student loans: is it time for employers to step in? loans.pdf · student loans: is it time for...

TRANSCRIPT

Student Loans: Is it Time for Employers to Step In?

1

Michael Doshier,

Global Head of

Retirement Marketing,

Franklin Templeton

Investments

Rachel Collins,

Counsel,

Congressman Rodney

Davis

Cindy Silva,

Head of Financial

Wellness Strategy,

Fidelity Investments

Kate Winget,

Chief Sales Officer,

Gradifi

Craig Copeland, Senior Research Associate, EBRI

#ebriPF83 #CollegeDebt

Trends in Student Loan Debt, 1992-2016

Craig Copeland, EBRI

EBRI Policy Forum

May 10, 2018

2

© Employee Benefit Research Institute 2018

Overview

• Student Loan Debt

• Incidence

• Amounts

• Payments

• Specific Assets and Student Loan Debt

• Data Source—Survey of Consumer Finances• Federal Reserve’s triennial survey on family wealth

• Most comprehensive government survey on American families’ total

wealth

• Contains all types of wealth including detailed data on all asset and

debt types

3

© Employee Benefit Research Institute 2018

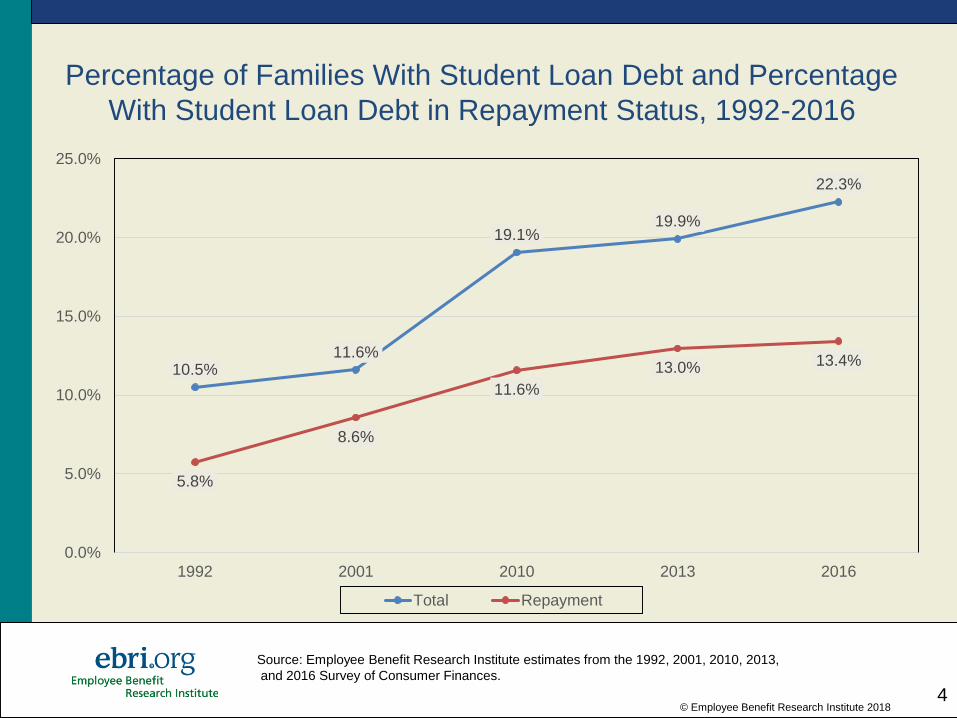

Percentage of Families With Student Loan Debt and Percentage

With Student Loan Debt in Repayment Status, 1992-2016

10.5%11.6%

19.1%19.9%

22.3%

5.8%

8.6%

11.6%

13.0% 13.4%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

1992 2001 2010 2013 2016

Total Repayment

4

Source: Employee Benefit Research Institute estimates from the 1992, 2001, 2010, 2013,

and 2016 Survey of Consumer Finances.

© Employee Benefit Research Institute 2018

Percentage of Families With Student Loan Debt,

by Age of Family Head, 1992-2016

24.4%26.0%

40.0%41.4%

44.8%

11.7% 11.9%

26.2%

28.7%

34.3%

5.7%

10.7%

17.5%18.4%

23.7%

2.9%

5.2%

9.3%

12.0%12.9%

1.2%0.4%

2.7% 2.1% 2.4%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

1992 2001 2010 2013 2016

<35 35-44 45-54 55-64 65 or Older

5

Source: Employee Benefit Research Institute estimates from the 1992, 2001, 2010, 2013,

and 2016 Survey of Consumer Finances.

© Employee Benefit Research Institute 2018

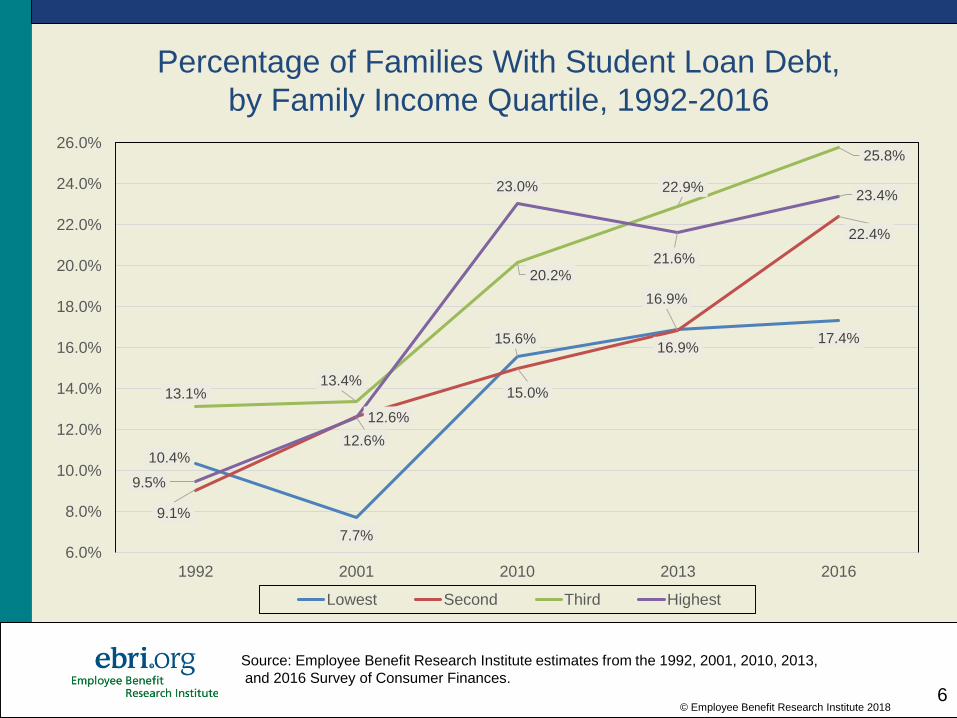

Percentage of Families With Student Loan Debt,

by Family Income Quartile, 1992-2016

10.4%

7.7%

15.6%16.9%

17.4%

9.1%

12.6%

15.0%

16.9%

22.4%

13.1%13.4%

20.2%

22.9%

25.8%

9.5%

12.6%

23.0%

21.6%

23.4%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

22.0%

24.0%

26.0%

1992 2001 2010 2013 2016

Lowest Second Third Highest

6

Source: Employee Benefit Research Institute estimates from the 1992, 2001, 2010, 2013,

and 2016 Survey of Consumer Finances.

Student Loan Debt Amounts

7

© Employee Benefit Research Institute 2018

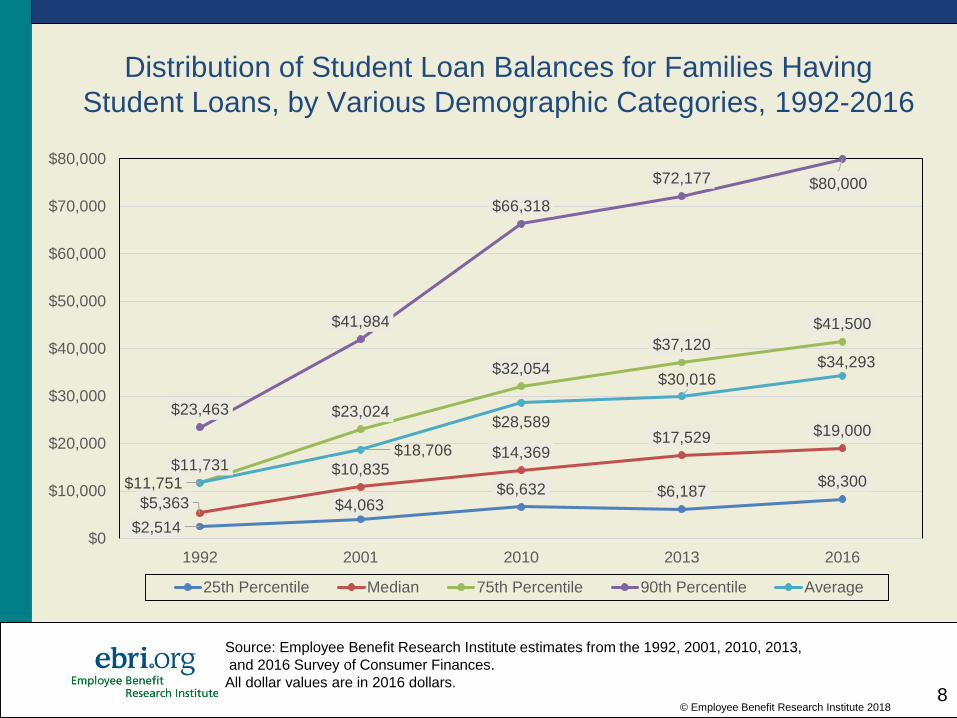

Distribution of Student Loan Balances for Families Having

Student Loans, by Various Demographic Categories, 1992-2016

$2,514

$4,063$6,632 $6,187

$8,300

$5,363

$10,835$14,369

$17,529 $19,000

$11,731

$23,024

$32,054

$37,120

$41,500

$23,463

$41,984

$66,318

$72,177 $80,000

$11,751

$18,706

$28,589

$30,016$34,293

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

1992 2001 2010 2013 2016

25th Percentile Median 75th Percentile 90th Percentile Average

8

Source: Employee Benefit Research Institute estimates from the 1992, 2001, 2010, 2013,

and 2016 Survey of Consumer Finances.

All dollar values are in 2016 dollars.

Median Monthly Required

Student Loan Debt Payments

and Percentage of Income the

Debt Payments Represent

9

© Employee Benefit Research Institute 201310

$100

$200

$350

$630

$3041.6%

3.1%

5.9%

9.9%

5.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

$0

$100

$200

$300

$400

$500

$600

$700

25th Percentile Median 75th Percentile 90th Percentile Average

Distribution of Reported Required Family Monthly Student Loan Debt Payments and Distribution of the Percentage of Family

Income That the Debt Payments Represent, 2016

Monthly Debt Payment Percentage of Income

Source: Employee Benefit Research Institute estimates of the 2016 Survey of Consumer Finances.

© Employee Benefit Research Institute 201311

$200 $200 $200 $200

$100

4.0%

2.8% 2.9%

3.1%

1.6%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

$0

$50

$100

$150

$200

$250

<35 35-44 45-54 55-64 65 or Older

Required Median Monthly Student Loan Debt Payments and Percentage of Income That the Debt Payments Represented, by

Family Head Age, 2016

Median Monthly Payment Percentage of Family Income

Source: Employee Benefit Research Institute estimates of the 2016 Survey of Consumer Finances.

Specific Assets and Student Loan

Debt

• Home Ownership

• DC Plans

12

© Employee Benefit Research Institute 2018

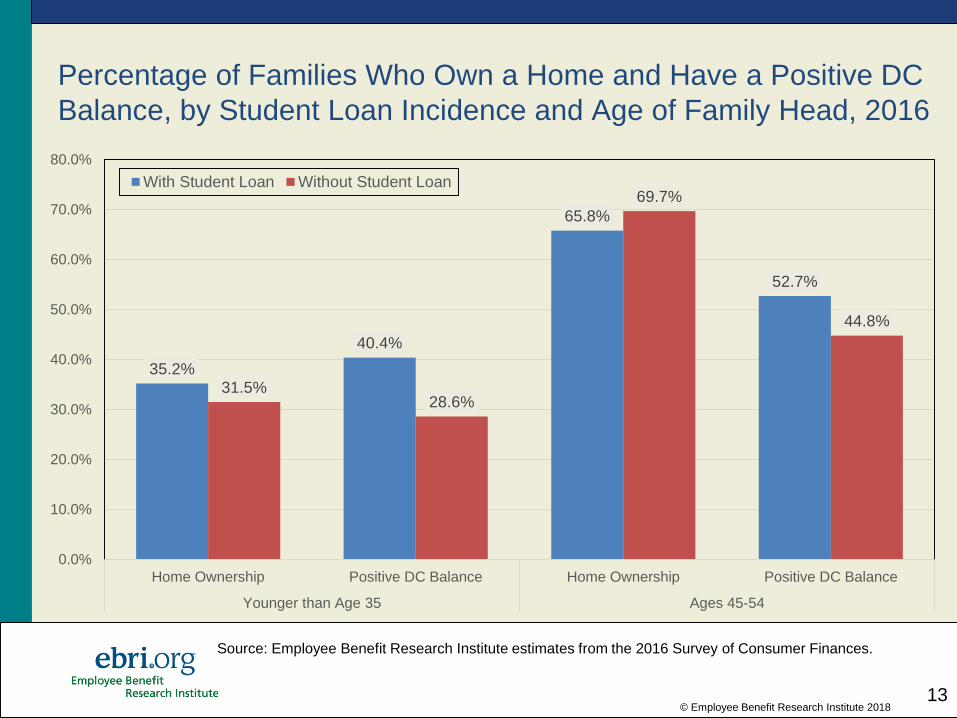

Percentage of Families Who Own a Home and Have a Positive DC

Balance, by Student Loan Incidence and Age of Family Head, 2016

13

35.2%

40.4%

65.8%

52.7%

31.5%28.6%

69.7%

44.8%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

Home Ownership Positive DC Balance Home Ownership Positive DC Balance

Younger than Age 35 Ages 45-54

With Student Loan Without Student Loan

Source: Employee Benefit Research Institute estimates from the 2016 Survey of Consumer Finances.

© Employee Benefit Research Institute 2018

Distribution of DC Plan Balances for Families With and Without

Student Loans, Families With Heads of Specific Ages, 2016

$2,400 $8,000$24,000

$62,000

$3,000 $11,000

$38,000

$90,000

$16,000

$46,000

$148,100

$410,000

$18,000

$80,000

$227,000

$500,000

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

$450,000

$500,000

25th Percentile Median 75th Percentile 90th Percentile

Younger than Age 35 with Student Loan Younger than Age 35 without Student Loan

Age 45-54 with Student Loan Age 45-54 without Student Loan

14

Source: Employee Benefit Research Institute estimates from the 2016 Survey of Consumer Finances.

© Employee Benefit Research Institute 201315

27.3%

24.9%26.5%

36.3%

0%

5%

10%

15%

20%

25%

30%

35%

40%

Home Ownership Positive Defined Contribution Balance

Percentage of Families With Heads Younger Than Age 35 and Having Some College That Own a Home and Have a Positive Defined Contribution

Balance, by Student Loan Incidence, 2016

With Student Loan No Student Loan

Source: Employee Benefit Research Institute estimates of the 2016 Survey of Consumer Finances.

© Employee Benefit Research Institute 201316

$1,600

$4,700

$15,300

$16,667

$3,000

$10,000

$23,200

$21,490

$0

$5,000

$10,000

$15,000

$20,000

$25,000

25th Percentile Median 75th Percentile Average

Distribution of Defined Contribution Balances for Families With Heads Ages Younger Than 35 and Some College, by Student Loan Incidence, 2016

With Student Loan No Student Loan

Source: Employee Benefit Research Institute estimates of the 2016 Survey of Consumer Finances.

© Employee Benefit Research Institute 2018

Takeaways

• The incidence of student loan debt has been growing

significantly (nearly doubling since 2001), particularly among

families with heads younger than age 35 and ages 35-44.

• The average student loan debt amount increased in real

amounts by 20% from 2010 to 2016, and the median

increased 32%.

• The required median debt payment was $200 in 2016, which

represented 3.1% of family income. However, these

payments reach 10 percent and above of family income for

those with the highest debt payments.

• DC balances are lower for those with student loan debt than

for those without it.

17

© Employee Benefit Research Institute 2018

1100 13th Street NW

Washington, D.C. 20005

202-659-0670

www.ebri.org www.choosetosave.org

18

© Employee Benefit Research Institute 201819

EBRI-ERF Policy Forum #83

Retirement, Health and Financial Wellbeing

Thursday, May 10, 2018

Wireless Network: DCCTR

Wireless Password: meeting2015DC

Tweet: #ebriPF83

EBRI Policy Forum

KATE W INGET

Debt directly impacts your employees and their performance

80% of working professionals with student debt consider their student

debt to be a source of significant or very significant stress.

1 2 - 2 0 H o u r sa month are uti l ized by

an estimated 80% of

employees who try to

deal with their f inancial

worries at work2

7 4 % of millennials that l ike

their job are sti l l

planning to leave in the

next three years

Four out of five employers report that their employee’s personal

financial issues impact their job performance resulting in:

Which translates to real costs for employers:

$30.5BMillennial turnover alone is estimated to

cost the U.S. economy $30.5 billion

90-200%Turnover costs up to 90 – 200% of an

employee’s annual salary

Corporate culture and benefits packages must be tailored to engage the needs of Millennials and give them reasons to stay

Attraction

Mid-level management

Master’s preferred

$200/month benefit

3 years

Diversity Women & Minorities

$100/month benefit Increase of $100/year

3 years

Competitive Talent Hire

High value employees with specialized training

One time hiring bonus of $7,200 after 1 year of employment

Retention Millennials $100/month benefit

6 years

Goal PlanTarget

Debt is not a one size fits all problem, and our solutions shouldn’t be either

Budget: $7.500/employee