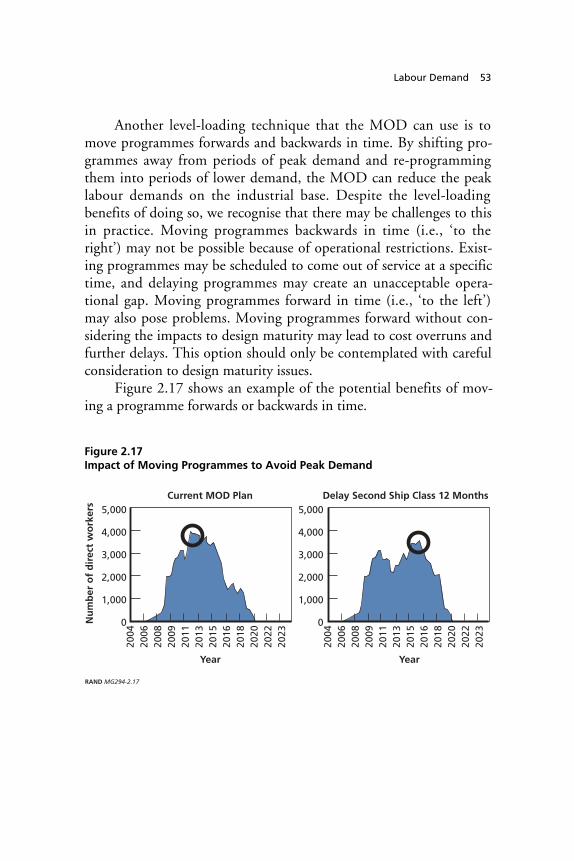

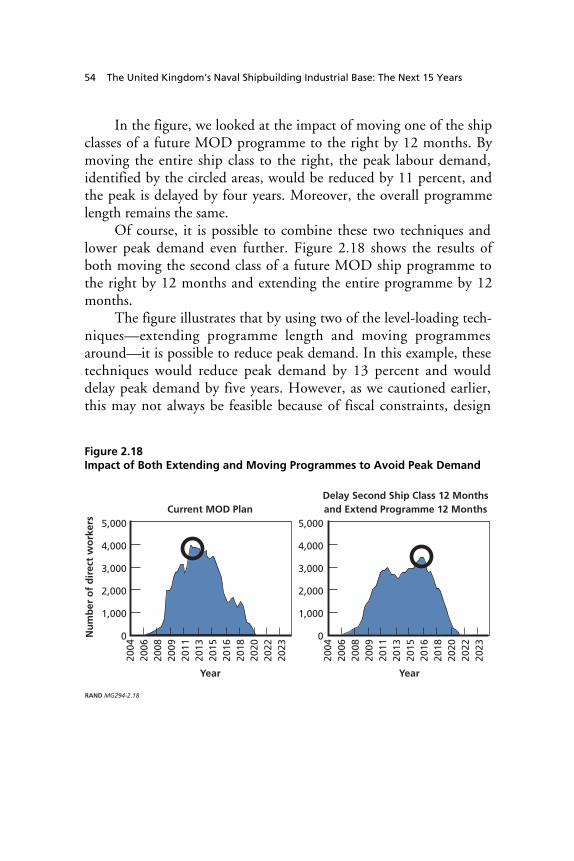

support rand for more information for the united kingdom‘s ministry of defence approved for public...

TRANSCRIPT

This PDF document was made available

from www.rand.org as a public service of

the RAND Corporation.

6Jump down to document

Visit RAND at www.rand.org

Explore RAND Europe

View document details

This document and trademark(s) contained herein are protected by law as indicated in a notice appearing later in this work. This electronic representation of RAND intellectual property is provided for non-commercial use only. Permission is required from RAND to reproduce, or reuse in another form, any of our research documents.

Limited Electronic Distribution Rights

For More Information

CHILD POLICY

CIVIL JUSTICE

EDUCATION

ENERGY AND ENVIRONMENT

HEALTH AND HEALTH CARE

INTERNATIONAL AFFAIRS

NATIONAL SECURITY

POPULATION AND AGING

PUBLIC SAFETY

SCIENCE AND TECHNOLOGY

SUBSTANCE ABUSE

TERRORISM AND HOMELAND SECURITY

TRANSPORTATION ANDINFRASTRUCTURE

The RAND Corporation is a nonprofit research organization providing objective analysis and effective solutions that address the challenges facing the public and private sectors around the world.

Purchase this document

Browse Books & Publications

Make a charitable contribution

Support RAND

This product is part of the RAND Corporation monograph series.

RAND monographs present major research findings that address the

challenges facing the public and private sectors. All RAND mono-

graphs undergo rigorous peer review to ensure high standards for

research quality and objectivity.

Prepared for the United Kingdom‘s Ministry of DefenceApproved for public release; distribution unlimited

The United Kingdom’s Naval Shipbuilding Industrial BaseThe Next Fifteen Years

Mark V. Arena

Hans Pung

Cynthia R. Cook

Jefferson P. Marquis

Jessie Riposo

Gordon T. Lee

The RAND Corporation is a nonprofit research organization providing objective analysis and effective solutions that address the challenges facing the public and private sectors around the world. RAND’s publications do not necessarily reflect the opinions of its research clients and sponsors.

R® is a registered trademark.

© Copyright 2005 RAND Corporation

All rights reserved. No part of this book may be reproduced in any form by any electronic or mechanical means (including photocopying, recording, or information storage and retrieval) without permission in writing from RAND.

Published 2005 by the RAND Corporation1776 Main Street, P.O. Box 2138, Santa Monica, CA 90407-2138

1200 South Hayes Street, Arlington, VA 22202-5050201 North Craig Street, Suite 202, Pittsburgh, PA 15213-1516

RAND URL: http://www.rand.org/To order RAND documents or to obtain additional information, contact

Distribution Services: Telephone: (310) 451-7002; Fax: (310) 451-6915; Email: [email protected]

Cover design by Barbara Angell Caslon

Cover photo from Reuters, via Landov LLC

The research described in this report was sponsored by the United King-dom’s Ministry of Defence. The research was conducted jointly in RAND Europe and the RAND National Security Research Division.

Library of Congress Cataloging-in-Publication Data

The United Kingdom’s naval shipbuilding industrial base : the next fifteen years / Mark V. Arena ... [et al.]. p. cm. “MG-294.” Includes bibliographical references. ISBN 0-8330-3706-4 (pbk. : alk. paper) 1. Shipbuilding industry—Great Britain. 2. Warships—Great Britain—Design and construction. 3. Great Britain. Ministry of Defence—Procurement. 4. Great Britain. Royal Navy—Procurement. I. Arena, Mark V.

VM299.7.G7U55 2005 338.4'7623825'0941—dc22

2005001980

iii

Preface

In the autumn of 2003, the United Kingdom’s Ministry of Defence(MOD) engaged the RAND Corporation to study the domesticcapacity for naval ship construction. The impetus for the study was aconcern on the MOD’s part that the confluence of several ship-building programmes (i.e., Astute, MARS, CVF, FSC, JCTS, andType 451) could potentially overburden the industry. The objectiveof the study was to take a strategic look at the shipbuilding industryover the next 15 years to determine where there might be capacitylimitations and to offer recommendations as to how any identifiedlimitations might be addressed. For example, are there productionskills or trades that will be in short supply? If so, what policy optionsare open to the government to remedy such a shortfall (trainingincentives, shifting of work, etc.)? The scope of the study was limitedto the UK industry, in line with current defence procurement policy.This report is the final product of that study and summarises theanalysis.

We organised our analysis by decomposing capacity into threemajor elements: labour, facilities, and suppliers. Labour encompassedall aspects of ship production (manufacture, design, engineering,management, outfitting, and support). The facilities analysis ad-dressed the throughput limitations of the major shipyard assets, suchas piers, docks, and slipways. For simplicity, we limited this examina-tion to facilities involved in final assembly and afloat outfitting. The____________1 For a full listing and description of these ships, see Table S.1 in the Summary.

iv The United Kingdom’s Naval Shipbuilding Industrial Base: The Next 15 Years

suppliers make up a major portion of the shipbuilding value chainand provide a wide range of different products and services—frompainting services to complex weapon systems. The suppliers’ ability tomeet any peak in demand will affect the ability of the MOD toprocure ships within the desired time frame and budget.

For our capacity evaluations, we relied on data surveys andinterviews with many firms and organisations associated with ship-building in the United Kingdom, including shipbuilders, ship repair-ers, suppliers, industry associations, and government organisations.This interaction took the better part of five months.

This report should be of special interest not only to the MOD’sDefence Procurement Agency (DPA) but also to service and defenceagency managers and policymakers involved in weapon system acqui-sitions on both sides of the Atlantic. It should also be of interest toshipbuilding industrial executives in the United Kingdom.

This research was sponsored by the MOD and conductedwithin RAND Europe and the International Security and DefensePolicy Center of the RAND National Security Research Division,which conducts research for the US Department of Defense, alliedforeign governments, the intelligence community, and foundations.

For more information on RAND Europe, contact the president,Martin van der Mandele. He can be reached by email at [email protected]; by phone at +31 71 524 5151; or by mail at RANDEurope, Netonweg 1, 2333 CP Leiden, The Netherlands. For moreinformation on the International Security and Defense Policy Center,contact the director, Jim Dobbins. He can be reached by email [email protected]; by phone at (310) 393-0411, extension5134; or by mail at RAND Corporation, 1200 South Hayes Street,Arlington, VA 22202-5050 USA. More information about RAND isavailable at www.rand.org.

v

Contents

Preface....................................................................... iiiFigures ...................................................................... xiTables .......................................................................xvSummary.................................................................. xviiAcknowledgements ...................................................... xxxvAbbreviations ...........................................................xxxvii

CHAPTER ONE

Introduction .................................................................1Warship Production Is a Unique Industry...................................2MOD Ship Programmes.....................................................5

Programmes Past Main Gate .............................................6Projects Pre–Main Gate...................................................7Other Speculative Programmes ...........................................9Notional Programme Timelines ........................................ 10

Business Environment of UK Naval Shipbuilding Industrial BaseSince 1985 ........................................................... 12

Issues for Policymakers..................................................... 16Study Structure ............................................................ 17

Plan ..................................................................... 18Labour .................................................................. 19Facilities................................................................. 19Suppliers ................................................................ 19

Survey of the UK Shipbuilding Industry .................................. 20Study Outline.............................................................. 21

vi The United Kingdom’s Naval Shipbuilding Industrial Base: The Next 15 Years

CHAPTER TWO

Labour Demand ........................................................... 23Methodology............................................................... 24Basic Assumptions ......................................................... 27

Additional Assumptions ................................................ 31Current MOD Plan: Overall Labour Demand ............................ 33Current MOD Plan: Demand for Specific Labour Skills.................. 35

Management Labour Skills ............................................. 35Technical Labour Skills ................................................. 36Structural Labour Skills................................................. 37Outfitting Labour Skills ................................................ 38Support Labour Skills................................................... 39

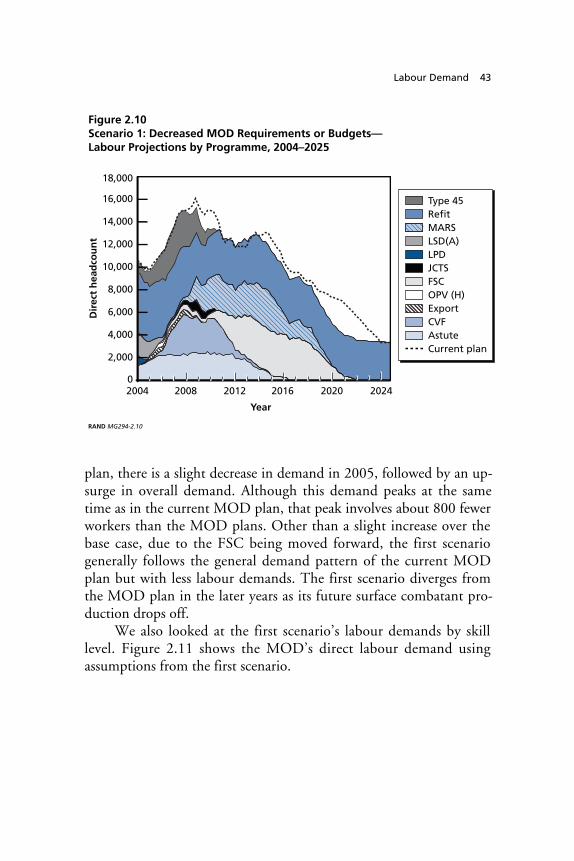

Macro Versus Micro View of Demand .................................... 39Alternate Future Scenarios ................................................. 41

Scenario 1: Decreased MOD Requirements or Budgets................ 42Scenario 2: Addition of Future Submarine to the MOD’s

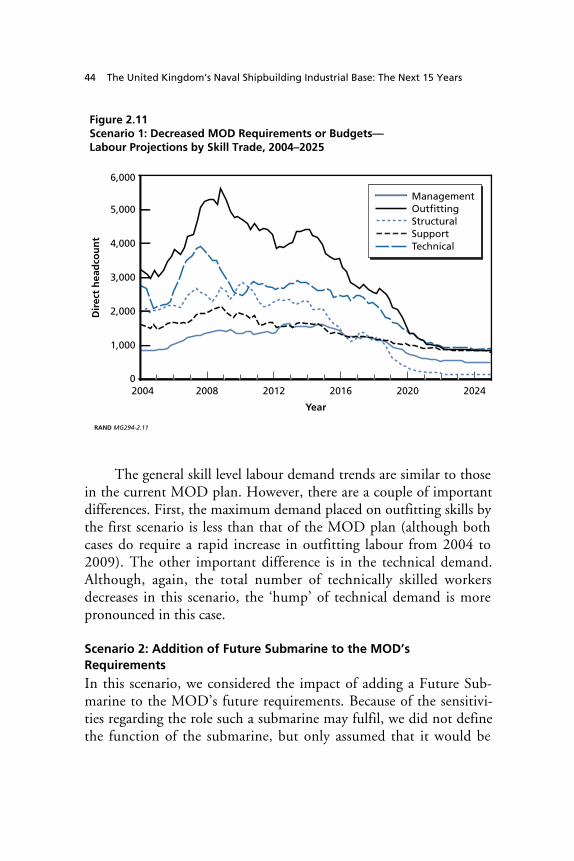

Requirements ........................................................ 44Scenario 3: Increased MOD Future Requirements..................... 47Future MOD Programme Challenges .................................. 50

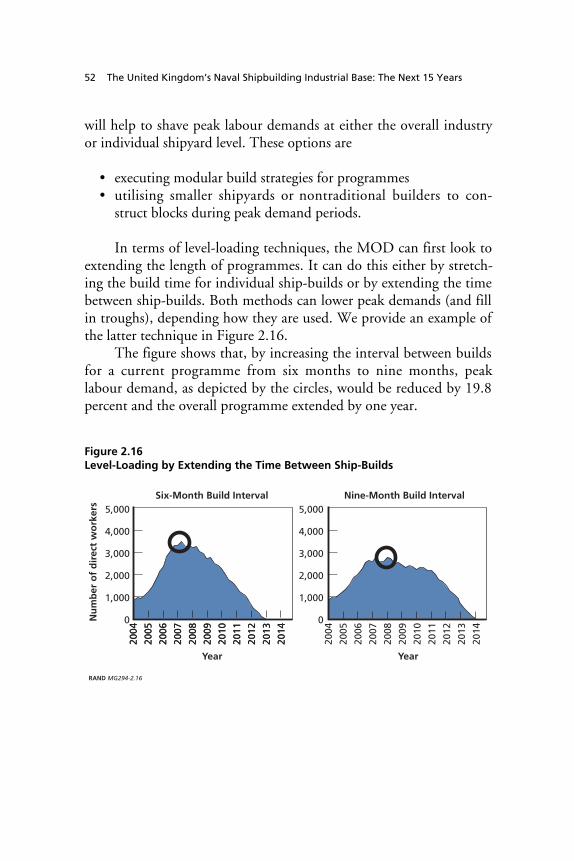

Options for Managing Increased MOD Demand......................... 51Illustrative Results of Level-Loading Future MOD

Labour Demand ..................................................... 55Other Build Strategies .................................................. 58

Summary................................................................... 59

CHAPTER THREE

The Supply of Naval Shipyard Labour in the United Kingdom ......... 61Employment Status of the UK Shipbuilding and Repair

Industrial Base ....................................................... 62Regional Differences in UK Shipyard-Related Employment........... 62Sector Employment in the UK Shipbuilding and Repair Industry..... 63UK Shipbuilding and Repair Industry Workers Are Ageing ........... 66Small Reliance on Temporary Workers................................. 67

Ability of the Naval Shipyards to Expand Their Workforces.............. 68Concerns About Labour Shortages ..................................... 68

Contents vii

Recruitment in the Shipbuilding and Repair Industry Faces SignificantObstacles ............................................................. 69

Shipyard Training Initiatives ........................................... 70Consequences of Unemployment, Demographic Changes, and Shipyard

Redundancies ........................................................ 71Recent Shipyard Recruiting Efforts..................................... 73Pools of Labour That Could Be Tapped................................ 75Shipyards Rely on Outsourcing to Varying Degrees ................... 76

A Comparison of the Supply of Naval Workers with the Demand UnderDifferent Future Scenarios........................................... 77

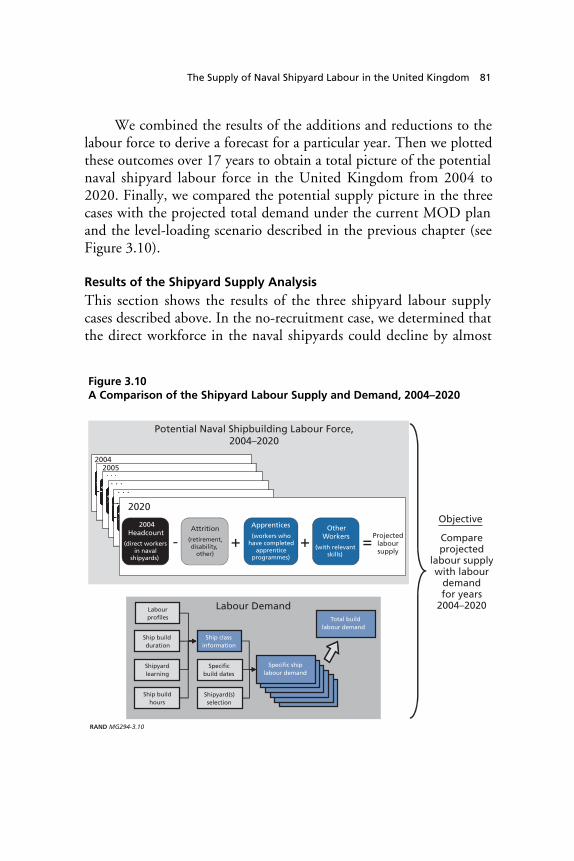

Three Supply Cases ..................................................... 78Shipyard Labour Supply Model ........................................ 80Results of the Shipyard Supply Analysis ................................ 81

Concluding Observations.................................................. 86

CHAPTER FOUR

Facilities Utilisation at the UK Shipyards ................................ 89Ship Production Facilities and Phases ..................................... 89How We Studied Facilities and Phases .................................... 91

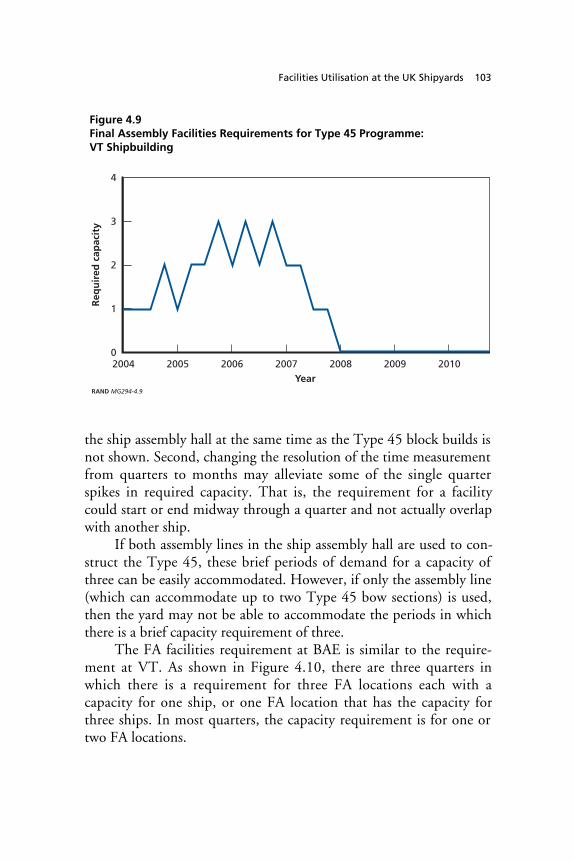

Identifying Demand and Assigning Facilities to Phases ................ 92Final Assembly Facilities’ Capacity and Considerations ................... 93Afloat Outfitting Facilities Capacity Considerations ...................... 96Capacity Implications for Future Programmes ...........................100

Type 45 ................................................................101CVF....................................................................106MARS..................................................................107Astute ..................................................................108LSD(A) ................................................................109Future Surface Combatant.............................................109Joint Casualty Treatment Ship ........................................110

Summary..................................................................110

CHAPTER FIVE

The UK Shipbuilding Supplier Industrial Base .........................113Research Approach........................................................113Characterising the Supplier Base—The Shipyard Perspective............115

viii The United Kingdom’s Naval Shipbuilding Industrial Base: The Next 15 Years

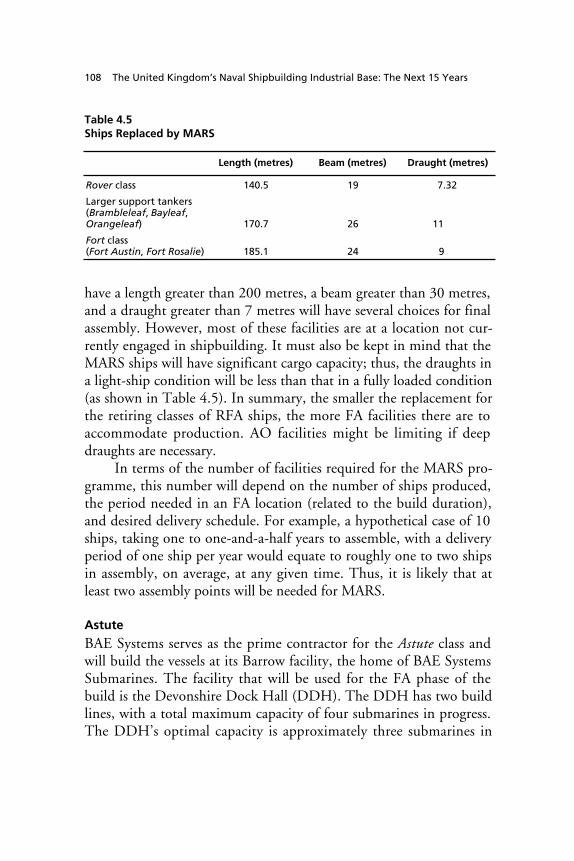

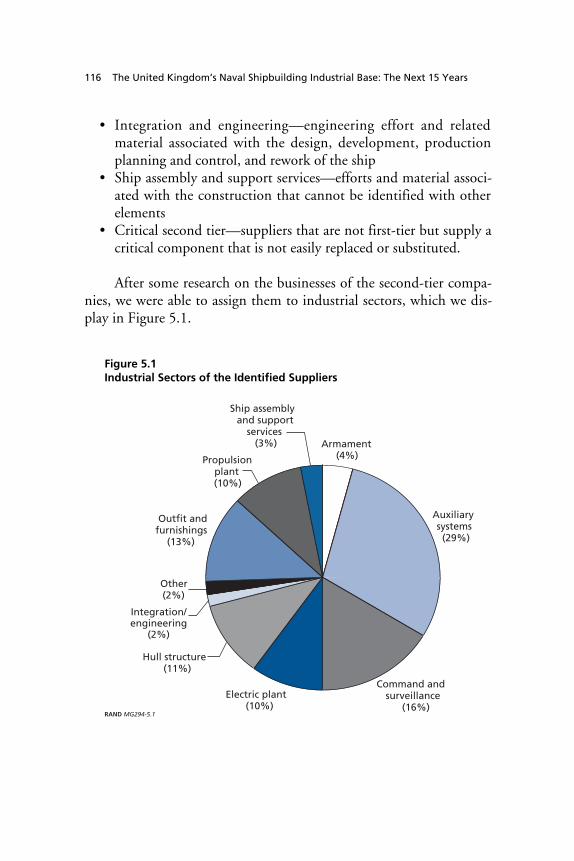

What They Supply.....................................................115Where They Are .......................................................117Three Measures of Supplier Strength ..................................118Summary...............................................................122

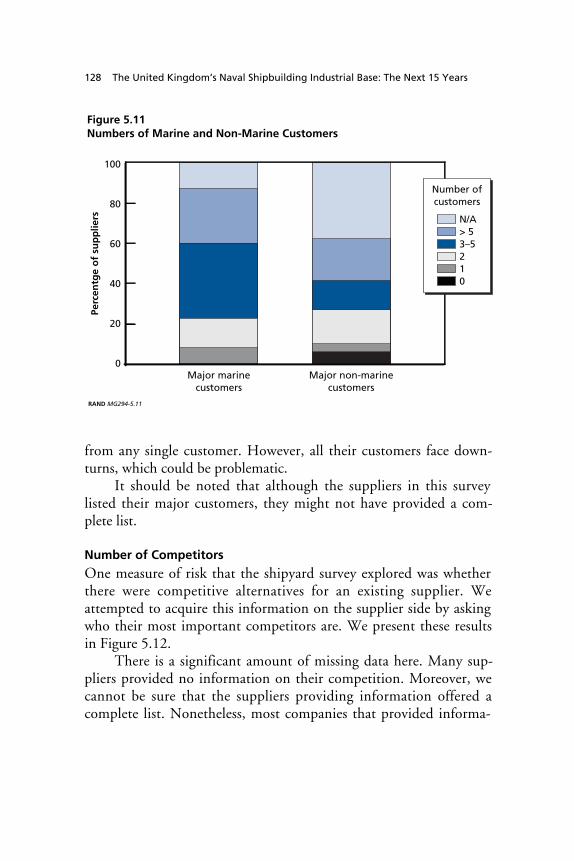

Supplier Survey Results ...................................................122Demographic Information on Sample Suppliers ......................123Suppliers’ Business Base................................................124Number of Customers .................................................127Number of Competitors ...............................................128Recruiting Challenges..................................................129Engineers Presented the Most Challenges for Recruiting..............129Challenges Working for the MOD ....................................130Summary...............................................................132

Results from Linking Shipyard and Supplier Surveys ....................132Developing an Effective Supplier Strategy................................133Conclusion................................................................134

CHAPTER SIX

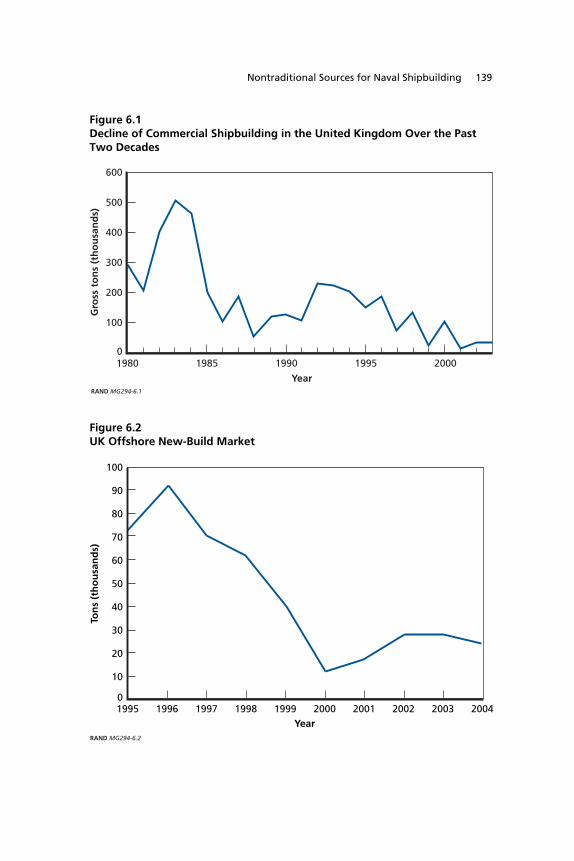

Nontraditional Sources for Naval Shipbuilding:Commercial Shipbuilding and Offshore Industries.................137

Declining Markets for Offshore and Commercial Work .................138Potential Resources Available .............................................140

Labour .................................................................141Facilities................................................................143

Strengths and Weaknesses of Using Offshore Firms in NavalProduction ..........................................................143

Summary..................................................................146

CHAPTER SEVEN

Issues for the Ministry of Defence to Consider .........................147Summary..................................................................147

Labour Demand .......................................................147Labour Supply .........................................................149Facilities................................................................150Suppliers ...............................................................151

Potential Remedial Actions That MOD Can Take ......................151

Contents ix

The MOD Needs to Make Long-Term Industrial Planning Part ofthe Acquisition Process .............................................154

Define the Appropriate Role of the Offshore Industry ................156Carefully Consider the Implications of Foreign Procurement of

Complete Ships .....................................................157Labour Wage Pressures During Peak Demand ........................158Encourage Long-Term Investment Through Multi-Ship Contracts ..159Consider the Feasibility of Competition in Light of the Industrial Base

Constraints..........................................................159Explore the Advantages of Common Design Tools ...................160

Conclusions ...............................................................160

APPENDIX

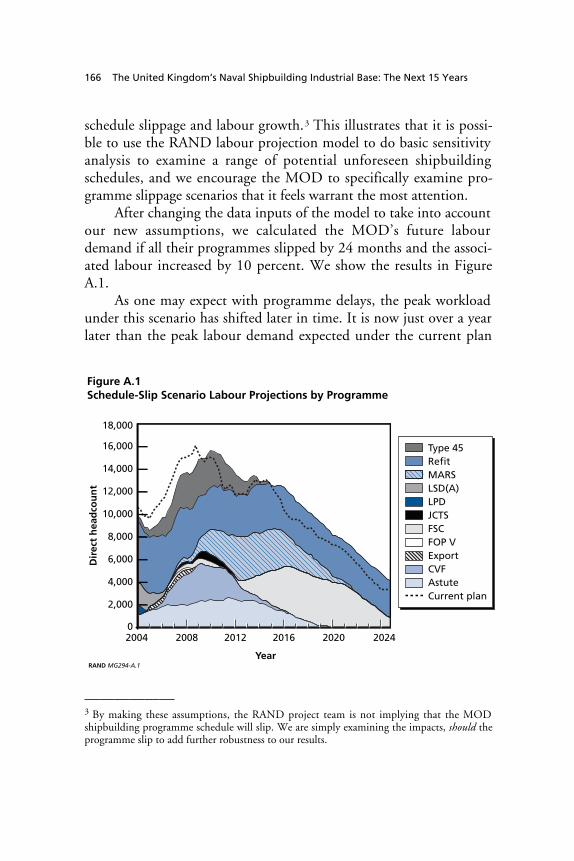

A. Effects of Schedule Slippage on MOD Labour Demands............163B. Ship Dimensions ......................................................171C. Skill Breakout, by Management/Technical and Manufacturing

Categories ............................................................173

References.................................................................175

xi

Figures

S.1. Schedule of MOD Naval Programmes, 2005–2020...............xxS.2. Future MOD Labour Demands, by Programme ................xxivS.3. Direct Labour Demands for the Current Plan and a Level-Loaded

Example...........................................................xxvS.4. Projected Shipyard Labour Supply Without Additional

Recruitment, 2004–2020 ........................................xxviS.5. Shipyard Employment Projections Versus Demand........... xxviiiS.6. Total UK Final Assembly and Afloat Outfitting Facility

Requirements, 2004–2020.......................................xxix1.1. Gantt Chart of MOD Naval Programmes over the Next

15 Years ........................................................... 101.2. Royal Navy Fleet Size over the Past Four Decades ............... 121.3. Number of Combatants Delivered Each Year .................... 131.4. History of Naval Shipbuilders Post-Privatisation................. 151.5. Study Hierarchy................................................... 182.1. RAND’s Basic Labour Forecasting Model........................ 242.2. Example of Direct Labour Distribution Curves for an Individual

Ship Class ......................................................... 272.3. Individual Ship Aggregation to Represent Entire Shipbuilding

Programme........................................................ 282.4. Future MOD Labour Demand, by Programme .................. 332.5. Future MOD Labour Demand for Management Skills,

2004–2025........................................................ 35

xii The United Kingdom’s Naval Shipbuilding Industrial Base: The Next 15 Years

2.6. Future MOD Labour Demands for Technical Skills,2004–2025........................................................ 36

2.7. Future MOD Labour Demand for Structural Skills,2004–2025........................................................ 37

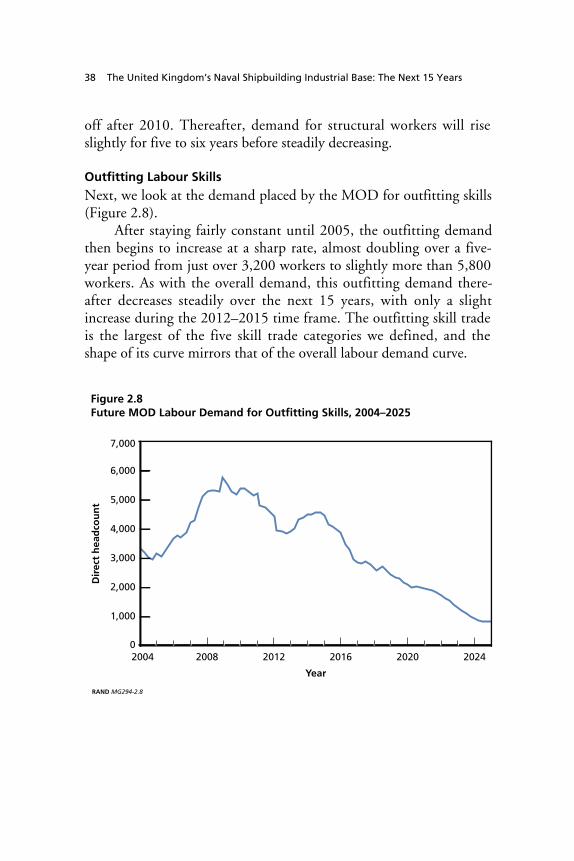

2.8. Future MOD Labour Demand for Outfitting Skills,2004–2025........................................................ 38

2.9. Future MOD Labour Demand for Support Skills,2004–2025........................................................ 39

2.10. Scenario 1: Decreased MOD Requirements or Budgets—Labour Projections by Programme, 2004–2025.................. 43

2.11. Scenario 1: Decreased MOD Requirements or Budgets—Labour Projections by Skill Trade, 2004–2025 .................. 44

2.12. Scenario 2: Addition of Future Submarine—Labour Projections by Programme, 2004–2025.................. 46

2.13. Scenario 2: Addition of Future Submarine—Labour Projections by Skill Trade, 2004–2025 .................. 47

2.14. Scenario 3: Increased MOD Future Requirements—Labour Projections by Programme, 2004–2025.................. 49

2.15. Scenario 3: Increased MOD Future Requirements—Labour Projections by Skill Level, 2004–2025 ................... 49

2.16. Level-Loading by Extending the Time Between Ship-Builds..... 522.17. Impact of Moving Programmes to Avoid Peak Demand ......... 532.18. Impact of Both Extending and Moving Programmes to Avoid

Peak Demand ..................................................... 542.19. Level-Loading Labour Projections, by Programme ............... 562.20. Base Case and Level-Loaded Demands Compared with Current

MOD Demand ................................................... 562.21. Level-Loading Labour Projections, by Skill Level ................ 573.1. UK Shipbuilding, Repair, and Offshore Employment in

the 1990s.......................................................... 633.2. Regional Shipbuilding, Repair, and Offshore Employment in

the 1990s.......................................................... 643.3. Share of Workers in Shipbuilding and Repair Subsectors

in 2000............................................................ 653.4. Number of Workers in the Naval Yards, 1999–2003 ............ 653.5. Age Profile of the Workforce in the Naval Shipyards in 2003 ... 67

Figures xiii

3.6. Unemployment Levels in Important Shipyard Townsin 2002............................................................ 72

3.7. Number of Recruits in the Naval Shipyards, 1999–2003 ........ 743.8. Total and Peak Outsourcing Undertaken by UK Naval

Shipbuilding and Repair Companies ............................. 773.9. Shipyard Labour Supply Model .................................. 80

3.10. A Comparison of the Shipyard Labour Supply and Demand,2004–2020........................................................ 81

3.11. Projected Shipyard Labour Supply by Skill Category WithoutAdditional Recruitment, 2004–2020 ............................. 82

3.12. Forecast of the Naval Shipyard Management and TechnicalWorkforce: Minimised Recruitment.............................. 83

3.13. Forecast of the Naval Shipyard Manufacturing Workforce:Minimised Recruitment .......................................... 84

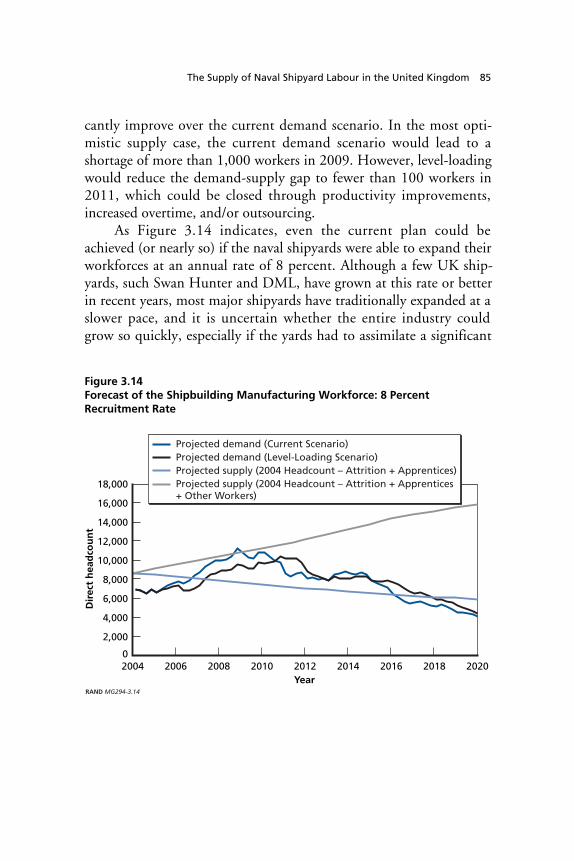

3.14. Forecast of the Shipbuilding Manufacturing Workforce:8 Percent Recruitment Rate ...................................... 85

4.1. Ship Production Timeline ........................................ 904.2. Distribution of Final Assembly Facility Lengths ................. 934.3. Distribution of Final Assembly Facility Beams ................... 954.4. Distribution of Final Assembly Facility Draughts ................ 954.5. Distribution of Afloat Outfitting Facility Lengths ............... 974.6. Distribution of Afloat Outfitting Facility Beams ................. 984.7. Distribution of Afloat Outfitting Facility Draughts .............. 994.8. Type 45 Work Allocation........................................1014.9. Final Assembly Facilities Requirements for Type 45 Programme:

VT Shipbuilding .................................................1034.10. Final Assembly Facilities Requirements for Type 45 Programme:

BAE Systems .....................................................1044.11. Afloat Outfitting Facilities Requirements for Type 45 Programme:

BAE Systems .....................................................1054.12. Final Assembly and Afloat Outfitting Facilities Requirements for

MOD Ships, 2004–2020 ........................................1115.1. Industrial Sectors of the Identified Suppliers ....................1165.2. Locations of Suppliers, by Country..............................1175.3. Suppliers’ Ability to Take on More Work .......................1195.4. Long-Term Stability and Viability of Suppliers .................120

xiv The United Kingdom’s Naval Shipbuilding Industrial Base: The Next 15 Years

5.5. Dependence on Supplier/Competition ..........................1215.6. Size of Suppliers, by Number of Employees in 2003............1235.7. Average Supplier Dependence on Different Sectors .............1255.8. Percentage of Suppliers’ Revenue Derived from MOD Ship

Programmes......................................................1265.9. Percentage of Suppliers’ Revenue Derived from All Ship and

Offshore Work...................................................1265.10. Percentage of Suppliers’ Revenue Derived from Military

Work.............................................................1275.11. Numbers of Marine and Non-Marine Customers...............1285.12. Numbers of Marine and Non-Marine Competitors.............1295.13. Ease of Recruiting Four Classes of Employees...................1306.1. Decline of Commercial Shipbuilding in the United Kingdom

Over the Past Two Decades .....................................1396.2. UK Offshore New-Build Market ................................139A.1. Schedule-Slip Scenario Labour Projections by Programme......166A.2. Schedule-Slip Scenario Labour Projections by Skill Level .......168A.3. Base Case, Level-Loaded, and Schedule Slip Demands Compared

to Current MOD Demand ......................................169

xv

Tables

S.1. Future MOD Ship Programmes.................................. xix1.1. Average Age and Full Ship Displacement of the Fleet............ 112.1. Current MOD Shipbuilding Programmes........................ 292.2. Projected MOD Shipbuilding Programmes ...................... 292.3. Scenario 1: Decreased MOD Requirements or Budgets

Programme Assumptions ......................................... 422.4. Scenario 2: Addition of Future Submarine Programme

Assumptions ...................................................... 452.5. Scenario 3: Increased MOD Future Requirements—

Programme Assumptions ......................................... 484.1. Number of Final Assembly Facilities at Naval Shipbuilders That

Can Accommodate a Ship with a Given Beam and Length ...... 964.2. Number of Final Assembly Facilities at Naval Repair and Other

Firms That Can Accommodate a Ship with a Given Beam andLength............................................................. 97

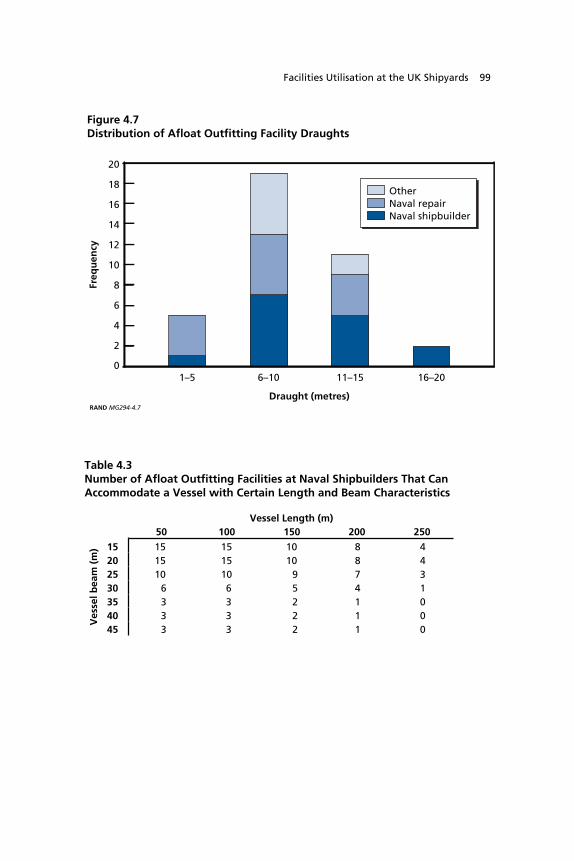

4.3. Number of Afloat Outfitting Facilities at Naval Shipbuilders ThatCan Accommodate a Vessel with Certain Length and BeamCharacteristics..................................................... 99

4.4. Number of Afloat Outfitting Facilities at Naval Repair and OtherFirms That Can Accommodate a Vessel with Certain Length andBeam Characteristics.............................................100

4.5. Ships Replaced by MARS........................................1086.1. Labour Resources of Medium-Sized Shipbuilders and

Other Firms......................................................142

xvi The United Kingdom’s Naval Shipbuilding Industrial Base: The Next 15 Years

7.1. Percentage Growth at Peak Demand Relative to CurrentEmployment Levels ..............................................148

B.1. Basic Ship Dimensions...........................................171C.1. Skill Breakout, by Management/Technical and Manufacturing

Categories ........................................................174

xvii

Summary

The United Kingdom’s Ministry of Defence (MOD) is in the earlystages of an ambitious effort to renew and upgrade its naval fleet overthe next two decades through the production of new ships and sub-marines. Defence policymakers are seeking to gain a fuller under-standing of the ability that shipyards, workers, and suppliers in theUnited Kingdom have to produce and deliver these vessels at the paceand in the order planned by the MOD.

This analysis, done at the request of the MOD’s Defence Pro-curement Agency (DPA), focused on answering three fundamentalquestions: Can the existing shipbuilding industrial base meet futuredemands? Do problems exist with the numbers and types of facilitiesor the numbers and skills of the workforce? and If problems exist orcan be anticipated, what can be done to alleviate them?

Relying both on public and proprietary data and on surveys ofgovernment and industry representatives,2 the analysis addressedthese questions by examining the capacity of the UK industrial base’scurrent workforce and facilities, identifying the demands for theseresources over the next two decades and exploring options to addresssituations in which future demands might exceed capabilities. Thestudy aimed to help MOD policymakers (1) gain an understanding ofthe capacity of the United Kingdom’s naval shipbuilding industrialbase to successfully implement the MOD’s current acquisition plan,____________2 By industry, we include naval shipbuilders and repairers; suppliers; design firms; and firmsinvolved in commercial maritime work (i.e., offshore industry, commercial repairers, andproducers).

xviii The United Kingdom’s Naval Shipbuilding Industrial Base: The Next 15 Years

and (2) gauge how alternative acquisition requirements, programmes,and schedules might affect the capacity of that industrial base.

MOD Ship Programmes3

The MOD is planning an extensive shipbuilding programme for thenext 15 years, which can be divided into two main categories. Thefirst category comprises programmes on contract that have alreadypassed through the MOD’s final approval process (Main Gate) andare somewhere in the demonstration and manufacture stage. The sec-ond category comprises prospective programmes that have yet to passMain Gate but which the MOD anticipates will be built. Of course,the future procurement programmes continue to evolve in line withthe strategic environment, financial imperatives, industrial develop-ments, and new opportunities. Any statement of the programmesthemselves, the number of ships, and the timings are speculative—particularly for the second category of programmes not yet past MainGate. Thus, the reader must keep this caveat in mind when inter-preting the results.

Table S.1 describes the potential future ship programmes and thepotential size of their production runs.

Figure S.1 lays out the potential design and production time-lines for the future programmes as identified in Table S.1.

The blue bars represent the programmes (or portions of pro-grammes) that are past Main Gate and on contract. The grey barsrepresent the programmes that are either pre–Main Gate or potentialadditional procurements for the class that have not been contracted.The timings are a synthesis of our assumptions, data provided by theIntegrated Project Teams (IPTs), and data provided by the shipyards.The dates are representative only and are not fixed as certain or arespecific requirements from the Equipment Capability Customers.____________3 The information for this section is extensively drawn from the DPA’s Web site(www.mod.uk/dpa/ipt/index.html) on the agency’s current projects, the Royal Navy Website (www.royal-navy.mod.uk), and Royal Navy (2003).

Summary xix

Table S.1Future MOD Ship Programmes

Programme Description

PotentialProduction

Run

On Contract/Past Main Gate

Astute-classattack sub-marine

The Astute is a new nuclear attack submarine (SSN)intended to replace the existing Trafalgar and Swiftsureclasses. It is being designed for the support of the Van-guard ballistic nuclear submarine (SSBN), antisubmarinewarfare, anti-surface warfare, surveillance and intelli-gence gathering, and land attack. There are three shipscurrently on order with the potential of six moreacquired, for a total of nine.

9

Bay-classlanding shipdock (LSD[A])

These new vessels are part of the Royal Fleet Auxiliary’s(RFA’s) rapid deployment force and will replace variouslanding ship logistic (LSL) classes in the RFA fleet. TheLSD(A)’s main role is logistic support, bringing troops,trucks, tanks, and cargo into battle. It can also be usedfor humanitarian missions.

4

Type 45 Type 45 will be a multi-role destroyer whose principalmission is antiair defence (DDG). The first six ships ofthe class are currently on order. There is a potential forup to six additional ships to be procured. Both BAESystems (Clyde Shipyards) and VT Shipbuildinga (Ports-mouth) are involved in the production of these ships.

12

Prospective/Pre–Main Gate

Future AircraftCarrier (CVF)

CVF is the Royal Navy’s next generation of aircraft car-rier, meant to replace the current Invincible-class (CVS)carrier.

2

Future SurfaceCombatant(FSC)

FSC is notionally thought to be frigate-sized vessel andwill replace the Type 23’s and Type 22’s currently in thefleet.

14

Joint CasualtyTreatmentShip (JCTS)

JCTS is single-ship programme that will provide ad-vanced medical capabilities to all three UK services. Theship can be used for combat operation support as wellas humanitarian missions. As a ‘grey hull’ and thereforedesignated to operate within a task force, the ship willnot be subject to the Geneva Conventions as would aconventional hospital ship.

1

Military AfloatReach andSustainability(MARS)

The MARS programme will be a series of ships (numberand types currently undefined) that will provide sup-plies to the fleet and forces ashore. These supplies are acombination of dry goods and provisions, generalstores, water, ammunition, and fuel products.

10

xx The United Kingdom’s Naval Shipbuilding Industrial Base: The Next 15 Years

Table S.1—Continued

Programme Description

PotentialProduction

Run

OffshorePatrol Vessels–(OPV[H])

The Royal Navy has provisional plans to replace theCastle class of offshore patrol vessels now in use in theFalkland Islands. These new ships will have the ability tooperate helicopters and will be leased on a similar basisas used with River-class patrol vessels.

2

Future Sub-marine

This submarine will be a follow-on to the Astute class.Its current size and mission are not yet defined.

7

Future Mine-hunter

This class will replace the minehunters currently in theRoyal Navy fleet.

4

aPart of VT Group, formerly known as Vosper Thornycroft.

Figure S.1Schedule of MOD Naval Programmes, 2005–2020

RAND MG294-S .1

2005 2010 2015 2020

LSD(A)

Type 45

OPV(H)

CVF

Astute

JCTS

MARS

FSC

Future Submarine

Future Minehunter

On Contract Prospective

Year

Figure S.1 shows that there will be periods when up to six pro-grammes will be in various stages of design and construction. Notonly will there be high concurrency, but these ships produced will be

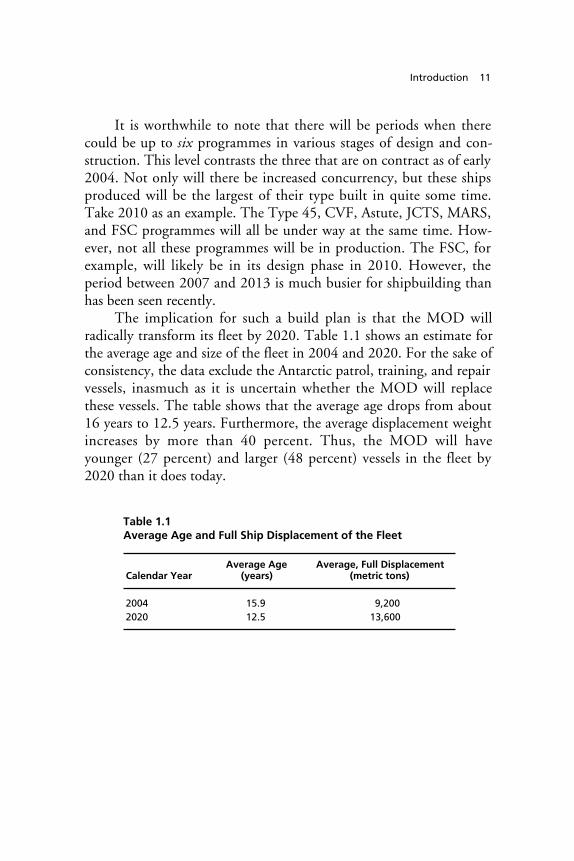

Summary xxi

the largest of their type built in quite some time. This situation con-trasts the current case in which there are only three programmes oncontract. In 2010, for example, the Type 45, CVF, Astute, JCTS,MARS, and FSC programmes will all be under way simultaneously;however, not all these programmes will be in production at the sametime. Nonetheless, the period between 2007 and 2013 is much busierfor naval shipbuilding than has been seen recently.

Today, only a handful of UK shipbuilders will likely be able toproduce these naval ships. After decades of consolidations and bank-ruptcies in the UK shipbuilding industry, only three major firms arecurrently involved in building ships for the MOD: BAE Systems,Swan Hunter, and VT Shipbuilding. In addition, there are threefirms primarily involved in the repair of warships: Babcock Engi-neering Services, Devonport Management Limited, and Fleet Sup-port Limited. For purposes of this report, the shipyards owned bythese six firms are collectively termed ‘naval shipyards’. An additionalfirm, Ferguson Shipbuilders, is also active but focuses mainly on thecoastal patrol, ferries, fishery protection, and other commercial mar-kets.

Policy Issues Pursued by RAND

This substantial MOD building programme, combined with theUnited Kingdom’s diminished industrial base, raises a number ofquestions for defence policymakers:4

• Is the MOD shipbuilding plan feasible given the constraints ofthe industrial base?

• What is the programme’s effect on the shipbuilders and shiprepairers?

____________4 An equally important issue, but beyond the scope of this study, is whether government canafford the shipbuilding plan. The increased level of shipbuilding activity will result in greaterdefence spending for naval acquisition. Whether this greater level of spending can be accom-modated within the broader defence budget is not clear.

xxii The United Kingdom’s Naval Shipbuilding Industrial Base: The Next 15 Years

• Is the supplier base robust enough to meet the demand?• Are there alternative timings for programmes that make the plan

more robust?• What is the effect if procurement quantities change?

At the request of the DPA, researchers of the RAND Corpora-tion began addressing these questions in the autumn of 2003. Theirmain goal was to help MOD decisionmakers understand the capacityof the UK naval shipbuilding industrial base and its ability to under-take the MOD’s shipbuilding programme over the next 15 years.

Study Structure

To analyse the issues facing the MOD, we decomposed the capacityevaluation into a supply and demand assessment in three distinctareas: labour, facilities, and suppliers. The study team evaluated theseareas with respect both to the MOD’s ‘current plan’ (which assumesthat everything will be built as envisioned by the MOD’s programmemanagers) and to several alternative shipbuilding scenarios:

• a pessimistic funding scenario, in which funding and/or require-ments decrease such that fewer vessels are purchased

• an optimistic funding scenario, in which requirements andfunding increase

• a new submarine scenario, in which a new, large submarine isdesigned and built

• a ‘level-loaded’ scenario, in which design and production tim-ings are lengthened.

Our evaluations depended on two surveys that we conductedwith firms involved in the shipbuilding industry and on interviewswith government officials and industry associations. The first surveythat the RAND team sent out requested information from severaldozen firms involved in maritime design, repair, and production ontheir employment, future workload demands, facilities available, and

Summary xxiii

their key suppliers. The second survey went to some 200 key suppli-ers that the firms had identified in the first survey. This latter surveyasked the suppliers about their employment, the relative competitive-ness of their market, their dependence on MOD and maritime work,and the challenges they anticipate in the future. After receiving bothsurveys, the RAND team held follow-on conversations with industryrepresentatives to clarify data and discuss issues about which the sur-veys had not inquired.

In addition, the RAND team interviewed officials at a numberof industry associations and government agencies.

How Will the MOD Programme Affect Shipyard Labour?

Labour Demand

This part of the analysis depended on a labour projection model thatthe RAND team developed.5 The team used data obtained in the firstsurvey of shipyards to populate this forecasting model, which allowedit to estimate future demands for labour emerging from the currentMOD acquisition plan and from the alternative scenarios describedabove.

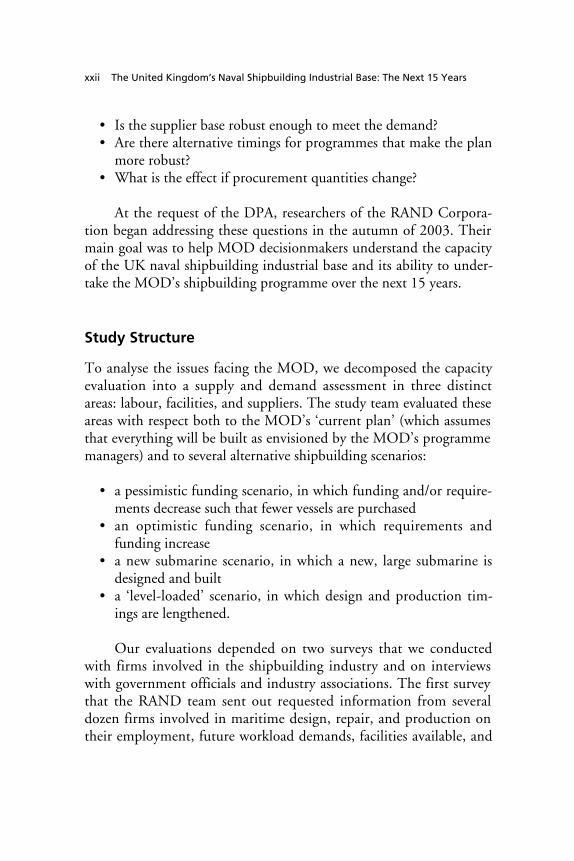

The team’s analysis of the current MOD plan found that over-lap of four large programmes—the Type 45, CVF, MARS, andAstute—is likely to cause demand for direct labour (all skills—e.g.,management, technical, and manufacturing) to peak in 2009 at alevel about 50 percent higher than the 2004 demand levels. Oncepast the peak, overall workload demand steadily declines for the fore-seeable future. We show this workload projection in Figure S.2.

Structural and outfitting trades likely will show the most signifi-cant increase (in absolute terms). The technical workforce demandpresents a more difficult challenge. The RAND team found that there

____________5 See Arena, Schank, and Abbott (2004) for more details.

xxiv The United Kingdom’s Naval Shipbuilding Industrial Base: The Next 15 Years

Figure S.2Future MOD Labour Demands, by Programme

Dir

ect

hea

dco

un

t

RAND MG294-S.2

18,000

0

Year

14,000

16,000

12,000

10,000

8,000

6,000

4,000

2,000

Type 45RefitMARSLSD(A)LPDJCTSFSCOPV (H)ExportCVFAstute

2004 20122008 2016 2020 2024

could be a sharp drop-off in demand for the technical workforce6 inthe next two to three years, resulting largely from the rundown of thedesign work for the Type 45 and Astute. Thereafter, the trendreverses dramatically as CVF, MARS, and JCTS place near-simultaneous demand for technical workers. In the span of a fewyears, the demand for technical workers nearly doubles from its low.

With one exception, the other scenarios we explored alsoinvolved similar sharp increases in demand for production labourfollowed by steady decreases. Such increases in labour demand willforce the naval shipbuilding and repair industrial base to rapidlyincrease its workforce, especially in specific outfitting, structural, andtechnical skills. Demands for technical workers under the alternativescenarios are much the same as the current plan. After an initialdecline, the demand for these workers increases drastically. One____________6 Technical workforce includes the follow functions: design, drafting/CAD, engineering,estimating, planning, and programme control. See Appendix C for more detail.

Summary xxv

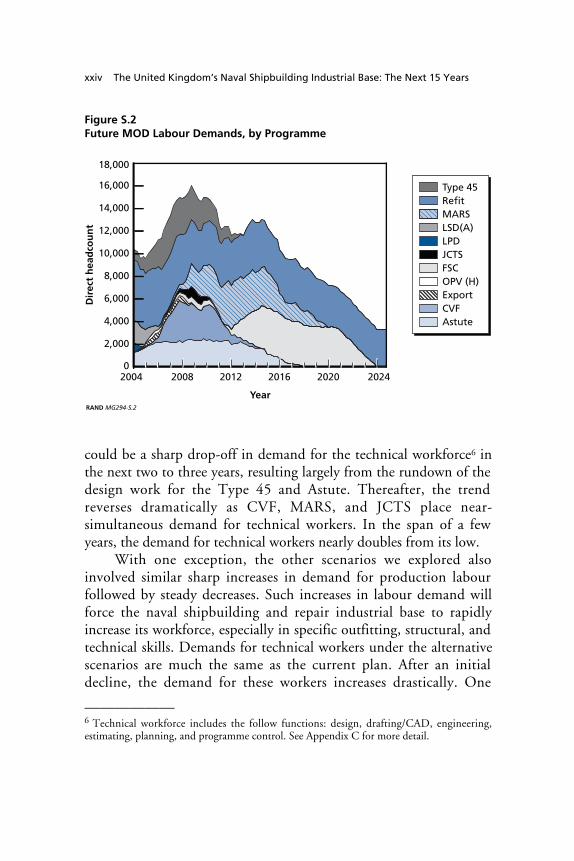

notable exception was the scenario that involved a Future Submarine,which could make substantial demands for technical workers past2010.

One way that the MOD could reduce these peak demandswould be to level-load the ship production plan, which would involvestarting programmes earlier or later, extending their build schedules,and increasing their build intervals. However, the MOD will need toconsider operational needs in determining whether such an approachis feasible. Figure S.3 shows the change in total, direct employmentfor the current plan and a level-loaded example relative to thedemand in 2004.

Labour Supply

The naval shipbuilding and repair industry will be challenged to meetthe peak workforce demands as outlined above. To determine thenature and extent of that challenge, the RAND team built a spread-sheet model to forecast the labour supply for naval shipbuilders andrepairers. The team then compared the potential supply picture withthe projected total demand under the current MOD plan and the

Figure S.3Direct Labour Demands for the Current Plan and a Level-Loaded Example

Level-loading

Current plan

–60

–40

–20

0

20

40

60

2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024Year

Perc

enta

ge

chan

ge

fro

m c

urr

ent

dem

and

RAND MG294-S.3

xxvi The United Kingdom’s Naval Shipbuilding Industrial Base: The Next 15 Years

level-loaded scenario described above. For the purposes of thisanalysis, the team combined the five skill subcategories into two:management/technical and manufacturing (structure, outfitting, anddirect support). This simplification was required because of thelimitations with data available.

As Figure S.4 indicates, the number of workers would drop frommore than 12,000 workers to around 4,600 in the next 17 years if nosteps are taken to replenish the workforce through hiring apprenticesor experienced workers from other industries or from the ranks of theunemployed. We in no way suggest that the shipyards will not replaceworkers. In fact, several have active apprentice and recruiting pro-grammes. Figure S.4 also shows how rapidly the current employmentranks decline because of the ageing of the workforce.

Figure S.4Projected Shipyard Labour Supply Without Additional Recruitment,2004–2020

Dir

ect

hea

dco

un

t

RAND MG294-S.4

16,000

0

Year’04 ’05 ’06 ’07 ’08 ’09 ’10 ’11 ’12 ’13 ’14 ’15 ’16 ’17 ’18 ’19 ’20

14,000

12,000

10,000

8,000

6,000

4,000

2,000

ManufacturingManagement and technical

Summary xxvii

Although there is no current shortage of workers, the shipyardsexpressed concern about their future ability to recruit particular skills(e.g., design, electrical, test and commissioning, and steel work).Many of the shipyards have begun apprentice programmes in recog-nition of the ageing problem that are aimed at maintaining current orcore workforce levels and not necessarily to meet future peak work-load.

There are, of course, other labour sources from which the ship-yards can draw workers. For example, some of the shipyards haverecently made workers redundant and may be able to rehire theseformer workers. There is also the opportunity to draw workers fromrelated industries and from among the general unemployed. Anotheralternative for the shipyards is to rely more heavily on outsourcedactivities, a trend that has been increasing as of late.7

Despite these additional sources of labour, the RAND teamconcluded that it will be difficult for the shipyards to grow to meetpeak labour demands. Figure S.5 shows workload demand for thebaseline and level-loading scenarios along with employment projec-tions. Assuming a modest growth rate, the shipyards as a whole maynot be able to meet peak labour demand for production workers.Even under the level-loaded scenario, shipyards will approximatelymeet the peak production demands. For the technical workforce,there are currently enough workers at the firms to grow to the neededpeak levels, but only if these workers are retained through the near-term downturn. In all, meeting the peaks in workload demand willrequire that shipyards share work to a greater extent than they donow.

These supply and demand results present labour issues at anaggregate (macro) level to simplify the presentation and to protectbusiness-sensitive information. The macro results are useful in thatthey portray the magnitude and the timing of the labour issues the

____________7 Of course, there is a limit to the extent that these activities can be outsourced. See Schanket al. (forthcoming) for more detail.

xxviii The United Kingdom’s Naval Shipbuilding Industrial Base: The Next 15 Years

Figure S.5Shipyard Employment Projections Versus Demand(baseline and level-loaded)

RAND MG294-S.5

Dir

ect

hea

dco

un

t

14,000

Employmentprojection

Employmentprojection

0

Year

12,000

10,000

8,000

6,000

4,000

2,000

2005 202020152010

Manufacturing

Dir

ect

hea

dco

un

t

7,000

0

Year

6,000

5,000

4,000

3,000

2,000

1,000

2005 202020152010

Management and Technical

BaselineLevel-loaded

BaselineLevel-loaded

industry faces. However, the macro view masks the effect at an indi-vidual shipyard or firm level. In a sense, the macro view could beinterpreted as a case in which there is an unlimited ability to sharework between firms. Thus, where the macro-level demand mightappear reasonable or achievable, there may be problems of either ir-regular or high demand for labour at an individual firm making sucha plan difficult to implement.

How Will the MOD Programme Affect Shipyard Facilities?

In this part of the analysis, the RAND study team focused on thefacility implications of the current MOD plan. In particular, the teamconcentrated on final assembly facilities (docks, slipways, land-levelareas, etc.) and afloat outfitting locations (mainly piers and quays).

Summary xxix

The facilities considered included those at the naval shipyards andsome commercial yards.

Not surprisingly, the RAND team found that different pro-grammes likely will stress different facilities. In general, as Figure S.6indicates, the demand for final assembly facilities will be particularlyhigh between 2006 and 2010.8

The Type 45 programme will create a substantial demand forfinal assembly and outfitting locations because of the build intervalbetween ships (assumed to be six months). Although the facilities onthe Clyde might be able to handle this schedule (with facilities up-grades and some careful scheduling), extending the build interval ofthe Type 45 to nine months might help to alleviate any potentialproblems and make the build schedule more robust.

Figure S.6Total UK Final Assembly and Afloat Outfitting Facility Requirements,2004–2020

RAND MG294-S.6

0

2

4

6

8

10

12

14

16

2004 2006 2008 2010 2012 2014 2016 2018 2020Year

Req

uir

ed c

apac

ity

FA facilityrequirement

AO facility requirement

Total numberavailableFA: 48AO: 37

____________8 Because of the sensitivity of the data, this demand does not include all refit and repairwork.

xxx The United Kingdom’s Naval Shipbuilding Industrial Base: The Next 15 Years

The sheer size of the ships in the CVF and MARS programmesposes challenges. CVF assembly will require some facilities upgradesand investments because no assembly location today could handle theCVF ships without modification or upgrade. Further complicatingthe picture is whether the final CVF assembly location will also beused to build large block portions of the ship. There is a potentialoverlap between the assembly of the first hull and the production ofblocks for the second hull. This overlap implies that the second hull’sblocks will either need to start construction outside the final assemblydock or be delayed until the first hull leaves the dock.

Similarly, large MARS ships will be equally challenged for a finalassembly location. Although there are facilities in the United King-dom that could construct these ships, it is likely that at least twofacilities (or a facility that can construct two ships at once) would beneeded based on the notional delivery schedule of one ship per year.In most cases, any of these candidate facilities would need to be up-graded or reopened—thus requiring investment.

How Will the MOD Programme Affect ShipbuildingSuppliers?

More than half the unit cost value of a naval vessel is provided byfirms other than the shipbuilder.9 So the ability of suppliers to meetthe demand based on the MOD’s plans is an important considerationin addressing the UK industry’s capacity. The study’s surveys of boththe shipyards and the suppliers indicate that there will be generallyfew issues surrounding the increased workload for the suppliers. Forthe most part, the suppliers do not rely on MOD business, so theyare less subject to the variations in demand (in contrast with the ship-yards). Further, most of the suppliers are based in the United King-dom. However, these suppliers have indicated that the uncertainty in____________9 The Clyde Shipyards Task Force Report (2002, p. 41).

Summary xxxi

the MOD’s programme hinders their ability to plan and invest in atimely way.

The Role of Nontraditional Sources for NavalShipbuilding

The UK commercial shipbuilding and offshore industry haveresources that may help to produce ships for the MOD. Theseresources are currently underemployed because of downturns in bothsectors; therefore, these resources could be available to the MOD forits shipbuilding programme. Medium-sized shipbuilders10 have had arole in the past and could play a role in the production of future shipclasses—from a builder of blocks and modules to a producer ofsmaller vessels. The offshore industry also has the potential to con-tribute to the programme. These firms have facilities and labourresources that could be employed—most notably in management andtechnical skills. However, its role, if any, will need to be carefullymatched to its capabilities and skills. For programmes that are similarto commercial products, the commercial/offshore industry could playa broader role in management, design, and production. However, forcombatant ships, their role will be more limited.

Issues for the MOD to Consider

The RAND team made short- and long-term observations for theMOD.

In the short term, the MOD could:

• Consider ways to level-load the labour demand. In essence, theMOD will need to carefully consider the timings of various pro-grammes. Some programmes will need to be shifted later, whileothers may need to have increased build intervals. It may also be

____________10 Appledore (owned by DML), Ferguson Shipbuilders, and Harland and Wolff.

xxxii The United Kingdom’s Naval Shipbuilding Industrial Base: The Next 15 Years

necessary to shift design work earlier to mitigate the near-termlack of demand (the near-term dip in technical labour demand).The DPA will need to consider the labour effects at the individ-ual firm or shipyard level to achieve the benefits of level-loading.Thus, any level-loading plan will need to be developed in con-sultation with industry.

• Work with the Department of Trade and Industry to encouragetraining in skills that are in demand outside the shipbuilding andrepair industry. The UK government and shipbuilding industryshould focus on training skills that are readily employable out-side shipbuilding. In this way, any resulting unemployment canbe minimised.

• Consider relaxing the shipbuilding industrial policy to mitigateproblems resulting from peak demand. The MOD should re-examine industrial policy with respect to obtaining work con-tent overseas. For example, the policy might allow UK shipyardsto obtain major units or subassemblies from abroad in cases inwhich there is peak demand and it is not possible to easilyobtain that content domestically.

• Encourage the use of more outsourcing. One way that commercialshipbuilders manage variable workloads is to employ out-sourcing vendors that provide services and goods.

• Evaluate the future of shipbuilding at Barrow. With the currentrealignment within BAE Systems, the Barrow-in-Furness facilityis exclusively dedicated to submarine production. The end ofsurface ship building in Barrow resulted in significant redun-dancies and the closure of some facilities. Barrow remains an un-tapped source of production capability and could likely play asignificant role in the coming shipbuilding programme.11

• Consider the use of medium-sized shipyards to meet some of thisdemand peak. Shipyards such as Ferguson, Appledore, and Har-land and Wolff could play a role in meeting the peak demandsby constructing blocks or structural units. Ferguson and Apple-

____________11 Since the original writing of the report, BAE Systems Naval Ships has stated that it is nowpossible to use Barrow surface ship capability.

Summary xxxiii

dore could produce smaller naval vessels, like the survey vesselsboth have produced in the last few years. Harland and Wolffwas, at one time, capable of producing large auxiliary vessels.Whether that capability could be cost-effectively reestablishedremains to be seen.

• Explore the utilisation of facilities for Type 45, CVF, and MARS.There may be facility challenges for these programmes, and theMOD needs to understand where there are potential conflictsand the actions that can be taken to mitigate them.

• Have the Supplier Relations Group (SRG) investigate suppliers thatare thought to be at risk. In our surveys, the shipyards identifiedcertain suppliers they felt were at risk. It might be worthwhilefor the SRG to interact with the shipyards and suppliers to bet-ter understand the ones at risk and any corrective actionsrequired.

In the long term, the MOD should, among other things:

• Make long-term industrial planning part of the acquisition process.This type of planning must become part of the process that theMOD uses to define the timing for the various naval require-ments. The potential benefits of long-term planning include theability to understand financial implications, reduce cost andschedule risks, and anticipate future problems. A strategicexamination of the overall build programme with respect to theindustrial impact should be done at least annually with an out-look of 10 to 15 years.

• Define an appropriate role for the offshore industry.12 Better work-sharing between the shipyards will be necessary to meet the peaklabour demand. The offshore industry may help the naval ship-building industry bring this collaboration about. Although theoffshore industry might not feature strongly in direct fabrica-

____________12 That is, those firms involved in the design, manufacture, and support of capital facilitiesfor oil and gas in the sea (mainly the North Sea for the United Kingdom).

xxxiv The United Kingdom’s Naval Shipbuilding Industrial Base: The Next 15 Years

tion, it might feature more prominently in assembly and inte-gration.

• Carefully consider the implications of foreign procurement of com-plete ships. Because foreign procurement carries risks, we rec-ommend that the MOD thoroughly take into account issuessuch as access to technology and political disruptions beforeprocuring entire vessels from abroad. The UK governmentcould allow shipyards to consider outsourcing work to foreignsources when there is a need to reduce a labour peak, workersare not available elsewhere in the United Kingdom, and workerswould only be needed for a short period.

• Encourage long-term investment through multi-ship contracts. Mostnaval shipyards have not modernised facilities during the pastseveral years. Longer-term contracts will allow the shipyards tojustify this type of major investment. However, the experienceof US programmes has shown that multi-ship contracts workbest for mature designs. So, such an approach may not includethe first-of-class ship.

• Consider the feasibility of competition in light of industrial baseconstraints. Competition may not always yield better prices orresult in a balanced allocation of work under conditions inwhich there are high resource demands. In such an environ-ment, it is possible that there will be fewer potential bidders onsubsequent programmes, that bidders will take on more workthan is optimal, or that shipyards will be less inclined to cooper-ate for fear of losing a competitive advantage.

• Explore the advantages of common and/or compatible three-dimensional computer-assisted design/computer-aided manufactur-ing (CAD/CAM) design tools. The MOD might want to facilitatea discussion among shipbuilding firms (and potentially includethe CAD/CAM vendors) to explore whether they should adopta common or interoperable design tool or establish standards sothat design work can be easily interchanged.

xxxv

Acknowledgements

This report would not have been possible without the contributionsof many firms and individuals. First, we would like to thank AndyMcClelland, Andrew Stafford, and David Twitchin of the DPA forguiding and helping to coordinate the study within the agency. Wewould also like to thank Stephen Highfield, also of the DPA, for hisassistance and coordinating our interaction with the Pricing andForecast Group. The authors would like to acknowledge the ship-building IPT leaders and members who participated in this study andprovided insight to and data for their programmes. Our gratitudegoes to Stephen French, Director General—Equipment, and themarine Directors of Equipment Capability (DECs) for their views onthe future shipbuilding programme. Also of the DPA, we are gratefulto Rear Admiral Ric Cheadle for his insightful comments on an ear-lier version of this report.

At RAND, we would like to thank the reviewers, Robert Mur-phy and Irv Blickstein, for the many improvements and suggestionsthey made to the text. The authors would also like to acknowledgethe assistance of Nathan Tranquilli and Ricardo Basurto-Dávila fortheir help with data analysis and modelling. We also thank JoanMyers for coordinating the document preparation.

Finally, we are deeply indebted to the shipbuilders, marinefirms, contractors, suppliers, and associations that participated in thestudy survey and interviews. Without their assistance and coopera-tion, this research would not have been possible.

xxxvii

Abbreviations

AO afloat outfitting

BES Babcock Engineering Services

BMT British Maritime Technologies

CAD/CAM computer-assisted design/computer-aidedmanufacturing

CVF Future Aircraft Carrier

CVS Invincible-class carrier

DDG antiair defence

DDH Devonshire Dock Hall

DEC Director of Equipment Capability

DML Devonport Management Limited

DPA Defence Procurement Agency

DTI Department of Trade and Industry

ECC Equipment Capability Customer

FA final assembly

FSC Future Surface Combatant

FSL Fleet Support Limited

HVAC heating, ventilation, and air conditioning

IPT Integrated Project Team

JCA Joint Combat Aircraft

JCTS Joint Casualty Treatment Ship

xxxviii The United Kingdom’s Naval Shipbuilding Industrial Base: The Next 15 Years

KBR Kellogg-Brown and Root

LPD(R) landing platform dock (replacement)

LPH helicopter landing platform

LSD(A) Landing Ship Dock Auxiliary

MARS Military Afloat Reach and Sustainability

MOD Ministry of Defence

ONS Office of National Statistics

OPV offshore patrol vessel

OPV(H) Offshore Patrol Vessel–Helicopter

PFG Pricing and Forecast Group

RFA Royal Fleet Auxiliary

SEMTA Sector Skills Council for Science, Engineering, andManufacturing Technology

SRG Supplier Relations Group

SSN nuclear attack submarine

STOVL short take-off, vertical landing

VAR voluntary attrition rate

VT Vosper Thornycroft

1

CHAPTER ONE

Introduction

Between September 2003 and April 2004, RAND researchers ana-lysed the capability of the shipbuilding industrial base in the UnitedKingdom to meet the demands of current and future Ministry ofDefence (MOD) programmes. The MOD is in the early stages of anambitious effort to procure upwards of 50 naval ships and submarinesover the next two decades, and defence policymakers are seeking togain a fuller understanding of the ability of UK shipyards, workers,and suppliers to produce and deliver those vessels at the pace and inthe order planned by the MOD.

This analysis, done at the request of the MOD’s Defence Pro-curement Agency (DPA), focused on answering three fundamentalquestions: Can the existing shipbuilding industrial base expand tomeet future demands? Do problems exist with the numbers and typesof facilities or the numbers and skills of the workforce? and If futureproblems do exist, what can be done to alleviate them?

Relying both on public and proprietary data and on surveys ofgovernment and industry representatives, the analysis addressed thesequestions by examining the capacity of the UK industrial base’s cur-rent workforce and facilities, identifying demands for those resourcesduring the next two decades, and exploring options to address situa-tions in which future demands might exceed available capabilities.The study aimed to help MOD policymakers (1) gain an under-standing of the capacity of the United Kingdom’s naval shipbuildingindustrial base to successfully implement the MOD’s current acquisi-

2 The United Kingdom’s Naval Shipbuilding Industrial Base: The Next 15 Years

tion plan, and (2) gauge how alternative acquisition requirements,programmes, and schedules might affect the capacity of that indus-trial base.

Warship Production Is a Unique Industry

The design and construction of warships1 is one of the more compli-cated weapon system engineering and manufacturing tasks that acountry can undertake. Warships require a complex integration ofcommunication, control, weapons, and sensors that must worktogether as a coherent system. These components, or subsystems, area mix of various technologies (e.g., electronics, mechanical systems,software). Oftentimes these technologies (particularly weapon sys-tems) are state of the art or are undergoing development at the time aprogramme begins.

Moreover, warships must generate power to operate these sys-tems and propel the ship. For surface ships, the method of powergeneration is typically gas turbines or diesel engines. Submarines gen-erate power from diesel engines or nuclear reactors. Similarly, aircraftcarriers can be conventionally or nuclear powered.

Warships must also be able to survive attack and protect its crewonboard. This protection ranges from the use of armour to systemsdesigned to isolate the crew from chemical, biological, and radiologi-cal attack. Much of the equipment is shock hardened or isolated fromblast shock. Some vessels also act as platforms for air vehicles, such asaircraft or helicopters.

Beyond their direct military mission capability, warships mustperform another set of functions: housing and feeding the hundredsof sailors (‘hotel’ functions). Warships also need to provide for thehealth of the crew and thus require medical facilities. All these capa-bilities must be sustained for up to several months, requiring a sig-____________1 For the purpose of discussion here, warship refers to a class of ship or submarine that isblue-water capable. That is, the ship can fulfil a role beyond coastal protection. Also, weinclude ships beyond the direct combatants, such as logistics ships.

Introduction 3

nificant amount of equipment and provision storage. These non-mission capabilities make warships unique compared with other mili-tary assets, such as tanks and aircraft.

To house all these functions and capabilities, warships must belarge weapon systems. For example, the crew size for a warship cannumber in the hundreds, and in some case thousands. These shipsweigh thousands of tonnes (displacement) and can reach lengths of afew hundred metres.

Given the size and complexity, manufacturing warships requiressubstantial design, engineering, management, testing, and productionresources. For even a modest vessel, the engineering and design work-forces can peak well in excess of 100 staff. Several engineering special-ties are involved in shipbuilding (e.g., electrical, mechanical, navalarchitecture). The design of modern naval ships is now done usingsophisticated three-dimensional computer-assisted design (CAD)tools. Thus, the design workforce must be highly skilled and edu-cated. Production also requires many proficient skills or trades, suchas electricians, welders, and painters. Testing these complex systemsalso requires commissioning and test specialists to verify functional-ity. For certain skills, it might take years to become proficient (e.g.,nuclear-qualified welders and commissioning engineers). The work-force for the production trades might peak in the thousands for atypical naval vessel.

The manufacture of warships also requires significant facilities.Shops and plate lines/steel fabrication facilities make componentparts and structure. Docks, slipways, piers, and cranes are used forassembly and integration activities. These facilities occupy large areasof land and must be water accessible (often the more valued realestate of any country). The facilities themselves are expensive to buildand maintain. Hence, shipbuilding is both a capital- and labour-intensive industry. As such, it cannot be developed or expandedwithout significant resources, planning effort, and a long lead time.

Another aspect to naval production is that it relies on a signifi-cant vendor base; these vendors supply products ranging from servicesto material and equipment. Painting services, modular unit (such asaccommodations) manufacturers, material suppliers, and sophisti-

4 The United Kingdom’s Naval Shipbuilding Industrial Base: The Next 15 Years

cated weapon systems providers (such as fire control and sonar sys-tems) are examples of the diversity of the vendor base. Thus, theshipbuilding industrial base encompasses a much broader array offirms beyond just the shipyards.

Nations that maintain a significant navy (particularly one withexpeditionary capabilities) have established domestic industries thatare specialised in warship production.2 This fact contrasts with thecommercial shipbuilding industry, in which a small number of coun-tries dominate the production in a particular market segment (such ascruise ships or bulk containers).3 There are many reasons given as towhy a domestic naval shipbuilding capability might be desirable.4

Although not advocating for or against these reasons, we will brieflydiscuss the issue to illustrate the broader issues involved in navalacquisition.

One reason a domestic industry might be necessary is that cer-tain technologies, such as nuclear propulsion, are sensitive and there-fore difficult to obtain from outside sources. A second reason couldbe political, because most shipbuilding industries employ large num-bers of workers. Thus, politicians have a vested interest in preservinga healthy domestic industry. But politicians are not alone in theirinterest in protecting large employers (such as shipyards). Shipyardsin the United Kingdom are long-established firms with extensive his-tories, which makes them even more politically difficult to close.Also, warships are paid with public funds. It is argued that these pub-lic funds should be spent to support or stimulate the domestic econ-omy. A further argument given is security. By maintaining a domesticsource of production a country is better able to control informationabout the technologies and capabilities of its warships. A final reasongiven in favour of having a domestic industry is that it can tailor thewarships better to meet a country’s specific needs or operating doc-trine. In buying vessels overseas, governments may find it more diffi-____________2 Todd and Lindberg (1996).3 Birkler et al. (forthcoming).4 Todd and Lindberg (1996).

Introduction 5

cult to obtain customised ships or may be restricted to only standarddesigns.

Recent trends in foreign purchases of warships (from both theUnited Kingdom and other nations) suggest that design and possiblyfirst-of-class are purchased abroad and follow-on ships are manufac-tured domestically.5 For the United Kingdom, shipbuilding is alsotied to national pride, since its history of the industry goes back cen-turies. The UK empire grew, in large part, because of a strong navyand merchant fleet. Whatever the reason for favouring domestic pro-duction, maintaining a strong navy seems to be inexorably tied to adomestic shipbuilding industry.6

MOD Ship Programmes7

Over the next 15 years, the MOD is planning an extensive ship-building programme. During this period, the MOD will be enhanc-ing the capabilities of the fleet as well as renewing it. The MOD’sshipbuilding programme can be divided into two main categories:those programmes that have already passed through the MOD’s finalapprovals process (Main Gate) and are somewhere in the demonstra-tion and manufacture stage, and those programmes that have yet topass Main Gate but which the MOD anticipates will be built. Below,we will describe the programmes in both categories.

Of course, the future procurement programmes continue toevolve in line with the strategic environment, financial imperatives,industrial developments, and new opportunities. Any statement of____________5 For example, the Super Vita class for the Hellenic Navy, based on a VT design, is producedin Greece. See Birkler et al. (forthcoming) for more detail.6 There are, of course, global firms that do successfully export warships (e.g., some Germanmanufacturers). BAE and VT export design and production warships to countries such asMalaysia, Brunei, Oman, Qatar, and Greece; however, it is a smaller portion of their overallwork.7 The information for this section is extensively drawn from the DPA’s Web site on theagency’s current projects (http://www.mod.uk/dpa/ipt/index.html), the Royal Navy’s Website (http://www.royal-navy.mod.uk), and Royal Navy (2003).

6 The United Kingdom’s Naval Shipbuilding Industrial Base: The Next 15 Years

the programmes themselves, the number of ships, and the timings arespeculative—particularly for the second category of programmes notyet past Main Gate. Thus, the reader must keep this caveat in mindwhen interpreting results.

Programmes Past Main Gate

As of the writing of this report, the following three programmes werein the design and production stage.

Astute-Class Attack Submarine. The Astute programme is a newnuclear attack submarine (SSN) intended to replace the existing Tra-falgar and Swiftsure classes. The tasks of the attack submarine arestated to be the following: support of the Vanguard class, antisubma-rine warfare, anti-surface warfare, surveillance and intelligence gath-ering, and land attack. Currently, three boats are on contract withBAE Systems, which is producing the boats at its facilities in Barrow.Additional submarines of the class may be procured—potentially upto six; however, the MOD has made no decision as to the numberbeyond the initial three vessels. The Astute class uses nuclear propul-sion and will displace approximately 7,800 metric tons (submerged).The crew complement is notionally 98 sailors. The length overall ofthe vessels is 97 metres with a beam of approximately 11 metres. Thevessels will be armed with Tomahawk cruise missiles and Spearfishtorpedoes.

Landing Platform Dock (Replacement)—LPD(R). The LPD(R) isa programme designated to replace the fleet’s amphibious capability.These replacement ships will provide landing capabilities for up toeight landing craft, which carry various combat vehicles and forces.The ships will displace approximately 18,500 metric tons (full load)and have a crew complement of 349 and an additional berthing capa-bility for up to 304 troops. The ships are also capable of having heli-copter operations from the flight deck; up to two medium-sized heli-copters can be accommodated. These ships will replace the fleet’s twoamphibious ships: HMS Fearless and HMS Intrepid. The first of theLPD(R) ships (HMS Albion) is already in service, and the second(HMS Bulwark) is expected to enter service in early 2005. The shipswere built at BAE’s facilities in Barrow. The length of the vessel is

Introduction 7

approximately 180 metres with a maximum beam of about 29metres.

Bay-Class Landing Ship Dock—LSD(A). These new vessels arepart of the Royal Fleet Auxiliary’s (RFA’s) rapid deployment force.These ships will replace the various landing ship logistic classes in theRFA fleet. The LSD(A)’s main role, as the designation implies, islogistic support by transport of troops, trucks, tanks, and cargo intobattle. The ships can also be used for humanitarian missions. Thedesign of the Bay class is a modification of the Dutch Rotterdam class.Swan Hunter and BAE Systems (Clyde Shipyards) are each produc-ing two vessels of the class. The ships have an approximate lengthoverall of 177 metres and a beam of 27 metres. The full displacementof the vessels is approximately 16,160 metric tons, and the crew sizeis approximately 60.

Type 45. The Type 45 is a multi-role destroyer whose principalmission is antiair defence (DDG). The first six ships of the class arecurrently on order, and there is a potential for up to six additionalships to be procured. BAE Systems Naval Ships (Clyde Shipyards) isthe prime contractor for the Type 45. VT Shipbuilding (Portsmouth)is a subcontractor on the programme. Each firm produces specificblocks for all the ships in the class, which are subsequently assembledat BAE’s Clyde Shipyards. The main weapon system on the ship, thePrincipal Anti-Air Missile System, is being jointly developed with theFrench and Italian navies. The ships could also be fitted with cruisemissiles and a 155-millimetre gun, but currently there is no require-ment for either system. The Type 45 ships are notionally replacingthe current Type 42 class. With approximate length overall of 152metres and a beam of 21 metres, the Type 45 displaces 7,350 metrictons. The crew complement is about 190.

Projects Pre–Main Gate8

Beyond the projects listed above, there are several programmes in theconceptual planning phase that have yet to pass through Main Gate____________8 Main Gate approval is the point at which DPA authorises a programme to proceed to thedemonstration and manufacturing stage.

8 The United Kingdom’s Naval Shipbuilding Industrial Base: The Next 15 Years

approval. As such, there is little that can be said definitively of eitherthe ship characteristics of or the contractors involved in these pro-grammes.

Future Aircraft Carrier (CVF). The CVF is the Royal Navy’s nextgeneration of aircraft carrier and is meant to replace the currentInvincible-class (CVS) carriers. The ships will be considerably largerthan previous UK aircraft carriers and potentially larger than any shipproduced for the Royal Navy in decades. The size is a result of thedesire to support an enhanced strike capability over the existing CVSclass. Two CVF class ships will be produced. The base design of theCVF is configured for short take-off, vertical landing (STOVL) air-craft operation but can be adapted to conventional flight operationsshould such a requirement materialise or the Royal Navy employ dif-ferent aircraft. These ships will carry a mix of F-35 aircraft (JointCombat Aircraft [JCA] STOVL variant) and helicopters.

The MOD has announced that it intends to deliver the CVFthrough an alliance approach comprising BAE Systems, Thales UK,and the MOD. The contracting arrangements have yet to be final-ised. BAE and Thales UK have formed the Aircraft Carrier Team totake the programme through the assessment phase leading up toMain Gate. Although the shipbuilding strategy continues to evolve, itis likely that multiple shipyards will be involved with CVF produc-tion, given its size and complexity. The planned in-service date forthe first CVF is 2012. No crew size has been stated for the ship.