substance over form in brazil (and la) in international...

TRANSCRIPT

Prof. Dr. Marcos Aurélio Pereira Valadão

(BRAZIL)

Substance over Form in

Brazil (and LA)

In International Tax Cases

1 FIT Conference 2012

Presentation Plan

• Theoretical approach: Common law vs. Civil law

• Brazil: Substance over Form (SoF) - historical perspective leading to introduction of GAAR (?!!)

• Brazil: Some important cases

• Latin America snapshot 2 FIT Conference 2012

The (SoF) approach is more suitable to common law systems, because the judge is allowed to innovate in cases that are not clearly described in the statutory law.

Brazil and Spanish speaking countries are civil law countries (Panama is “mixed”).

In Central and South Americas 95% is civil law. 3 FIT Conference 2012

• In the last few decades businesses have diversified a lot. Innovative financial schemes, creative business restructurings, innumerous derivative instruments, etc., provide current businesses with almost unlimited opportunities.

• Consequence: traditional normative systems are no longer sufficient to cope with the problem of aggressive tax planning.

4 FIT Conference 2012

TAX PLANNING --TSUNAMI

5 FIT Conference 2012

BRAZIL Since the 1960s judicial courts applied

the (SoF) doctrine to tax cases on a very limited basis. Mostly, when case was pretty clear, and in terms of Private Law it was considered an unlawful action (civil wrong).

Later in the 1980s, there was an important decision by the Fed. Court of Appeals in the case of Grendene (1987), where the court decided that the transaction was abusive (SoF).

6 FIT Conference 2012

BRAZIL

• In 2001, Complementary Law n. 104 introduced a GAAR rule in the National Tax Code (which is applicable also to States and Local Governments).

• In 2003, a new Civil Code (2002) entered into force with a clear notion of illegality of “fraud against imperative law”, and of “abuse of rights”.

7 FIT Conference 2012

BRAZIL

Civil Code (2002)

Art. 187. The holder of a right also commits a tort when, in exercising such right, clearly exceeds the limits imposed by its economic or social purpose, good-faith or morals.

8 FIT Conference 2012

BRAZIL

Art. 116 National Tax Code (2001) states:

Tax authority may disregard acts or legal acts performed for the purpose of dissimulating (disguising) the occurrence of the event giving rise to the tax or the nature of the elements that compose the tax liability, subject to procedures to be established in statutory law.

9 FIT Conference 2012

BRAZIL

This paragraph demands other laws to establish the procedure.

In 2002 the Congress did not approve the procedural law bill.

However, since then, the decisions regarding tax planning matters

rely more on substance over form. 10 FIT Conference 2012

Jurisprudence of Administrative Court of

Tax Appeals (CARF)

1) Legal? >> YES

2) Simulation? >> NO

3)There is a economic

rationality on business

restructurings? >>YES

Valid transaction

However, the jurisprudence is not plain and predictable.

11 FIT Conference 2012

CASE I : CARF 104-20749 (2005)

CARF found that the taxpayer (Case Mario

Frering) was liable regarding taxable dividend

distributions from B to C (ac. B>A). SoF.

TAXPAYER

(BRAZIL)

A

(BRAZIL)

C

(CAYMAN)

B

(BERMUDA)

Taxpayer owns

49,99% of A´s shares

1) A owns

100% of B´s shares;

3) 50% of B´s

shares was sold to C

2) C was created by

Taxpayer (100%).

4) B makes a dividend

distribution do C

12 FIT Conference 2012

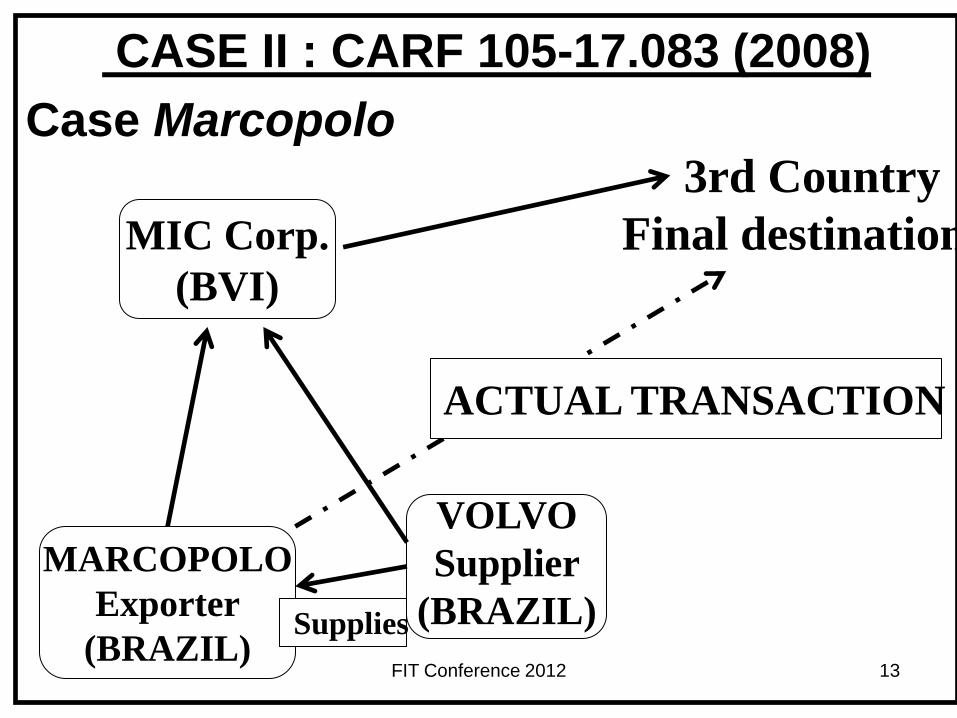

CASE II : CARF 105-17.083 (2008)

Case Marcopolo

MARCOPOLO

Exporter

(BRAZIL)

VOLVO

Supplier

(BRAZIL)

MIC Corp.

(BVI)

3rd Country

Final destination

Supplies

ACTUAL TRANSACTION

13 FIT Conference 2012

CASE II : MARCOPOLO - FACTS

• MIC Corp is 100% controlled by

Marcopolo.

• Transactions between Marcopolo and

MIC Corp. (BVI) were correctly

performed considering transfer

pricing regulations.

• No CFC rules applicable at this time.

There are similar transactions with offshore

jurisdiction of Uruguay (ILMOT). 14 FIT Conference 2012

CASE II : Marcopolo Case – Decision

CARF found no business

purpose for establishing MIC Corp.

in BVI, based on lack of economic

substance. All steps of the

transactions were deemed to be

legal, however the substance over

form (SoF) approach was applied

finding Marcopolo liable to tax.

15 FIT Conference 2012

ADDITIONAL COMMENTS

-- CARF, in an similar case (Marcopolo,

different years, CFC rules applied),

decided in a different way. Under

appeal, the Upper Chamber, did not

reverse the decision.

-- However, in another similar case

(Arcelor Mittal, 2012) the same

chamber adopted the SoF doctrine.

16 FIT Conference 2012

CASE III : CARF 101-97070 (2008)

Eagle 2

EAGLE

(AMBEV)

(BRAZIL)

MONTHIERS

(URUGUAY) &

CCBA

(ARGENTINA)

JALUA

(SPAIN)

100 %

100%

Indirect control 17 FIT Conference 2012

Case Eagle 2

What is at stake in Eagle 2 Case?

• Application of the Brazilian CFC

regulations towards the subsidiary in Spain

(that owns a subsidiary in Uruguay).

• Application of the Brazil-Spain DTA (arts. 7,

10, 23, IV, or none).

• Concept of “indirect control” (which here

means SoF). 18 FIT Conference 2012

Eagle 2 -- Decision

The lower chamber of CARF decided

that, in this case, EAGLE Co. through

an indirect control scheme would have

wrongly avoided to apply the CFC rule

and that the DTA would not apply.

(SoF doctrine and tax transparency

were applied, thus EAGLE was liable

to tax). 19 FIT Conference 2012

LATIN AMERICAN SNAPSHOT

Argentina – has applied the disregard of

legal entity doctrine for a long time.

Mexico – Article 109 (iv) of the Tax Code

contains a provision that allows substance

over form, but of limited application.

Reforms?

Colombia – formal approach (one exception

for transactions with shares), no GAAR.

Venezuela - Following the trend (new law

since 1999 allows substance over form). 20 FIT Conference 2012

THANK YOU

FIT CONFERENCE -- 2012

FIT Conference 2012 21