structuring the global investment process · 2008-07-22 · in a traditional pension fund, all...

TRANSCRIPT

Copyright © 2009 Pearson Prentice Hall. All rights reserved.

Chapter 13

Structuring the Global Investment Process

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 2

Introduction

In this chapter we discuss:The functions and relationships among the major participants in the global investment industry.The components of a formal investment policy statement.The various steps of the global portfolio management process.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 3

Introduction

Compare and contrast the major choices –active/passive, top-down/bottom-up, global/specialized, currency, quantitative/subjective – available in structuring the global investment decision making process.Discuss the important issues – particularly scope, weights and currency allocation – in choosing a global benchmark for strategic asset allocation.Evaluate the implications of a portfolio performance analysis for a global investor.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 4

A Tour of the Global Investment Industry - Investors

Private Investors:Usually belong to two broad categories: private and institutional.Usually refers to an individual or small group of individuals.Can buy foreign shares, mutual funds or have their money managed by investment professionals.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 5

A Tour of the Global Investment Industry - Investors

Institutional Investors:Refers to an organization that invests on behalf of others, such as a mutual fund, pension fund, insurance companies or charitable organization.Endowments and foundations accumulate the contributions made to charitable and educational institutions.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 6

Participants in the Global Investment Industry

Investment managersRange from asset management departments of banks to independent asset management boutiques.

BrokersPlay an important role in terms of implementing security trades and in research of companies and markets.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 7

Participants in the Global Investment Industry

Consultants and AdvisersBetter known for their work with with pension funds, but they also work with private clients and other types of investors.

CustodiansInformation technology is an important component of custodial services.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 8

Investment Managers

Range from the asset management department of banks to independent asset management boutiques specializing in offering specific investment products.Some asset managers cater to retail clients as well as institutional clients, while others serve the needs of one client.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 9

Brokers

Sell-side analysts: work for brokerage firms and make recommendations to clients.Buy-side analysts: work for investment managers and institutional investors.All CFA® charter holders and CFA candidates must follow the CFA Institute®

Code of Ethics and Standards of Professional Conduct, wherever they work and invest.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 10

Consultants and Advisers

Play a major role in the asset management industry.Independent consulting firms have traditionally advised U.S. pension funds, while actuaries played a similar role in the U.K.Consultants also focus on services such as recommending asset allocation, selecting investment managers and monitoring performance, and giving tax and legal advice.Their most sensitive role is the process of selecting, hiring and firing external managers.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 11

Custodians

Securities owned by investors are deposited with a custodian, which often uses a global network of sub-custodians.With the high development costs of software, many banks have sold their custodial activities, and further consolidation is expected in the future, because economies of scale can be significant in this business.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 12

Institutional Investors - Pension Funds

There are two different systems:The system found in France, Italy and most of Continental Europe, where active workers pay for the pensions of retired workers (“pay as you go” or PYG).The Anglo-American system, where workers and their employers contribute to a pension fund, which capitalizes all contributions and pays them back at the time of retirement. In this case, pension funds are considered to be long-term investors.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 13

Pension Funds

The investment approach of pension funds is greatly affected by the way future benefits are planned.There are basically two plan types and a combination thereof…(following slide)

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 14

Pension Funds — Types

A defined benefit pension plan (DB) which promises to pay beneficiaries a defined income after retirement. The benefit depends on factors such as the workers’salary and years of service.A defined contribution plan (DC) where the amount of contributions paid is set, usually as a percentage of wages, but future benefits are not fixed.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 15

Pension Funds — Types

In a traditional pension fund, all contributions are pooled and the total money is managed collectively. A board sets the investment policy of the fund.A recent trend is to give more investment decision power to each employee.(E.g., 401(k) plans in the U.S.)

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 16

Institutional Investors: Endowments and Foundations

Concerned about total return in the long run.Capital gains and income on the assets can be used to meet budgetary needs.Tend to have great investment freedom, because they operate under few regulatory constraints.Often the most aggressive institutional investors, with many having extensive global and alternative investments.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 17

Institutional Investors: Insurance Companies

Collect premiums on life insurance and on property and casualty insurance, which are invested until claims are paid.Heavily regulated in each country and state in which they operate.Tend to adopt conservative investment policies.Tend to focus on fixed income assets, in order to assure their claim-paying ability.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 18

Global Investment Philosophies

An investment management organization must make certain major choices in structuring its global decision process, based on:

Its view of the world regarding security price behaviorIts strengths, in terms of research and managementCost aspectsIts location and prospective domestic/global marketing strategy

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 19

Global Investment Philosophies

The Passive ApproachThe Active ApproachBalanced and SpecializedIndustry or Country ApproachTop-Down or Bottom-UpStyle ManagementCurrencyQuantitative or Subjective

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 20

Global Investment Philosophies: Passive Approach

This approach simply attempts to reproduce a market index of securities (index fund approach).It is an extension of modern portfolio theory, which claims that the market portfolio should be efficient.The trend toward global indexing is strongly felt among institutional investors.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 21

Global Investment Philosophies: Passive Approach

Various indexing methods can be used:Full replicationStratified samplingOptimization samplingSynthetic replication

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 22

Global Investment Philosophies: Active Approach

A benchmark is often imposed in the mandate set by the client, and it will clearly guide the structure of the portfolio.Active decisions show up at various levels:

Regional/country allocationSector/industry selectionStyle selectionSecurity selectionMarket timingCurrency hedging

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 23

Global Investment Philosophies: Active Approach

A new dimension:Sector selection/credit selectionDuration/yield curve managementYield enhancement techniques

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 24

Global Investment Philosophies: Balanced or Specialized

A balanced asset manager decides on all aspects of the global portfolio, from asset allocation to security selection and currency management.A specialized asset manager focuses on a particular investment area, such as Japanese equity or European value stocks or currency overlay. The asset allocation decision remains with the client (possibly helped by advisers), who uses many specialized managers for the various asset classes.Industry or Country approach

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 25

Global Investment Philosophies: Top-Down or Bottom-Up

Top-down approachThe manager first allocates his assets across asset classes and then selects individual securities to satisfy that allocation.The most important decision in this approach is the choice of markets and currencies.

Bottom-up approachThe manager studies the fundamentals of many individual stocks, from which she selects the best securities (regardless of their national origin or currency denomination) to build a portfolio.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 26

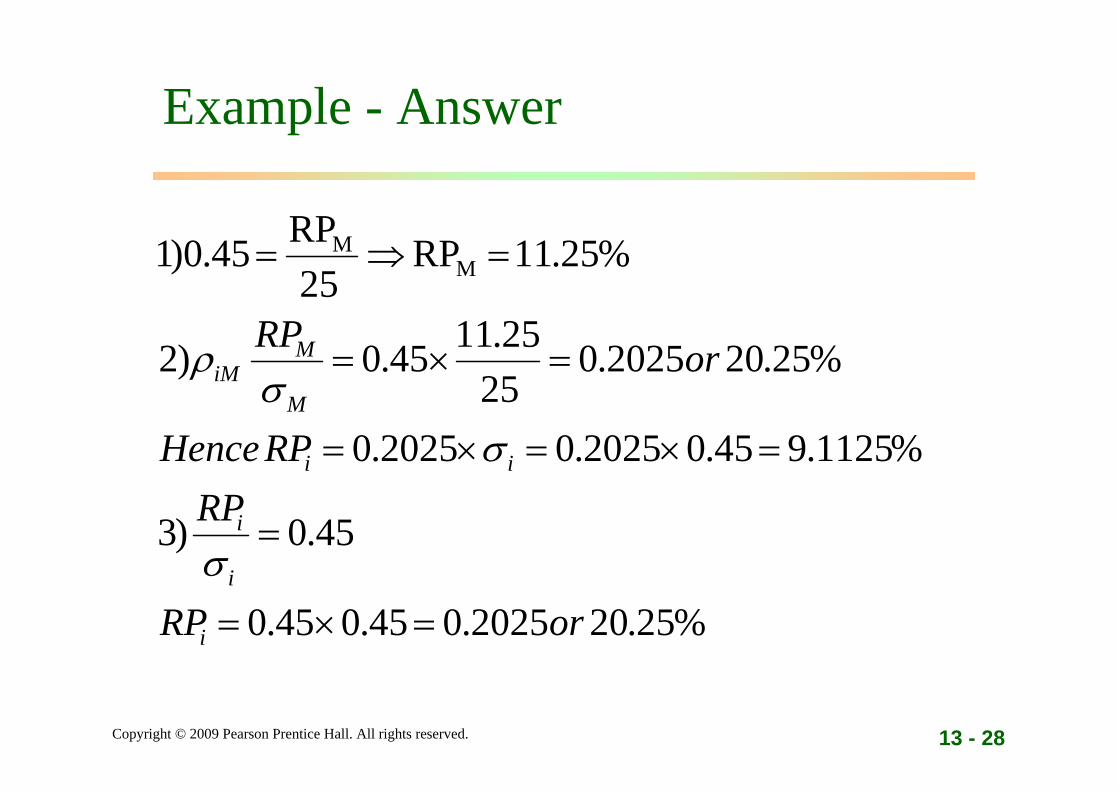

Example - Risk Premium

Suppose all investors in the world have similar risk aversion and require a Sharpe ratio of 0.45 on their diversified portfolios. The world market portfolio has a volatility of 25 percent. The emerging market asset has a volatility of 45 percent and a correlation of 0.45 with the world market portfolio. The beta of the emerging market asset class is 0.81

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 27

Example - Risk Premium

1) What is the equilibrium for the market portfolio?

2) Assuming full integration, what is the equilibrium risk premium for the emerging market?

3) Assuming full segmentation, what is the equilibrium risk premium for the emerging market?

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 28

Example - Answer

%25.202025.045.045.0

45.0)3

%1125.945.02025.02025.0

%25.202025.025

25.1145.0)2

%25.11RP 25

RP45.0)1 MM

orRP

RPRPHence

orRP

i

i

i

ii

M

MiM

=×=

=

=×=×=

=×=

=⇒=

σ

σσ

ρ

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 29

Style Management

Common style decisions:Value versus growth stocksSmall versus large firms

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 30

Currency

Some managers treat currencies only as residual variables.Others fully hedge or decide on a permanent hedge ratioCurrency overlay managers actively manage the currency exposure of a portfolio and often resort to currency options and forward or futures contracts for selective hedging or speculation.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 31

The Investment Policy Statement

The investment policy statement (IPS) is the cornerstone of the portfolio management process.Prepared by the adviser and the client.A well constructed policy statement typically includes a summary of the various elements:

Client description and purpose.Return and risk objectivesConstraintsAsset allocation considerations.Schedule for review and monitoring.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 32

Constraints

Fall into one of five categories:1) Liquidity requirements2) Time horizon3) Tax concerns4) Legal and regulatory factors5) Unique circumstances constrain asset

allocation.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 33

Schedule for Review and Monitoring

Performance evaluation is a critical stepPerformance measurementPerformance appraisal

Performance attribution allows us to understand the sources of performance.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 34

Capital Market Expectations

Expectations about future distributions of returns to asset classes.The formulation process is usually decomposed into three steps:

Defining asset classes.Formulating long-term expectations used in strategic asset allocation.Formulating shorter-term expectations used in tactical asset allocation.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 35

Defining Asset Classes

The segmentation of asset classes is usually based on various criteria:

Asset type (e.g., debt, equity real estate)Geography (domestic vs. international, or regional)Sector (e.g., technology stocks, high yield bonds, energy stocks)Style (e.g., growth vs. value stocks)

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 36

Long-Term Capital Market Expectations: Historical Returns

Long-term typically refers to five to ten years or more.Two basic approaches are used to formulate long-term expectations:

historical returns forward-looking returns.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 37

Long-Term Capital Market Expectations: Forward-Looking Returns

The approach can be summarized in three steps:

1) Calculate an updated covariance matrix (volatility and correlation of asset classes).

2) Infer expected returns for each asset class, using the CAPM.

3) Adjust expected returns for possible market segmentation and liquidity.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 38

Short-Term Capital Market Expectations: Historical Returns

Short-term typically refers to a year or less than a year.Short-term capital market expectations will suggest (temporary) tactical deviations from the strategic asset allocation.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 39

Strategic Asset Allocation (SAA)

SAA is derived by conducting an asset allocation optimization using long-term capital market expectations.The choice of the proper global benchmark is important.Three important issues are:

Scope of the benchmarkSet of weights chosenAttitude toward currency risk.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 40

Strategic Asset Allocation (SAA)

Individual clients – use investment policy statement.Institutional clients – use investable benchmark.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 41

Tactical Asset Allocation (TAA)

Also called dynamic allocation.Some managers use a disciplined risk-return optimization process. TAA is the process of deciding:

1) which asset classes are currently attractively or unattractively priced

2) making short-term departures from the long-term policy by buying more of the attractive markets and reducing the holding of unattractive markets.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 42

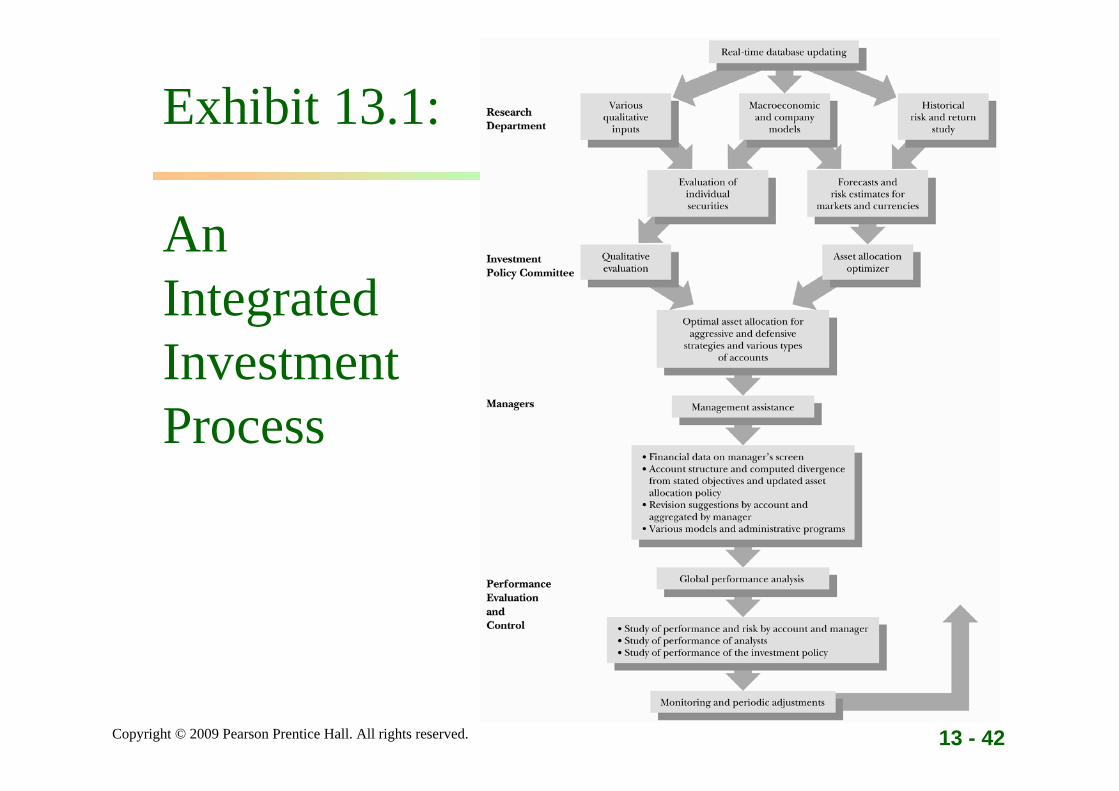

Exhibit 13.1:

An Integrated Investment Process

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 43

Limitations of Mean-Variance Optimization

Mean-variance optimization assumes that return distributions are normal.Rather than minimizing variance, another approach is to set a specific loss level (shortfall) and to build a portfolio that minimizes the probability of losing more than this set value.This is often known as minimizing shortfall or downside risk.

Copyright © 2009 Pearson Prentice Hall. All rights reserved. 13 - 44

Performance and Risk Control

Performance control should be driven by an organization’s daily accounting system.The following questions should be examined:

What is the total return on the fund over a specific period?What is the breakdown of the return in terms of capital gains, currency fluctuations and income?To what extent is the performance explained by asset allocation,market timing, currency selection or individual security selection?How does the overall return compare with that of certain benchmarks?Is there evidence of particular expertise in various asset classes and markets?Has the risk diversification objective been achieved?How aggressive is the manager’s strategy? How does this compare wit the goals of the client?