,846 2.09% 59,820,407

Amounts owed to other banks 4,692,600 -54.31% 10,270,533

Amounts owed to customers 108,061,781 34.52% 80,334,021

Equity (incl. minorities and profit) 34,797,404 62.97% 21,351,973

Balance-sheet total 157,137,065 9.13% 143,988,821

Regulatory information

Total own funds 38,425,084 69.56% 22,661,800

Own funds requirement 13,976,977 36.61% 10,231,426

Core capital ratio 19.60% 35.45% 14.47%

Own funds ratio 22.00% 24.15% 17.72%

Performance

Return on equity (ROE) before tax 20.47% 23.85% 16.53%

Return on equity (ROE) after tax 20.19% 20.90% 16.70%

Cost/income ratio 58.85% 1.47% 58.00%

Return on assets (ROA) before tax 2.66% 62.20% 1.64%

Risk/earnings ratio 9.85% -48.96% 19.30%

Resources

Number of staff on balance-sheet date 2,008 20.31% 1,669

Business outlets 91 34.33% 67

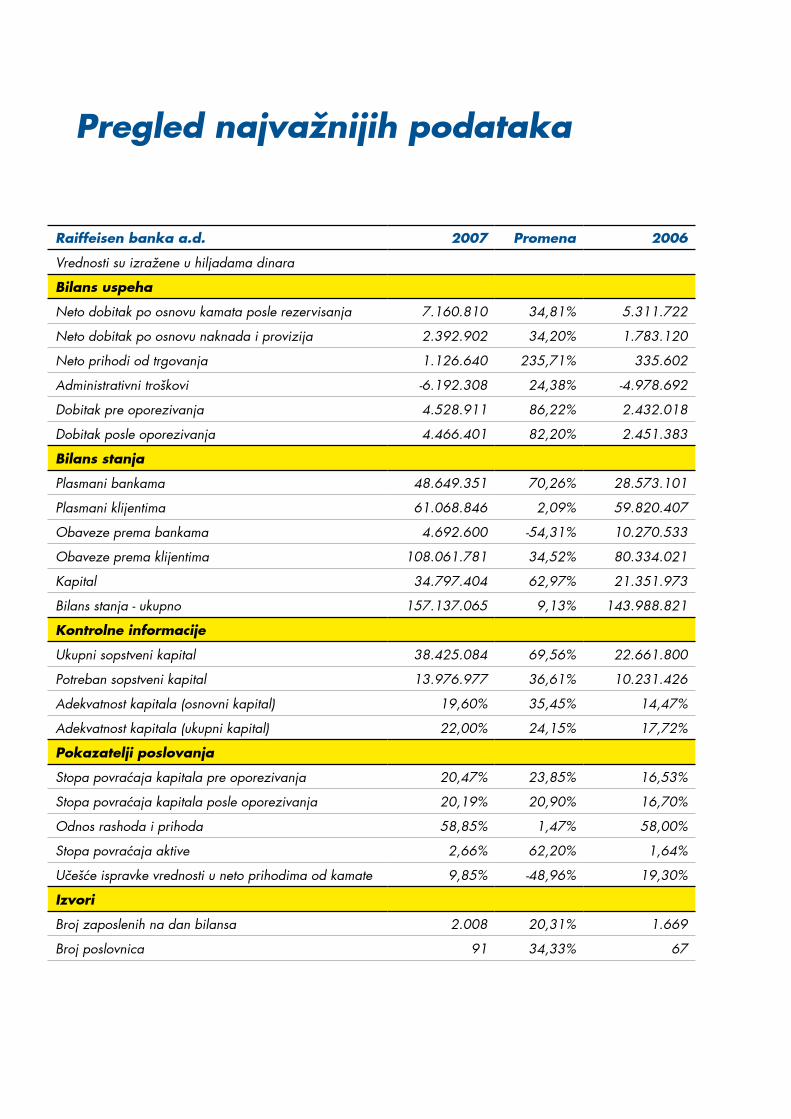

Pregled najvažnijih podataka

Raiffeisen banka a.d. 2007 Promena 2006

Vrednosti su izražene u hiljadama dinara

Bilans uspeha

Neto dobitak po osnovu kamata posle rezervisanja 7.160.810 34,81% 5.311.722

Neto dobitak po osnovu naknada i provizija 2.392.902 34,20% 1.783.120

Neto prihodi od trgovanja 1.126.640 235,71% 335.602

Administrativni troškovi -6.192.308 24,38% -4.978.692

Dobitak pre oporezivanja 4.528.911 86,22% 2.432.018

Dobitak posle oporezivanja 4.466.401 82,20% 2.451.383

Bilans stanja

Plasmani bankama 48.649.351 70,26% 28.573.101

Plasmani klijentima 61.068.846 2,09% 59.820.407

Obaveze prema bankama 4.692.600 -54,31% 10.270.533

Obaveze prema klijentima 108.061.781 34,52% 80.334.021

Kapital 34.797.404 62,97% 21.351.973

Bilans stanja - ukupno 157.137.065 9,13% 143.988.821

Kontrolne informacije

Ukupni sopstveni kapital 38.425.084 69,56% 22.661.800

Potreban sopstveni kapital 13.976.977 36,61% 10.231.426

Adekvatnost kapitala (osnovni kapital) 19,60% 35,45% 14,47%

Adekvatnost kapitala (ukupni kapital) 22,00% 24,15% 17,72%

Pokazatelji poslovanja

Stopa povraćaja kapitala pre oporezivanja 20,47% 23,85% 16,53%

Stopa povraćaja kapitala posle oporezivanja 20,19% 20,90% 16,70%

Odnos rashoda i prihoda 58,85% 1,47% 58,00%

Stopa povraćaja aktive 2,66% 62,20% 1,64%

Učešće ispravke vrednosti u neto prihodima od kamate 9,85% -48,96% 19,30%

Izvori

Broj zaposlenih na dan bilansa 2.008 20,31% 1.669

Broj poslovnica 91 34,33% 67

Report by the Chairman of the Board of Directors 6

Introductory Address by the Chairman of the Managing Board 8

The RZB Group and Raiffeisen International at a glance 14

Macroeconomic Enviroment, Opportunities for Foreign Investors and Prospects 18

Corporate Social Responsibility: Donation to Foster Home “Spomenak”, Pančevo 26

Corporate Banking 30

Consumer Banking 38

Small Enterprises and Micro Business 44

Treasury and Investment Banking 48

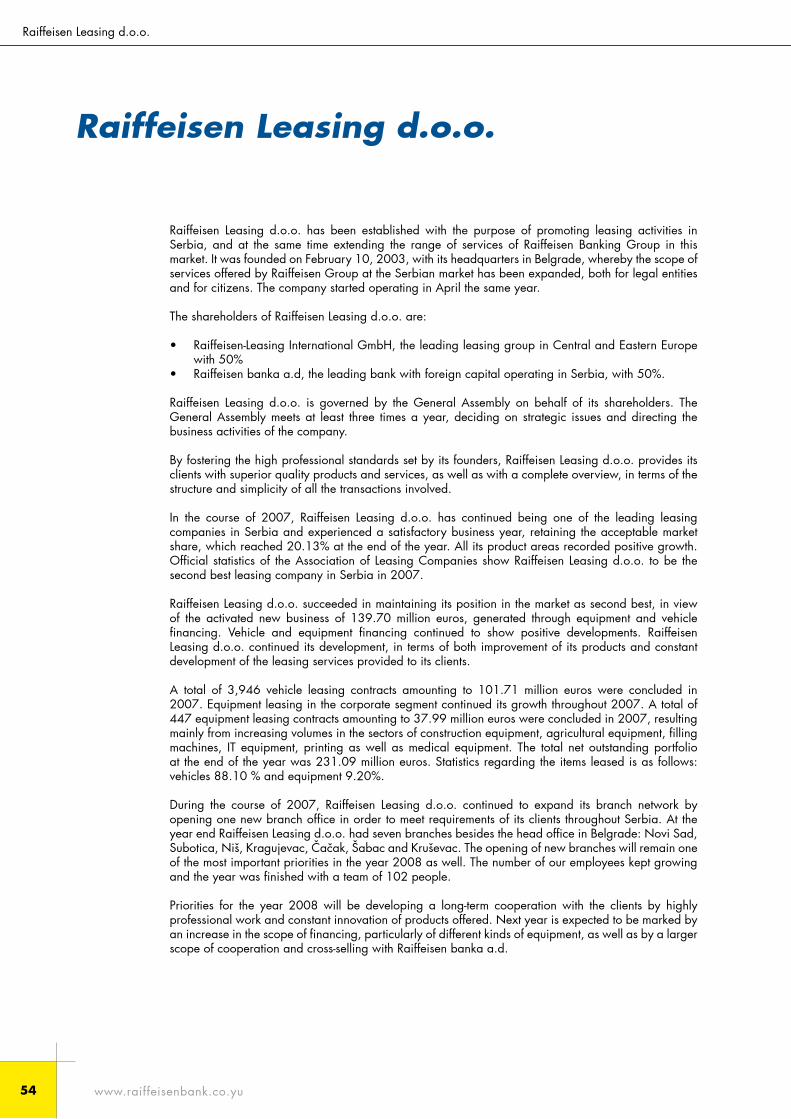

Raiffeisen Leasing d.o.o. 54

Raiffeisen Future 58

Raiffeisen Invest 62

Branch Network 64

Organization Structure 66

Maps 68

Addresses 70

Financial Statements

Independent Auditor’s Report 81Income Statement for the year ended 31 December 2007 82Balance Sheet as at 31 December 2007 83Statement of Changes in Equity for the year ended 31 December 2007 84Cash Flow Statement for the year ended 31 December 2007 85Notes to Financial Statements 86

Contents

Izveštaj predsednika Upravnog odbora 7

Uvodna reč predsednika Izvršnog odbora 9

Kratak osvrt na RZB grupaciju i Raiffeisen International 15

Makroekonomsko okruženje, mogućnosti za strane investitore i perspektive 19

Društveno odgovorno ponašanje: donatorska akcija za dom “Spomenak”, Pančevo 27

Poslovanje sa privredom 31

Poslovanje sa stanovništvom 39

Poslovanje sa malom privredom 45

Sredstva i investiciono bankarstvo 49

Raiffeisen Leasing d.o.o. 55

Raiffeisen Future 59

Raiffeisen Invest 63

Mreža filijala 64

Organizaciona struktura banke 66

Mape 68

Adrese 70

Finansijski izveštaj

Nezavisno mišljenje revizora 81Bilans uspeha za godinu završenu 31. decembra 2007. 82Bilans stanja na dan 31. decembra 2007. 83Promene na kapitalu za godinu završenu 31. decembra 2007. 84Bilans tokova gotovine za godinu završenu 31. decembra 2007. 85Napomene uz finansijske izveštaje 86

Sadržaj

� www.raiffeisenbank.co.yu

On behalf of the Board of Directors of Raiffeisen banka, I am very pleased to state that 2007 was another successful business year for the bank. The extraordinary results achieved in 2007, mirrored, among others, by the profit that nearly doubled, have a special significance, considering that they were accomplished in market conditions that brought new challenges and requirements for the bank.

As a universal bank, Raiffeisen banka firmly adhered to its determination to satisfy the requirements of its clients in a full and efficient manner, developing partner relations with them on a longstanding basis, and introducing new products, as well as innovating the existing ones. As a result, the bank managed to maintain the continuity of success of its operation, remaining synonymous of leadership in the country’s banking sector.

The development of the network, the high standard of the banking services and the permanent advanced professional training of the employees, also contributed to the fact that a large number of clients opted for Raiffeisen banka as their business bank.

The continuing success of Raiffeisen banka is also due to the fact that it is a member of the Raiffeisen International Group, one of the leading banking groups in Central and Eastern Europe, as well as due to the significant support provided by the Group’s majority owner Raiffeisen Zentralbank Österreich AG, Vienna.

A confirmation of the success of Raiffeisen banka and the whole Group is the series of awards received in 2007, as in the years before. Raiffeisen banka was declared “Best Bank” by many eminent magazines: The Banker (for the third time in a row, and fourth in total), Euromoney (for the sixth time in a row) and Global Finance (for the fourth consecutive time).

The bank’s staff and management and I, personally, were profoundly grieved by the demise of Budimir Boško Kostić, Deputy Chairman of the Board of Directors. We all have lost a precious associate and close friend, while the bank will miss an extraordinary colleague and expert, who has made an invaluable contribution to the business success we have had so far.

On behalf of the Board of Directors, I thank the management team and all employees for their hard work, high professionalism, expertise and team work that have made the continuous success of the bank possible.

We highly appreciate the trust that our clients have laid in Raiffeisen banka, firmly believing that our successful business cooperation will further develop in the coming year, to our mutual satisfaction.

Herbert Stepic,Chairman of the Board of Directors

Report by the Chairman of the Board of Directors

Report by the Chairman of the Board of Directors

�www.raiffeisenbank.co.yu

Zadovoljstvo mi je što mogu u ime Upravnog odbora Raiffeisen banke a.d. da konstatujem da je 2007. godina bila još jedna uspešna poslovna godina za ovu banku. Izuzetni rezultati koje je banka ostvarila u 2007., a koji se ogledaju, između ostalog, i u skoro dvostruko većem ostvarenom profitu u poređenju sa prethodnom godinom, imaju poseban značaj, s obzirom da su postignuti u tržišnim uslovima koji su pred banku postavili nove izazove i zahteve.

Raiffeisen banka je, kao univerzalna banka, ostala čvrsto opredeljena, da u potpunosti i na efikasan način zadovolji potrebe klijenata, da sa njima razvija partnerske odnose na dugoročnoj osnovi, uvodi nove proizvode i inovira postojeće. Time je banka uspela da održi kontinuitet u svom uspešnom poslovanju i ostane sinonim liderstva u bankarskom sektoru zemlje.

Razvoj mreže, visok standard bankarskih usluga i permanentno stručno usavršavanje zaposlenih, takođe su doprineli da veliki broj klijenata odabere Raiffeisen banku za svoju poslovnu banku.

Kontinuiranom uspehu Raiffeisen banke doprinela je i činjenica da je banka član Raiffeisen International grupe, jedne od vodećih bankarskih grupacija u zemljama centralne i istočne Evrope, kao i značajna podrška Raiffeisen Zentralbank Österreich AG, Beč, većinskog vlasnika grupacije.

Potvrda uspeha Raiffeisen banke i čitave grupacije jesu nagrade dobijene u 2007. godini. Raiffeisen banka je proglašena za najbolju banku od strane eminentnih časopisa: The Banker (treći put uzastopno, četvrti put ukupno do sada), Euromoney (šesti put uzastopno) i Global Finance (četvrti put uzastopno).

Rukovodstvo banke i ja lično bili smo duboko potreseni smrću gospodina Budimira Boška Kostića, zamenika predsednika Upravnog odbora banke. Njegovim odlaskom izgubili smo dragocenog saradnika i bliskog prijatelja, a banka je izgubila izuzetnog kolegu i stručnjaka, koji je dao neprocenjiv doprinos dosadašnjem poslovnom uspehu banke.

U ime Upravnog odbora zahvaljujem se rukovodstvu banke i svim zaposlenima, bez čijeg zalaganja, visoke profesionalnosti, stručnosti i timskog rada banka ne bi mogla da ostvari kontinuirani uspeh.

Izuzetno cenimo poverenje koje su klijenti ukazali Raiffeisen banci, uvereni da će se dosadašnja uspešna poslovna saradnja nastaviti i u narednoj godini na obostrano zadovoljstvo.

Herbert Stepic,Predsednik Upravnog odbora

Izveštaj predsednika Upravnog odbora

Izveštaj predsednika Upravnog odbora

� www.raiffeisenbank.co.yu

I have the very special pleasure to inform our distinguished shareholders and business partners, on behalf of the Managing Board of Raiffeisen banka a.d, that the bank achieved extremely good results in 2007.

The continued success of the bank - reflected throughout 2007 in the remarkable increase in the number of its clients, as well as in the growth of its deposit base, the scope and structure of its financial support for the clients, the significant growth in the profit achieved, and in its maintaining the leading position in practically all the segments of banking activities - was the result of the efforts the bank made to establish and cherish long-term partnership relations with its clients, and to satisfy their needs in the most efficient way, with regard to both the banking products and first-rate banking services it provided.

The support that Raiffeisen International, Vienna, has provided for its shareholders, and the very fact that Raiffeisen banka is an integral part of a banking group which has been extremely active in the countries of Central and Eastern Europe, have largely contributed to the bank assuming the leading role in the country’s banking sector.

Raiffeisen Group, as the major creditor of the Serbian economy, offered credit lines to clients in Serbia, not only via Raiffeisen banka, Belgrade, but also by means of direct cross-border financing by Raiffeisen International head office, giving its clients the possibility of opting for the most favourable form of financing. This provided significant support in obtaining credits for the Serbian economy under more favourable terms.

With a view to enhancing its capacities for satisfying the needs of its clients, Raiffeisen banka increased its capital in 2007, by EUR 115.0 million.

Proceeding with the extension of its network based on a thoroughly elaborated plan, Raiffeisen banka closed the year 2007 with 91 branch offices in operation.

The leasing company established by Raiffeisen banka a.d. continued its extremely successful operation as one of the leading leasing companies in the country.

In addition to the voluntary pension fund established in 2006, Raiffeisen banka also established an investment fund in 2007.

A testimony to the success of Raiffeisen banka is the series of awards it received in 2007. Raiffeisen banka was declared the “Best Bank” by eminent magazines: The Banker, Euromoney and Global Finance.

In 2007, we were faced with the painful fact that Mr. Budimir Boško Kostić, Deputy Chairman of the Managing Board of the bank and longstanding Chairman of Raiffeisen banka since its establishment, had passed away. In memory of this extraordinary banking expert, remarkable professional, and primarily colleague and humanist, Raiffeisen banka a.d. launched an initiative for the establishment of the “Budimir Boško Kostić Humanitarian Fund”, its purpose being to provide support for humanitarian activities in line with one of the principles of the Raiffeisen banking group as a whole, calling for responsible behaviour and care for the environment in which it operates.

Introductory Address by the Chairman of the Managing Board

Introductory Address by the Chairman of the Managing Board

�www.raiffeisenbank.co.yu

U ime Izvršnog odbora Raiffeisen banke a.d, Beograd, sa posebnim zadovoljstvom mogu da obavestim uvažene akcionare i cenjene poslovne partnere, da je banka ostvarila izuzetno dobre rezultate u 2007. godini.

Kontinuiran uspeh banke koji se u 2007. godini ogleda u značajnom rastu broja klijenata, depozitne baze, obima i strukture finansijske podrške klijentima, značajnom porastu ostvarenog profita, kao i u održanju vodeće pozicije u gotovo svim segmentima bankarskih aktivnosti, rezultat su nastojanja banke da sa klijentima uspostavi i neguje dugoročne partnerske odnose i da na najefikasniji način zadovolji njihove potrebe kako u pogledu ponuđenih bankarskih proizvoda tako i u pogledu pružanja prvoklasne bankarske usluge.

Podrška Raiffeisen International, Beč kao akcionara i činjenica da je Raiffeisen banka u sastavu bankarske grupe koja je izuzetno aktivna u zemljama centralne i istočne Evrope, umnogome su pomogli da banka preuzme lidersku ulogu u bankarskom sektoru zemlje.

Raiffeisen grupacija, kao najveći kreditor srpske privrede, ponudila je klijentima u Srbiji kreditne linije, i to ne samo preko Raiffeisen banke, Beograd, već i putem direktnog finansiranja iz inostranstva od strane centrale Raiffeisen International, tako da klijenti mogu da odaberu za njih najpovoljniji oblik finansiranja. Na ovaj način pružena je značajna podrška kreditiranju srpske privrede pod povoljnijim uslovima. U cilju jačanja svoje sposobnosti da u većem obimu izađe u susret potrebama klijenata, Raiffeisen banka je u 2007. povećala kapital za dodatnih EUR 115,0 miliona evra. Nastavljajući sa osmišljenim širenjem svoje mreže, Raiffeisen banka je 2007. godinu završila sa 91 otvorenom filijalom.

Lizing kompanija koju je osnovala Raiffeisen banka a.d. nastavila je sa izuzetno uspešnim poslovanjem i jedna je od vodećih lizing kompanija u zemlji.

Pored dobrovoljnog penzijskog fonda osnovanog u 2006, Raiffeisen banka je u 2007. osnovala i investicioni fond.

Potvrda uspeha Raiffeisen banke jesu nagrade dobijene u 2007. godini. Raiffeisen banka je proglašena za najbolju banku od strane renomiranih časopisa: The Banker, Euromoney i Global Finance.

U 2007. godini suočili smo se sa tužnom činjenicom da je preminuo gospodin Boško Kostić, zamenik predsednika Upravnog odbora banke, dugogodišnji direktor Raiffeisen banke od njenog osnivanja. U znak sećanja na izuzetnog bankarskog stručnjaka, vrsnog profesionalca, a, pre svega, kolegu i humanistu, Raiffeisen banka a.d. je pokrenula incijativu za osnivanje Humanitarnog fonda “Budimir Boško Kostić” sa namerom da se podrže humanitarne akcije shodno jednom od principa cele Raiffeisen bankarske grupacije, da se odgovorno ponaša i vodi računa o sredini u kojoj posluje.

Uvodna reč predsednika Izvršnog odbora

Uvodna reč Predsednika Izvršnog odbora

10 www.raiffeisenbank.co.yu

The extraordinary results that Raiffeisen banka a.d. has achieved in its activities so far, would not have been accomplished if it had not been for the extraordinary efforts of all the employees, their professional approach to their assignments, and their team work. I am using this opportunity on behalf of the Managing Board to express my gratitude to all of them for their efforts and their personal engagement.

The forthcoming year will be a year of new challenges for all of us, additional effort and commitment to surpass the results achieved, to increase the number of clients, innovate the offer of banking products, further improve service quality, expand the network, so that Raiffeisen banka would remain recognizable for its professional approach, expertise and leadership in the banking industry.

Oliver RoeglChairman of the Managing Board

Vision & Mission Statement ofRaiffeisen banka a.d.Vision

Raiffeisen banka a.d. is the leading bank in all target customer segments across the country.

Mission

We seek long-term customer relationships.We provide a full range of high quality financial services with a special focus on lending.We are a friendly, flexible and constructive partner for our customers and we are proactive, innovative and quick in developing new products and in delivering our services.As part of the Raiffeisen International network we contribute to the achievement of the overall group objectives, while generating sustainable and above-average return on equity for our shareholders.As a member of the RZB Group, we cooperate closely with Raiffeisen Zentralbank Österreich AG and the other members of the Austrian Raiffeisen Banking Group.We empower our employees to be entrepreneurial, to show initiative and we foster their development.

•

•••

•

•

•

Introductory Address by the Chairman of the Managing Board

11www.raiffeisenbank.co.yu

Izuzetni rezultati koje je Raiffeisen banka a.d. ostvarila u dosadašnjem radu ne bi se mogli ostvariti bez izuzetnog zalaganja svih zaposlenih, profesionalnog odnosa prema poslu i timskog rada. Ovom prilikom im se u ime Izvršnog odbora zahvaljujem na uloženom trudu i ličnom angažovanju. Naredna godina biće godina novih izazova za sve nas, dodatnog truda i zalaganja da se postignuti rezultati prevaziđu, poveća broj klijenata, inovira ponuda bankarskih proizvoda, dalje unapredi kvalitet usluga, širi mreža, kako bi i u uslovima pojačane konkurencije, Raiffeisen banka ostala prepoznatljiva po profesionalnosti, stručnosti i liderstvu u bankarskom sektoru.

Oliver Roegl,Predsednik Izvršnog odbora

Vizija i misija Raiffeisen banke a.d.Vizija

Raiffeisen banka a.d. je vodeća banka u svim segmentima ciljnih grupa širom zemlje.

Misija

Želimo da održavamo dugoročne veze sa klijentima.Obezbeđujemo širok dijapazon prvoklasnih finansijskih usluga, a poseban akcenat stavljamo na kreditiranje.Mi smo otvoren, fleksibilan i konstruktivan partner, proaktivni smo i inovativni u brzom razvoju novih proizvoda, kao i u pružanju usluga.Kao deo mreže Raiffeisen International doprinosimo ostvarenju svih ciljeva grupacije, u isto vreme stvarajući održiv i natprosečan povraćaj uloženog kapitala za naše akcionare.Kao članica RZB grupacije, blisko sarađujemo sa Raiffeisen Zentralbank Österreich AG i ostalim članicama austrijske Raiffeisen bankarske grupacije.Ohrabrujemo naše zaposlene da budu preduzimljivi i pokazuju inicijativu, te podstičemo njihov razvoj.

•

••

•

•

•

•

Uvodna reč predsednika Izvršnog odbora

Oliver Roegl

Predsednik Izvršnog odbora

Chairman of the Managing Board

Zoran Petrović

Zamenik predsednika Izvršnog odbora

Deputy Chairman of the Managing Board

Nenad Sibinović

Član Izvršnog odboraOperativni i opšti poslovi, IT

Member of the Managing BoardOperations, General Services & IT

Goran Kesić

Član Izvršnog odboraPoslovanje sa privredom

Member of the Managing BoardCorporate Banking

Svetozar Šijačić

Član Izvršnog odboraPoslovanje sa stanovništvom,

malim preduzećima i preduzetnicima

Member of the Managing BoardRetail Banking

1� www.raiffeisenbank.co.yu

Macroeconomic Enviroment, Opportunities for Foreign Investors and Prospects

Macroeconomic Enviroment, Opportunities for Foreign Investors and Prospects

Political and Economic Environment

The developments last year were mainly marked by the parliamentary elections and the announcement of the presidential election scheduled for the beginning of 2008. The central issue in the first half of the year was the negotiations among the coalition partners regarding the composition of the Government, that resulted in its formation in May 2007. That fact, as well as the improvement in the cooperation with the Hague Tribunal, resulted in the European Commission adopting a decision to proceed with the negotiations on the Stabilisation and Association Agreement, which had been frozen for a year. Finally, two years after the commencement of the negotiations on that document, the Government of the Republic of Serbia and the European Union initialled the Stabilisation and Association Agreement in November 2007, while the signing of the Agreement has been postponed until the establishment of full cooperation with the Hague Tribunal.

In addition to this success, the Government signed the Visa Facilitation and Readmission Agreement, as well as a new Instruments of Pre-Accession (IPA) Agreement providing it access to the funds from that programme in the period from 2007 – 2013, in the amount of EUR 971 million in total. These funds are intended for preparing candidate countries and potential candidates for using EU structural funds, once they become full members.

A positive impetus to improving the foreign trade balance as well as to attracting foreign direct investments is expected to take place after the coming into force of the Central European Free Trade Agreement (CEFTA).

The credit rating of the country followed the developments on the political and the economic planes. The positive macroeconomic results prompted the rating agency “Standard & Poor’s” to confirm the country’s rating as being BB-, in April 2007, as well as confirming its positive perspective, only to change the perspective in mid-July from positive to stable based on the country’s expansive fiscal policy, which, as the rating agency estimates, could lead to a growth in its external imbalance.

Macroeconomic Aggregates

Double digit inflation as well as a relatively high foreign trade deficit remained the key threats to macroeconomic stability. Despite the restrictive policy that the National Bank of Serbia (NBS) pursued in 2007, inflation reached 10.10% at the annual level, largely exceeding the target rate of 6.5% that had been initially set by the Government. Namely, in accordance with the new monetary strategy, maintaining a low and stable inflation rate became the joint responsibility of the NBS and the Government, the NBS controlling the part of the inflation determined by the market (basic inflation) and the Government being responsible for the part of the inflation resulting from regulated price adjustments.

Core inflation amounting to 5.4% was kept within the limits set by the NBS for 2007 which ranged from 4% - 8%. However, the second part of the total inflation which was under the competence of the Government went up as a result of a significant rise in the salaries in the public sector, as well as in the prices of agricultural produce (caused by drought), and oil and electrical energy prices.

Even though the NBS reduced the range of the target core inflation for next year from 3%-6%, so as to be more efficient in counteracting the expected inflationary trends, a more stringent monetary policy has been announced for the year 2008, if inflationary pressures escalate.

1�www.raiffeisenbank.co.yu

Makroekonomsko okruženje, mogućnosti za strane investitore i perspektive

Makroekonomsko okruženje, mogućnosti za strane investitore i perspektive

Političko i ekonomsko okruženje

Prethodna godina je najvećim delom prošla u znaku održanih parlamentarnih izbora, kao i najave predsedničkih izbora za početak 2008. godine. Naime, prva polovina godine je protekla u pregovorima koalicionih partnera o formiranju republičke Vlade, koji su rezultirali njenim formiranjem u maju 2007. godine. Ta činjenica, kao i poboljšanje saradnje sa Haškim tribunalom, rezultirala je odlukom Evropske komisije da se nastave pregovori o Sporazumu o stabilizaciji i pridruživanju, koji su bili zamrznuti godinu dana. Konačno, dve godine posle pokretanja pregovora o ovom dokumentu, Vlada Republike Srbije i Evropska unija su parafirale Sporazum o stabilizaciji i pridruživanju u novembru 2007. godine, dok je potpisivanje ovog Ugovora odloženo dok se ne uspostavi puna saradnja sa Haškim tribunalom. Pored ovog uspeha, Vlada je potpisala Sporazum o viznim olakšicama i readmisiji, kao i Ugovor o dobijanju sredstava iz novog Instrumenta za pretpristupnu pomoć (IPA) za period od 2007 – 2013, u ukupnom iznosu od 971 milion evra. Ova sredstva su namenjena pripremi država kandidata i potencijalnih kandidata za korišćenje strukturnih fondova Evropske unije kada postanu punopravne članice.

Pozitivan impuls poboljšanju spoljnotrgovinskog bilansa kao i rastu stranih direktnih investicija se očekuje nakon stupanja na snagu Ugovora o zoni slobodne trgovine u centralnoj Evropi (CEFTA). Kreditni rejting zemlje je pratio dešavanja na političkom i ekonomskom planu. Dobri makroekonomski rezultati su naveli rejting agenciju „Standard & Poor’s“ da u aprilu 2007. potvrdi rejting zemlje BB- i pozitivnu perspektivu, da bi već sredinom jula agencija promenila izgled sa pozitivnog na stabilan, zbog ekspanzivne fiskalne politike koja bi, prema procenama rejting agencije, mogla voditi rastu spoljne neravnoteže.

Makroekonomski agregati

Dvocifrena inflacija i relativno visok spoljnotrgovinski deficit i dalje predstavljaju ključne pretnje makroekonomskoj stabilnosti. I pored restriktivne politike koju je Narodna banka Srbije (NBS) vodila u 2007. godini, ostvarena inflacija od 10,10% na godišnjem nivou, daleko je premašila ciljanu stopu od 6,5%, koju je Vlada inicijalno postavila. Naime, u skladu sa novom monetarnom strategijom, održanje niske i stabilne inflacije je postalo zajednička odgovornost NBS i Vlade, i to tako što NBS kontroliše deo inflacije koji je tržišno determinisan (bazna inflacija), dok je Vlada odgovorna za deo inflacije koji nastaje kao rezultat korekcija regulisanih cena.

Bazna inflacija u iznosu od 5,4% je realizovana u granicama postavljenim od strane NBS koje su za 2007. godinu bile u rasponu od 4% - 8%, ali drugi deo ukupne inflacije koji je u nadležnosti vlade je porastao zahvaljujući značajnom rastu plata u javnom sektoru, cena poljoprivrednih proizvoda (izazvanih sušom), cena nafte i električne energije.

Iako je za sledeću godinu NBS smanjila interval ciljane bazne inflacije na 3% - 6% kako bi efikasnije uticala na inflatorna očekivanja, najavljeno je i zaoštravanje monetarne politike u 2008. godini ukoliko se pojačaju inflatorni pritisci.

20 www.raiffeisenbank.co.yu

The key policy rate, being the basic monetary policy instrument, was reduced several times during the first half of 2007, considering that core inflation remained within the level planned. The rate was reduced from 14% at the beginning of the year, to 9.5% in June. Due to increasing inflationary pressures, the key policy rate reached 10% following several adjustments, showing a tendency towards further increasing due to growing inflationary expectation in 2008.

As regards the foreign exchange policy, the NBS remarkably reduced its presence in the foreign currency market in 2007. In 2008, NBS interventions are expected only with a view to restricting excessive daily oscillations, limiting the threat that financial and price stability are exposed to, and maintaining an adequate level of foreign currency reserves.

The large influx of foreign currency in the market based on FDI contributed to the oscillations of the dinar to euro rate throughout the year, which ranged from 76.81 to 84.75. The dinar depreciated nominally in relation to the euro by 0.30%, reaching the level of RSD 79.24 to EUR 1, as of December 31, 2007.

The foreign trade deficit (based on the dollar value) increased by 41.24% in relation to the level in 2006, reaching the amount of USD 9.53 billion. Despite the fact that the annual export and import growth rates were almost at the same level (37% and 39%), the deficit continued to rise as the result of rather low import coverage. The high dependence on the import of oil and oil derivatives and steel, whose prices went up significantly, certainly had an impact on the growth of imports. On the other hand, this was largely contributed by the public and personal consumption, which was financed from consumer credits.

The high foreign trade deficit resulted in a current account deficit, its share in the GDP increasing from 11.5% in 2006, to an estimated 16.1% in 2007. In addition to this factor, the deficit in the balance of payments was also affected by the drop in the current transfers, as well as the lower influx of FDI. As regards foreign direct investments, the level of USD 2.20 billion that had been reached in 2007, was half the amount achieved in 2006, when FDIs amounted to USD 4.26 billion. Further rise in the deficit of the balance of payments may be mitigated by the privatisation of the remaining public enterprises, as well as by further improving the results of the companies privatised so far, and by arranging for an increase in FDIs and promoting exports.

The estimated GDP growth rate in 2007 as compared to the year before, amounted to 7.5%, significantly exceeding the rate of 5.7% that had been achieved in 2006. The major contribution to the growth of GDP was achieved in the sectors of transport, trade, civil engineering and financial intermediation.

Industrial production in 2007 rose by 3.7% (2006: 4.7%). The reason for the decline in the industrial production rate in relation to 2006 was the reduced volume of production in the mineral and stone extraction sectors by 0.6%. The electrical energy production and distribution sector marked a growth of 2.8%, while the processing industry realized a growth of 4.2%.

Macroeconomic Enviroment, Opportunities for Foreign Investors and Prospects

21www.raiffeisenbank.co.yu

Referentna kamatna stopa, kao osnovni instrument monetarne politike, je u toku prve polovine 2007. godine nekoliko puta snižavana, s obzirom da je bazna inflacija bila u okviru planirane. Tačnije, stopa je snižena sa 14% na početku godine na 9,5% u junu. Usled naraslih inflatornih pritisaka, referentna stopa je posle nekoliko korekcija dostigla 10%, sa tendencijom daljeg povećanja zbog inflatornih očekivanja u 2008. godini. Što se tiče politike deviznog kursa, NBS je u 2007. godini značajno smanjila svoje prisustvo na deviznom tržištu. U 2008. godini se očekuju intervencije NBS samo u cilju da se ograniče preterane dnevne oscilacije, limitira opasnost po finansijsku i cenovnu stabilnost i održi adekvatan nivo deviznih rezervi.

Veliki priliv strane valute na tržištu po osnovu stranih direktnih investicija doprineo je da kurs dinara u odnosu na evro u toku godine oscilira u rasponu od 76,81 do 84,75. Dinar je nominalno depresirao u odnosu na evro za 0,30%, dostigavši nivo od 79,24 dinara za jedan evro, na dan 31. decembra 2007. godine. Spoljnotrgovinski deficit (na bazi dolarskih vrednosti) je u odnosu na 2006. godinu porastao za 41,24% i dostigao iznos od 9,53 milijardi dolara. Iako su godišnje stope rasta izvoza i uvoza bile na skoro istom nivou (37% i 39%), deficit je kontinuirano rastao zbog dosta niske pokrivenosti uvoza sa izvozom. Naime, visoka zavisnost od uvoza nafte i naftnih derivata i čelika, čije su cene značajno porasle, svakako je uticala na rast uvoza. Sa druge strane, u velikoj meri su doprinele javna i lična potrošnja, koja je finansirana iz potrošačkih kredita.

Visok spoljnotrgovinski deficit rezultirao je i deficitom tekućeg bilansa, čije je učešće u BDP-u poraslo sa 11,5% u 2006. godini na procenjenih 16,1% u 2007. godini. Pored ovog faktora, na deficit platnog bilansa je uticao i pad tekućih transfera, kao i slabiji priliv stranih direktnih investicija. Što se tiče stranih direktnih investicija, dostignuti iznos od 2,20 milijardi dolara u 2007. godini je dva puta niži u odnosu na 2006. godinu, kada su strane direktne investicije iznosile 4,26 milijardi dolara. Dalji rast deficita platnog bilansa može se ublažiti privatizacijom preostalih javnih preduzeća, daljim poboljšanjem rezultata do sada privatizovanih preduzeća, rastom stranih direktnih investicija i promocijom izvoza.

Procenjena stopa rasta BDP-a u 2007. godini u odnosu na prethodnu godinu iznosila je 7,5% i značajno je premašila ostvarenu stopu od 5,7% u 2006. godini. Najveći doprinos rastu BDP-a ostvaren je u sektorima saobraćaja, trgovine, građevinarstva i finansijskog posredovanja. Industrijska proizvodnja je u 2007. godini porasla za 3,7% (2006: 4,7%). Razlog pada stope rasta industrijske proizvodnje u odnosu na 2006. godinu je pad proizvodnje u sektoru vađenja rude i kamena od 0,6%. Sektor proizvodnje i distribucije električne energije je zabeležio rast od 2,8% dok je prerađivačka industrija ostvarila porast od 4,2% .

Makroekonomsko okruženje, mogućnosti za strane investitore i perspektive

22 www.raiffeisenbank.co.yu

Consolidation of the Banking Sector and Changes in Legislature

Consolidation of the market took place through mergers of the banks acquired, or in the direction of announced mergers, in view of which only one new bank appeared in the market. The Belgian KBC bank acquired A banka Belgrade. Kulska banka Novi Sad, Zepter banka Beograd and Niška banka Niš merged into a single bank – OTP banka Novi Sad, while Opportunity savings bank was transformed into Opportunity banka Novi Sad. In September 2007, the total number of banks was 35, down from 37 in 2006. Since January 1, 2008, Banca Intesa Belgrade and Panonska banka Novi Sad will be operating as a single bank. The process of consolidation will continue in 2008, including the privatisation of state-owned banks. An announcement has been issued for the sale of the majority block of shares in Srpska banka Belgrade, Privredna banka Pančevo and Credy banka Kragujevac. The state does not intend to keep its stakes in the banks where it is a shareholder, and their sale will depend on the need of the state for liquid funds.

In accordance with the new monetary strategy, the main instruments of monetary policy were key policy rate and the ratio of gross consumer loans to local Tier 1 capital, while the mandatory reserve rates remained practically unchanged. More precisely, in order to strengthen dinar deposits, the NBS reduced the dinar mandatory reserve from 10% to 5%, however, only for dinar term deposits for a tenor longer than one month.

In reference to the adjustments of gross consumer placements to the bank’s Tier 1 capital, the first time the NBS limited the balance of gross placements granted to the consumer sector was in September 2006, specifying that placements may not exceed 200% of the value of the Tier1 capital of the bank at the end of each month. In view of the comparatively high rate of growth in consumer loans, the NBS further reduced this indicator, and thus, since December 31, 2007, the balance of these placements at the end of each month is to be maximum 150% of the value of the bank’s Tier 1 capital. The only placement excluded from the respective calculation are credits granted for investments in agricultural production and credits granted to entrepreneurs.

Further on, the NBS has limited the maximum tenor for cash loans. Namely, a large number of banks extended their repayment tenors for such credits to as long as 10 years in order to rapidly increase their market share. As a result of this, a larger number of citizens were able to meet the criteria prescribed by the NBS, based on which the total monthly credit liability may not exceed 30% of their regular monthly income, and 50% in the case of liabilities based on housing credits. Such a development of the market prompted a response from the NBS in September 2007, which limited the tenor for approving cash loans to a maximum of two years.

Lending Structure and Fund Sources of the Serbian Banking Sector

The restrictive monetary policy prompted direct corporate financing from abroad, as a result of which the increment of new banking assets in 2007 fell below the level reached in the same period the year before, amounting to EUR 5.09 billion (2006: EUR 5.40 billion).

The structure of banking sector financing improved, given the continued downward trend in the share of cross-border credits, while the share of retail savings and capital kept increasing.

Macroeconomic Enviroment, Opportunities for Foreign Investors and Prospects

23www.raiffeisenbank.co.yu

Konsolidacija bankarskog sektora i promene regulative

Konsolidacija na tržištu se odvijala u pravcu spajanja kupljenih banaka ili najave spajanja, tako da je samo jedna nova banka ušla na tržište. Naime, Belgijska KBC banka je kupila A banku Beograd. Kulska banka Novi Sad, Zepter banka Beograd i Niška banka Niš su spojene u jednu banku, OTP banku Novi Sad, dok je Opportunity štedionica transformisana u Opportunity banku Novi Sad. U septembru 2007. godine ukupan broj banaka je smanjen na 35 sa 37 u 2006. Od 1. januara 2008. godine, Banca Intesa Beograd i Panonska banka Novi Sad će poslovati kao jedna banka. Proces konsolidacije se nastavlja u 2008. godini privatizacijom banaka u državnom vlasništvu. Najavljena je prodaja većinskog paketa akcija u Srpskoj banci Beograd, Privrednoj banci Pančevo i Credy banci Kragujevac. Država nema nameru da zadrži udeo u bankama u kojima je akcionar, a prodaja će zavisiti od potreba države za likvidnim sredstvima.

U skladu sa novom monetarnom strategijom, NBS je kao glavne instrumente monetarne politike koristila referentnu kamatnu stopu i racio usklađivanja plasmana stanovništvu sa osnovnim kapitalom banke, dok su stope obavezne rezerve ostale skoro nepromenjene. Tačnije, u cilju jačanja dinarskih depozita, NBS je smanjila dinarsku obaveznu rezervu sa 10% na 5%, ali samo za dinarske depozite oročene preko jednog meseca.

Kada je u pitanju usklađivanje plasmana stanovništvu sa osnovnim kapitalom banke, NBS je prvi put ograničila stanje bruto plasmana odobrenih stanovništvu u septembru 2006. godine i to tako da plasmani ne budu veći od 200% vrednosti osnovnog kapitala banke na kraju svakog meseca. Zbog relativno visoke stope rasta kreditiranja stanovništva, NBS je dodatno pooštrila ovaj pokazatelj, tako da počevši od 31. decembra 2007. godine, stanje tih plasmana na kraju svakog meseca treba da maksimalno iznosi 150% vrednosti osnovnog kapitala banke. Iz obračuna su isključeni samo krediti odobreni za ulaganje u poljoprivrednu proizvodnju i krediti odobreni fizičkim licima koja samostalno obavljaju privrednu delatnost.

Pored ove mere, NBS je ograničila rok na koji mogu da se odobre gotovinski krediti. Naime, veliki broj banaka je produžavao rok otplate ovih kredita čak do 10 godina, a u cilju što bržeg povećanja svog učešća na tržištu. Na taj način se veći broj građana mogao uklopiti u kriterijume propisane od strane NBS, gde ukupna mesečna kreditna obaveza ne sme preći 30% njihovih redovnih mesečnih prihoda, a 50% sa obavezama po stambenim kreditima. Ovakav razvoj tržišta iznudio je reakciju NBS koja je od septembra 2007. ograničila rok za odobravanje gotovinskih kredita na maksimalno dve godine.

Struktura plasmana i izvora bankarskog sektora Srbije

Restriktivna monetarna politika podstakla je direktno finansiranje privrede iz inostranstva, usled čega je prirast nove bankarske aktive u 2007. godini bio ispod nivoa kreiranog u istom periodu prošle godine i iznosio je 5,09 milijarde evra (2006: 5,40 milijarde evra).

Struktura finansiranja bankarskog sektora je poboljšana, budući da se nastavio trend smanjenja učešća kredita uzetih iz inostranstva, dok se učešće štednje stanovništva i kapitala povećalo.

Makroekonomsko okruženje, mogućnosti za strane investitore i perspektive

24 www.raiffeisenbank.co.yu

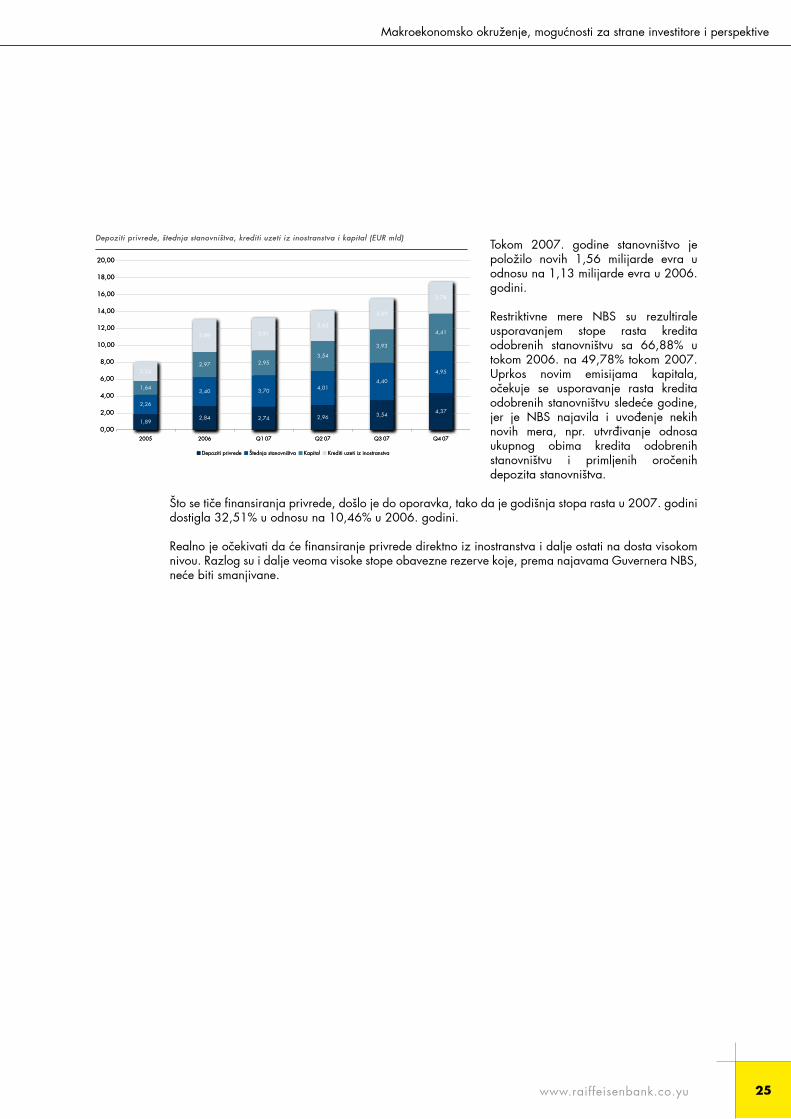

In 2007, the retail sector deposited an additional amount of EUR 1.56 billion, compared to EUR 1.13 billion in 2006.

The restrictive measures introduced by the NBS resulted in a slowdown of the growth rate of the loans granted to the retail sector, down from 66.88% in 2006, to 49.78% in 2007. Despite new capital issues, the growth of credits granted to the retail sector is expected to slow down next year, as the NBS announced introducing certain new measures, e.g. establishing the ratio between the total volume of credits granted for the retail sector and the time deposits received in the retail sector.

As regards corporate financing, it experienced a recovery thanks to which the annual growth rate in 2007 reached 32.51% as compared to 10.46% in 2006.

It is realistic to expect that direct cross-border corporate financing will remain at quite a high level. The reason for this is that the mandatory reserve rates have remained very high and are not going to be reduced, as annouced by the Governor of NBS.

Macroeconomic Enviroment, Opportunities for Foreign Investors and Prospects

25www.raiffeisenbank.co.yu

Tokom 2007. godine stanovništvo je položilo novih 1,56 milijarde evra u odnosu na 1,13 milijarde evra u 2006. godini.

Restriktivne mere NBS su rezultirale usporavanjem stope rasta kredita odobrenih stanovništvu sa 66,88% u tokom 2006. na 49,78% tokom 2007. Uprkos novim emisijama kapitala, očekuje se usporavanje rasta kredita odobrenih stanovništvu sledeće godine, jer je NBS najavila i uvođenje nekih novih mera, npr. utvrđivanje odnosa ukupnog obima kredita odobrenih stanovništvu i primljenih oročenih depozita stanovništva.

Što se tiče finansiranja privrede, došlo je do oporavka, tako da je godišnja stopa rasta u 2007. godini dostigla 32,51% u odnosu na 10,46% u 2006. godini.

Realno je očekivati da će finansiranje privrede direktno iz inostranstva i dalje ostati na dosta visokom nivou. Razlog su i dalje veoma visoke stope obavezne rezerve koje, prema najavama Guvernera NBS, neće biti smanjivane.

Makroekonomsko okruženje, mogućnosti za strane investitore i perspektive

Within the scope of its corporate social responsibilities, Raiffeisen banka a.d. created the concept and realized a special donation activity: fully equipped computer classroom and paid computer courses for children who live in the foster home „Spomenak“ in Pančevo.

The donation was realized in close cooperation with the Ministry of Employment and Social Policy, government of the Republic of Serbia. Apart from the computer classroom with ten computers, a scanner and a printer, this donation also comprises paid courses of learning to work with a computer for the children and their educators.

Raiffeisen banka realized this donation in order to contribute to the mastering of new technologies and easier communication, to facilitate access to an almost limitless information source through the internet, but also as an expression of special gratitude for the drawings on the subject „What will I be when I grow up“ which the children from „Spomenak“ gave to Raiffeisen banka: in the course of preparing the annual report for 2007, the idea emerged to enable the children from „Spomenak“ to enrich this report, which is the bank’s most representative business document.

The foster home for children and youth without parental care „Spomenak“ in Pančevo is an institution of social protection that provides for children and youth without parental care, as well as for children whose development is impaired by their family environment, until conditions are met for them to return either to their own environment, to their relatives, to a foster family, or until they are ready to lead a life on their own.

At the moment, there are about fifty children and young people in „Spomenak“, attended by thirty employees, half of which are experts. The main function is meeting the children’s needs, taking care of their health, development and upbringing, providing help in their education and support for working and an independent life.

The children and young people who live in „Spomenak“ attend regular and specialized primary and secondary schools; there are also two students in residence. Lots of them successfully go in for sports, they like computers, have published five books, write for the foster home’s newspaper, draw, embroider, weave and like to cast and colour plaster figurines. It was these artistic tendencies that initiated the idea in Raiffeisen banka to include the works of children from this foster home. Their wishes, apart from their artistic expression, have also been articulated in the short messages noted on every drawing, showing that, notwithstanding the difficulties these children are faced with at the beginning of their young lives, they are still full of desire for self-realization and look upon the future with faith.

Donation to „Spomenak“, Foster Home for Children and Youth without Parental Care in Pančevo

2� www.raiffeisenbank.co.yu

U okviru svojih aktivnosti društveno odgovornog ponašanja, Raiffeisen banka a.d. je osmislila i realizovala posebnu donatorsku akciju: kompletna kompjuterska učionica i plaćeni kursevi za osposobljavanje za rad na računarima poklonjeni su deci smeštenoj u Domu za decu i omladinu bez roditeljskog staranja „Spomenak“ u Pančevu. Donacija je sprovedena u bliskoj saradnji sa Ministarstvom rada i socijalne politike Vlade Republike Srbije, a pored kompjuterske učionice koju sačinjavaju deset računara, skener i štampač, u ovu donaciju su uključeni i plaćeni kursevi za osposobljavanje za rad na računarima za decu i njihove vaspitače.

Raiffeisen banka je donaciju uputila najpre kao izraz želje da doprinese ovladavanju novim tehnologijama, lakšoj komunikaciji i pristupu skoro neiscrpnom izvoru informacija preko interneta, ali i kao izraz posebne zahvalnosti za likovne radove na temu “Šta ću biti kad porastem” koje su deca “Spomenka” prethodno poklonila Raiffeisen banci. Naime, tokom pripremanja godišnjeg izveštaja za 2007.godinu u banci se rodila ideja da se omogući deci iz “Spomenka” da svojim crtežima obogate ovaj izveštaj, koji je najreprezentativniji poslovni dokument banke. Dom za decu i omladinu bez roditeljskog staranja „Spomenak“ u Pančevu je ustanova socijalne zaštite koja zbrinjava decu i omladinu bez roditelja ili roditeljskog staranja, kao i decu čiji je razvoj ometen porodičnim prilikama, do obezbeđivanja uslova za povratak u sopstvenu, srodničku, ili hraniteljsku porodicu, odnosno do osposobljavanja za samostalni život.

U domu trenutno živi oko pedesetoro dece i mladih o kojima brine oko trideset zaposlenih. Osnovna funkcija doma odnosi se na brigu o zadovoljavanju potreba dece, negu i staranje o njihovom zdravlju, razvoju i vaspitanju, pomoći u obrazovanju i osposobljavanju za rad i samostalan život.

Deca i mladi koji žive u „Spomenku“ pohađaju redovne i specijalne osnovne i srednje škole, a na smeštaju su i dva studenta. Mnogi se uspešno bave sportom, vole kompjutere, izdali su pet knjiga svojih radova, pišu za domski list, crtaju, bave se vezom, tkanjem i vole da izlivaju i boje ukrasne figurice od gipsa.

Upravo su ove umetničke sklonosti inicirale ideju u Raiffeisen banci da se u godišnji izveštaj ukomponuju crteži dece ovog doma. Njihove želje su, pored likovnog izraza, potkrepljene i porukama zabeleženim na svakom crtežu i pokazuju da su, uprkos otežanim uslovima na početku njihovih mladih života, ona ipak puna želje za samoostvarenjem i sa verom okrenuta budućnosti.

Donatorska akcija za decu smeštenu u Domu za decu i omladinu bez roditeljskog staranja „Spomenak“ u Pančevu

2�www.raiffeisenbank.co.yu

30 www.raiffeisenbank.co.yu

The corporate banking segment continued with its successful business activities and recorded a substantial increase in its business volume, extending its client base by 300 new corporate partners in 2007. In line with the bank’s ambitious plans, the previous year was marked by a further expansion of the branch network, enabling clients in all parts of Serbia to have access to the services of Raiffeisen banka.

In 2007, in collaboration with the Raiffeisen Banking Group, Raiffeisen banka continued to provide its clients with competitive financing from abroad, in addition to the existing financing models, making this available through its head office Raiffeisen International. This quite attractive financing vehicle has met a very large market demand and thus contributed to the strong growth of Raiffeisen total corporate credit portfolio of 22% in 2007.

Also, considering a substantial plunge of BELIBOR accompanied by the stability of the local currency, the bank expanded its scope of financing in local currency without foreign currency clause and made it even more competitive. By increasing the availability of products such as project financing and introducing new ones, such as factoring, Raiffeisen banka successfully supported the financial needs of its corporate clients in all business segments.

The credit portfolio structure in 2007 was dominated by short-term and medium-term loans, with an exceedingly pronounced tendency for longer maturity. The table below shows the corporate credit structure split by maturity.

Corporate Credit Exposure by Maturity in 2007

<1 year 9.3%

1-3 years 63.8%

3-5 years 9.7%

>5 years 17.2%

Total 100.0%

In view of the fact that Raiffeisen banka covers the largest share of the corporate market, the main strategy in this segment is primarily extending the scope of cooperation with existing clients, but also acquiring new companies, all with the aim of keeping its leading market position.

Additional proof of the bank’s success is also the fact that out of 20 major foreign investors in Serbia, excluding banks, 18 are clients of Raiffeisen banka. Moreover, the volume of domestic payment transactions increased by 42% in 2007, while the volume of international payment transactions grew by as much as 51%.

Raiffeisen banka was active in supporting the further development of local municipalities and the public sector by actively financing this very important segment of the economy.

Corporate Banking

Corporate Banking

31www.raiffeisenbank.co.yu

Segment poslovanja sa privredom nastavio je sa uspešnim radom i visokim rastom obima poslovanja, povećavši svoju bazu klijenata sa 300 novih korporativnih partnera u 2007. godini. Shodno ambicioznim planovima banke, predhodnu godinu obeležila je dalja ekspanzija mreže ekspozitura i filijala, omogućavajući klijentima u svim krajevima Srbije korišćenje usluga Raiffeisen banke.

U 2007. godini, pored postojećih modela finansiranja, banka je, zajedno sa Raiffeisen grupom, nastavila da svojim klijentima pruža mogućnost finansiranja iz inostranstva direktno preko centrale Raiffeisen International. Ovaj veoma atraktivan način finansiranja, praćen intenzivnom tražnjom na tržištu, rezultirao je snažnim rastom ukupnog kreditnog portfelja privrede Raiffeisen grupacije u Srbiji od 22% u 2007. godini.

Takođe, usled značajnog pada BELIBOR-a i stabilne lokalne valute, banka je proširila obim finansiranja u lokalnoj valuti bez devizne klauzule i učinila ga još povoljnijim. Povećanjem dostupnosti proizvoda, kao što je projektno finansiranje i uvođenjem novih, kao što je faktoring, Raiffeisen banka je uspešno podržala finansijske potrebe svojih klijenata u svim segmentima poslovanja.

U strukturi kreditnog portfelja u privredi u 2007. godini dominiraju kratkoročni i srednjoročni krediti, sa sve izraženijim trendom produžetka ročnosti. Tabela u prilogu pokazuje strukturu kreditnih plasmana privredi po ročnosti.

Struktura kredita privredi po ročnosti u 2007. godini

<1 godine 9.3%

1-3 godine 63.8%

3-5 godina 9.7%

>5 godina 17.2%

Ukupno 100.0%

S obzirom da banka pokriva najveći deo tržišta privrede, glavna strategija u ovom segmentu se ogleda prevashodno u proširenju obima saradnje sa postojećim klijentima, ali i u akviziciji novih firmi, a u cilju održavanja vodeće tržišne pozicije.

Potvrda uspeha je i činjenica da su od 20 najvećih stranih investitora u Srbiji, isključujući banke, 18 klijenti Raiffeisen banke. Takođe, obim domaćeg platnog prometa korporativnih klijenata se u 2007. godini povećao za 42%, dok se obim platnog prometa sa inostranstvom povećao za čak 51%.

Raiffeisen banka je i u 2007. godini podržala dalji razvoj lokalne samouprave i javnog sektora krozaktivno finansiranje ovog veoma značajnog dela privrede.

Poslovanje sa privredom

Poslovanje sa privredom

32 www.raiffeisenbank.co.yu

The following table shows the credit structure in 2007, broken down by industries:

Corporate Credit Exposure by Industry %

Trade 28.6%

Consumer Non-Cyclical (food, beverages, pharmaceuticals, etc.) 23.6%

Construction 18.9%

Consumer Cyclical (furniture, household appliances, etc.) 7.5%

Industrials 7.3%

Energy (including oil & gas) 4.8%

Materials 4.7%

Information Technology 1.1%

Special 1.0%

Financials (classified as corporate) 0.7%

Telecommunications 0.7%

Healthcare 0.5%

Real Estate 0.5%

Utilities 0.2%

Total 100.0%

Regarding corporate deposits, Raiffeisen banka retained the leading market position, increasing its total deposits volume by 38%, compared to 2006. A very high growth rate of 42% was achieved inlocal currency deposits, which was made possible also by the stable local currency, as well as thecontinuation of the privatization process, and the inflow of foreign investments in 2007. Total depositsat the end 2007 reached EUR 559 million.

Corporate Banking

33www.raiffeisenbank.co.yu

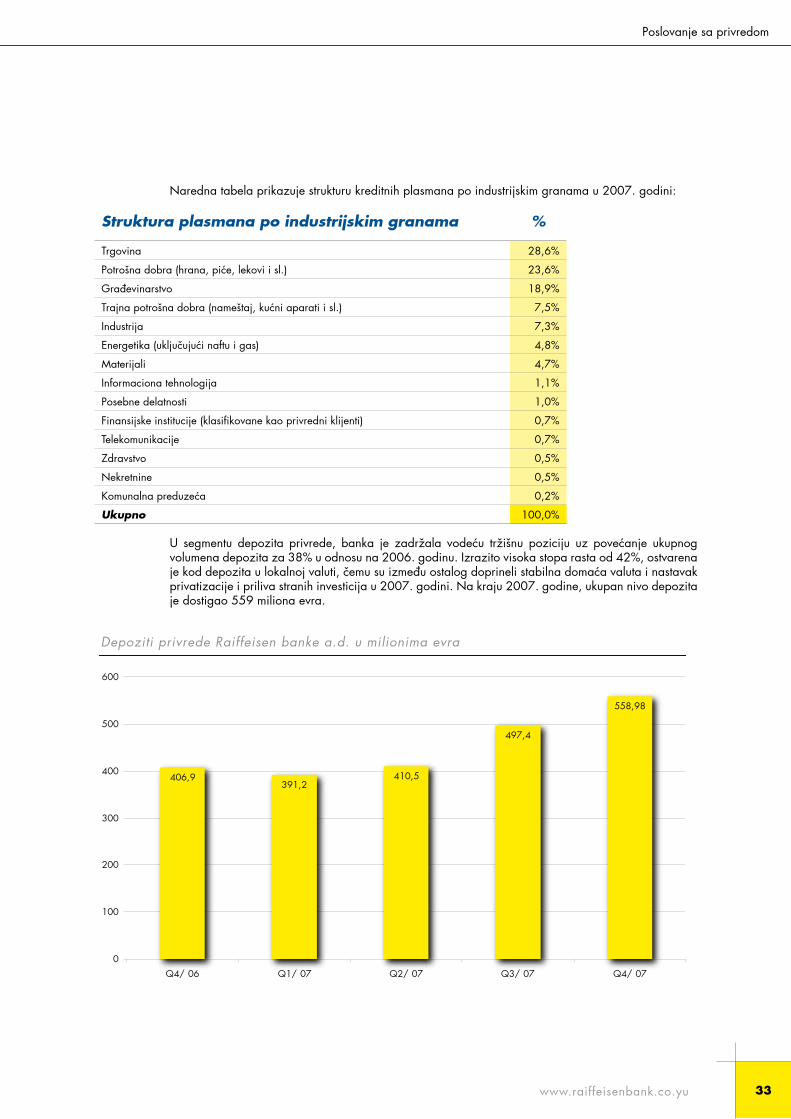

Naredna tabela prikazuje strukturu kreditnih plasmana po industrijskim granama u 2007. godini:

Struktura plasmana po industrijskim granama %

Trgovina 28,6%

Potrošna dobra (hrana, piće, lekovi i sl.) 23,6%

Građevinarstvo 18,9%

Trajna potrošna dobra (nameštaj, kućni aparati i sl.) 7,5%

Industrija 7,3%

Energetika (uključujući naftu i gas) 4,8%

Materijali 4,7%

Informaciona tehnologija 1,1%

Posebne delatnosti 1,0%

Finansijske institucije (klasifikovane kao privredni klijenti) 0,7%

Telekomunikacije 0,7%

Zdravstvo 0,5%

Nekretnine 0,5%

Komunalna preduzeća 0,2%

Ukupno 100,0%

U segmentu depozita privrede, banka je zadržala vodeću tržišnu poziciju uz povećanje ukupnog volumena depozita za 38% u odnosu na 2006. godinu. Izrazito visoka stopa rasta od 42%, ostvarena je kod depozita u lokalnoj valuti, čemu su između ostalog doprineli stabilna domaća valuta i nastavak privatizacije i priliva stranih investicija u 2007. godini. Na kraju 2007. godine, ukupan nivo depozita je dostigao 559 miliona evra.

Poslovanje sa privredom

34 www.raiffeisenbank.co.yu

Documentary Business

Thanks to the active engagement on the part of the team of professionals in the Documentary Business & Guarantees Department, in recent years Raiffeisen banka has had a significant impact on the rise in the demand for these products in the local market. Due to the corporate clients’ pronounced need for using documentary instruments, especially letters of guarantee and letters of credit, service quality has become the focus, which has been reflected in the growth of the total portfolio by 70% in comparison to the year 2006.

Service Quality and Innovation

As shown by the results of corporate customer satisfaction study conducted by Raiffeisen banka in 2007, high level of professionalism, efficiency and expert staff are key factors enabling the bank to keep its status of the leading commercial bank in the Serbian market. Sophisticated and efficient e-banking systems (ROL and Halcom) are available to all the clients of Raiffeisen banka who have opted for making their payments by themselves.

The series of products that Raiffeisen banka upgraded in 2007 includes, among others, project financing service, which provides a secure financing solution for a great number of capital investment and civil-engineering companies, its aim being successful implementation of projects across Serbia. Also, in order to meet the clients’ needs, the bank introduced another new, even more flexible product – factoring, which was unique in the Serbian banking market in 2007.

Strongly focusing on improving the existing products and developing new and innovative ones, Raiffeisen banka plans to offer new financial solutions in the form of attractive products, and to continue being a reliable partner to its clients.

Corporate Banking

35www.raiffeisenbank.co.yu

Dokumentarni poslovi

Kroz aktivan angažman profesionalnog tima iz Odeljenja za dokumentarne poslove i garancije, Raiffeisen banka je uticala na proširivanje tražnje za ovim proizvodima na lokalnom tržištu poslednjih godina. Usled postojanja izražene potrebe korporativnih klijenata za upotrebom dokumentarnih instrumenata, a posebno garancija i akreditiva, jak akcenat je stavljen na kvalitet pruženih usluga, što pokazuje i prirast ukupnog portfelja od 70% u odnosu na kraj 2006. godine.

Kvalitet usluge i inovacija

Kako je pokazalo istraživanje o kvalitetu usluga Raiffeisen banke, koje je sprovedeno u 2007. godini, visoki nivo profesionalizma, efikasnost i stručno osoblje su ključni faktori koji banci omogućavaju očuvanje statusa vodeće poslovne banke na srpskom tržištu. Razvijen i efikasan sistem elektronskog bankarstva (ROL i Halcom) dostupan je svim klijentima Raiffeisen banke koji se opredele da svoja plaćanja vrše samostalno.

Među uslugama koje je banka ove godine unapredila, između ostalog, jeste i usluga projektnog finansiranja, koja je velikom broju investicionih i građevinskih kompanija ponudila rešenje sigurnog finansiranja u cilju uspešne realizacije projekata širom Srbije. Takođe, u skladu sa potrebama klijenata, banka je uvela i usluge novog, još fleksibilnijeg kreditnog proizvoda, faktoringa, koji je u 2007. godini bio jedinstven u bankarskom sektoru na srpskom tržištu.

Sa snažnim fokusom na unapređenje postojećih i razvoj novih i inovativnih proizvoda, banka planirada i narednih godina ponudi nova finansijska rešenja kroz atraktivne proizvode i da nastavi da budepartner od poverenja svojim komitentima.

Poslovanje sa privredom

3� www.raiffeisenbank.co.yu

The consumer banking segment continued with succesfull business activities and achieved significant growth in 2007 as well. The total number of clients is 486,332 which is an increase of 20.2% in relation to the year before.

The total credit portfolio placed at the disposal of individuals amounted to EUR 442.5 million, contributing to an annual growth in this segment of operations by 25.7%.

The total number of retail deposits amounted to EUR 720.9 million, representing an increase of 31.5% in relation to the year before, which is a reaffirmation of the great interest the citizens have in keeping their savings at Raiffeisen banka.

In order to provide best quality services for its clients in the field of mortgage loans, specialised branch offices – Raiffeisen Mortgage Loan Centers were established, where mortgage loan experts provided the clients with all the information they needed, including full professional assistance from selecting an apartment to implementing a mortgage loan.

Introduction of mobile advisors for mortgage loans also significantly facilitated obtaining the loans. This service provides maximum assistance to the clients, considering that it facilitates their getting information on mortgage loans at the time and place that best suits them. The clients get maximum assistance from the beginning of the process of submission of loan applications to the end, considering that mobile advisors provide them with all the information they need, assisting them in collecting the necessary documents and also being able to submit the documents on behalf of the clients.

Consumer Banking

Consumer Banking

3�www.raiffeisenbank.co.yu

Segment za poslovanje sa stanovništvom nastavio je uspešno poslovanje i ostvario značajan rast i u toku 2007. godine. Ukupan broj klijenata je 486.332, što predstavlja povećanje od 20,2% u odnosu na prethodnu godinu.

Ukupan portfelj kredita koji su plasirani fizičkim licima je 442,5 miliona evra i u ovom segmentu poslovanja zabeležen je godišnji rast od 25,7%.

Ukupan iznos depozita stanovništvu je 720,9 miliona evra, što je rast od 31,5% u odnosu na prethodnu godinu, čime je potvrđeno veliko poverenje građana u štednju u Raiffeisen banci.

U cilju pružanja najkvalitetnije usluge klijentima u oblasti stambenog kreditiranja, otvorene su specijalizovane ekspoziture – Raiffeisen kuće, u kojima klijenti uz pomoć specijalista za stambene kredite mogu na jednom mestu dobiti sve informacije i kompletnu stručnu pomoć, od izbora stana do realizacije stambenog kredita.

Uvođenje mobilnih savetnika za stambene kredite je takođe značajno olakšalo put do ovih kredita. Ovom uslugom se maksimalno izlazi u susret klijentima, budući da im je omogućeno da informacije o stambenom kreditu dobiju u vreme i na mestu koje njima najviše odgovara. Klijenti dobijaju maksimalnu pomoć od početka do kraja procesa podnošenja zahteva za kredit, jer mobilni savetnici pružaju sve potrebne informacije, pomažu pri prikupljanju neophodne dokumentacije i u mogućnosti su da dokumentaciju predaju umesto klijenta.

Poslovanje sa stanovništvom

Poslovanje sa stanovništvom

40 www.raiffeisenbank.co.yu

In collaboration with Uniqa insurance, all the clients using cash, consumer, car loans and credit cards are provided with additional protection because, in the event of any of the accidents provided for by the insurance, the insurance company Uniqa will assume the obligation of repayment of the debt arising from the loan or credit card, on behalf of the client or his/her family.

The total number of active VISA revolving cards at the end of 2007 amounted to 140,442, which was by 10.67% more than at the end of 2006. During 2007, the number of transactions carried out on the basis of this product alone was 2,157,983, reaching a turnover of more than EUR 65 million.

In June 2007, Raiffeisen banka offered a new card product – the MasterCard Installment credit card. The principle of functioning of this credit card is based on repayment of transactions carried out with the card based on a predetermined number of monthly installments (the number of installments and the interest rate amount depend on the transaction amount). By the end of 2007, Raiffeisen banka issued 9,912 MasterCard Installment credit cards, that had a turnover of more than EUR 6 million.

In addition to the licence for accepting and processing VISA “mobile service” transactions, in the second half of 2007, Raiffeisen banka obtained a licence for accepting and processing MasterCard “mobile service” transactions.

In the field of e-banking, clients have the possibility of issuing on-line orders for securities trading. Also available is the free payment service with authorisation via SMS codes, thanks to which dinar payments can be effected without the need to go to the bank and previously predefine the payment order.

The quality of client services was additionally upgraded by implementing the Sales Force Effectiveness (SFE) Project in all the branch offices. This approach was extremely well received by the clients who were provided expert advice regarding the products and services that best suited their needs.

The intensive development of the branch office network continued throughout 2007 as well, with the opening of 24 new branch offices, thanks to which the business network increased to 91 branch offices across the country.

Consumer Banking

41www.raiffeisenbank.co.yu

U saradnji sa Uniqa osiguranjem, svi klijenti koji koriste gotovinske, potrošačke, auto kredite i kreditne kartice su dodatno zaštićeni, jer u slučaju nastanka nesrećnih slučajeva predviđenih osiguranjem, osiguravajuća kuća Uniqa preuzima otplatu duga po kreditu i kreditnoj kartici, umesto samog klijenta ili njegove porodice.

Ukupan broj aktivnih VISA revolving kartica na kraju 2007. godine iznosi 140.442, što je za 10,67% više nego na kraju 2006. godine. Samo po ovom proizvodu, u toku 2007. godine realizovano je ukupno 2.157.983 transakcija sa prometom od preko 65 miliona evra.

U junu 2007. godine Raiffeisen banka je ponudila novi kartični proizvod, MasterCard Installment kreditnu karticu. Princip funkcionisanja ove kreditne kartice zasniva se na otplati transakcija napravljenih karticom na unapred utvrđeni broj mesečnih rata (broj rata i visina kamatne stope zavise od iznosa transakcije). Do kraja 2007. godine Raiffeisen banka je izdala 9.912 MasterCard Installment kreditnih kartica koje su ostvarile promet od preko 6 miliona evra.

Pored licence za prihvatanje i procesiranje VISA „mobile service“ transakcija, u drugoj polovini 2007. godine, Raiffeisen banka je dobila licencu za prihvatanje i procesiranje MasterCard „mobile service“ transakcija.

U oblasti elektronskog bankarstva, klijentima je omogućeno elektronsko kreiranje naloga za trgovanje hartijama od vrednosti. Takođe, ponuđena je usluga slobodnog plaćanja uz autorizaciju putem SMS koda, koja omogućava dinarska plaćanja bez potrebe dolaska u banku i prethodnog predefinisanja naloga.

Kvalitet usluga klijentima je dodatno unapređen implementacijom projekta povećanja efikasnosti prodaje (SFE – Sales Force Effectiveness) u svim poslovnicama. Ovakav pristup je imao odličan prijem kod klijenata koji dobijaju stručan savet u vezi sa proizvodima i uslugama koje najviše odgovaraju njihovim potrebama.

Intenzivan razvoj mreže poslovnica je nastavljen i u toku 2007 godine kada je otvoreno 24 novih poslovnica, čime je poslovna mreža povećana na 91 poslovnica širom zemlje.

Poslovanje sa stanovništvom

44 www.raiffeisenbank.co.yu

For the SE&M Division, that works with small enterprises and entrepreneurs (with an annual income of up to EUR 5 million) and micro companies and entrepreneurs (with an annual income of up to EUR 0.5 million), the past year was marked by an extraordinary growth trend in all the segments of its operation. The total number of clients at the end of 2007 was 23,956, representing an increase of 36.28% compared to the year before. The loan portfolio expanded by 11.48% in relation to 2006, reaching EUR 157.5 million. The fact that has to be stressed in particular is the very dynamic activity which was evident in the field of loan placements based on direct cross-border financing, their value at the end of the year amounting to EUR 54.6 million. As a result, placements in the SE&M segment as of December 31, 2007, totalled EUR 212.1 million, marking an increase of 46.82% in relation to 2006.

The portfolio of approved guarantees and L/Cs also registered an increase of 131.31% in relation to the previous year, thanks to which its amount reached EUR 21 million at the end of 2007.

The deposits segment also marked a growth of 47.51%, thanks to which the deposits portfolio reached EUR 72 million at the end of 2007.

As regards the offer of products and services intended for small enterprises and entrepreneurs, the emphasis in 2007 was placed on standardising the existing offer and upgrading the models of loans, deposit and documentary products intended for the segments of operations involving small enterprises, micro companies and entrepreneurs.

The products available for this segment of clients support a broad range of needs of enterprises and entrepreneurs, involving loans without firm collateral granted for a term of up to three years, which can be obtained in a matter of hours, framework lines with the possibility of renewal, general purpose loans for a term of up to five years, as well as MasterCard business credit cards catering for current needs of companies, and long-term loans for financing investments granted for a term of up to 12 years.

In the micro companies and entrepreneurs segment, the offer available to lump sum tax payers was also extended by an investment credit granted for a term of up to five years, which was introduced as an addition to the already existing loan for working capital and the business credit card.

A major novelty in the operation of both of these segments was the new approach introduced through the Sales Force Effectiveness Project, which contributed to increasing the quality of sales, as well as raising the level of efficiency and speed of operation.

The advancement of the quality of sales ran parallel to achieving significant progress in reducing the time required for processing loan applications by decentralising and automating the process of work, as well as by using alternative sales channels (Contact Centre, direct sales agents, direct mailing offers sent to clients directly). The above improvements have contributed to our maintaining our competitive advantage in the market and achieving a high level of satisfaction of our clients.

Small Enterprises and Micro Business

Small Enterprises and Micro Business

45www.raiffeisenbank.co.yu

Protekla godina je za Sektor poslovanja sa malim preduzećima i preduzetnicima (sa godišnjim prihodima do 5 miliona evra) i mikropreduzećima i preduzetnicima (sa godišnjim prihodima do 0,5 miliona evra) bila obeležena izuzetnim trendom rasta u svim domenima poslovanja. Ukupan broj klijenata na kraju 2007. godine iznosi 23.956, što, u odnosu na prethodnu godinu, predstavlja povećanje od 36,28%. Kreditni portfelj je povećan za 11,48% u odnosu na 2006. godinu i iznosi 157,5 miliona evra. Posebno treba istaći veoma dinamičnu aktivnost koja je ostvarena u domenu kreditnih plasmana putem direktnog finansiranja iz inostranstva, a koje je na kraju godine iznosilo ukupno 54,6 miliona evra. Ukupni plasmani maloj privredi na dan 31.12.2007. godine time iznose 212,1 miliona evra i povećani su u odnosu na 2006. godinu za 46,82%.

Portfelj odobrenih garancija i akreditiva je takođe povećan u odnosu na prethodnu godinu i to za 131,31%, tako da je na kraju 2007. godine iznosio 21 milion evra. U segmentu depozita je takođe zabeležen porast za 47,51%, tako da depozitni portfelj na kraju 2007. godine iznosi 72 miliona evra.

Kad je reč o ponudi proizvoda i usluga namenjenih maloj privredi, u toku 2007. godine je akcenat stavljen na standardizaciju postojeće ponude i unapređenju modela kreditnih, depozitnih i dokumentarnih proizvoda, namenjenih kako segmentu malih, tako i segmentu mikropreduzeća i preduzetnika.

Ponuda proizvoda ovom segmentu klijenata pokriva širok spektar potreba preduzeća i preduzetnika, počev od kredita bez čvrstog obezbeđenja na rok do tri godine koji se odobravaju u roku od nekoliko sati, preko okvirnih linija sa mogućnošću obnavljanja i kredita za opšte namene na rok do pet godina, MasterCard biznis kreditnih kartica za tekuće potrebe preduzeća, pa sve do dugoročnih kredita za finansiranje investicija na rok do 12 godina.

U segmentu mikropreduzeća i preduzetnika, ponuda za paušalne poreske obveznike je dopunjena i investicionim kreditom do pet godina, pored dotadašnje ponude koju je činio kredit za obrtna sredstva i biznis kreditna kartica.

Veliku novinu u poslovanju oba segmenta predstavlja novi pristup koji je uveden kroz Projekat povećanja efikasnosti prodaje, a koji je doprineo poboljšanju kvaliteta prodaje, kao i podizanju efikasnosti i brzine rada.

Pored unapređenja kvaliteta prodaje, učinjen je značajan napredak u pogledu skraćenja procesa obrade kreditnih zahteva, putem decentralizacije i automatizacije procesa rada, kao i korišćenjem alternativnih kanala prodaje (Kontakt centar, direktni agenti prodaje, slanje direktnih ponuda klijentima). Pomenuta poboljšanja doprinela su očuvanju konkuretne prednosti na tržištu i postizanju visokog nivoa zadovoljstva klijenata.

Poslovanje sa malom privredom

Poslovanje sa malom privredom

4� www.raiffeisenbank.co.yu

Foreign currency trading

In 2007, Raiffeisen banka retained its leading position in the market with regard to trading in foreign currency and banknotes. Within the total volume of foreign exchange trade, the market share achieved by trading with corporate clients accounted for 19.01%, while the share representing trading with banks accounted for 13.68%.

The dynamic of offer and demand on the market led to a significant growth in the annual interbank trade turnover, from EUR 7.2 billion in 2006 to EUR 23.0 billion in 2007, also leading to an enhancement of the volatility of the euro to dinar exchange rate. In the second half of the year, banks reached an agreement on further advancing SPOT trade and introducing new mechanisms in the system of trading, which are going to be implemented during the course of 2008.

In reference to the foreign exchange rate policy, the National Bank of Serbia shifted to the flexible foreign exchange management regime in 2007, significantly reducing its presence in the foreign currency market (in 2006, the NBS intervened 132 times, and in 2007 only 17 times). The scope of NBS interventions in 2007 amounted to EUR 135.5 million. Furthermore, starting from June, the NBS also sold euros in a direct trade with banks based on the inflow coming from authorised exchange offices, in amounts not exceeding EUR 3.0 million a day.

Money Market

The National Bank of Serbia kept its restrictive monetary policy course. The basic instrument used to this effect was reference rate (two-week repo). Reference rate early in 2007 amounted to 14%, gradually dropping to the level of 9.5%, only to be raised by the NBS to 10% late in the year in accordance with the development of basic inflation and the objective for 2008. The scope of interest in placements in repo transactions and NBS bills remained at an enviable level throughout the whole year. The year 2007 marked a growth trend in transactions in the interbank money market. The biggest growth was registered in O/N placements in the local and foreign currencies.

At the initiative of Raiffeisen banka, the NBS assumed the task of collecting data about O/N placements among banks, enhancing the credibility and depth of the entire banking market by the published data – BEONIA (Belgrade Over Night Index Average), which has been published daily by the National Bank of Serbia, on its internet page.

Treasury and Investment Banking

Treasury and Investment Banking

4�www.raiffeisenbank.co.yu

Trgovanje devizama

Raiffeisen banka je u 2007. godini očuvala lidersku poziciju na tržištu u trgovanju devizama i efektivnim stranim novcem. U ukupnoj trgovini devizama, sa korporativnim klijentima ostvareno je tržišno učešće od 19,01%, dok je u trgovini sa bankama udeo iznosio 13,68%.

Dinamika ponude i tražnje na tržištu je dovela do značajnog rasta u godišnjem prometu trgovanja među bankama, sa 7,2 milijardi evra u 2006. na 23,0 milijardi evra u 2007. godini, kao i do povećane volatilnosti kursa dinara u odnosu na evro. U drugoj polovini godine banke su postigle dogovor o daljem unapredenju SPOT trgovine i uvođenju novih mehanizama u sistem trgovanja, koji će biti implementirani tokom 2008. godine.

Što se tiče politike deviznog kursa, Narodna Banka Srbije je u drugoj polovini 2007. godine prešla na režim fleksibilnog deviznog kursa i značajno smanjila svoje prisustvo na deviznom tržištu (2006. godine NBS je intervenisala 132 puta, a 2007. godine samo 17 puta). Obim intervencija NBS u 2007. godini iznosio je 135,5 miliona evra. Takođe, počevši od juna, NBS je prodavala evre i u direktnoj trgovini sa bankama, iz priliva od ovlašćenih menjača, i to u iznosima koji nisu prelazili tri miliona evra dnevno.

Tržište novca

Narodna banka je zadržala restriktivni kurs monetarne politike. Kao osnovni instrument korišćena je referentna stopa (dvonedeljni repo). Referentna stopa je početkom 2007. godine iznosila 14%, i postepeno se spuštala na nivo od 9,5%, da bi, u skladu sa razvojem bazne inflacije i ciljem za 2008. godinu, NBS na kraju godine podigla referentnu kamatnu stopu na 10%. Interesovanje za plasmane u repo poslove i blagajničke zapise NBS je ostalo na zavidnom nivou tokom čitave godine. U 2007. godini zabeležen je trend rasta transakcija na međubankarskom novčanom tržištu. Najveći rast zabeležili su O/N plasmani u domaćoj i stranoj valuti.

Na inicijativu Raiffeisen banke, NBS je preuzela na sebe prikupljanje podataka o O/N plasmanima između banaka, dajući kredibilitet i dubinu celog bankarskog tržišta u publikovanom podatku – BEONIA (Belgrade Over Night Index Average), koji sada, uz ostale stope, Narodna Banka Srbije objavljuje dnevno na svojoj internet stranici.

Sredstva i investiciono bankarstvo

Sredstva i investiciono bankarstvo

50 www.raiffeisenbank.co.yu

Investment Banking and Brokerage Department

During the course of 2007, Raiffeisen banka achieved significant business results in the segment of investment banking. In securities trading, the bank positioned itself as one of the leaders among the banks authorised for trading on the stock exchange. Investment Banking and Brokerage Department achieved record results in both dealing and brokerage operations.

In the area of corporate activities in 2007, the bank organised share issues for local public companies.

The bank was the first in the country to provide the service of e-trade via its RaiffeisenOnLine system.

Custody Services