streamlined investor accting · mix of hedge funds, private equity funds and mutual funds. the...

TRANSCRIPT

Streamlined Investor Accounting And Servicing

Authors:Contact: Stephen Mackin Global Product Manager

+1 732 356 1200 x1212 | [email protected]

David A.A. Ross Global Head of Marketing

+1 732 318 7109 | [email protected]

USA: NJ +1 732 356 1200 | NY +1 646 861 3409 EMEA: +44 20 7016 9171 EMAIL: [email protected]

www.viteos.com

TECHNOLOGY SOLUTIONS

1 Streamlined Investor Accounting and Servicing

Contents

Streamlined Investor Accounting and Servicing .............................................. 1

Introduction ................................................................................................ 2

Wealth Management: A New Channel For Alternatives ................................... 2

Tracking Can Benefit From Consolidation ...................................................... 3

Back Office Issues Stemming From Multiplicity .............................................. 3

The Problem in Detail ..................................................................................... 6

Fund Structure Level Issues ........................................................................... 7

Investor Level Issues ...................................................................................... 7

The Administrator’s Dilemma ......................................................................... 8

The Ideal Solution .......................................................................................... 9

The Right Solution Expands the Target Market............................................. 11

2

Introduction

Wealth Management: A New Channel For Alternatives

There’s an old adage stating if the only tool you have is a hammer, every problem will look like a nail. We all know that a hammer is not always the best tool for a job. If we are sensible, we look to the hammer to solve only those problems that involve nails.

Financial service providers are generally sensible people, so if they have only hedge fund allocation systems, they will probably approach only hedge fund clients. This effectively cuts them out of large swathes of the potential market for their services, since they cannot approach wealth management or mutual fund clients without the ability to calculate, track and pay brokers’ fees or to use different systems and procedures for different clients.

The typical investor today wants diversified assets that provide the upside performance of alternative investments along with the market protection and liquidity of a mutual fund. Those investors with greater liquid investable assets make greater use of wealth managers who can help them invest in alternatives and structure their accounts to more closely conform to their individual needs.

Wealth managers use managed accounts to structure highly personalized portfolios for the benefit of their clients. These accounts may include a unique mix of hedge funds, private equity funds and mutual funds. The wealth man-ager collects fees based on the underlying assets by using back-end fees from mutual funds or participation in the performance of alternatives.

This is a new channel for alternatives. Historically, alternatives were always funded directly from investors; that direct relationship enabled the fund man-ager to collect performance and management fees without having to pay any additional fees to wealth managers or brokers. It was an easy model for inves-tors and fund managers alike.

Now, with the proliferation of alternative products and investment channels, investors are less comfortable making decisions and less confident overall about investing on their own. They have turned to wealth managers as knowl-edgeable intermediaries who can structure their portfolios to manage risk and growth.

3

As a result of these new intermediary relationships with alternative fund man-agers, service providers find they need multiple systems to handle different types of funds. Using multiple systems to handle different aspects of servicing across various types of funds has caused changing workflow and processing challenges. To complicate matters further, alternative funds come with com-plexities that do not exist in mutual funds, while wealth managers face addi-tional challenges that go beyond a typical servicing business model.

Investor demands for diversification have led wealth managers to invest their clients’ funds in multiple products, creating new kinds of account complexities and making the calculation and payment of fees difficult without an automated tracking mechanism.

Alternative products are generally not stand-alone funds but complex struc-tures with underlying classes of investors and, in many cases, side pocket assets. Profit and loss must be allocated and fees charged across multiple classes of investors and levels of the fund hierarchy.

By contrast, mutual funds are far simpler, consisting of long-only assets re-quiring simple daily fund accounting and liquidity rights that alternatives do not have.

The convergence of these differing products in an investor portfolio leads to greater complexity, given the need to track different kinds of investments and fees in a consolidated manner.

Back office processing environments were designed to routinely handle one type of investment product. The convergence of funds with different kinds of complexities has led to a proliferation of back-office processing systems, fur-ther complicating an already complex environment. To support these chang-es, providers must enter data into multiple systems, which can lead to errors and reconciliation delays. Providers running systems such as Hedge Tek, NTAS or Multifonds for their hedge funds along with traditional systems for mutual funds such as those provided by PNC or DST often face reconciliation and processing issues stemming from the multiplicity of systems.

Blockstream’s Liquid aims to move some transactions off the primary block-chain to smaller sidechains that manage smart contracts quickly and seam-lessly.

Barclay’s Accelerator has funded several Bitcoin and Blockchain focused startups, including Safello, BlockTrace and Atlas card.

Tracking Can Benefit From Consolidation

Back Office Issues Stemming From Multiplicity

4

The list goes on, but suffice it to say that with the heavy support to fund new ideas based on cryptocurrency and blockchain technologies, this area is poised to create fundamental shifts in the investment industry.

Further complicating investor account management, multiple account types are established according to varying liquidity needs: alternative funds may be redeemed at intervals of only a month or more, while ‘40 Act funds allow for daily withdrawals. For wealth managers investing in a mixed portfolio, just determining a strategy for investment and redemption can be complex, even without the added challenge of differing fee payments and system require-ments.

Spreadsheets can be used to reconcile the results from the disparate back-office systems, but spreadsheets have issues of their own. They are time-consuming, error-prone and inefficient. In addition, they are red flags for auditors, who frequently view them as innately problematic and lacking automated controls.

5

6Streamlined Investor Accounting and Servicing

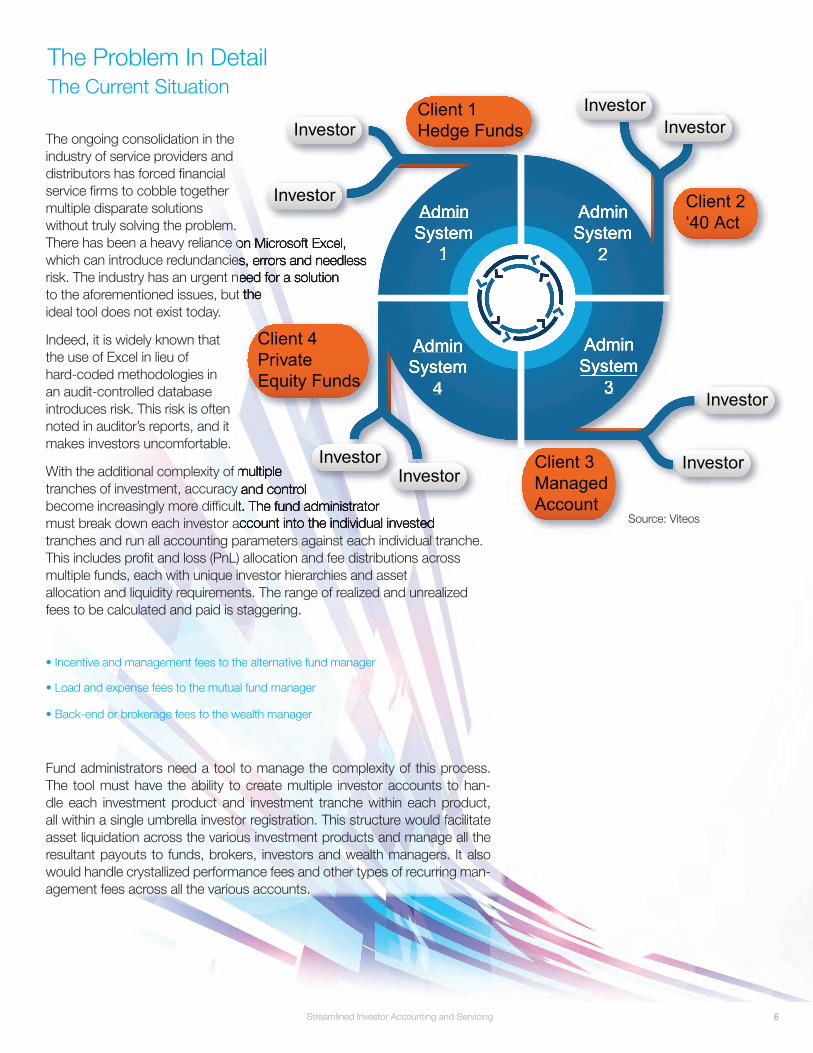

The ongoing consolidation in the industry of service providers and distributors has forced financial service firms to cobble together multiple disparate solutions without truly solving the problem. There has been a heavy reliance on Microsoft Excel, which can introduce redundancies, errors and needless risk. The industry has an urgent need for a solution to the aforementioned issues, but the ideal tool does not exist today.

Indeed, it is widely known that the use of Excel in lieu of hard-coded methodologies in an audit-controlled database introduces risk. This risk is often noted in auditor’s reports, and it makes investors uncomfortable.

With the additional complexity of multiple tranches of investment, accuracy and control become increasingly more difficult. The fund administrator must break down each investor account into the individual invested tranches and run all accounting parameters against each individual tranche. This includes profit and loss (PnL) allocation and fee distributions across multiple funds, each with unique investor hierarchies and asset allocation and liquidity requirements. The range of realized and unrealized fees to be calculated and paid is staggering.

Fund administrators need a tool to manage the complexity of this process. The tool must have the ability to create multiple investor accounts to han-dle each investment product and investment tranche within each product, all within a single umbrella investor registration. This structure would facilitate asset liquidation across the various investment products and manage all the resultant payouts to funds, brokers, investors and wealth managers. It also would handle crystallized performance fees and other types of recurring man-agement fees across all the various accounts.

The Problem In Detail The Current Situation

AdminSystem

1

AdminSystem

2

AdminSystem

3

AdminSystem

4

There has been a heavy reliance on Microsoft Excel, which can introduce redundancies, errors and needless risk. The industry has an urgent need for a solution to the aforementioned issues, but the

With the additional complexity of multiple tranches of investment, accuracy and control become increasingly more difficult. The fund administratormust break down each investor account into the individual invested

There has been a heavy reliance on Microsoft Excel, which can introduce redundancies, errors and needless

AdminSystem

1

AdminSystem

2

AdminSystem

3

AdminSystem

4

Client 1Hedge Funds

Client 2‘40 Act

Client 3ManagedAccount

Client 4PrivateEquity Funds

Investor

Investor

InvestorInvestor

Investor

Investor InvestorInvestor

Source: Viteos

7

Simple alternative fund structures resemble master feeders in which fees and investor capital are held, only at the feeder level. Complex fund struc-tures have multiple levels where allocations for PnL and fees occur. These transactions flow both up and down the various levels. Subscriptions and redemption transactions also cross the structure at multiple levels, with investors in some cases residing at not only the feeder level but also at the master level or within a side pocket or special purpose vehicle class with its own accounting parameters.

Investor account assets must be segregated to enable application of unique fee and other expense allocation calculations to each asset type. Hedge funds, ‘40 Act funds, private equity funds and packaged products from wealth management accounts must all be segregated within the investor account and undergo separate fee calculations and PnL allocations. To en-able payout of capital and fees to the different parties involved, there must also be a mechanism that allows each individual investment to be realized or liquidated independently from other assets held in the same account.

To function correctly, the investor level hierarchy must allow for at least three levels. In its simplest form, such a hierarchy would assign an individual in-vestor to the highest level as both the registered investor and a beneficial owner.

For more complex investors, the highest level is the investing entity. Under-lying this investing entity, there may be multiple beneficial owners or hold-ers. Each beneficial holder may be assigned to multiple accounts to enable tracking specific tranche investments. At the account level, each investor would be able to invest in various product types, so there must be at least one account for each product type. There may also be multiple accounts

for tranches or for varying fee structures.

Investor Level Issues

Fund Structure Level Issues

Administrators who service various types of funds today face a manual deci-sion for every investor transaction or trade. They must analyze each trade to determine the right system of record for the trade, and then verify and ensure they have all the right information to process the transaction quickly and ac-curately.

It is impossible to do this manual analysis efficiently and consistently if you are using multiple systems. As a result, funds have assembled teams of people to process redundant data into two or three different systems to ensure an accurate validation. The process is slow and inefficient. The process workflow functions in fits and starts rather than flowing smoothly through the entire process, as it should ideally.

The challenges are also a matter of training. Staff must be conversant in mul-tiple systems so they understand the intricacies of processing various trades. This requires two to three times the training effort just to bring the team up to speed. People become frustrated and unhappy because of the unnecessary burden of double or triple data entries and the difficulty in completing their assigned tasks.

Employee turnover increases because of the mounting frustration, but it is harder than ever to recruit qualified people because they don’t want to work in an environment with poor systems that result in unnecessary drudgery. In short, while the administrator needs more people to process transactions correctly, the absence of a cohesive system makes it harder to recruit and retain qualified personnel. The systems and the workflow, rather than being the smooth foundation required for efficient operations, become stumbling blocks and impediments.

The ideal solution must allow the entire investor hierarchy, at each of the three levels, to track investor transactions and be capable of rolling up fee calcula-tions and payments for reporting and payouts. Current systems typically stop at one or two levels.

The Administrator’s DilemmaLegacy systems create separate flows on multiple systems

Distributed Ledger

8

Source: Viteos

The Ideal SolutionOne flow in a single database solution

Without the third level in the hierarchy, the solution falls short of real world requirements. Fund administrators must be able to easily and accurately seg-regate tranches for all investors or holders, calculate all the varying fees, and pay the fees to the appropriate party or parties.

Service providers that want to deal in multiple classes of assets require a system designed to handle different fund types within a single workflow. The system must be equally adept at handling both simple ‘40 Act ac-counts and complex hedge fund accounts with their multi-level structures and intricate investment restrictions. To effectively service wealth manage-ment clients, the system must be able to deal with one-of-a-kind “fund of funds” that may include a unique mix of alternative and mutual funds.

The new breed of investors and their wealth managers are a two-edged sword for both fund managers and administrators. On one hand, they rep-resent a large expansion in the pool of potential investors and assets. On the other, they represent a serious, on-going and expensive management issue that requires a solution.

Fund administrators know they can solve the problem by hiring more peo-ple, but it is difficult if not impossible to hire people who know all the dispa-rate systems required. Plus, increasing headcount is expensive.

Robotics or artificial intelligence is a way to solve the problem, but it can be time-consuming and expensive to create and maintain a bespoke system.

An asset allocator could solve for all the issues described, but the only as-set allocators that cross multiple systems are tied together by Excel. Excel is complicated and potentially error-prone, as well as a red flag for auditors.

Fund managers and administrators recognize the need to address three basic problems to support new style investors:

1. They must develop efficient workflow processes or smart processes for control of human resources and business model

2. They must create or purchase a tool that can support fund structures with multiple legal entity levels.

3. They must have a tool to manage complex investor account hierarchies.

Source: Viteos

9

10

11

The Right Solution Expands The Target Market

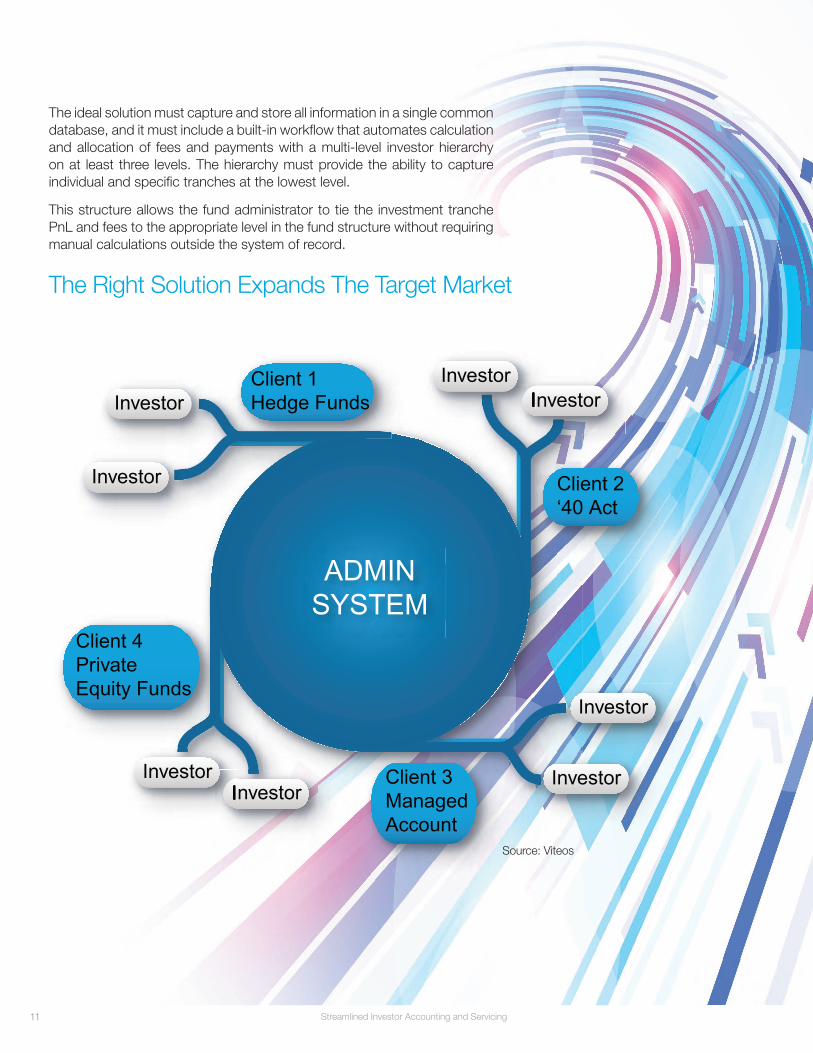

The ideal solution must capture and store all information in a single common database, and it must include a built-in workflow that automates calculation and allocation of fees and payments with a multi-level investor hierarchy on at least three levels. The hierarchy must provide the ability to capture individual and specific tranches at the lowest level.

This structure allows the fund administrator to tie the investment tranche PnL and fees to the appropriate level in the fund structure without requiring manual calculations outside the system of record.

ADMINSYSTEM

Client 1Hedge Funds

Client 2‘40 Act

Client 3ManagedAccount

Client 4PrivateEquity Funds

Investor

Investor

InvestorInvestorInvestor

Investor

Investor InvestorInvestorInvestor

Source: Viteos

12

With a multi-level investor hierarchy and workflow on a unified platform, ad-ministrators would have access to a broader client base. The ideal solution described would solve problems that presently preclude or discourage the taking on of complex investors and portfolios that include hedge funds, mutu-al funds and a wealth management dimension. Rather than being constrained by inadequate systems, service providers would gain access to a larger cross-section of customers and funds.

When systems can track only a single type of investment, the service pro-vider is limited to pursuing clients who offer that product. But with a system that easily supports multiple products across market segments—even for the same client—the potential market immediately expands.

13

TECHNOLOGY SOLUTIONS

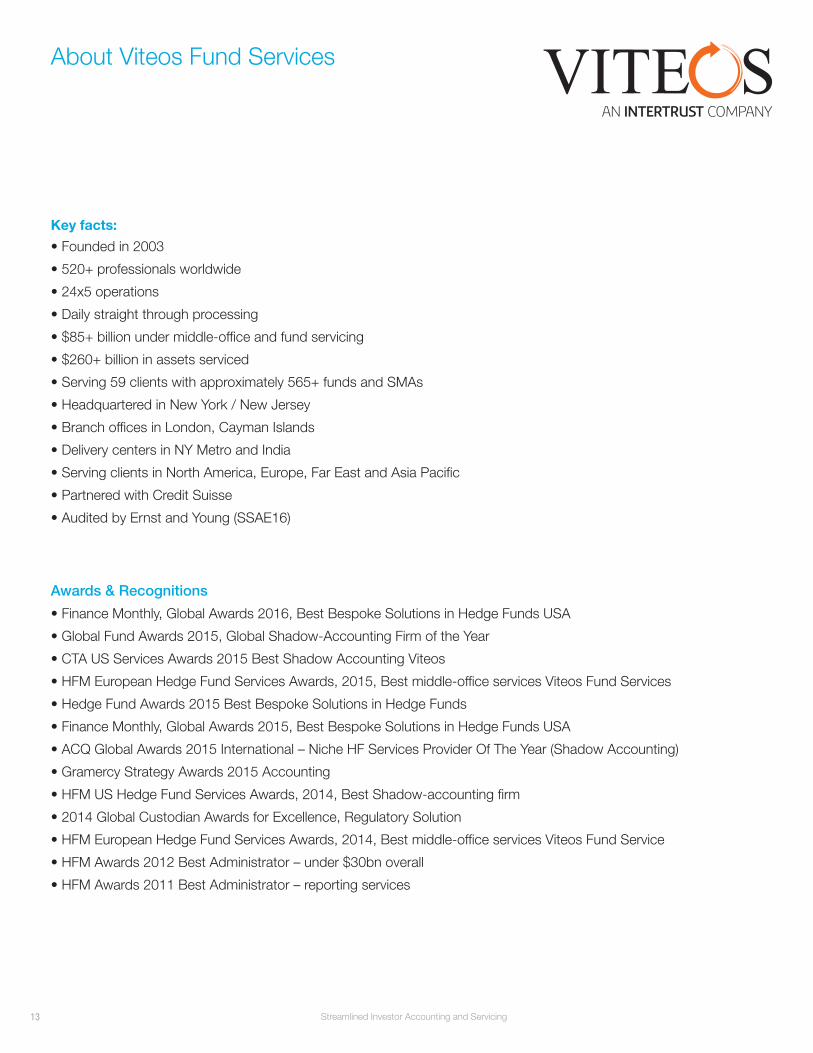

About Viteos Fund Services

Key facts:

Awards & Recognitions

Streamlined Investor Accounting and Servicing 14Integrated Reconciliation 27

TECHNOLOGY SOLUTIONS

www.viteos.com