supporting standards comprise 35% of the u. s. history test 16 (e)

TRANSCRIPT

Supporting standards comprise 35% of the U. S. History Test

16 (E)

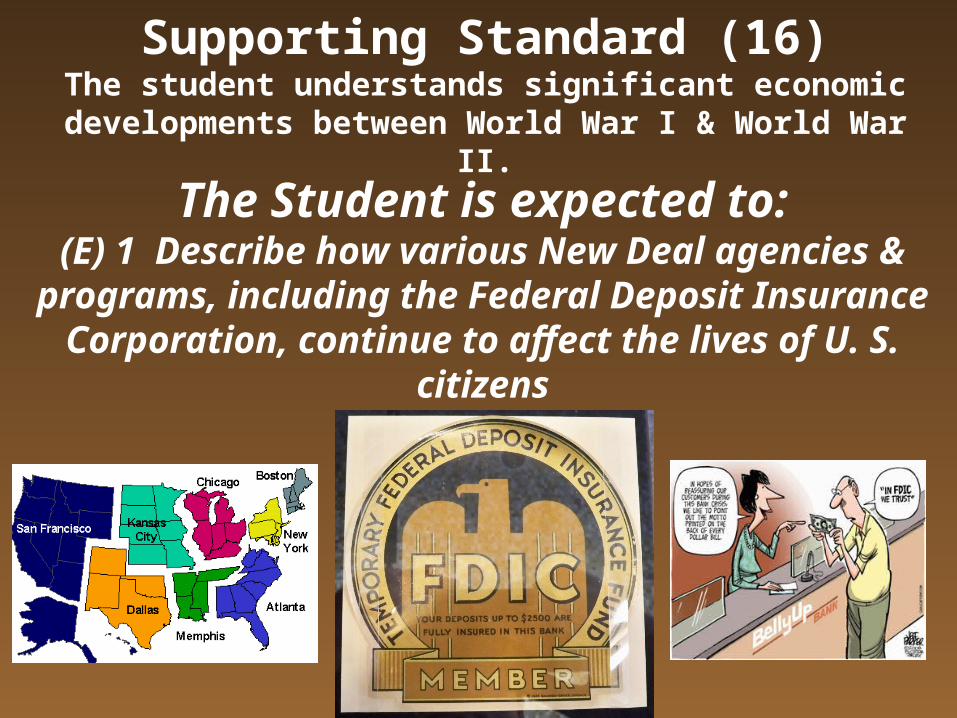

Supporting Standard (16)The student understands significant economic developments between World War I & World

War II.

The Student is expected to:(E) Describe how various New Deal agencies &

programs, including the Federal Deposit Insurance Corporation, the Securities & Exchange Commission, & the Social Security Administration,

continue to affect the lives of U. S. citizens

Supporting Standard (16)The student understands significant economic developments between World War I & World

War II.The Student is expected to:

(E) 1 Describe how various New Deal agencies & programs, including the Federal Deposit Insurance Corporation, continue to

affect the lives of U. S. citizens

The first crisis of FDR’s presidency was the

imminent collapse of America’s banking system.

FDR responded by announcing to Americans

that the banks would close

until the government

could address the difficulty

The President’s actions The President’s actions forestalled further panic forestalled further panic

created by a nationwide run created by a nationwide run on the banks. on the banks.

THE CREATIONDuring the 1930s, the U.S. and the rest of the world experienced a severe

economic contraction known as the Great Depression. In the U.S. during the height of the Great Depression, the official unemployment rate was 25% and

the stock market had declined 75% since 1929. Bank runs were common because there was not insurance on deposits at banks, banks kept only a

fraction of deposits in reserve, and customers ran the risk of losing the money that they had deposited if their bank failed.

The Federal Deposit Insurance Corporation (FDIC) is a U. S. government corporation operating as an

independent agency created by the Banking Act of 1933 signed June 16, 1933 by President Franklin

Roosevelt. This legislation:

THE CREATIONDuring the 1930s, the U.S. and the rest of the world experienced a severe

economic contraction known as the Great Depression. In the U.S. during the height of the Great Depression, the official unemployment rate was 25% and

the stock market had declined 75% since 1929. Bank runs were common because there was not insurance on deposits at banks, banks kept only a

fraction of deposits in reserve, and customers ran the risk of losing the money that they had deposited if their bank failed.

The Federal Deposit Insurance Corporation (FDIC) is a U. S. government corporation operating as an

independent agency created by the Banking Act of 1933 signed June 16, 1933 by President Franklin

Roosevelt. This legislation:

• Established the FDIC as a temporary government corporation. The Banking Act of 1935 made the FDIC a permanent agency of the government and provided permanent deposit insurance maintained at the $5,000 level.

• Gave the FDIC authority to provide deposit insurance to banks• Gave the FDIC the authority to regulate and supervise state non-member

banks• Funded the FDIC with initial loans of $289 million through the U.S.

Treasury and the Federal Reserve, which was later paid back with interest• Extended federal oversight to all commercial banks for the first time• Separated commercial and investment banking (Glass–Steagall Act)• Prohibited banks from paying interest on checking accounts• Allowed national banks to branch statewide, if allowed by state law.

THIS LEGISLATION:

In 1933, the FDIC insured depositors money up to $2,500. That amount has increased over the last 80 years. As of January 2013, the FDIC

provides deposit insurance guaranteeing the safety of a depositor’s accounts in member banks up to $250,000 for each deposit ownership

category in each insured bank. As of September 30, 2012, the FDIC insured deposits at 7,181 institutions.

Historical insurance limits•1934 – $2,500•1935 – $5,000•1950 – $10,000•1966 – $15,000•1969 – $20,000•1974 – $40,000•1980 – $100,000•2008 – $250,000

In 1933, the FDIC insured depositors money up to $2,500. That amount has increased over the last 80 years. As of January 2013, the FDIC

provides deposit insurance guaranteeing the safety of a depositor’s accounts in member banks up to $250,000 for each deposit ownership

category in each insured bank. As of September 30, 2012, the FDIC insured deposits at 7,181 institutions.

The FDIC also examines and supervises certain financial institutions for safety and soundness, performs certain consumer-protection functions, and manages banks in receiverships (failed banks). The FDIC receives no congressional appropriations — it is

funded by premiums that banks and thrift institutions pay for deposit insurance coverage and from earnings on investments in

U.S. Treasury securities.

Insured institutions are required to place signs at their place of business stating that “deposits are

backed by the full faith and credit of the United States Government.” Since the start of FDIC insurance on January 1, 1934, no depositor has lost any insured

funds as a result of a failure.

The FDIC also examines and supervises certain financial institutions for safety and soundness, performs certain consumer-protection functions, and manages banks in receiverships (failed banks). The FDIC receives no congressional appropriations — it is

funded by premiums that banks and thrift institutions pay for deposit insurance coverage and from earnings on investments in

U.S. Treasury securities.

Insured institutions are required to place signs at their place of business stating that “deposits are

backed by the full faith and credit of the United States Government.” Since the start of FDIC insurance on January 1, 1934, no depositor has lost any insured

funds as a result of a failure. Today, each ownership category of a depositor’s money is insured separately up to the insurance limit, and separately at each bank.

Thus a depositor with $250,000 in each of three ownership categories at each of two banks would have six different insurance limits of

$250,000, for total insurance coverage of 6 × $250,000 = $1,500,000.

The Board of Directors of the FDIC is the governing body of the FDIC. The board is composed of five members, three appointed by the U. S. President with the consent of the U. S. Senate and two ex officio members. The three appointed members each serve six year terms. No more than three members of the board may be of the same political affiliation. The president, with the consent of the Senate, also designates one of the appointed members as chairman of the board, to serve a five-year term, and one of the appointed members as vice chairman of the board, to also serve a

five-year term. The two ex officio members are the Comptroller of the Currency and the director of the Consumer Financial Protection Bureau (CFPB).

The Board of Directors of the FDIC is the governing body of the FDIC. The board is composed of five members, three appointed by the U. S. President with the consent of the U. S. Senate and two ex officio members. The three appointed members each serve six year terms. No more than three members of the board may be of the same political affiliation. The president, with the consent of the Senate, also designates one of the appointed members as chairman of the board, to serve a five-year term, and one of the appointed members as vice chairman of the board, to also serve a

five-year term. The two ex officio members are the Comptroller of the Currency and the director of the Consumer Financial Protection Bureau (CFPB).

The first Board of Directors of the Federal Deposit The first Board of Directors of the Federal Deposit Insurance Corporation was sworn in all the Insurance Corporation was sworn in all the Treasury Department, Washington, D.C., on Treasury Department, Washington, D.C., on

September 11, 1933 From left, E. G. Bennett, FDIC September 11, 1933 From left, E. G. Bennett, FDIC Director; Walter J. Cummings, FDIC Chairman; J. Director; Walter J. Cummings, FDIC Chairman; J. F. T. O'Conner, Comptroller of the Currency and F. T. O'Conner, Comptroller of the Currency and FDIC Board Member, Administering the oath is J. FDIC Board Member, Administering the oath is J.

F. Douglas of the Treasury Department.F. Douglas of the Treasury Department.

Supporting Standard (16)The student understands significant economic developments between World War I & World

War II.

The Student is expected to:(E) 2 Describe how various New Deal agencies & programs, including the Securities & Exchange Commission,

continue to affect the lives of U. S. citizens

The U.S. Securities and Exchange Commission (SEC) is an agency of the U. S. federal government. It was created during the Great Depression that followed the Crash of 1929. The main reason for the creation of the SEC was to regulate the stock market. The SEC holds primary responsibility

for enforcing the federal securities and regulating the securities industry, the nation’s stock and options exchanges, and other activities and

organizations, including the electronic securities markets in the United States.

The Securities Exchange Act of 1934 (15 U. S. C., § 78d) regulates sales of securities in the secondary market . Section 4 of the 1934 act created the U.S. Securities

and Exchange Commission to enforce the federal securities laws; both laws are considered parts of FDR’s

New Deal raft of legislation.

The U.S. Securities and Exchange Commission (SEC) is an agency of the U. S. federal government. It was created during the Great Depression that followed the Crash of 1929. The main reason for the creation of the SEC was to regulate the stock market. The SEC holds primary responsibility

for enforcing the federal securities and regulating the securities industry, the nation’s stock and options exchanges, and other activities and

organizations, including the electronic securities markets in the United States.

In addition to the June 6th Securities Exchange Act of 1934 that created it, the SEC enforces the Securities

Act of 1933, the Trust Indenture Act of 1939, the Investment Company Act of 1940, the Investment Advisers Act of 1940, the Sabanes-Oxley Act of 2002,

and other statutes.

The enforcement authority given by Congress allows the SEC to bring civil enforcement actions against individuals or companies

alleged to have committed accounting fraud, provided false information, or engaged in insider trading or other violations of

the securities law. The SEC also works with criminal law enforcement agencies to prosecute individuals and companies

alike for offenses which include a criminal violation.

In addition to the June 6th Securities Exchange Act of 1934 that created it, the SEC enforces the Securities

Act of 1933, the Trust Indenture Act of 1939, the Investment Company Act of 1940, the Investment Advisers Act of 1940, the Sabanes-Oxley Act of 2002,

and other statutes.

The enforcement authority given by Congress allows the SEC to bring civil enforcement actions against individuals or companies

alleged to have committed accounting fraud, provided false information, or engaged in insider trading or other violations of

the securities law. The SEC also works with criminal law enforcement agencies to prosecute individuals and companies

alike for offenses which include a criminal violation.

To achieve its mandate, the SEC enforces the statutory requirement that public companies submit quarterly and annual

report, as well as other periodic reports. In addition to annual financial reports, company executives must provide a

narrative account, called the “management discussion & analysis” (MD&A), that outlines the previous year of operations and

explains how the company fared in that time period.

The SEC consists of five Commissioners appointed by the U. S. President, with the advice and consent of the U. S. Senate. Their

terms last five years, and are staggered so that one Commissioner’s term ends on June 5 of each year. To ensure that the SEC

remains non-partisan, no more than three Commissioners may belong to the same political party. The President also designates one of the Commissioners as Chairman, the SEC’s top executive.

The SEC consists of five Commissioners appointed by the U. S. President, with the advice and consent of the U. S. Senate. Their

terms last five years, and are staggered so that one Commissioner’s term ends on June 5 of each year. To ensure that the SEC

remains non-partisan, no more than three Commissioners may belong to the same political party. The President also designates one of the Commissioners as Chairman, the SEC’s top executive.

First SEC Commission: Ferdinand Pecora, George C. Mathews, Joseph P. Kennedy, Robert E. Healy and James M.

Landis

President Roosevelt appointed Joseph P. Kennedy Sr., father of future President John F.

Kennedy, to serve as the first Chairman of the SEC.

What is the grand irony of Kennedy’s appointment?

• Martha Stewart—2002 (in prison for 5 months in 2005)

• Bernie Madoff—2009 (at age 71, sentenced to 150 years imprisonment and forfeiture of $17.179 billion)

• Allen Stanford—2009 (110 year prison sentence plus forfeiture of $5.9 billion)

Recent High Profile SEC Cases

One of the most recent frauds addressed by the SEC concerns Bernard Madoff’s “feeder fund” that only invested with Madoff, and which,

according to the SEC, promised “curiously steady” returns. Initially, the SEC did not investigate indications that something was amiss in Madoff's investment firm. The SEC has been accused of missing numerous red flags and ignoring tips on Madoff's alleged fraud.

Ultimately, the SEC examination revealed that Madoff was running a Ponzi scheme.

A similar failure occurred in the case of Allen Stanford, who sold fake certificates of deposit to tens of thousands of people, many

of them working-class retirees. In 1997, the SEC’s own examiners spotted the fraud and warned about it. But the Enforcement

division would not pursue Stanford, despite repeated warnings by SEC examiners over the years. After the Madoff fraud emerged,

the SEC finally took action against Stanford in 2009.

One of the most recent frauds addressed by the SEC concerns Bernard Madoff’s “feeder fund” that only invested with Madoff, and which,

according to the SEC, promised “curiously steady” returns. Initially, the SEC did not investigate indications that something was amiss in Madoff's investment firm. The SEC has been accused of missing numerous red flags and ignoring tips on Madoff's alleged fraud.

Ultimately, the SEC examination revealed that Madoff was running a Ponzi scheme.

A similar failure occurred in the case of Allen Stanford, who sold fake certificates of deposit to tens of thousands of people, many

of them working-class retirees. In 1997, the SEC’s own examiners spotted the fraud and warned about it. But the Enforcement

division would not pursue Stanford, despite repeated warnings by SEC examiners over the years. After the Madoff fraud emerged,

the SEC finally took action against Stanford in 2009.

In an acknowledgment that the Securities and Exchange

Commission has fallen behind the traders it regulates, the agency is

turning to one of those high-frequency trading firms for help.

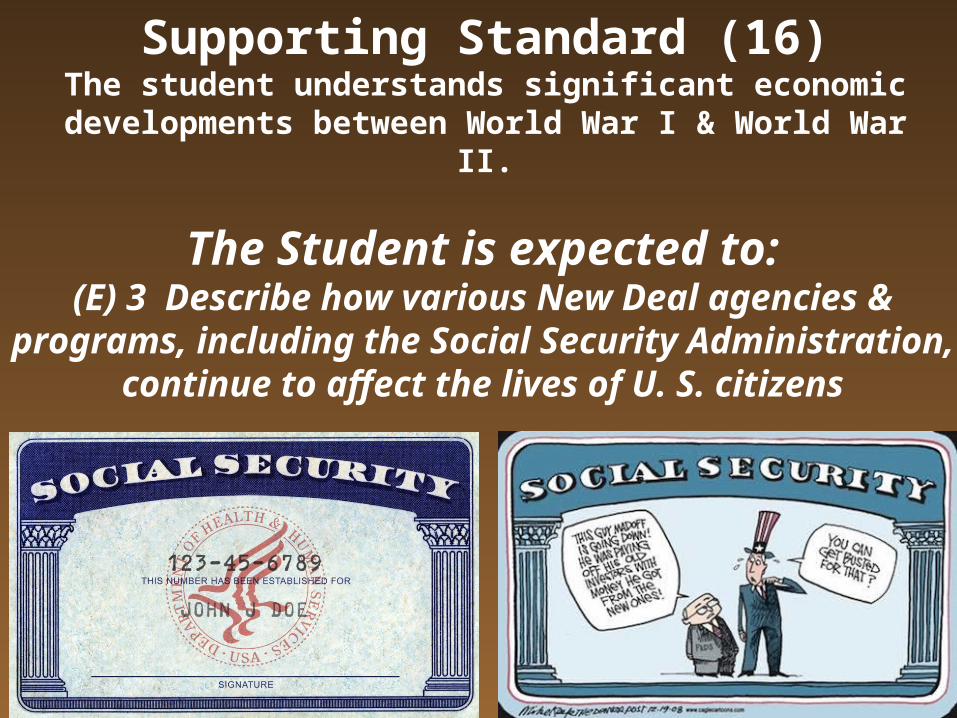

Supporting Standard (16)The student understands significant economic developments between World War I & World

War II.

The Student is expected to:(E) 3 Describe how various New Deal

agencies & programs, including the Social Security Administration, continue to affect

the lives of U. S. citizens

The U. S. Social Security Administration (SSA) is an independent agency of the United States federal government that administers Social Security, a social insurance program consisting of retirement, disability,

and survivors’ benefits. To qualify for these benefits, most American workers pay Social Security taxes on their earnings; future benefits are

based on the employees’ contributions. Social Security is the largest social welfare program in the United States, constituting 37% of

government expenditure and 7% of GDP.

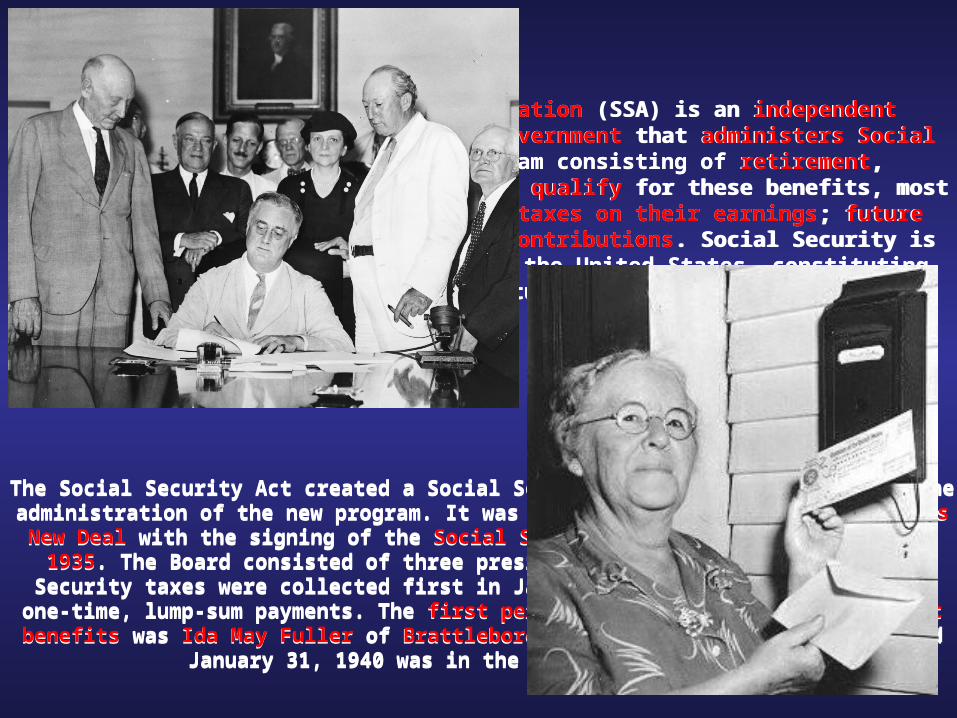

The Social Security Act created a Social Security Board (SSB), to oversee the administration of the new program. It was created as part of President FDR’s New Deal with the signing of the Social Security Act of 1935 on August 14,

1935. The Board consisted of three presidentially appointed executives. Security taxes were collected first in January 1937, along with the first one-time, lump-sum payments. The first person to receive monthly retirement

benefits was Ida May Fuller of Brattleboro, Vermont. Her first check, dated January 31, 1940 was in the amount of US$22.54.

The U. S. Social Security Administration (SSA) is an independent agency of the United States federal government that administers Social Security, a social insurance program consisting of retirement, disability,

and survivors’ benefits. To qualify for these benefits, most American workers pay Social Security taxes on their earnings; future benefits are

based on the employees’ contributions. Social Security is the largest social welfare program in the United States, constituting 37% of

government expenditure and 7% of GDP.

The Social Security Act created a Social Security Board (SSB), to oversee the administration of the new program. It was created as part of President FDR’s New Deal with the signing of the Social Security Act of 1935 on August 14,

1935. The Board consisted of three presidentially appointed executives. Security taxes were collected first in January 1937, along with the first one-time, lump-sum payments. The first person to receive monthly retirement

benefits was Ida May Fuller of Brattleboro, Vermont. Her first check, dated January 31, 1940 was in the amount of US$22.54.

The administration of the Medicare program is a responsibility of the Centers for Medicare & Medicaid Services, but SSA offices are used for determining initial eligibility, some processing of premium payments, and for limited public

contact information. They also administer a financial needs-based program which supplements Medicare Part D program

enrollees.

The SSA’s coverage under the Social Security Acts originally covered nearly all workers in the continental U. S. and Alaska, Hawaii, & the

territories of, Guam and the Commonwealth of the Northern Marianas Islands below the age of 65. All workers in interstate

commerce & industry were required to enter the program, except railroad, state and local government workers. In 1939, the age

restriction for entering Social Security was eliminated.

Most state and local government workers were eventually brought into the Social Security system under “Section 218

Agreements.” The original 218 interstate instrumentalities were signed in the 1950s. All states have a Section 218 agreement

with the Federal government's Social Security Administration. For more information see Chapter 10 of this Social Security

Handbook.

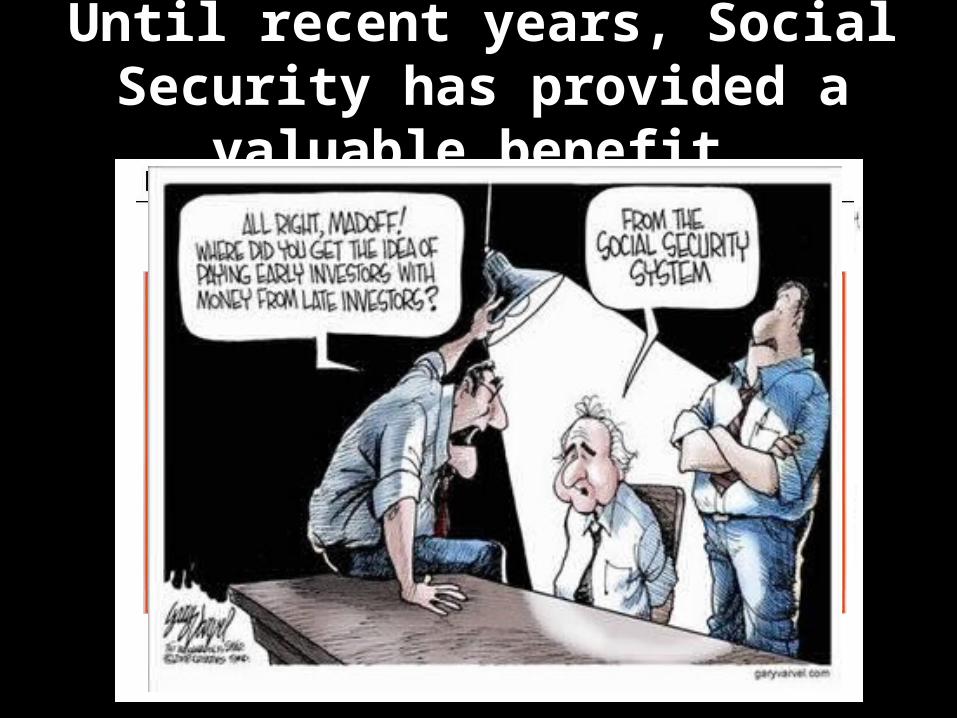

Until recent years, Social Security has provided a

valuable benefit.

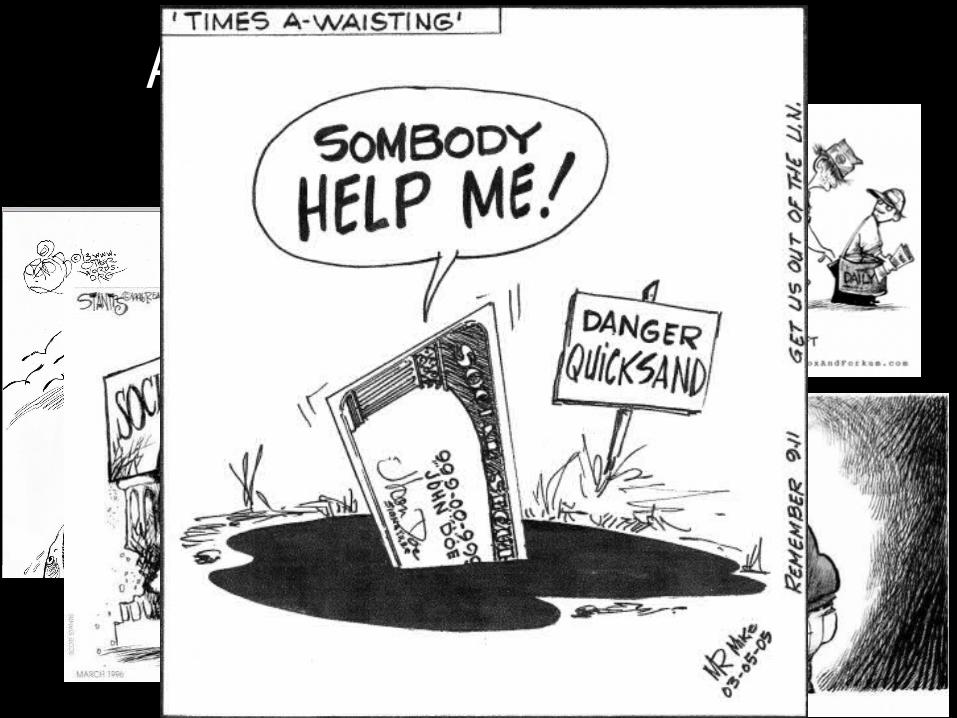

WHO is going to pay for all of this???

And the cartoonists continue on

Who will make up the difference?

The “Numbers” Don’t Lie

Fini