sun pharmaceuticals (sunpha) | 568static-news.moneycontrol.com/...sunpharmaceuticals... ·...

TRANSCRIPT

May 29, 2017

ICICI Securities Ltd | Retail Equity Research

Result Update

Numbers tumble beyond comprehension…

Revenues declined 7% YoY to | 7137 crore (I-direct estimate: | 8065

crore). US declined fell 37% YoY to | 2477 crore (I-direct estimate:

| 3690 crore) mainly due to challenging generic pricing environment.

Domestic sales grew 10% YoY to | 1916 crore (I-direct estimate:

| 1987 crore)

EBITDA margins declined 800 bps YoY to 21.7% vs. I-direct estimate

of 29.5%. EBITDA declined 32% YoY to | 1545 crore (I-direct

estimate: | 2381 crore). Taro Pharma’s EBITDA margins declined to

53.7% from 69.8% in Q4FY16

Net profit declined 17% YoY to | 1183 crore (I-direct estimate: | 1515

crore) mainly due to lower than expected operational performance

US business key lever for growth but new challenges emerge

The US business, which constitutes ~45% of turnover, has grown at 10%

CAGR in FY12-17, on the back of successful acquisitions like Caraco, Taro,

Dusa, URL and timely product launches (gGleevec, gBenicar AG under

exclusivity). US product basket remains robust - 584 ANDAs filed, 427

approvals received. Some niche launches include Lipodox, Doxil,

Doxycycline, Nystatin, etc, besides complex/limited competition products

and plain vanilla generics. US growth is also being backed by extensive

infrastructure - out of the ~50 global manufacturing facilities more than

20 have been approved by USFDA. However, warning letters to Karkhadi,

Halol and acute pricing pressure in the US base business are new

challenges even as it attempts to achieve Ranbaxy synergy.

Ranbaxy’s stronghold in fast growing emerging markets (50% of

Ranbaxy's sales) will complement Sun’s presence in this space. Regarding

US, it is determined to address Ranbaxy’s cGMP issues as four out of five

US centric facilities remain under USFDA embargo. Sun will gain

leadership position in the niche generic derma space and also get entry to

branded and OTC segments. In the domestic space, the acquisition is

likely to provide more therapeutic diversification to Sun’s portfolio and is

likely to improve its market share in key segments in the domestic space.

Its domestic market share has substantially improved to 8.9% from 5.5%

with leadership in as many as 11 therapies. The management expects

~US$300 million synergy benefits by FY18. We expect US sales to

decline at a CAGR of 8% to | 11580 crore in FY17-19E due to high base

and price erosion in base business. Similarly, the Indian formulations

business is likely to grow at 10% CAGR to | 9417 crore in FY17-19E.

Delay in Halol resolution, US pricing pressure major dampeners

Dismal Q4 numbers (both from Taro, Sun) have summarised the recent

pricing woos in the US generics space but more worrisome for Sun is the

delay in Halol resolution. By the management’s own assertion the

resolution is unlikely before FY18 end against earlier expectation of

Q2FY18. Unlike other generic players, the approval momentum is also

dismal in Sun’s case, mainly due to pending Halol resolution. On the US

generic pricing front, the management expects challenges to remain in

FY18 as well. Hence, they have guided for single digit revenue decline for

the year. The shift towards specialty products such as Tildrakizumab

(dermatology), BromSite, Seciera (both ophthalmic) and Odomzo

(oncology) are long term game plans, the benefits of which are back-

loaded. For now, the company is bracing for ‘’new normal’’, a scenario

where product specific price erosion continuum and prolonged cGMP

resolution delays are here to stay. We downgrade to HOLD with a new

target price of | 550 based on 20x FY19E EPS of | 25.7 and | 36 NPV for

Tildrakizumab.

Rating matrix

Rating : Hold

Target : | 549

Target Period : 12-15 months

Potential Upside : -3%

What’s Changed?

Target Changed from | 850 to | 549

EPS FY17E Changed from | 30.1 to | 29

EPS FY18E Changed from | 31.9 to | 20.9

EPS FY19E Changed from | 38.7 to | 25.7

Rating Unchanged

Quarterly Performance

Q4FY17 Q4FY16 YoY (%) Q3FY17 QoQ (%)

Revenue 7,137.0 7,654.3 -6.8 7,912.7 -9.8

EBITDA 1,547.5 2,271.9 -31.9 2,453.1 -36.9

EBITDA (%) 21.7 29.7 -800 bps 31.0 -932 bps

Adj. Net Profit 1,182.7 1,416.1 -16.5 1,471.8 -19.6

Key Financials

(| Crore) FY16 FY17E FY18E FY19E

Net Sales 28563.0 31557.7 30143.5 32901.2

EBITDA 8724.3 10089.3 7912.1 9291.9

Adj. Profit 5652.6 6964.4 5014.0 6162.7

Adj. EPS (|) 23.4 29.0 20.9 25.7

Valuation summary

FY16 FY16 FY18E FY19E

PE (x) 27.6 27.6 27.2 22.1

EV to EBITDA (x) 15.0 15.0 15.9 13.1

Price to book (x) 4.4 4.4 3.3 3.0

RoNW (%) 18.0 18.0 12.3 13.4

RoCE (%) 18.6 18.6 14.0 15.2

Stock data

Particular

Market Capitalisation

Debt (FY16)

Cash & Cash Equivalents (FY16)

EV (| Cr)

52 week H/L (|) 855/564

Equity capital

Face value | 1

| 124616 crore

| 240.7 crore

Amount

| 136192 crore

| 8091 crore

| 19667 crore

Price performance (%)

1M 3M 6M 1Y

Sun Pharma -11.7 -15.8 -20.5 -27.2

Dr Reddy's -7.5 -16.4 -23.8 -21.9

Lupin -18.9 -23.3 -26.3 -24.3

Research Analyst

Siddhant Khandekar

Mitesh Shah

Harshal Mehta

Sun Pharmaceuticals (SUNPHA) | 568

ICICI Securities Ltd | Retail Equity Research Page 2

Variance analysis

Q4FY17 Q4FY17E Q4FY16 Q3FY17 YoY (%) QoQ (%) Comments

Revenue 7,137.0 8,065.2 7,654.3 7,912.7 -6.8 -9.8 YoY decline of 35% in the US was partly offset by consolidation of acquisitions in

Japan and Russia

Raw Material Expenses 2,195.2 2,097.0 1,408.6 2,248.7 55.8 -2.4 YoY decline of 1140 bps in gross margins to 69.2% mainly due to adverse

product mix and one-off US$ 45 million of inventory write-off

Employee Expenses 1,248.8 1,209.8 1,187.0 1,215.1 5.2 2.8

Other Expenditure 2,145.5 2,377.3 2,786.8 1,995.8 -23.0 7.5

Total Expenditure 5,589.5 5,684.0 5,382.4 5,459.5 3.8 2.4

EBITDA 1,547.5 2,381.2 2,271.9 2,453.1 -31.9 -36.9

EBITDA (%) 21.7 29.5 29.7 31.0 -800 bps -932 bps YoY decline mainly due to a sharp decline in gross margins. Miss vis-à-vis I-

direct estimates was mainly due to lower-than-expected gross margins

Interest 45.0 166.5 103.0 166.5 -56.3 -73.0 Volatility mainly due to forex element

Depreciation 338.2 302.5 288.0 306.8 17.4 10.2

Other income 224.5 124.5 206.0 122.2 9.0 83.8

EO 0.0 0.0 0.0 0.0 NA NA

PBT 1,388.8 2,036.7 2,086.9 2,102.0 -33.5 -33.9

Tax 44.3 305.5 417.6 372.9 -89.4 -88.1

MI 161.9 216.3 246.7 250.0 -34.4 -35.3

Adj. Net Profit 1,182.7 1,514.9 1,416.1 1,471.8 -16.5 -19.6 YoY decline and miss vis-a-vis I-direct estimates mainly due to lower operational

performance, which was partly offset by lower taxation and interest expenses

Key Metrics

India formulations 1,916.4 1,987.2 1,743.5 1,969.4 9.9 -2.7

US formulations 2,554.5 3,689.9 3,910.3 3,419.3 -34.7 -25.3 YoY sharp decline mainly due to higher-than-expected price erosion and

postponement of few products to the next quarters

Emerging Markets 1,212.7 1,003.8 836.5 1,159.9 45.0 4.6 Included consolidation of JSC Biosintez acquisition in Russia

RoW 732.3 776.5 533.2 760.3 37.3 -3.7 Included consolidation of acquisition in Japan

APIs 409.3 372.9 392.5 365.7 4.3 11.9

Source: Company, ICICIdirect.com Research

Change in estimates

(| Crore) Old New % Change Old New % Change

Total Operating Income 31,689.1 30,143.5 -4.9 37,013.0 32,901.2 -11.1 Downward revision mainly due to higher-than-expected price erosion and

delay in product approvals in the US

EBITDA 10,621.3 7,912.1 -25.5 12,045.6 9,291.9 -22.9

EBITDA Margin (%) 33.5 26.2 -725 bps 32.5 28.2 -430 bps Change mainly due to lower US sales estimates on the back of higher

than expected price erosion

Adjusted PAT 7,241.0 5,014.0 -30.8 8,476.7 6,162.7 -27.3

EPS (Adjusted) 30.1 20.9 -30.6 35.3 25.7 -27.3 Change in sync with EBITDA

FY18E FY19E

Source: Company, ICICIdirect.com Research

Assumptions

| crore FY16 FY17E FY18E FY19E FY18E FY19E

Indian Formulations 7,299.2 7,749.1 8,408.5 9,417.5 8,758.2 9,809.2

US Formulations 13,516.9 13,758.8 10,679.7 11,580.3 13,490.5 15,618.8 Downward revision mainly due to higher-than-expected price erosion in base

business and delay in product approvals

RoW markets 5,746.1 7,128.0 8,545.8 9,400.4 8,199.6 9,019.6

APIs 1,475.2 1,634.5 1,667.2 1,700.5 1,630.0 1,662.6

Current Earlier

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 3

Company Analysis

Established in 1983, Sun Pharma is the largest Indian pharmaceutical

company both in terms of market capitalisation and turnover (FY16).

The company manufactures and markets a large basket of pharmaceutical

formulations in India, the US and several other markets across the world.

However, US and Indian formulations are by far the core strengths and

growth drivers for the company. The company has ~50 manufacturing

sites across the world.

The US business has been built mostly on acquisitions and generic focus.

It owns the largest product basket among Indian players with as many as

584 product (ANDA) filings.

In Indian formulations, the company is a leader in niche therapy areas of

psychiatry, gastroenterology, neurology, cardiology, nephrology,

orthopaedics and ophthalmology.

The company completed the $3.2 billion acquisition of Ranbaxy

Laboratories after almost a year of navigating the regulatory gauntlet to

create the world’s fifth-largest generic pharmaceutical company by

revenue.

The company has planned a capex of US$250 million for Tildrakizumab,

the IL-23 monoclonal anti-body in-licensed from MSD (US) over four or

five years to be utilised for its psoriasis trials. The company has guided

for filing of Investigational IL-23p19 inhibitor, Tildrakizumab, in FY18 and

potential approval in FY19

Sun acquired Odomzo (oncology) from Novartis in December, 2016, for

$175 million and additional milestones payments. USFDA approved this

in July, 2015 for treatment of locally advanced basal cell cancer and is the

first branded oncology product for Sun Pharma in the US. Total 70% who

prescribe are dermatologists and rest are oncologists for this drug.

Seciera (for dry eyes disease), which was acquired from Ocular

Technologies, has shown promising phase III results. The company will

enter into dialogue with FDA regarding further course of action for the

product.

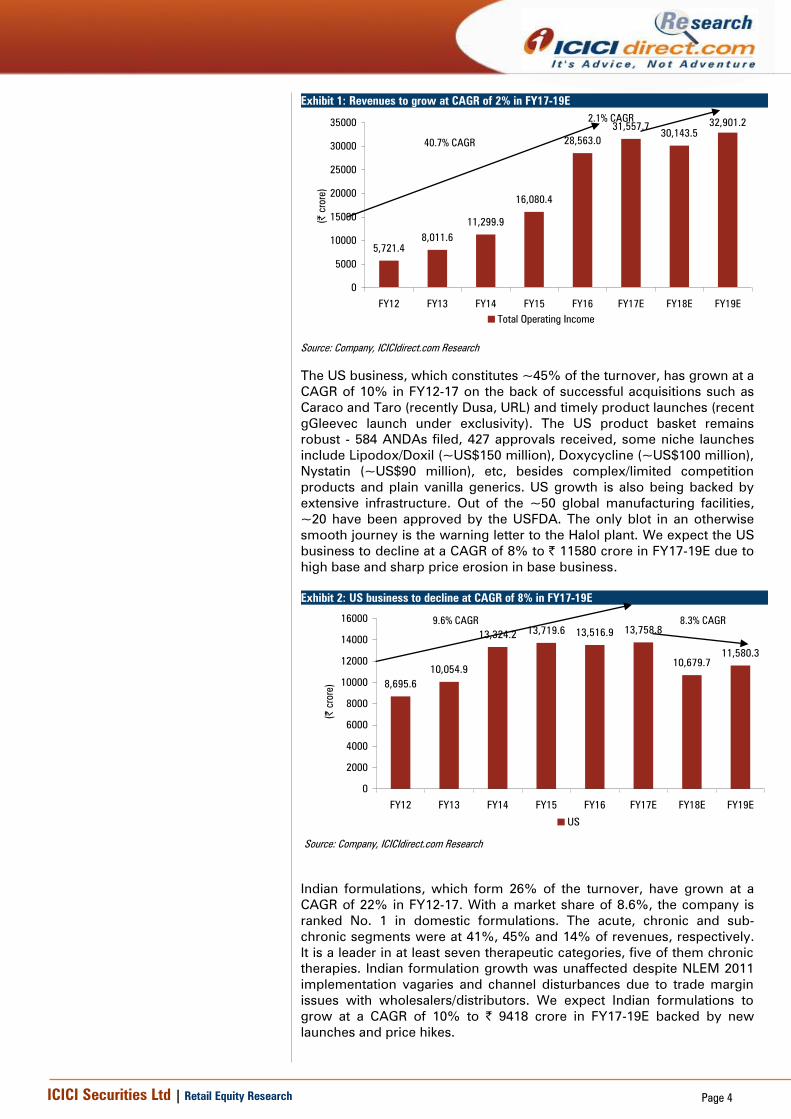

A snapshot of the galloping performance in the last five years - sales grew

at ~40% CAGR to | 31558 crore, EBIDTA grew at CAGR of ~39% to

| 10089 crore. Adjusted PAT grew at a CAGR of ~31% to | 6964 crore.

Going ahead, we expect revenues to grow at a CAGR of 2% in FY17-19E

to | 32901 crore after considering Ranbaxy acquisition.

ICICI Securities Ltd | Retail Equity Research Page 4

Exhibit 1: Revenues to grow at CAGR of 2% in FY17-19E

5,721.4

8,011.6

11,299.9

16,080.4

28,563.0

31,557.730,143.5

32,901.2

0

5000

10000

15000

20000

25000

30000

35000

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

(|

crore)

Total Operating Income

Source: Company, ICICIdirect.com Research

The US business, which constitutes ~45% of the turnover, has grown at a

CAGR of 10% in FY12-17 on the back of successful acquisitions such as

Caraco and Taro (recently Dusa, URL) and timely product launches (recent

gGleevec launch under exclusivity). The US product basket remains

robust - 584 ANDAs filed, 427 approvals received, some niche launches

include Lipodox/Doxil (~US$150 million), Doxycycline (~US$100 million),

Nystatin (~US$90 million), etc, besides complex/limited competition

products and plain vanilla generics. US growth is also being backed by

extensive infrastructure. Out of the ~50 global manufacturing facilities,

~20 have been approved by the USFDA. The only blot in an otherwise

smooth journey is the warning letter to the Halol plant. We expect the US

business to decline at a CAGR of 8% to | 11580 crore in FY17-19E due to

high base and sharp price erosion in base business.

Exhibit 2: US business to decline at CAGR of 8% in FY17-19E

8,695.6

10,054.9

13,324.213,719.6 13,516.9 13,758.8

10,679.7

11,580.3

0

2000

4000

6000

8000

10000

12000

14000

16000

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

(|

crore)

US

Source: Company, ICICIdirect.com Research

Source: Company, ICICIdirect.com Research

Indian formulations, which form 26% of the turnover, have grown at a

CAGR of 22% in FY12-17. With a market share of 8.6%, the company is

ranked No. 1 in domestic formulations. The acute, chronic and sub-

chronic segments were at 41%, 45% and 14% of revenues, respectively.

It is a leader in at least seven therapeutic categories, five of them chronic

therapies. Indian formulation growth was unaffected despite NLEM 2011

implementation vagaries and channel disturbances due to trade margin

issues with wholesalers/distributors. We expect Indian formulations to

grow at a CAGR of 10% to | 9418 crore in FY17-19E backed by new

launches and price hikes.

40.7% CAGR

2.1% CAGR

9.6% CAGR 8.3% CAGR

ICICI Securities Ltd | Retail Equity Research Page 5

Exhibit 3: India sales to grow at CAGR of 10% in FY17-19E

2,915.4 2,965.7

3,691.8

6,716.6

7,299.2

7,749.1

8,408.5

9,417.5

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E(|

crore)

Domestic

Source: Company, ICICIdirect.com Research

Exhibit 4: Sales from RoW markets to grow at CAGR of 15% in FY17-19E

1,112.41,527.1

1,908.4

6,064.65,746.1

7,128.0

8,545.8

9,400.4

0

2000

4000

6000

8000

10000

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

(|

crore)

ROW

Source: Company, ICICIdirect.com Research

24.2% CAGR

10.5% CAGR

45.0% CAGR

14.8% CAGR

ICICI Securities Ltd | Retail Equity Research Page 6

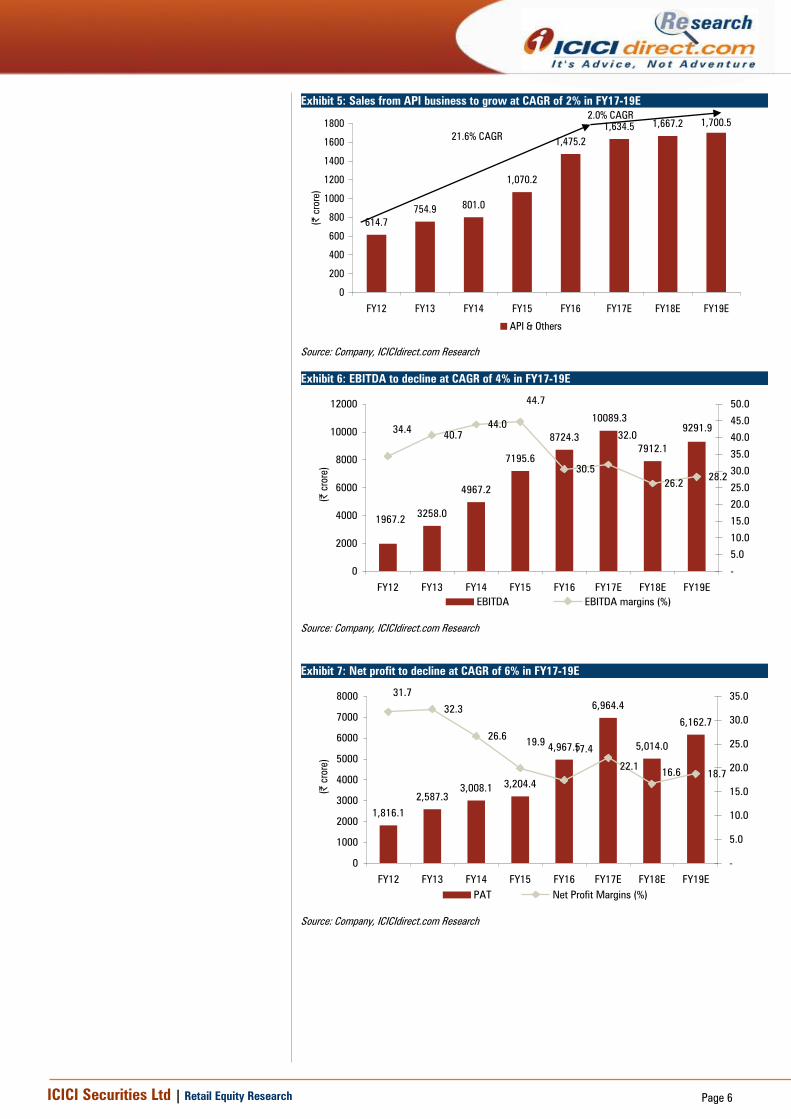

Exhibit 5: Sales from API business to grow at CAGR of 2% in FY17-19E

614.7

754.9801.0

1,070.2

1,475.2

1,634.51,667.2 1,700.5

0

200

400

600

800

1000

1200

1400

1600

1800

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E(|

crore)

API & Others

Source: Company, ICICIdirect.com Research

Exhibit 6: EBITDA to decline at CAGR of 4% in FY17-19E

1967.23258.0

4967.2

7195.6

8724.3

10089.3

7912.1

9291.9

40.7

44.0

30.5

26.228.2

34.4

44.7

32.0

0

2000

4000

6000

8000

10000

12000

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

(|

crore)

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

EBITDA EBITDA margins (%)

Source: Company, ICICIdirect.com Research

Exhibit 7: Net profit to decline at CAGR of 6% in FY17-19E

1,816.1

2,587.3

3,008.13,204.4

4,967.5

6,964.4

5,014.0

6,162.7

32.3

26.6

18.7

31.7

19.9

17.4

22.116.6

0

1000

2000

3000

4000

5000

6000

7000

8000

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

(|

crore)

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

PAT Net Profit Margins (%)

Source: Company, ICICIdirect.com Research

21.6% CAGR

2.0% CAGR

ICICI Securities Ltd | Retail Equity Research Page 7

Exhibit 8: Trends in return ratios

27.8

34.3 34.3

18.8 18.6

21.3 21.321.9

19.8

14.0

19.217.0

18.6 18.0

19.0

12.3

0

5

10

15

20

25

30

35

40

FY12 FY13 FY14 FY15 FY16 FY17E FY18E FY19E

(|

crore)

RoCE(%) RoNW (%)

Source: Company, ICICIdirect.com Research

SWOT Analysis

Strengths - Above average profitability margins, healthy return ratios

despite higher cash component, one of the first companies to identify

potential of innovative R&D and generic R&D, robust infrastructure to

scale up US business, India business built around chronic focus, one of

the few companies defying the slowdown in Indian formulations.

Weakness - Pending Ranbaxy compliance issues.

Opportunities - The US generics space, the biosimilars space where Sun

is yet to make meaningful foray.

Threats - Increased USFDA scrutiny across the globe regarding cGMP

issues, pricing pressure due to client consolidation in the US, pricing

probe by the Department of Justice (DoJ) in the US, proposed tightening

by the new regime by adapting to the bidding process and imposition of

border adjustment tax on imported drugs in the US. Halol facility has

received warning letter from the USFDA which is yet to be resolved.

ICICI Securities Ltd | Retail Equity Research Page 8

Exhibit 9: Trends in quarterly financials

(| Crore) Q4FY15 Q1FY16 Q2FY16 Q3FY16 Q4FY16 Q1FY17 Q2FY17 Q3FY17 Q4FY17 YoY (%) QoQ (%)

Total Operating Income 6157.0 6761.5 6873.3 7122.3 7654.3 8243.0 8265.1 7912.7 7137.0 -6.8 -9.8

Raw Material Expenses 1597.4 1691.2 1497.8 1732.8 1408.6 1847.0 1839.9 2248.7 2195.2 55.8 -2.4

Gross Profit Margin (%) 74.1 75.0 78.2 75.7 81.6 77.6 77.7 71.6 69.2

Employee Expenses 1128.6 1235.2 1212.4 1137.7 1187.0 1239.3 1199.1 1215.1 1248.8 5.2 2.8

% of Revenue 18.3 18.3 17.6 16.0 15.5 15.0 14.5 15.4 17.5

Other Expenditure 2638.6 2067.2 2290.2 2006.2 2786.8 2235.7 2058.4 1995.8 2145.5 -23.0 7.5

% of Revenue 42.9 30.6 33.3 28.2 36.4 27.1 24.9 25.2 30.1

Total Expenditure 5364.7 4993.7 5000.4 4876.7 5382.4 5322.0 5097.4 5459.5 5589.5 3.8 2.4

% of Revenue 87.1 73.9 72.8 68.5 70.3 64.6 61.7 69.0 78.3

EBITDA 792.4 1767.8 1872.9 2245.6 2271.9 2921.0 3167.7 2453.1 1547.5 -31.9 -36.9

EBITDA Margin (%) 12.9 26.1 27.2 31.5 29.7 35.4 38.3 31.0 21.7

Depreciation 461.8 240.2 258.4 250.9 288.0 316.0 303.8 306.8 338.2 17.4 10.2

Other Income 382.5 164.1 115.2 172.9 206.0 157.1 119.4 122.2 224.5 9.0 83.8

Profit before Interest & Tax 713.0 1691.8 1729.8 2167.7 2189.9 2762.1 2983.3 2268.5 1433.8 -34.5 -36.8

Interest 124.8 134.5 158.2 127.6 103.0 134.6 53.7 166.5 45.0 -56.3 -73.0

Less: Exceptional Items 0.0 685.2 0.0 0.0 0.0 0.0 0.0 0.0 0.0 NA NA

PBT 588.3 872.1 1571.6 2040.1 2086.9 2627.5 2929.5 2102.0 1388.8 -33.5 -33.9

Total Tax -599.9 112.8 294.6 88.8 417.6 352.7 441.7 372.9 44.3 -89.4 -88.1

PAT 1188.2 759.3 1277.0 1951.3 1669.3 2274.8 2487.9 1729.1 1344.5 -19.5 -22.2

Minority Interest 301.2 203.4 270.4 394.8 246.7 241.1 236.0 250.0 161.9 -34.4 -35.3

PAT after MI 886.9 555.9 1006.6 1556.4 1422.7 2033.7 2251.9 1479.1 1182.7 -16.9 -20.0

EPS (|) 3.7 2.3 4.2 6.5 5.9 8.5 9.4 6.2 4.9 -16.9 -20.0

Share Capital (cr) 239.9 239.9 239.9 239.9 239.9 239.9 239.9 239.9 239.9

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 9

Conference call highlights

US finished dosage sales benefited from authorised generic sales

of gBenicar (Olmesartan; CVS) and its combinations during the

quarter

The management has ruled out Halol resolution in FY18. It is

looking for site transfer arrangements for some of the key

products from Halol

The management has cautioned on a challenging FY18 mainly on

account of US generic pricing pressure and pending Halol

resolution. It expects single digit de-growth in overall revenues for

FY18

R&D spend for FY18 will be 9-10% of overall revenues

It has guided for ~US$350 million capex for FY18

The management has identified dermatology, ophthalmology,

oncology and CNS as priority areas

As per management, pricing pressure in the US generics space is

product specific and not for the entire segment

It expects price erosion in generics even in exclusivity period,

going forward

As per the management, the company has achieved two-third of

the targeted US$300 million synergy pertaining to Ranbaxy

acquisition

The managements expects Tildrakizumab launch in early FY19.

Currently, trials are ongoing for application in other indications

Taro’s revenues declined 26% YoY to US$196 million in the

backdrop of continuing increased competition and a challenging

pricing environment. Overall volumes increased 3%. EBITDA

margins contracted 1608 bps YoY to 53.7%. Net profit declined

28% YoY to US$83 million

For Q4FY17, 14 ANDAs were filed while four approvals were

received. Overall, 427 ANDA have been approved in the US while

157 ANDAs await approval. Additionally, the pipeline includes 36

approved NDAs while five NDAs pending for approval

The company launched 11 new products in the Indian market in

Q4FY17

Odomzo (oncology) was acquired from Novartis in December,

2016, for $175 million and additional milestones payments. This

was approved by USFDA in July, 2015 for treatment of locally

advanced basal cell cancer and is the first branded oncology

product for Sun Pharma in the US. Total 70% who prescribed this

drug are dermatologists while the rest are oncologists

Seciera (for dry eyes disease), which was acquired from Ocular

Technologies, has shown promising phase III results. The

company will enter into dialogue with FDA regarding further

course of action for the product

The company has guided for filing of Investigational IL-23p19

inhibitor, Tildrakizumab, in FY18 and potential approval in FY19

ICICI Securities Ltd | Retail Equity Research Page 10

Exhibit 10: Trends in return ratios

Location Segmant Regulatory Approvals

Samba J&K Formulations

Jammu, J&K Formulations

Baddi Himachal Prdesh Formulations

Batamandi, Himachal Pradesh Formulations

Mohali, Punjab Formulations

Paonta Sahib, Himachal Pradesh Formulations

Taonsa, Punjab API

Sikkim Formulations

Guwahati, Assam Formulations

Malanpur, Madhya Pradesh API

Dewas, Madhya Pradesh Formulations

Halol, Gujarat Formulations USFDA, UKMHRA

Baska, Gujrat Formulations

Karkhadi, Gujrat Formulations, API USFDA, EU GMP

Ankleshwar, Gujrat API ISO 9002, WHO GMP

Panoli, Gujarat API USFDA, TGA, EU GMP, DKMA

Ahmadnagar, Maharashtra API USFDA, EU GMP

Dadra, Dadra & Nagar Haveli Formulations USFDA

Silvassa, Dadra & Nagar Haveli Formulations

Goa Formulations

Madhuramthakam, Tamil Nadu API ISO 9002, WHO GMP

Sungai Patani, Malasia Formulations

Dhaka, Bangladesh Formulations

Be-Tabs, South Africa Formulations

Lagos, Nigeria Formulations

Morocco, Africa Formulations

Egypt, Africa Formulations

Haifa, Isreal Formulations USFDA

Terapia S.A., Cluj, Romania Formulations

Tiszavasvari, Hungary Formulations USFDA, EU GMP

Cashel, Isreal Formulations

Jardin Pompeia, Brazil Formulations

Soa Paolo, Brazil Formulations

Del. Iztapalapa, Mexico Formulations

Chattanooga, TN, USA API USFDA

Philladelphia, PA, USA Formulations USFDA

Wilmington, MA, USA Formulations USFDA

Cranbery, New Jersey, USA Formulations USFDA

New Brunwick, NJ, USA Formulations

North Brunswick, NJ, USA Formulations

Brampton, Canada Formulations USFDA

Detriot, MI, USA Formulations USFDA

Chicago, IL, USA Formulations USFDA

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 11

Valuation

Dismal Q4 numbers (both from Taro and Sun) have summarised the

recent pricing woos in the US generics space. However, more worrisome

for Sun is the delay in Halol resolution. By the management’s own

assertion, the resolution is unlikely before the end of FY18 against earlier

expectation of Q2FY18. Unlike other generic players, the approval

momentum is also dismal in Sun’s case, mainly due to pending Halol

resolution. On the US generic pricing front, the management expects

challenges to remain in FY18 as well. Hence, it has guided for single digit

revenue decline for the year. The shift towards specialty products such as

Tildrakizumab (dermatology), BromSite, Seciera (both ophthalmic) and

Odomzo (oncology) are long term game plans, the benefits of which are

back-loaded. For now, the company is bracing for a ‘’new normal’’, a

scenario where product specific price erosion continuum and prolonged

cGMP resolution delays are here to stay. We downgrade the stock to

HOLD with a new target price of | 550 based on 20x FY19E EPS of | 25.7

and | 36 NPV for Tildrakizumab.

Exhibit 11: One year forward PE

0

500

1000

1500

2000

2500

May-1

1

Nov-1

1

May-1

2

Nov-1

2

May-1

3

Nov-1

3

May-1

4

Nov-1

4

May-1

5

Nov-1

5

May-1

6

Nov-1

6

May-1

7

(|)

Price 66.2x 54.3x 34.5x 18.7x 10.7x

[

Source: Company, ICICIdirect.com Research

Exhibit 12: One year forward PE of company vs. CNX Pharma

-10

0

10

20

30

40

50

60

70

80

90

May-11

Nov-11

May-12

Nov-12

May-13

Nov-13

May-14

Nov-14

May-15

Nov-15

May-16

Nov-16

May-17

(x)

Sun Pharma CNX Pharma

50% premium

Source: Company, ICICIdirect.com Research

Exhibit 13: Valuation

Revenues Growth EPS Growth P/E EV/EBITDA RoE RoCE

(| crore) (%) (|) (%) (x) (X) (%) (%)

FY16 28563 4.1 23.4 18.3 27.6 15.0 18.0 18.6

FY17E 31558 10.5 29.0 23.2 19.6 12.8 19.0 19.8

FY18E 30144 -4.5 20.9 -28.0 27.2 15.9 12.3 14.0

FY19E 32901 9.1 25.7 22.9 22.1 13.1 13.4 15.2

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 12

Recommendation history vs. Consensus

0

200

400

600

800

1,000

1,200

May-17Feb-17Dec-16Sep-16Jul-16May-16Feb-16Dec-15Sep-15Jul-15May-15

(|

)

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

(%

)

Price Idirect target Consensus Target Mean % Consensus with BUY

Source: Reuters, Company, ICICIdirect.com Research

Key events

Date Event

Jun-09 USFDA seizes more than 33 generic drugs from Caraco for failing to meet FDA cGMP requirements

Aug-10 Manufacturing facility in Cranbury, New Jersey receives warning letter from USFDA

Sep-10 Increases stake in Taro Pharma to 48.7% with voting rights of 65.8%

Apr-11 Forms joint venture with Merck & Co Inc to develop, manufacture and commercialise new combinations, novel formulations and branded generics in emerging

markets

Sep-11 Receives establishment inspection report (EIR) from USFDA for its Cranbury, New Jersey facility

Feb-12 USFDA grants special approval to Sun Pharma to supply short supply oncology product Doxil to the US market

Aug-12 USFDA gives approval to Caraco Pharma’s manufacturing facility & packaging sites to resume production for two drugs

Nov-12 Acquires US based dermatology company Dusa Pharma, which was marketing innovative drug & device Levulan (aminolevulinic acid HCl)

Dec-12 Acquires generic business of URL Pharma from Takeda Pharmaceuticals

Feb-13 Receives final approval for Doxorubicin Hcl Liposome injection (Doxil)

May-14 Karkhadi unit receives warning letter from the USFDA

Sep-14 Halol unit receives Form 483 observation letter from the USFDA

Mar-15 Sun Pharma acquires GSK's Opiates Business in Australia with two Opiates manufacturing facilities in Port Fairy & Latrobe

Apr-15 Completes Ranbaxy merger

Dec-15 Receives warning letter from the USFDA for its Halol manufacturing facility

Feb-16 Launches generic version of Gleevec (Imatinib Mesylate Tablets) in the US. The company has sole 180 days exclusivity for this product

Mar-16 Acquires14 established prescription brands in Japan from Novartis for a cash consideration of US$ 293 million

Dec-16 Halol unit receives Form 483 observations from the USFDA post re-inspection of the plant

Source: Company, ICICIdirect.com Research

Top 10 Shareholders Shareholding Pattern

Rank Investor Name Latest Filing Date % O/S PositionPosition Change

1 Shanghvi (Dilip Shantilal) 5-Oct-16 0.10 230.52m (0.62)m

2 Viditi Investment Pvt. Ltd. 5-Oct-16 0.08 200.85m (0.54)m

3 Tejaskiran Pharmachem Industries Pvt. Ltd. 5-Oct-16 0.08 194.82m (0.52)m

4 Family Investment Pvt. Ltd. 5-Oct-16 0.08 182.44m (0.49)m

5 Quality Investment Pvt. Ltd. 5-Oct-16 0.08 182.38m (0.49)m

6 Virtuous Finance, Ltd. 5-Oct-16 0.04 96.84m (0.26)m

7 Virtuous Share Investment Pvt. Ltd. 5-Oct-16 0.03 83.75m (0.22)m

8 Life Insurance Corporation of India 30-Sep-16 0.03 82.33m 0.00m

9 Aditya Medisales, Ltd. 5-Oct-16 0.02 40.15m (0.05)m

10 GIC Private Limited 30-Sep-16 0.01 35.03m (1.62)m

(in %) Dec-15 Mar-16 Jun-16 Sep-16 Dec-16

Promoter 54.7 55.0 55.0 55.0 54.4

Others 45.3 45.0 45.0 45.0 45.6

Source: Reuters, ICICIdirect.com Research

Recent Activity

Investor name Value ($) Shares Investor name Value ($) Shares

Valia (Sudhir V) 160.7m 14.3m OppenheimerFunds, Inc. -109.9m -10.6m

ICICI Prudential Asset Management Co. Ltd. 51.3m 5.0m Axis Asset Management Company Limited -68.9m -7.4m

Pratham Investments. 51.4m 4.6m Capital International Investors -71.1m -6.4m

J.P. Morgan Asset Management (Hong Kong) Ltd. 44.0m 4.2m Fidelity Management & Research Company -49.0m -4.7m

SBI Funds Management Pvt. Ltd. 21.7m 2.1m GIC Private Limited -18.1m -1.6m

Buys Sells

Source: Reuters, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 13

.

Financial summary

Profit and loss statement | Crore

(Year-end March) FY16 FY17E FY18E FY19E

Revenues 28,563.0 31,557.7 30,143.5 32,901.2

Growth (%) 4.1 10.5 -4.5 9.1

Raw Material Expenses 6,483.2 8,130.7 8,741.6 9,212.3

Employee Expenses 4,765.2 4,902.3 5,049.6 5,349.2

Other Expenditure 8,590.3 8,435.4 8,440.2 9,047.8

Total Operating Expenditure 19,838.7 21,468.5 22,231.5 23,609.3

EBITDA 8,724.3 10,089.3 7,912.1 9,291.9

Growth (%) 10.9 15.6 -21.6 17.4

Depreciation 1,026.3 1,264.8 1,401.3 1,473.3

Interest 476.9 399.8 304.6 254.6

Other Income 481.0 623.2 586.0 642.0

PBT 7,702.0 9,047.9 6,792.3 8,206.0

Less: Exceptional Items 685.2 0.0 0.0 0.0

Total Tax 934.9 1,211.6 1,018.8 1,230.9

PAT 4,967.5 6,964.4 5,014.0 6,162.7

Minority Interest 1,114.5 889.0 799.5 852.4

Adjusted PAT 5,652.6 6,964.4 5,014.0 6,162.7

Growth (%) 18.3 23.2 -28.0 22.9

EPS (Adjusted) 23.4 29.0 20.9 25.7

Source: Company, ICICIdirect.com Research

Cash flow statement | Crore

(Year-end March) FY16 FY17E FY18E FY19E

Profit/(Loss) after taxation 4967.5 6964.4 5014.0 6162.7

Depreciation 1026.3 1264.8 1401.3 1473.3

(Inc)/Dec in Current Assets -153.6 -1056.2 72.9 -2298.4

(Inc)/Dec in Current Liabilities -699.0 1874.7 -119.8 1010.6

Others 476.9 399.8 304.6 254.6

CF from operation 5618.1 9447.4 6672.9 6602.7

Purchase of Fixed Assets -3366.9 -2844.4 -1200.0 -1200.0

(Inc)/Dec in Investments 1407.7 116.7 -2305.4 -2305.4

Others 417.0 -3134.1 487.7 523.8

CF from Investing Activities -1542.1 -5861.8 -3017.7 -2981.6

Inc / (Dec) in Loan Funds -658.0 -247.1 -2000.0 -1000.0

Inc / (Dec) in Equity Capital -14.2 -0.7 0.0 0.0

Dividend and dividend tax -233.5 -1785.7 -857.1 -1053.4

Other Financial Activities -179.3 -400.5 -304.6 -254.6

CF from Financing Activities -1085.0 -2434.0 -3161.6 -2308.0

Cash generation during the year 2990.9 1151.6 493.6 1313.0

Op bal Cash & Cash equivalents 10998.3 13989.2 15140.8 15634.4

Closing Cash/ Cash Equivalent 13989.2 15140.8 15634.4 16947.4

Free Cah Flow 2251.2 6603.0 5472.9 5402.7

Source: Company, ICICIdirect.com Research

Balance sheet | Crore

(Year-end March) FY16 FY17E FY18E FY19E

Equity Capital 240.7 239.9 239.9 239.9

Reserve and Surplus 31,163.6 36,342.2 40,499.1 45,608.4

Total Shareholders funds 31,404.9 36,582.2 40,739.1 45,848.3

Total Debt 8,338.1 8,091.0 6,091.0 5,091.0

Deferred Tax Liability 61.6 314.8 339.7 364.6

Minority Interest 4,085.3 3,790.9 4,590.3 5,442.7

Other LT Liabitlies & LT Provision 2,303.4 1,496.1 1,570.9 1,649.5

Total Liabilities 46,193.3 50,274.9 53,331.0 58,396.1

Gross Block 18,005.9 22,154.5 23,354.5 24,554.5

Accumulated Depreciation 8,750.8 10,015.5 11,416.8 12,890.0

Net Block 9,255.2 12,138.9 11,937.7 11,664.4

Capital WIP 4,105.5 2,801.4 2,801.4 2,801.4

Total Fixed Assets 13,360.6 14,940.3 14,739.1 14,465.8

Investments 1,308.6 1,191.9 3,497.3 5,802.7

Deferred tax assets 2,187.5 2,492.8 2,617.5 2,748.3

Goodwill on Consolidation 4,181.1 5,536.2 5,536.2 5,536.2

LT Loans & Advances & Assets 3,032.4 4,526.2 4,752.5 4,990.2

Cash 13,989.3 15,140.8 15,634.4 16,947.4

Debtors 6,795.9 7,202.6 6,422.2 7,035.3

Loans and Advances 2,640.4 1,244.9 1,702.4 2,159.9

Inventory 6,423.6 6,832.8 6,473.0 7,091.0

Other current assets 300.1 1,935.9 2,545.7 3,155.5

Total Current Assets 30,149.3 32,357.0 32,777.7 36,389.2

Creditors 3,489.6 4,394.9 3,612.5 3,957.4

Provisions & other current liability 4,536.7 6,374.7 6,976.8 7,578.9

Total Current Liabilities 8,026.3 10,769.6 10,589.2 11,536.2

Net Current Assets 22,123.0 21,587.5 22,188.5 24,852.9

Application of Funds 46,193.3 50,274.9 53,331.0 58,396.1

Source: Company, ICICIdirect.com Research

Key ratios

(Year-end March) FY16 FY17E FY18E FY19E

Per share data (|)

Adjusted EPS 23.4 29.0 20.9 25.7

BV per share 130.2 152.5 169.8 191.1

Dividend per share 1.0 7.4 3.6 4.4

Cash Per Share 58.0 63.1 65.2 70.6

Operating Ratios (%)

Gross Margin 77.3 74.2 71.0 72.0

EBITDA Margin 30.5 32.0 26.2 28.2

PAT Margin 19.8 22.1 16.6 18.7

Inventory days 82.1 79.0 78.4 78.7

Debtor days 86.8 83.3 77.8 78.0

Creditor days 44.6 50.8 43.7 43.9

Asset Turnover 0.6 0.7 0.6 0.6

EBITDA Conversion rate 64.4 93.6 84.3 71.1

Return Ratios (%)

RoE 18.0 19.0 12.3 13.4

RoCE 18.6 19.8 14.0 15.2

RoIC 30.6 29.8 21.0 23.2

Valuation Ratios (x)

P/E 27.6 19.6 27.2 22.1

EV / EBITDA 15.0 12.8 15.9 13.1

EV / Net Sales 4.6 4.1 4.2 3.7

Market Cap / Sales 4.8 4.3 4.5 4.1

Price to Book Value 4.4 3.7 3.3 3.0

Solvency Ratios

Debt / EBITDA 1.0 0.8 0.8 0.5

Debt / Equity 0.3 0.2 0.1 0.1

Current Ratio 2.0 1.6 1.6 1.7

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 14

ICICIdirect.com coverage universe (Healthcare)

Company I-Direct CMP TP Rating M Cap

Code (|) (|) (| Cr) FY16 FY17E FY18E FY19E FY16 FY17E FY18E FY19E FY16 FY17E FY18E FY19E FY16 FY17E FY18E FY19E

Ajanta Pharma AJAPHA 1785 1,960 Buy 15711.5 45.4 59.7 66.3 75.3 39.3 29.9 26.9 23.7 42.9 39.2 34.9 31.7 34.2 33.1 28.4 25.6

Alembic Pharma ALEMPHA 561 615 Hold 10572.0 38.2 22.0 24.5 30.6 14.7 25.5 22.9 18.3 51.5 26.0 23.1 24.8 44.9 21.9 20.8 21.9

Apollo Hospitals APOHOS 1247 1,440 Buy 17348.2 22.2 21.8 31.4 45.3 56.2 57.2 39.7 27.5 8.2 8.1 10.3 13.3 8.9 8.2 10.7 13.6

Aurobindo Pharma AURPHA 658 965 Buy 38524.6 33.9 40.1 40.7 50.7 19.4 16.4 16.2 13.0 23.3 24.3 21.3 23.0 28.1 25.3 20.7 20.8

Biocon BIOCON 1075 1,120 Buy 21508.0 23.1 32.6 34.4 44.2 46.5 32.9 31.2 24.3 9.1 13.0 13.7 16.5 11.4 14.4 13.7 15.4

Cadila Healthcare CADHEA 365 380 Hold 37392.2 15.0 11.2 15.1 18.9 24.4 32.5 24.1 19.4 26.7 14.4 18.3 20.9 28.6 18.5 21.1 22.0

Cipla CIPLA 576.1 575 Hold 46338.2 18.5 17.8 24.7 31.9 31.1 32.3 23.3 18.1 12.0 10.9 14.0 16.6 12.5 10.9 13.4 15.0

Divi's Lab DIVLAB 725 925 Buy 19233.2 41.8 44.6 51.8 57.9 17.3 16.3 14.0 12.5 30.7 28.5 28.0 26.5 25.9 23.0 22.2 20.7

Dr Reddy's Labs DRREDD 2941 2,930 Hold 48727.8 141.4 74.5 114.5 154.3 20.8 39.5 25.7 19.1 17.3 7.0 11.5 15.1 20.6 10.0 13.6 15.8

Glenmark Pharma GLEPHA 946 1,155 Buy 26686.1 32.2 63.0 54.4 60.8 29.4 15.0 17.4 15.6 16.2 26.8 20.8 21.9 21.2 29.7 20.6 18.8

Indoco Remedies INDREM 267 315 Buy 2460.4 9.4 8.9 14.2 18.5 28.4 30.1 18.8 14.4 12.9 9.7 14.9 18.1 14.8 12.6 17.4 19.2

Ipca Laboratories IPCLAB 522 560 Hold 6589.9 10.0 15.1 24.1 31.2 52.1 34.6 21.7 16.8 5.7 9.9 12.8 14.8 5.5 7.8 11.3 13.0

Jubilant Life JUBLIF 681.5 810 Buy 10855.0 26.0 37.4 53.9 67.5 26.2 18.2 12.6 10.1 12.0 14.2 16.2 18.3 14.2 17.3 20.2 20.4

Lupin LUPIN 1431 1,890 Buy 64616.9 50.4 62.2 67.5 83.8 28.4 23.0 21.2 17.1 18.6 20.3 20.8 23.9 20.7 21.1 19.2 19.9

Natco Pharma NATPHA 776 750 Buy 13526.3 8.5 12.8 13.1 15.0 91.3 60.6 59.3 51.6 16.0 19.9 17.5 17.8 11.9 15.6 14.0 14.1

Sun Pharma SUNPHA 649 765 Buy 155780.7 23.4 29.9 29.9 35.3 27.7 21.7 21.7 18.4 18.6 19.1 17.3 18.0 18.0 19.2 16.6 16.8

Syngene Int. SYNINT 485 570 Hold 9708.0 11.1 15.5 16.9 20.5 51.3 36.7 33.7 27.7 13.2 17.8 18.1 20.7 21.0 23.2 20.6 20.4

Torrent Pharma TORPHA 1260 1,475 Buy 21317.0 107.8 55.7 62.2 77.6 11.7 22.6 20.3 16.2 46.7 21.0 23.8 26.5 53.8 23.0 21.5 22.3

Unichem Lab UNILAB 278.3 285 Hold 2529.0 12.3 13.2 17.5 23.7 22.6 21.1 15.9 11.7 13.8 14.5 16.2 18.9 11.7 11.3 13.3 15.6

RoE (%)EPS (|) PE(x) RoCE (%)

Source: Company, ICICIdirect.com Research

ICICI Securities Ltd | Retail Equity Research Page 15

RATING RATIONALE

ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com assigns

ratings to its stocks according to their notional target price vs. current market price and then categorises them

as Strong Buy, Buy, Hold and Sell. The performance horizon is two years unless specified and the notional

target price is defined as the analysts' valuation for a stock.

Strong Buy: >15%/20% for large caps/midcaps, respectively, with high conviction;

Buy: >10%/15% for large caps/midcaps, respectively;

Hold: Up to +/-10%;

Sell: -10% or more;

Pankaj Pandey Head – Research [email protected]

ICICIdirect.com Research Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

ICICI Securities Ltd | Retail Equity Research Page 16

ANALYST CERTIFICATION

We /I, Siddhant Khandekar CA-INTER, Mitesh Shah MS (Finance) Harshal Mehta MTech (Biotechnology) Research Analysts, authors and the names subscribed to this report, hereby certify that all of the

views expressed in this research report accurately reflect our views about the subject issuer(s) or securities. We also certi fy that no part of our compensation was, is, or will be directly or indirectly related

to the specific recommendation(s) or view(s) in this report.

Terms & conditions and other disclosures:

ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities

Limited is a Sebi registered Research Analyst with Sebi Registration Number – INH000000990. ICICI Securities is a wholly-owned subsidiary of ICICI Bank which is India’s largest private sector bank and has

its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fund management, etc. (“associates”), the details in respect of which

are available on www.icicibank.com.

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking

and other business relationship with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts

and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and

meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without

prior written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current.

Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended

temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory capacity to this

company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This

report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial

instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their

receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific

circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment

objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate

the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any

loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the

risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to

change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment

in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in

respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned

in the report in the past twelve months.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did not receive any

compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts

and their relatives have any material conflict of interest at the time of publication of this report.

It is confirmed that Siddhant Khandekar CA-INTER, Mitesh Shah MS (Finance) Harshal Mehta MTech (Biotechnology) Research Analysts of this report have not received any compensation from the

companies mentioned in the report in the preceding twelve months.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month

preceding the publication of the research report.

Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject

company/companies mentioned in this report.

It is confirmed that Siddhant Khandekar CA-INTER, Mitesh Shah MS (Finance) Harshal Mehta MTech (Biotechnology) Research Analysts do not serve as an officer, director or employee of the companies

mentioned in the report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report.

We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution,

publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities

described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and

to observe such restriction.

report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial

instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their

receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific

circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment

objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate

the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any

loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the

risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to

change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment

in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in

respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned

in the report in the past twelve months.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its analysts did not receive any compensation

or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts have any

material conflict of interest at the time of publication of this report.

It is confirmed that Siddhant Khandekar CA-INTER Mitesh Shah MS (Finance), Harshal Mehta MTech (Biotechnology) Research Analysts of this report have not received any compensation from the

companies mentioned in the report in the preceding twelve months.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.