studie...

TRANSCRIPT

On behalf of the Bundesministerium für Wirtschaft und Technologie

June 2012

Study on Fast Growing Young Companies (Gazelles) - Summary

STUDY ON FAST GROWING YOUNG COMPANIES (GAZELLES)

Contact: Dr. Kirsti Dautzenberg Business Manager Rambøll Management

T 030 / 30 20 20-271 F 030 / 30 20 20-299 M 0151 / 44 006-271 [email protected]

Authors: Dr. Kirsti Dautzenberg

Marius Ehrlinspiel Dr. Hardy Gude, Creditreform Judith Käser-Erdtracht Philipp Till Schultz

Julian Tenorth Michael Tscherntke Prof. Dr. Frank Wallau, Fachhochschule der Wirtschaft Paderborn/Bielefeld

1. Introduction

The overall economic significance of fast growing young companies is estimated to be high. Various studies find that young fast growing companies create a high increase in qualified employment in both the short- and medium- term and in the long run. They further deploy strong positive effects on the dynamics of the future economic development. In order to do justice to the significance of young fast growing companies David Birch introduced the term “gazelle”. In light of this, the present research study was conducted between 08/01/2011 and 02/29/2012.

2. Approach

In a first step of the study, the scientific literature on fast growing young companies (“gazelles”) is reviewed and assessed (see chapter 3). On the one hand the review focuses on the definitions of young fast growing companies used in the literature. On the other hand an assessment of the empirical findings about the characteristics of young fast growing companies is developed. Hypotheses for an empirical study on gazelle companies are

derived based on the assessment of the literature. These hypotheses are then integrated into the questionnaires used for a telephone survey and the development of the interview guidelines used for case studies with selected companies. In the next step, the definition of a “gazelle company” used in this study is determined and elucidated (see chapter 4.1). The definition takes into account the state of the art research, the comparability to other studies as well as the specific features of the “Creditreform” data base. Thereupon, all young fast

growing companies in Germany established between 1995 - 2007 – therefore, all gazelle companies until 2011- are identified via the Creditreform data basis. The identified companies are then characterized and assessed by applying the following criteria: Number of companies, number of employees, development of the number of employees, sector and regional aspects. The results can be found in chapter 4.2. In order to conduct a telephone survey among founders and /or managers, a randomized sample was

taken from the population of young fast growing companies in Germany. Furthermore, in- depth case studies were carried out with selected companies. Both, the survey and the case-studies aimed at analyzing the contribution of “gazelles” to the branch and structural change. While also stressing the current and potential role of public authorities with regards to the support of young fast growing

companies, the survey and the case studies offer valuable clues to the growth drivers and - obstacles with which young fast growing companies find themselves confronted.

3. State of the art David Birch first coined the term “gazelle” in the 1980s. The term “gazelle” is used to describe companies which exhibit high growth rates during a limited amount of time. Birch postulated that a major share of

new jobs is created in SME, particularly in new and highly innovative SME. Birch and his colleagues empirically verified this hypothesis for the US.1 According to his study, on average two thirds of all jobs are created by SME. His results were confirmed for Europe2 and have proven to be particularly similar in Germany.3 Moreover, studies find that the share of these companies measured against the overall number of companies or the number of companies founded in a respective year is very small in any given economy. However, these numbers vary between 2% and 15%, depending on the study.

1 Birch, D. L., Haggerty, A. und W. Parsons (1998): Who's creating jobs?. Cambridge, MA: Cognetics. 2 See: Kirchhoff, Bruce A. (1994): Entrepreneurship and Dynamic Capitalism. The Economics of Business Firm Formation and Growth. London:

Greenwood. S. 120ff. / Siebert, H. (1999): How can Europe solve its unemployment problem? Kieler Diskussionsbeiträge 342, Kiel: Institut für

Weltwirtschaft / OECD (1998): Technology, productivity and job creation. Best policy practices.Paris: OECD Publishing. / Schreyer, P. (2000):

High-growth-firms and employment. STI Working Papers 2000/3. 3 See: Brüderl, J., Preisendörfer, P. und R. Ziegler (1996): Der Erfolg neugegründeter Betriebe. Berlin: Duncker & Humblot. / Harhoff, D. und G.

Licht (1996): Innovationsaktivitäten kleiner und mittlerer Unternehmen. Baden-Baden: Nomos. / Almus, M. und E. A. Nerlinger (1999):

Wachstumsdeterminanten junger innovativer Unternehmen. Empirische Ergebnisse für Westdeutschland. Jahrbuch für Nationalökonomie und Statistik, Heft 3/4, P. 257-273 / Kahmann, M. (2000): Schöpferische Zerstörung und Gründungsdynamik im marktwirtschaftlichen

Entwicklungsprozess. Berlin: Mensch & Buch / Rammer, Ch. et al. (2006): Unternehmensgründungen in der Biotechnologie in Deutschland 1991

bis 2004. ZEW Dokumentation Nr. 06-03. Mannheim. P. 47 ff. / UNICE (Union of Industrial and Employers' Conferation of Europe) (1999):

Fostering Entrepreneurship in Europe. The UNICE Benchmarking Report 1999. P. 11. Eventhough the share of gazelle companies is much higher

in the US than in Europe.

David Birch not only established the “gazelle” term but also was the first one to define what constitutes a

“gazelle” company.4 Subsequently, a multitude of different definitions emerged. The definitions can be distinguished according to the following criteria: growth indicator, measuring method, considered time period and the introduction of additional criteria. The two most frequently used indicators are the number of employees and revenues. Also, the measuring method varies significantly depending on the applied definition. Having said this, growth is determined using either relative or absolute growth as well as a mix

of the two. With respect to the considered time period definitions only vary insignificantly. The examined growth period in research studies usually is three years. In general, the choice of the appropriate definition highly depends on the data base. Due to the multitude of definitions a comparative analysis of different countries or studies is not feasible. This conclusion stresses the inevitable necessity of a common definition which would allow for comparative analyses of different countries. Further limitation with regards to the comparability of results is owed to different data sources and methods of data

collection. Regardless of theses complicacies, there is a multiplicity of empirical studies on fast growing young companies allowing for the derivation of some fundamental, abstracted findings on young fast growing companies. Altogether three meta-studies and 22 empirical studies, conducted between 1994 and 2011, were found. The number of empirical studies though has augmented significantly over the past years. The three

meta-studies collectively come to the conclusion that gazelle companies only account for a small share of

all companies. When measured against the number of job creating companies, however, gazelle companies account for a substantial share. The 22 empirical studies largely rely on individual company data, which was collected between the late 1970s and mid-2000. The bulk of company data stems from the 1990s. Five out of 22 studies were conducted in the US, two in Canada and the rest in European countries such as Germany (3), Finland (3), Sweden (1), UK (1), Spain (2) and the Netherlands (1). Furthermore, four studies simultaneously scrutinized several European and North American countries.

Those studies largely sticking to the definition used by the OECD, come to the conclusion that 2% to 5% of companies in a population can be labeled a gazelle company. However, 60%- 75% of all newly created jobs can be allotted to gazelle companies. Thus, gazelle companies, despite their small share measured against all companies, deploy above average employment effects. Based on David Birch´s work it was long assumed that mainly the companies´ young age would drive growth. Recent works by Acs et al. (2008), however, suggest that the average fast growing company is 25 years old. Bearing that in mind, it

seems helpful to reconsider what the term “young” company actually means. Also, this ought to be included in the definition of a “gazelle” company. Hölzl (2008) finds that fast growth is rather a temporary phenomenon. With regards to the sector in which “gazelle” companies operate, contradicting results can

be found. Works by Bos and Stam (2011) find that sectors such as education, sanitary services and knowledge- and technology intensive branches generate an above-average number of “gazelle” companies. Hölzl (2009), on the other hand, finds that gazelle companies are not over-represented in high tech branches -even though, in highly- industrialized countries, “gazelle” companies are, in fact,

characterized by an affinity to technology, research and innovation. Nonetheless, “gazelle” companies do exist in all branches. Current research on company growth has increasingly been discussing the significance of knowledge as a main driver for innovation, growth and employment. While research used to mainly focus on the circumstances which favor growth, these new approaches also aim at explaining the influential drivers for economic growth.5 Works by Bottazzi et al. (2001) and Geroski et al. (1997) find no significant relationship between company growth and innovation activity.6

Empirical studies that explicitly focus on fast growing companies, on the other hand, find a positive relationship between innovation activity and growth.7

4 Birch, D. L. und Medoff, J. (1994): Gazelles. In: Solmon, L. C. und A. R. Levenson (Hrsg): Labor markets, employment policy and job creation.

Boulder, CO: Westview und Birch. P. 159–167. 5 Gablers Wirtschaftslexikon: Neue Wachstumstheorie: wirtschaftslexikon.gabler.de. 6 See: Bottazzi, G. et al. (2001): Innovation and Corporate Growth in the Evolution of the Drug Industry. International Journal of Industrial

Organization 19: S. 1161-1187 / Geroski, P. A., Machin, S. J. und C. F. Walters (1997): Corporate Growth and Profitability. Journal of Industrial Economics 45(2): P. 171-189.

7 See: Coad, A. und R. Rao (2008): Innovation and Firm Growth in High-Tech Sectors: A Quantile Regression Approach. Research Policy 37(4): S.

633-648 / Hölzl, W. (2009): Is the R&D behaviour of fast-growing SMEs different? Evidence from CIS III data for 16 countries. Small Business

Economics 33(1): S. 59-75 / Stam, E. und K. Wennberg (2009): The roles of R&D in new firm growth. Small Business Economics 33(1): P. 77-

89.

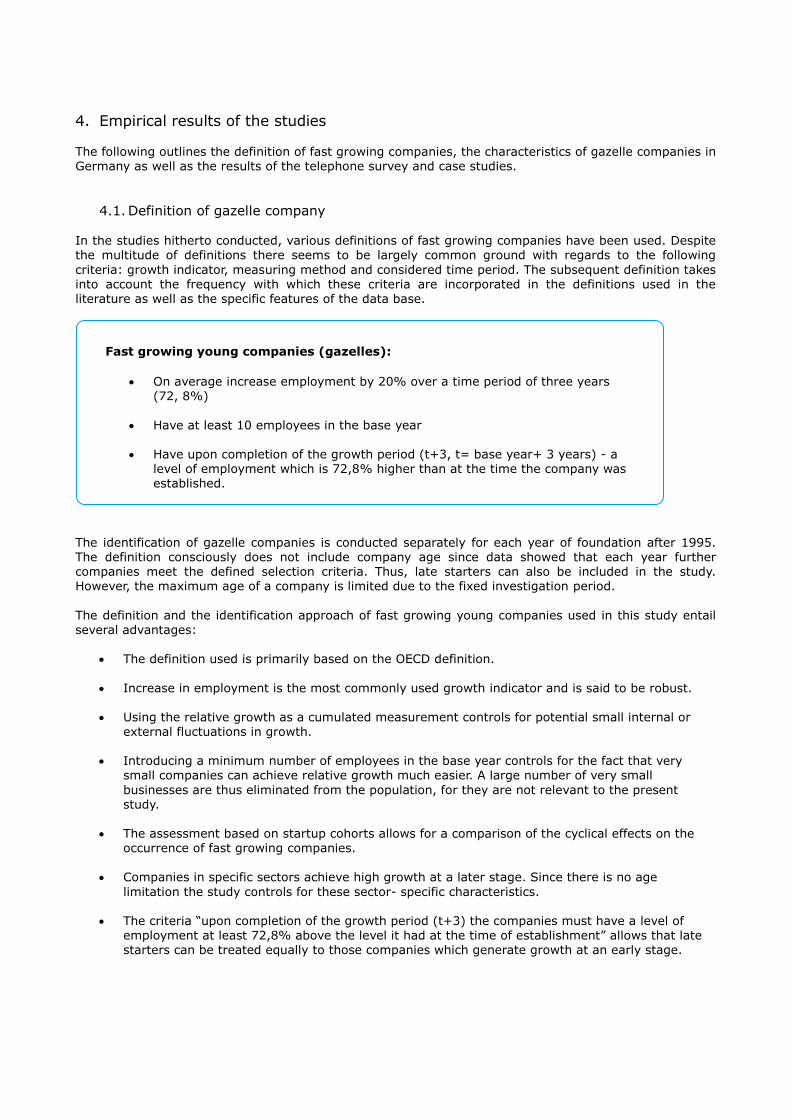

4. Empirical results of the studies The following outlines the definition of fast growing companies, the characteristics of gazelle companies in Germany as well as the results of the telephone survey and case studies.

4.1. Definition of gazelle company In the studies hitherto conducted, various definitions of fast growing companies have been used. Despite the multitude of definitions there seems to be largely common ground with regards to the following

criteria: growth indicator, measuring method and considered time period. The subsequent definition takes into account the frequency with which these criteria are incorporated in the definitions used in the literature as well as the specific features of the data base.

The identification of gazelle companies is conducted separately for each year of foundation after 1995. The definition consciously does not include company age since data showed that each year further companies meet the defined selection criteria. Thus, late starters can also be included in the study. However, the maximum age of a company is limited due to the fixed investigation period.

The definition and the identification approach of fast growing young companies used in this study entail

several advantages:

The definition used is primarily based on the OECD definition.

Increase in employment is the most commonly used growth indicator and is said to be robust.

Using the relative growth as a cumulated measurement controls for potential small internal or external fluctuations in growth.

Introducing a minimum number of employees in the base year controls for the fact that very

small companies can achieve relative growth much easier. A large number of very small

businesses are thus eliminated from the population, for they are not relevant to the present study.

The assessment based on startup cohorts allows for a comparison of the cyclical effects on the

occurrence of fast growing companies.

Companies in specific sectors achieve high growth at a later stage. Since there is no age

limitation the study controls for these sector- specific characteristics.

The criteria “upon completion of the growth period (t+3) the companies must have a level of employment at least 72,8% above the level it had at the time of establishment” allows that late starters can be treated equally to those companies which generate growth at an early stage.

Fast growing young companies (gazelles):

On average increase employment by 20% over a time period of three years (72, 8%)

Have at least 10 employees in the base year

Have upon completion of the growth period (t+3, t= base year+ 3 years) - a level of employment which is 72,8% higher than at the time the company was established.

4.2. Results of the characterization of gazelle companies in Germany When applied to all businesses established between 1995- 2006 the definition used in this study yields an overall number of 13.021 gazelle companies in Germany. Table 4-1 shows the number of gazelle

companies for each of the identified cohorts in the investigation period. The columns depict the respective startup cohort and the rows show the respective “year of gazelle companies”. The “year of gazelle companies” refers to the year in which a company of a certain startup cohort meets the defined growth criteria. When looking at table 4-1 horizontally the rows show how many companies of a specific year (year of

gazelle companies) became a gazelle accompany and from which startup cohort these companies have emerged. For instance, in the year of gazelle companies 2002, 87 companies were established in 1995, 129 were established in 1996, 156 were established in 1997 and 734 were established in 1998. Thus, an overall number 1.106 companies became gazelle companies in 2002.

Table 4-1: Number of gazelle companies according to start-up cohort und gazelle-age group

Gazelles-age group

cohort 1995

cohort 1996

cohort 1997

cohort 1998

cohort 1999

cohort 2000

cohort 2001

cohort 2002

cohort 2003

cohort 2004

cohort 2005

cohort 2006

Total

1999 793 793

2000 174 898 1.072

2001 143 191 819 1.153

2002 87 129 156 734 1.106

2003 87 99 116 155 765 1.222

2004 66 81 99 92 135 580 1.053

2005 52 74 78 90 127 141 496 1.058

2006 53 62 69 55 101 95 100 498 1.033

2007 45 50 68 48 99 94 114 103 482 1.103

2008 41 51 42 54 73 82 96 81 118 521 1.159

2009 53 62 40 59 66 65 66 92 77 132 491 1.203

2010 37 44 60 33 63 52 53 62 75 89 120 378 1.066

Total 1.631 1.741 1.547 1.320 1.429 1.109 925 836 752 742 611 378 13.0218

Source: Own Calculations Rambøll, Data Creditreform

8 For the start-up cohort 2007, 427 gazelle companies were identified until the key date 12/31/2011. However, this startup-age group cannot be included any more in the analysis of this study. Still

it seems interesting that the number of the gazelle companies increases again.

The development of the number of gazelle companies depicted in table 4-1 allows for the identification of two general trends. When looking at table 4-1 vertically, the number of gazelle companies per startup cohort shows that most companies become gazelle companies immediately after they were established. As far as the development of gazelle companies which belong to rather old start up cohorts is concerned, it can thus be said that roughly 50% earned their status as a gazelle company directly after the company was set up.9

Therefore, the number of newly emerged gazelle companies from a respective start-up cohort decreases

gradually as time progresses.

The second trend shown in table 4-1 is that the start-up cohorts from 1995 - 1999 on average generate 800 gazelle companies right after the companies were established. As of the year 2000, however, this average only adds up to 480 gazelle companies. Graph 4-1 illustrates this finding specifically for those companies that accomplished their growth period four years after the company was established (“early starters”). It is shown that the number of “early starters”, identified from any respective start-up cohort, declines continuously over

time. While in 1999 793 companies met the criteria of a gazelle company directly after the company was founded this was only true for 378 companies in 2010.

Graph 4-1: Number of gazelle companies per startup cohort which began their growth period one year after the business was established and became a gazelle company 4 years after foundation (early starter gazelles)

Source: Own Calculations Rambøll, Data Creditreform

As illustrated in graph 4-1 this decline does not occur gradually over time. The number of companies drops

drastically in 2000. While between 1995 and 1995 an admittedly volatile average of 800 early emerging gazelle companies per start-up cohort was reached, graph 4-1 shows a significant decline in the number early emerging gazelle companies as of 2000. The average number of early emerging gazelle companies as of 2000 is 492 per start-up cohort. Possibly, this decrease can be attributed to the external crises in 2000/01

(dot com bubble, 9/11) which had a negative effect on the overall economic situation in Germany.

9 The statement about the proportional share refers only to the considered investigation period, because every year other fast-growing start-up

companies from a start-up cohort are added, however, a point about the proportional share cannot be made.

793

898

819

734765

580

496 498 482521

491

378427

0

100

200

300

400

500

600

700

800

900

1000

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Num

ber

of gazelle c

om

panie

s

Year of gazelle companies

In the foundation year 2000 the number of gazelle companies drops erratically

In large part gazelle companies develop directly after foundation

This seems natural for the negative impact of these crises not only affected the general entrepreneurial – and growth activity but also impeded the development of fast growing companies. The lowest number of gazelle companies (378) falls in the year 2006.10 Combined both trends lead to the conclusion that the general growth dynamic of newly founded companies decelerated substantially between 1995 and 2006.

As frequently stated in the literature, gazelle companies contribute disproportionately to the creation of new jobs. Therefore, the following compares the number of jobs created by gazelle companies as opposed to the

number of jobs created by the overall number of startups in the investigated time period. This is depicted in graph 4-2. It is shown that in the investigation period the share of jobs provided by gazelle companies varies significantly. While gazelle companies of the startup cohort 1997 account for almost 27% of all jobs provided by startup companies, this number drops to 10% for businesses of the startup cohort 2002. Disregarding these fluctuations, a general tendency towards a decreasing share of jobs provided by gazelle companies

measured against all startups can be observed over the investigation period. The share drops from more than 20% to below 15%.

Graph 4-2: Share of gazelle companies measured against the overall number of jobs provided by start-ups

Source: Own Calculations Rambøll, Data Creditreform

This decline can be attributed to the fact that within the investigation period the number of gazelle companies decreased substantially. In absolute terms 8.371.681 jobs were created by all startups in 2010, 1.347.482 of which account for jobs created by gazelle companies. Hence, one in six jobs of all newly founded businesses as of 1995 was created by a gazelle company.

10

In 2011 427 companies from the start-up cohort fulfilled the defined growth criteria in 2007 (see remark table 4-1). Whether it becomes a new

upward trend or however, hardening at a new low level, cannot be predicted.

20,57%22,91%

26,98%

16,58%

19,98%

16,54%14,71%

10,16%

14,85%

10,99%9,70%

0%

5%

10%

15%

20%

25%

30%

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Share

startup cohort

The largest growth effects are attributed to gazelle companies which meet the “gazelle”- criteria

directly after the companies were established

One in six jobs generated by startup companies is created by a gazelle company

As mentioned above, a large part of gazelle companies emerges directly after the companies were established. The following graph 4-3 depicts the development of early and later starters with respect to their average number of employees.11 It can be discerned that early emerging gazelle companies grow continuously in the investigated time period (from an average of 16 employees in the starting year to 43 at the end of the growth period). However, gazelle companies which start their growth period at a later stage, meaning after the first year post-startup, usually generate the defined increase in employment (72,8%)

within one year and stop growing after that. This holds true for all other gazelle companies and is depicted exemplary in graph 4-3 for companies starting their growth period 4,7,10 and 15 years after the companies were established.

Graph 4-3: Development of the number of the employees in early and late starters of gazelle companies

Source: Own Calculations Rambøll, Data Creditreform

Partly due to the definition (a minimum number of 10 employees), the number of employees at the beginning of the growth period is almost the same for all gazelle companies (15 employees). Remarkably though, graph 4-3 illustrates that late starting gazelle companies – at the end of the defined growth period- have created significantly fewer jobs than their early starting companions. Furthermore, early – and late

starters grow differently. Whereas late starters grow rather erratically, early starters grow relatively constant within the three year growth period. Also, early- and late starting gazelle companies differ regarding their

development after the growth period. While early starters continue to grow, late starting gazelle companies rather maintain their level of employment and seemingly consolidate. Having said this, 8 years after completing the three year growth period, early starting gazelle companies have increased employment by yet another 20%. Thus, companies which start growing at an early stage continue to grow even if at a decelerated pace. On the other hand, late starting gazelle companies do not achieve further growth. With

respect to job creation, this finding underscores the significance of companies which grow at an early stage.

The above already hints at the fact that gazelle companies are far from being a homogenous group in terms

of growth. Thus, the following looks at two different groups: the companies which grow over 100 employees

11 Technical remark: Because the values of the number of employees in the period under consideration are decreasing and during the late years dates

were not available, therefore the values were forecast. On this occasion, the growth rate of the employee's growth was determined for every year and in another step this was calculated averaged for every year.

0

10

20

30

40

50

60

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Em

plo

yees (

Media

n)

Year after foundation

gazelles 4 years after foundation gazelles 7 years after foundation gazelles 10 years after foundation gazelles 15 years after foundation

A quarter of gazelle companies starts growing with more than 50 employees and grows above 100

employees

in the investigation period and those that do not. In order to distinguish the first group from the latter it will hence be referred to as “super – gazelles”. One in four companies provides more than 100 jobs. Interestingly, this number does not change in the investigated time period. Consequently, the potential to create jobs remains stable, regardless of the decline of gazelle companies in absolute numbers after 2000. So even if external crises do influence the likelihood with which companies become gazelle companies, they seemingly do not affect the number of jobs gazelle companies create once this status is achieved. Hence, in

economically difficult times fewer companies generate fast growth. The growth which is generated, however, is not influenced by this factor. In this context it is interesting to find out whether the two groups (super- gazelles and gazelle companies) already differ when establishing the company with regards to the number of employees. Do the companies over 100 employees start out with the same number of employees as smaller companies? Graph 4-4

compares the median of people employed in the base year, after the 3 year growth period and at the point with the highest number of employees for all gazelle companies and “super- gazelles”. Graph 4-4: Comparison of number of employees and super-gazelles at different stages

Source: Own Calculations Rambøll, Data Creditreform

Super-gazelles start out with substantially more employees than other gazelle companies. Before the defined growth period they employ 50 people; after this period they employ 150 people. Gazelle companies, on the other hand, start out with 14 employees and have 34 employees after the growth period. Consequently, the number of employees in super -gazelles is not only higher than in the control group but also the rate of increase is superior. Despite higher absolute numbers of employees in the base year, super gazelles were

able to increase the number of employees by 200% in the 3 year growth period. The control group was able to increase the number of employees by 143%. Hence, the rather small share of “super- gazelles” contributes disproportionally high to the employment effect deployed by gazelle companies. This even holds true for when the three year growth period is completed. Super-gazelles realized further growth of 33%, whereas gazelle companies only reached 18%. Thus it can be concluded that the starting point of a company determines the further growth path. Companies which start with a high number of employees hence generate stronger growth than those which start out with fewer employees. If one only considers the companies which

realized the defined gazelle criteria as early as possible (4 years after foundation of the company), this correlation is even stronger.

On a detailed industry level, the study shows the development of gazelle companies in relation to the startup cohorts from 1995 to 2006. It is examined how many gazelle companies emerged from different industries in relation to the overall number of newly established businesses in a respective industry. The overall number of

0

50

100

150

200

250

Num

ber

of em

plo

yees (

Media

n)

Super-Gazelle

Gazelle

Employees in base-year Employees after Max. employees growth period

Gazelle companies emerge more frequently in knowledge intensive branches

startups between 1995 and 2006 is 2.159.543.12 Measured against the number of gazelles (13.021) this yields a quota of 0,60%. Therefore, one in 165 companies founded between 1995 and 2006 became a fast growing young company according to the definition used in this study. Compared to the overall number of startups in an industry the share of gazelle companies is particularly high in the branches “temporary employment agencies” (5,16%) and the social sector (4,67%). Among the 20 branches yielding the highest likelihood of gazelle companies are 14 branches concerned with the

manufacturing of products – inter alia the production of parts and accessories for trucks (4,51%), electronic components (4,47%), machine tools (4,37%), chemical raw materials (4,35%) and plastic products (4,25%). Also service sectors such as research and development in natural-, engineering and agricultural sciences and medicine (2,34%) can be found. In summary it can, therefore, be said that gazelle companies mainly come from branches in producing and processing sectors. The very opposite is true for those branches that measured against the total number of startups generate the smallest share of gazelle companies.17 of these

branches are service branches, with a majority evolving around the sectors retail trade and specialized trade: Inter alia real estate services (0,18%), travel agencies (0,33%), advertising (0,36%) and wholesaling on a fee (0,21%). All in all, measured against the total number of startups, the largest share of gazelle companies operates in manufacturing while the lowest share of gazelle companies operates in service sectors. Graph 4-5: 20 industries with the highest share in all gazelle companies and the highest gazelle-share (WZ-3-Level) measured by all start-up companies 1995-2006

Source: Own Calculations Rambøll, Data Creditreform

12 The number of the start-ups, which is taken as a comparative size in the database of the Creditreform deviates from the calculated start-ups by the

ZEW. Nevertheless, it is calculated at this point on the dates of the Creditreform, because these are available at an industry level and in addition the comparison to the gazelle companies at this level is conducted.

0% 1% 2% 3% 4% 5% 6%

Production of electronic components

Production of machine tools

Production of hardware, sheet metal and metal goods

Production of machines for other branches of industry

Detective agencies and protective services

Production of machines for generating and use of mechanical energy …

Research and development in the field of nature-, engineer-, …

Steel and light metal construction

Other food industry (without beverage industry)

Production of plasticware

Surface finishing, heat treatment and mechanics

Forwarding, other transport agencies

Cleaning of buildings, inventory and means of transportation

Software houses

Architecture and engeneering offices

Other surface transport

Social affairs

Placement and transfer of workers

Other services activities predominantly for companies

Structural and civil engineering

Gazelle-share in all gazellesGazelle-share in all companies

of the industry

A detailed consideration of the branches which generate a large share of gazelle companies measured against both the total number of gazelle companies and the number of startups in a respective branch is shown in graph 4-5. For they fulfill both criteria, these branches are assumed to have the greatest potential for young fast growing companies. Among these branches are mainly knowledge intensive services such as the provision of corporate services, architecture - and engineering firms, software companies and research and development in natural-, engineering and agricultural sciences and medicine. Also the branches

manufacturing of electronic components and machine tools can be found among the top 20 branches.In conclusion, the branch specific consideration of fast growing young companies shows that when compared to the size of the branches, gazelle companies are most likely generated in knowledge intensive branches.

The regional distribution of all identified gazelle companies in Germany reveals that, in line with the economic structure in Germany, most gazelle companies are located in North Rhine Westphalia (22%), Bavaria (15%) and Baden Württemberg (12%). Also, 4% of all gazelle companies in Germany are located in Berlin and 3%

Hamburg. In relation to the overall number of startups the share of gazelle companies varies from 0,35% to 1%. The largest share can be found in the state of Saarland followed by the East German states of Saxony, Thuringia and Saxony-Anhalt. Having said this, the share of gazelle companies is particularly high in regions in which both the overall number of companies and the entrepreneurial activity are low. In the following, 8 branches which entail the greatest potential to generate gazelle companies will be analyzed with regard to region specific aspects. This aims at identifying whether there are regional foci or

clusters where certain branches predominantly operate. Graph 4-6 depicts the regional distribution of 4 branches of the manufacturing sector and graph 4-7 shows the distribution of 4 branches in the service

sector. Graph 4-6 illustrates that there is a notable regional focus in terms of companies which operate in the branch of manufacturing machine tools in Baden-Württemberg and Bavaria. 54% of all companies are located in those two regions. Moreover, the city-states Berlin, Bremen and Hamburg have hardly any companies in the 4 examined branches. With regards to the manufacturing of electronic components there is a cluster in

Saxony and Thuringia (27% of all companies are located in these two states). Graph 4-6: Regional distribution of the four main industries of the manufacturing industry in gazelle companies

Source: Own Calculations, Data Creditreform

0%

5%

10%

15%

20%

25%

30%

35%

40%

Production of machines for specific branches Production of machine tools

Manufacturing of electronic components Manufacturing of other iron- metal sheet and metal

Gazelle companies emerge depending on their branch in regional clusters

The picture changes when looking at the service sector (see graph 4-7). In the branches corporate services, architecture - and engineering firms, software companies and research and development in natural-, engineering and agricultural sciences and medicine a regional cluster can be found in North Rhine Westphalia, Bavaria and Baden Württemberg. The city states show a focus in the service sector, too. Berlin, for instance clusters companies in the field of research and development in natural-, engineering and agricultural sciences and medicine (10% of all companies). Also, the rather small state of Saxony has a

relatively large share of knowledge intensive services. Graph 4-7: Regional distribution of the four main industries of the service industry in gazelle companies

Source: Own Calculations, Data Creditreform

4.3 Results of the survey of gazelle companies and case studies From the total number of 13.021 identified gazelle companies a randomized sample was taken, in order to conduct a telephone survey. 3.602 companies were asked to participate in the survey. In between

10.10.2011 and 28.10.2011 211 surveys were completed successfully. The return rate thus was at 5,86%. A unit- non response analysis revealed no significant differences between non respondents and participants, the exception being the company size. Having said this, the interpretation of the results is to be seen in the context of an overrepresentation of small companies. Moreover, in- depth interviews / case studies were conducted with 8 selected companies.

The main purpose of the case studies and the telephone survey was to find detailed information on gazelle companies, and the identification of decisive growth-obstacles and drivers in particular. Also, the hypotheses suggested by the literature were put to a test. The primary aim of the case studies was to conduct a detailed, in depth and exemplary consideration of these companies which allows tracing their growth strategies. The results of both empirical investigations will be presented jointly.

The literature analysis showed that the degree of formal education and branch specific experience – a company´s human capital- have an effect on growth.13 The result on the age of the surveyed founders shows

that almost half of the people were between 30-39 years old when founding the company. Another 28% even

13 See: KfW, ZEW (2010): Aufbruch nach dem Sturm. Junge Unternehmen zwischen Investitionsschwäche und Innovationsstrategie. KfW ZEW

Gründungspanel 2010.

0%

5%

10%

15%

20%

25%

30%

Software houses Archtiecture - and engineering offices

R&D in natural- engineering-agricultural sciences and medicine Provision of other (business-) services

Founders of gazelle companies have many years of professional- and branch specific experience.

Besides, one in three founders has previously founded a business

were between 40-49 years old. The age groups 20-29 years and 50-59 years are equally big and amount to 12% each. Approximately half of the businesses were set up in a team, the average team size being 3 people. With regards to prior experience in setting up a business almost one in three surveyed founders (29%) indicates that he/she had set up a business before. Among the surveyed CEOs 41% had worked in leading

management positions before. In terms of educational background, 54% of founders indicate to have a completed an apprenticeship – equally distributed among technical- and commerce related apprenticeships. Another 38% possess an academic degree either in the field of Economics and Social Sciences (67%) or in natural sciences and technology (24%). One in ten founders, CEOs respectively, has a doctorate. The majority (more than 60%) of both founders and CEOs had more than 10 years of professional experience. When setting up the business or starting work in the company almost half of the founders and CEOs already

had more than 10 years of experience in the respective industry. All companies investigated in the case studies were founded by a team. Much like the surveyed entrepreneurs the majority had extensive professional and industry specific experience. Moreover, 3 founders of companies investigated in the case studies state to have set up a business before. Thus, when setting up their business they already had experience in starting a business as well as managerial skills. Among the founders six come from a family of entrepreneurs. When asked about their initial motives the majority stated that they had always wanted to start a business and that they had already acquired experience in leading a

business.

When asked about their motives to grow all entrepreneurs said that growth had been strategically planned or

had been inherent in the business model. The market is also assumed to be a key driver of the largely continuous growth of the case study companies. So in other words the market in which the companies operate forces them to either grow or vanish. Thus, from the entrepreneurs´ perspective, a strategy which is not aimed a growth causes the company to fail. Also, entrepreneurs state that the market demands a certain company size which is necessary in order to operate successfully. This suggests that for gazelle companies

growth can be viewed as a constituent feature. Consequently, the motives to grow are a combination of the founders’ intrinsic motivation and external market circumstances.

76% of all gazelle companies have produced an innovation. According to “The Mannheim Innovation Panel”

43% of all SME in Germany consider themselves innovators14. This suggests that the innovation activity of gazelle companies is far above- average. Among the surveyed companies 80% have created a product- or service innovation and 37% have created an innovative method or process. While 41% state to have created an incremental innovation which has led to a slight improvement of the product/service, 59% of all surveyed

companies consider their innovation a radical improvement of a product/service. Empirical studies which exclusively focus on fast growing companies find a correlation between innovation and growth.15 The present study investigates this hypothesis by dividing the surveyed gazelle companies into two groups (1) companies which grow above- average and companies which grow below average. This categorization is based on a growth coefficient which was calculated for each of the surveyed companies. The

growth coefficient relates individual companies to all companies from their respective foundation cohort with regard to their growth. It shows that the group of companies growing above average more often indicates to

14 Aschhoff/Doherr/Köhler/Peters/Rammer/Schubert und Schwiebacher (MIP 2008), Innovationsverhalten der deutschen Wirtschaft – Indikatorenbericht

zur Innovationserhebung 2008, ZEW, infas, FhG ISI, Januar 2009. 15 See: Coad, A. und R. Rao (2008): Innovation and Firm Growth in High-Tech Sectors: A Quantile Regression Approach. Research Policy 37(4):633-648

/ Hölzl, W. (2009): Is the R&D behaviour of fast-growing SMEs different? Evidence from CIS III data for 16 countries. Small Business Economics 33(1):59-75 / Stam, E. und K. Wennberg (2009): The roles of R&D in new firm growth. Small Business Economics 33(1):77-89.

The gazelle companies strongest in growth are especially innovative

When starting their business, gazelle companies already incorporate growth in their strategy

have created an innovation (53%) than the group of companies growing below average (47%). Furthermore, it can be shown that companies which grow above average are more likely in to create radical innovations than companies which grow below average. In addition, the study shows that gazelle companies mostly operate in young, emerging and growing markets (77%). Especially technology oriented case study companies considered continuous innovation a key driver for growth. The ability to successfully create and position innovation can, however, not be dissociated from a

certain company size. Having said this, there is an interrelationship between the necessity to grow and the ability to successfully create and position innovation.

Current research finds integrating foreign markets and/or economic activity in foreign countries opens new growth perspectives to companies. Consequently, the present study also looks at the degree of internationalization of the surveyed companies. 31% of all companies indicate that they operate internationally. A study conducted in 2004 suggests that 24% of all SME in Germany show economic activity

beyond national borders16. Thus it can be derived that gazelle companies in Germany rather tend to operate internationally than other SME. The study also investigates at which stage companies started to operate internationally. It can be shown that a majority of internationally operating gazelle companies indicates that they started expanding their markets at a relatively early stage. On average the surveyed companies launch their exports 2,6 years after the company was set up. This suggests that the decision to operate internationally is, from a very early stage, a crucial element of the business model.

Approximately one in four surveyed companies started off with less than 20.000 Euro startup capital. 28% state that they had between 40.001 and 60.000 Euro startup capital. The largest group of companies (29%) had 100.000 Euro startup capital. The amount of startup capital varies significantly. While the median is at 25.000 Euro, the arithmetic mean is at 649.530 Euro. Thus, with regards to the financing strategy when setting up the business gazelle companies differ substantially. 73% of the startup capital come from own funds and 27% come from outside equity. 64% stated that they

used own savings and 10% used savings from friends and family. While 17% received public or institutional funding only 2% used venture capital. None of the surveyed companies used financing through Business Angels. These findings link up well with a study on the access to capital of SME, especially gazelle companies, conducted in 201117. Outside equity is primarily raised in the form of bank loans (58%) and start-up loans

(39%). Subordinated loans were used by 7% of all surveyed companies. Almost one in three companies did not take up any outside equity at all.

Besides looking at early stage financing it is interesting to investigate with which means gazelle companies finance their growth. 76% of all companies indicate that the ability of capital necessary to realize the planned growth steps was satisfactory. On the other hand 24% state that they were unable to realize the planned growth steps due to the insufficient availability of capital. Graph 4-8 depicts the relevance companies assign to different capital sources. In the further course of the companies retained earnings become a relevant financial instrument. 42% of the surveyed companies consider retained earnings very important and another

34% consider them important. Thus, when financing growth retained earnings are considered the most important source of capital.

16 EU- Kommission (2003/4): Internationalisierung von KMU 17 See: Söller, Rene (2011): Der Zugang kleiner und mittlerer Unternehmen zu Finanzmitteln, Destatis.

www.destatis.de/jetspeed/portal/cms/Sites/destatis/Internet/DE/Content/Publikationen/Querschnittsveroeffentlichungen/WirtschaftStatistik/UnternehmenGewerbeanzeigen/MittlereUnternehmenFinanzmittel,property=file.pdf.

The financing strategy of gazelle companies varies greatly

Gazelle companies operate internationally more often and at a very early stage

Graph 4-8: Evaluation of the relevance of financial sources for growth financing

Source: Own Calculations, Rambøll

Much like in early stage financing, the relevance of own saving/friends/family continues to be high. As far as outside equity is concerned, more than half of the companies surveyed assign “very high” (24%) or “high” relevance to bank loans. Surprisingly though 26% of the surveyed companies consider traditional bank laons

not relevant at all when financing growth. While 35% view public funding as important, 42% consider public

funding not important at all. One in four surveyed companies is of the opinion that Venture capital is very important/important. More than half of the surveyed companies, however, regard Venture Capital as not impornat at all.

The present study also aims at identifying growth drivers and growth obstacles of gazelle companies in Germany. Therefore, the surveyed companies were asked to list the most important drivers and obstacles for growth by means of an open question in the questionnaire. The literature distinguishes between internal and external growth determinants.

According to the surveyed companies the focus on quality, clients and distribution is by far most important growth driver. Within this context marketing plays a crucial role. The interviews conducted in the framework of case studies echo these results. The quality of the product/service and a focus on distribution were thus identified as the main growth drivers. In addition, the surveyed companies attribute growth to an appropriate market dynamic (a growing market). Essentially, the combination of a young dynamic market and a strong

focus on clients, a qualitatively high product and/or service are key drivers for a successful company and growth respectively. The surveyed companies largely locate external growth drivers on the market. According to one entrepreneur “the market and ultimately the client are the decisive growth drivers”. In this regard it is interesting that all case study companies were exclusively founded in growing or even new markets. Besides the market, actions taken by the government also have a positive effect on growth. This is especially true for legal regulations and public funding.

The surveyed companies consider the creation of innovations and employees further growth drivers. The

importance of employees is also emphasized in all conducted case study interviews. Entrepreneurs consider their employees the most significant resource, also with regard to growth. Interestingly, the analysis shows that entrepreneurs attribute very little stimulation for growth to external circumstance; generally growth drivers are assumed to be of internal nature. Having said this, company

42%

44%

24%

14%

10%

34%

16%

33%

21%

15%

11%

11%

11%

14%

8%

2%

7%

7%

9%

14%

11%

22%

26%

42%

52%

0% 20% 40% 60% 80% 100%

Retained earningsGewinne (N=202)

Own savings/friends / family

(N=206)

Bank loans (N=203)

Public funding programs(N=203)

Venture Capital (N=202)

Focussing on quality, clients and distribution is a crucial driver for growth

growth is largely triggered by the company itself – respectively management and employees. The above suggests that there is limited room for support options regarding growth drivers from external sources.

Unlike growth drivers, growth obstacles are largely seen outside the company. The most frequently indicated growth obstacle is skills shortage. According to the case study interviews SME and startups face skills shortage due to a lack of “branding”, whose inhibitory effects are twofold. One the

one hand employees would rather not work for unknown, small or recently launched businesses. This is particularly true for highly skilled personnel, who often prefer working in a big corporation since the

likelihood of job loss is assumed to be lower. Also, big corporations are mostly able to pay better. One the other hand employees highly value a company´s reputation. Furthermore, the unwillingness to work in startups is traced back to the generally negative picture of entrepreneurs in Germany. Nonetheless this phenomenon is also discussed from a positive perspective. Employees who choose to work in startups often do so consciously for they appreciate the flat hierarchies, flexibility, dynamic and high responsibility offered in

startups. Having said this, a positive selection of employees takes place which tends to result in the hiring of particularly highly motivated personnel. However, a certain company size is considered crucial in order to perform successfully on the market. This applies to both B2B and B2C businesses. According to the surveyed entrepreneurs startup companies have a hard time establishing trust on the market. The lack of branding thus not only inhibits the acquisition of qualified personnel but also impedes the customers´ trust on the market. Both facts have a negative effect on growth. On the other hand both aspects also encourage companies to realize fast growth.

Internal growth obstacles occur if employees cannot be motivated sufficiently. In general though, employee

motivation in startups is very high, which is mainly due to flat hierarchies, good opportunities for promotion and a high level of responsibility. According to the surveyed entrepreneurs, problems in motivating employees may occur once the company is established and the dynamic slows down and structures solidify. However, through trainings companies counter this trend. Since fast growth leads to continuously changing

company structures and often causes restructuring measures, there are always times in which the company structures are not optimal. The surveyed entrepreneurs refer to these times as “critical moments” which always bear risks for the company. A lack in structure, therefore, is also regarded a growth obstacle. However, it is argued that such “critical moments” are part of the business and is, therefore, considered a challenge rather than a problem. “Skills shortage impedes growth.” The majority of case study companies confirm this statement. Skills

shortage has a various reasons, one of which is the lack of branding which is pivotal in the acquisition of skilled personnel. Startups are often in need of excellent staff they are, however, unable to measure up to

the salaries big corporations offer. Moreover, one entrepreneur reports that some customers are reluctant to work with foreign employees. Nonetheless, the surveyed entrepreneurs criticize the limited access for foreign employees to the German job market. One entrepreneur in the interview states: “The opening of the job markets, also in the EU, occurred too late.

The best brains are already somewhere else.” The call for a reduction of formal requirements when wanting to enter the German job market, therefore, not only applies to EU citizens but also to highly qualified, experienced employees from outside the EU. The surveyed entrepreneurs further state that more incentives for those employees should be created since Germany has a language related disadvantage vis–á-vis Anglo-Saxon countries. Moreover, it was mentioned

that especially fast growing companies are targeted by international job-hoppers. In this context the current German social system ought to be called into question. While all of the entrepreneurs of the case study companies indicate that securing skilled personnel is a major challenge none of the companies actually

suffers from an acute lack of qualified employees. The challenge was tackled as a strategic matter from an early stage on coped with through intensive recruiting: ways to recruit qualified personnel range from directly approaching universities and universities of applied science to making use of headhunters and the

Skills shortage is the main growth obstacle for gazelle companies

implementation of dual study programs in which part of the degree is completed in a company. Also, employees are awarded bonuses if they successfully recruit personnel. In this context the importance of motivating and keeping employees was stressed. As far as the education system in Germany in concerned entrepreneurs encourage policy makers to increase the quality as well as social mobility. More precisely it is suggested that academic fields in which Germany currently succeeds such as mathematics, engineering and natural sciences should be further strengthened. Among the surveyed entrepreneurs skills shortage is

generally viewed as a future issue which needs to be tackled strategically today.

Besides the above, the financial and economic crisis is considered a growth obstacle. This is in line with the empirical evidence which suggests that the dropping number of fast growing companies was mainly caused by external crises. All case study companies express that external crises have impeded company growth. However, the extent to which a deteriorating economy negatively affects business varies greatly due to branch specific characterizations. While those who consider the branch in which they operate largely crisis

resistant have not really suffered any losses, others claim the crisis caused “a massive slump in orders” which substantially slowed down growth with respect to both employees and revenue. This is particularly felt by technology-oriented businesses with high funding needs, because in economically difficult times both the demand for new technology and the general financing situation deteriorate. Consequently, these businesses had to reduce the employment level shortly after a crisis. However, they were able to recover quickly. In this context the introduction of the exceptional regulation on “short-time work” in 200918 was mentioned positively. It allowed companies to hold on to employees and thus assured immediate reaction once the

economy started improving again instead of having to hire new personnel.

Among those who were surveyed by phone a lack in financing possibilities was perceived a key growth obstacle. In this context the lack of financing opportunities through banks and the difficult access to loans were criticized. The case study companies echo this result by stating that the acquisition of financing in the startup phase as well as to realize growth is a key challenge. Especially, the rigid loan conditions applied by banks are regarded as a growth obstacle.

“The lack of startups is primarily due to the fact that the risk aversion of banks has increased over the past years. If you´re lucky enough to get a loan, then only if you pay extremely high interest rates.”

The surveyed entrepreneurs largely agree upon “the unwillingness of conventional banks to provide loans.” With respect to the relevance of Venture capital on the other hand there is a wide range of different views. Especially at an early stage some entrepreneurs are critical towards VC because they fear “loss of control”.

Others think the bad reputation of the VC market is not justified. Among the surveyed companies some used VC for both startup and growth financing. These companies mainly operate in software, IT and technology branches. This suggests that the acceptance and use of VC highly depends on the branch. Those that did use VC consistently said that their business model was thus inherently growth oriented. Despite the fact that the majority consider financing a major concern in the process of setting up a business and realizing growth, only very few actually have had too little capital. Nonetheless, it is assumed that given a better financing situation

even further growth could have been achieved. In general the above suggests that the financing situation is in fact a major challenge for startups and may impede growth.

18 See: http://statistik.arbeitsagentur.de/Statischer-Content/Arbeitsmarktberichte/Berichte-Broschueren/Arbeitsmarkt/Generische-

Publikationen/Arbeitsmarkt-Deutschland-Kurzarbeit-Aktuelle-Entwicklungen.pdf, P. 6.

A clear legal framework is the basis for growth

Startup financing is the biggest challenge

Economic- and financial crises mostly impede growth of innovative technology businesses

Current legislation and bureaucracy were also identified as an obstacle for fast growth. In this context it is mainly the planning uncertainty caused by the government which impedes growth. Besides, opening the German job market for foreign employees, other legal conditions are considered as growth obstacles, too. It is stressed that “many regulatory decisions are motivated politically”, rather than focused on the necessities of business. Also, many legal decisions must be clarified by the Federal Constitutional Court. This causes a legal uncertainty which can last for years and has clearly a negative effect on businesses. Having said this,

the surveyed entrepreneurs jointly call for clear legal conditions. The securing of the competitive environment by breaking up cartels and forcing monopolies to open, the market for competition is considered one of the main tasks of the legislation. In this field, entrepreneurs desire intensified efforts. Furthermore the tax legislation for retained profits is criticized, because of its large contributions towards liquidity shortage and thus to one of the main problems for companies. “This should be

managed by taxation, as for example in the Netherlands or Switzerland, which has to be paid only, if capital is deducted from the company or in general its capital stock is reduced”. A general demand to reduce administrative costs is often mentioned and is directed towards the organization of public funding programs.

“Considering the huge funding scene in Germany, the effort to examine and combine all existing programs in order to obtain the desired funding is too high”.

Costly application procedures are evaluated negatively as administrative barriers Particularly, the huge number of funding possibilities has a negative impact, because focusing on the optimal funding strategy is a very time-consuming procedure. In addition, the obligation to disclose all relevant information and schemes deters a o lot of persons to make use of a funding. Although the opinion was expressed to abandon all funding programs, the majority of the sample evaluates funding programs as a driver for their growth. . This is especially true for business concepts that entail a high risk factor.

Particularly companies which develop basic technologies attach high importance to the funding through subsidies. According to the respondents within the overall financing framework the funding has a significant influence on growth of the company. Nevertheless, the opinion was expressed that public funding programs were neither efficient nor effective. But it is feared, that public funding may offer incentives apart from the logic of the market and companies survive artificially.

Some respondents even demanded general restructuring. The restructuring is discussed at two levels. Besides, the already mentioned changes within the modalities, it is mainly a question for whom and in which industries funding programs make sense. Young founders, who have neither capital nor other securities, are in particular considered to be suitable recipients of funding programs. This coincides with the image that above all, funding should support the foundation of companies, while other growth steps should be financed by the market. Another proposal is to promote funding of clusters and concentrate on specific industries. Therefore, the expressed criticism of funding by public authorities contains criticism of the formalities and the

arrangement of contents. Taken all together, it can be said, that pro and contra of public funding is discussed extremely controversially by the respondents.

Another aspect mentioned several times by the entrepreneurs was the negative image of entrepreneurs in Germany. From their point of view the entrepreneur´s negative public image and the general risk aversion in Germany are jointly responsible for a decreasing number of gazelle companies. Through initiatives at schools and universities –and therefore, a stronger presence of entrepreneurship in educational institutions, it is

possible to improve the ailing image of an entrepreneur in a lasting way. As a consequence, more young graduates could be attracted to the idea of self-employment and realize it.

A positive image of entrepreneurs strengthens foundation activity and growth