strategies for selecting a third party administrator - asbo · strategies for selecting a third...

TRANSCRIPT

strategies for selecting a third party administrator

overview If you have reviewed the requirements of the IRS regulations that govern your retirement savings plan, such as a 403(b) or 457(b) plan, and want to use the services of a Third Party Administrator (TPA), the next step is selecting the right company to perform these services.

To find the right TPA, you need to know what services are important to you, and select a TPA that best meets your needs. Not all TPAs are alike and you must ensure the company you select is capable of handling the responsibilities and tasks required under the regulations.

How to Use This Brochure This brochure offers you key strategies, outlined in a three-step process, for reviewing and selecting a suitable TPA:

• Step 1 provides you with a brief overview of the differences between companies in the marketplace.

• Step 2 provides you with a range of questions you can use to learn more about each company.

• Step 3 includes a checklist to help you compare each company.

2 step 1 | understand your options — know the differences

There are differing levels of services available and it is important to understand the key differences between the types of companies you’ll find in the market—a recordkeeper, a common remitter, a quasi-TPA, and a full-service TPA like PlanConnect®. See below for definitions of each type.

Recordkeeper • Keeps records and maintains accounting of values attributable to each participant.

• Some recordkeepers keep track of the sources of money, e.g., pre-tax vs. Roth contributions.

• Typically does not handle compliance services.

Common Remitter • Captures data from the employer’s payroll.

• Compares the amounts with expected contributions.

• Reconciles errors in contributions (exceptions) with the payroll department.

• Identifies employees eligible for “catch-up” contributions and applies contributions in the proper order.

• Distributes contributions to investment providers.

Quasi-TPA • May be referred to as a “TPA” but does not provide all TPA services, as described in the TPA section

on the following page.

• Some offer one or more of the following services:

– Common remitter services

– Consulting

– Educational materials

– Plan Document; Specimen documents only

understand your options — know the differences

Step 1Step 1

step 1 | understand your options — know the differences 3

Full-Service TPA • May be independent or owned by an investment provider.

• Acts as a central point of contact for plan level information.

• Provides common remitter and recordkeeping services.

• Provides overall compliance for transactions at the plan level (such as loans, hardship withdrawals, tracking suspensions and reinstatement, distributions, and monitors required minimum distributions).

• Coordinates various vendor activities.

• Maintains employer plan website.

• Develops and maintains plan document.

• Maintains administrative forms.

• Provides employer manual.

• Offers employee and employer education.

• Assists and advises employers regarding eligibility and participation requirements, e.g., universal availability rule.

• Provides audit support (IRS and/or independent audits).

• Can provide data aggregation and other services to assist in maintaining ERISA exemption.

• A TPA provides additional services for ERISA plans:

– Assists in the calculation of contributions

– Monitors eligibility

– Assists in plan design to eliminate compliance issues

– Maintains plan and Summary Plan Description (SPD)

– Prepares Form 5500 reporting

– Performs compliance testing, including employer match contributions, etc.

“ There are differing levels of services available and it is

important to understand the key differences between

the types of companies you’ll find in the market.”

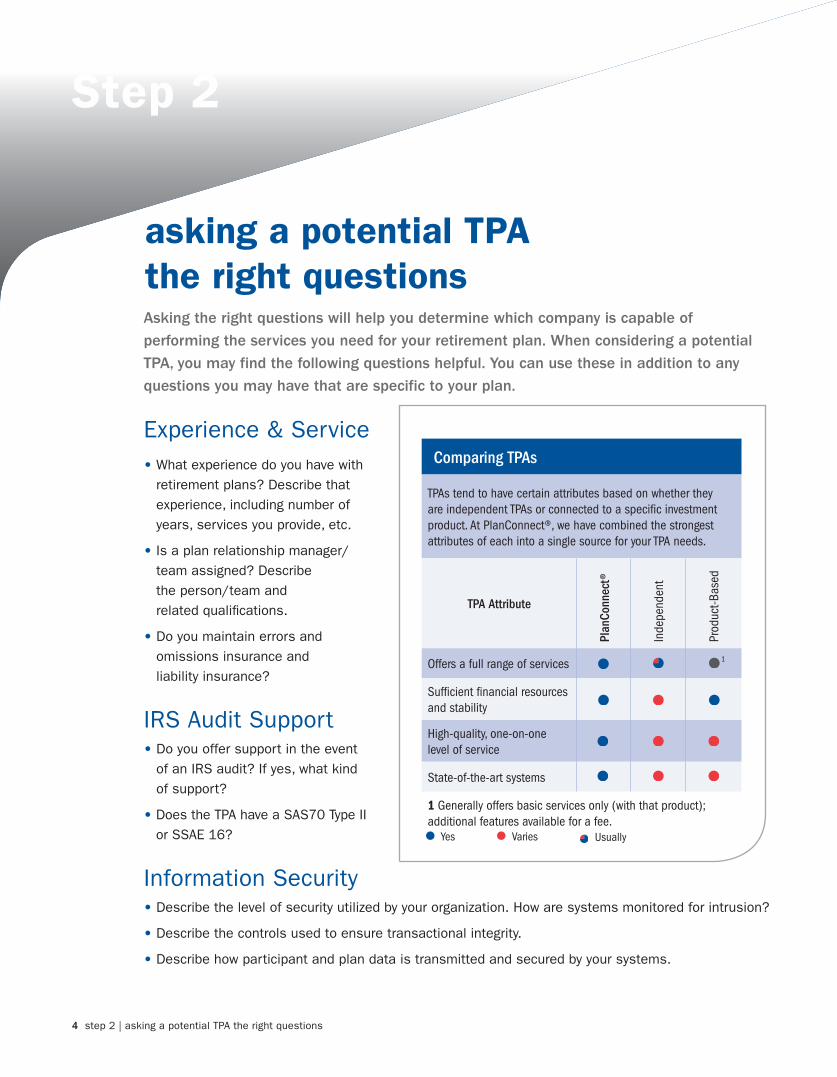

Asking the right questions will help you determine which company is capable of performing the services you need for your retirement plan. When considering a potential TPA, you may find the following questions helpful. You can use these in addition to any questions you may have that are specific to your plan.

Experience & Service • What experience do you have with

retirement plans? Describe that experience, including number of years, services you provide, etc.

• Is a plan relationship manager/team assigned? Describe the person/team and related qualifications.

• Do you maintain errors and omissions insurance and liability insurance?

IRS Audit Support • Do you offer support in the event

of an IRS audit? If yes, what kind of support?

• Does the TPA have a SAS70 Type II or SSAE 16?

Information Security • Describe the level of security utilized by your organization. How are systems monitored for intrusion?

• Describe the controls used to ensure transactional integrity.

• Describe how participant and plan data is transmitted and secured by your systems.

4 step 2 | asking a potential TPA the right questions

asking a potential TPA the right questions

Step 2

Comparing TPAs

TPAs tend to have certain attributes based on whether they are independent TPAs or connected to a specific investment product. At PlanConnect®, we have combined the strongest attributes of each into a single source for your TPA needs.

TPA AttributePl

anCo

nnec

t®

Inde

pend

ent

Prod

uct-B

ased

Offers a full range of services

Sufficient financial resources and stability

High-quality, one-on-one level of service

State-of-the-art systems

1 Generally offers basic services only (with that product); additional features available for a fee.

UsuallyVariesYes

1

step 2 | asking a potential TPA the right questions 5

Recordkeeping/Contributions • Do you offer common remitter services?

• Describe the method/process used to perform recordkeeping and report contributions from multiple investment providers in a single plan. Include a typical timeline and how differences are reconciled. Provide a sample report.

• How will participant deferrals be monitored? Explain how the 15-year catch-up contributions and the age 50 catch-up contributions are handled.

• How are excess contributions monitored? Are corrections for single investment providers handled in the same manner as a plan with multiple investment providers?

• Explain how excess contributions are applied for a participant contributing to multiple plans. Would the process be the same if a participant in the 403(b) or 457(b) plan owns or controls another business?

• How many contribution sources can your system handle, e.g., rollovers, pre-tax deferrals, Roth deferrals, employer contributions, etc.?

• Explain the method used by your organization to update plan records where multiple investment providers handle financial transactions. How frequently are participant balances updated on the consolidated participants’ website?

• Describe the procedures used to ensure the recordkeeping system remains in compliance with changes in the law or regulations.

• Can you provide services tailored to a plan looking to maintain an ERISA exemption?

Transactions • Describe your compliance monitoring process. Explain how

this process is designed to prevent a compliance error as opposed to correcting it after it has occurred.

• Explain the process for receiving and qualifying hardship distributions.

• How are available loan amounts determined? How are loans issued among multiple investment providers? Are loans with multiple investment providers and/or multiple plans monitored for compliance? Explain the process when a loan is in default.

• Describe the process for handling required minimum distributions, from identification to distribution.

• Describe the process for handling other transactions, including transfers, Qualified Domestic Relations Orders (QDROs), disability distributions, and other distributions.

• Explain the compliance monitoring in place for “control” of other companies by employees.

Plan Documentation & Materials • Is an employer implementation guide or administration manual provided to support set-up and

ongoing administration?

• Do you offer customized plan documents or specimen documents only?

• If you offer customized plan documents, do you automatically offer ongoing amendments as required?

• Do you provide and maintain administrative forms?

• Do you provide and assist with Information Sharing Agreements?

6 step 2 | asking a potential TPA the right questions

Education• What type of educational services do you provide?

• What educational material do you make available via the web?

• Do you provide examples of educational material?

• How do you keep an employer informed of regulation changes?

• How do you promote participation in the plan?

Online Capabilities • Is a website available for participants to access account information? Does it provide the amount available for

transactions such as loans or hardship withdrawals?

• Describe the site and its functions. Is a sample website available to preview?

• Does the website include information for each provider?

• Is a website available for the employer? If yes, what information is available? Is a sample website available to preview? Does the website include information for each provider?

• What reporting is provided via your website? Provide examples.

• What type of support/training do you provide to employees trying to access the site?

step 2 | asking a potential TPA the right questions 7

Step 3

Compare PlanConnect®PlanConnect® Other TPA

Experience & ServiceExperience in the 403(b) and 457(b) market Yes No

Plan relationship manager assigned Yes No

Maintains errors and omissions insurance and liability insurance Yes No

IRS Audit SupportAssistance in event of IRS audit Yes No

Information SecurityEnsures privacy of plan participant information Yes No

Secure electronic data transmission Yes No

Secure website for data uploads Yes No

Recordkeeping/ContributionsCommon remitting processing/services Yes NoMonitors contribution limits, including catch-up contributions; monitors ordering rules, if applicable Yes No

SAS70 Type II or SSAE 16 performed by top-tier accounting firm Yes No

Supports multiple source accounts (e.g; rollover, Roth, employer contributions, etc.) Yes No

TransactionsProvides and updates required loan policy Yes No

Provides and updates required hardship withdrawal policy Yes No

Assures that plan and underlying contracts are consistent Yes NoCompliance review for loans, hardships, exchanges, transfers, Qualified Domestic Relations Orders, disability distributions, required minimum distributions, etc. Yes No

Online facility for transaction requests and approvals where applicable Yes No

Plan Documentation & MaterialsOngoing employer’s plan implementation guide/manual Yes No

Provides initial plan documents Yes No

Maintains and amends all legal documents as required Yes No

Customized plan documents, if necessary Yes No

Information sharing agreements Yes No

EducationOnline support for plan sponsors and participants Yes No

Plan sponsor-directed educational material Yes No

Tools, calculators, and webinars for plan participants on various retirement topics Yes No

Web, e-mail, and print participant education material Yes No

Live and/or virtual training seminars Yes No

WebsitesAvailability of website for participants Yes No

Availability of website for plan sponsors Yes No

Required plan reporting available online Yes No

Provider information is available on these websites Yes No

Now that you understand what’s required of a full-service TPA, compare PlanConnect® and its services to those of our competitors.

a footer

Contact PlanConnect®PlanConnect®, 100 Madison Street, Syracuse, NY 13202

Find us on the Web at: www.planconnect.com

Email us at: [email protected]

Call us at:800-923-6669

PlanConnect, LLC is a wholly owned subsidiary of AXA Distribution Holding Corporation, an indirect subsidiary of AXA Financial, Inc. PlanConnect®, Connect2Remit®, Connect2Comply®, and Connect2Maintain® are registered service marks of AXA Distribution Holding Corporation. Connect2Achievesm is a service mark of PlanConnect, LLC. PlanConnect® may not be available in all states. AXA Financial, Inc. and its family of companies do not provide tax advice. Please consult with your tax advisor regarding your particular circumstances. Each company is affiliated. AXA Distribution Holding Corporation and AXA Financial, Inc. are located at 1290 Avenue of the Americas, New York, NY 10104, (212) 554-1234

PlanConnect, LLC is located at 100 Madison Street, Syracuse, NY 13202, 800-923-6669.

G25885