supply chain logistics post recovery landscape€¦ · 1 supply chain logistics post recovery...

TRANSCRIPT

1

Supply Chain LogisticsPost Recovery Landscape

Rotary Club of Saint PaulOctober 12, 2010

Richard Murphy Jr.President & CEOwww.murphywarehouse.comandPast ChairCouncil of Supply Chain Management Professionals (CSCMP)Center For Transportation Studies (CTS), U of MNAmerican Society of Landscape Architects – MN Chapter

Presentation Flow5 Major Topics

Logistics Industry Perspective

Transportation• Trucking, Rail, Ocean, River, Fuel

Global Supply Chains: Impacts on U.S. Logistics

• Land Bridges, Inland ports, Import Warehouses, Plant Locations

Domestic Logistics• Retail / Consumer Demands, Geographic “Mega Regions,” Land

Prices Impacts, Freight Security / Theft, Network Design Changes

Green Logistics

• Green measures, Urban Heat Island, Stormwater, EnergyManagement & Production

2

Why Care About:Supply Chain Logistics…???

Why Care About:Supply Chain Logistics…???

10.1% of Economy!

3

Why Care About:Supply Chain Logistics…???

Perspective

U.S. Logistics costs represent:10.1% of GDP

$4,483 per person

Logistics Cost

$122B is the cost of warehousing in U.S. (CSCMP)

Equates to $407.00 per person in the USA

$680B - cost of trucking in U.S. (CSCMP)

Equates to $2,267.00 per person in the USA

$63B - cost of rail in U.S. (CSCMP)

Equates to $210.00 per person in the USA

Perspective

U.S. Logistics costs represent10.1% of GDP - $4,483 per person

4

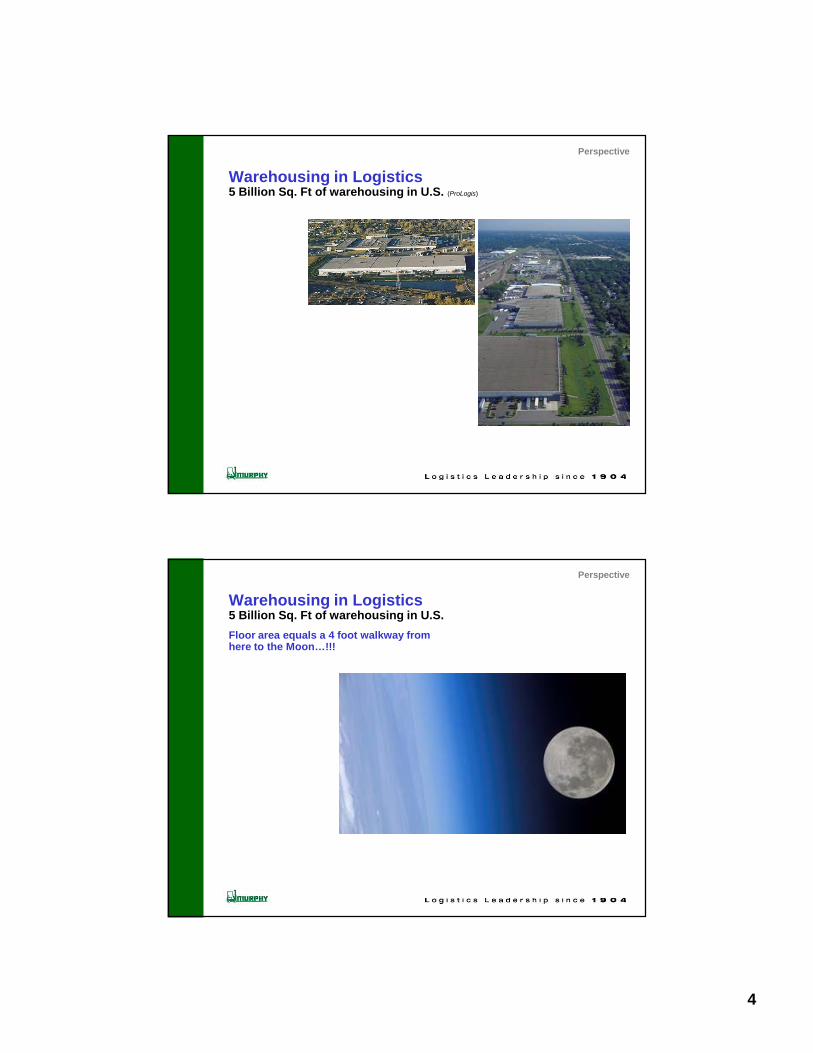

Warehousing in Logistics5 Billion Sq. Ft of warehousing in U.S. (ProLogis)

Perspective

Warehousing in Logistics5 Billion Sq. Ft of warehousing in U.S.

Floor area equals a 4 foot walkway fromhere to the Moon…!!!

Perspective

5

Who is MurphySupply Chain Logistics Services / 3PL

We are a Service Company Warehousing, distribution, transportation, value-added,

fulfillment, international, etc.

We handle products throughout their life-cycle From raw materials to in-process goods to finished

products to returns for numerous industry segments.

3PL – “3rd Party Logistics Services Provider”

Companies Served:Fortune 100 to Small EntrepreneursDomestic and Global

Industries Served:Retail / Catalogue / ConsumerMedical / Health CareGrocery / Food ProcessingBeveragePlasticsRecreational / CampingIndustrialForest Products (Paper/Packaging)International

Perspective

Who is MurphySupply Chain Logistics Services / 3PL

Murphy Family, 4thGeneration (1904)Square Feet Operated: 2,500,000Employees: 180

ISO 9001 Certified / ISO 14001 (pending)

OSHA - MNSHARP Certified ASI Food Certified / Organic Food Certified

LEED “Gold” Certified (2 facilities)

Energy Star Certified (Top 1%)

US Customs Bonded – CES, CFS, GO

FTZ (Foreign Trade Zone)

SKU’s Controlled: 29,000+

Order Activity / Month: 30,000+

Truck Loads Handled / Year: 120,450

Rail Cars Handled / Year: 10,000

Perspective

6

How do firms use Murphy13 Examples

1. Big Box / Mass Merchant / Retail

2. Global Sourcing – Domestic Distribution

3. Domestic Sourcing – Domestic Distribution

4. Vendor Consolidation Park

5. Seasonal Space Offsets

6. Domestic Manufacturing Support / JIT Plant

Support

7. Distribution / Transportation Services

• Regional Distribution

• U. S. Distribution

• Consolidation / Cross Docking

• Rail Transload / Truck-Rail-Ocean Integration

8. Contract Logistics

9. Medical Support Logistics

10. Value Added Services

• Parts Assembly

• Pick and Pack operations

• Packaging

11. Customer Returns Processing

12. Core Competency Strategies Solutions

13. Build to Suit Operations and Warehouses

Perspective

0%

20%

40%

60%

80%

100%

Jan

Feb

March

April

May

June

July

Aug

Sep

t

Oct

Nov

Dec

Murphy Rigging & Erecting, Inc.A Rigging / Millwright Contractor

Clients:Manufacturers to Printers

Medical to High Tech.

Artists to Classified Military.

From Very Precarious Handling….to Very

Heavy Lifts ….to Fragile Works of Art….to

Delicate and Expensive Medical Devices

7

• Truck

• Rail

• Ocean

• River Barge

• Fuel Prices

Transportation –

Trends & Implications–

Trucking IndustryCapacity Reductions

Parked equipment

Bankruptcy as fuel prices rose

200

400

600

800

1,000

1,200

1,400

Q1

00

Q1

01

Q1

02

Q1

03

Q1

04

Q1

05

Q1

06

Q1

07

Q1

08

Q1

09

Q1

10

Transportation

8

Trucking IndustryCapacity Reductions

Equipment Sell-offUsed Class 8 Tractor Exports

Trucking companies soldtractors to overseasmarkets when engines hitmajor overhaul point.

During recession practicegrew to get rid of capacity.

March 2010 U.S. tradedata

0

5,000

10,000

15,000

20,000

25,000

2004 2005 2006 2007 2008 2009 2010

Nigeria

Russia

Canada

Rest of the World

Transportation

69%

7%1% 0%

15% 10%

0%

70%

15%

9%7% 2%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Truck Rail Pipeline Water RailIntermodal

Air

2005

2017

U.S. Commercial Freight Activity By %Sources: Cureau of Transportation Statistics

& U.S. Freight Transportation Forecast to…2016

0%

10%

20%

30%

40%

50%

60%

70%

80%

Truck Rail Pipeline Water Multimodal Air

1993

1997

2002

2004

2016

Source: U.S. Freight Transportation Forecast to…2017

Freight Modal SharesIn domestic tonnage

Trucking capacity issuewill plaque economy foryears!

Transportation

9

Transportation ImplicationsTrucking Industry

Trucks Will Remain a Major Player Trucks expected to continue to handle 60-70%

of all freight. Most freight involving rail / ocean / river handled

by trucks at beginning & end of movements.

Severe shortage of capacity will grow

Equipment will not be replaced as fast aseconomic recovery

Prices will rise faster than economicrecovery

Carriers must make up cash from last few yearslosses to survive.

Driver shortage will reappear driving upcosts & reducing service levels

Transportation

Rail IndustryTrucking not alone!

Container & Rail Car business inching up

Transportation

10

Rail IndustryEquipment Parking

On every available siding upto 31.9% of capacity

Transportation

Rail IndustryRebirth Before Recession Hit

Key Realities: More energy efficient Lower emissions Lower cost Longer lead-times Were at max capacity Intermodal growing

Intermodal – Major Growth Area Grew to off-set diesel prices

and congested seaports

“Intermodal is a core growthopportunity for the railroads, butthey must adapt to expectationsof typical truckload customers”

Steve Weiby, VP, CH Robinson.

Transportation

11

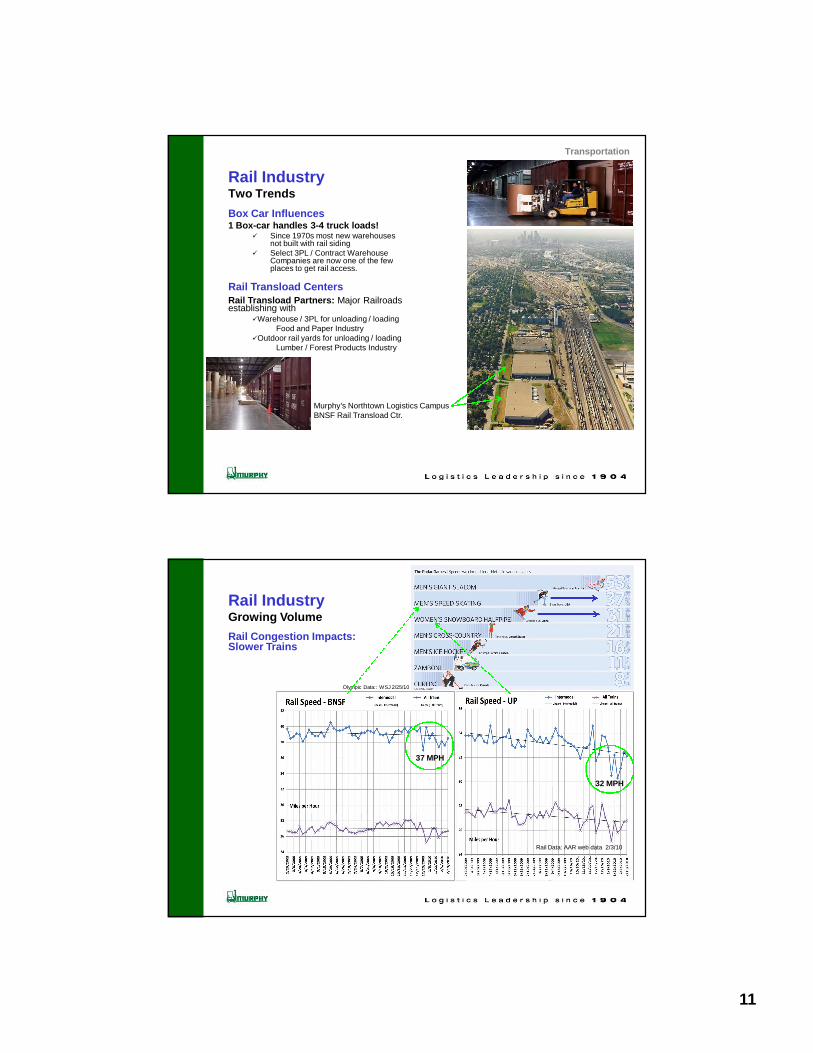

Rail IndustryTwo Trends

Box Car Influences1 Box-car handles 3-4 truck loads!

Since 1970s most new warehousesnot built with rail siding

Select 3PL / Contract WarehouseCompanies are now one of the fewplaces to get rail access.

Rail Transload CentersRail Transload Partners: Major Railroadsestablishing with

Warehouse / 3PL for unloading / loadingFood and Paper Industry

Outdoor rail yards for unloading / loadingLumber / Forest Products Industry

Murphy’s Northtown Logistics CampusBNSF Rail Transload Ctr.

Transportation

37 MPH

32 MPH

Olympic Data:: WSJ 2/25/10

Rail IndustryGrowing Volume

Rail Congestion Impacts:Slower Trains

Rail Data: AAR web data 2/3/10

12

Transportation ImplicationsRail Industry

Railroads making a comeback Will play a greater role in the future.

Rail carriers raising prices as if norecession

Will again feel capacity constraints Equipment & labor - when activity levels reach

pre-recession volumes, will push prices higher

Intermodal must meet trucking serviceexpectation levels to compete

Unless fuel prices reach astronomical levels andforce traffic to intermodal, despite the railsservice postures.

Environmental efficiency, esp. fromcarbon footprint, will push growth.

Box car use will grow

Transportation

Ocean IndustryOver Capacity

Two Issues Impacting:1. Drop in business had carriers parking equipment

throughout the world waiting for resurgence2. Carriers ordered many new and much larger

capacity ships over the past few years. Started arriving in 2009 Rates plummeted in response + impact of world

recession. Bigger ships will keep arriving no matter what

freight is available!

Transportation

13

Ocean IndustryNew Ships Huge

Photos show Emma MaerskWorlds largest container ship

Transportation

Container ShortageRaised Fees Significantly This Summer

Started With Container Plants ShuttingDown in China Late 2008

2010 Shipping rebound caught industry off guard

Supply & Demand allowed carriers to raise rates

Have been slow to reduce with additions to containerpools and reduced demand

Slower Speeds & Other RoutesTo Save Fuel & Canal Fees

Started in 2008 Fuel Price Bubble

Returned in 2010 to off-set lowfreight volumes

Added minimum one week toPacific transit

Results in 1 - 3 weeks additional inventoryrequired in system.

Carriers say they will continueslow sailing.

Transportation

14

River Barge IndustryInland Waterway

Keep in mind the inland waterwaysas a transportation option

Transportation

TransportationEconomic Comparison

Transportation

15

Transportation ImplicationsOcean Industry

Severe over capacity will linger for years! Prices will continue to stay low as a result.

New, bigger ships will add operationalefficiencies

Cost savings will not be realized till smaller, olderships retired.

Fuel price increases will push higher rates,over capacity will keep downward pressure

If global sourcing reduces significantly asfuel prices rise, carriers will be left withhuge ships with no freight to move

Smaller, older ships may be sorely missed.

Slow speeds will remain a tactic to savefuel and reduce carbon

Has added 1 - 3 weeks to system inventory.

River Barge IndustryMay see rebirth, esp. 300 miles of coast

Fuel efficiency very good Compared to land transpiration modes on tonnage

basis

Transportation

Source: Department of Energy, August 11, 2010

Fuel PricesWe all know what happened in 2008, but notice 2010!

($/Gallon)

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

$5.00

Ja

n0

5,

20

04

Ma

r0

5,

20

04

Ma

y0

5,

20

04

Ju

l05

,2

00

4

Se

p0

5,

20

04

No

v0

5,

20

04

Ja

n0

5,

20

05

Ma

r0

5,

20

05

Ma

y0

5,

20

05

Ju

l05

,2

00

5

Se

p0

5,

20

05

No

v0

5,

20

05

Ja

n0

5,

20

06

Ma

r0

5,

20

06

Ma

y0

5,

20

06

Ju

l05

,2

00

6

Se

p0

5,

20

06

No

v0

5,

20

06

Ja

n0

5,

20

07

Ma

r0

5,

20

07

Ma

y0

5,

20

07

Ju

l05

,2

00

7

Se

p0

5,

20

07

No

v0

5,

20

07

Ja

n0

5,

20

08

Ma

r0

5,

20

08

Ma

y0

5,

20

08

Ju

l05

,2

00

8

Se

p0

5,

20

08

No

v0

5,

20

08

Ja

n0

5,

20

09

Ma

r0

5,

20

09

Ma

y0

5,

20

09

Ju

l05

,2

00

9

Se

p0

5,

20

09

No

v0

5,

20

09

Ja

n0

5,

20

10

Ma

r0

5,

20

10

Ma

y0

5,

20

10

Ju

l05

,2

01

0

Pri

ce

per

Gallo

n

U.S. No 2 Diesel Retail Sales Price

$3.00

Transportation

16

$2.50

$2.75

$3.00

$3.25

2009

:Q4

2010

:Q1

Q2

Q3

Q4

2011

:Q1

Q2

Q3

Q4

Die

se

lP

ric

ep

er

Ga

llo

n

Forecasts

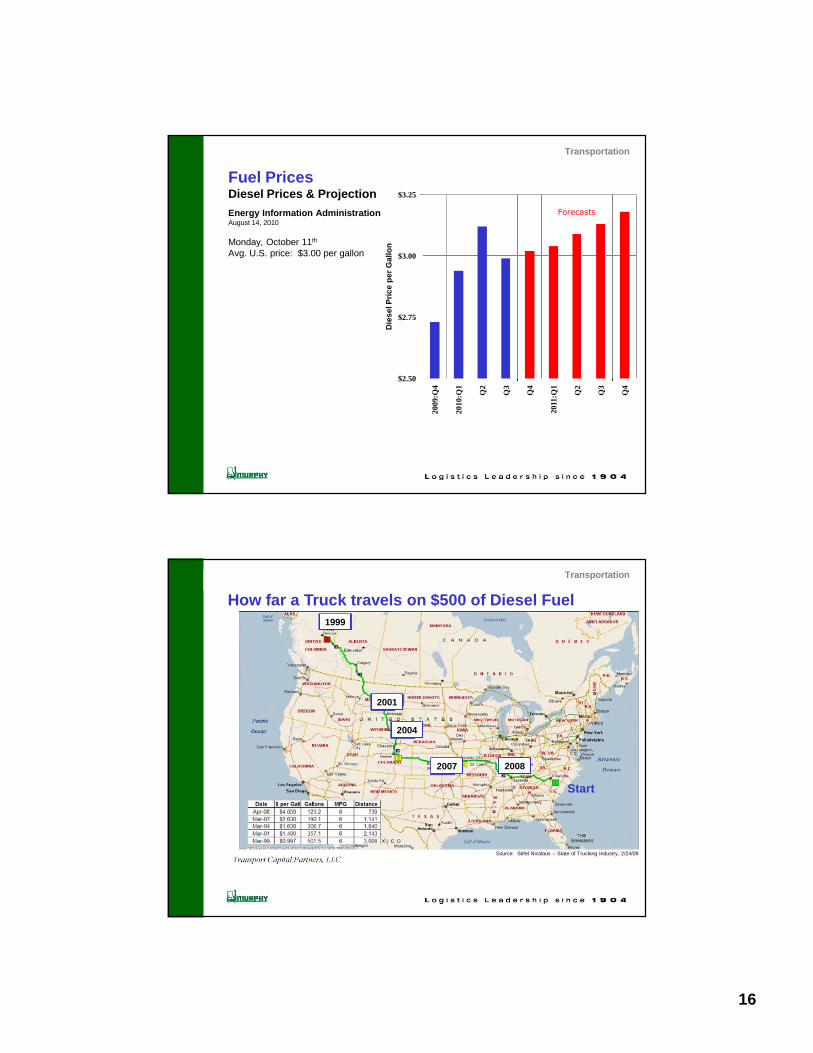

Fuel PricesDiesel Prices & Projection

Energy Information AdministrationAugust 14, 2010

Monday, October 11th

Avg. U.S. price: $3.00 per gallon

Transportation

Source: Stifel Nicolaus – State of Trucking Industry, 2/24/09

20082007

2004

2001

1999

Start

How far a Truck travels on $500 of Diesel Fuel

Transportation

17

Crude Oil SupplyU.S. Energy Information Administration View

Note how price projection jumped from 2008 to 2009 to 2010 report!

Source: US Energy Info Admin 2010 Energy Outlook

Transportation

NOTE: Est’ed price in year 2015 – highlighted in green.

2008 projection: $ 77.00 / barrel2009 “ 119.00 / barrel2010 “ 147.00 / barrel

Crude Oil SupplyStrategic Perspective

Oil supply subject to serious geographic “choke points”If closed prices will rise drastically!

Transportation

18

Transportation ImplicationsFuel Prices

Will go up!

Will impact Logistics• Transportation Rates• Sourcing Locations• Domestic Distribution Networks

Next two sections will review these trends.

Smart Supply Chain, Logistics and Transportationfolks already planning changes to offset increaseimpacts as long as possible

Transportation

Source: “Preliminary National Rail Plan” Fed Rail Admin., Oct 2009

Transportation ImplicationsMode Integration Will Increase

Tonnage on Highways,Railroads and InlandWaterways 2002

Powder River BasinMontana Coal Fields

Transportation

19

Transportation ImplicationsMode Integration

Mode Shifting to Occur More FrequentlyShippers moving down rungs to save moneyand reduce carbon footprint

Air Ground

Air Ocean

Intermodal Boxcar

Truckload Intermodal

LTL Truckload

Rail Barge

Transportation

• Landbridge Evolution & Changes

• Panama Canal Influence

• Northwest / Northeast Passages

• Inland Ports Landscape

• Import Warehouses

• Sourcing Locations Network Redesign

Near Sourcing

Made in the USA

Global Supply ChainsImpacts on U.S. LogisticsTrends & Implications

–

20

If Only The World’s ContinentsWere Closer TogetherWe Would Not Need Container Ships

–

Global Supply ChainImpacts on U.S. Logistics

If Only InternationalSourcing Was Easy

–

Global Supply ChainImpacts on U.S. Logistics

21

and Then There’s Pirates!2010 as of October 11th

– Source: http://www.icc-ccs.org/

Global Supply ChainImpacts on U.S. Logistics

Implications of Offshore SourcingChanging U.S. Distribution PatternsLess manufacturing required in U.S.

Distance adds time More safety stock required

More DC / warehouse space needed in U.S.1 month of inventory minimum added to system tocover travel times

Slower containership speeds adding additional timeand thus inventory to system; 1-3 weeks.

Domestic Product FlowsHistoric Domestic Oriented Networksvs. New Import Oriented NetworksProduct flow evolved over past 20 years to today’s importfocused flow

Large shippers like Wal-Mart have adjusted networks /warehouse locations as a result

–

Global Supply ChainImpacts on U.S. Logistics

22

Domestic Import TransportationLandbridges Evolved

To haul import containers by rail from west coastto markets in mid & eastern parts of U.S.

–

Global Supply ChainImpacts on U.S. Logistics

Domestic Import TransportationLandbridge Changing Economics

All Water (vs. Rail) to East Coast All water usually cheaper

Mini Landbridge Impact – Line Moving West Trend started only 3 years ago.

–

Global Supply ChainImpacts on U.S. Logistics

23

Panama CanalCanal Expansion Changing The Game

More Asian Freight to East & Gulf Ports Landbridge cost portion pushing many to

consider ocean voyages through thePanama Canal for better access to eastcoast and gulf ports.

In 2008 – 25% of U.S. imports flowedthrough the Panama Canal.

Starting in 2014 with expansion ofPanama Canal finished domesticintermodal will face steep competition offthe west coast ports. All-water route willbe cheaper, esp. as fuel prices rise.

–

Global Supply ChainImpacts on U.S. Logistics

Panama CanalToday’s New Ships Too WideFor Existing Lock Widths

Expansion Completion in 2014

6-12” clearance!

–

24

Global Logistics Route“Northwest Passage”

Feasibility for Container Ships. A cable-laying ship sailed through in 2008

from Hong Kong to a project in the NorthAtlantic.

Coast Guard data finds 62 othercommercial and re-supply ships and threeore carriers in the Passage in 2008.

Shorter route to East coast and St.Laurence Seaway ports from Asia.

Global Supply ChainImpacts on U.S. Logistics

Global Logistics Route“Northeast Passage”

Europe and Russia BenefitsAsia Benefits

34% Less Miles, Less Carbon, Less Fuel Use

Global Supply ChainImpacts on U.S. Logistics

25

Domestic Import LogisticsPort Congestion andHigh Fuel Price Impacts

Creation of Inland Ports Chicago Columbus DFW Texas Kansas City Memphis Atlanta

Global Supply ChainImpacts on U.S. Logistics

Domestic Import LogisticsPort Congestion andHigh Fuel Price Impacts

Creation of Import WarehousesUp to 100 Miles from Ocean PortsServices Often Provided by 3PLs

3 - 40’ ocean containers = 2 - 53’ trailers

Reasons for: Land shortages near seaports Transportation efficiencies gained by

transloading containers to 53’ trailers –whether intermodal or over-the-road

Activities include: Transloading Repack Value add labeling

30.2% of all U.S. import containers wheretransloaded into 53’ trailers so far in 2010.

Global Supply ChainImpacts on U.S. Logistics

26

Global Supply ChainImpacts on U.S. Logistics

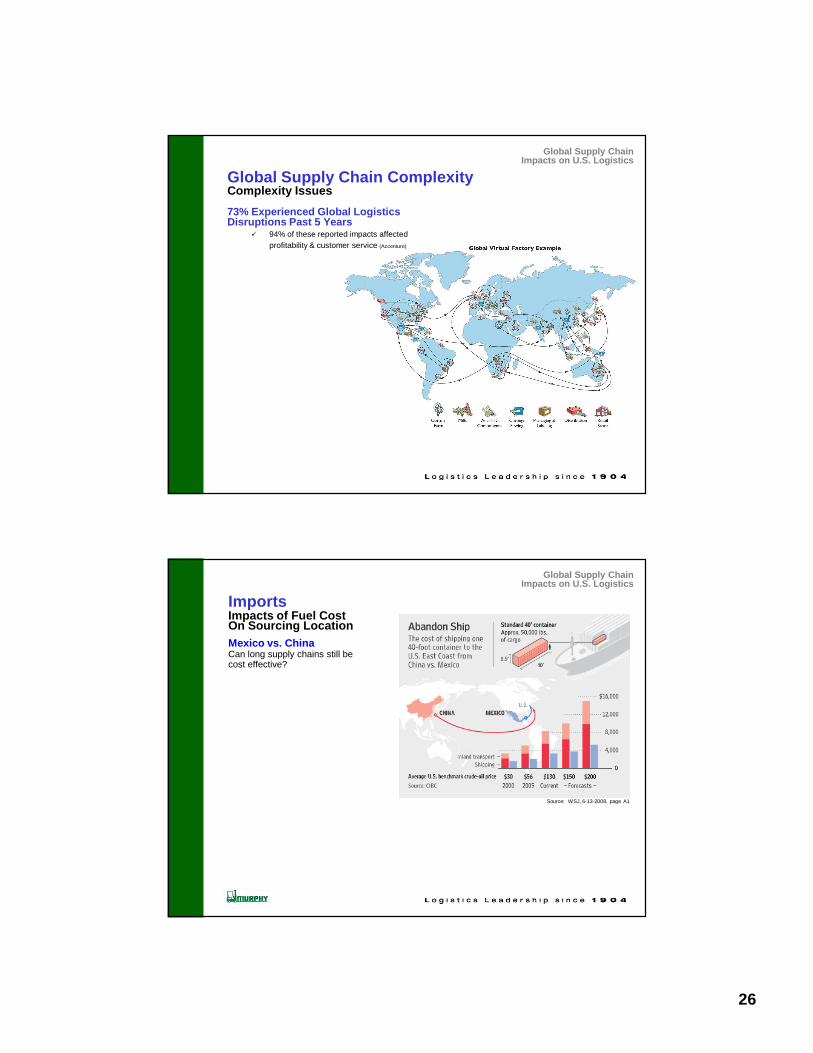

Global Supply Chain ComplexityComplexity Issues

73% Experienced Global LogisticsDisruptions Past 5 Years

94% of these reported impacts affected

profitability & customer service (Accenture)

ImportsImpacts of Fuel CostOn Sourcing Location

Mexico vs. ChinaCan long supply chains still becost effective?

Source: WSJ, 6-13-2008, page A1

Global Supply ChainImpacts on U.S. Logistics

27

Imports“Near Sourcing”

Factors influencing re-evaluationof offshore manufacturing:

Energy costs – esp. in logistics /transportation

Complexity of supply chains andvisibility issue

Long lead times

Excess inventory required

Larger carbon footprints – “Green”movement impact

Product Quality Controls

Available labor pools in select countries

Impact in China from growing internalconsumer market (vs. export market)

Global Supply ChainImpacts on U.S. Logistics

Changes In Offshore CostsLogic Changing

Total Landed Cost vs. Only Labor Cost Corporations are abandoning their myopic

focus on hourly wages for “Total Landed Cost”.

Total Landed Cost Model

Global Supply ChainImpacts on U.S. Logistics

28

Global Sourcing Network EvaluationBecoming More Important

When to move from Offshoring to Inshoring

Source: MIT 10-2008

Global Supply ChainImpacts on U.S. Logistics

Global Sourcing Network EvaluationCase Study 1 - impact of fuel prices and rising Asian labor cost

Source: MIT 10-2008

Global Supply ChainImpacts on U.S. Logistics

29

Global Sourcing Network EvaluationCase Study 2 - impact of fuel prices and rising Asian labor cost

Global Supply ChainImpacts on U.S. Logistics

69%

7%1% 0%

15% 10%

0%

70%

15%

9%7% 2%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Truck Rail Pipeline Water RailIntermodal

Air

2005

2017

Source: U.S. Freight Transportation Forecast to…2017

Global Supply ChainImpacts on U.S. Logistics

Freight TransportationTruck and Rail Capacity Limits willPlaque Post-Recession Economy

Trucks Handle 69% of Freight!In Domestic Tonnage

Rail & Intermodal will be key, but still onlyhandle 16-20% in foreseeable future

30

Global Supply ChainImpacts on U.S. Logistics

Global Supply ChainImpacts on U.S. LogisticsImplications

Ocean Freight Lanes More traffic through the Panama Canal – esp.

after major lock expansion completed in 2014. More cargo will arrive at gulf & east coast

ports Land bridge cost from west coast ports will

continue to rise relative to all water routeforcing more Asian containers to east and gulfcoast ports.

Northwest passage may open and allowcontainer ships to more economically reachupper east coast & St. Laurence Seaway ports.

Inland Ports & Import Warehouses Continue to grow These two trends creating large Logistics

Centers in key inland markets.

Plant Locations Total landed cost will be the driver - not just

labor cost per hour; especially as fuel prices rise. “Near sourcing” will grow - Mexico, Central

America & South America. “Made in USA” will see more movement.

• Retail / Consumer Demands

• Geographic “Mega Regions”

• Network Design Changes:“More is Less”

Fuel Price Impact

Carbon Footprint Impact

• Freight Security / Theft

• Land Prices & Urban Proximity

• The Sky’s The Limit

Domestic LogisticsTrends & Implications

–

31

Domestic Logistics

Retail / Consumer DemandsGrowing Impact of Big-Box Retailers

Less backroom stock space

Pushing inventory up-stream Reducing cash flow tie-up a factor

Demanding frequent replenishment & smaller orders

–

Order Profile ChangesOld Rules No Longer Apply

Christmas SalesNow in July…!!!

32

Domestic Logistics

Retail Options GrowIn the Internet Age…

No Longer Know: Where sales are going top come from When they will arrive How they will arrive

Makes Demand Planning Difficult

Domestic Logistics

Retail Options Grow“Growing” New Consumers

33

Domestic Logistics

Consumer DemandSKU Proliferation

“We want it Now!....and Our Way!”

Source: The Tioga Group

Domestic Logistics

North America “Mega-Regions”Eastern Market Still Biggest Impact To Models

34

Network DesignReceiving More Attention Today

Last 15 yrs trend - fewer & bigger warehouses: 3 - 5 Total JIT, ERP, TQM, Lean Impacts Lower fuel costs helped also

Today, attention given to increasing number of warehouses:6-10 Locations Network

Impact of higher local delivery cost (vs. long haul cost) is changing networks. Trend also towards smaller warehouses.

Source: New Age of Trade. Cushman & Wakefield, 2009

Green TrendsLogistics Industry

“DC” stands for Distribution Center / Warehouse

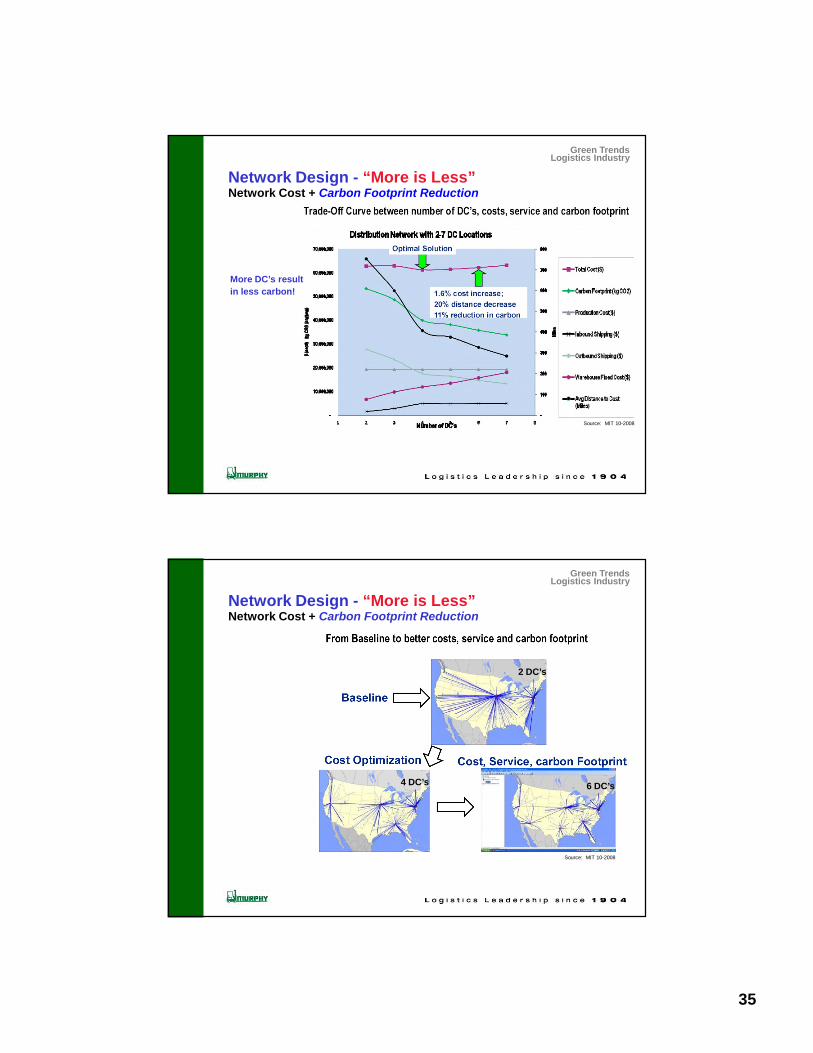

Network DesignNetwork Design - “More is Less”

Green TrendsLogistics Industry

35

Network Cost + Carbon Footprint Reduction

Source: MIT 10-2008

More DC’s result

in less carbon!

Network Design - “More is Less”

Green TrendsLogistics Industry

Network Cost + Carbon Footprint Reduction

2 DC’s

6 DC’s4 DC’s

Network Design - “More is Less”

Source: MIT 10-2008

Green TrendsLogistics Industry

36

Domestic Logistics

Logistics SecurityCargo Theft Incidents Past 12 Months

Warehouse Break-insTruck Heisting

FBI estimates $15-50B / year Warehouses & Carriers handling high value

products see increase in out-side initiated theft

Map / Diagram: July 2010 ReportFreightWatch Internationalhttp://www.freightwatchintl.com/?q=node/3

Domestic Logistics

Logistics SecurityWhy Logistics Theft Growing

Product Value Increasing + Counterfeiting Esp. electronics, meat / fish, cigarettes,

metals.

Easily sold domestically & globally Orders go out for products from

organized gangs/crime. Cuban criminals been hard at work

steeling Cigarettes.

Low risk of being caught Since 911 FBI’s Cargo Theft Teams

assigned to domestic security.

Inadequate criminal justice system Drug arrest yields 20 years in prison $2M Cigarette heist yields 10 year

max, usually less! Result, drug criminals have shifted to

Logistics theft. “Crime doesn’t pay” no longer applies!

37

Domestic Logistics

Urban Land Prices500% Increase in 10 Years

Pushing Logistics CampusesFurther Out

To suburban edge sites: 2nd tier-plusoutward suburban locations & ruraledge

Adding increased transportation time,cost & congestion

500% land price increases are sitesnear freeway rung system closer tourban center

Big campuses can’t be too closeto cities, but they also can’tbe too far out

Domestic Logistics

Urban Land PricesWhere to Find Warehouses / DCs Today

Logistics Parks & Corridors – Freight Villages Regional Economic Development Drivers

38

Domestic Logistics

The Sky’s the LimitExisting Warehouse Upgrade

Raising the Roof Conversion of low height warehouses to tall structures Cheaper than new construction Photos: Albertson 600,000 sq. ft. DC Chicago – 18’ up to 38’

A. Epstein and Sons International, Inc. Chicago

Domestic LogisticsImplications

Retail / Consumer Demands…. Retailers & consumers demands are playing havoc

with inventory management, cycles, & productionplanning.

Geographic “Mega Regions”…. Regionally concentrating freight delivery areas.

Local delivery costs rising – congestion, fuel, labor

Land Prices & Urban Closeness Continued pressure pushing DC’s / warehouses

further out, thus adding to local delivery costs andtime.

Economics of “raising the roof” to modernize olderfacilities gaining momentum – will pick up steam onceindustrial vacancy rates lower which may take 3 years.

Domestic Logistics

39

Domestic LogisticsImplications

Freight Security / Theft Growing during the recession.

Increasing values of cargo and lenient justicesystem insure theft will continue escalating

Logistics industry fighting back with technology andbetter law enforcement coordination.

Not just unique to USA.

Network Design Changes - “More is Less” Fuel price increases forcing changes to Supply

Chain Networks – domestically and globally.

Growing interest in more DC and Crossdocklocations.

Likely to see 6-10 DC/Warehouse networks (vs.3-5 which was common since the late 1980’s).

Carbon footprint influence will grow as a factorin network design – in some cases, this leads tomore locations.

Domestic Logistics

Green Logistics–

–

–

–

• Green Performance Measures –Impact on Speed of Supply Chain

• Urban Heat Island

• Facility Design & StormwaterManagement

• Energy Creation Measures

40

Major corporations Green InitiativesPerformance Measures - two new examples

100% Order Accuracy

Traditional Focus - Customer satisfaction.

Green Focus - to avoid redelivery and thusreduce carbon emissions.

Zero Customer Order Complaints

Traditional Focus - do whatever it takes to makecustomer happy!...order minimums are noproblem…delivery ASAP!

Green Focus - increasing order minimums toreduce delivery frequency, and longer orderlead times to facilitate transportationconsolidation.

Green Logistics

Facility DesignStormwater Regulation Impacts

Few outside profession realize growing impact…!!!

EPA mandated cities to control their stormwater – quantity & quality Regulations required cities to comply with no additional Federal Funds,

thus local fees.

Stormwater fees growing 1400+ cities to date nationwide.

Minneapolis - $3,400 per acre (i.e. $0.12 per sq. ft. of warehouse).Most DC/warehouses use 20+ acres; cost is $68,000+/yr.

Green Logistics

41

Facility DesignNative Prairie Planting vs. Lawn

Maintenance Cost DifferenceIf all

Cut Lawn

Prairie Lawn Lawn

Areas Areas AreasAnnual Costs 6 acres 4.19 acres 10.19 acres

Maintenance 4,240$ -$ -$

Mowing - 12,015.00 29,220.25

Watering - 8,630.00 20,988.00

Fertilization - 1,005.00 2,444.14

Total Cost: 4,240$ 21,650$ 52,652$

Cost / Acre.: 707$ 5,167$ 5,167$

Existing Set-up

Manicured Lawn costs 7.3x more to maintainthan native prairie plants!

“Since 1994 we have saved over $520,000while being green…!!!”

Green Logistics

Energy Creation - Solar PowerRoofs - Large available flat areas “just sit there.”Solar panels not great load factors

Commercial solutions include: “Solar Energy Service Provider” - 100% responsibility to design, build,

own and operate the asset - including all upfront purchase andinstallation costs.

to solutions where building owner owns the solar assets and providerdesign-builds the system.

Staples Store, CA

2 SolarProviders:

Green Logistics

42

Energy Creation - Solar PowerMinnesota Manufactured Panels

Jim Losleben, 952-303-7600, [email protected]

Run at lower voltage – increases efficiency and solves firedepartment issues with live systems.

Solved “shadow problem” – shading a portion of panel nowdoesn’t shut system down!

Meets Minnesota’s new law to receive state grants for usingMN manufactured panels.

Murphy installed 3 systems Fall 2010 – 140KW total power

• 3 buildings; each w 40 KW array

• Array size: 5,000 sq. ft., less than 2% of building.

• Produces 50+% of energy use…!!!

Green Logistics

Energy Creation - WindWind power units – individual fans, horizontal row of blades, & stand alone tower units.

Horizontal wind power units – research in Chicago on units mounted in horizontal rowof blades at roof edge to capture air flow rising up and over building, and to better handleturbulent urban air patterns.

Green Logistics

43

Urban Heat Island ImpactsPotential solution - green roofs

Minneapolis LibraryGreen roof temperature statistics

Situation: 90-degree day

Green Roof: 92° F

White Roof: 125° F

Dark Ballast: 145° F

Black Roof: 170° F

Green LogisticsImplications

Green Logistics is in “Green” seen as a reflection of good management

by Wall Street and public.

Could lead to less service & options for shippers

Likely see a “slow-down of logistics velocity” As transportation modes slow down to maximize fuel

efficiency & consolidation

LEED & other environment certifications willgrow in importance

Facility design changes including green roofs, stormwater management, &

other planting concepts.

Wind & Solar energy production on logisticsfacilities roofs

44

Supply Chain LogisticsPost Recovery Landscape

Rotary Club of Saint PaulOctober 12, 2010

Richard Murphy Jr.President & CEOwww.murphywarehouse.comandPast ChairCouncil of Supply Chain Management Professionals (CSCMP)Center For Transportation Studies (CTS), U of MNAmerican Society of Landscape Architects – MN Chapter